200? APR -2 AMU: 28 - Louisiana Legislative Auditor APR -2 AMU: 28 CONSOLIDATED GRAVITY DRAINAGE...

35

, rn RECEIVf n LEGISLATIVE /-UOITOR 200? APR -2 AMU: 28 CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2 of the Parish of St. Mary State of Louisiana FINANCIAL REPORT For the Year Ended September 30, 2006 Under provisions of state law, this report is a public document. Acopy of the report has bean submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, at the office of theparish clerk of court. • > / . X / . .^ Release Date

Transcript of 200? APR -2 AMU: 28 - Louisiana Legislative Auditor APR -2 AMU: 28 CONSOLIDATED GRAVITY DRAINAGE...

, rn RECEIVf nLEGISLATIVE /-UOITOR

200? APR -2 A M U : 28

CONSOLIDATED GRAVITY DRAINAGEDISTRICT NO. 2

of the Parish of St. MaryState of Louisiana

FINANCIAL REPORTFor the Year EndedSeptember 30, 2006

Under provisions of state law, this report is a publicdocument. Acopy of the report has bean submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of theparish clerk of court.

• > / . X / . .^

Release Date

Consolidated Gravity Drainage District No. 2of the Parish of St. Mary

State of Louisiana

Financial Report

For the Year EndedSeptember 30,2006

Under provisions of state law, this report is a publicdocument. Acopy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

Release Date

Consolidated Gravity Drainage District No. 2of the Parish of St. Mary

State of LouisianaAnnual Financial Report

For the Year Ended September 30, 2006

TABLE OF CONTENTS

Page

Financial Section:INDEPENDENT AUDITORS' REPORT 1-2BASIC FINANCIAL STATEMENTS:

Government Wide Financial Statements:Statement of Net Assets 3Statement of Activities 4

Fund Financial Statements — Governmental FundsBalance Sheet 5Statement of Revenues, Expenditures, and Changes in

Fund Balances 6Reconciliation of the Governmental Fund Balance Sheet

to the Statement of Net Assets 7Reconciliation of the Statement of Revenues, Expenditures,

and Changes in Fund Balance of Governmental Funds tothe Statement of Activities 8

Notes to Financial Statements 9-21

Required Supplemental Information:BUDGET COMPARISON SCHEDULE:

General Fund 22

Reports Required by Government Auditing Standards:Report on Compliance and on Internal Control Over

Financial Reporting Based on an Audit of Financial StatementsPerformed in Accordance with Government Auditing Standards 23-24

Schedule of Findings and Questioned Costs 25-27

Status of Prior Year Audit Findings 28

Corrective Action Plan 29

Financial Section

ADAMS & JOHNSONCERTIFIED PUBLIC ACCOUNTANTS

P.O. BOX 729 • 517 WISE STREETPATTERSON, LOUISIANA 70392 MEMBERS:

HERBERT J. ADAMS, JR., C.RA. (985) 395-9545

W!LLIAM H. JOHNSON, III, C.RA.SOCIETY OF LOUISIANA

CERTIFIED PUBLIC ACCOUNTANTS

To the Board of CommissionersConsolidated Gravity Drainage District No. 2of the Parish of St. MaryState of LouisianaMorgan City, Louisiana

We have audited the accompanying component financial statements of the Consolidated GravityDrainage District No. 2 of the Parish of St. Mary, State of Louisiana, as of and for the year endedSeptember 30, 2006, as listed in the financial section of the table of contents. These financialstatements are the responsibility of the District's management. Our responsibility is to express anopinion on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United Statesof America. Those standards require that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free of material misstatement. An audit includesexamining, on a test basis, evidence supporting the amounts and disclosures in the financialstatements. An audit also includes assessing the accounting principles used and significant estimatesmade by management, as well as evaluating the overall general purpose financial statementpresentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the basic financial statements referred to above present fairly, in all material respects,the financial position of the Consolidated Gravity Drainage District No. 2 as of September 30, 2006,and the results of its operations for the year then ended in conformity with accounting principlesgenerally accepted in the United States of America.

The Management's Discussion and Analysis is not a required part of the financial statements but issupplementary information required by the Governmental Accounting Standards Board. However,management elected not to include this information in the financial statements for the year endedSeptember 30, 2006.

Our audit was made for the purpose of forming an opinion on the financial statements taken as awhole. The accompanying supplementary information, as listed in the table of contents, while notconsidered necessary for a fair presentation of the financial statements, is presented as supplementaryanyalytical data.

Such information, except for that portion marked "unaudited"., on which we express no opinion, hasbeen subjected to auditing procedures applied in the audit of the financial statements, and in ouropinion, the information is fairly stated in all material respects in relation to the financial statementstaken as a whole.

In accordance with Government Auditing Standards, we have also issued a report dated March 5,2007 on our consideration of Consolidated Gravity Drainage District No. 2's internal control overfinancial reporting and our tests of its compliance with certain provisions of laws, regulations,contracts, and grants. That report is an integral part of an audit in accordance with GovernmentAuditing Standards and should be read in conjunction with this report in considering the results of ouraudit.

Adams and JohnsonCertified Public Accountants

Patterson, LouisianaMarch 5, 2007

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

STATE OF LOUISIANAStatement of Net Assets

September 30, 2006

GovernmentalActivities

ASSETSCurrent assets:Cash and cash equivalentsDue from other governmentsPrepaid expenses

Total current assets

Non-current assets:Bond issue and refunding cost, net of amortizationCapital assets, net of depreciation

Total non-current assetsTotal assets

LIABILITIESCurrent liabilities:Accounts payablePayroll taxes payableInterest payable

Bonds payable - current

Total current liabilities

Non-current liabilities:Bonds payable - long term

Total non-current liabilitiesTotal liabilities

NET ASSETSInvested in capital assets, net of related debtRestricted for:Capital Projects

Debt Service

Unrestricted

Total net assets

$

$

$

3,686,1882,926

49,5563,738,670

136,4318,408,4228,544,853

$ 12,283,523

24,876797

23,763

355,000

404,436

6,090,0006,090,000

$ 6,494,436

$ 1,963,422

3,406,736

335,209

83,720

$ 5,789,087

The accompanying notes are an integral part of these financial statements.3

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

STATE OF LOUISIANAStatement of Activities

For the Year Ended September 30, 2006

Governmental Activities - Gravity Drainage

Program expenses:Maintenance labor, pump operators $ 56,871Fuel and electricity 13,426Repairs and maintenance 149,058Insurance 67,313Other operating costs 81,720Interest 274,623Amortization 105321Depreciation 299,722

Total program expenses $ 953,054

General revenues:Ad valorem taxes $ 971,096Interest income earned 14,186

Total general revenues 985,282

Change in net assets $ 32,228

Net assets - beginning 5,756,859

Net assets - ending $ 5,789,087

The accompanying notes are an integral part of these financial statements.4

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST.^MARY

STATE OF LOUISIANABalance Sheet

September 30, 2006

ASSETS

Cash and cash equivalentsDue from other fundsDue from other governments

Total assets

LIABILITIES

Accounts payablePayroll taxes payableDue to other funds

Total liabilities

General Capital ProjectOper/Maint Project

$ 59,837 $ 3,414,701-_

$ 59,837 $ 3,414,701

$ 24,876 $797

42,109

DebtService

$ 211,65042,1092,926

$ 256,685

$--

TotalGovernmental

Funds

$ 35686,18842,1092,926

$ 3,731,223

$ 24,876797

42,109

$ 25,673 $ 42,109 $ $ 67,782

FUND BALANCES

Reserved-reported in:Capital Projects FundDebt Service Fund

Unreserved-reported in:General Fund

Total fund balances

Total liabilities andfund balances

34,164

34,164

$ 3,372,592 $ - $ 3,372,592256,685 256,685

34,164

3,372,592 256,685 3,663,441

$ 59,837 $ 3,414,701 $ 256,685 $ 3,731,223

The accompanying notes are an integral part of these financial statements.5

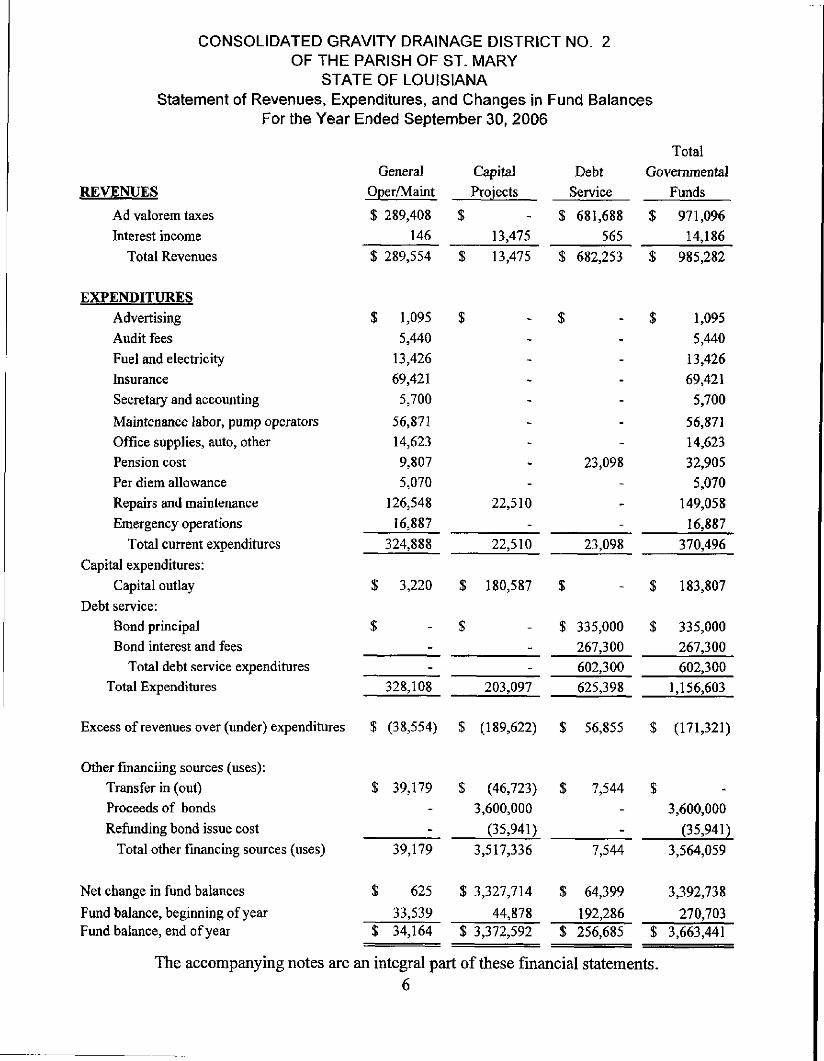

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

STATE OF LOUISIANAStatement of Revenues, Expenditures, and Changes in Fund Balances

For the Year Ended September 30, 2006

REVENUES

Ad valorem taxesInterest income

Total Revenues

EXPENDITURESAdvertisingAudit feesFuel and electricityInsuranceSecretary and accounting

Maintenance labor, pump operatorsOffice supplies, auto, otherPension costPer diem allowanceRepairs and maintenanceEmergency operations

Total current expendituresCapital expenditures:

Capital outlayDebt service:

Bond principalBond interest and fees

Total debt service expendituresTotal Expenditures

Excess of revenues over (under) expenditures

Other financiing sources (uses):Transfer in (out)Proceeds of bondsRefunding bond issue cost

Total other financing sources (uses)

Net change in fund balances

Fund balance, beginning of yearFund balance, end of year

The accompanying notes are an integral part of these financial statements.6

GeneralOper/Maint

$ 289,408146

$ 289,554

$ 1,0955,440

13,42669,421

5,700

56,87114,6239,8075,070

126,54816,887

324,888

$ 3,220

$--

328,108

$ (38,554)

$ 39,179--

39,179

$ 625

33,539$ 34,164

CapitalProjects

$13,475

$ 13,475

$----

----

22,510-

22,510

$ 180,587

$--

203,097

$ (189,622)

$ (46,723)3,600,000

(35,941)3,517,336

$ 3,327,714

44,878$ 3,372,592

DebtService

$ 681,688565

$ 682,253

$----

--

23,098---

23,098

$

$ 335,000267,300602,300625,398

$ 56,855

$ 7,544--

7,544

$ 64,399192,286

$ 256,685

TotalGovernmental

Funds

$ 971,09614,186

$ 985,282

$ 1,0955,440

13,42669,421

5,700

56,87114,62332,905

5,070149,05816,887

370,496

$ 183,807

$ 335,000267,300602,300

1,156,603

$ (171,321)

$3,600,000

(35,941)3,564,059

3,392,738

270,703$ 3,663,441

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

STATE OF LOUISIANA

Reconciliation of the Governmental Fund Balance Sheet to the Statement of Net AssetsSeptember 30, 2006

Total Fund Balances - Governmental Funds (Page 6) $ 3,663,441

The purchase of capital assets are reported as expenditures asthey are incurred in the government funds. The Statement ofNet Assets reports capital assets as an asset and thesecapital assets are depreciated over their estimated usefullives and are reflected as depreciation expense in theStatement of Activities.

Cost of Capital Assets at September 30, 2006 12,167,824Less: Accumulated Depreciation as of September 30, 2006 (3,759,402)

Interest payable on long-term debts does not require currentfinancial resources. Therefore interest payable is not reported asa liability in the governmental funds balance sheet. (23,763)

Expenditures for prepaid expenses in governmental activities are notfinancial resources and therefore are not reported in the funds

Prepaid insurance 49,556Bond isssue and refunding cost 146,752Bond issue and refunding cost accumulated amortization (10,321)

Long-term liabilities are not due and payable in the current periodand, therefore, they are not required in the governmental fundsbalance sheet. (6,445,000)

Net Assets - Government - Wide Statement (Page 4) $ 5,789,087

The accompanying notes are an integral part of these financial statements.7

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

STATE OF LOUISIANAReconciliation of the Statement of Revenues, Expenditures, and

Changes in Fund Balances of Governmental Fundsto the Statement of Activities

For the Year Ended September 30, 2006

Net change in fund balances - total governmental funds (fund financial statements) $ 3,392,738

Amounts reported for governmental activities in the statement of activities(government-wide financial statements) are different because:

Governmental funds report capital outlays as expenditures in the individual fund.Governmental activities report depreciation expense to allocate the cost ofthose capital assets over the estimated useful lives of the asset.

Capital outlay $ 183,807Depreciation expense (299,722)

(115,915)The issuance of long-term debts (e.g. bonds) provides current financial resourcesto government funds, while the repayment of the principal of long-term debtconsumes the current resources of government funds. Neither transactionhowever, has any effect on net assets. Also, governmental funds report theeffect of issuance cost when the debt is first issued, whereas the issuance costare deferred and amortized in the statement of activities,consist of: Bond proceeds $ (3,600,000)

Bond principal retirement 335,000Bond issuance cost 35,941Bond issue cost and refunding amortization (10,321)

(3,239,380)

Some expenses reported in the statement of activities do not requirethe use of current financial resources; therefore, are not reportedas expenditures in governmental funds.

Accrued interest expense on long-term debt is reported in thegovernment-wide statement of activities and changes in net assets,but does not require the use of current financial resources;therefore, change in accrued interest expense is not reported asexpenditures in governmental funds. (7,323)

Current financial resources utilized for prepaid expenses are reportedas expenditures in the governmental funds. 2,108

Change in net assets of governmental activities 32,228

The accompanying notes are an integral part of these financial statements.8

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

On November 12, 1997, the St. Mary Parish Council created "Consolidated Gravity Drainage DistrictNo. 2 of the Parish of St. Mary," a consolidated gravity drainage district which included theboundaries of Gravity Drainage District No. 3 and Gravity Drainage District No. 5. The ConsolidatedGravity Drainage District No. 2 was created and established pursuant to the provisions of anordinance adopted by the St. Mary Parish Council, all in accordance with the provisions of Part II,Chapter 7, Title 38 of the Louisiana Revised Statutes of 1950, as amended. The District is managedby five board of commissioners as appointed by the St. Mary Parish Council. The District has fullpower and authority to drain lands in the district by construction, maintenance and operation ofgravity and/or forced drainage facilities, including drains, drainage canals, ditches, pumps andpumping plants, dikes, levees and other related works.

Note 1 -Summary of Significant Accounting Policies

The accounting and reporting policies of the Consolidated Gravity Drainage District No. 2(the District) conform to generally accepted accounting principles as applicable togovernments. The Governmental Accounting Standards Board (GASB) is the acceptedstandard-setting body for establishing governmental accounting and financial reportingprinciples.

The following is a summary of certain significant accounting policies:

A. Reporting Entity

As the governing authority of the parish, for reporting purposes, the St. Mary ParishCouncil is the financial reporting entity for St. Mary Parish. The GovernmentalAccounting Standards Board established criteria for determining which component unitsshould be considered part of the St. Mary Parish Council for financial reporting purposes.The St. Mary Parish Council appoints a voting majority of the District's governing bodyand can impose its will on the District. Based on criterion applied, the District is acomponent unit of the St. Mary Parish Council. The accompanying financial statementspresent information only on the funds maintained by the District and do not presentinformation on the St. Mary Parish Council, the general government services provided bythe Council, or the other governmental units that comprise the financial reporting entity forSt. Mary Parish, Louisiana.

The District has no entities or organizations that are required to be included in its financialreport as defined by Government Accounting Standards Board (GASB) Statement 14.

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

Note 1 -Summary of Significant Accounting Policies, (Continued)

B.Basic Financial Statements - Basis of Presentation

Government - Wide and Fund Financial Statements

The District's basic financial statements include both government-wide (reporting theDistrict as a whole) and fund financial statements (reporting the District's major funds).Both the government-wide and fund financial statements categorize primary activities asgovernmental type activities. All of the District's administrative services are classified asgovernmental activities.

In the government-wide Statement of Net Assets, the governmental activities are reportedon a full accrual, economic resource basis, which recognizes all long-term assets andreceivables as well as long-term debt and obligations. The District's net assets are reportedin three parts - invested in capital assets, net of related debt; restricted net assets; andunrestricted net assets.

The government-wide Statement of Activities reports both the gross and net cost of eachof the District's functions and activities. These functions are also supported by generalgovernment revenues (ad valorem taxes and interest earned). The Statement of Activitiesreduces gross expenses (including depreciation) by related program revenues, operatingand capital grants. Program revenues must be directly associated with the function.

The net costs (by function) are normally covered by general revenue (ad valorem taxes andinterest earned, etc.). This government-wide focus is more on the sustainability of theDistrict as an entity and the change in the District's net assets resulting from the currentyear's activities.

Fund Accounting

The District uses funds and account groups to report on its financial position and theresults of its operations. Fund accounting is designed to demonstrate legal compliance andto aid financial management by segregating transactions related to certain governmentfunctions or activities. A fund is a separate accounting entity with a self-balancing set ofaccounts.

10

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

Note 1 -Summary of Significant Accounting Policies, (Continued)

B.Basic Financial Statements — Basis of Presentation, (Continued)

Governmental Funds

Governmental Funds are those through which the governmental functions of the Districtare financed. The acquisition, uses and balances of the District's expendable financialresources and the related liabilities are accounted for through Governmental Funds. Themeasurement focus is upon determination of changes in financial position, rather thanupon net income determination. The Governmental Funds of the District are as follows:

General Fund - The General Fund is the general operating fond of the District. Itis used to account for all financial resources except those that are required to beaccounted for in another fund.

Capital Projects Fund - The Capital Projects Fund is used to account forfinancial resources to be used for the acquisition or construction of major capitalfacilities or repair or replacement of major capital facilities (other than thosefinanced by proprietary funds and trust funds).

Debt Service Fund - The Debt Service Fund is used to account for theaccumulation of resources for, and the payment of general long-term obligationprincipal, interest and related costs.

C. Measurement Focus. Basis of Accounting and Financial Statement Presentation

The government-wide financial statements are reported using the economic resourcesmeasurement focus and the accrual basis of accounting. Revenues are recorded whenearned and expenses are recorded when a liability is incurred, regardless of the timing ofrelated cash flows. Property taxes are recognized as revenues in the year for which they areboth levied and budgeted as general revenue. Grants and similar items are recognized asrevenue as soon as all eligibility requirements imposed by the provider have been met. Thegovernmental fund financial statements are accounted for using a current financialresources measurement focus. With this measurement focus only current assets and currentliabilities are generally included on the balance sheet. Operating statements of these fundspresent increases and decreases in net current assets. The modified accrual basis ofaccounting is used by the governmental fund financial statements. Under the modifiedaccrual basis of accounting, revenues are recognized when susceptible to accrual (i.e.,when they become both measurable and available). "Measurable" means the amount of thetransaction can be determined and "available" means collectible within the current periodor soon enough thereafter to be used to pay liabilities of the current period.

11

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

Note 1-Summary of Significant Accounting Policies, (Continued)

CMeasurement Focus, Basis of Accounting and Financial Statement Presentation,(Continued)

Ad valorem taxes are considered susceptible to accrual. Interest income is recorded whenreceived by the District. Expenditures are generally recognized under the modified accrualbasis of accounting when the related fund liability is incurred.

D.Budgets and Budgetary Accounting

The District complies with the "Louisiana Local Government Budget Act" and henceforth,budgets are adopted for its general fund on a modified accrual basis that is consistent withgenerally accepted accounting principles. Annual budgets are prepared by the Board ofCommissioners of the District along with a budget message and presented to the Board foradoption no later than 15 days prior to the beginning of the fiscal year. Budgets areadopted for the fiscal year and lapse at year-end. The budget is amended by supplementalappropriations as needed to during the year to comply with state law.

The Consolidated Gravity Drainage District No. 2 follows these procedures in establishingthe budgetary data reflected in the financial statements:

a. Formal budgetary integration is employed as a management control deviceduring the year for the General Fund. The budget is prepared and adopted on abasis consistent with generally accepted accounting principles (GAAP), whichfor the General Fund is the modified accrual basis of accounting.

b. The District approves and adopts total budget revenue and expenditures only.The District transfers budget amounts between expenditure classifications withinthe General Fund. Therefore, the level of budgetary responsibility is by totalexpenditures; however, for report purposes, this level has been expanded toclassifications of expenditures. Unused appropriations lapse at the end of theyear.

E. Cash and Investments

Cash includes amounts in demand deposits, interest-bearing deposits, and money marketaccounts. Under state law, the District may deposit funds in demand deposits, interest-bearing demand deposits, money market accounts, or time deposits with state banksorganized under Louisiana law and national banks having their principal offices inLouisiana.

Under state law, the District may invest in Louisiana Asset Management Pool (LAMP),United States bonds, treasury notes, or certificates. Investments are stated at cost.

12

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

Note 1-Summary of Significant Accounting Policies, (Continued)

E. Cash and Investments, (Continued)

State law also requires that deposits of all political subdivisions be fully collateralized atall times. Acceptable collateralization includes the FDIC insurance and the market value ofsecurities purchased and pledged to the political subdivision. Obligations of the UnitedStates, the State of Louisiana and certain political subdivisions are allowed as security fordeposits. Obligations furnished, as security must be held by the political subdivision orwith an unaffiliated bank or trust company for the account of the political subdivision.

F. Bad Debts

Uncollectible amounts due for ad valorem taxes are recognized as bad debts in the yearthey are deemed uncollectible. The failure to utilize the allowance method to account forbad debts is not material to the financial statements.

G. Capital Assets

Capital assets, which include property, plant, and equipment, are reported in thegovernment-wide financial statements. Capital assets are capitalized at historical cost.Donated assets are recorded as capital assets at their estimated fair market value at the dateof donation.

The costs of normal maintenance and repairs that do not add to the value of the asset ormaterially extend asset lives are not capitalized. Major outlays for capital assets andimprovements are capitalized as projects are constructed. All capital assets, other thanland, are depreciated using the straight-line method over the following useful lives:

EstimatedDescription Lives

Buildings, pump stations and improvements 15-40 yearsDrainage system improvements 20-25 yearsEquipment, pumps and engines 15-25 yearsLand, canals, levees and construction in progress Not being depreciated

13

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

Note 1 -Summary of Significant Accounting Policies, (Continued)

H.Long-Term Debt

In the government-wide financial statements, long-term debt and other long-termobligations are reported as liabilities in the applicable governmental activities statement ofnet assets. In the fund financial statements, governmental fund types recognize bondpremiums and discounts, as well as bond issuance costs, during the current period. Theface amount of the debt issued is reported as other financing sources. Premiums receivedon debt issuances are reported as other financing sources while discounts on debt issuancesare reported as other financing uses. Issuance costs, whether or not withheld from theactual debt proceeds received, are reported as debt service expenditures.

l.Fund Equity

In the fund financial statements, governmental funds report reservations of fund balancesfor amounts that are not available for appropriation or legally segregated by outside partiesfor a specific future use.

] Estimates

The preparation of financial statements in conformity with accounting principles generallyaccepted in the United States of America require management to make estimates andassumptions that affect the reported amounts of assets and liabilities and disclosure ofcontingent assets and liabilities at the date of the financial statements and the reportedamounts of revenues, expenditures, and expenses during the reporting period. Actualresults could differ from those estimates.

Note 2 - Cash and Interest Bearing Deposits

At present, all of the District's cash and cash equivalents are in demand deposits at a fiscalagent bank. These deposits are stated at cost, which approximates market. Under state law,these deposits, (or the resulting bank balances) must be secured by federal depositinsurance or the pledge of securities owned by the fiscal agent bank. The market value ofthe pledged securities plus the federal deposit insurance must at all times equal the amounton deposit with the fiscal agent bank. Acceptable collateralization includes the $100,000FDIC/FSLIC insurance and the market value of securities purchased and pledged.Obligations of the United States, the State of Louisiana and certain political subdivisionsare allowed as security for deposits. Obligations furnished as security must be held by theDistrict or with an unaffiliated bank or trust company for the account of the District.

14

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

Note 2-Cash and Interest Bearing Deposits, (Continued)

The District's deposits are categorized to give an indication of the level of risk assumed bythe District at September 30, 2006:

Category 1 - Insured or collateralized with securities held by the District or by its agent inthe District's name.

Category 2 - Collateralized with securities held by the pledging financial institution's trustdepartment or agent in the District's name.

Category 3 - Uncollateralized (this includes any bank balance that is collateralized withsecurities held by the pledging financial institution, or by its trust departmentor agent but not in the District's name).

At September 30, 2006, the District has cash and interest-bearing deposits (book balances)totaling $3,686,188 as follows:

Operation & Debt CapitalMaintenance Service Project Total

Cash-Interest bearing checking $ 59,837 $211,650 $ 3.414,701 $3,686.188

Total $ 59.837 S 211.650 $ 3.414.701 $3.686.188

Deposit balances (bank balances) at September 30, 2006, are secured as follows:

Bank balances $ 3.697.024

Federal deposit insurance (Category 1) $ 200,000Pledged securities (Category 1) 5,237,301

Total federal insurance and pledged securities S5.437.3Q1

Excess SI.740.277

15

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

NOTE 3 - Due from Other Governments

The amounts due from other governmental units consisted of property taxes due from St.Mary Parish Sheriff.

2006General Fund:

*Louisiana Bond Commission

* These funds are owed to the District because the District overpaid bond issue costs to theLouisiana Bond Commission but was not refunded until after year end.

Note 4-Ad Valorem Tax Assessment

Consolidated Gravity Drainage District No. 2 submitted a proposition that received voterapproval in May 1998 that includes millage for operation and maintenance and millage forrepayment of a substantial bond issue for capital improvement projects. 4.67 mills and11.0 mills was assessed for the operation and maintenance fund and the debt service fundrespectively for 2006.

Property taxes are levied each November 1 on the assessed value listed as of the priorJanuary 1 for all real property, merchandise and movable property located in the District'sboundaries. Assessed values are established by the St. Mary Parish Assessor's Office andthe State Tax Commission at percentages of actual value as specified by Louisiana law. Areevaluation was completed for the list of properties at January 1, 2006. Taxes are due andpayable December 31 and are delinquent after that date with interest being charged. Liendate for all delinquent properties is April 1.

16

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

Note 5 - Capital Assets

GovernmentalActivities:

Cost of Capital assets, not beingdepreciated

Land, canals and leveesConstruction in progress

Total not being depreciated

Cost of Capital assets, being depreciatedPumps & enginesPump station improvements, buildingsDrainage improvements

Total being depreciated

BeginningBalance

$ 2,315,3528,973

$ 2,324,325

$ 2,122,6625,546,5221,990,508

$ 9,659,692

Increases

$104,584

$ 104,584

$ 3,22076,003

-$ 79,223

Decreases

---

$--

$

EndingBalance

$ 2,315,352113,557

$ 2,428,909

$ 2,125,8825,622,5251,990,508

$ 9,738,915

Less accumulated depreciation:Pumps & enginesPump station improvements, buildingsDrainage improvements

TotalsCapital assets, net

$ 1,652,3081,356,000

451,372$ 3,459,680$ 8,524,337

$ 56,012179,90563,805

$ 299,722-

$

$ 1,708,3201,535,905

515,177$ 3,759,402$ 8,408,422

Note 6 - On-Behalf Payments for Fringe Benefits

Property tax revenues include amounts withheld by the Sheriff to make "on-behalfpayments for fringe benefits" which represent the District's pro-rata share of retirementplan contributions for other governmental units. Because the District is one of severalgovernmental agencies receiving proceeds from a property tax assessment, it has to beara pro-rata share of the pension expense relating to the public employees who participatein the Parochial Employees Retirement System. The District's pro-rata share of therequired contribution $32,905, which was withheld by the Sheriff from property taxcollections to satisfy the District's obligation, has been presented as an "ad valorem taxdeduction" expenditure of the general fund in these financial statements. The Districthas also increased its property tax revenues by the same as the intergovernmentalexpenditure.

17

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

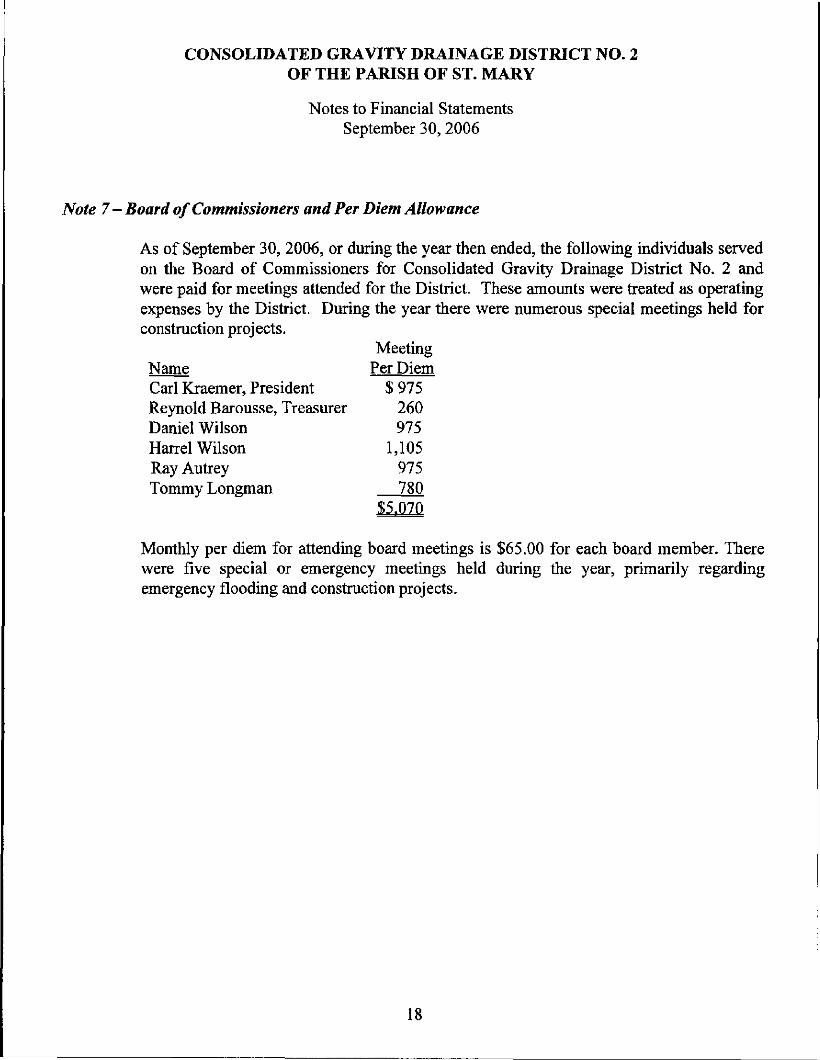

Note 7 - Board of Commissioners and Per Diem Allowance

As of September 30, 2006, or during the year then ended, the following individuals servedon the Board of Commissioners for Consolidated Gravity Drainage District No. 2 andwere paid for meetings attended for the District. These amounts were treated as operatingexpenses by the District. During the year there were numerous special meetings held forconstruction projects.

MeetingName Per DiemCarl Kraemer, President $ 975Reynold Barousse, Treasurer 260Daniel Wilson 975Hairel Wilson 1,105Ray Autrey 975Tommy Longman 780

Monthly per diem for attending board meetings is $65.00 for each board member. Therewere five special or emergency meetings held during the year, primarily regardingemergency flooding and construction projects.

18

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes to Financial StatementsSeptember 30, 2006

Note 8 - General Long-Term Debt

A summary of general long-term debt is as follows:

Description

$5,240,000 of GeneralObligation Bonds, Series 1998,payable in annual installmentsof $225,000 to $250,000through March 1,2008,with interest rate at 5.4%

Balance at9-30-05

Defeased/Issued Retired

Balance at9-30-06

$710,000 $ $ 225,000 $ 485,000

$2,470,000 of GeneralObligation Refunding Bonds,Series 2005 to defease a portion ofThe General Obligation BondsSeries 1998, payable in annualinstallments of $5,000 to $305,000payable through March 1, 2018with interest at 3.8%

$3,600,00 of GeneralObligation Bonds, Series 2005,payable in annual installmentsof $105,000 to $280,000 throughMarch 1, 2025, with interest of4.25% to 5.25%

2,470,000 5,000 2,465,000

3,600.000 105,000 3,495.000

$3.180.000 S3.6QO.OQO S335.0QO £6.445.000

19

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

Notes To Financial StatementsSeptember 30, 2006

Note 8- General Long-Term-Debt, (Continued)

On September 1, 2006, the District issued $2,470,000 in General Obligation Refunding Bonds with aninterest rate of 3.8% for the purpose of advance refunding of the callable maturities of the Issuer'sGeneral Obligation Bonds, Series 1998, dated September 1998, which mature serially on March 1 ofthe years 2009 through 2018, inclusive in principal and accrued interest to their redemption date ofMarch 1, 2008 and paying the cost of the issuance of the Bonds. The 1998 series had an averageinterest rate of 4.62%. The Bond proceeds of the $2,470,000 and $1,045,000 of surplus funds in theDistrict's Debt Service Fund were deposited into an irrevocable trust with an escrow agent to providefuture debt service payments of the Series 1998 General Obligation Bonds, and for payment of the$23,107 in Bond issue cost of the 2006 General Obligation Refunding Bonds. As a result as ofSeptember 30, 2006 $3,420,000 of the 1998 bonds are considered defeased and that portion of theliability has been removed from the government-wide statement of net assets.

As required by GASB 23 the District did not reflect an economic gain or loss on the advancerefunding of the bonds due to the fact there was not a premium or discount on the call date of theoriginal bonds and there were no unamortized bond issue costs on the original bonds. The differencebetween the cash flows required to service the old debt and the cash flows required to service the newdebt and the complete refunding resulted in a net savings, the present value of which is $119,868.

The deferred amount on refunding on the government-wide financial statements in the amount of$71,893 is reflected as an asset on the statement of net assets. The deferred amount on refunding isthe difference between the reacquistion price of $3,491,893 (which is the funds required to refund theold debt) and the net carrying amount of $3,420,000 of the old debt.

The deferred amount on the refunding and the bond issue cost are being amortized over the life of thedebt on the statement of net assets.

There are a number of limitations and restrictions contained in the general obligation bond indentures.The District is in compliance with all significant limitations and restrictions at September 30, 2006.See page 21 for a summary of bond principal maturities and interest requirements.

20

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARYNotes to Financial Statements

September 30, 2006

Note 8- General Long-Term-Debt, (Continued)

The following is a summary of bond principal maturities and interest requirements as of September30, 2006

Un refundedSeries 1998 Bonds

5.40%Payment Prinicpal Interest

Date Due Due3/1/2007 $ 235,000 $ 13,0959/1/2007 6,7503/1/2008 250,000 6,7509/1/20083/1/20099/1/20093/1/20109/1/20103/1/20119/1/20013/1/20129/1/20123/1/20139/1/20133/1/20149/1/20143/1/20159/1/20153/1/20169/1/20163/1/20179/1/20173/1/20189/1/20183/1/20199/1/20193/1/20209/1/20203/1/20219/1/20213/1/20229/1/20223/1/20239/1/20233/1/20249/1/20243/1/2025

$ 485,000 $ 26,595

Series 2005Refunding Bonds

3.80%Prinicpal Interest

Due$ 5,000 $

5,000

195,000

205,000

215,000

225,000

240,000

245,000

260,000

275,000

290,000

305,000

-

-

-

-

-

-

-

$ 2,465,000 $

Due46,83546,74046,74046,64546,64542,94042,94039,04539,04534,96034,96030,68530,68526,12526,12521,47021,47016,53016,53011,30511,3055,7955,795

-

-

-

-

-

-

-

-

-

-

-

-

-

-

691,315

Series 2005General Obligation Bond

Principal InterestDue Due

$ 115,000 $

120,000

125,000

130,000

140,000

145,000

155,000

160,000

170,000

175,000

185,000

195,000

205,000

215,000

225,000

240,000

250,000

265,000

280,000

$ 3,495,000 $ 1,

82,64680,20380,20377,65377,65374,99674,99672,23472,23469,25969,25966,17866,17862,88462,88459,48459,48455,87155,87151,89051,89047,58947,58942,95842,95837,98637,98632,61132,61126,98626,98620,80620,80614,30614,3067,3507,350

885,131

CalendarYearTotals

$ 631,269

632,990

562,234

564,215

570,498

571,081

580,871

574,963

583,355

585,596

591,579

596,341

285,944

285,598

284,598

287,793

285,113

286,656287,350

$ 9,048,041

21

Required SupplementalInformation

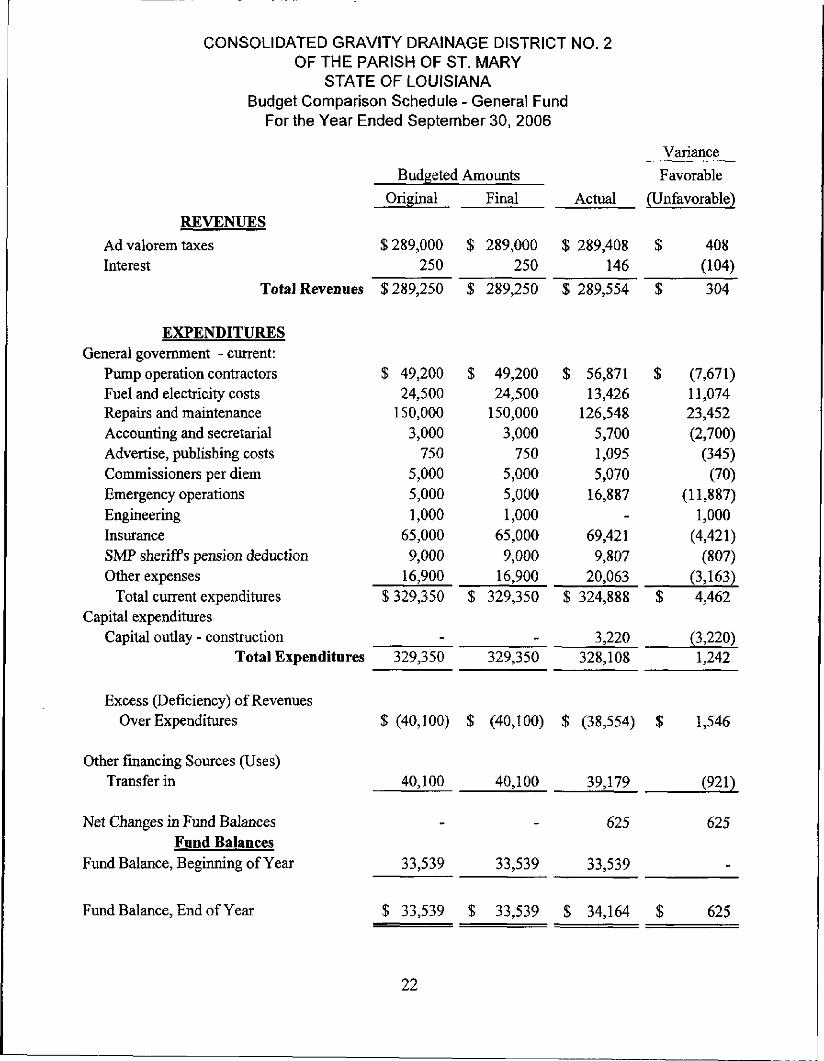

CONSOLIDATED GRAVITY DRAINAGE DISTRICT NO. 2OF THE PARISH OF ST. MARY

STATE OF LOUISIANABudget Comparison Schedule - General Fund

For the Year Ended September 30, 2006

REVENUES

Ad valorem taxesInterest

EXPENDITURESGeneral government - current:

Pump operation contractorsFuel and electricity costsRepairs and maintenanceAccounting and secretarialAdvertise, publishing costsCommissioners per diemEmergency operationsEngineeringInsuranceSMP sheriffs pension deductionOther expenses

Total current expendituresCapital expenditures

Capital outlay - constructionTotal Expenditures

Excess (Deficiency) of RevenuesOver Expenditures

Other financing Sources (Uses)Transfer in

Net Changes in Fund BalancesFund Balances

Fund Balance, Beginning of Year

Fund Balance, End of Year

Budgeted

Original

$ 289,000250

$ 289,250

$ 49,20024,500

150,0003,000

7505,0005,0001,000

65,0009,000

16,900$ 329,350

_

329,350

$ (40,100)

40,100

-

33,539

$ 33,539

Amounts

Final

$ 289,000250

$ 289,250

$ 49,20024,500

150,0003,000

7505,0005,0001,000

65,0009,000

16,900$ 329,350

_

329,350

$ (40,100)

40,100

-

33,539

$ 33,539

Actual

$ 289,408146

$ 289,554

$ 56,87113,426

126,5485,7001,0955,070

16,887-

69,4219,807

20,063$ 324,888

3,220328,108

$ (38,554)

39,179

625

33,539

$ 34,164

Variance

Favorable

(Unfavorable)

$ 408(104)

$ 304

$ (7,671)11,07423,452(2,700)

(345)(70)

(11,887)1,000

(4,421)(807)

(3,163)$ 4,462

(3,220)1,242

$ 1,546

(921)

625

-

$ 625

22

Reports Required by GovernmentAuditing Standards

HERBERT J. ADAMS, JR., C.PA.

WILLIAM H. JOHNSON, lit, C.PA

ADAMS & JOHNSONCERTIFIED PUBLIC ACCOUNTANTS

P.O. BOX 729 • 517 WISE STREETPATTERSON, LOUISIANA 70392

(985) 395-9545

MEMBERS:

AMERICAN INSTITUTE OFCERTIFIED PUBLIC ACCOUNTANTS

SOCIETY OF LOUISIANACERTIFIED PUBLIC ACCOUNTANTS

REPORT ON COMPLIANCE AND ON INTERNAL CONTROLOVER FINANCIAL REPORTING BASED ON AN AUDIT

OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCEWITH GOVERNMENT AUDITING STANDARDS

To the Board of CommissionersConsolidated Gravity Drainage District No. 2of the Parish of St. MaryState of LouisianaMorgan City, Louisiana

We have audited the basic financial statements of Consolidated Gravity Drainage District No. 2 of theParish of St. Mary, State of Louisiana as of and for the year ended September 30, 2006, and haveissued our report thereon dated March 5, 2007. We conducted our audit in accordance with auditingstandards generally accepted in the United States of America and the standards applicable to financialaudits contained in Government Auditing Standards, issued by the Comptroller General of the UnitedStates.

Compliance

As part of obtaining reasonable assurance about whether the Consolidated Gravity Drainage DistrictNo. 2's basic financial statements are free of material misstatement, we performed tests of itscompliance with certain provisions of laws, regulations, contracts and grants, noncompliance withwhich could have a direct and material effect on the determination of financial statement amounts.However, providing an opinion on compliance with those provisions was not an objective of our auditand, accordingly, we do not express such an opinion. The results of our tests disclosed a materialinstance of noncompliance that is required to be reported under Government Auditing Standardswhich is described in the accompanying schedule of Findings and Questioned Cost as 2006-2.

Internal Control Over Financial Reporting

In planning and performing our audit, we considered the Consolidated Gravity Drainage District No.2's internal control over financial reporting in order to determine our auditing procedures for thepurpose of expressing our opinion on the basic financial statements and not to provide assurance onthe internal control over financial reporting. However, we noted certain matters involving the internalcontrol over financial reporting and its operation that we consider to be reportable conditions.

23

Internal Control Over Financial Reporting, (Continued)

Reportable conditions involve matters coming to our attention relating to significant deficiencies inthe design or operation of the internal control over financial reporting that, in our judgment, couldadversely affect the Consolidated Gravity Drainage District No. 2's ability to record, process,summarize and report financial data consistent with the assertions of management in the basicfinancial statements. Reportable conditions are described in the accompanying schedule of findingsand questioned costs as item 2006-1.

A material weakness is a condition in which the design or operation of one or more of the internalcontrol components does not reduce to a relatively low level the risk that misstatements in amountsthat would be material in relation to the basic financial statements being audited may occur and not bedetected within a timely period by employees in the normal course of performing their assignedfunctions. Our consideration of the internal control over financial reporting would not necessarilydisclose all matters in the internal control that might be reportable conditions and, accordingly, wouldnot necessarily disclose all reportable conditions that are also considered to be material weaknesses.However, we consider the reportable condition identified as 2006-1 in the accompanying schedule offindings and questioned costs to be a material weakness.

This report is intended solely for the information and use of the Board of Commissioners(management), and the St. Mary Parish Council. However, under Louisiana Revised Statute 24:513,this report is distributed by the Louisiana Legislative Auditor as a public document, therefore itsdistribution is not limited.

Adams and JohnsonCertified Public Accountants

March 5,2007Patterson, Louisiana

24

Consolidated Gravity Drainage District No. 2 of the Parish of St. MaryState of Louisiana

Schedule of Findings and Questioned CostsFor The Year Ended September 30, 2006

We have audited the financial statement of Consolidated Gravity Drainage District No. 2 as of and for theyear ended September 30, 2006, and have issued our report thereon dated May 15, 2006. We conductedour audit in accordance with auditing standards generally accepted in the United States of America and thestandards applicable to financial audits contained in Government Auditing Standards, issued by theComptroller General of the United States. Our audit of the financial statements as of September 30,2006resulted in an unqualified opinion.

Section I - Summary of Auditor's Reportsa. Report on Internal Control and Compliance Material to the Financial Statements

Internal Control:Material Weakness fxlYES [Z|NO

Reportable Conditions £jYES |x]NO

Compliance:Compliance Material to Financial Statements [XjYES | [NO

b. Federal AwardsThe auditor has determined that there were no federal awards received bythe District therefore this section is not applicable.Internal Control:

Material Weakness F^YES NO

Reportable Conditions MYES LJNOBif] Qualifiedf!r| I Adverse FJ

Type of Opinion on Compliance UnqualifiedF] Qualified!for Major Programs: Disclaimer!

Are their findings required to be reported in accordance with Circular A-133, Section .510(a)?

DYES PINO•̂•Jc. Identification of Major Program:

CFDA Number (s) Name of Federal Program (or Cluster)The auditor has determined that there were no federal awards received by the Districttherefore this section is not applicable.

25

Consolidated Gravity Drainage District No. 2 of the Parish of St. MaryState of Louisiana

Schedule of Findings and Questioned CostsFor The Year Ended September 30, 2006

Section II - Financial Statement Findings

2006-1: Material Weakness - Segregation of DutiesOur examination disclosed that there is very little segregation of duties among theDistrict's accounting functions, particularly in the areas of cash disbursements, cashreceipts, bank reconciliations, general ledger and journal entries. This weakness isdue to the fact that the District employs only one person to attend to the variousaccounting functions. Due to the lack of segregation of duties, possible errors orirregularities could occur in the accounting records and not be detected timely.

We recommend the District continue to follow our prior year suggestions to compensate for thelack of segregation of duties within the District's accounting function which are as follows:

1) Board approval for all invoices before the invoice is paid.2) Require signatures of two approved Board members on each check to be written.3) Have the monthly bank statement mailed directly to a Board member each month. This

member could prepare the monthly bank reconciliation or at least do a review of checksclearing the bank statement. This review would include comparing the information oneach cancelled check to the check register maintained by the bookkeeper, verifyingpayments were made to authorized vendors, and verifying approved signatures.

4) On a monthly basis the Board should review the cash disbursements journal foragreement to the check register and cancelled checks.

5) On a monthly basis the Board should review the general ledger and journal entries toascertain if the recorded transactions were consistent with those previously approvedby the Board.

6) The Board should review bank statements and journals to verify that tax collectionsare deposited timely and to agree to the remittance stub information received from thesheriff. Also, verify that property taxes have been correctly allocated between thegeneral fund and the debt service fund.

This list is not intended to be all inclusive of procedures that could be instituted to strengtheninternal controls but to provide suggestions that the Board may consider to better monitor itsaccounting functions.

26

Consolidated Gravity Drainage District No. 2 of the Parish of St. MaryState of Louisiana

Schedule of Findings and Questioned Costs(Continued)

For The Year Ended September 30,2006

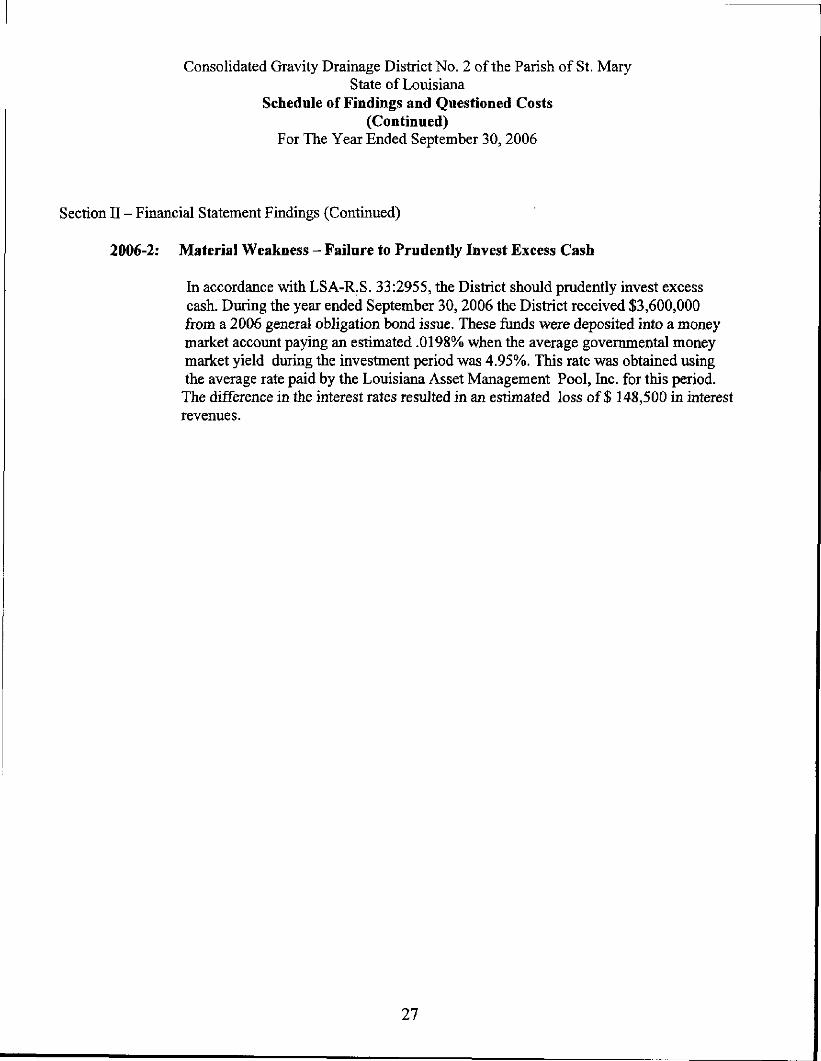

Section II - Financial Statement Findings (Continued)

2006-2: Material Weakness - Failure to Prudently Invest Excess Cash

In accordance with LSA-R.S. 33:2955, the District should prudently invest excesscash. During the year ended September 30, 2006 the District received $3,600,000from a 2006 general obligation bond issue. These funds were deposited into a moneymarket account paying an estimated .0198% when the average governmental moneymarket yield during the investment period was 4.95%. This rate was obtained usingthe average rate paid by the Louisiana Asset Management Pool, Inc. for this period.The difference in the interest rates resulted in an estimated loss of $ 148,500 in interestrevenues.

27

Consolidated Gravity Drainage District No. 2 of the Parish of St. MaryState of Louisiana

Status of Prior Audit FindingsFor The Year Ended September 30, 2005

A. Summary of Prior Year Findings:

05-01 Finding:

Lack of segregation of duties.

Status:

This finding still exists. See 06-01 on the schedule of the current year findings andquestioned costs.

05-02 Finding:

The Consolidated Gravity Drainage District No. 2 did not prepare and adopt an amendedbudget for the September 30, 2006, year-end after notification that a five percent variancehad occurred.

Status:

During the current year the District complied with the budget law requirements.

05-03 Finding:

Missing Invoices.

Status:

In the current year there was no findings of missing invoices.

28

Consolidated Gravity Drainage District No. 2 of the Parish of St. Mary

State of LouisianaCorrective Action Plan

For The Year Ended September 30, 2006

ReferenceNumber Description of Finding

Corrective ActionPlanned

Name(s) ofContact

Person(s)Anticipated

Completion Date

Section I - Internal Control and Compliance Material to the Financial Statements:

2006-1 Segregation of Duties (See Response) Carl Kraemer Continue Monitoring

Corrective Action Plan

The Board of Commissioners has provided the following response and corrective action planto the segregation of duties finding. The Board has identified the following compensatingcontrols that are in effect. The Board has always reviewed and approved invoices prior topayment or any other cash disbursements to be made. The Board has always required dualsignatures of approved members on any checks to be written. The Board reviews the bankbalances at the monthly meetings. The Board has changed the monthly bank statement mailing ancreconciliation procedures. The statements are mailed to and reviewed by a board member each moiDue to the limited number of accounting personnel, the most ideal system of internal control maynot be practicable. Also, the cost of additional employees might exceed any benefits gained. TheBoard acknowledges the loss of internal control that results with their limited staff and areconstantly monitoring for any problems or irregularities.

Section II - Internal Control and Compliance Material to Federal Awards:

The auditor has determined that there were no federal awardsreceived by the District, therefore this section is not applicable.

Section III - Management Letter:

Suggestion2006-02

Failure to prudentlyinvest excess cash

(See Response) Carl Kraemer Continue Monitoring

Corrective Action PlanResponse: The Board informed the bank to invest the bond proceeds into a money market account

and assumed the bank would pay them the bank's prevailing money market rate on thisaccount. Instead the bank put the money into a yield restricted account earning .0198%when the bank's average rate for the year for a governmental account was estimated at3.85%. The board is currently in negotiations with the bank in an effort to recoup thedifference between what the yield restricted account earned and the amount that wouldhave been earned based on the bank's average yield on governmental money marketaccounts. The Board will closely monitor all investment accounts at their monthlymeetings.

29