The goal of Mike & Kelley Engstrom and KAM Kartway is to ...

Upload

daniel-florenceCategory

view

355download

1

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter, not necessarily those of the IASC Foundation or the IASB

© 2008 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

Fair ValueMeasurement

Jan Engstrom

Sao Paulo

September 2009

2

Let’s start with:- How would you like it?

today’s value? can’t answer? historical cost?

3

Let’s start with:- How would you like it?

today’s value historical cost

OK, but – who are you? It might make a difference.

an investor?

a regulator?

a banker?

a supplier?

a distributor?

an employee?

4

Let’s continue with:- How would you like it?

today’s value historical cost

US $ 100 ?

50 shares in Google ?

A 5 year fixed rate treasury bond ? ?

A currency hedge !

Office building ?

General purpose machine ? ?

Product specific production line ?

A business closing down ?

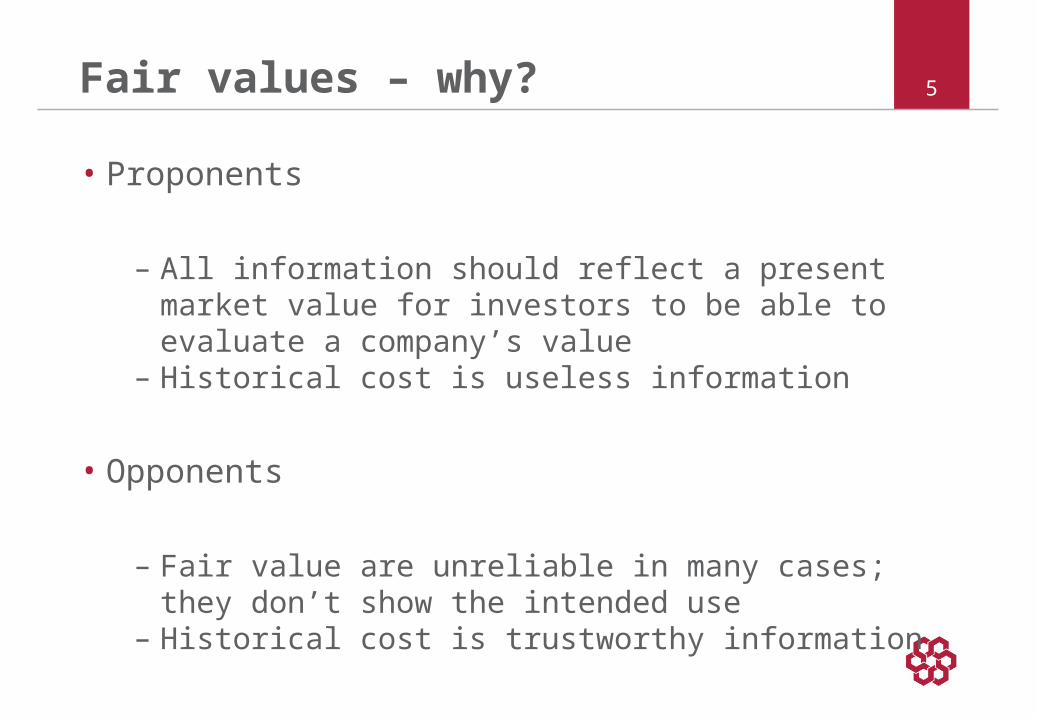

5Fair values – why?

• Proponents

– All information should reflect a present market value for investors to be able to evaluate a company’s value

– Historical cost is useless information

• Opponents

– Fair value are unreliable in many cases; they don’t show the intended use

– Historical cost is trustworthy information

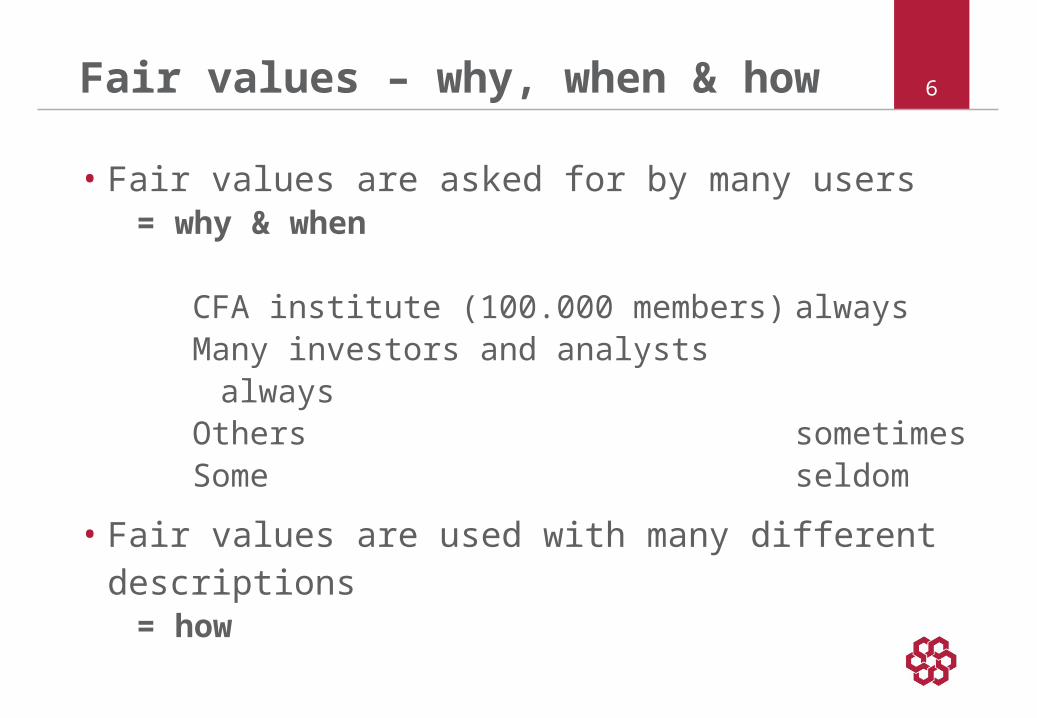

6Fair values – why, when & how

• Fair values are asked for by many users = why & when

CFA institute (100.000 members) alwaysMany investors and analysts alwaysOthers sometimesSome seldom

• Fair values are used with many different descriptions= how

7Fair value – when?

• Some say:– always and for all items (ex. CFA)

• Others say:– For all items not engaged in a “repetitive” business

process (buying-producing-selling-buying-prod…)

• One can also hear:– Only for assets that shall be liquidated soon

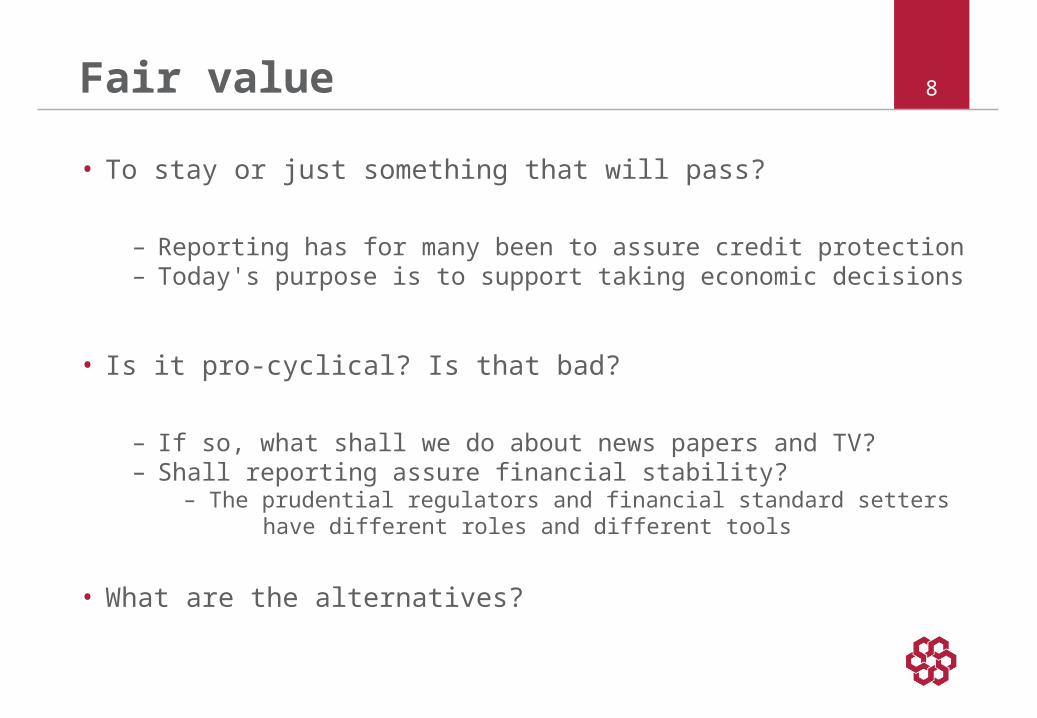

8Fair value

• To stay or just something that will pass?

– Reporting has for many been to assure credit protection– Today's purpose is to support taking economic decisions

• Is it pro-cyclical? Is that bad?

– If so, what shall we do about news papers and TV?– Shall reporting assure financial stability?

– The prudential regulators and financial standard setters have different roles and different tools

• What are the alternatives?

9Health warnings and presentations!

• How much warning is needed for the stated value of:

– US $ 100 – The home cooked cash-flow forecast based value (level 3)– The historical cost of old things

• Can disclose substitute information in the main statements?

– Some say yes– Others say no

10Why an IASB project?

• Fair value guidance is inconsistent

• Fair value guidance is dispersed across many IFRSs

• Fair value guidance have been added piecemeal over many years

• Increase convergence with US GAAP

11Dispersed IFRS guidance

© 2008 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

11

IFRS Refers to …

IAS 39 the ‘most advantageous’ market

IAS 41 the ‘most relevant’ market

IAS38the amount an entity would have paid for the asset but states that the most appropriate market price is the current bid price

IAS 40 tax benefits or burdens that are not specific to the current owner

IAS 17 fair value, but does not provide guidance on how to measure it

IAS 19fair value of defined benefit plan assets, but does not provide guidance on how to measure it

12The IASB project…

Clarifies the measurement objective

Creates a single source of guidance

Improves and harmonises disclosures

13This project… continued

Does not introduce new fair values

Does not change the measurement objective in existing IFRSs

14How does this project fit with others?

© 2008 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

14

Why?

When?

How? Fair Value Measurement Project

Conceptual Framework Project

IAS 39 IAS 41 IFRS 3 IFRS 5 etc…

15Core principle – on how

• Proposed definition

The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date

– exit price notion (selling vs. using and settle vs. transfer)– current price– not a liquidation price or a forced sale – market participant assumptions vs. entity intentions

© 2008 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

15

16Fair value hierarchy

• Level 1 inputs are quoted prices for identical assets and liabilities (unadjusted)

• Level 2 inputs are observable inputs other than quoted prices included within Level 1

• Level 3 inputs are inputs not based on observable market data (unobservable inputs)

© 2008 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

16

17Exit price notion

• Embodies expectations about the future cash inflows and outflows:

– Assets: cash inflows from selling vs. using the asset

– Liabilities: cash outflows from settle vs. transferring

18The transaction

• A fair value measurement assumes that the transaction to sell takes place in the most advantageous market

• No need for an exhaustive search of all possible markets to identify the most advantageous market

19Highest and best use

The use of an asset by market participants that would maximise the value of the asset or group of assets and liabilities within which the asset would be used

Ex: a downtown parking lot has higher value when sold for to build an office building than the cash flow generated by the parking business

© 2008 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

19

20Market participants continued

• The fair value of the asset or liability shall be measured using the assumptions that a market participant would use in pricing the asset or liability

21Market participants

• Independent buyers and sellers that are not related

• Knowledgeable sufficiently informed about the asset or liability

• Able to enter into a transaction for the asset or liability

• Willing to enter into a transaction for the asset or liability (not forced)

22

Specific challenges of complex financial instruments

• Distinguishing between orderly and distressed transactions in inactive markets

• Market participant assumptions in Level 3

• Highest and best use

• Transfer price for a liability

….. and more!

© 2008 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

23Steps towards a standard

• ED comment deadline 28 September 2009

• Hold round-table discussions

• Re-deliberate issues

• Publish final IFRS

• It will answer how – but not why and when!

© 2008 IASC Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.iasb.org

23

![United States Court of Appeals - CAFA Law Blog...Stephen C. Engstrom also served as plaintiffs’ counsel, but the district court found that Engstrom “b[ore] no responsibility for](https://static.fdocuments.net/doc/165x107/601bc8b40737d0651c1c22b4/united-states-court-of-appeals-cafa-law-stephen-c-engstrom-also-served-as.jpg)