2007 Activities Reviewing and Compiling control points for Site AART Presented to : Process Owners...

23

O FFIC E O F TH E C HIEF FIN ANC IA L O FFIC ER C FO O FFIC E O F TH E C HIEF FIN ANC IA L O FFIC ER C FO 2007 Activities Reviewing and Compiling control points for Site AART Presented to : Process Owners By Grace Huang, Project Manager O FFIC E O F TH E C HIEF FIN ANC IA L O FFIC ER C FO O FFIC E O F TH E C HIEF FIN ANC IA L O FFIC ER C FO OMB Circular A-123 (Appendix A) OMB Circular A-123 (Appendix A) Implementation Implementation

-

Upload

tristan-grymes -

Category

Documents

-

view

214 -

download

0

Transcript of 2007 Activities Reviewing and Compiling control points for Site AART Presented to : Process Owners...

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

2007 Activities

Reviewing and Compiling control points

for Site AART

Presented to : Process Owners

By Grace Huang, Project Manager

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

OMB Circular A-123 (Appendix A)OMB Circular A-123 (Appendix A)ImplementationImplementation

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

What is OMB Circular A-123?What is OMB Circular A-123?

• Provides Federal managers guidance on improving the accountability and effectiveness of Federal programs and operations by establishing, assessing, correcting, and reporting on management controls*

• Appendix A was added late 2005 with a focus of the management process for assessing internal control over financial reporting

* From “Purpose and Authority” of Circular No. A-123

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

Assurance reporting at different levelsAssurance reporting at different levels

DOE Headquarters

Assurance Statement

Chicago Field Office

Roll up Site A-123 Assessment and Reporting Tool (AARTs)

Assurance Statement

LBNL Site AART

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

Site AART Site AART • Material accounts

Balance sheet• Other Liabilities• Accounts Payables• Other Non-

intragovernmental assets• General Property, Plant,

and Equipment

Stmt of Net Costs• World Class Scientific

Research Capacity• Reimbursable Programs

Stmt of Financing • Depreciation and

Amortization

• Major processes

Entity Controls Process Controls

• Budget to Close• Procure to Pay• Enterprise Resource

Management• Project to Asset• Quote to Cash

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

FY07 TimelinesFY07 TimelinesMilestones Due Dates

Internal Control training 10/1/2006 through 12/15/2006

Revised Site AART toolkit Mid December

Review of Site AART data (including Financial Statement Assertion linkage)

12/15/2006 through 2/15/2007

OMBA-123 Webpage development 11/1/2006 through 12/31/2006

1st Quarterly reporting 1/5/2007 (tentative)

Realignment of FY 2006 Data for new Site AART features

2/15/07 through 5/15/2007

Testing 2/15/2007 through 7/31/2007

2nd Quarterly reporting 4/6/2007 (tentative)

Remediation of controls 2/15/2007 through 6/15/2007

3rd Quarterly reporting 7/6/2007 (tentative)

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

FY07 Timelines (Continued)FY07 Timelines (Continued)Milestones Due Dates

Preliminary assurance reporting 8/10/2007 (tentative)

Final assurance reporting 8/27/2007 (tentative)

Periodic assessment team meeting Ongoing

Quarterly Steering Committee meeting Ongoing

Periodic status report to CFO Ongoing

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

New/Changed process?New/Changed process?

• Note any significant process change that may have been prompted by or resulted in any of the following

New regulations requiring additional controls to ensure compliance

Organizational changes in which new leadership has implemented new procedures or directives

Existing automated processes changed to manual ones

Process owners are required to discuss any of the above with the implementation team

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

WhyWhy

• Hours required for testing activities in FY2006

• Agreed controls required clarification or revisions

• Required resources to track the revised controls

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

How toHow to

• Review the controls under the sub-processes rated “Moderate” and “Low” risks

• Based on the way the control is worded, conclude the following:

What does the control accomplish (its objective)?

Is the control objective preventive, detective, or both in nature (Control Set Mode)?

Mark the key control(s) with two asterisks at the end of the sentence and list the key control(s) first

Re-rate the Control Set Design Effectiveness based on the new definition of the rating

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

Key Controls/Controls SetKey Controls/Controls Set

• Key Controls are: Controls that have the greatest and most critical impact in mitigating risk occurrence

• A control Set is A logical grouping of controls designed to mitigate a common risk statement

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

Control Set Design EffectivenessControl Set Design EffectivenessRating FY 2007 (New) FY 2006 (Old)

3 Significant Design Deficiency

High probability of the risk occurring

Material Weakness

More than a remote likelihood of material misstatement of Financial Statement

4 Design Deficiency

More than a remote possibility of the risk occurring

Reportable Condition

More than a remote likelihood and more than inconsequential misstatement of Financial Statement

5 Minor Design Deficiency

Only a remote possibility of the risk occurring

Control Deficiency

The control will prevent or detect a misstatement of Financial Statements

6 Designed Effectively

Less than a remote possibility of the risk occurring

Designed Effectively

The control will prevent or detect a misstatement of Financial Statements

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

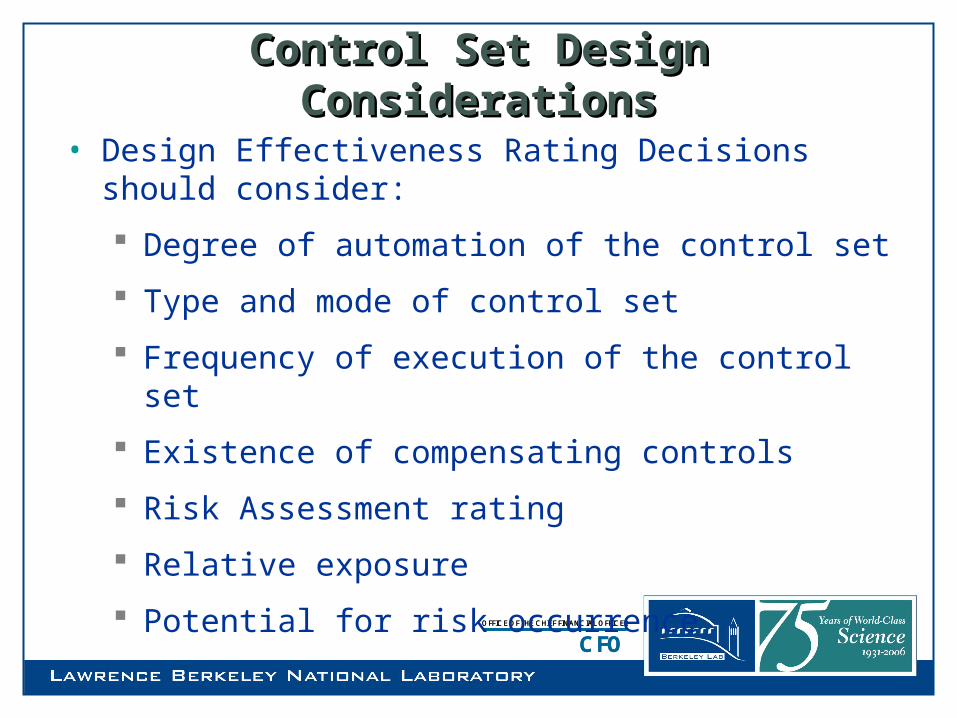

Control Set Design ConsiderationsControl Set Design Considerations

• Design Effectiveness Rating Decisions should consider:

Degree of automation of the control set

Type and mode of control set

Frequency of execution of the control set

Existence of compensating controls

Risk Assessment rating

Relative exposure

Potential for risk occurrence

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

How toHow to

• Design Effectiveness Rationale (An example) for a rating of 6 (control set designed effectively):

Control set contains both manual and automated controls directly linked to key risks. The control set provides for preventive and detective controls to mitigate the risk and provides for identification of issues should the risk occur. The number of controls also appears adequate based on the level of risk.

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

How toHow to

• Project team will determine the following for review:

The direct impact on the DOE entity-wide financial statements if the control is not able to mitigate the risk(s) involved

• DOE entity-wide statements

– Balance Sheet

– Statement of Net Costs

– Statement of Financing

In the event that the impact on the entity- wide financial statement is indirect, reference “Indirect impact”

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

How toHow to

• The five financial statement assertions (project team will complete this for review):

Presentation and disclosure

Is it recorded in the right place?

Existence or occurrence

Did it happen and when?

Rights and obligations

Do we own or owe what we think we do?

Completeness and accuracy

Is anything missing?

Valuation or allocation

Are the numbers right?

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

How toHow to• Revising controls

When?

• It is not possible to form a clear, concise control objective which addresses how the risk involved may be averted or detected

• Lack of specificity in the Risk/Control set

• Underlying business processes have changed prompting the controls to be changed or eliminated

• Controls as worded are inaccurate depiction of the actual business processes and procedures

• The Control Set Type (Auto vs. Manual) and Frequency have changed

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

How toHow to

• A risk/control set – before and after

Example (before):

Risk: Improper orders can occur

Control: Procurement supervisors review the purchase requisitions for any unallowable items and assign transactions to buyers. Buyers review transactions then source requisitions into purchase orders and place orders with vendors.

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

How toHow to• A risk/control set – before and after

Example (After):

Risk: Prohibited items may be ordered via LBNL Procurement systems

Controls: Procurement supervisors review the purchase requisitions for any unallowable items.

The DPU Supervisor signs off on monthly statement and reviews the backup documentation.

Buyers review and approve those purchase orders within their delegated signature authority.

SAS approvers review for any prohibited items and approve the requisitions.

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

How toHow to

• How is after different from before?

A more clear control objective – prevents unallowable costs from incurring by preventing and/or detecting the requisition of prohibited items

Specific reference to multiple processes in which the control objective is achieved

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

Our goalsOur goals

• To address the feedback from DOE HQ OMB A-123 Project Management Team (PMT) :

Most risk statements are detailed and well formed, but some lack specificity

While the control activities are defined, it is difficult to discern the control objectives.

• To streamline effort for FY07 implementation activities by striving for more clear and concise control objectives

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

Optional/RecommendedOptional/Recommended

• Efficiency Opportunities Identifier

While the control set design may be effective, A-123 evaluations should also assess efficiency where possible. If during the course of the evaluation opportunities to improve the efficiency of controls are identified, record a “Yes” in the Efficiency Opportunities Column (Col. V). The nature of the potential efficiency should be recorded in the detailed A-123 Documentation.

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

Design Efficiency Opportunities Design Efficiency Opportunities

• Automation of manual controls

• Elimination of duplicative controls

• Consolidation of multiple controls into a more effective control

• Alteration of control frequency

• Transition from detective to preventive controls

• Alignment of numbers and complexity of controls with level of risk

OFFICE OF THE CHIEF FINANCIAL OFFICER

CFOOFFICE OF THE CHIEF FINANCIAL OFFICER

CFO

Questions?