1ENT SCIENCE - ir.unilag.edu.ng

18

Transcript of 1ENT SCIENCE - ir.unilag.edu.ng

IVIERNATIO AL JOURNAL OF MANAGEl\1ENT SCIENCE(IJO 1AS)

VOLUME 2 2012 NUl\1BER 1&2

EDITORIAL BOARDChief Editor

Professor B.E.E. Oghojafor (Ass. Prof)University of LagosLagos State, Nigeria

Professor linus OsuagwuLagos State University,

Lagos State, Nigeria.

Prince Umor C. Agundu (Ph. D)Rivers State University of Science and Tech.

PortHarcourt, Nigeria

Professor Nathaniel Ozigbo Dr. c.c. OkekeUniversity of Abuja Federal Polytechnic OkoAbuja Nigeria Anambra State, Nigeria

Professor A.S. OgunsijiLadoke Akintola University Of Tech.

Ogbomoso, Oyo State, Nigeria

AIMS AND SCOPESInternational Journal of Management Science (IJOMAS) is published bi-annually by IndustrialScience Centre ( ISC). The Journal deals with emerging contemporary principles and practices ofenvironment, business, management, and development strategies. It is a multi-disciplinaryjournal, global in context, expository in approach and policy driven in orientation.

The journal fosters exchange of new ideas between scholars, professionals, academics, investor:policy formulators, government officials and researchers.

The opinions, statements as well as interpretations expressed in this journal are those of theindividual authors, they do not represent the views of industrial Science Centre (ISC) or of itsdirectors, editors. Publishers, workers and agents Copying of articles is not permitted except forpersonal and internal use, to the extent permitted by national copyright law, or under the of alicence issued by the National Reproduction Rights Organisation.

lndustrial Science Centre (ISC) does not guarantee the accuracy of data included in thispublication and assumes no responsibility or liability for any damage or injury to persons orproperty arising out of the use of any materials, instructions, methods, data or ideas containedherein. Hence, Industrial Science Centre (ISe) or its directors, Editor-In-Chief, editors, publisherworkers and agents cannot accept any responsibility for views expressed in this journal or in arof it, special publications.

Cc1n'.ri1wt ion« to this Journal are welcome. They may be drawn from theory and practice. Theymay however be edited for reasons of space or clarity. Contributcrc must coroplv with guidclirpi ovided at the inside back cover on strict buses.

EXCHANGE RATE VOLATILITY AND ECONOMIC GROWTH IN NIGERIABY

DR.J.E. EZIKE&

AJAYI, L.B.ABSTRACTConsequent upon the simultaneous collapse of the Bretton wood system andthe adoption of the flexible exchange rate system in many countries, economistand policy maker are concerned about the effect of exchange rate volatility onthe economy in general. However, theoretical, and empirical work on the subjecthas produced mixed results. This study investigate the likely impact ofexchange rate volatility on Nigeria economy using Generalized Method ofMoment analysis and GARCH and ARCH modeling with annual time seriescovering the period between 1980 to 2009. Interesting result was found,exchange rate was found to have a negative and significant effect on Nigeriaeconomy. It was also discovered that exchange rate generated via GARCH wasvolatile during the period studied. Based on this, it is instructive, therefore, that acoordinated monetary and fiscal policy should be put. in place 10checkmate thefluctuation of exchange rate so as to bring rapid development to Nigeriaeconomy.Keywords: Exchange rate volatility; Economic Growth; General method ofMoment; Autoregressive Conditional Heteroscedasticity; GeneraliseAutoregressive Heteroscedasticity.

1. INTRODUCTIONThe exchange rate is the price of one currency in terms of another

currency and it is the number of units of a currency required to buy anothercurrency. Exchange rate plays increasingly significant roles in an economy as itdirectly affect domestic price level, profitability of trade goods investmentdecision. Like other economic variable which include interest rate, inflation rate,unemployment rate, money supply etc exchange rate is a strong indicator forassessing the performance of an economy. It is one of the macro-economicvariables that reflects the strength or weakness of an economy and movementin exchange rate are known to have ripple effect in other economic variables

Volatility means fluctuation, therefore, volatility in exchange rate impliesinstability in exchange rates and the problems of exchange rate volatilitybecome too disturbing after the emergence of the generalized floating ratesystem in the early 1970s. most highly industrialized countries then began towitness volatile movement which is called strong currencies, as well as lessdeveloped countries(LDCS) this undesirable experience sparked off theemergence of serious theoretical and empirical studies in the problems ofexchange rate volatility that dominated the literature. In the 1970::; c;nd:980.it hasbeen established in literature that "getting the exchange rate right "ormaintaining relative stability is critical for both internal and external balance and

202

Or. J.E. Eezike & Ajayi L.B.

hence growth on an economy. Failure to properly manage the exchange rateinduces distortions in consumption and production patterns Excessive volatilityin exchange rate creates uncertainty and risks for economic agent withdestabilizing effect.

Exchange rate is a key price variable in an economy that perform dual roleof maintaining international competitiveness and serving as nominal anchor fordomestic prices. Since the collapse of the generalized fixed exchange rateregime and the adoption of a generalized floating system by the industrializedcountries in 1973. most countries including Nigeria, have experimented withvarious types of exchange rate arrangement ranging from the peg system toweighted currency basket to managed floating and more recently to themonetary zone arrangement. The modern view of exchange rate determinationsargues that the exchange rate has been a relative price of this nation. Moniesand that it is determined primarily by the relative supplies and demands forthese monies. The approach is also referred asset market approach to thedetermination of exchange rate since the demand for the various nation moniesdepends on expectation income and rate of return and other factors relevant forportfolio choice. The naira exchange rate as shed us initial overvaluation. Theovervaluation of the naira exchange rate during the oil boom had a significantimpact on the Nigeria economy. It cheapened import and stunted the growth ofnon- oil exports with consequent for the balance of payment of domestic front. Itplaced on agricultural product and other exports as an uncompetitive in theworld market.

Over the year before, during and after the introduction of SAP, the flow offoreign exchange has faced several bottlenecks whether in the form of reducedinflow and distortion in the allocation of foreign exchange. In searching for arealistic foreign exchange rate, Nigeria adopted the floating exchange rate in1986. A realistic foreign exchange rate is however achieved the objective ofinternal and external balance without the imposition of traded exchange control.Internal balance is achieved (when a non-inflation rate of economic growth isachieved, low inflation and high sustainable rate of economic growth) whileexternal balance assumed the attainments of a realistic exchange rate thatpromote external sector competitiveness and balance of payment stability. Theexchange rate policy before structural adjustment program (SAP) were toequilibrate the balance of payment, preserve the value of the external reserveand maintain a stable naira exchange rate, however, up to the time of SAP,Nigeria's exchange rate appreciate by an average of 7.3% (Obadan 1997) .During the period of structural adjustment program (SAP) exchange rate policywere pursued within the institutional tramework of second-lie!" foreign exchanqemarket (SFEM) which was established in September 1986. The market latermetamorphosed in to the foreign exchange market (IFEM). In this direction,SFEM was predicted on the attainment of a realistic exchange rate of the nairathrough the market force of supply and demand for foreign exchange. It was

203

International Journal of Management SCiences Vol 5, No 1 June 2012

then expected -that a realistic exchange rate should excessive demand forforeign exchange expected for important of finished goods and services as welleliminated prevailing distortion in the economy and stimulate non- oil exports.

A look at foreign exchange management in the past ten years suggeststhat something has apparently been wrong with the management policy(Obadan 1993). Not did the search for a realistic exchange rate was persistentlyunstable and speculative demands for foreign exchange transaction have beenfactors causing exchange rate instability. The export based has remained verynarrow while export. Receipts have remained low commodity prices. Theperformance of the non-oil export sectors has been abysmal in term of foreignexchange earning. The overall balance of payment position has also beenweek, while a large proportion of foreign exchange earning is still devoted todept services payment. Due to the neglect in the agricultural sectors,agricultural commodities have been downwards, the naira price has generallymoved upwards due to the depreciation of the naira, liberal export policy. Theincrease in commodity price resulted in improved nominal of producers. Butwhether or not real income increased in the face of escalating inflation isanother issue, unlike the positive effect on government revenue and producerprice. Exchange rate policy has not had the expected impact on the balance ofpayment in term of enhanced non oil export earning, capital flow and reducedcapital outflow and import. Also the objective of structural to the information ofthe economy remains largely unfulfilled.

It is against these background that this study is set to examine the impactof exchange rate volatility on the growth of Nigeria economy and specifically toinvestigate; the effect of exchange rate on gross domestic product, the impact offoreign investment on the Nigeria real gross domestic product and the empiricalrelationship between term of trade and Nigeria economic growth.

Due 10 the nature of the research, the period of analysis shall cover 1980-2009 this will enable us to analyze the pre - SAP and post SAP era. This is dueto the fundamental macro-economic policy reform brought about by SAP. Apartfrom the introductory part, the rest of the paper are organize as follows; reviewof relevant theoretical framework and literature are contained in part two, partthree contains the methodology, while part four identify data and sources andthe analysis and interpretation of result, pan live gives the summary, conclusionand recommendations.

2. LITERATURE REVIEW AND THEORETICAL FRAMEWORK LiteratureReview

Since the evolution of the international monetary system into the floatingexchange rate, there has been increase interest on issue relating to exchangerate. This has led to new and rapid development in theoretical and empiricalanalysis of exchange rate. A lot of writers have discovered that volatility inexchange rate in most economy of the world tend to be as a result of float and

204

Dr. J.E. Eezike & Ajayi L.B

performances of other economic factors (Ogundipe 1987). In the literature,many factors are usually specified as influencing the real exchange rate, theseinclude different in inflation rate, interest rate, growth in national incomebetween one country and another as well as incident of speculation. Otherfactors are; integrated flow model, monetary model and portfolio balance model,contrary to expected feature of stability. One striking feature of the recentfloating period has been the volatility of bilateral exchange rate.

Volatility in this sense refers to the short term fluctuations of nominal andreal exchange rate (Frenkel and Goldstein 1998) with effect from 1973, mostindustrialized countries and some LOCs began to witness volatile movement intheir major currencies (Berian 1985). For instance, Mckinnon (1976) observedduring the early part of the floating period thus, current movement of sport ofexchange rate of 20% quarter to quarter, 5% week to week or even 1% in anhour to hour basis are not unusual, although they are very unusual by historicalstandard. Frenkel and Goldstein (1999) have also show that the short termbehaviors of major currencies exchange rates over the 1973- 1988 period couldbe characterized by the following features; one, exchange rate volatility duringthe present floating rate regime has been far greater than that of the fixedBreton woods system, perhaps five times as greater. Another one is that shortterm exchange rate variability has been significantly greater than the variabilityof natural price levels, resulting in substantial deviation from PPP. The thirdfeature is that there has not been a tendency for the short run variability ofexchange rate to decline over time.

Exchange rate is the price in the economy that influences all areas ofeconomic activities. Valdan 1986), Ishibaka (1986), calvadd and minndiak(1982)claimed that some economic policies on domestic agricultural could occurthrough their effects and the real exchange rate and this could in turn influenceagricultural output, Fleming (1974) stressed that the role of exchange ratemanagement policies in influencing the structure, pattern and direction of growthof an economy. He buttressed this point by his argument that exchange rateeffect capital movement inwardly and outwardly via two mechanisms.

i. A change in the actual rate associated with corresponding change in theexpected future rate resulting in a proportionate change in the yield ofdomestic capital invested in a country,

ii. A change in the actual rate unaccompanied by a corresponding changein the expected future rate.

The introduction of the structural adjustment programmed in many of thesecountries and the attendants liberalization of exchange rate have further broughtthe discussion of this issue into sharp focus. A review of exchange rate showsthat the issue is far from settled though not all studies are fully comparable forexample, Lastrapes and Karany (1990), Cusman(1988), Caballero and Carbo(1989) indicated a significant depressive effect of exchange risk. IMF (1981),Gotour (1988) and chambers (1991), however maintained a contrary view. Abel

205

International Journal of Management SCiences Vol 5, No 1 June 2012

(1983) also showed that if one ·assumed perfect competition convex andsymmetric cost of adjusting capital and risk mentality, investment is a directfunction of exchange rate uncertainty. Maskus (1999) by comparing the effectsof exchange rate across major sections oi'the economy e.g. manufacturingagriculture, chemical, industrial e.t.c provided a link between his study andprevious work. He found aggregate bilateral agricultural trade (Us and the majorwestern trading patterns to be particularly sensitive to exchange rate).Theoretical FrameworkBalance of Payment Theory. Under free exchange rates, the exchange rate ofthe currency of a country depends upon its balance of payments. A favourablebalance of payments raises the exchange rate, This theory implies that theexchange rate is determined by the demand for and supply of foreign exchange

r.F.

b ROR a

0

U

Fig.1. The determination of exchange rate under the balance of payments theory

The purchasing power parity theory states that equilibrium exchange ratebetween two inconvertible papers currencies is determined by the equality oftheir purchasing power. In other words, the rate of exchange between twocountries is determined by their relative price levels. According to the theory,exchange rate between two countries is determined at a point, which expressesthe equality between the respective purchasing power of the two currencies.This is the purchasing power of the two currencies. R = Domestic price of aforeign x domestic price index

206

Or. J.E. Eezike & Ajayi L.B ..

R = DOIl1I!~ll\:pril:t: of a foreign :-..dOIOc'sli•.: pr~ce indc>.. #

Foreign price index

t,

D

Commodity exportpoint

Commodityrmponpoint

fig 2. The Plln:ha~iJ)g Power Parit) Curve

The traditional flow model sees exchange rate as the product of interactionbetween the demand for and the supply of foreign exchange (Sulaiman (2008).The theory relies on the equilibrium in the foreign exchange market as thedetermining factor of the appropriate exchange rate.The portfolio balance approach conceptualized the exchange rate as the resultof the substitution between money and financial assets in the domesticeconomy and the assets (Sulaiman 2006). This model holds that the portfolioequilibrium of wealth holders in each country simultaneously determines theexchange and interest rate.The short fails of the initial two approach which include the over shooting of theexchange rate target and the Tact that the substitutability between money andfinancial assets may not be automatic, led to the development of monetaryapproach. This approach which is predicted on the important of money seesexchange rate as a function of a relative shifts in money, stock, inflation rate orit proxy and domestic output between an economy and trading partner(Sulaiman 2006).

Concept of Exchange RateThe concept of exchange rate has three important connotations in the literaturethese are: Nominal exchange rate, Real exchange rate and Effective exchangerate. Exchange rate mechanism or regimes are different system of determiningthe exchange rate of a nation currency in terms of other currencies. The variousregimes or system of exchange rate determination permit the two extremes offree floating and rigid fixed exchange rate mechanism since there are strictly infree floating and rigidly fixed systems in the real sense, there abound in real lifevariant of the two extreme. These variance otherwise referred to as hybridsystem combine element of the extremes, this we have the mange float,crawlino and adjustable pegs arnonq ()th8r~. The exchanqe rate system

207

International Journal of Management SCiences Vol 5, No 1 June 2012

adopted at any point in time reflects the stance of exchange rate policy whichthe authorities intend to excite and operates.

Exchange Rate Policy in NigeriaExcept for the brief period of confusion in exchange rate policy formulated InNigeria (1972-1974) four different exchange rate regimes were noticeableovertime. Era of fixed exchange rate, the fixed exchange rate is the one that hasthe following features: it guarantees stability and precision in decision making, itis more dependent on stable macro-economic policies than on the form ofexchange rate regimes in places and it is potentially susceptible to absorption ofexternal shocks. The era of adjusted peg and managed float; this is acombination of the element of fixed and flexible exchange rate. The internationalmonetary found (IMF) started advocating for a system of managed floating in1974 and by 1976, the system was legalized at the IMF meeting held inJamaica The era of flexible exchange rate; up to the time of SAP, it appearedthat Nigeria exchange rate policy failed to encourage over valuation of the nairaand this in turn encouraged import, discourage non oil export and helped themanufacturing sectors over dependent on imported input.

3. METHODOLOGYThis section presents the methodology and the analytical framework adopted inanalyzing the impact of exchange rate volatility on economic growth in Nigeria.The model for the study takes from the existing in the literature such as Sarkerand Amor (2009), in an effort to establish a relationship between exchange ratevolatility and economic growth in Nigeria. The growth equation is thereforestated as follows:RGDP = f(REXR, INF, FDL TOT) (1)This can be written in estimation form as:RGDP=BO+BIREXR+B2INF+B3FDI+$4TOT+ (2)Where:RGDP = Real Gross Domestic ProductREXR = Real Exchange RateINF=lnflation RateFDI= Foreign Direct Investment.TOT = Term of TradeBO - B4 = Slope coefficientso = Error term.

Estimation techniqueThe empirical analysis adopted the use of Generalized Method of Moment

(GMM). The GMM is used for the purposed of established the relationshipbetween the dependent and explanatory variables and to determined thestatistical significant of all the parameter 11~l?tj. .A.C'':():':!i~g tc /\~c;::a'li0 dllU Bond

208

Dr. J.E. Eezike & Ajayi L.B.

(1991), this method allows tor resolving problems of simultaneous bias,causality inverse, and omitted variable,The following are the expected relationships which are expected to existbetween the dependent variable and other explanatory variablesRGDP = F (REXR); F' (REXR) < 0This implies that a negative relationship is expected to exist between realexchange rate and real gross domestic product in NigeriaRGDP = F (INF); F' (INF) <0This implies that a negative relationship is expected to exist between inflationrate and real gross domestic product in NigeriaRGDi' F(FD1 );F'(FD1»0This implies that there is a positive relationship between foreign directinvestment and real gross domestic productRGDP - F (TOT); F (TOT) > 0This also implies that there is a positive relationship between term of trade andreal gross domestic product Analysis of the

Degree of Exchange rate Volatility,In this section, Autoregressive conditional Heteroscedasticity (ARCH) andGeneralized Autoregressive conditional Heteroscedasticity (GARCH), that isARCH and GARCH (1,1) model is used to estimate the degree of exchange ratevolatility in Nigeria, where the two terms in parenthesis refer to the first-order ofGARCH term and the first-order of ARCH term respectively, the model can bestated as:52t-1= X + a 21_1+ pS21 -1Where:5~ = conditional variance a, -constant term2t_1= the arch term -news about volatility from previous period measured as thelog of squared residual from the mean equation S2t_l= the ARCH term-the lastperiod forecast variationAccording to Yinusa (2004), the role of thumb for determine the presence ofvolatility i.e. that, we find the sum of the root of the autoregressive model.In this case,If a + B < 0.5, there is no volatilityIf a + B-> I, there is volatilityIf a + B>I this is a case of overshooting

The evaluation procedure is considered under the following three criteriavis-a-vis the economic criterion, the statistic criterion and the econometriccriterion. The economic criterion will test the plausibility of the signs andmagnitude of the regression parameters, The statistical criterion will involves theanalysis of the R2 the t-test and f- test and The econometric criteria will employthe use of Durbin Watson test to detect the presence of autocorrelation in themodel.

209

International Journal of Management Sciences Vol 5, No 1 June 2012

4. PRESENTATION AND ANALYSIS OF THE RESULTThis section presents the analysis and discussion of empirical results, based onthe collected data and in line with the methodology specified in the previouschapter of this study. The analysis started by examine the relationship betweenthe dependent variable and the explanatory variables using the Generalizedmethod of moment (GMM) after which the test for exchange rate volatility wascarried out using Autoregressive Conditional Heteroscedasticity (ARCH) andGeneralizedAutoregressive Heteroscedasticity (GARCH) model.

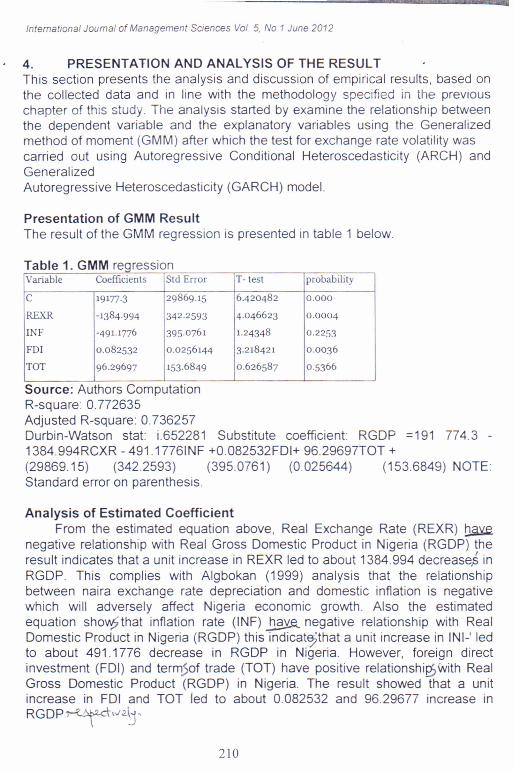

Presentation of GMM ResultThe result of the GMM regression is presented in table 1 below.

T bl 1 GMMa e regressionVariable Coefficients Std Error T- test probability

C 19177·3 29869.15 6-420482 0.000

REXR -1384.994 342.2593 4.046623 0.0004

INF -491.1776 395·0761 1.24348 0.2253

FDI 0.082532 0.0256144 3.218421 0.0036

TOT 96.29697 153.6849 0.626587 0.5366

Source: Authors ComputationR-square 0.772635Adjusted R-square: 0.736257Durbin-Watson stat: i.652281 Substitute coefficient: RGDP =191 774.3 -1384.994RCXR - 491.1776INF +0.082532FDI+ 96.29697TOT +(29869.15) (342.2593) (395.0761) (0.025644) (153.6849) NOTE:Standard error on parenthesis.

Analysis of Estimated CoefficientFrom the estimated equation above, Real Exchange Rate (REXR) ~

negative relationship with Real Gross Domestic Product in Nigeria (RGDP) theresult indicates that a unit increase in REXR led to about 1384. 994 decreases inRGDP. This complies with Algbokan (1999) analysis that the relationshipbetween naira exchange rate depreciation and domestic inflation is negativewhich will adversely affect Nigeria economic growth. Also the estimatedequation sho~that inflation rate (INF) ~ negative relationship with RealDomestic Product in Nigeria (RGDP) this indicat~that a unit increase in INI-' ledto about 491.1776 decrease in RGDP in Nigeria. However, foreign directinvestment (FDI) and term50f trade (TOT) have positive relationshipywith RealGross Domestic Product (RGDP) in Nigeria. The result showed that a unitincrease in FDI and TOT fed to about 0.082532 and 96.29677 increase inRGDP~l,2.c\-l"~'

210

Dr. J.E. Eezike & Ajayi LB.

The R2 - squared of about 0.772635 implies that about 77% of the total variationin RGDP is being explained by the explanatory variables in the model. Thisconfirms the goodness of fit of themodel. The standard error test is used to test for the statistical significance ofindividual estimated parameters since the number of observation is up to thirty(i.e., n = 30)The hypothesis of the study is stated as follows:Ho: a -0 (not significant).HI: = en = (significant) Decision rules.Reject Ho, if 11/2xl > standard error.Accept H 1, if /1/2x/ < standard error.

The result of the Standard Error Test is presented in table 4.2 below. Table 2.Standard Error TestVariable Coefficient(a) /l/2X/ Std Error Remark

REXRINF -1384·994 - 692.497 342.2593 Significant Not

491.1776 245·5888 395·6761 Significant

FDI 0.082532 0.041266 0.025644 Significant

TOT 96.29677 48.148485 153·6349 Not Significant

Source: Authors computationThe statistic is used in this case to test for the overall significant of the

model based on the generalized method of moment (OMM) technique adciPted.The y-statistic gave a value of 0.008697 which is relatively less than 1%

and 5% level of significance. It can therefore be conclud~{that the model isoverall significant. He Hansen y - statistic confirmed the validity of theinstrument.

The Dirbin - Watson (D.W) statistic gave a coefficient value of 1,65228,which implies.J!Jjnconclusive evidence of autocorrelation in the model thishowever J.rJ.one of the shortcoming of Durbin - Watson test. Test of ExchangeRate VolatilityThis study went further to determine the degree of exchange rate volatility andthe result is presented in~ appendix.In the previous section, we established that the degree of exchange ratevolatility through the sum of the roots of the autoregressive model, ARCH (1)and GARCH (1) from the result, the model can be expressed thus:52t = 270000000 +0.860413 2t_1- 0.106097521 -1 Where a = 0.86041313 = - 0.106097 a + (3= 0.860413 + (-0.106097) = 0.754316The sum of the root of the above equation is 0.754316. Following the rule ofthumb that says:If a + 13 < 0.5 there is no volatilityIf a + (3-1. There is volatility

211

Intemational Journal of Management SCiences Vol. 5, No 1 June 2012

If a + 13> 1 , There is a case of over shooting.From the above result, the sum is greater than 05 and tends towards one, thisimplies that there is volatility. The volatiiity of exchange rate in Nigeria is anindication of poor macro-economic management Discussion and PolicyImplication of FindingsThis study has examined the impact of exchange rate volatility on the Nigeriaeconomy. The analysis started by examining the relationship between thevariable and explanatory variables in the model using the Generalized methodof moment (GMM) technique from the result of GMM, several interestingconclusion were drawn. Real exchange rate (REXR) was found to have anegative significant relationship with Real Gross Domestic Product (RGDP).This result conform to a priori expectation this result implies that depreciation ofexchange rate dampens growth in Nigeria. This result corroborate with the workof Aliyu (2009). The negatively of exchange rate is an indication of highexchange rate of Naira to other foreign currencies (in this case, U,S dollar) inthe international market couple with this fact is the volatile nature of exchangerate in Nigeria. Similarly, inflation rate (INF) has a negative but insignificantrelationship with the growth of Nigeria economy, this result conforms to a priorexpectation. The high inflation rate discourages foreign investor, bring down thevalue of Nigeria currency and lead to unfavorable balance of payment. All thesehave bad effect on Nigeria economy. Also, high rate of inflation often lead tohigh cost of factor input in the Nigeria manufacturing industries andconsequently lead to low industrial output. However, foreign direct investment(FDI) was found to have positive and significant relationship with the growth ofNigeria economy this result conforms to a priori expectation. This result can beattributed to the recent effort of the Nigeria Government to woo investors to thecountry. Another reason that can be attributed to this effect is the liberalizationof the Nigeria economy.Term of trade (TOT) also has a positive insignificant relation with economicgrowth in Nigeria. This result conforms to prior expectation. This result impliesthat the volume of Nigeria export exceeded the total imports within the period ofthe study. This may be as a result of various policies of the Nigeria Government,such as export promotion strategy and import substitutionstrategy. Though most of Nigeria export comes from oil sector of the economy,The insignificant of the result can be as a result of the fact that Nigeria exportbasically primary product whose price are elastic in the international market andconsequently, whose product are vulnerable to ail manners of intimidation andfrustration in the international market.The analysis of the exchange rate volatility revealed the existence of exchangerate volatility in inc Nigeria economy. Exchange rate volatility raises twoconcerns: One, exchange rate volatility makes the plan and prediction of theeconomic variable difficult, consequently, volatility hinder growth through itadvert pffl'>,t ("In i~'.'C:;t:T.Gr.~3~ a rC:~U;l UI the uncertainty it inflict on theinvestment environment. Two, unguided exchange rate volatility like the. one we

212

Or. J.E. Eezike & Ajayi l.B.

observed in Nigeria in' this study is an indication of improper management of theeconomy Volatility is inherent in exchange rate due to the fact that theexchange rat is not determine within the domestic economy, rather domesticforce of the economy interact with international economic force to determine theexchange rate. In order word, the forces responsible for the frequent change inthe exchange rate are partly internal and partly external.The exchange rate management has implication for balance of payment ability,external debt management, inflation, productivity, consumption, investment andthe general welfare of the economy. So there is need for the stability of theexchange rate, since a stable exchange rate will lead to a viable balance ofpayment position and the macro economic stability that will spur investment andgrowth.5. SUMMARY, CONCLUSIONS, AND RECOMMENDATIONSThis work examined the impact of exchange rate volatility on economic growthin Nigeria between 1980- 2009, using Generalized Method of Moment (GMM)analysis with annual time series, it examine the exchange rate volatility theimpact it plays in the development of Nigeria economy. The study usedAutoregressive conditional Heteroscedasticity (ARCH) and GeneralizedAutoregressive Conditional Heteroscedasticity (GARCH) analysis to estimatethe degree of volatility in Nigeria exchange rate. The study reviews theexchange rate management and polic> in Nigeria during the SAP, PRE- SAPand POST-SAP era. Attention was also paid to review the basic modelapproaches to exchange rate determination which happens to be vital areas offoreign exchange management. Real exchange rate (REXR) was found to havea negative Significant relationship with Real Gross Domestic Product (RGDP).This result conform to a priori expectation this result implies that depreciation ofexchange rate dampens growth in Nigeria. This result corroborate with the workof Aliyu (2009). The negatively of exchange rate is an indication of highexchange rate of Naira to other foreign currencies(in this case, U.S dollar) in the international market couple with this fact is thevolatile nature of exchange rate in NigeriaThe Nigeria economy has been faced with problems that are peculiar to thecountry. The value of the naira has been on the downward trend in the foreignexchange market in recent years. The Naira value had depreciated to as low as148.30 to a Dollar for the official rate and 151.70 at the parallel market which iscausing some stir in the financial circle. The state of the Naira is a reflection ofstate of affairs in the economy. The value of the nation's currency (#) is not justan economic indicators, it is a status symbol of the nation and a measure of herdignity and status. The British, in spite of the economic benefit of a singleEuropean currency was unwilling to give up the pound for the euro. One of thefactors that counted as the problem militating against economic developmentwas the instability of the naira value. The stability of the exchange rate isimportant in a number of ways. It provides a barometer for measuring theresilience of the economy and the confidence of investors and other people in

213

International Journal of Management Sciences Vof. 5, No 1 June 2012

the economy. It allows certainty gives investors the opportunity to make mediumor long-run investment plan. The naira is under depreciation primarily becausethe economy which the naira supports has a weak productive base Thecapacity of the manufacturing sector has over the years been declining due to acombination of factors. One of the failures of the sector was its inability to showpositive resiiib for the foreign exchange access and import protection supportswhich have not been effective over the years.There is also the unabated decline in the purchasing power of the Nigerianconsumers as a result of mass poverty induced by prolonged inflation andunemployment. It has been observed that the achievement of the real-sectorhas been hampered largely by low level investment and the decay ofinfrastructural facilities has had negative cost implication for the productivesector, social unrest and improper implementation of government policies. Theeconomy is characterized by low productive capacity and high dependent onimports virtually every item of daily of Nigerian households, firms and industrieswere imported. Government is not doing much to encourage the productivesector. Most of the industrial establishments are either dead or operating atlevels that are unprofitable.It is good to point out that the cost of running the country remains a big drain onpublic treasury. Money spent that could otherwise be expended into productionis spent on grandiose ritual by government official who are supposed to addressthe problems of unemployed youths who ought to be in factories instead ofhawking second hand goods and other imported junk items. The sharp declinein the value of the nation's currency is also attributed to the mounting tensionand rising crime wave in the country, which is scaring away prospective investorand also fuelled an increase demand for foreign exchange by investors insearch of stable markets.Base on the finding of this study, some fact have shown which ought to beadhere to from the analysis need some policies recommendation, theserecommendation are stated bellow:In order to enhance the exchange rate stability, the authority should efficientlymanage the foreign exchange market through appropriate monitoring of theoperation of the authorized dealer as well as the use to which foreign exchangeare put when they are purchased.The need for local sourcing of raw materials and input through agricultureshould be intensified. A technological policy aimed at developing a localengineering industry is advocated. By so doing, the link between agriculture andthe manufacturing sector will be established, leading to expansion of exportbase which would attract more foreign exchange into the country. This couldculminate into high external reserves build -up and reduce adverse pressure onbalance of payment.Change in exchange rate management strategy should be allowed to run areasonable course of time. Jettisoning strategies at will and on frequent basish?~ i"!:pi!C2ti':':i fer C)(C~3iigc rate and uu"iuu::, consequence for a sector that

214

Or. J.E. Eezike & Ajayi L.B.

depends on foreign inputs. T-he monetary authority (the Central Bank of Nigeria)should monitor the unethical practices of some commercial bank which haveresulted in much fluctuation in the rate of exchange. More stringent punitivemeasures have to be taken against the culprit banks.Banks should take on additional responsibilities; they should ensure that foreignexchange allocated to their customer is used for the purpose they wereintended for. The handling of these monitoring obligations should be one of thecriteria for future participation in the foreign exchange market and also, theinterest rate should be kept on a low rate for it to stimulate economic Ratherthan rely absolute!) on market forces for determining the value of the naira, thenation's policy must become more innovative in their quest makers to theeconomy around. The exchange rate should be regulated, so that the cost ofdoing business should be regulated, so that the cost of doing business shouldbe less prohibitive. However, a good monetary and credit policy should beadopted in the Nigeria economy. A monetary policy should be such way thatprevents high inflation, which is a source of instability which leads to a reductionin investment. A monetary or credit policy should also be designed to bringabout a low but positive real interest rate and exchange rate in the Nigeriaeconomy.Finally, government must also pursue stable credible and stable macroeconomic policies. These should include the adoption of realistic exchange ratepolicies as this will directly affect the price of tradable relative to non tradable,the greater will be the country's ability to import, also revealed by the sign andmagnitude of the coefficient of inflation in the study is negative which exertconsiderably pressure on exchange rate. With low predictable inflation, firmscan plan and invest with the confidence they have a reasonable knowledge ofthe price that they will receive for future output relative to cost.

21)

International Journal of Management SCiences Vol 5. No 1 June 2012

·REFERENCESAlgokhan B.E, Obadan M.I And G,N Osagie (1998), "investment decisionand the effect of exchange rate liberalization in Nigeria", Wise ISSCNNational research Nehvork on liberalization policy in Nigeria. Ajakaye 0.0(1997), "Effect of exchange rate a sectional price" Niser monograph Series.1991AKINNIFESSI E 0 (1981), "The determinant of private foreigninvestment in Nigeria manufacturing industries" CBN Economic and financialreview (June) pg 13 29 Adebiyi M.A (2002), 'The Role of Interest Rate andSavings in Nigeria" Firm Bank of Nigeria PieQuarterly review Vol. 2, Nol, Pp 32-43Adihoya (1998), "Impact of Financial Sector Reform on the Supply of andDemand for Agricultural Credit and Real Sector in Nigeria", First Bank of NigeriaPie, Bi- Annual Review, Vol. 16 Afeikhena Jerome and John Adeyemo (1998),"Exchange Rate and Trade Liberalization Policies andthe Promotion of Manufacturing Export in Nigeria" A Publication of NISERIbadan. Aciene, C.E (1991), Foreign Exchange and International Trade inNigeria. Gene Publication Lagos P.16 Ahmadu Hi and A. 0 Zarma (1997), "The Impact of Parallel Market on theStability of Exchange RateEvidence from Nigeria" NDCI Quarterly, Vol. 17, no 2Allison, A (1987), Refection on Nigeria Development, Adison Publishing Limited,Lagos. Alien P and stain J (1989), Finance and International Economy the RealExchange Can't be Explainedon Basis for Policy. Anyanwu, J.E (1999), Structural Adjustment Programme,Financial Deregulation and FinancialDeepening in Sub-Scheme Africa Economies: The Nigerian Case Vol. 1, no 1.Anyanwu, J.C (1997), Monetary Economic Theory, Policy and InstitutionGabestar EducationalPublisher, IbadanAkinlo, E.A (1996), "Improving the Performance of the Nigerian Manufacturingsub-Sector after Adjustment Selected Issues and Social Proposals"Nigerian Journal of Economics andSocial Studies Vol. 38. pp 91 -111. Akinrimisi (1993), "The Nigerian Real Sectorand its Determinants", Nigeria Journal of Economicsand Social-Sciences, University of Lagos Vol. 8, No 2. Ajayi, S.I (1999), "TheImpact of Parallel Market on the Stability of Exchange rate Evidence fromNigeria" NDCI Quarterly Publication, Vo!. 20Akpakpan (1994). Manufacturing in Structure of the Nigerian Economy. F.AMacmillan Press Limited.Banerjee, A. Dolado, J.J Galbraith J.W and Hendry. D.F (1993). Co-Integration, Error Correctiond(/(j tne econometric Analysis of Non-Stationary Data, Advanced Texts inEconometrics,

216

Dr. J.E. Eezike & Ajayi L.B.

Oxford University Press, London:Central Bank of Nigeria Statistical Bulletin 2004, 2007, Vol. 18 Davidson J.H.D.F SRBA; & S Yoo (1978), "Economic Modeling of the Aggregative TimeSeries"Economic JournalDamodar N, Gujarati, (2007), Basic Econometric, 4th Edition, Delhi India, TataMcGraw Hill Dickey D. A and WA fuller (1981), "Likelihood Ratio Statistics forAuto-regressing Time Series witha Unit Root" Econometrical Vol. 49 No 4 Dun Combe (1992), "Exchange Rateand Economic Growth, an Unpublished Paper Presented to theDepartment of Economics. University oflbadan. Ekong (1994): "Fiscal Incentivesand the Manufacturing Investment in Nigeria''', Selected Papersfor the 1989 Annual Conference FLOOD R P and Rose, AK (1999),"understanding exchange rate volatility without the contrivance ofmacroeconomic''htTp://hass. berkele\. ed u/aroseJohn black (2003), Oxford Dictionary of Economics, Oxford University Press, 2nd

Edition Kane, D.B 0 998), Intermediate Economic Analysis Case Press,Canterbury, London P. 607 Klaus Waiter (1998), "Inefficiencies from FinancialLiberalization in the Absence of Well FunctioningEquity Market", Journal of Money Credit Banking Vol.1 8 N02, Pp 199-201 KeithPibeam (1991), "Equilibrium Interest Rates and Financial Liberation inDeveloping Countries"Development Studies 32, Pp 391-413. Nwankwo (1 987), "Foreign PrivateCapital Flows to Nigeria 1970-1983 "Nigerian Financial ReviewVo1.2, No 4.Obadan, M.I (2003). "Overview of Nigeria's Exchange Rate Policy andManagement since the Structural Adjustment programme", CBN Economic andFinancial Review Vol. 31, No 4. Pp337. Obaseki P. G ( 2002), "ForeignExchange Management in Nigeria Past, Present and Future" CBNEconomic and Financial Review Vol. 29: No tOloyede, B. (1999). Principles of Money and Banking Forthright EducationalPublisher, Nigeria. Olukole R.A (1992), "Exchange Rate Development inNigeria" CBN Bullion Vol. 16, No 1 Oyejide, TA (2005), 'Thought on Stability ofNigeria Exchange Rate" The Nigeria Banker Sept. Dec.Issues. This day, Thursday Aug. 1 2002. Todaro. M.O (1997), Economics for aDeveloping Worfd: An Introduction to Principles, Problems andPolicies for Development Longman Publishers, Singapore Pp. 314-317.

"1'7