1311 aqua chile's corporate presentation 0

47

Pág. Nº1 AQUACHILE Corporate Presentation 2013 EMPRESAS AQUACHILE S.A.

-

Upload

valdinei-farias -

Category

Food

-

view

147 -

download

1

Transcript of 1311 aqua chile's corporate presentation 0

Pág. Nº1AQUACHILE

Corporate Presentation

2013

EMPRESAS AQUACHILE S.A.

Pág. Nº2AQUACHILE

Pág. 03

Pág. 09

Pág. 28

Pág. 36

Pág. 40

INDEX

01 Overview

02 About AquaChile

03 Industry Performance & New Regulation

04 Sustainability and Stakeholders

05 New Developments

Pág. Nº3AQUACHILE

01

Overview

Pág. Nº4AQUACHILE

AquaChile is a Chilean company that

produces and commercializes Atlantic

Salmon, Pacific Salmon, Sea Trout and Tilapia.

Empresas AquaChile at a glance.

Source: Infotrade

It owns inland farms in Costa Rica and

the only three farming licenses granted

in the Bayano Lake in Panama to

produce Tilapia.

It has operations in Chile, Costa Rica, Panama

and a commercial office in the United States.

It is the largest producer in Chile of Salmon

and Sea Trout. It owns 150 sea licenses which

provide a solid basis for its growth.

It has more than

230customers in

30countries.

Pág. Nº5AQUACHILE

Main Shareholders:

Puchi and Fischer Families

Public since

May 19th, 2011

Market capitalization of

USD 578 millionsas of October 30, 2013

Empresas AquaChileat a glance.

Shareholder’s Structure**

Fischer Family

33,03%

Puchi Family

33,03%Pension Funds

4,53%

Others

29,41%

Others

33,95%

Source: The Company

*As of October 30, 2013 ** As of September 30, 2013

578

283 281163 143

34

Chilean Salmon Companies by

Market Cap (MUSD)*

Source: Bloomberg

Pág. Nº6AQUACHILE

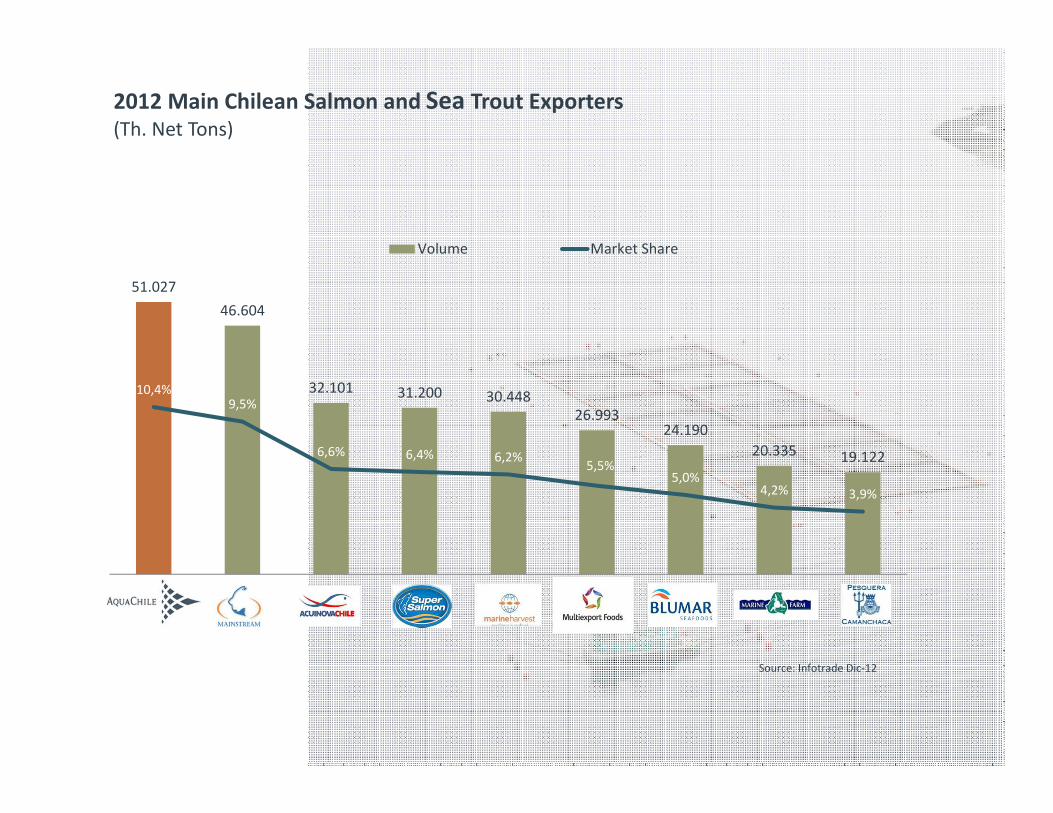

2012 Main Chilean Salmon and Sea Trout Exporters

(Th. Net Tons)

51.027

46.604

32.101 31.200 30.448

26.99324.190

20.335 19.122

10,4%9,5%

6,6% 6,4% 6,2%5,5%

5,0%4,2% 3,9%

Volume Market Share

Source: Infotrade Dic-12

Pág. Nº7AQUACHILE

Annual SalesIn MUSD

Source: The Company

25 years of succesful track record.

Crisis

• ISA virus effects• Financial restructuring• New legal framework focused

in long term sustainability• Advantages of diversification

2006 – 2007 Period

• 3rd largest world producer• Global presence and

reputation• IPO and acquisition plans

Beginnings

• 25 years of history• Merger with Salmones Pacífico

Sur • Track record forming strategic

alliances• Sustained growth

Today

• Diversified business model• Vertical integration• High growth potential• Industry consolidation capacity

RevenuesIn MUSD

2012

410

Pág. Nº8AQUACHILE

19%

36%

20%

25%

17%

31%

16%

15%

Atla

ntic

Sal

mon

Sea

Tro

utP

acifi

c S

alm

onT

ilapi

a

Bayano Lake Guanacaste

X and XI Region

Source: The Company as of December 31, 2012

X and XI Region

X and XI Region

Focus indiversification for success.

% of Consolidated Sales (US$ )

% of Consolidated Sales (tons)

Geographic Diversification

Pág. Nº9AQUACHILE

02

AquaChile

Pág. Nº10AQUACHILE

AquaChile:Strong organic growth plan based on unique assets

Fresh Water: Flexibility and excess installed capacity

Processing: Installed capacity to absorb growth

Vertical integration throughout the value chain

Sea Water: High quality and diversified license portfolio

Global presence and reputation

Pág. Nº11AQUACHILE

Sea water:Unique, diversified and large license portfolio.

One of the largest sea licenses base and the largest presence within sanitary areas in the Chilean industry.

150*Sea licenses distributed in

29 Sanitary Areas

-Geographic distribution

-Organic growth capacity

-Operational and productive continuity

-Continuous supply to clients

-Species diversification

-Natural, climate and sanitary risk diversification

* Include 7 brackish water licenses

Pág. Nº12AQUACHILE

Sea water:Unique, diversified and large license portfolio.

INDUSTRY

Total of 34 sanitary areas

AQUACHILE

95 sea licenses and 17 sanitary areas

50% of sanitary areas of the Aysen Region

Sea licenses Sanitary areas

INDUSTRY

Total of 24 sanitary areas

AQUACHILE

55 sea licenses in 12 sanitary areas

50% of sanitary areas of the Los Lagos Region

Aysen Region

Los Lagos Region

Geographical

diversification in sea

licenses for Salmon

and Sea Trout

production.

Pág. Nº13AQUACHILE

Tilapia Costa Rica & Panama:Large water volume and favorable climate.

Costa Rica

-Strategic access to large volumes of high-quality water

-Optimal location for logistics

-21,000 tons WFE capacity

Panama

-The Company has the only three tilapia farming licenses granted in the Bayano Lake

-Potential to produce over 20,000 ton WFE

Geographical diversification in Tilapia production

Guanacaste

Bayano Lake

Costa Rica

Panama

Pág. Nº14AQUACHILE

AquaChile:Strong organic growth plan based on unique assets

Fresh Water: Flexibility and excess installed capacity

Processing: Installed capacity to absorb growth

Vertical integration throughout the value chain

Sea Water: High quality and diversified license portfolio

Global presence and reputation

Pág. Nº15AQUACHILE

Fresh water:Flexibility and excess installed capacity.

24*hatcheries from the IXth Region to

the XIth Region, including 1 hatchery

near Santiago.

14**fresh water farming licenses in the

Xth and XIth Regions for Sea Trout and

Coho smoltification.

7brackish water licenses in the XIth

Region for Coho smoltification.

* Seven of them are rented under long term contract

** Two of them are rented under long term contract

Geographical

diversification in fresh

water.

1River licenses in the XVth Regions for

Atlantic Salmon smoltification.

Pág. Nº16AQUACHILE

AquaChile:Strong organic growth plan based on unique assets

Fresh Water: Flexibility and excess installed capacity

Processing: Installed capacity to absorb growth

Vertical integration throughout the value chain

Sea Water: High quality and diversified license portfolio

Global presence and reputation

16

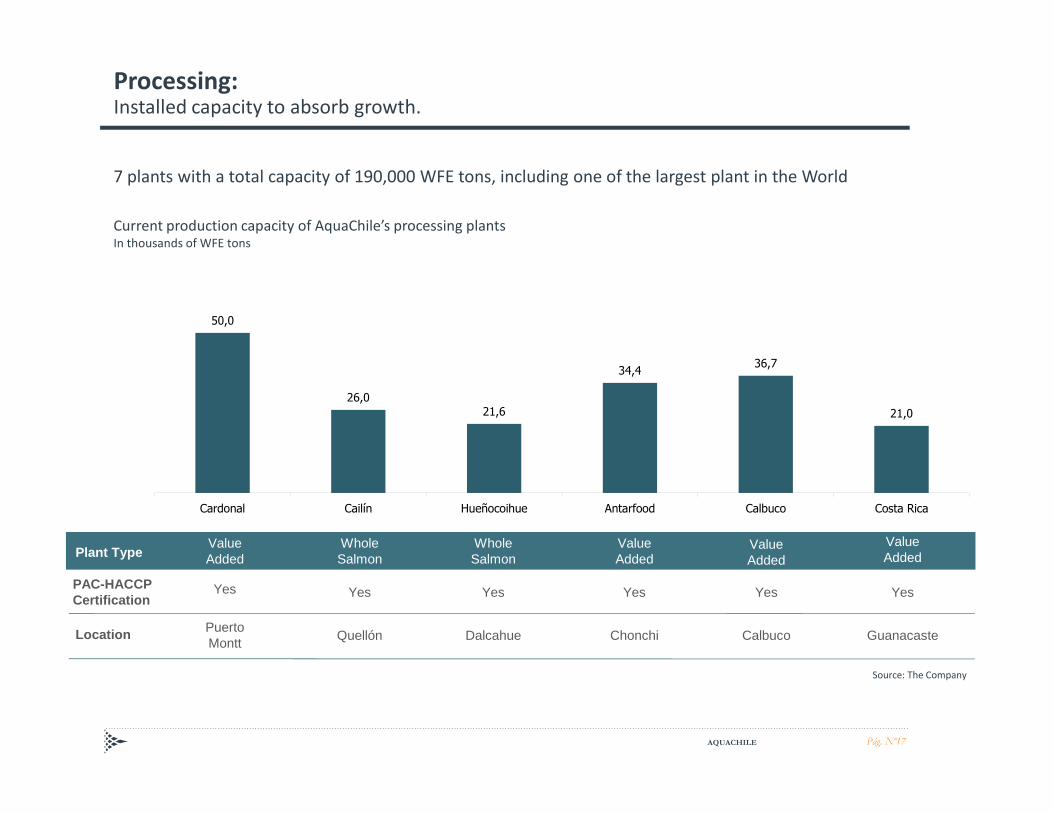

Pág. Nº17AQUACHILE

50,0

26,021,6

34,436,7

21,0

Cardonal Cailín Hueñocoihue Antarfood Calbuco Costa Rica

Current production capacity of AquaChile’s processing plantsIn thousands of WFE tons

7 plants with a total capacity of 190,000 WFE tons, including one of the largest plant in the World

Processing:Installed capacity to absorb growth.

Location Puerto Montt

CalbucoQuellón Dalcahue Chonchi

Plant TypeValue Added

Value Added

Whole Salmon

Whole Salmon

Value Added

PAC-HACCP Certification

Yes YesYes Yes Yes

Value Added

Yes

Guanacaste

Source: The Company

Pág. Nº18AQUACHILE

Diversity of Salmon Products

Whole HG Trim C

PortionsTrim ETrim D

Whole

Breaded Fillets

Fillets

Diversity of Tilapia Products

Processing:Installed capacity to absorb growth.

Chile Costa Rica

Pág. Nº19AQUACHILE

AquaChile:Strong organic growth plan based on unique assets

Fresh Water: Flexibility and excess installed capacity

Processing: Installed capacity to absorb growth

Vertical integration throughout the value chain

Sea Water: High quality and diversified license portfolio

Global presence and reputation

Pág. Nº20AQUACHILE

GENETICS

FRESH WATEREggs & Smolts

SEA WATERFarming

PROCESSING COMMERCIALIZATION

FEED

SALMON AND

SEA TROUT

TILAPIA

Vertical integrationtroughout the value chain.

INTEGRATION AquaChile is vertically integrated in the Salmon and Tilapia business.

The Company adds value to all of its productive chain, from genetics up to commercialization.

FRY PRODUCTION

GENETICS

FARMING

FEED*

PROCESSING COMMERCIALIZATION

FEED

Pág. Nº21AQUACHILE

Source: The Company

Universidad

de Chile

0,12%

AquaChile

99,88%

Increase in harvest weight of the Pacific SalmonIn WFE kg

∆+40%

Aquainnovo: Created to be a world class center for genetic improvement in aquaculture

Source: The Company Source: The Company

Improvement in Tilapia conversion factor of ACI Group Reduction in the Tilapia’s on growing cycleIn number of days

Δ-36%Δ-21%

Genetics:15 years of succesfull and proven genetic development.

Pág. Nº22AQUACHILE

Genetics in Salmon and Sea Trout Genetics in Tilapia

Genetics:15 years of succesfull and proven genetic development.

Pág. Nº23AQUACHILE

Fish feed plant:State of the art assets to feed our fish.

Joint venture with Biomar in Chile, one of the

world’s leading suppliers of high performance

fish feed.

126,000 tons of installed capacity.

Modular design allows the company to double

its output capacity.

Pág. Nº24AQUACHILE

AquaChile:Strong organic growth plan based on unique assets

Fresh Water: Flexibility and excess installed capacity

Processing: Installed capacity to absorb growth

Vertical integration throughout the value chain

Sea Water: High quality and diversified license portfolio

Global presence and reputation

Pág. Nº25AQUACHILE

AquaChile has over 230 clients in more than 30 countries in the five continents

We have more than 19 years of experience in Asia and over 20 years in the fresh salmon market

Source: The Company

Destination of AquaChile’s main Salmon, Sea Trout and Tilapia salesIn net tons

Commercialization:Global presence and reputation.

Operations

Salmon and Sea Trout sales 2012 (net tons)

Tilapia Sales 2012 (net tons)

Salmon

Tilapia

3.690

1.012

810

274

16.577

54

127

21

84

23

127

78

6.870

127

793

1.859

6.709

157

132

2.018

5.563

146

32 1.230

867

2.094

,

1.505

268

Pág. Nº26AQUACHILE

The only Salmon & Tilapia company with

operations inside Miami International

Airport

Improved cold chain

Less handling involved

AquaChile Inc:Servicing the United States from Miami.

Experienced customer service

Reliability and commitment

We deliver!

Pág. Nº27AQUACHILE

Renowned Brands Reputable Clients

Our brands andour main clients.

Pág. Nº28AQUACHILE

03

Industry

Performance &

New Regulation

Pág. Nº29AQUACHILE

1,20%0,70%

1,65%

0%

5%

10%

15%

20%

ag

o-0

8

dic

-08

ab

r-0

9

ag

o-0

9

dic

-09

ab

r-1

0

ag

o-1

0

dic

-10

ab

r-1

1

ag

o-1

1

dic

-11

ab

r-1

2

ag

o-1

2

dic

-12

ab

r-1

3

ag

o-1

3

Pacific Salmon Atlantic Salmon Sea Trout

Chilean industryProductivity performance

Significant mortality reduction in the industry since 2009

Sea lice level increasing according to the increase in the industry biomass

Source: Aquabench

Monthly mortality rates

(%)

0,6

7,45,9

0

10

20

30

40

50

60

70

ma

r-0

7

jul-

07

no

v-0

7

ma

r-0

8

jul-

08

no

v-0

8

ma

r-0

9

jul-

09

no

v-0

9

ma

r-1

0

jul-

10

no

v-1

0

ma

r-1

1

jul-

11

no

v-1

1

ma

r-1

2

jul-

12

no

v-1

2

ma

r-1

3

jul-

13

Pacific Salmon Atlantic Salmon Sea Trout

Sea lice monthly monitoring 2007-2013

(Number of sea lice per fish)

Source: Aquabench, Sernapesca

Pág. Nº30AQUACHILE

Ova imports with no restrictions.

Non-existence of biosecurity standards.

Low-quality Smolts.

Inadequate regulation.

Excessive densities.

Non-interrupted cycles, with no fallowing.

Deficient coordination among production sites.

Low usage and low quality vaccines.

0%

5%

10%

15%

20%

mar-08 ago-08 ene-09 jun-09

Pacific Salmon Atlantic Salmon

Sea Trout

0

20

40

60

80

mar-07 ago-07 ene-08

Pacific Salmon Atlantic Salmon

Sea Trout

Monthly mortality rates

(%)

Sea lice monthly monitoring

(Number of sea lice per fish)

Con

sequ

ence

s

Sea lice Crisis

ISAv Crisis

Origin of the sanitary crisis:

Pág. Nº31AQUACHILE

New regulationsStructural Changes in the Industry: Controlling Risk

AS: Atlantic Salmon; ST: Sea Trout; PS: Pacific Salmon

Fresh water AS ST PS

Restrictions and new sanitary protocols on egg imports and hatchery use ✓✓✓

Individual Screening of Broodstock ✓✓✓

Affluent and effluent treatment ✓✓✓

Land based hatcheries ✓

Safe mortality disposal ✓✓✓

Standardization and validation of diagnostic laboratories ✓✓✓

Smolts: ISA free certification before transferring to the sea ✓✓✓

Safeguards and optimization of freshwater production ✓✓✓

Clear and strong disinfection protocols ✓✓✓

Sea water AS ST PS

Sanitary areas ✓✓✓

Operating and fallowing schedules in sanitary areas ✓✓✓

Macrozone definition: 4 in the Xth Region and 3 in the XIth Region ✓✓✓

Corridors definition between macrozones(5 miles) ✓✓✓

Minimum distance between licenses (1.2-1.7 miles) and sanitary areas (3.5 miles)

✓✓✓

Re-location of licenses located in corridors ✓✓✓

New licenses granted for 25 years with the option to be renewed ✓✓✓

Sanitary zoning for diseases ✓✓✓

Strengthening of control powers (biomass stamping out in case of disease) and forfeiture conditions of the farming licenses

✓✓✓

Establishment of specific sanitary programs for ISA, Sea Lice and SRS ✓✓✓

Pág. Nº32AQUACHILE

AS: Atlantic Salmon; ST: Sea Trout; PS: Pacific Salmon

Sea water (Cont..) AS ST PS

Improved adherence of legal framework regarding sanitary and environmental issues ✓ ✓ ✓

Coordinated programs for sea lice control ✓ ✓

Safe mortality disposal ✓ ✓ ✓

No fish movements between marine sites ✓ ✓ ✓

Restrictions and new sanitary protocols for wellboats ✓ ✓ ✓

Application of maximum farming densities in the sanitary areas ✓ ✓ ✓

Standardization and validation of diagnostic laboratories ✓ ✓ ✓

Re-location allowed in the XIth Region ✓ ✓ ✓

License application suspended in the Xth and XIth Region until 2015 ✓ ✓ ✓

Penalties increase (penalty equal to economic value of biomass) ✓ ✓ ✓

Increase in patents: more resources for research ✓ ✓ ✓

New regulationsStructural Changes in the Industry: Controlling Risk

Pág. Nº33AQUACHILE

AS: Atlantic Salmon; ST: Sea Trout; PS: Pacific Salmon

Final steps on the legal framework : pending final decree AS ST PS

Flexibility in the fallowing period of licenses

• Extended fallowing periods without expiring dates

• Licenses located in corridors allowed to stand by without expiring✓ ✓ ✓

Density restriction per license

Biosafety qualification regarding mortality records from the last productive cycle

• Low mortality: maximum allowed density

• High mortality: stocking restrictions

✓ ✓ ✓

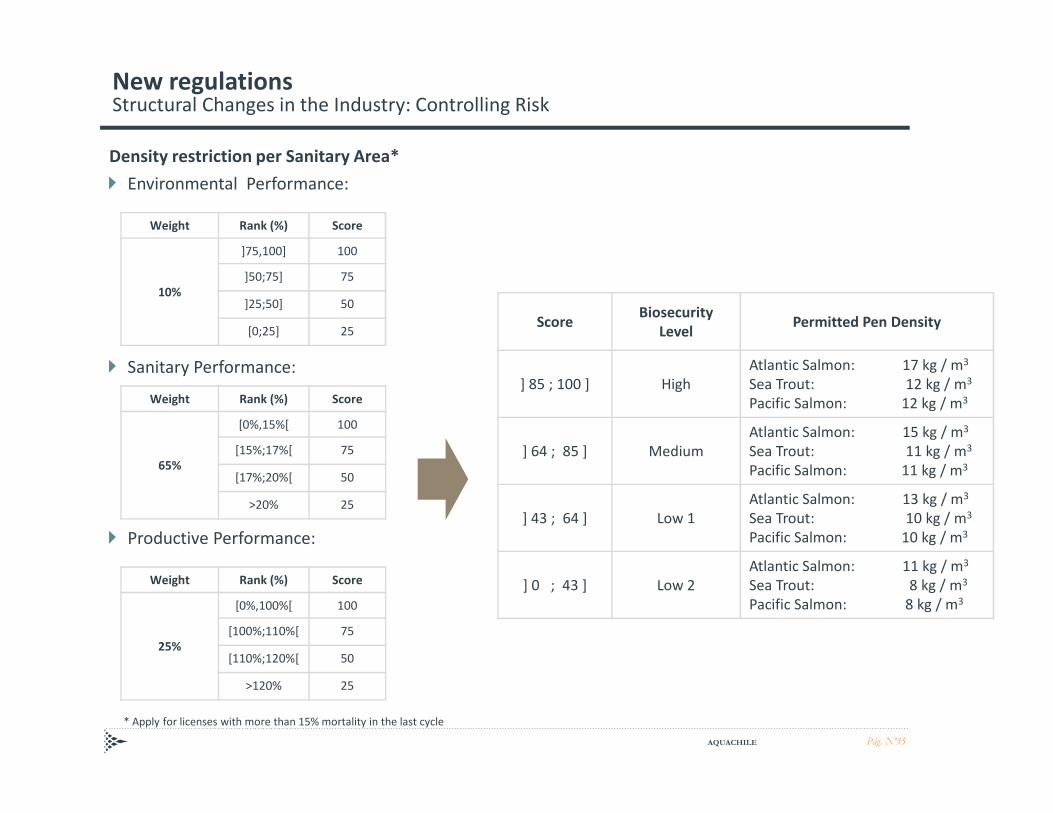

Density restriction per sanitary area

• The sanitary area density will determine the maximum number of fish to stock in each pen, except

those licenses with low mortality performance during the last productive cycle (less than 15%)

• The density will be determined by:

• Environmental performance (10%): Number of licenses presenting aerobic conditions at the end

of the productive cycle

• Sanitary performance (65%): Total mortality within the last period

• Productivity performance (25%): Stocking intention in the sanitary area compared with the

optimal stocking

• Optimal stocking in the sanitary area depends of the mortality in the last productive cycle.

• Low mortality: optimal stocking increase in 16%

• High mortality: optimal stocking decrease 24%

✓ ✓ ✓

New regulationsStructural Changes in the Industry: Controlling Risk

Pág. Nº34AQUACHILE

New regulationsStructural Changes in the Industry: Controlling Risk

Density restriction per License

MortalityBiosecurity

LevelNext Cycle Smolt stocking

] 0% ; 15% ] High Maximum allowed density

] 15% ; 18% ] Medium High 10% smolt stocking reduction

] 18% ; 22% ] Medium 20% smolt stocking reduction

] 22% ; 26% ] Low 1 40% smolt stocking reduction

> 26% Low 2 60% smolt stocking reduction

Pág. Nº35AQUACHILE

New regulationsStructural Changes in the Industry: Controlling Risk

Environmental Performance:

Weight Rank (%) Score

10%

]75,100] 100

]50;75] 75

]25;50] 50

[0;25] 25

Sanitary Performance:

Weight Rank (%) Score

65%

[0%,15%[ 100

[15%;17%[ 75

[17%;20%[ 50

>20% 25

Productive Performance:

Weight Rank (%) Score

25%

[0%,100%[ 100

[100%;110%[ 75

[110%;120%[ 50

>120% 25

ScoreBiosecurity

LevelPermitted Pen Density

] 85 ; 100 ] High

Atlantic Salmon: 17 kg / m3

Sea Trout: 12 kg / m3

Pacific Salmon: 12 kg / m3

] 64 ; 85 ] Medium

Atlantic Salmon: 15 kg / m3

Sea Trout: 11 kg / m3

Pacific Salmon: 11 kg / m3

] 43 ; 64 ] Low 1

Atlantic Salmon: 13 kg / m3

Sea Trout: 10 kg / m3

Pacific Salmon: 10 kg / m3

] 0 ; 43 ] Low 2

Atlantic Salmon: 11 kg / m3

Sea Trout: 8 kg / m3

Pacific Salmon: 8 kg / m3

Density restriction per Sanitary Area*

* Apply for licenses with more than 15% mortality in the last cycle

Pág. Nº36AQUACHILE

New regulationsStructural Changes in the Industry: Controlling Risk

Final steps on the legal framework : pending final decree AS ST PS

Smoltification in lakes, rivers and brackish water

• Minimum distance between smoltification sites and on growing sites / gathering sites / docks for

aquaculture operations (3 miles)

• Smoltification area must be located in disease free area from list # 2 with specific sanitary control

program

• However Sea Trout and Pacific Salmon smoltification area can be located in surveillance area from list

# 2 with sanitary control program for 3 years

✓ ✓ ✓

Pág. Nº37AQUACHILE

04

Sustainability

and

Stakeholders

Pág. Nº38AQUACHILE

-More than

5,100 employees in Chile, Costa Rica, Panama & United States

-Benefits above legal requirements

-On the job training

-Costa Rica: ISO 14001:2004, OHSAS 18001:2007 and BAP for Global Aquaculture

Alliance, the most demanding at present

-Chile: Global GAP certification in progress

-Social Responsibility Report available (www.aquachile.com/sustainability)

OUR LABOR AND

ENVIROMENTAL

STANDARDS

We are committedto our employees, our clients and the environment.

Pág. Nº39AQUACHILE

-To produce quality, healthy and safe food

-To act in a proactive and respectful way towards the environment

-To develop in a safe and healthy work environment

-To benefit the communities and suppliers in the places where the

company operates

OUR CORPORATE

SOCIAL

RESPONSIBILITY

PRINCIPLES

We are committedto our employees, our clients and the environment.

Pág. Nº40AQUACHILE

We are committedto our employees, our clients and the environment.

Pág. Nº41AQUACHILE

05

New

Developments

Pág. Nº42AQUACHILE

Disease free eggsrecirculation hatchery: Chaicas.

Pág. Nº43AQUACHILE

State of the artresearch facility: Lenca.

Pág. Nº44AQUACHILE

Alejandro Cristian

Verlasso salmon

Verlasso farms

Harmoniously raised fishwww.verlasso.com

Pág. Nº45AQUACHILE

Fish feed in Costa Rica:association with Biomar.

Pág. Nº46AQUACHILE

Pet food flavoring plant:association with SPF.

Pág. Nº47AQUACHILE

Note on forward-looking statements

This report includes forward-looking statements. These may

include words like “anticipates”, “estimates”, “expects”,

“projects”, “intends”, “plans”, “believes” or other

comparable expressions. Forward-looking statements do not

represent past events, including statements on the beliefs

and expectations of the company. These statements are

based on current plans, estimates and projections, and

therefore cannot be overrated. Forward-looking statements

entail certain risks and uncertainties. The company notes

that a significant number of factors could result in current

results to differ materially from those contained in any

forward-looking statement. These factors and uncertainties

include in particular those described in the document that

the company submitted to the Chilean Securities and

Insurance Commission (SVS), section on Risk Factors.

Forward-looking statements are related only to the date

when they are made and the company assumes no

obligation to publicly update any such statements in the

presence of new information, future events or otherwise.

This document purports to deliver general information on

Empresas AquaChile S.A. Under no circumstance does it

constitute an exhaustive analysis of the financial, productive,

commercial and health situation of the company, and

therefore any consideration on the advisability of acquiring

or selling securities of the company would require the

interested party to conduct an independent analysis.

In accordance with applicable standards, Empresas

AquaChile S.A. has sent its financial statements and notes to

the Securities and Insurance Commission, which are

available for consultation and analysis on its webpage at

www.svs.cl and also at www.aquachile.com.