13 externality

36

MACRO ECONOMICS- Externality , Public Goods Sonu Chowdhury Faculty- Sangam University

-

Upload

nishank100ny -

Category

Economy & Finance

-

view

115 -

download

1

Transcript of 13 externality

MACRO ECONOMICS- Externality , Public Goods

Sonu ChowdhuryFaculty- Sangam University

THE EFFICIENCY OF PRIVATE EXCHANGE

A private market transaction is one in which a buyer and seller

exchange goods or services for money or other goods or

services.

Voluntary private market transactions will occur between

buyers and sellers only if both parties to the transaction expect

to gain, otherwise that transaction would not occur.

private market transactions are usually considered to be

“efficient” because these transactions result in all the parties

being as well off as possible, given their initial resources.

The argument above for the efficiency of private market

exchanges works well with “pure private goods.”

A pure private good is a good whose production and consumption neither harm nor benefit people uninvolved in its production or consumption.

But some goods are not pure private goods, because they involve externalities. An externality occurs if a person’s activity, such as consumption or production, affects the well-being of an uninvolved person.

The term externality comes from the fact that someone external to the action or transaction is affected by the production of consumption of the good.

Economic functions of Government:

1) Enforce laws and contracts.

3) Redistribute income--providing an economic safety net.

4) Provide public goods

5) Correct Market Failures

-provide market information

-correct negative externalities

-subsidize goods with positive

externalities

6) Stabilize the economy

- fight unemployment

- encourage price stability

- promote economic growth

EXTERNALITIES

Meaning of externality

Externalities are common in virtually every area of

economic activity.

They are defined as third party (or spill-

over) effects arising from

the production and/or consumption of goods and services

for which no appropriate compensation is paid.

The effects of a decision by consumers and producers that has an impact on a third party.

Positive Externalities – beneficial effects on third parties

Negative Externalities – costs incurred by third parties

Positive:An external benefit is imposed on someone.

NegativeAn external cost is imposed on someone. (examples: exhaust from autos, barking dogs, noise from airplanes)

Are there benefits for other people in the parking lot when someone puts their car alarm on?

Your neighbor puts in a nice garden. Are you receiving a benefit?

PUBLIC GOODS

The two most important microeconomic

roles of government are

its role in providing public goods

and its role in dealing with market

failure due to externalities

IMPORTANT TERMINOLOGIES

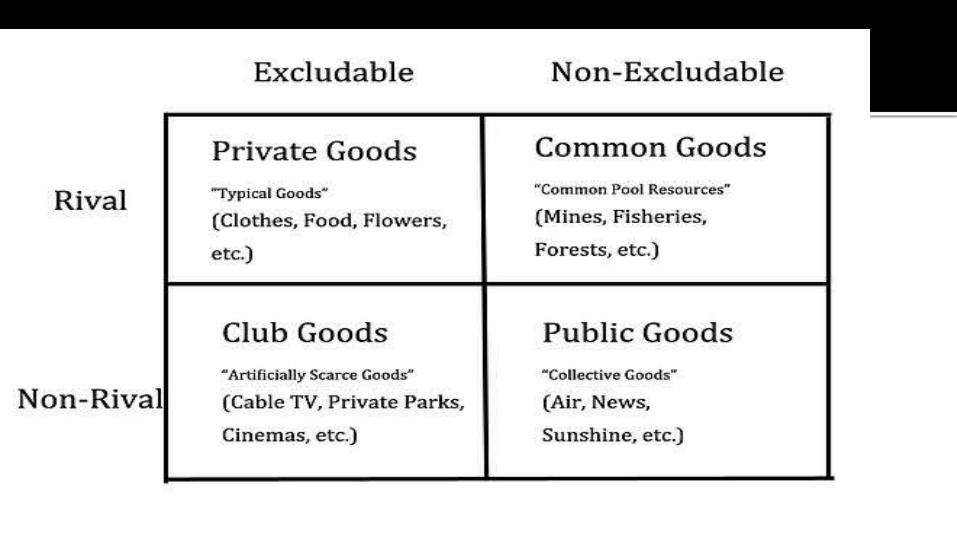

1. RIVALROUS GOODS: Those which can be consumed by only

one person at the same time.

2. NON-RIVALROUS GOODS: Those goods which can consumed

by many at the same time at no additional cost.

3. EXCLUDABLE GOODS: AS good is excludable if it is possible to

prevent some people from enjoying it. If the good is

excludable it is possible to limit the benefit to those who pay

for it.

CHARACTERISTICS OF PUBLIC GOODS

1. Non-rivalry (in consumption):

It means that one person’s consumption of a good does not preclude

consumption of the good by others.

Everyone can simultaneously obtain the benefit from a public good.

Example: national defense, street lighting, or environmental protection.

2. Non-excludability :

It means there is no effective way of excluding individuals from

the benefit of the good once it comes into existence.

For example: national defense, street lighting, a global

positioning system, or environmental protection.

End of the Topic

TAXATION/ TAX BURDEN

A means by which governments finance their expenditure by imposing charges on citizens and corporate entities.

Governments use taxation to encourage or discourage certain economic decisions.

TAX A fee charged ("levied") by a government on a product, income, or activity. If tax is levied directly on personal or corporate income, then it is a direct tax. If tax is levied on the price of a good or service, then it is called an indirect tax.

The purpose of taxation is to finance government expenditure. One of the most

important uses of taxes is to finance public goods and services, such as street

lighting and street cleaning.

TAX BURDEN

The amount of income, property, or sales tax levied on an individual or business.

Tax burdens vary depending on a number of factors including income level, jurisdiction, and current tax rates.

Income tax burdens are typically satisfied by deductions from an individual's paycheck each time he or she is paid

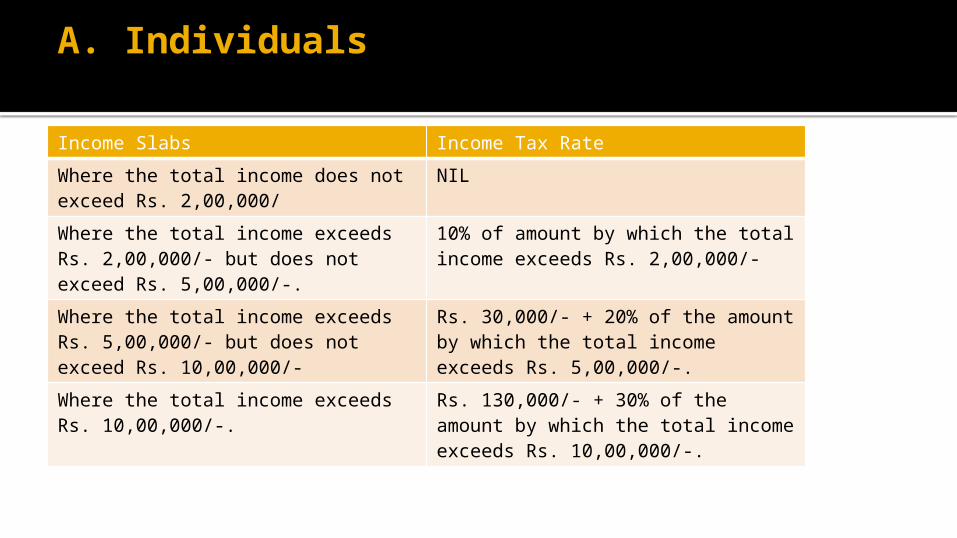

A. Individuals

Income Slabs Income Tax Rate

Where the total income does not exceed Rs. 2,00,000/

NIL

Where the total income exceeds Rs. 2,00,000/- but does not exceed Rs. 5,00,000/-.

10% of amount by which the total income exceeds Rs. 2,00,000/-

Where the total income exceeds Rs. 5,00,000/- but does not exceed Rs. 10,00,000/-

Rs. 30,000/- + 20% of the amount by which the total income exceeds Rs. 5,00,000/-.

Where the total income exceeds Rs. 10,00,000/-.

Rs. 130,000/- + 30% of the amount by which the total income exceeds Rs. 10,00,000/-.

How the burden of tax is shared?

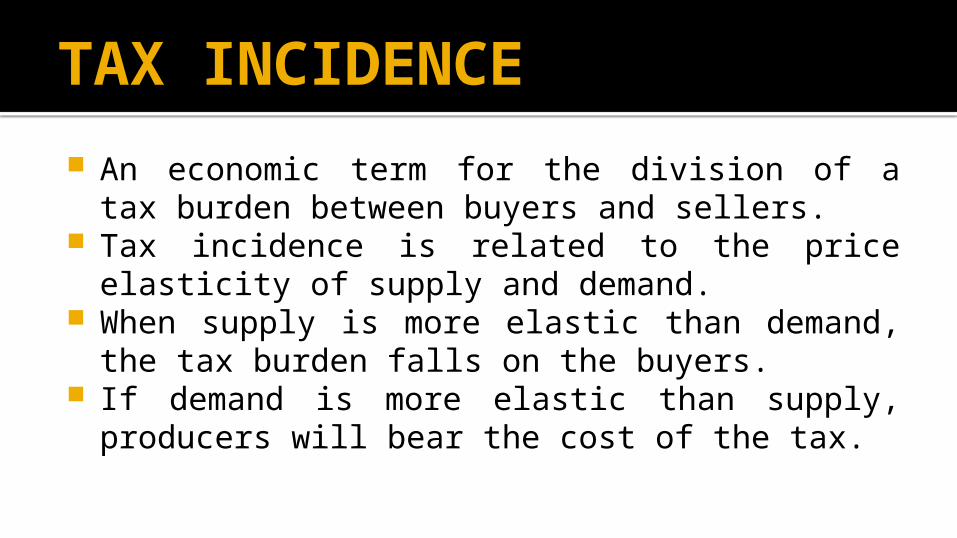

TAX INCIDENCE

An economic term for the division of a tax burden between buyers and sellers.

Tax incidence is related to the price elasticity of supply and demand.

When supply is more elastic than demand, the tax burden falls on the buyers.

If demand is more elastic than supply, producers will bear the cost of the tax.

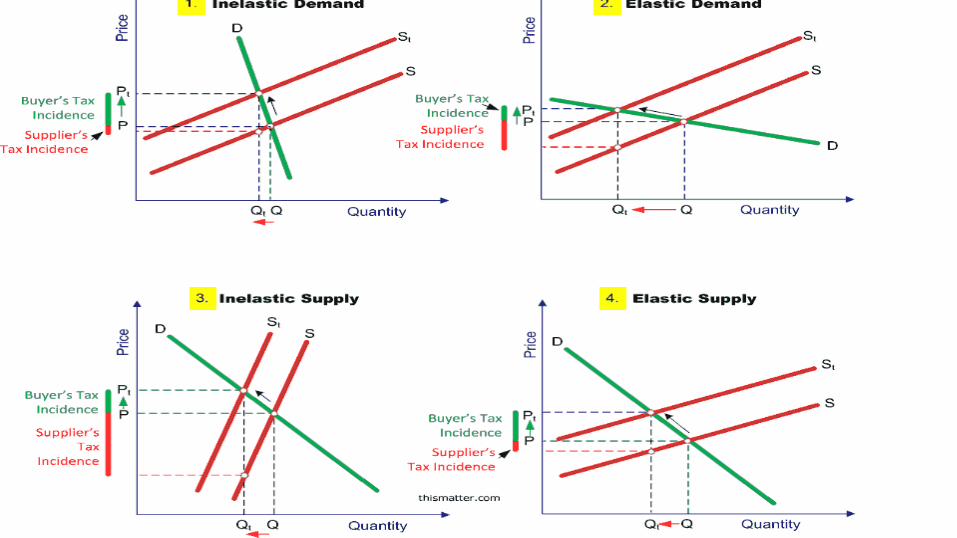

Tax incidence reveals which group, the consumers or producers, will pay the price of a new tax.

For example, the demand for cigarettes is fairly inelastic, which means that despite changes in price, the demand for cigarettes will remain relatively constant. Let's imagine the government decided to impose an increased tax on cigarettes. In this case, the producers may increase the sale price by the full amount of the tax. If consumers still purchased cigarettes in the same amount after the increase in price, it would be said that the tax incidence fell entirely on the buyers.

Tax on a particular product increases its price and decreases the quantity supplied, since suppliers are getting less revenue for their product.

The assessed tax shifts the supply curve upward, from S to St, the price increases from P to Pt, and the quantity declines from Q to Qt. But how the tax incidence, or tax burden, is shared between buyer and seller depends on the elasticity of both demand and supply.

The buyer bears a greater portion of the tax burden when either demand is inelastic or supply is elastic, as depicted in diagrams # 1 and # 4, respectively. When demand is elastic or supply is inelastic, then the seller bears the major portion of the tax, as depicted in diagrams # 2 and # 3, respectively.

TAX SHIFTING

Transferring some or all of a tax burden of an entity (such as a subsidiary) to another (such as the parent firm).

The objective behind tax shifting is to stop taxing the things we do want (like income and savings) and shift towards taxing things people collectively do not want (like waste and pollution).

End of the topic