14873 252039 Annuity Basics 101. 14873 252039 2 Products and riders are available in most states....

35

14873 252039 Annuity Basics 101

-

Upload

edwin-lawder -

Category

Documents

-

view

216 -

download

1

Transcript of 14873 252039 Annuity Basics 101. 14873 252039 2 Products and riders are available in most states....

14873 252039

Annuity Basics 101

214873 252039

Products and riders are available in most states. Availability of some product features may vary by state. Please consult your attorney or accountant for legal and tax advice. All value and numerical demonstrations are for illustration only. Actual results may vary.

314873 252039

An annuity is a contract between an insurance company and the individual purchasing the annuity (the owner). In return for a sum of money (the premium), the insurance company makes guarantees to the purchaser.

◦ a guaranteed minimum interest rate for a guaranteed period of time,

◦ a lifetime guarantee that the owner will never receive less than a minimum interest rate while the money is with the insurance company (regardless of how low interest rates go)

414873 252039

You start an annuity by sending money (called the “premium”) to the insurance company◦ Depending upon the annuity’s provisions, the owner may have the

ability to pay additional premiums into the contract value

The premium goes into the annuity’s contract value (or accumulated value)

The account value has a way that it can grow◦ Fixed and fixed indexed annuities credit interest to the account value

similar to a bank savings account or certificate of deposit◦ Variable annuities may credit interest and/or have unit values that can

increase or decrease the value of the account similar to a mutual fund

Guarantees provided by annuities are subject to the financial strength of the issuing insurance company; not guaranteed by any bank or the FDIC.

514873 252039

The owner has the ability to take withdrawals (called “partial withdrawals” or “partial surrenders”) from the contract value◦ Doing so may possibly incur a back-end sales charge, called a

“withdrawal charge”

The owner also has the ability to terminate the contract and receive the accumulated value, less any surrender charge

If the owner dies, the owner’s beneficiary receives the “death benefit,” which is usually equal to the contract value◦ The beneficiary has no rights under the contract, other than to receive

the death benefit◦ Most carriers do not assess a withdrawal charge on the death benefit

614873 252039

Tax deferred growth

Safety of principal and earnings

Guaranteed minimum interest rate

Long-term accumulation vehicle

May avoid probate with current beneficiary designation

Protected from creditors (varies by state)

Liquidity options

Flexible income payouts

No limits on contributions (non-qualified annuities)

There is no additional tax deferral benefit for contracts purchased in an IRA or a tax-qualified plan, since these are already afforded tax-deferred status. Therefore, an annuity should only be purchased if the client values some of the other features of the annuity. Guarantees provided by annuities are subject to the financial strength of the issuing insurance company; not guaranteed by any bank or the FDIC. Annuities contain limitations including withdrawal charges, fees and a market value adjustment which may affect contract values. Guaranteed principal assumes no withdrawals in excess of the free amount.

714873 252039

Ways that Your Annuity Value Can Grow

814873 252039

There are three different types of annuities

They differ primarily in how your contract value has the opportunity to grow◦ Fixed annuity: credits a fixed interest rate declared by the insurance

company

◦ Fixed Indexed annuity: credits interest based on a portion of upward movement of a stock market index

◦ Variable annuity: is invested in stock, bond, or other sub-accounts that can increase or decrease in value daily based on the market performance and underlying funds

All three types offer tax deferral of growth

Tax-deferral offers no additional value if an annuity is used to fund an IRA; purchase an annuity for reasons other than tax-deferral benefits beyond those inherently provided by an IRA, such as lifetime income and a death benefit.

914873 252039

Fixed Annuity◦ Contractually guarantees that your principal is protected from loss,

subject only to a surrender charge, which is an avoidable charge

◦ Credits a fixed interest rate that is declared in advance by the company and is typically guaranteed not to change for one or more years at a time

After that initial guarantee period, the interest rate is subject to change by the carrier and is typically set at the carrier’s sole discretion

◦ Has a liquidity restriction in the form of a withdrawal charge which is assessed against large withdrawals or total cancellation in the early years of the contract

1014873 252039

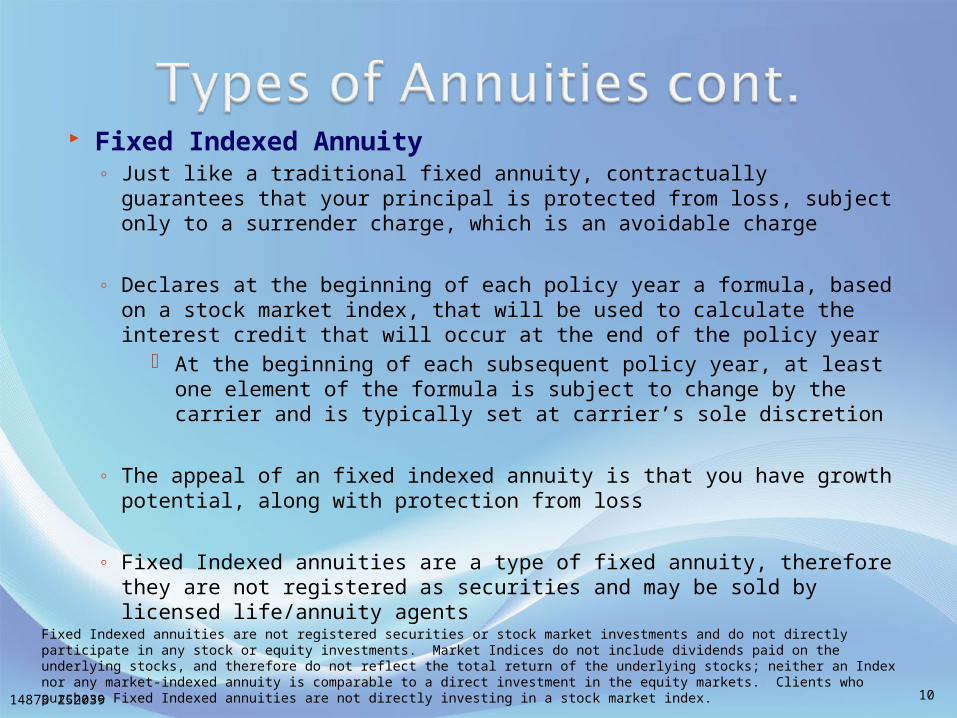

Fixed Indexed Annuity◦ Just like a traditional fixed annuity, contractually guarantees that your

principal is protected from loss, subject only to a surrender charge, which is an avoidable charge

◦ Declares at the beginning of each policy year a formula, based on a stock market index, that will be used to calculate the interest credit that will occur at the end of the policy year

At the beginning of each subsequent policy year, at least one element of the formula is subject to change by the carrier and is typically set at carrier’s sole discretion

◦ The appeal of an fixed indexed annuity is that you have growth potential, along with protection from loss

◦ Fixed Indexed annuities are a type of fixed annuity, therefore they are not registered as securities and may be sold by licensed life/annuity agents

Fixed Indexed annuities are not registered securities or stock market investments and do not directly participate in any stock or equity investments. Market Indices do not include dividends paid on the underlying stocks, and therefore do not reflect the total return of the underlying stocks; neither an Index nor any market-indexed annuity is comparable to a direct investment in the equity markets. Clients who purchase Fixed Indexed annuities are not directly investing in a stock market index.

1114873 252039

Variable Annuity◦ Allows the owner to choose from a variety of mutual fund-like sub-

accounts, such as bond and stock accounts, which can increase or decrease in value daily, along with a menu of standard and optional benefits that can provide important and valuable protections against loss

◦ Can provide a hedge against inflation and an increased opportunity for growth, but there is also a risk the investment performance will be poor and the annuity’s value will be reduced or lost

◦ Variable annuities are securities, thus to sell them you must hold a valid FINRA Series 6 and state license series 63 where required

1214873 252039

This hypothetical example is for illustration purposes only and is not indicative of past, nor intended to predict future performance of any Index or annuity. This example includes the optional restart of the Accumulation Period at the end of the 10th Contract Year. The Income Account Value may not quadruple if you do not elect the restart. The owner is responsible for electing the restart.

1. What is your tax rate? 28%2. What rate would you like to earn?

6%3. How much can you invest?

$100,000

1314873 252039

$142,429

$162,889

$169,979

$207,293

$265,330

$202,859

The illustration assumes a $100,000 payment, a 5.0% interest rate, and a 28% tax bracket. It is important to remember that money distributed from an annuity will be subject to taxation at that time.

This hypothetical example is for illustration purposes only and is not indicative of past, nor intended to predict future performance of any Index or annuity product. Tax-deferral offers no additional value if an annuity is used to fund an IRA; purchase an annuity for reasons other than tax-deferral benefits beyond those inherently provided by an IRA, such as lifetime income and a death benefit.

1414873 252039

Benefits of Owning an Annuity

1514873 252039

The following provisions might not be available on all contracts and there might be an extra charge:

Withdrawal Privileges

Guarantee Return of Premium

Disability Waiver

Terminal Illness Waiver

Nursing Home Waiver

Lifetime Income Options Waiver availability varies by State; additional limitations may apply. Guarantees provided by annuities are subject to the financial strength of the issuing insurance company; not guaranteed by any bank or the FDIC.

1614873 252039

Benefits Fixed or Index

Annuity

Money Market

CD Corporate Bond

Contractual Protection

from Loss of Value

Ability to Add Money

at Any Time

Tax Deferral

No Fees Required To Purchase

X

XXX XX X

Comparison of BenefitsComparison of Benefits

Legend: =Benefit Included X=Benefit Not Included

X

1714873 252039

Details on Annuity Taxation

This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice. Please consult with a professional specializing in these areas regarding the applicability of this information to your situation.

1814873 252039

This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

Non-qualified Plans

An annuity purchased by an individual to meet retirement income needs. Non-qualified contributions are made with after-tax funds, interest accumulations grow tax-deferred until withdrawn. The policyholder has already paid income taxes on the money that is placed into this policy. When the money is taken out, taxes are paid on the “gain.”

Qualified Plans

A retirement plan offered by an employer and established under the federal income tax code which permit the exclusion of plan contributions from current income tax (pre-tax funds). Interest accumulates tax-deferred until it’s withdrawn. Examples: 401K and 403b

Tax-Advantaged AnnuitiesOffer similar tax benefits as employer-sponsored qualified plans, but they set up and owned by an individual. Examples: IRAs & SEPs

1914873 252039

Section 1035 Tax-Free Exchange

Rollover Transfer

This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

2014873 252039

1. The original investment, paid for with after-tax dollars represents the cost basis in the annuity and will be returned tax free.2. The untaxed earnings on the principal will be subject to tax.

Non Taxable Portion

Cost Basis

Taxable Portion

Tax Authority

This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

2114873 252039

Accumulation Annuities

Taxation

•Interest is tax-deferred

•No tax until withdrawal

•Principal is never taxed

(non-qualified)

•10% Federal penalty may

apply on withdrawals prior to age

59 ½

•1035 tax-free exchanges

Most annuities allow you to take unscheduled partial or full withdrawals from your annuity contract. If you make such a withdrawal, for tax reporting purposes, you are deemed to be withdrawing any untaxed interest or growth first, and any untaxed amounts must be exhausted before you are deemed be withdrawing non-taxable cost basis.

Annuities also optionally allow you to receive the proceeds of your annuity as a series of scheduled periodic payments over a period of years. The rules in section 72 of the Internal Revenue Code govern the income taxation of such payments. In general, section 72 permits you to recover your non-taxable cost basis in the contract on a pro rata basis over your life expectancy. To achieve this, each annuity payment is divided into two parts:1. The nontaxable portion that represents the return of premiums paid into the annuity (cost basis).2. The taxable portion that represents the interest earnings that were not taxed previously during the accumulation period.This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon

for, accounting, legal, tax or investment advice.

2214873 252039

This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

Source: Internal Revenue Service Publication 575 – Pension and Annuity Income.

2314873 252039

Taxable + Penalty

Not Taxable, No Penalty

The 10% penalty for withdrawals prior to age 59½ does not apply in the case of death, disability, or lifetime payouts. Withdrawals in excess of the contract’s free amount may not be credited with interest for that term, are subject to withdrawal charges which may result in the loss of principal if taken during the first 5-10 years of the contract. This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

2414873 252039 24

Annuity IRA 401(k) Securities

Original Investment

Not deductible

Maybe deductible

Made with pre-tax dollars

Not deductible

Earnings Tax-deferred

Tax-deferred Tax-deferred

Taxable unless in tax-exempts

Distributions

Partially taxable

Taxable, except for

nondeductible contributions

Taxable Both earnings and capital gains are taxable

Estate Tax Included in gross estate

Included in gross estate

Included in gross estate

Included in gross estate

This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice. Tax consequences may vary by state.

2514873 252039

Annuitization

2614873 252039

At some point, the owner (or, after the owner’s death, the beneficiary) may come to prefer to receive the value of the annuity as a stream of income

The owner can always choose to simply take partial withdrawals from the annuity’s contract value instead of annuitizing the contract

Or, the owner can choose to “annuitize” the contract, that is, trade the contract value to the insurance company in exchange for a guaranteed stream of income◦ After the trade, the account value becomes zero, but the insurance

company is obligated to make the promised payments◦ Payments are made to the “annuitant,” who is usually the same person

as the owner

AnnuitizationAnnuitization

2714873 252039

Annuitization cont.Annuitization cont.

Premium Payments

Growth Period

“Annuitization” or Payout Period

Annuity Starting Date:Account Value is Traded In

Account Value

2814873 252039

Life Only: The annuitant receives payments for as long as he or she lives with all payments stopping when the annuitant dies.

Life with a Period Certain: The annuitant receives payments for as long as he or she lives. If the annuitant dies within the certain period (for example, 20 years), the remainder of the certain period payments will continue to a stated beneficiary.

Period Certain: Rather than having payments tied to the lifetime of the annuitant, the annuitant receives payments over the specified period chosen. If the annuitant dies within the certain period, the remainder of the certain period payments will continue to a stated beneficiary.

Annuitization OptionsAnnuitization Options

2914873 252039

Joint and Survivor: The annuitant and the chosen survivor receive the annuity payments for as long as they are alive. Upon death of one of the named individuals, a percentage of the annuity will continue to be paid to the survivor for as long as he/she lives. The percentage can be as high as 100% of the payout or can be reduced to a lower selected percentage. The spouse is the most commonly selected beneficiary.

Annuitization Options cont.Annuitization Options cont.

3014873 252039

Account Value at the time of annuitization Gender

◦ Statistics show that females live longer than males; therefore, the amount paid monthly to a female is less than to a male.

Age◦ The younger age at which a policy owner elects to “annuitize,”

the longer the payments will be made to the annuitant. The longer the payout period, the lower the monthly payments.

Interest Rate◦ The higher the interest rate the insurance company expects to

earn after the trade, the higher the initial monthly payments will be.

Annuity payout option◦ The more guarantee chosen, the higher the minimum payout by

the insurance company, and the lower the monthly payments made to the annuitant.

3114873 252039

After annuitization, unless the annuity is part of a tax-qualified plan or an IRA:

Each payment is taxed as partly interest and partly return of principal◦ The “exclusion ratio” is the portion of each payment that is considered

return of principal and is thus not considered taxable income◦ The remainder of each payment is considered interest and is thus

reported as taxable income

Taxation After AnnuitizationTaxation After Annuitization

This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

3214873 252039

Investment in the Contract

Expected ReturnEXCLUSION RATIO =

Investment in the contract is the total of premiums paid minus any interest received. This amount is alsominus any other amounts received under the contract that were excluded from gross income as a tax-freerecovery of cost basis. If the contract has a refund feature or unpaid policy loan, the investment in the contract is reduced by the value of the refund feature or the unpaid loan.

Expected return is the estimated or actual amount to be received under the contract. For a fixedannuity, simply multiply the periodic payment amount by the number of periods it will be paid, based on the annuitants life expectancy. The expected return multiples are determined from the IRS tables or from the installment amount and period, whichever is appropriate.

Exclusion Ratio formula

This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

3314873 252039

Premiums(Accumulation Period)

Income(Payout Period)

Tax deferredgrowth

Designatedin Agreement

Policy Owner or Annuitant Insurance Company

Beneficiary(s)

•Greater income•No greater tax•Income that cannot be outlived•Creditor proof

Death benefit paid to designated beneficiary(s)

This material has been prepared for informational and educational purposes only. It is not intended to provide, and should not be relied upon for, accounting, legal, tax or investment advice.

3414873 252039

Summary

3514873 252039

The information contained herein is based on our current understanding of federal tax laws as they relate to life insurance and/or annuities or other subject matter discussed. These laws are subject to change in the future. Please consult your own personal advisor for legal, tax or accounting advice.

![Licensing MotorcycleRiders’ Handbookironbrothersmc.com/motors/[Riders' book]/Riders' handbook.pdf · MotorcycleRiders’ Handbook. Motorcycle Riders’ Handbook Learner Approved](https://static.fdocuments.net/doc/165x107/5a7801147f8b9ad22a8e985c/licensing-motorcycleriders-ha-riders-bookriders-handbookpdf-motorcycleriders.jpg)