14th Annual Syndications

57

1 London, 6 th March 2012 14 th Annual Syndications and Co-financiers Meeting London 6 th March 2012 European Bank for Reconstruction and Development

Transcript of 14th Annual Syndications

1

London, 6th March 2012

14th Annual Syndicationsand Co-financiers Meeting

London6th March 2012

European Bankfor Reconstruction and Development

2

London, 6th March 2012

EBRD’s Loan Syndication Activities

Lorenz JorgensenDirector, Head of Loan Syndications

EBRD

14th Annual Syndications and Co-financiers Meeting

6th March 2012, London

3

London, 6th March 2012

Agenda

The global setting

The EBRD region

EBRD’s syndication activities

Outlook

4

London, 6th March 2012

Some recent headlines

The good …“Relationships … under scrutiny but bank liquidity remains for IG borrowers”

– Euroweek, 18 Nov 2011

The bad … and the ugly …“Eastern Europe has most to fear from banks’ retreat”

– Financial Times, 15 Nov 2011

“CEE to be battered most by deleveraging”– Euroweek, 18 Nov 2011

“Banks face a perfect storm that is getting worse”– Financial Times, 25 Jan 2012

“Gulf opens in loan markets as lenders discriminate”– Euroweek, 2 March 2012

5

London, 6th March 2012

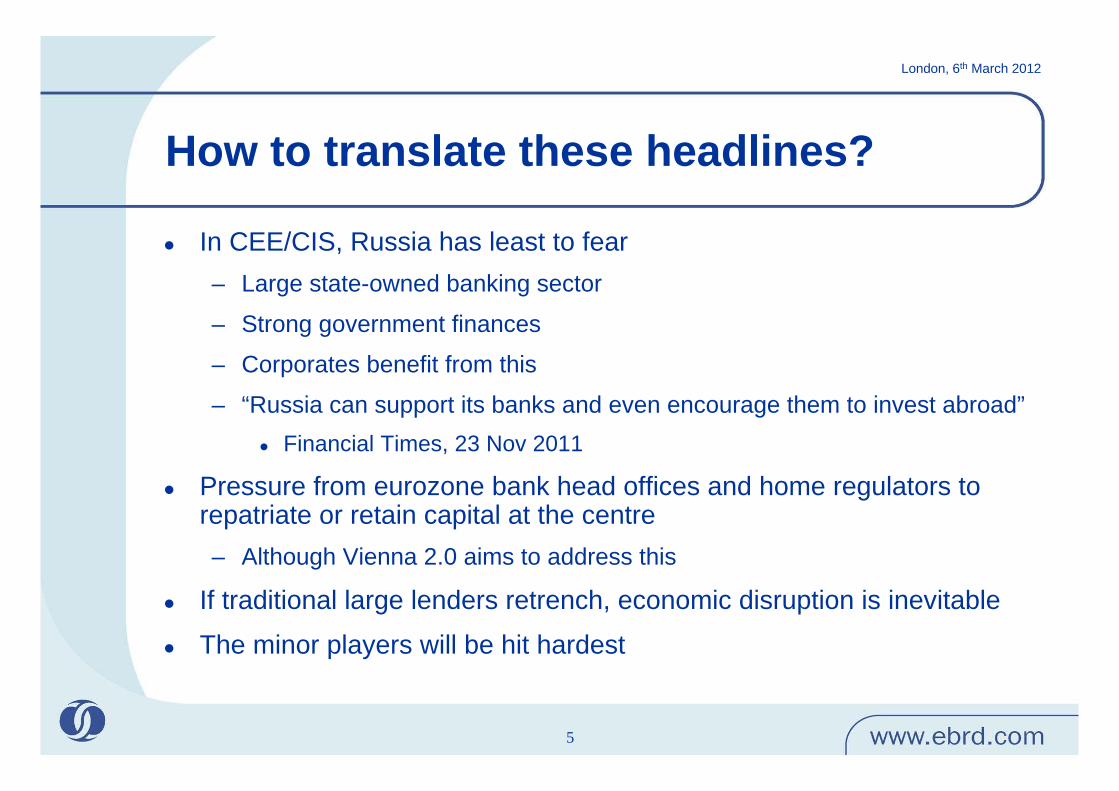

How to translate these headlines?

In CEE/CIS, Russia has least to fear– Large state-owned banking sector

– Strong government finances

– Corporates benefit from this

– “Russia can support its banks and even encourage them to invest abroad”Financial Times, 23 Nov 2011

Pressure from eurozone bank head offices and home regulators to repatriate or retain capital at the centre– Although Vienna 2.0 aims to address this

If traditional large lenders retrench, economic disruption is inevitable

The minor players will be hit hardest

6

London, 6th March 2012

Global loan volumes 2007-2011

0

200

400

600

800

1,000

1,200

1,400

1,600

2007Q1

2007Q2

2007Q3

2007Q4

2008Q1

2008Q2

2008Q3

2008Q4

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

2010Q4

2011Q1

2011Q2

2011Q3

2011Q4

0

500

1,000

1,500

2,000

2,500

3,000

Americas EMEA Asia-Pacific No of deals

USD

bn

No of deals

Gradualincrease from 3Q10,

falling in 2H11

7

London, 6th March 2012

Global loan volumes 2007-2011:Refinancing as % of total

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 20110

10

20

30

40

50

60

Total loan volume Refinancing as % of total volume

USD

bn

Refinancing as %

of volume

High quality, large volumeborrowers continuously seeking

to pre-fund requirements

8

London, 6th March 2012

Average pricing by rating

0

50

100

150

200

250

300

350

400

450

500

2008Q1

2008Q2

2008Q3

2008Q4

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

2010Q4

2011Q1

2011Q2

2011Q3

2011Q4

As BBBs BBs Bs

Bas

is p

oint

s

Weaker names facerising spreads

Spreads continue tofall for the best names

9

London, 6th March 2012

European loans vs bonds volumes

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

2005 2006 2007 2008 2009 2010 2011

Loans Bonds

USD

trn

Loans suffered in the crisis,but have pulled ahead again

10

London, 6th March 2012

Agenda

The global setting

The EBRD region

EBRD’s syndication activities

Outlook

11

London, 6th March 2012

Loan volumes in key EBRD COOs, 2000-11

0

20

40

60

80

100

120

140

160

180

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Russia Turkey Kazakh Poland Ukraine Other

USD

bn

12

London, 6th March 2012

Effects of the crisis on Russian banks

Global financial volatilityReduced access to wholesale fundingCapital flight

Liquidity squeeze (partly offset by higher deposits)

Slower credit growthIncreased spreadsTighter collateral

13

London, 6th March 2012

Russian banks syndicated loan volumes, 2005-2011

US

D m

m

Num

ber of deals

0

2000

4000

6000

8000

10000

12000

14000

2005 2006 2007 2008 2009 2010 20110

10

20

30

40

50

60

70

80

State/muni-owned Other Number of deals

Private banks, 2007: 34Private banks, 2011: 7

14

London, 6th March 2012

Bank borrower dynamics

State-owned banks are the major drivers of volume (no surprise)

Private banks increasing their share from a low in 2009– But still only at 50% of 2008 volume

– Main private banks able to continue borrowing through the crisis are the top names, including, for example:

Alfa Bank

MDM Bank

Uralsib

Promsvyazbank

Very hard for banks outside top 20 (maybe 30?) to borrow

Pricing movements become somewhat academic– When the question of any market access (at all) becomes starkly binary

15

London, 6th March 2012

Russian banks,2005-2008 syndicated loan volume share

Sberbank23%

MDM Bank13%

Alfa Bank14%

Other banks37%

Bank of Moscow2% VTB Group

9%

VEB2%

Total Russian bank syndicated loan volume of USD 38.2 billion, 2005-200875 banks in total have borrowed in the market

16

London, 6th March 2012

Russian banks,2009-2011 syndicated loan volume share

VEB31%

Sberbank19%

VTB18%

MDM Bank3%

Gazprombank12%

Promsvyazbank3%

Other banks14%

Total Russian bank syndicated loan volume of USD 17.5 billion, 2009-201119 banks in total have borrowed in the market

17

London, 6th March 2012

Maturities of Russian banks’ eurobondsand foreign syndicated loans

0

2

4

6

8

10

12

2011 2012 2013 2014 2015

Eurobonds Syndicated loans

USD

bn

High volumesfalling due in 2013

18

London, 6th March 2012

Summary: effect of the crisis on syndicated loans to Russian banks

Number of syndicated loan bank borrowers:– 2005-2008: 75

– 2009-2011: 19

Volume of syndicated loan bank deals:– 2005-2008: USD 38.2 bn

– 2009-2011: USD 17.5 bn

Share of “state quartet”*– 2005-2008: 34%

– 2009-2011: 80%

* VEB, VTB, Sberbank, Gazprombank

19

London, 6th March 2012

All Russian borrowers* by %, 2010-2011:concentrated at the top of the credit curve

Other47%

VEB11%

Tatneft10%

Gazprom-Neft9%

Metallo-invest

5%

Severnefte-gazprom

5%

Sberbank4%

Renova4%Mechel

5%TNK-BP5%

> 50% captured by 9 names and 3 sectors

* ie FIs plus corporates

20

London, 6th March 2012

Corporates and retail will benefit from the strength of the Russian banks

Russian bank lending grew 30% in 2011

Russian bank lending forecast to grow 20% in 2012– Slower than 2011 because corporate investment is slowing

– Prediction for USD 150 bn equivalent of lendingOf which USD 110 bn to corporates

Sberbank takes approx 35% of loan market

However, pricing is moving up by 50-100 bp– Reflecting withdrawal of French banks and higher USD funding costs

Top borrowers can be choosy about when they come to the market– eg VEB, NLMK

Western/international banks will find it tougher to compete than ever

21

London, 6th March 2012

Agenda

The global setting

The EBRD region

EBRD’s syndication activities

Outlook

22

London, 6th March 2012

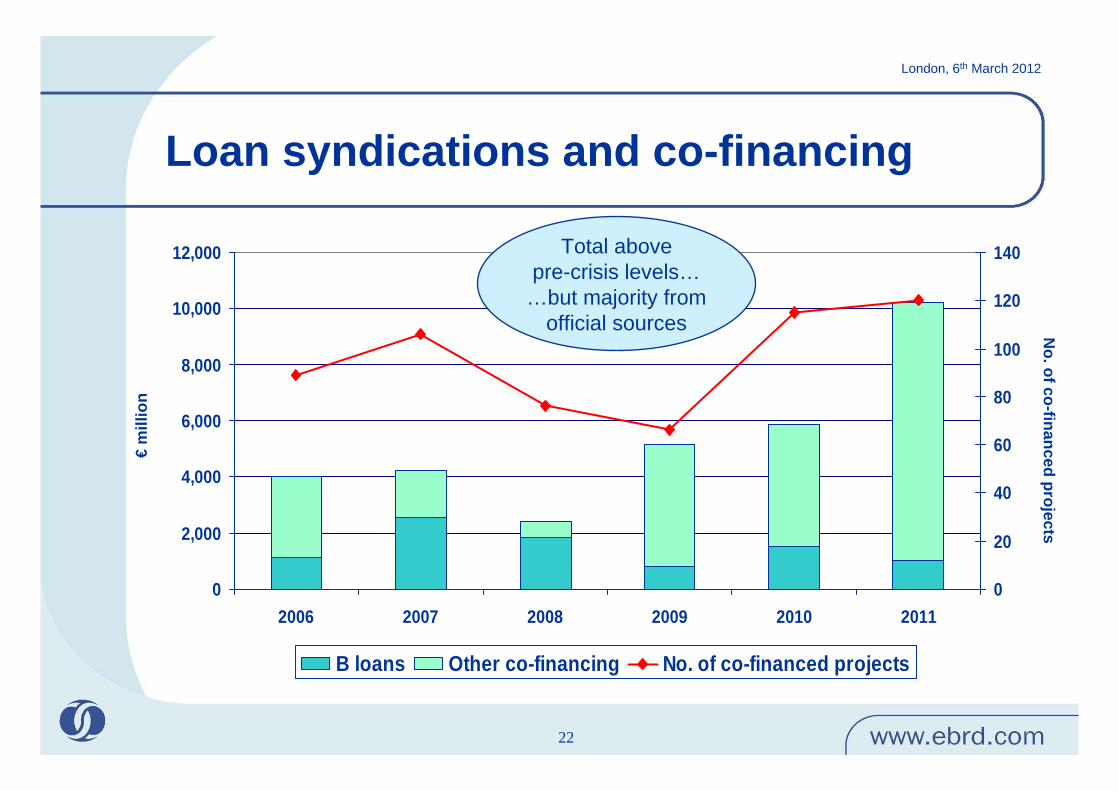

Loan syndications and co-financing

0

2,000

4,000

6,000

8,000

10,000

12,000

2006 2007 2008 2009 2010 20110

20

40

60

80

100

120

140

B loans Other co-financing No. of co-financed projects

No. of co-financed projects

€m

illio

n

Total abovepre-crisis levels…

…but majority fromofficial sources

23

London, 6th March 2012

B loan volumes by country, 2011, € mm

Romania, 294

Russia, 218Slovenia, 100

Ukraine, 71

Kazakhstan, 54

Azerbaijan, 50

Croatia, 43Serbia, 40

Poland, 36

Bosnia & Herz, 13 Georgia, 9 Armenia, 7 Tajikistan, 5 Kyrgyz Rep, 4

24

London, 6th March 2012

B loan volumes by sector, 2011, € mm

Power, 271

Financial institutions, 226

Natural resources, 140

Building materials, 100

Transport, 94

Agribusiness, 55

Real estate, 45Telecoms, 13

25

London, 6th March 2012

Noteworthy successes in difficult countries

Ukraine– Kubgas: USD 40 mm, 7 yrs

– Interleasinvest: USD 90 mm, 7 & 5 yrs

Kazakhstan– KEGOC: USD 156 mm, 12 &

15 yrs

Bosnia & Herzegovina– Telemach d.o.o. Sarajevo:

€ 25 mm, 6 & 8 yrs

Armenia– Araratbank: USD 12 mm, 1,3

and 5 yrs

Tajikistan– Bank Eskhata: USD 8 mm, 4

yrs

Kyrgyz Republic– Mol Bulak: USD 8 mm, 3 yrs

26

London, 6th March 2012

26

Top B lenders*

* Active commitments for funded participations

1. UniCredit Group2. Raiffeisen Bank International3. ING Group4. Erste Group5. Credit Agricole 6. Societe Generale7. Nordea8. Intesa Sanpaolo9. BNP Paribas10. Cordiant Capital

11. Commerzbank12. Kommunalkredit Austria13. Bayern LB14. RLB Oberoesterreich15. Bankia16. FMO17. Fortis Bank18. SEB19. Danske Bank20. Rabobank

27

London, 6th March 2012

Agenda

The global setting

The EBRD region

EBRD’s syndication activities

Outlook

28

London, 6th March 2012

Declining retail appetite:MLAs/investors per deal, Russia 2005-2011*

0

2

4

6

8

10

12

14

2005 2006 2007 2008 2009 2010 2011

Investors/deal MLAs/deal

* All deals: FIs plus corporates

29

London, 6th March 2012

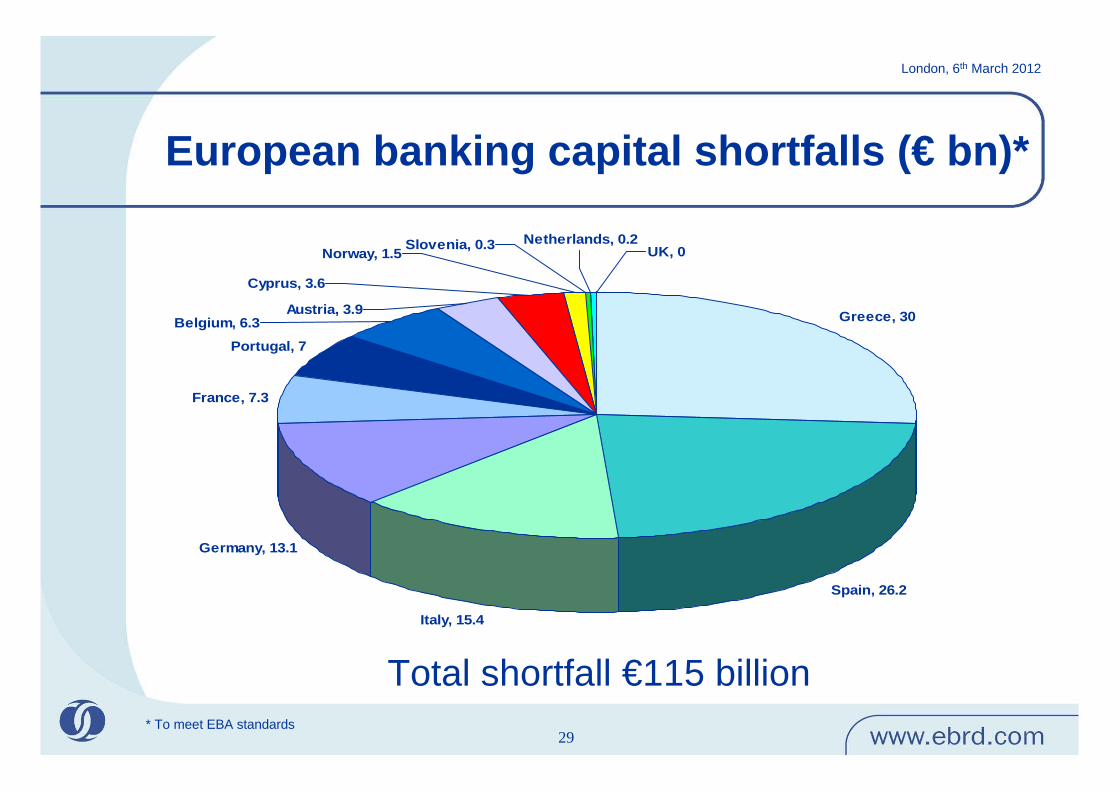

European banking capital shortfalls (€ bn)*

Greece, 30

Spain, 26.2

Italy, 15.4

Germany, 13.1

France, 7.3

Portugal, 7

Norway, 1.5

Belgium, 6.3Austria, 3.9

Cyprus, 3.6

UK, 0Slovenia, 0.3 Netherlands, 0.2

* To meet EBA standards

Total shortfall €115 billion

30

London, 6th March 2012

Key banks in Eurozone, China and Gulf, assets (USD bn)

0

500

1,000

1,500

2,000

2,500

3,000

BNPPHSBC

Credit A

gricole

ICBC

ING

CBCSan

tande

r

BoC ABC SGUnic

redit

Intes

a

CDBB o

Comm

CPSB

QNBNBAD

NBK

Chinese banks growing at20% pa for last few years

Eurozone banks shrinkingtheir balance sheets

31

London, 6th March 2012

Are Chinese and Gulf banks the answer?

They could be a strong source of USD fundingBUTNeither group considers the EBRD region a core marketChinese banks support projects which benefit China– All are still majority state-owned

Gulf banks may be good for new SEMED regionNeither group yet ready to support small transactions for mid-tier corporates in countries where they do not have an active presence

32

London, 6th March 2012

Why Chinese banks are not (yet) the answer

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011

Rest of world China

Chinese banks’ share of global syndicated lending

33

London, 6th March 2012

Conclusions

Eurozone crisis and Basel III dominate and shape lending appetitesStrong names are still able to retain good access to the loan market

– But maybe the relationship and ancillary business argument is looking increasingly weak

“Everybody is questioning whether their relationships are as good as they really think they are, and just who is worth lending to”

– Euroweek, 2 March 2012

– So pricing is rising and tenors shortening for even the good names (but not the best)

Division between high- and low-quality credits will persist and increaseUSD funding availability – a serious problem for eurozone banksDeclining retail investor baseStructures are key

– If security is tangible and measurable, the Basel capital allocation is softened, and this sells a deal

34

London, 6th March 2012

Some closing thoughts…

35

London, 6th March 2012

Russia – top ten syndicated loan providers 2011(and EBRD Russia volume 2011 – inc. equity)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

CACIB

Unicredit Citi

BNPP

HSBC

SGCIB

Sberban

k

BTMU

SMBC ING

EBRD

Of which majorityat 5 yrs or longer

USD

bn

36

London, 6th March 2012

EBRD has a co-financing mandate

Article 11.1 of the TreatyEstablishing the EBRD:

The Bank shall carry out its operations by …“co-financing together with … commercial

banks … or other sources … to facilitate … the participation of private

and/or foreign capital”

37

London, 6th March 2012

37

EBRD B loan portfolio performance

Total B loans committed: €11.4 billion

Strong EBRD B Loan portfolio performance– Gross write-offs/Total B Loans committed: 0.20%

– Net write-offs/Total B Loans after recoveries /write-backs: 0.15%

– These are cumulative data since establishment of EBRD in 1991 (not per annum data)

Key assumptions/provisos:1. That a commercial bank writes off the same percentage of its B Loan as the EBRD writes off on its A Loan2. Currency exchange rates vary, and thus precise percentages may vary3. Information and data as per end of December 2011 (subject to confirmation by auditors)

38

London, 6th March 2012

Agenda

The global setting

The EBRD region

EBRD’s syndication activities

Outlook

39

London, 6th March 2012

Thank you for your attention!Lorenz JorgensenDirector, Head of Loan SyndicationsTel: +44 20 7338 6902Email: [email protected] loan market data sourced from Dealogic LoanAnalytics

40

London, 6th March 2012

41

London, 6th March 2012

Thank you for coming!14th Annual Syndications

and Co-financiers MeetingLondon

6th March 2012

Presentations will be posted to http://www.ebrd.com/oppor/syndi/meeting/index.htm

European Bankfor Reconstruction and Development

42

London, 6th March 2012

14th Annual Syndicationsand Co-financiers Meeting

London6th March 2012

Presentations will be posted to http://www.ebrd.com/oppor/syndi/meeting/index.htm

European Bankfor Reconstruction and Development

43

London, 6th March 2012

Annexes

Selected Recent Co-financings

44

London, 6th March 2012

44

Selected Recent Co-financings

ARARATBANK (Armenia)– USD 12 mm senior loan for on-lending to local micro, small

and small enterprises– The first syndicated loan to Araratbank, with oversubscribed

B Loan and three new B-lenders joining EBRD B Loan for the first time

– EBRD A Loan USD 3 mm; 5 years – EBRD B1 Loan USD 3 mm; 3 years– EBRD B2 Loan USD 6 mm; 1 year– Signed October 2011

45

London, 6th March 2012

45

Selected Recent Co-financings

Raiffeisen Bank S.A. (Romania)– EUR 150 mm senior loan for trade finance, corporate, SME and retail

financing

– The first syndicated loan transaction in the financial sector inRomania since the global financial crisis (October 2008), aimed at re-opening access to debt capital markets for Romanian commercial banks

– EBRD A Loan EUR 40 mm; 5 years

– EBRD B Loan EUR 110 mm; 2 years

– Signed September 2011

46

London, 6th March 2012

46

Selected Recent Co-financings

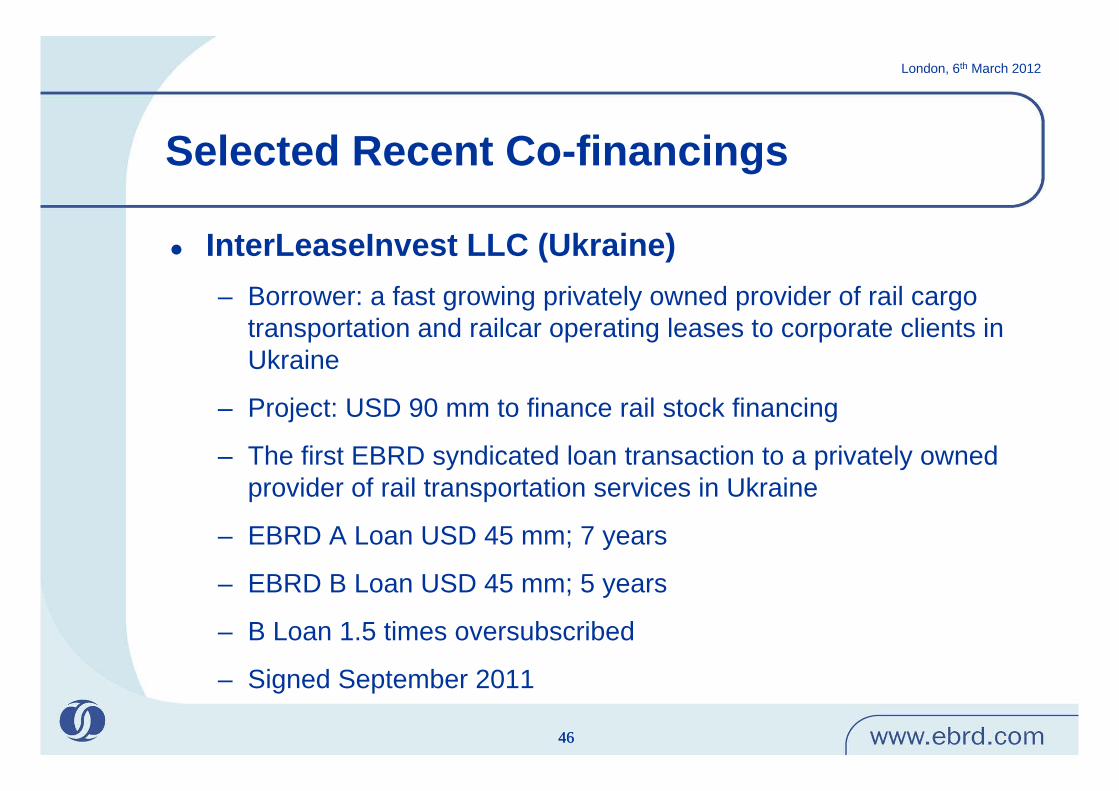

InterLeaseInvest LLC (Ukraine)– Borrower: a fast growing privately owned provider of rail cargo

transportation and railcar operating leases to corporate clients in Ukraine

– Project: USD 90 mm to finance rail stock financing

– The first EBRD syndicated loan transaction to a privately owned provider of rail transportation services in Ukraine

– EBRD A Loan USD 45 mm; 7 years

– EBRD B Loan USD 45 mm; 5 years

– B Loan 1.5 times oversubscribed

– Signed September 2011

47

London, 6th March 2012

47

Selected Recent Co-financings

Aura Shopping Centre Surgut (Russia)– EUR 70 mm senior loan to finance the development and construction of

a class-A retail and entertainment centre with a total gross buildable area of over 90,000 sqm located in Surgut, Western Siberia

– Replicate of business model already successfully implemented in other regions of Russia by the client

– EBRD A Loan EUR 45 mm; 10 years

– EBRD B Loan EUR 25 mm; 7 years

– Signed September 2011

48

London, 6th March 2012

48

Selected Recent Co-financings

Bank Eskhata (Tajikistan)– USD 8 mm senior loan for on-lending to local micro and

small enterprises– The first syndicated loan transaction in Tajikistan since 2008

and a first time a German cooperative bank committed to socially responsible lending has invested in Tajikistan alongside EBRD as a B lender

– EBRD A Loan USD 2 mm; 4 years – EBRD B Loan USD 6 mm; 4 years– Signed September 2011

49

London, 6th March 2012

49

Selected Recent Co-financings

Paravani Power Plant (Georgia)– USD 63.5 mm 15-year senior loan to Georgian-Urban

Enerji Ltd for the construction, financing, operation, maintenance and management of the Paravani hydro power plant and the transmission lines (allowing connection to the Georgian grid and export to Turkey)

– EBRD A Loan USD 52 mm; 15 years

– EBRD B Loan USD 11.5 mm; 15 years

– USD 52 mm Parallel Loan from IFC

– Signed August 2011

50

London, 6th March 2012

50

Selected Recent Co-financings

TransCapitalBank (Russia)– USD 13 mm senior loan for on-lending to local small and

medium-sized enterprises

– The first time an institution with a specific mandate to act as a socially responsible lender participates as co-financier to raise funds for a Russian borrower

– EBRD A Loan USD 10 mm; 4.5 years

– EBRD B Loan USD 3 mm; 3 years

– Signed August 2011

51

London, 6th March 2012

51

Selected Recent Co-financings

Credit Europe Bank (Russia)– USD 250 mm EBRD and IFC joint senior syndicated loan facility for

trade finance, corporate, SME and retail financing

– One of very limited number of syndicated loans completed for a private mid-sized Russian bank since the global financial crisis (October 2008)

– Syndication oversubscribed, raising double the sum originally intended from a wide range of investors (16 commercial banks)

– EBRD A Loan USD 50 mm; 3 years

– EBRD B Loan USD 75 mm; 1 year, with extension option for anotheryear

– Signed August 2011

52

London, 6th March 2012

52

Selected Recent Co-financings

MK Group and Sunoko (Serbia)– EUR 80 mm capex, working capital financing and

balance sheet restructuring senior secured loan

– The first international syndication with EBRD’s involvement in Serbia after the global financial crisis in the agricultural sector

– EBRD A Loan EUR 40 mm; 5 & 7 years

– EBRD B Loan EUR 40 mm; 5 years

– Signed August 2011

53

London, 6th March 2012

53

Selected Recent Co-financings

EDPR Cernavoda & Pestera wind farms (Romania)– EUR 188 mm EBRD and IFC joint project financing

for the construction, commissioning and operation of two adjacent wind farms: Pestera (90 MW) and Cernavoda (138 MW), both located in SE Romania

– EBRD A Loan EUR 69 mm; 14.5 years

– EBRD B Loan EUR 25 mm; 14.5 years

– EUR 94 mm Parallel Loan from IFC

– Signed July 2011

54

London, 6th March 2012

54

Selected Recent Co-financings

HIDROELECTRICA S.A. (Romania)– EUR 110 mm senior loan to finance the rehabilitation

of six units at Stejarul Bicaz, a 50-year old hydro power plant with a total capacity of 210 MW on the Bistrita River in the north-eastern Romania

– Hidroelectrica has a market share of 35% in Romania, with a network of 273 power plants and pumping stations with a total capacity of 6,482 MW

– EBRD A Loan EUR 69 mm; 14.5 years

– EBRD B Loan EUR 25 mm; 14.5 years

– Signed July 2011

55

London, 6th March 2012

55

Selected Recent Co-financings

Kazakhstan Electricity Grid Operating Company (Kazakhstan)– USD 156 mm senior loan for refinancing

purposes and for financing CAPEX associated with the rehabilitation of substations and high-voltage equipment

– The first syndicated loan for a Kazakh borrower since the global financial crisis (October 2008)

– EBRD A Loan USD 86 mm; 15 years

– EBRD B Loan USD 70 mm; 12 & 15 years

– Signed May 2011

56

London, 6th March 2012

56

Selected Recent Co-financings

Kubgas (Ukraine)– USD 40 mm 7-year senior loan for the development

of on-shore gas and condensate fields in the Lugansk region, eastern Ukraine, in the period of 2013

– One of very few transactions in Ukraine with a long term tenor for an independent natural resources sector company

– EBRD A Loan USD 25 mm; 7 years

– EBRD B Loan USD 15 mm; 7 years

– Signed May 2011

57

London, 6th March 2012

57

Selected Recent Co-financings

Termoelektrarna Šoštanj d.o.o. (TEŠ) (Slovenia)– EUR 200 mm to finance a EUR 1.2 billion investment

plan to replace four ageing power generation units with a new 600 MW unit utilising supercritical technologies

– TEŠ is the largest power generation plant in Slovenia with an installed capacity of 779 MW, generates, on average, one third of the energy in Slovenia.

– EBRD A1 Loan EUR 80 mm; 15 years

– EBRD A2 Loan EUR 20 mm; 12 years

– EBRD B1 Loan EUR 80 mm; 15 years

– EBRD B2 Loan EUR 20 mm; 12 years

– Signed January 2011