16th Annual Budget Forum - Constant...

51

16th Annual Budget Forum Building a Budget for Connecticut's Future

Transcript of 16th Annual Budget Forum - Constant...

16th Annual

Budget Forum

Building a Budget

for Connecticut's

Future

Fiscal Overview

• State of the economy as it relates to children and families

• Investments in children

• General fund and revenue trends

• Looking forward

Investments Contribute to

Quality of Life

9th lowest child poverty rate

6th lowest poverty rate

6th highest median household

income

5th highest share of individuals with

bachelor’s degrees

3rd most productive workforce

#1 rated human development index

American Community Survey, CERC, Measure of America

Disparities Remain – By Race

6%

25%

21%

3%

15%

9%

0%

5%

10%

15%

20%

25%

30%

White Black Latino

Poverty (CT =10.5%) Uninsured (6%)

CT Voices analysis of census data

Disparities Remain – By Place

CT Voices analysis of census data

10.5%

20.6%

14.1% 10.0%

9.3%

28.3%

26.8%

31.5%

27.3%

0%

10%

20%

30%

40%

2007 2014

Share of General Fund Spent

on Children Reaches New Low

32.8%

29.5%

26%

28%

30%

32%

34%

2008 2010 2012 2014 2016

Children’s Budget

CT Voices budget analysis

Children’s Budget Cut by

$82.1 Million

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

K-12 Early Careand Ed

Higher Ed Health andHuman

Services

1.4% cut

1.4% cut

0.01% cut

CT Voices budget analysis

5.2% cut

Spending on children, FY16 and FY17

(millions)

Top 10 Cuts to the Children’s

Budget, FY16 – FY17 Category Program Amount Cut

K-12 Transportation of School Children -$22,336,353

K-12 Education Equalization Grants -$15,666,899

Higher-Ed Connecticut State University -$13,454,053

Higher-Ed University of Connecticut -$9,747,484

Human Services Juvenile Alternative Incarceration -$7,125,349

ECE Birth to Three/Early Intervention -$6,984,070

K-12 Magnet Schools -$5,665,134

Higher-Ed Office of Higher Education -$5,508,226

Human Services Personal Services (DCF) -$4,762,828

K-12 Excess Cost - Student Based -$4,287,828

Spending on Children Shrinking

as a Share of the Economy

2.6%

2.4%

2.2%

2.4%

2.6%

2.8%

3.0%

2008 2010 2012 2014 2016

CT Voices budget analysis. BEA Total Personal Income, 2008 – 2016. 2017 based on OPM estimates.

Spending on children as a share of personal income

Modest General Fund Spending

as a Share of the Economy

8.0%

8.7%

8.2%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2008 2010 2012 2014 2016

General Fund with Federal Medicaid Share

CT Voices budget analysis. BEA Total Personal Income, 2008 – 2016. 2017 based on OPM

General Fund spending as a share of personal income

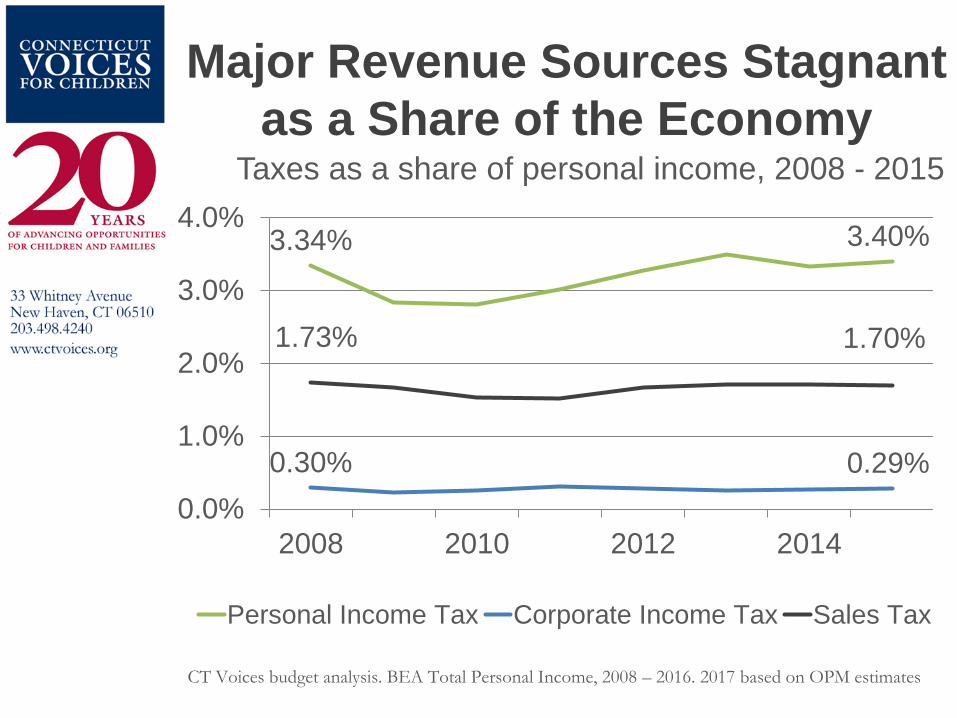

Major Revenue Sources Stagnant

as a Share of the Economy

3.34% 3.40%

0.30% 0.29%

1.73% 1.70%

0.0%

1.0%

2.0%

3.0%

4.0%

2008 2010 2012 2014

Personal Income Tax Corporate Income Tax Sales Tax

CT Voices budget analysis. BEA Total Personal Income, 2008 – 2016. 2017 based on OPM estimates

Taxes as a share of personal income, 2008 - 2015

Fiscal Challenges Ahead

$3 billion biennial budget

deficit

$1.4 billion in 2017-18

$1.6 billion in 2018-19

A Balanced Approach

Address Budget Shortfalls and

Build a Stable Revenue System

• Modernize Outdated Sales Tax

– Could lower rate and still raise $1.18 billion

• Strengthen Corporate Income Tax

– Address growth in business tax breaks and

sophisticated avoidance strategies

• Reform Wealth and Income Taxes

– A half-percentage point increase on top one

percent could raise $238 million

16th Annual

Budget Forum

Building a Budget

for Connecticut's

Future

Equal Funding for Equal

Effort

A Model Reforming Property

Tax Funding for Local

Education in Connecticut

Ray Noonan

Connecticut Voices for Children

Education Finance System

Education Finance

How you RAISE

the money

How you determine if

there’s ADEQUATE

money

How you DISTRIBUTE the money

Education Finance System

Education Finance

How you RAISE

the money

Raising Education Funds in

CT

• Majority of CT education funding

comes from property taxes

• This has four major flaws…

1. Contributes to

Educational Inequities

Source: OPM, Municipal Fiscal Indicators. FY 2014 data.

0

2

4

6

8

10

12

14

16

Canaan Groton

Eq

ua

lize

d M

Ill R

ate

Equalized Mill Rate

Towns that have the same tax rate…

1. Contributes to Educational

Inequities

Source: State Department of Education. 2013-2014 school

year.

…can’t always raise the same amount of money for

education.

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Canaan Groton

Net

Cu

rre

nt

Ex

pe

nd

itu

res

Pe

r P

up

il

Net Current Expenditures Per Pupil

2. Stifles Economic

Development

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Darien Fairfield Bridgeport

Re

al P

rop

ert

y

Share of Exempt Property by Town

Non-Exempt Exempt

Source: Office of Fiscal Analysis FY 15-16 Budget Book.

3. Penalizes Poor Families

Source: DRS Tax Incidence Report. 2011 tax year.

0%

2%

4%

6%

8%

10%

12%

14%

1 2 3 4 5 6 7 8 9 10

Eff

ec

tive

Pro

pe

rty T

ax

Ra

te

Income Decile

Effective Property Tax Rate by Income Decile

4. Exacerbates Racial

Inequalities

Source: Connecticut Data Collaborative and OPM, Municipal

Fiscal Indicators. FY 2014 data.

27.73 26.6

21.82 21.01

0

5

10

15

20

25

30

Black Latino Asian White non-LatinoA

ve

rag

e E

qu

alize

d M

ill R

ate

Race

Average Equalized Mill Rate by Race

What can we do about

this?

The Vermont Model

Equal effort means equal spending

Why This Approach?

1. Learn from lessons of neighboring

state

2. Honor tradition of local control

3. Honor property-tax-based

education funding paradigm

4. Introduce equity into property-tax-

based education funding paradigm

How it Works

Let’s follow Wolcott through this process…

How it Works

1. Wolcott decides to spend $18

million on education from local

property taxes (~$7,000 per pupil after

adjusting for need)

How it Works

2. General Assembly sets three rates:

- Nonresidential tax rate (15.35 mills)

- Residential tax rate (14.03 mills)

How it Works

3. State calculates Wolcott’s residential tax rate based on its per-pupil spending

- More it spends per pupil, the higher its tax rate

- Base per-pupil spending amount = $11,525 per pupil

Wolcott’s residential tax rate would be 14.03 x ($6,981/$11,525) = 8.50 mills.

How it Works

4. Wolcott collects the residential tax +

nonresidential tax and remits it to the

state

Wolcott would collect and remit

$12.4 million in state education taxes.

How it Works

5. The General Assembly gives

Wolcott its $18 million in education

funding plus its $2,000 in statutory

PILOT funds owed

How it Works

State ed. funds

received

$18M

State ed. taxes paid - $12.4M

Net money received + $5.6M

6. Wolcott cuts its local property tax

levy by $5.6M.

The Result

Equal effort means equal spending

Towns that spend the same per-pupil

are taxed at the same rate

What are the Benefits?

PILOT at Current Levels

PILOT at Statutory Levels

PILOT at 100%

Number of people receiving tax cut

2.79 million

2.73 million

2.70 million

Average tax cut

$403 per person

$400 per person

$395 per person

Who Would Benefit? Predicted Property Tax

Changes by Town

Source: Connecticut Voices for Children analysis.

Create Your Own Model

Source: Connecticut Voices for Children Tableau page.

What are the downsides?

• Town-based mill rate not responsive

to individual finances

• Must pair with an income-based

“circuit breaker”

Takeaway

• A Vermont-like model would reduce

disparities and cut taxes

Need Further Research

Education Finance

How you RAISE

the money

How you DISTRIBUTE the money

Whether there’s ADEQUATE

Money

Need Further Research

Education Finance

How you DISTRIBUTE the money

- Funding formula

Whether there’s ADEQUATE

Money

- Adequacy studies

16th Annual

Budget Forum

Building a Budget

for Connecticut's

Future

A Fair Approach at Developing

Connecticut’s Economy

Growth in Business Tax Breaks, FY02 - FY17 (millions)

$0

$100

$200

$300

$400

$500

$600

$700

$800

FY02 FY09 FY12 FY14 FY16

Personal Income Tax Corporate Income Tax

Insurance Premium Single Sales Factor

CT Voices analysis of state budget trends and OFA tax expenditure reports.

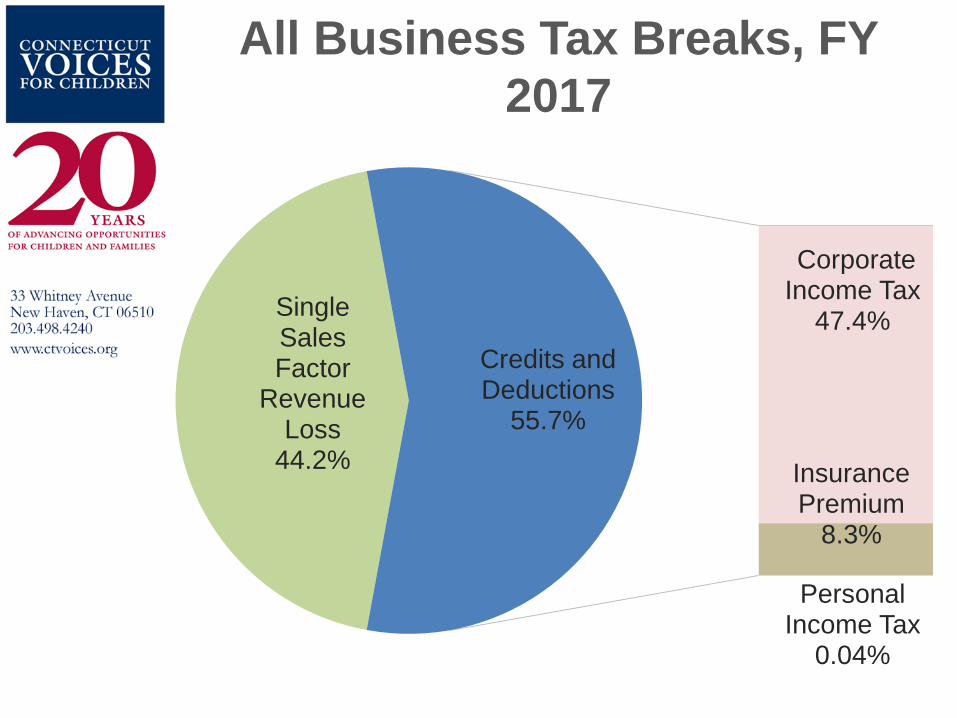

All Business Tax Breaks, FY

2017

Single Sales Factor

Revenue Loss

44.2%

Personal Income Tax

0.04%

Corporate Income Tax

47.4%

Insurance Premium

8.3%

Credits and Deductions

55.7%

Business Tax Breaks Have Grown

Faster Than Spending On Children

-1.27%

3.1%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Children's Budget Business Tax Breaks

Change in Spending, 2016 to 2017

CT Voices analysis of state budget trends and OFA tax expenditure reports

Among the Most Costly

Business Tax Breaks

• Research and Development Tax Credit

– Est. cost of $26.1 million in FY 2017

– $2.2 billion in carryforward credits

• Single Sales Factor

– Est. cost of $302.9 million in FY 2017

– Reduced corporate income tax revenue

by a third

Building on Connecticut’s

Commitment to Transparency

• Require Regular Review of Business Tax Breaks – Just like spending on education, roads,

and other spending

• Require Corporate Tax Disclosure – To determine how much state and local

taxes large corporations are paying

• Prepare for GASB 77 – Forthcoming treasure trove of data on

business tax breaks

Contact Information • Ellen Shemitz, Executive Director

– 203-498-4240 x 114

• Derek Thomas, Fiscal Policy Fellow

– 203-498-4240 x 111

• Ray Noonan, Associate Policy Fellow – [email protected]

– 203-498-4240 x 113

• Website: http://www.ctvoices.org/

• Twitter (@CTVoices): https://twitter.com/CTVoices

• Facebook: https://www.facebook.com/CTVoicesforChildren/

16th Annual

Budget Forum

Building a Budget

for Connecticut's

Future

![Volunteer Income Tax Assistance “VITA” Earned Income Tax ... · Volunteer Income Tax Assistance “VITA” Earned Income Tax Credit “EITC” Revised 1/28/19 [DOCUMENT TITLE]](https://static.fdocuments.net/doc/165x107/5fa5a5c85aa0bb13122ce462/volunteer-income-tax-assistance-aoevitaa-earned-income-tax-volunteer-income.jpg)