16.5 Comparing depreciation methods

14

16.5 COMPARING DEPRECIATION METHODS

-

Upload

vce-accounting-michael-allison -

Category

Education

-

view

131 -

download

1

Transcript of 16.5 Comparing depreciation methods

16.5COMPARING DEPRECIATION METHODS

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

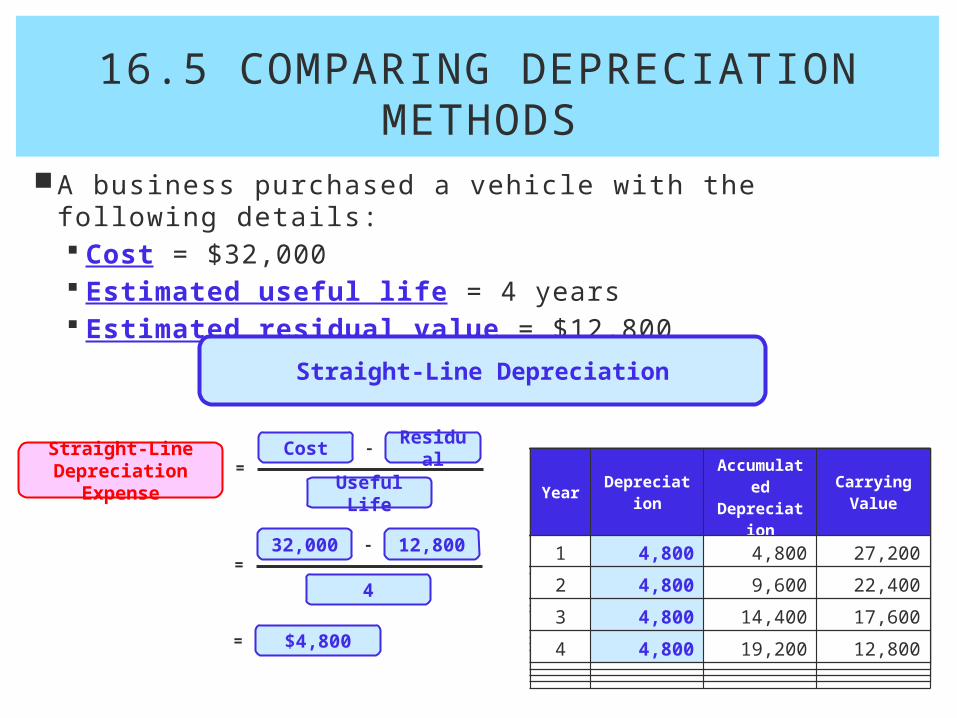

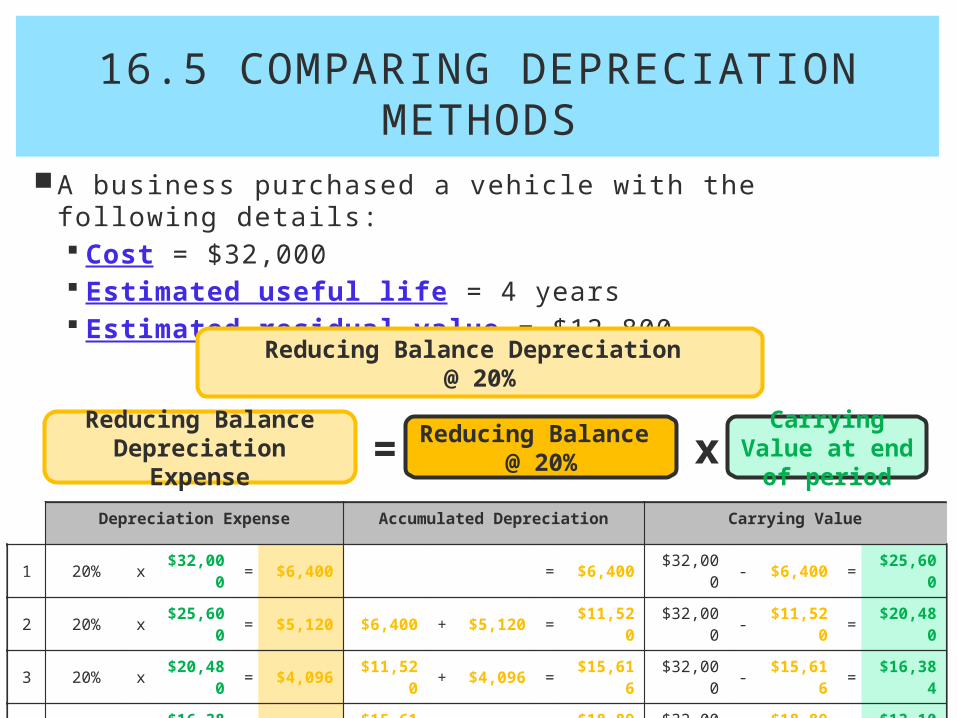

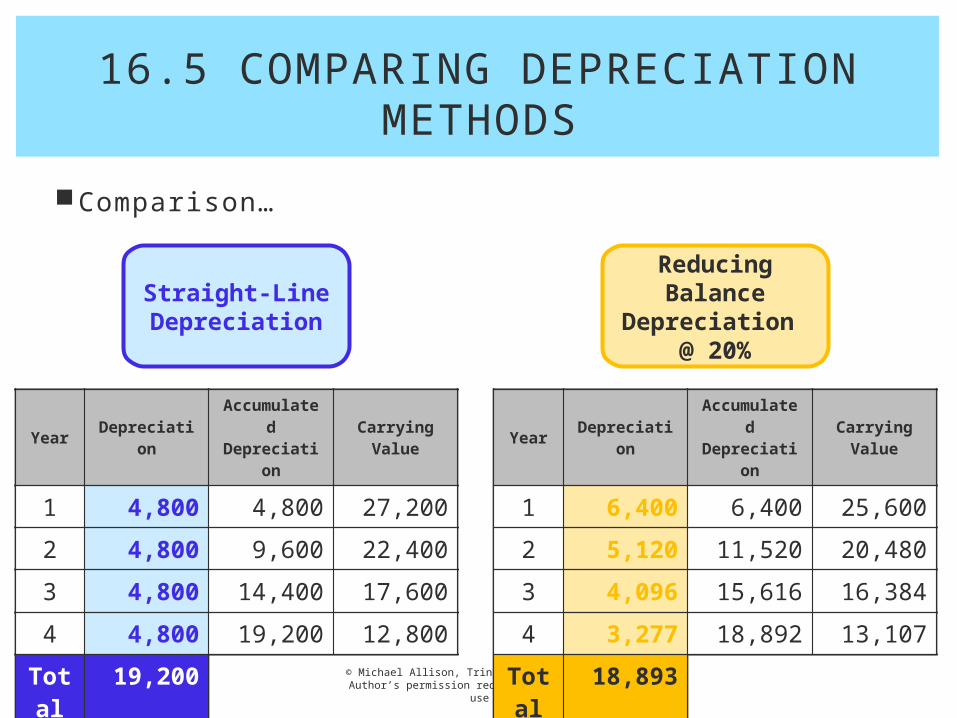

A business purchased a vehicle with the following details:

Cost = $32,000

Estimated useful life = 4 years

Estimated residual value = $12,800

The fi rm is debating which depreciation

16.5 COMPARING DEPRECIATION METHODS

Reducing Balance

Depreciation @ 20%

Straight-Line Depreciation or

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

A business purchased a vehicle with the following details: Cost = $32,000 Estimated useful life = 4 years Estimated residual value = $12,800

Straight-Line Depreciation

Expense=

Residual

Cost -

Useful Life

= $4,800

=12,80032,000 -

4

YearDepreciati

on

Accumulated

Depreciation

Carrying Value

YearDepreciati

on

Accumulated

Depreciation

Carrying Value

1 4,800 4,800 27,200

YearDepreciati

on

Accumulated

Depreciation

Carrying Value

1 4,800 4,800 27,200

2 4,800 9,600 22,400

YearDepreciati

on

Accumulated

Depreciation

Carrying Value

1 4,800 4,800 27,200

2 4,800 9,600 22,400

3 4,800 14,400 17,600

YearDepreciati

on

Accumulated

Depreciation

Carrying Value

1 4,800 4,800 27,200

2 4,800 9,600 22,400

3 4,800 14,400 17,600

4 4,800 19,200 12,800

Straight-Line Depreciation

16.5 COMPARING DEPRECIATION METHODS

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

A business purchased a vehicle with the following details: Cost = $32,000 Estimated useful life = 4 years Estimated residual value = $12,800

Reducing Balance @ 20%=

Carrying Value at end

of period

Reducing Balance Depreciation

Expensex

Reducing Balance Depreciation @ 20%

16.5 COMPARING DEPRECIATION METHODS

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

Depreciation Expense Accumulated Depreciation Carrying Value

1 20% x$32,00

0= $6,400 = $6,400

$32,000

- $6,400 =$25,60

0

2 20% x$25,60

0= $5,120 $6,400 + $5,120 =

$11,520

$32,000

-$11,52

0=

$20,480

3 20% x$20,48

0= $4,096

$11,520

+ $4,096 =$15,61

6$32,00

0-

$15,616

=$16,38

4

4 20% x$16,38

4= $3,277

$15,616

+ $3,277 =$18,89

2$32,00

0-

$18,892

=$13,10

7

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

Cost$32,000

$4,800

Carrying Value

$27,200

Carrying Value

$22,400

Carrying Value

$17,600

Straight-line depreciation…

$4,800 $4,800

0 1 2 3 4

$4,800

Carrying Value

$12,800

Cost$32,000

32,000 x 20% =

$6,400

Carrying Value

$25,600

Carrying Value

$20,480

Carrying Value

$16,384

Reducing balance depreciation…

0 1 2 3 4

Carrying Value

$13,107

25,600 x 20% =

$5,120

20,480 x 20% =

$4,096

16,384 x 20% =

$3,277

16.5 COMPARING DEPRECIATION METHODS

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

Comparison…

Reducing Balance

Depreciation @ 20%

Straight-Line Depreciation

16.5 COMPARING DEPRECIATION METHODS

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 4,800 4,800 27,200

2 4,800 9,600 22,400

3 4,800 14,400 17,600

4 4,800 19,200 12,800

Total

19,200

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 6,400 6,400 25,600

2 5,120 11,520 20,480

3 4,096 15,616 16,384

4 3,277 18,892 13,107

Total

18,893

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 4,800 4,800 27,200

2 4,800 9,600 22,400

3 4,800 14,400 17,600

4 4,800 19,200 12,800

Total

19,200

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 6,400 6,400 25,600

2 5,120 11,520 20,480

3 4,096 15,616 16,384

4 3,277 18,892 13,107

Total

18,893

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 4,800 4,800 27,200

2 4,800 9,600 22,400

3 4,800 14,400 17,600

4 4,800 19,200 12,800

Total

19,200

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 6,400 6,400 25,600

2 5,120 11,520 20,480

3 4,096 15,616 16,384

4 3,277 18,892 13,107

Total

18,893

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 4,800 4,800 27,200

2 4,800 9,600 22,400

3 4,800 14,400 17,600

4 4,800 19,200 12,800

Total

19,200

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 6,400 6,400 25,600

2 5,120 11,520 20,480

3 4,096 15,616 16,384

4 3,277 18,892 13,107

Total

18,893

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 4,800 4,800 27,200

2 4,800 9,600 22,400

3 4,800 14,400 17,600

4 4,800 19,200 12,800

Total

19,200

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 6,400 6,400 25,600

2 5,120 11,520 20,480

3 4,096 15,616 16,384

4 3,277 18,892 13,107

Total

18,893

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 4,800 4,800 27,200

2 4,800 9,600 22,400

3 4,800 14,400 17,600

4 4,800 19,200 12,800

Total

19,200

YearDepreciatio

n

Accumulated

Depreciation

Carrying Value

1 6,400 6,400 25,600

2 5,120 11,520 20,480

3 4,096 15,616 16,384

4 3,277 18,892 13,107

Total

18,893

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

Comparison…

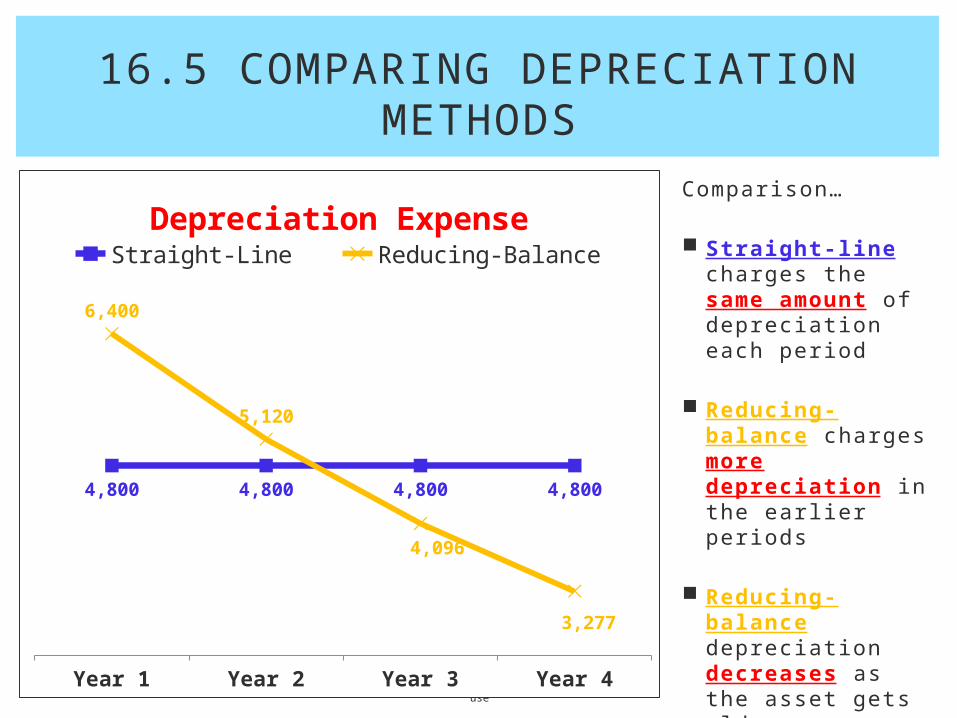

Straight-line charges the same amount of depreciation each period

Reducing-balance charges more depreciation in the earlier periods

Reducing-balance depreciation decreases as the asset gets older

Year 1 Year 2 Year 3 Year 4

4,800 4,800 4,800 4,800

6,400

5,120

4,096

3,277

Depreciation ExpenseStraight-Line Reducing-Balance

16.5 COMPARING DEPRECIATION METHODS

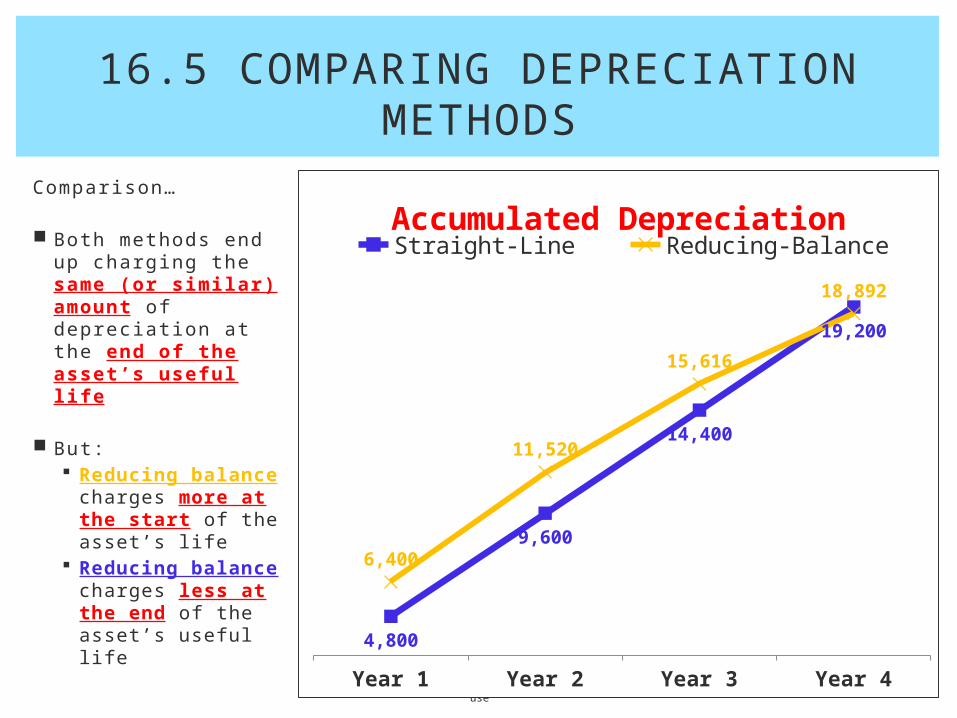

© Michael Allison, Trinity Grammar School.Author’s permission required for external useYear 1 Year 2 Year 3 Year 4

4,800

9,600

14,400

19,200

6,400

11,520

15,616

18,892

Accumulated DepreciationStraight-Line Reducing-Balance

Comparison…

Both methods end up charging the same (or similar) amount of depreciation at the end of the asset’s useful life

But: Reducing

balance charges more at the start of the asset’s life

Reducing balance charges less at the end of the asset’s useful life

16.5 COMPARING DEPRECIATION METHODS

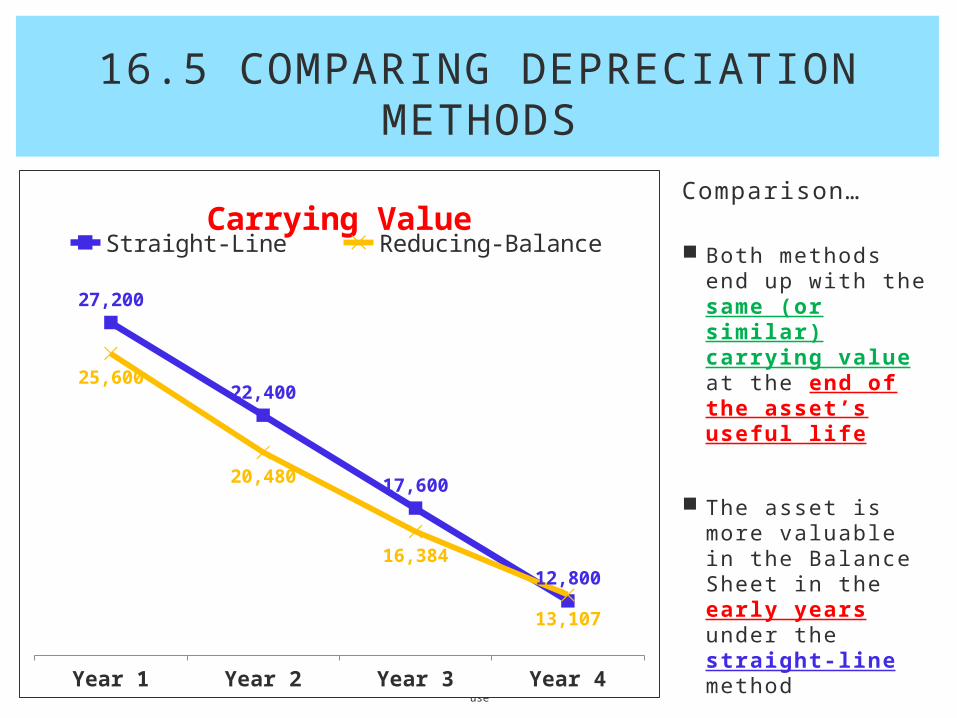

© Michael Allison, Trinity Grammar School.Author’s permission required for external useYear 1 Year 2 Year 3 Year 4

27,200

22,400

17,600

12,800

25,600

20,480

16,384

13,107

Carrying ValueStraight-Line Reducing-Balance

Comparison…

Both methods end up with the same (or similar) carrying value at the end of the asset’s useful life

The asset is more valuable in the Balance Sheet in the early years under the straight-line method

16.5 COMPARING DEPRECIATION METHODS

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

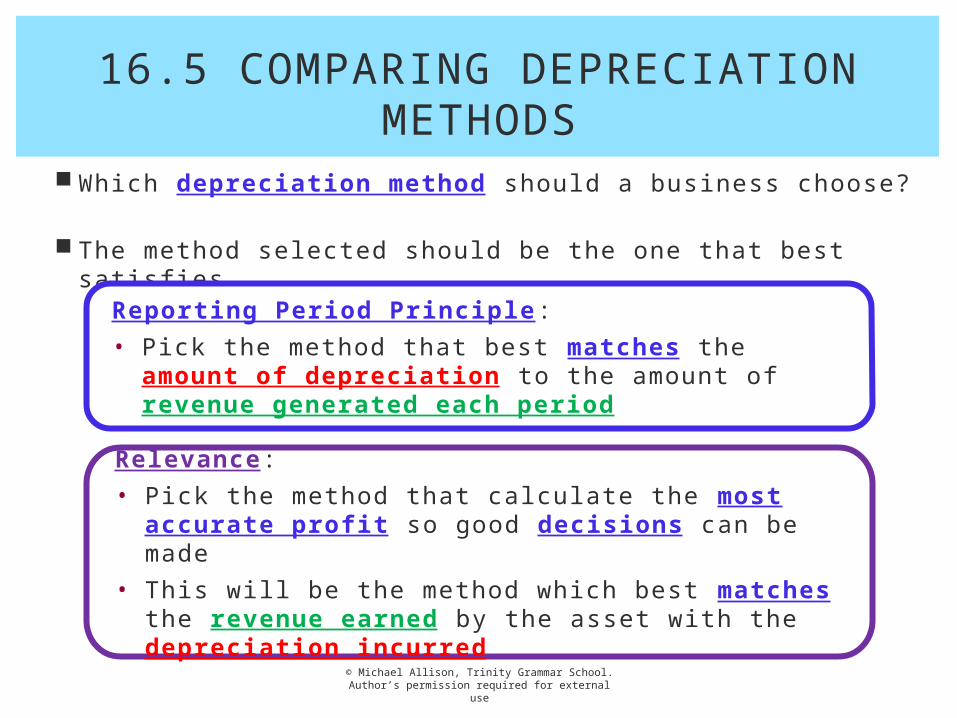

Which depreciation method should a business choose?

The method selected should be the one that best satisfi es…

Reporting Period Principle :

• Pick the method that best matches the amount of depreciation to the amount of revenue generated each period

Relevance:

• Pick the method that calculate the most accurate profi t so good decisions can be made

• This will be the method which best matches the revenue earned by the asset with the depreciation incurred

16.5 COMPARING DEPRECIATION METHODS

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

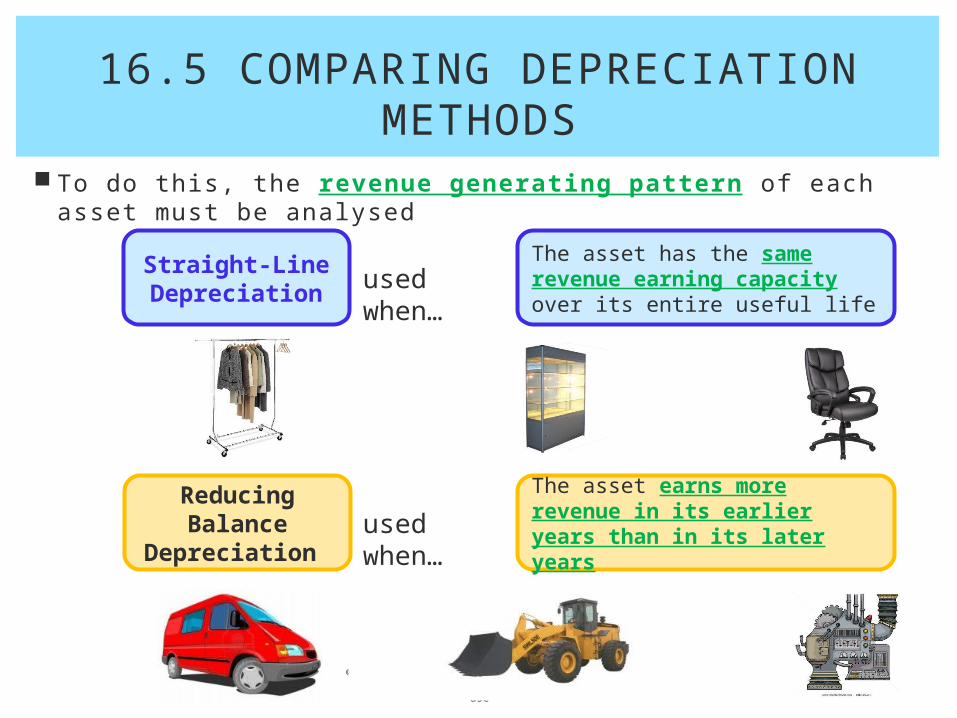

To do this, the revenue generating pattern of each asset must be analysed

Reducing Balance

Depreciation

Straight-Line Depreciation used

when…

used when…

The asset has the same revenue earning capacity over its entire useful life

The asset earns more revenue in its earlier years than in its later years

16.5 COMPARING DEPRECIATION METHODS

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

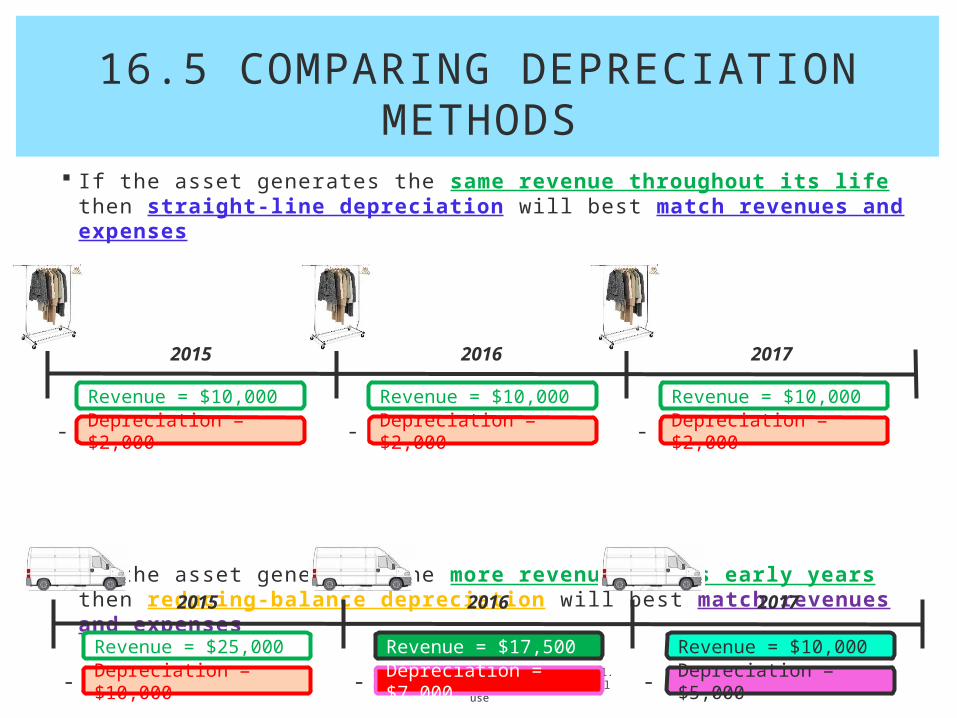

If the asset generates the same revenue throughout its life then straight-line depreciation will best match revenues and expenses

If the asset generates the more revenue in its early years then reducing-balance depreciation will best match revenues and expenses

2015 2016 2017

Revenue = $10,000 Revenue = $10,000 Revenue = $10,000Depreciation = $2,000- Depreciation =

$2,000- Depreciation = $2,000-

2015 2016 2017

Revenue = $25,000 Revenue = $17,500 Revenue = $10,000Depreciation = $10,000- Depreciation =

$7,000- Depreciation = $5,000-

16.5 COMPARING DEPRECIATION METHODS

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

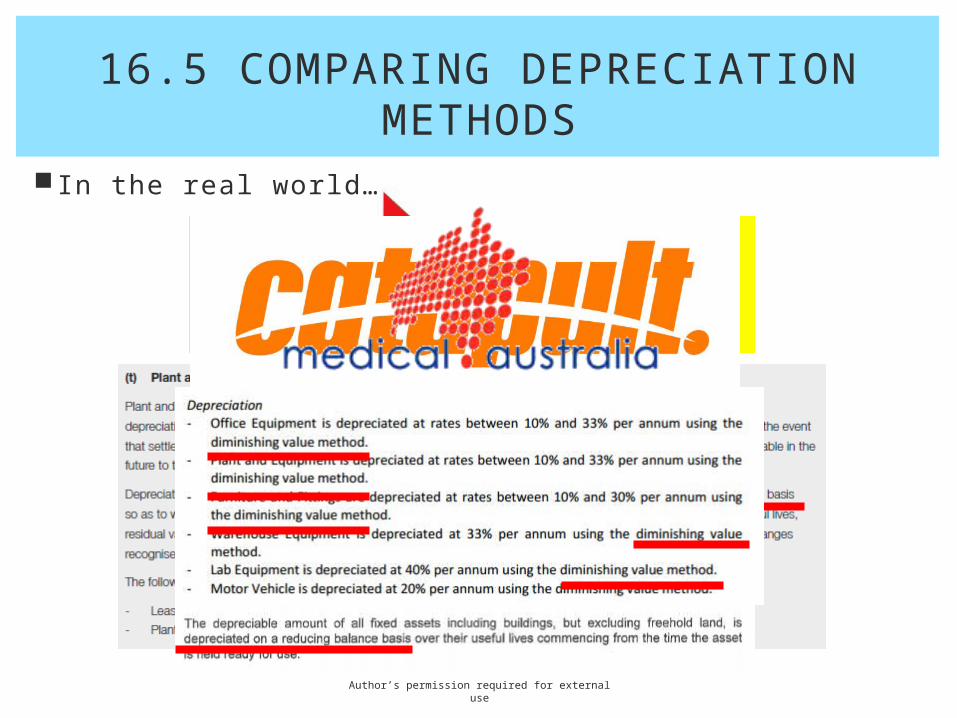

In the real world…

16.5 COMPARING DEPRECIATION METHODS

© Michael Allison, Trinity Grammar School.Author’s permission required for external use

TASK

In-class Homework

SQ3 XSQ4 XSQ5 XSQ6 XSQ8 XSQ9 XSQ10 X