11068- Islamic Finance - Sourcingfocus · 1 Islamic Finance: from niche to mainstream For many...

12

Islamic Finance: From niche to mainstream

-

Upload

truongkien -

Category

Documents

-

view

215 -

download

0

Transcript of 11068- Islamic Finance - Sourcingfocus · 1 Islamic Finance: from niche to mainstream For many...

Islamic Finance:From niche to mainstream

1

Islamic Finance: from niche to mainstreamFor many years, Islamic finance has been regarded as a niche market by theconventional financial services industry. But the growth and development offinance products generally has enabled competitive Islamic financial productsto be developed. This, combined with the growing affluence of manyMuslims, means it is well worth examining the potential for Islamic finance.

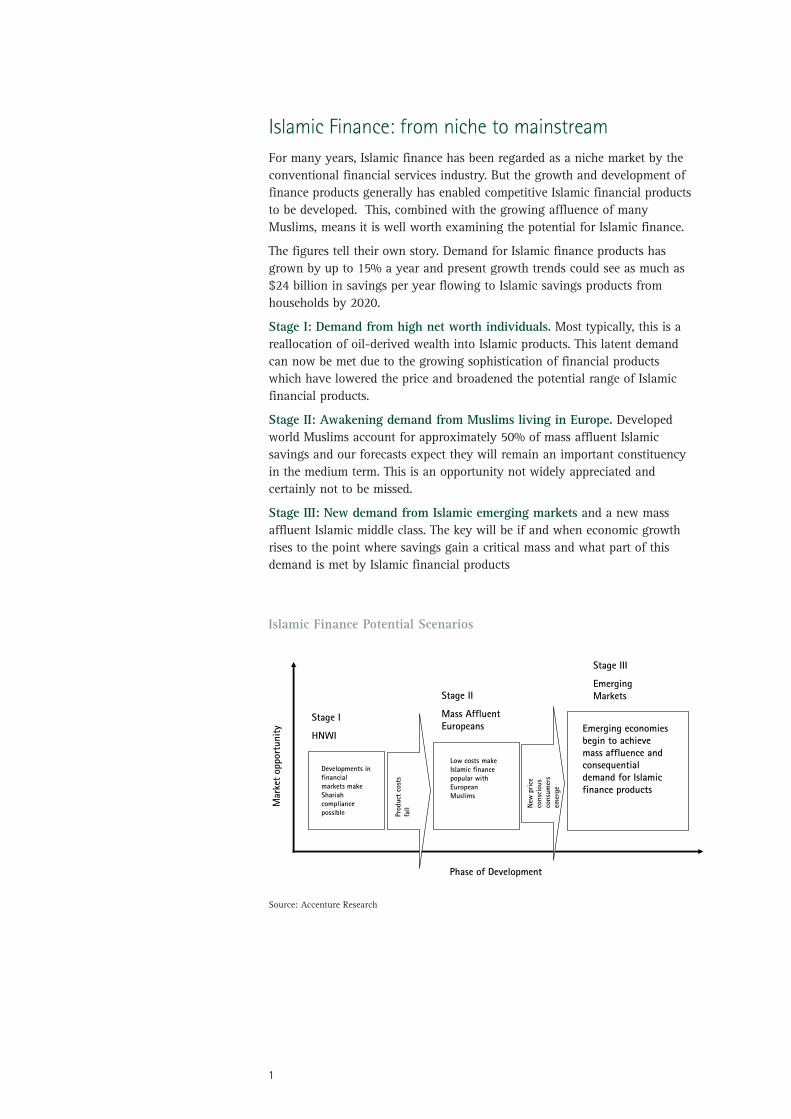

The figures tell their own story. Demand for Islamic finance products hasgrown by up to 15% a year and present growth trends could see as much as$24 billion in savings per year flowing to Islamic savings products fromhouseholds by 2020.

Stage I: Demand from high net worth individuals. Most typically, this is areallocation of oil-derived wealth into Islamic products. This latent demandcan now be met due to the growing sophistication of financial productswhich have lowered the price and broadened the potential range of Islamic financial products.

Stage II: Awakening demand from Muslims living in Europe. Developedworld Muslims account for approximately 50% of mass affluent Islamicsavings and our forecasts expect they will remain an important constituencyin the medium term. This is an opportunity not widely appreciated andcertainly not to be missed.

Stage III: New demand from Islamic emerging markets and a new massaffluent Islamic middle class. The key will be if and when economic growthrises to the point where savings gain a critical mass and what part of thisdemand is met by Islamic financial products

Islamic Finance Potential Scenarios

Phase of Development

Mar

ket

oppo

rtun

ity

Stage I

HNWI

Stage II

Mass Affluent Europeans

Stage III

Emerging Markets

Developments in financial markets make Shariah compliance possible

Low costs make Islamic finance popular with European Muslims

Emerging economies begin to achieve mass affluence and consequential demand for Islamic finance products

Prod

uct

cost

s fa

ll New

pric

e co

nsci

ous

cons

umer

s em

erge

Source: Accenture Research

2

Defining Islamic FinanceThere is no absolute authority (and plenty of debate) as to which particularfinancial practices are allowable under Shariah law, and therefore whatconstitutes “Islamic Finance". Banks and other institutes seeking to marketShariah compliant products must seek a review of their product by Islamicscholars who judge each case on its merits. Having said there is no over-arching law, there are a number of guiding principles for any financialproduct wishing to comply with Shariah law:

• There is a prohibition on usury, which is generally interpreted as a banon interest payments.

• Investments in gambling, pornography, tobacco, pig products andalcohol are all forbidden.

• Finally, Islamic finance is required to focus on real trade andtransactions rather than speculation.

this in context, conventionalinvestment funds have $55,000billion under management, whilehedge funds control $3,000 billion.Looking to the future, StandardChartered has estimated thatsovereign wealth funds could beworth up to $13,400 billion by2017.

Composition of Islamic Finance(2005, %)

Source: Islamic Finance Service Board

Enabling growth with newproducts

Islamic finance as an industry hasbeen benefiting from significantdevelopments within the broadermarket for financial products.Falling costs of complex financialinstruments have enabled banks to

Debate continues over whatconstitutes “Islamic Finance",but general guidelines are clear

Stage I: Capture ofMarket ShareStage I of the growth in Islamicfinance has been under way forsome time. This has been drivenprimarily by demand from HighNet Worth Individuals (HNWI) inMuslim countries, or the sovereignfunds of those countriesthemselves. Where there is demand,banks will create a supply, in thiscase through utilising their widerange of financial instruments inorder to create cost effective,Shariah compliant, Islamicfinancial products.

This demand has been furtherboosted by high oil prices; the IMFestimating that Arab statescollected around $500 billion of oilrevenue in 2006 alone. Much ofthis money is controlled bysovereign wealth funds, which areestimated to amount to $2,800billion, of which approximately60% are controlled by Muslimcountries1. As this capital seeks ahome, Muslim nations andindividuals in the post 9/11 worldare both wary of investing in theUnited States, and increasinglyinterested in investments whichcomply with Shariah law. Placing

Banking Windows

Bank Assets

Shariah StocksFI Assets

Sukukdebt

MalaysianBonds

IslamicFunds

TakafulInsurance

High oil prices haveexpanded demand, whiledevelopments in financialproducts have created asupply of cost effectiveIslamic financial products

1. Sovereign Wealth Funds, Peterson Institute, August 2007.

create a variety of Shariah-compliant financial products whichclosely emulate standard non-Islamic financial products.

Developments of Islamic financeproducts have taken place acrossfour principal areas: insurance;capital markets; wealthmanagement; and retail banking.The interrelation between theseareas is helping to underpin not justthe pace of progress, but also itssustainability over the long term.

• Insurance - recent developmentshave focused on Takaful, a formof Islamic insurance similar toconventional mutual insurance.Takaful provides attractive coverto the historically under-insuredMuslim community, and createsinstitutional demand forShariah-compliant products. Ifrecent growth rates of around20% in Takaful continued, theworld premiums would rise fromjust over $2 billion in 2005 to$7.4 billion by 2015. With majorglobal insurers and reinsurersnow entering the market,together with the UK's first ‘pureplay' Takaful provider, there isscope for expansion into bothLife and Property & Casualtysectors.

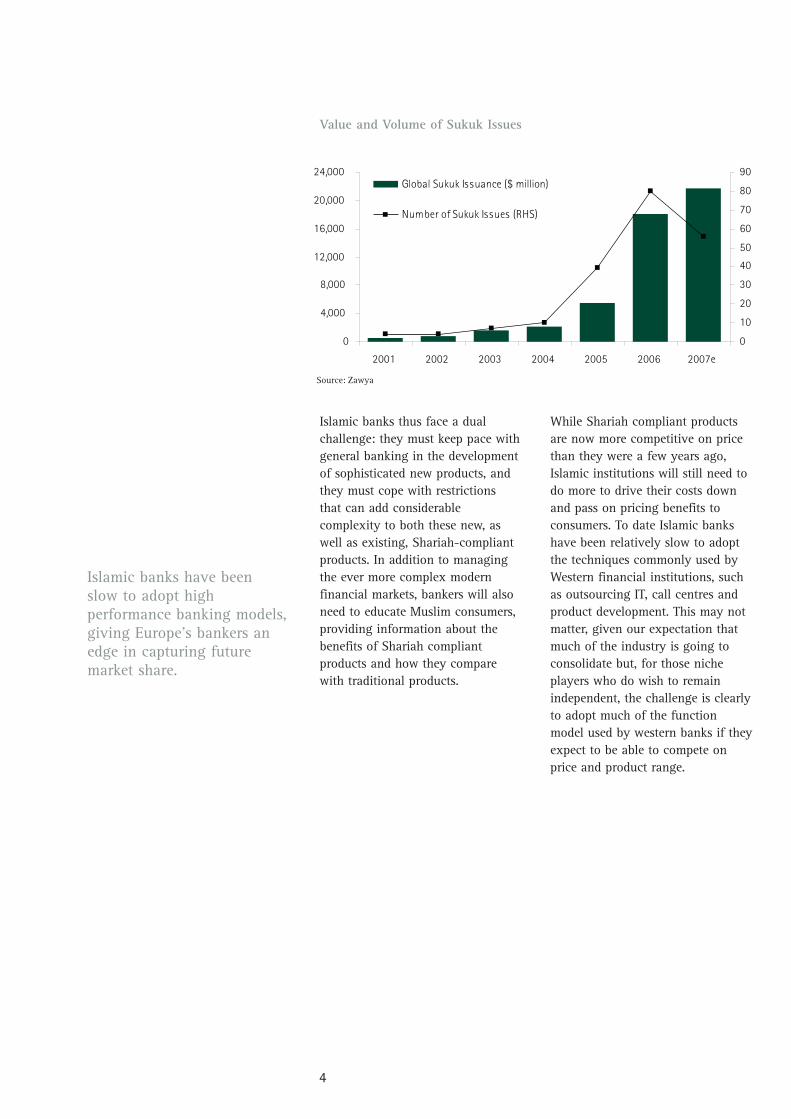

• Capital markets - The growth inTakaful is in turn fuelling Islamiccapital markets, with a risingnumber of global investmentbanks now involved in Islamicproducts including structuredfinance, wealth management,and trade finance. With theSukuk market estimated byBloomberg at $16 billion in2006, Islamic products are alsobecoming more sophisticated,extending to cross-currencyprofit rate swaps, puttable andcallable Musharaka Sukuks,convertible Sukuks, and evenShariah-compliant hedge funds.

• Wealth management - Wealthmanagers and private bankersare another sector gettinginvolved in Islamic finance,distributing Shariah-compliantcapital markets products andtailored structured products tohigh net worth individuals.Traditional money managershave also been innovating inthis area, and in the near futurewe may see the emergence ofShariah-compliant ExchangeTraded Funds (ETFs). Shariah-compliant private equity andreal estate funds are alsobecoming available.

• Retail banking - Even basicIslamic savings instrumentsrequire a degree of cross productco-ordination, which results ingreater complexity than wouldbe present in equivalent non-Islamic financial products. It isbecause the price of financialinstruments is falling, as well asbecause complexity is no longerthe impediment that it once was,that Islamic services haveadvanced from niche tomainstream in markets such asBahrain, Qatar, United ArabEmirates, Kuwait and Malaysia.

At present many of thedevelopments in regional markets,such as the Middle East andMalaysia, have been driven by alarge numbers of small focusedplayers. Many of these smallerbanks are now realising that theylack the scale to compete in such afast-growing and competitivemarketplace, opening the way tosignificant consolidation.

3

Islamic finance has fourdistinct areas: insurance;capital markets; wealthmanagement and retailbanking

Today's market has a largenumber of small playerswho have developed nichecapabilities in developingand selling Islamic financeproducts

4

Islamic banks thus face a dualchallenge: they must keep pace withgeneral banking in the developmentof sophisticated new products, andthey must cope with restrictionsthat can add considerablecomplexity to both these new, aswell as existing, Shariah-compliantproducts. In addition to managingthe ever more complex modernfinancial markets, bankers will alsoneed to educate Muslim consumers,providing information about thebenefits of Shariah compliantproducts and how they comparewith traditional products.

While Shariah compliant productsare now more competitive on pricethan they were a few years ago,Islamic institutions will still need todo more to drive their costs downand pass on pricing benefits toconsumers. To date Islamic bankshave been relatively slow to adoptthe techniques commonly used byWestern financial institutions, suchas outsourcing IT, call centres andproduct development. This may notmatter, given our expectation thatmuch of the industry is going toconsolidate but, for those nicheplayers who do wish to remainindependent, the challenge is clearlyto adopt much of the functionmodel used by western banks if theyexpect to be able to compete onprice and product range.

Islamic banks have beenslow to adopt highperformance banking models,giving Europe's bankers anedge in capturing futuremarket share.

0

4,000

8,000

12,000

16,000

20,000

24,000

2001 2002 2003 2004 2005 2006 2007e

0

10

20

30

40

50

60

70

80

90Global Sukuk Issuance ($ million)

Number of Sukuk Issues (RHS)

Value and Volume of Sukuk Issues

Source: Zawya

5

Stage II: Expanding intothe European MassMarketThe key for the next stage of growthin Islamic finance is not the highnet worth markets of the MiddleEast, or even the rise of Islamicemerging markets: it is the massmarket of Muslims living in Europe.

The European Commission hasestimated that there areapproximately 13 million Muslimsin the European Union2. Given theprosperity of Europe, these Muslimsrepresent a block of Islamic massaffluence second only to theenergy-rich states. What is neededto market to these people is anattractive set of products whichcost-effectively mirrors what ismore widely available in non-Shariah products, and asimportantly, a comprehensivedistribution network.

Our forecast is for the total amountof savings by European Muslims totop $14 billion by 2020, an annualgrowth rate of almost 14%. Thisrepresents a conservative forecast,incorporating a considerableslowing of the 22% annual growthrate seen in recent years. Growthwill also continue with the savingsof energy-intensive IslamicCountries rising by almost 6% perannum. Meanwhile the growth insavings from rapidly developingIslamic countries is forecast to bejust over 20% per annum, albeitfrom a very low base.

While our forecast only considersthe macro-economic GDP growth,the consequential propensity tosave, and the resulting money putinto some form of savings, thesefigures and trends clearly haveimplications for a wide array ofIslamic financial products.

Europe's 13 million Muslim'srepresent the next stage ofgrowth for Islamic finance.

2. “Muslims in the European Union", European Monitoring Centre on Racism and Xenophobia, 2006.

Stage I

Stage III

Stage II

Turkey begins to save significantly

0

5

10

15

20

25

30

35

40

1990 1995 2000 2005 2010 2015 2020

Rapidly Developing Is lam

Energy Is lam

Islamic Europe

Islamic Savings ($ billion)

Source: IMF, UN Population Database, Accenture Research forecasts

6

Stage III: Growth ofIslamic EconomiesIf the marketing of Islamicfinancial products represent animmediate opportunity, it is theemergence of Islamic emergingmarkets which represents the mostexciting medium to longer termprospect. Our estimate is that, by2020, Islamic savings emanatingfrom emerging markets could wellbe as large as the combined Islamicsavings of oil rich Islam andEuropean Muslims.

Our forecast starts by looking atthe trend rate of growth ofindividual countries purchasingpower parity GDP per capita andthe trend rate of growth of cashGDP, and converging the latter onthe former.

As economies develop, they movethrough a number of reasonablypredictable stages. When GDP percapita reaches approximately$7000 (in real cash terms, not on a

purchasing power parity basis),demand for financial products suchas life insurance rises rapidly3. Ourmodel has therefore assumed thatwhen per capita GDP movesthrough this threshold, five percentof income is saved.

The next question is what portionof savings is likely to be placed inIslamic financial products.Penetration rates vary by country,but today's mature markets averagebetween 15-20% of customerschoosing Islamic financial products.We have assumed that increasingsophistication of Islamic productsmeans that penetration rates rise to25% of new savings. Thus ourmodel assumes that Islamicfinancial products' market sharerises from 2% of Muslim savings in1990, to 16% in 2007 to slowlycapturing 25% of savings by 2016.Growth beyond this level isdependant upon the unlikelyagreement of a common set of rulesas to what qualifies as Shariah.

Emerging markets Islamicsavings could top those ofboth resource rich andEuropean Muslims by 2020

Growth in Islamic finance isbeing hindered by debateover what qualifies as aShariah complaint product

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1990 1995 2000 2005 2010 2015 2020

Rapidly Developing Is lam

Emerging Is lam

Energy Is lam

Stagnant Is lam

Islamic GDP Down

Islamic GDP Upside

Islamic GDP: Forecast Scenarios ($ billion)

3 Exploiting the Growth of Emerging Insurance Markets, Swiss Re, Sept 2004.

Source: IMF, UN Population Database, Accenture Research forecasts

7

Looking at the present stage ofdevelopment and the potential forfuture development in individualIslamic countries, as well as theprospects of countries such as Indiawhere there are significant Muslimpopulations, we believe economicgrowth is going to be concentrated in a relatively few countries. In everycase, our candidates for rapiddevelopment have already achievedcash GDP of at least $5,000 per annum.

In determining our forecast, we havetwo central questions: what sort ofgrowth can emerging markets expectand what will be the demand forIslamic financial products as theseeconomies grow?

In our Islamic GDP growth scenarios,we have divided countries into fourdistinct categories:

• Rapidly developing Islam, whereeconomic growth has moved to thepoint where the economy is fullymonetised (e.g. there is little or no

subsistence farming or barter).Such countries have diversifiedeconomies and a growing andvibrant middle class. There is everyreason to believe that sucheconomies will continue to grow.This category includes countriessuch as Malaysia, Turkey, the UAE,and Oman.

• Emerging Islam, where purchasingpower parity GDP per capita maybe reasonable, but cash GDP is farlower, indicating that much of theeconomy remains semi-subsistence.In such circumstances, demand forfinancial products will only growwhen the economies themselvesmonetise. Breaking through intobeing a rapid growth economy ispossible, but in no way assuredwithin our time frame. Thiscategory includes such countries asMorocco, Tunisia, Egypt, India and Indonesia.

Our growth forecasts remainconservative, only focusingon the potential of thoseeconomies where cash GDPper capita rises above $7,000per annum

Once mass affluence isachieved, we assume that 5%of income is saved and thatup to 25% of that is placedin Shariah compliantproducts

02040

6080

100120

140160180

1990 1995 2000 2005 2010 2015 2020

of which Is lamic savings

Total Savings of Is lamic Countries

Savings within Islamic Countries ($ billion)

Source: IMF, UN Population Database, Accenture Research forecasts

8

Our base case is for Islamicsavings to grow by 12% p.a.,our downside where growthfails to materialise seesgrowth of 6%p.a.

0

5

10

15

20

25

30

35

40

45

1990 1995 2000 2005 2010 2015 2020

Total Islamic Savings

Islamic Savings Upside

Islamic Savings Down

Potential Islamic Savings: Forecast Scenarios ($ billion)

Source: IMF, UN Population Database, Accenture Research forecasts

• Energy Islam, where oil and gasextraction, and accompanyingactivities, account for themajority of the GDP. Suchcountries do not have welldiversified economies capable ofgenerating wealth outside oil andgas, which limits their growthprospects. They do howeveralready have middle classes whowill often seek Islamic financialproducts. This category includessuch countries as Saudi Arabia,Kuwait, Qatar, Algeria and Libya.

• Stagnant Islam, countries which,in our view, are unlikely to seesignificant economic growthinto the medium term. Thesecountries often have high birthrates and have proven unable togenerate useful employment fortheir growing populations. Theresult is low rates of economicgrowth and in some casesfalling levels of economicprosperity. These countries will

not feature in any calculationabout the long term potentialdemand for Islamic finance. Thiscategory includes such countriesas Mauritania, Syria, Yemen andBangladesh.

In contrast to our scenario forIslamic GDP, where there issignificant potential for greatergrowth than we expect in our basecase, the danger in our savingsforecast is significantunderperformance when comparedto our base case. This is a result ofour forecast for many economies togrow well (boosting GDP) withoutreaching the point where theaverage household can be expectedto afford to put savings aside.

Finally it must be noted that thefigures in our forecasts are forIslamic savings, and we have notmade any attempt to forecast whichfinancial products would benefitfrom these savings.

9

Islamic finance is overcominga legacy of expensive andlittle understood products andcreating liquidity in theprocess

ChallengesIslamic financial services providersstill face several challenges, somerelating to their own capabilities,and some to the market as a whole.

• Islamic retail products havetraditionally been expensive.While the pricing gap hasnarrowed thanks to greatercompetition and commoditisationof financial products, it has notdisappeared all together.

• Consumers lack knowledgeabout Shariah compliantproducts. Providers of Islamicfinancial services need to workharder than their conventionalcounterparts to educate people onIslamic principles and products,with Shariah complianceappearing to add a further levelof complexity to a subject that most consumers already find daunting.

• There is a shortage of liquidityin some products. This isparticularly the case within theSukuk market, where investorscan end up holding their assetsfor longer than they intendedbecause of secondary marketilliquidity.

These external challenges arecompounded by internal issuesbeing faced by Islamic bankers.

• The growing significance ofIslamic Finance has led to ashortage of skilled staff, drivingsalaries upwards.

• There is a high degree ofinherent complexity. This bringsin concerns over riskmanagement, given the greaterdifficulty of hedging and swapstransactions in a Shariah-compliant environment and thegenerally lower levels of liquiditythan conventional markets.

• Rigid, yet unclear rules.Shariah-compliant financialinstitutions have little or nolatitude when implementing the opinions of its Shariahadvisers, but the advice itself can be inconsistent, varyingbetween advisors.

• Shariah compliance itselfremains a thorny issue. Whilethe creation of the Accountingand Auditing Organisation forIslamic Financial Institutions(AAOIFI) will help to drivestandardisation and convergence,the fact remains thatinterpretation by individualscholars will always play a role.The ‘pure play' Islamic providerswill face additional regulatorychallenges, not only aroundcompliance with Basel II but alsorelating to the capitalrequirements laid down by theIslamic Financial Services Board(IFSB) in Malaysia.

There remain internal issues,including staff shortages, andcomplying with differinginterpretations of Shariahcompliance

10

ConclusionsHigh Net Worth Individuals, largelyfrom the Middle East, have been akey to the development of Islamicfinancial products. While thesecustomers remain important forprivate bankers and wealthmanagers, the next challenge is tomarket these Islamic financeproducts to a mass EuropeanMuslim clientele.

The rise of sovereign funds offerssignificant scope for IslamicFinancial products. High oil priceshave enriched oil rich states fundswhich are now estimated to have atleast $1,700 billion in funds undermanagement.

Marketing of Islamic Finance tothe mass of potentially interestedEuropeans requires highly costeffective products. This will mostoften mean utilising large universalbanks' low cost bases andoperating models.

Small scale Islamic banks arelikely to lose out in Stage II asIslamic finance will be dominatedby those developed market bankswhich effectively capture businessfrom European Muslims.

The rules surrounding whatqualifies for Shariah financeremain uncertain. So long asinterpretation of what is “Islamic"is open to a wide variety ofopinions, consumers will remainuncertain and wide scale marketdevelopment will be hindered.

The long term potential forIslamic finance is good supportedby the growth of a range ofemerging Islamic markets such asTurkey and Malaysia.

ContactsJames SprouleAccenture ResearchGrowth & StrategyTel. +44 207 844 3387Mob. +44 7866 808 [email protected]

Ismail AmlaAccenture Capital MarketsTel. +44 161 435 5507Mob. +44 7785 300 [email protected]

Sohail SyedAccenture Capital MarketsTel. +44 207 844 0824Mob. +44 7917 050 [email protected]

Anton PichlerAccenture ResearchGrowth & StrategyTel. +44 207 844 [email protected]

Copyright © 2007 AccentureAll rights reserved.

Accenture, its logo, andHigh Performance Deliveredare trademarks of Accenture.

About AccentureAccenture is a global managementconsulting, technology services andoutsourcing company. Committed todelivering innovation, Accenturecollaborates with its clients to helpthem become high-performancebusinesses and governments. Withdeep industry and business processexpertise, broad global resources anda proven track record, Accenture canmobilize the right people, skills andtechnologies to help clients improvetheir performance. Withapproximately 170,000 people in 49countries, the company generated netrevenues of US$19.70 billion for thefiscal year ended Aug. 31, 2007. Itshome page is www.accenture.com.