2005 Interim Results - Santos - Home · 2005 Interim Results 25 August 2005 2 Disclaimer &...

27

1 1 Delivering Growth Delivering Growth 2005 Interim Results 2005 Interim Results 25 August 2005 25 August 2005 2 Disclaimer & Important Notice Disclaimer & Important Notice This presentation contains forward looking statements that are s This presentation contains forward looking statements that are subject to ubject to risk factors associated with the oil and gas industry. It is bel risk factors associated with the oil and gas industry. It is bel ieved that the ieved that the expectations reflected in these statements are reasonable, but t expectations reflected in these statements are reasonable, but t hey may hey may be affected by a range of variables which could cause actual res be affected by a range of variables which could cause actual results or ults or trends to differ materially, including but not limited to: price trends to differ materially, including but not limited to: price fluctuations, fluctuations, actual demand, currency fluctuations, geotechnical factors, dril actual demand, currency fluctuations, geotechnical factors, dril ling and ling and production results, gas commercialisation, development progress, production results, gas commercialisation, development progress, operating results, engineering estimates, reserve estimates, los operating results, engineering estimates, reserve estimates, loss of market, s of market, industry competition, environmental risks, physical risks, legis industry competition, environmental risks, physical risks, legislative, fiscal lative, fiscal and regulatory developments, economic and financial markets cond and regulatory developments, economic and financial markets conditions in itions in various countries, approvals and cost estimates. various countries, approvals and cost estimates. All references to dollars, cents or $ in this document are to Au All references to dollars, cents or $ in this document are to Au stralian stralian currency, unless otherwise stated. currency, unless otherwise stated.

Transcript of 2005 Interim Results - Santos - Home · 2005 Interim Results 25 August 2005 2 Disclaimer &...

1

1

Delivering GrowthDelivering Growth2005 Interim Results2005 Interim Results

25 August 200525 August 2005

2

Disclaimer & Important NoticeDisclaimer & Important Notice

This presentation contains forward looking statements that are sThis presentation contains forward looking statements that are subject to ubject to risk factors associated with the oil and gas industry. It is belrisk factors associated with the oil and gas industry. It is believed that the ieved that the expectations reflected in these statements are reasonable, but texpectations reflected in these statements are reasonable, but they may hey may be affected by a range of variables which could cause actual resbe affected by a range of variables which could cause actual results or ults or trends to differ materially, including but not limited to: pricetrends to differ materially, including but not limited to: price fluctuations, fluctuations, actual demand, currency fluctuations, geotechnical factors, drilactual demand, currency fluctuations, geotechnical factors, drilling and ling and production results, gas commercialisation, development progress,production results, gas commercialisation, development progress,operating results, engineering estimates, reserve estimates, losoperating results, engineering estimates, reserve estimates, loss of market, s of market, industry competition, environmental risks, physical risks, legisindustry competition, environmental risks, physical risks, legislative, fiscal lative, fiscal and regulatory developments, economic and financial markets condand regulatory developments, economic and financial markets conditions in itions in various countries, approvals and cost estimates.various countries, approvals and cost estimates.

All references to dollars, cents or $ in this document are to AuAll references to dollars, cents or $ in this document are to Australian stralian currency, unless otherwise stated.currency, unless otherwise stated.

2

3

AgendaAgenda

OverviewOverview

Financial performance Financial performance

Delivering Growth Delivering Growth

Enhancing existing core areasEnhancing existing core areas

Maturing emerging core areasMaturing emerging core areas

Identifying new core areasIdentifying new core areas

Q&AQ&A

4

Record First Half ResultRecord First Half Result

Production (mmboe) 26.3 21.2 24

Sales revenue ($m) 1019.1 590.5 73

Net profit after tax ($m) 289.5 85.3 240

Operating cash flow ($m) 565.3 192.6 194

Gearing (%) 33.6 37.9 -4.3

Dividend (cents) 18.0 15.0 20

TSR (% annualised) 73.0 12.6

Half Year Half Year Half YearHalf Year ChangeChange20052005 20042004 %%

AA--IFRSIFRS

John ElliceJohn Ellice--FlintFlintCEO & Managing DirectorCEO & Managing Director

3

5

Safety Continues to ImproveSafety Continues to Improve…45% reduction over 3 years

Total Recordable Case Frequency Rate(recordable injuries per million work hours)

0

2

4

6

8

10

Jan-03 Jan-04 Jan-05 Jul-05

Full Year 2002

Full Year 2003Full Year 2004

YTD 2005 = 4.9

6

Focused Growth StrategyFocused Growth Strategy

2001 2005 2007 2009 2011 20132003

Identifying Identifying New Core AreasNew Core AreasNorth Africa, Central & SE Asia, USANorth Africa, Central & SE Asia, USA

Maturing Maturing Emerging Core AreasEmerging Core AreasIndonesia, Timor/Bonaparte, PNGIndonesia, Timor/Bonaparte, PNG

Enhancing Enhancing Existing Core AreasExisting Core AreasEastern Australia conventional gas and oil, CSGEastern Australia conventional gas and oil, CSGWestern Australia gas and oil Western Australia gas and oil

4

7

Growth Strategy is DeliveringGrowth Strategy is Delivering

• Mutineer-Exeter start-up• Cooper oil production +20%• Bayu-Undan condensate• Average gas price +10%

Earnings Momentum

• Maleo sanctioned• Oyong in development• Casino development drilling above expectations• Bayu-Undan pipeline completed• John Brookes good appraisal results• Jeruk 3D seismic acquired

Near Term Growth

• Exploration successes(Hiu Aman, Hurricane, Henry, Cooper Oil)

• 1.5 bn boe contingent resources• Tipperary acquisition

Longer Term Optionality

8a

Measured progress as at end Dec 2004

Maleo

Mutineer-Exeter

20

40

60

80

100

Prog

ress

(Po

st s

anct

ion)

%

Strong Offshore Development ProgressStrong Offshore Development Progress

Delivery

Entry

Jeruk

Sole

Minerva

Bayu-Undan Liquids

John Brookes

Casino

Bayu-Undan LNG

KipperOyong

5

8b

Measured progress as at end July 2005

20

40

60

80

100

Prog

ress

(Po

st s

anct

ion)

%

Strong Offshore Development ProgressStrong Offshore Development Progress

Delivery

Entry

Jeruk

Minerva

Bayu-Undan Liquids

John Brookes

Casino

Maleo

Sole

Oyong

Bayu-Undan LNG

Kipper

Mutineer-Exeter

6

9

Delivering GrowthDelivering Growth Peter WasowPeter WasowChief Financial OfficerChief Financial Officer

OverviewOverview

Financial performanceFinancial performance

Delivering Growth Delivering Growth

Enhancing existing core areasEnhancing existing core areas

Maturing emerging core areasMaturing emerging core areas

Identifying new core areasIdentifying new core areas

Q&AQ&A

10

0

50

100

150

200

250

300

1st Half 2005

Underlying Profit Up 48%...Underlying Profit Up 48%...

1st Half 2004

$m

Adjusted 1st Half 2004

Recurring Profit

85

79 164

105 (27)242

48 290

Non-recurring Items*

Operating Items

Exploration Expensed

Non-recurring Items*

…headline profit up 240%

* Non-recurring items detailed in reference slides

7

11

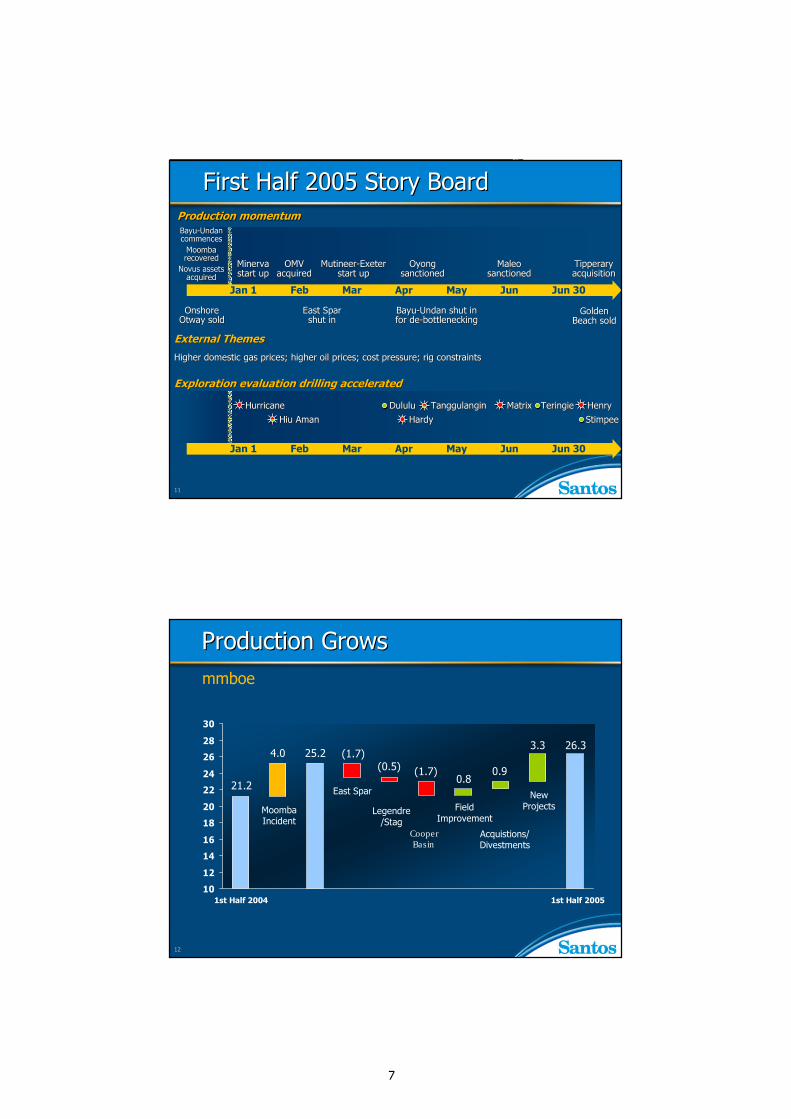

First Half 2005 Story BoardFirst Half 2005 Story Board

External ThemesExternal Themes

Higher domestic gas prices; higher oil prices; cost pressure; riHigher domestic gas prices; higher oil prices; cost pressure; rig constraintsg constraints

BayuBayu--UndanUndancommencescommences

MoombaMoombarecoveredrecovered

Novus assets Novus assets acquiredacquired

Onshore Onshore Otway soldOtway sold

MinervaMinervastart upstart up

OMVOMVacquiredacquired

MutineerMutineer--ExeterExeterstart upstart up

East SparEast Sparshut inshut in

OyongOyongsanctionedsanctioned

MaleoMaleosanctionedsanctioned

BayuBayu--Undan shut inUndan shut infor defor de--bottleneckingbottlenecking

TipperaryTipperaryacquisitionacquisition

Production momentumProduction momentum

Golden Golden Beach soldBeach sold

Feb Mar Apr May Jun Jun 30Jan 1

StimpeeStimpeeHurricaneHurricane

Hiu AmanHiu AmanDululuDululu

HardyHardyTanggulanginTanggulangin MatrixMatrix TeringieTeringie HenryHenry

Exploration evaluation drilling acceleratedExploration evaluation drilling accelerated

Jan 1 Feb Mar Apr May Jun Jun 30

12

10

12

14

16

18

20

22

24

26

28

30

Production GrowsProduction Growsmmboe

1st Half 2005

26.33.3

21.2

4.0

0.8(0.5)

25.2

1st Half 2004

(1.7)

East Spar

Moomba Incident

Legendre /Stag

Field Improvement

0.9

Acquistions/ Divestments

New Projects

(1.7)

CooperBasin

8

13

400

500

600

700

800

900

1000

1100

Sales Grow FasterSales Grow Faster

1st Half 2005

$m

590

1,019

Gas Volumes

Moomba Incident

Gas Prices

103 26Liquids Prices693

1st Half 2004

USD Weakness

5938

(39)194

Liquids Volumes

Controllable Items

48

Mix

Market

14

70

80

90

100

110

120

130

140

150

160

170

1st Half 2005Production Cost

$6.29/boe

Production Costs Inch HigherProduction Costs Inch Higher

1st Half 2004Production Cost

$5.98/boe

127

165

Moomba Incident

(16)

Acquisitions

$m

8119

(14)

(16)

New Fields

Increase in Volumes

Increased Costs

Production Cost$5.67/boe

9

15

Key Initiatives: A$m

Supply & contracting 17

Drilling 10

Organisational redesign 8

Engineering initiatives 5

Shared business services 5

Other savings 11

56 0

5

10

15

20

25

30

35

40

45

50

55

60

Jan Feb Mar Apr May Jun

Opex actual savings Capex actual savings

Savings Projects Reduce Cost PressureSavings Projects Reduce Cost PressureJune YTD savings $56m, on track to achieve full year target of $120m

A$m

16

14

16

18

20

22

24

26

28

30

(0.63)

$/boe netback

Margins HigherMargins Higher

1st Half 2004 1st Half 2005

17.78

Moomba Incident

1.58 19.36

5.61

1.551.25

27.50

0.36

Gas Volumes

Liquids Prices

Liquids Volumes

Gas Prices

Costs

Controllable Items

10

17

0

100

200

300

400

500

600

700

800

900

$m

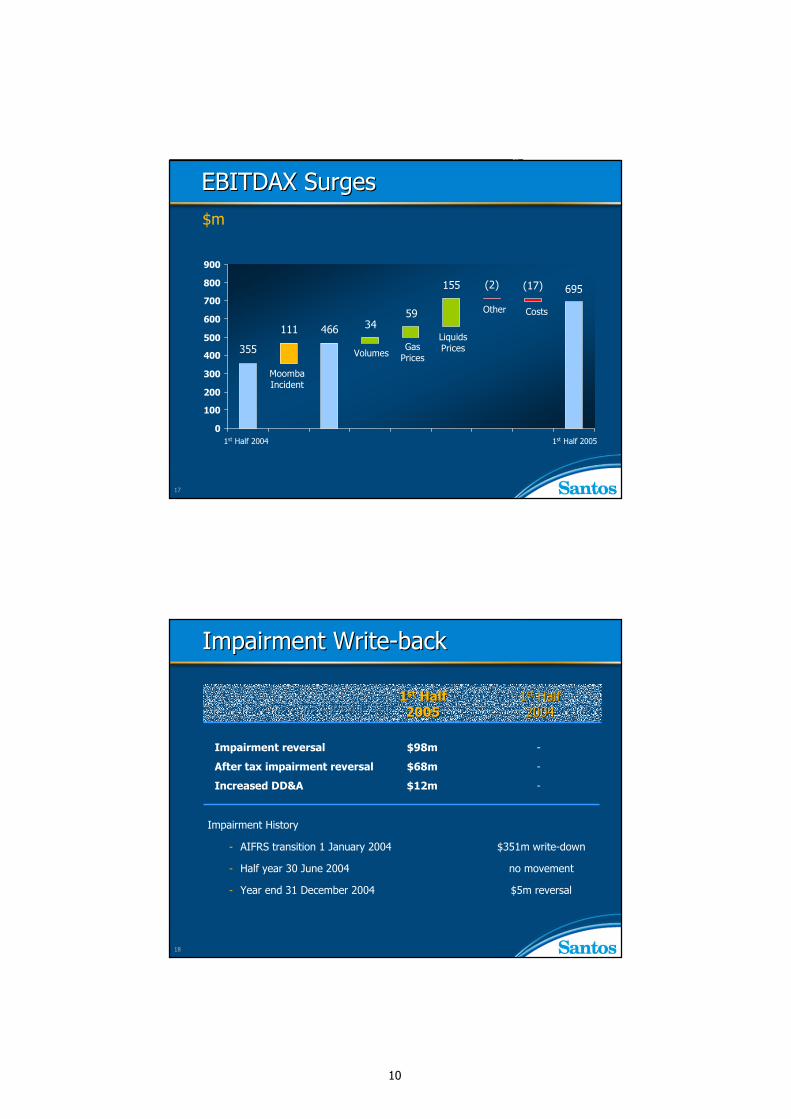

EBITDAX SurgesEBITDAX Surges

1st Half 2004 1st Half 2005

355

695(2)155

34

Volumes

111 466

(17)

Moomba Incident

Gas Prices

Other Costs59

Liquids Prices

18

Impairment WriteImpairment Write--backback

11stst HalfHalf 11stst HalfHalf20052005 20042004

Impairment reversal $98m -

After tax impairment reversal $68m -

Increased DD&A $12m -

Impairment History

- AIFRS transition 1 January 2004 $351m write-down

- Half year 30 June 2004 no movement

- Year end 31 December 2004 $5m reversal

11

19

0

25

50

75

100

125

150

175

200

225

250

275

300

Depreciation, Depletion & AmortisationDepreciation, Depletion & Amortisation

$m

1st Half 2005$10.38/boe

Increased Volumes

172

273

(19)

(23)

Moomba Incident

(13)

1st Half 2004$8.11/boe

New Fields

16

Acquisitions / Disposals

191

(18)

(13)(19)

(12)

East Spar shut in

Impairment Reversal

YE 04 Reserves & FDC’s

$8.03/boe $9.24/boe

Rate Increase One-offs

OtherAsset

Additions

20

Exploration & Evaluation ExpenseExploration & Evaluation Expense

$m$m 11stst HalfHalf 11stst HalfHalf20052005 20042004

37.2 71.4 71.3 109.7 Total

7.0*41.2 37.6 75.8 Drilling

30.2 30.2 33.7 33.9 Seismic, G&G, studies

ExpensedIncurredExpensedIncurred

* Includes $6m credit for previous period drilling claim settlement

12

21

0

50

100

150

200

250

300

350

NPAT: Structural ImprovementNPAT: Structural Improvement$m

149

85

(25)

1st Half 20051st Half 2004

10

43

64

60(27)

(27)290

Moomba Incident

Volumes Gas Prices

Costs (inc DD&A) Impairment

Exploration & Evaluation

Expense

Other

107

Liquids Prices

22

100

200

300

400

500

600

Cash Flow Growth StrongCash Flow Growth StrongHalf yearly operating cash flow

Tax change

Moomba incident

94 95 96 97 98 99 00 01 02 03 04 05

12% CAGR

$m

13

23

Delivering GrowthDelivering Growth John ElliceJohn Ellice--FlintFlintCEO & Managing DirectorCEO & Managing Director

OverviewOverview

Financial performance Financial performance

Delivering GrowthDelivering Growth

–– Enhancing existing core areasEnhancing existing core areas

–– Maturing emerging core areasMaturing emerging core areas

–– Identifying new core areasIdentifying new core areas

Q&AQ&A

24

Focused Growth StrategyFocused Growth Strategy

2001 2005 2007 2009 2011 20132003

Enhancing Enhancing Existing Core AreasExisting Core AreasEastern Australia conventional gas and oil, CSGEastern Australia conventional gas and oil, CSGWestern Australia gas and oil Western Australia gas and oil

ProductionProduction 89%89%2P Reserves2P Reserves 78%78%ContingentContingentResourcesResources 26%26%

15

27

500km

• Interests in all major supply basins

• Extensive infrastructure

• Gas marketing expertise

• Swap opportunities

• Innovative contracting options

• Storage infrastructure

Eastern Gas CommercialisationEastern Gas Commercialisation

NSWNSW

QLDQLD

SASA

NTNT

VicVic

MoombaMoombaHubHub

TasTas

WallumWallum--billabillaHubHub

PNGPNG

PP--B B HubHub

Otway Otway HubHub

28

Southern Gas DevelopmentsSouthern Gas Developments

Casino (50%, operator)

• 35 PJ/yr, 283 PJ 2P

• Construction 63% complete

• Henry 1 discovery to supplement Casino

Patricia-Baleen Hub (100%)

• Acquired OMV & Trinity interests

• Reviewing potential for third party processing

16

29

Western Australian Oil & GasWestern Australian Oil & Gas

Mutineer-Exeter (33.4%, operator)• Commenced production March 2005

• 3 months early, 10% under budget

• Averaged 72,000 bopd in Q2

• Current rate >80,000 bopd

• Rapid payback

John Brookes (45%)• Successful appraisal drilling

• Development drilling completed

• CO2 removal facility accelerated

• Startup expected September 2005

• More gas sold (Wambo)

30

Second Phase Second Phase –– Emerging Core AreasEmerging Core Areas

2001 2005 2007 2009 2011 20132003

Maturing Maturing Emerging Core AreasEmerging Core AreasIndonesia, Timor/ Bonaparte, PNGIndonesia, Timor/ Bonaparte, PNG

ProductionProduction 7%7%2P Reserves2P Reserves 21%21%ContingentContingentResourcesResources 74%74%

17

31 0 1000

DarwinDarwin

East JavaEast Java

BrowseBrowse

Timor SeaTimor Sea

KuteiKutei

West NatunaWest Natuna

Emerging Core AreasEmerging Core Areas

• LNG infrastructure• Drilling material prospects• Large contingent gas resources

Timor / Bonaparte Gas & Oil

• Material portfolio• Multiple exploration targets• Acreage position

Indonesia Gas & Oil

Papua New GuineaPapua New Guinea

• 391 mmboe contingent resource, including 25% of Hides

Papua New Guinea Gas & Oil

BonaparteBonaparte

32

Bayu-Undan Liquids (10.6%)

• Statutory inspection, pipeline tie in and debottlenecking completed

• 100,000+ bpd liquids post shutdown

Bayu-Undan LNG (10.6%)

• Ramp up to 3 MT/yr from early 2006

• Strategic infrastructure

• LNG contracts formalised

• Exploration drilling at Caldita and Firebird

Northern Australia Gas DevelopmentsNorthern Australia Gas Developments

18

33

Indonesia Core Area EstablishedIndonesia Core Area Established

Acreage Acreage Acquisition Acquisition & Evaluation& EvaluationEast JavaEast JavaKuteiKuteiNorth BaliNorth Bali

ExplorationExplorationNyariNyariHerbrasHerbrasBanjar PanjiBanjar Panji

AppraisalAppraisalJerukJeruk

Hiu AmanHiu Aman

DevelopmentDevelopmentOyongOyongMaleoMaleo

ProductionProductionBrantasBrantasKakapKakap

34

Indonesian Gas DevelopmentsIndonesian Gas Developments

Oyong (45%, operator)

• First phase: oil production to start end 2005 to early 2006

• Development drilling in progress

• Second phase: gas likely 2007

Maleo (75%, operator)

• Gas sales agreement signed

• Start-up second half 2006

• Gas reserves sold for electricity

• Production up to 115 TJ/d

19

35

East Java UpdateEast Java Update

Regional Exploration

• 3D seismic survey acquired

• Data being processed

• Two to three wells planned to be drilled during second half

Jeruk (45%, operator)

• Jeruk 2 ST5 in progress• Jeruk 2 ST4 data being

assimilated into models Oil Field

Gas field

Gas Pipeline

3D Seismic

Madura Island

East Java

JerukJerukOyongOyong MaleoMaleo

Java Sea

Grati

NyariNyari

HerbrasHerbras

36

0620052004

New appraisal drilling

3D seismic interpretation

3D seismic processing

3D seismic acquisition

Jeruk 2 re-entry

Jeruk 2 appraisal

Jeruk 1 discovery

Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4

03

Jeruk Appraisal TimelineJeruk Appraisal Timeline

• Appraisal drilling may extend through to late 2006

• Early production concept design continues in parallel

20

37

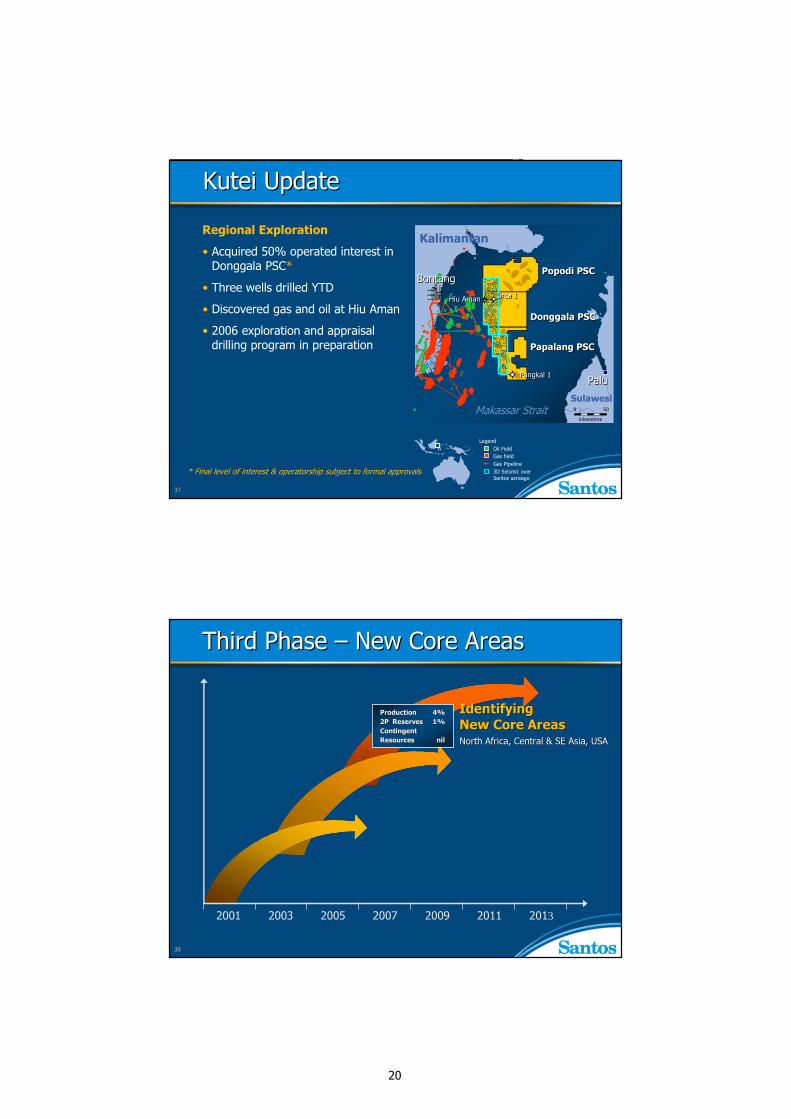

Kutei UpdateKutei Update

Regional Exploration

• Acquired 50% operated interest in Donggala PSC*

• Three wells drilled YTD

• Discovered gas and oil at Hiu Aman

• 2006 exploration and appraisal drilling program in preparation

LegendOil FieldGas fieldGas Pipeline3D Seismic over Santos acreage

PaluPalu

BontangBontang

Sulawesi

Kalimantan

Makassar Strait

Papalang PSC Papalang PSC

Popodi PSCPopodi PSC

Donggala PSC Donggala PSC

Pangkal 1Pangkal 1

Hiu AmanHiu Aman Orca 1Orca 1

50

kilometres

0

* Final level of interest & operatorship subject to formal approvals

38

Third Phase Third Phase –– New Core AreasNew Core Areas

2001 2005 2007 2009 2011 20132003

Identifying Identifying New Core AreasNew Core AreasNorth Africa, Central & SE Asia, USANorth Africa, Central & SE Asia, USA

ProductionProduction 4%4%2P Reserves2P Reserves 1%1%ContingentContingentResourcesResources nilnil

21

39

Kyrgyzstan UpdateKyrgyzstan Update

• Recent farm-in, due diligence review in progress

• Staged work program 2005 to 2008

• 16,500 km2 in 10 blocks

• Earning 80% equity

Kyrgyzstan

China

KazakstanBishkek

Djalal-AbadFergana BasinFergana Basin

TarimTarim BasinBasinTajikistan

Uzbekistan

Fergana

40

OutlookOutlook• Production

- Increased to 55 mmboe in 2005

- At least 10% further growth in 2006

• Development

- Start-up of John Brookes

- Progress at Casino, Oyong, Bayu-Undan, Maleo, Fairview

• Appraisal

- John Brookes, Reindeer, Jeruk, Legendre, Hurricane, Hiu Aman

• Exploration

- 19 wildcats in second half

22

41

Delivering GrowthDelivering Growth John ElliceJohn Ellice--FlintFlintCEO & Managing DirectorCEO & Managing Director

OverviewOverview

Financial performance Financial performance

Delivering Growth Delivering Growth

Enhancing existing core areasEnhancing existing core areas

Maturing emerging core areasMaturing emerging core areas

Identifying new core areasIdentifying new core areas

Q&AQ&A

442

23

43

Reference slides

44

Drilling50OilGulf of SuezRas Abu Darag

Fourth50OilGulf of SuezPawnee

Fourth100GasTexas state watersCougar LB54

Fourth50OilGulf of SuezNZB-3

Fourth100GasTexasBlack Horse

Fourth43OilBarrowBricklanding

Fourth45OilEast JavaHerbras

Third60OilCooperSaratoga

Third75OilEast JavaNyari (Nuri)

Third50GasBowenGreenmount

Third 60OilCooperWindula

Third18OilEast JavaBanjar Panji

Third 50GasBowenYamala

Third 50OilGulf of SuezNZB-2

Third21GasBonaparteFirebird

Third100GasTexas state watersBobcat A

Third20OilGulf of SuezKhufu

Drilled50GasOtwayHenry

Drilling40GasBonaparteCaldita

%>250100 - 25050 -1001 - 50

TimingSantos InterestUpside Resource Potential (mmboe)TargetBasin / AreaWell Name

Upcoming ExplorationUpcoming Exploration

√√

√√

√√

√√

√√

√√√√√√√√

√√√√

√√

√√

√√

√√

√√

√√√√

√√

√√

The exploration portfolio is constantly being optimised therefore the above program may vary as a result of rig availability, drilling outcomes and as new prospects mature

24

45

Prices & Exchange Rates Prices & Exchange Rates

-6.169.7874.01A$/US$ Exchange Rate

(after hedging)

+10.03.213.53Santos Average Gas Price A$/GJ

+47.745.4367.11Realised Oil Price (A$/bbl)

+56.731.7049.67Realised Oil Price (US$/bbl)

Half Year Half Year Half Year Half Year ChangeChange20052005 20042004 %%

46

Half Year Half Year Half Year Half Year ChangeChange20052005 20042004 %%

Cost of SalesCost of Sales

48.8385573Cost of sales

58.7172273D,D&A

-(17)Inventory movement

359Gas purchases

22.9210258Total operating costs

-18.52722PRRT

38.53954Royalties

-1717Pipeline tariffs

29.9127165Production costs

$m

25

47

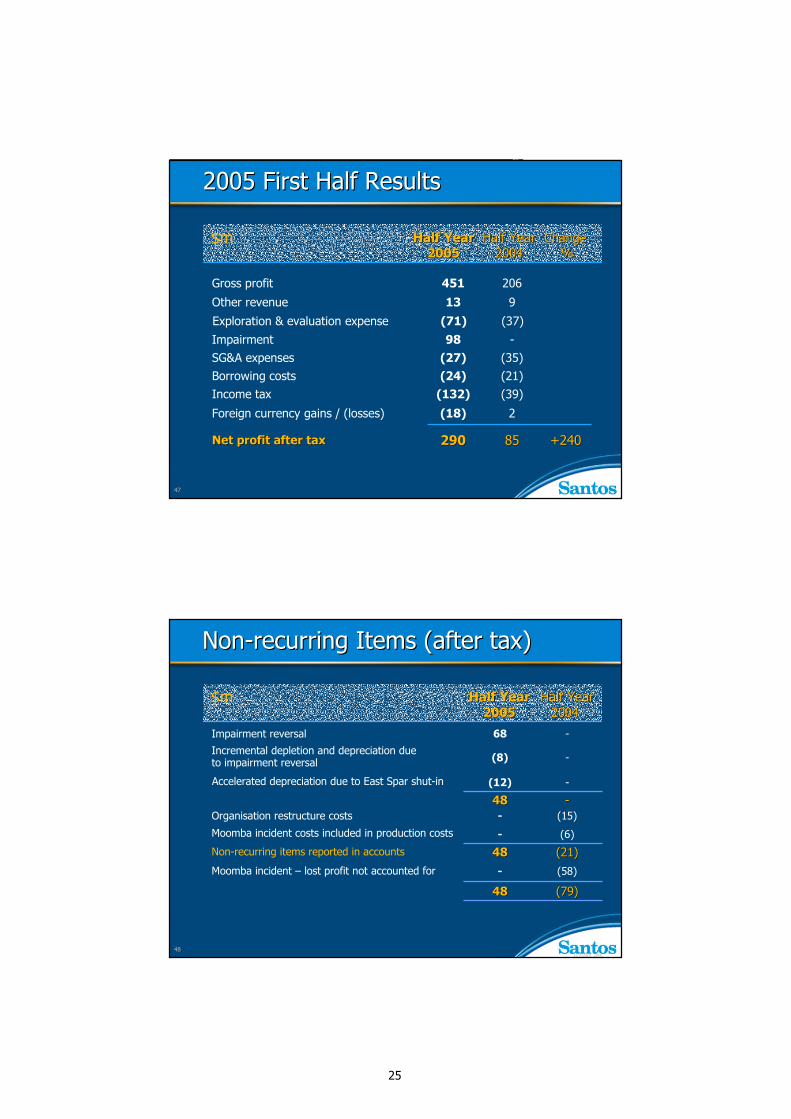

2005 First Half Results2005 First Half Results

Half Year Half Year Half Year Half Year ChangeChange20052005 20042004 %%

+240+2408585290290Net profit after taxNet profit after tax

2(18)Foreign currency gains / (losses)

(39)(132)Income tax(21)(24)Borrowing costs(35)(27)SG&A expenses

-98Impairment

913Other revenue

206451Gross profit

(37)(71)Exploration & evaluation expense

$m

4815 August, 2000

Non-recurring items reported in accounts

NonNon--recurring Items (after tax)recurring Items (after tax)

Half Year Half Year Half Year Half Year 20052005 20042004

Moomba incident – lost profit not accounted for

(15)-

Moomba incident costs included in production costs

Organisation restructure costs

-(12)

-(8)Incremental depletion and depreciation due to impairment reversal

-68Impairment reversal

Accelerated depreciation due to East Spar shut-in

--4848

(6)-

4848 (21)(21)(58)-

4848 (79)(79)

$m

26

49

20052005 20042004

127612Acquisitions

9309301,0111,011TOTALTOTAL

713716Development

91122Delineation

126173Exploration

2005 Capital Expenditure2005 Capital Expenditure OutlookOutlook

$m

50

Record Development ContinuesRecord Development Continues1st Half 2004 - $390m1st Half 2005 - $463m

100 80 60 40 20 0

Exploration

Bayu-Undan liquids

Bayu-Undan LNG

Mutineer-Exeter

Cooper gas

Cooper oil D&D

Moomba LRP rebuild

USA

Southern Australia

Corporate & Other

20

22

79

97

32

0

23

21

38

29

66

53

5

64

26

36

25

3

10

26

John Brookes

Indonesia

35

4179

23

0 20 40 60 80 100

27

51

Profit Comparison Profit Comparison 2004 2004 Half Year Half Year

AGAAPAGAAP VarianceVariance AIFRSAIFRS2004 2004 Full Year Full Year

AGAAPAGAAP VarianceVariance AIFRSAIFRS

Sales

Operating costs

Depletion & depreciation

Other revenueExploration & evaluation

Impairment

Foreign currency

Finance costs

Other expenses

Net profit after tax

Income tax expense

Net profit before tax

591 - 591(213) - (213)

(208) 36 (172)

9 - 9

- (37) (37)

- - -

2 - 2

(40) 5 (35)

(12) (9) (21)

129 (5) 124

(42) 3 (39)

87 (2) 85

1,501 - 1,501(527) - (527)

(512) 65 (447)

194 9 203

- (119) (119)

(16) 24 8

- 6 6

(69) 10 (59)

(30) (17) (47)

541 (22) 519

(161) (3) (164)

380 (25) 355

$m$m

52

2005 Second Half Sensitivities 2005 Second Half Sensitivities

ChangeChange NPAT impactNPAT impact((A$mA$m))

SensitivitySensitivity

5.01%Interest rates

5.01 cent$A/$US exchange rate

8.0US$1/bblUS dollar oil price