10-15% of the adult population without access to bank accounts 7-10 million with limited access to...

9

•10-15% of the adult population without access to bank accounts •7-10 million with limited access to financial services •12 million people use sub prime market in the UK •Sub prime market estimated value of £16 billion/year •3-5m using doorstep lenders •1m+ using pay day lenders According to the FSA, Government and Financial Inclusion Taskforce

-

Upload

janel-banks -

Category

Documents

-

view

220 -

download

0

Transcript of 10-15% of the adult population without access to bank accounts 7-10 million with limited access to...

• 10-15% of the adult population without access to bank accounts

• 7-10 million with limited access to financial services

• 12 million people use sub prime market in the UK

• Sub prime market estimated value of £16 billion/year

• 3-5m using doorstep lenders• 1m+ using pay day lenders

According to the FSA, Government and Financial Inclusion Taskforce

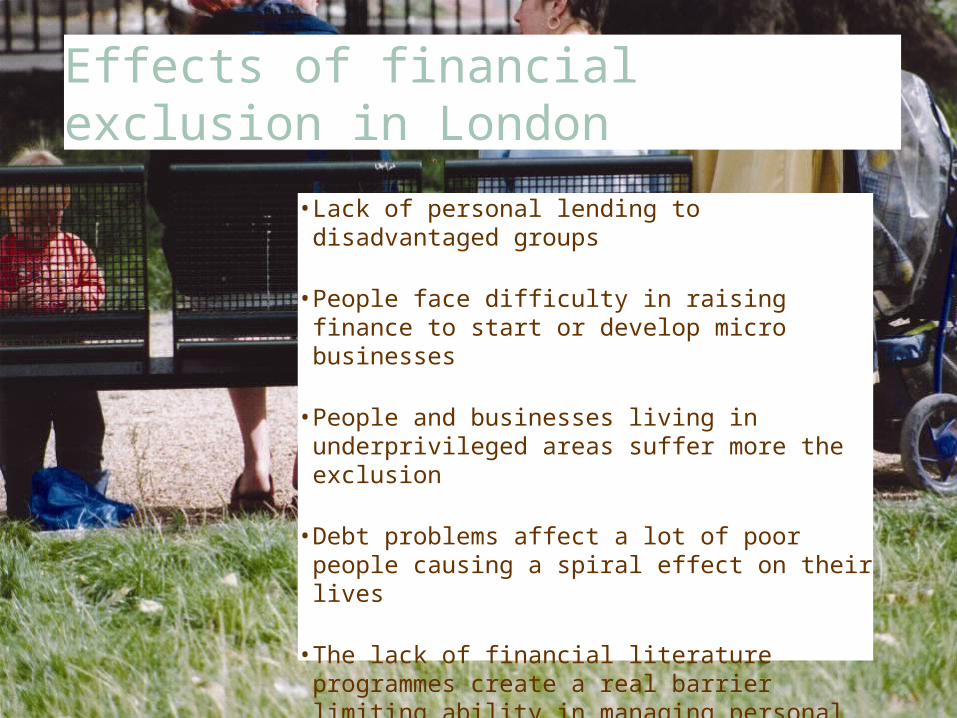

• Lack of personal lending to disadvantaged groups

• People face difficulty in raising finance to start or develop micro businesses

• People and businesses living in underprivileged areas suffer more the exclusion

• Debt problems affect a lot of poor people causing a spiral effect on their lives

• The lack of financial literature programmes create a real barrier limiting ability in managing personal finance

Effects of financial exclusion in London

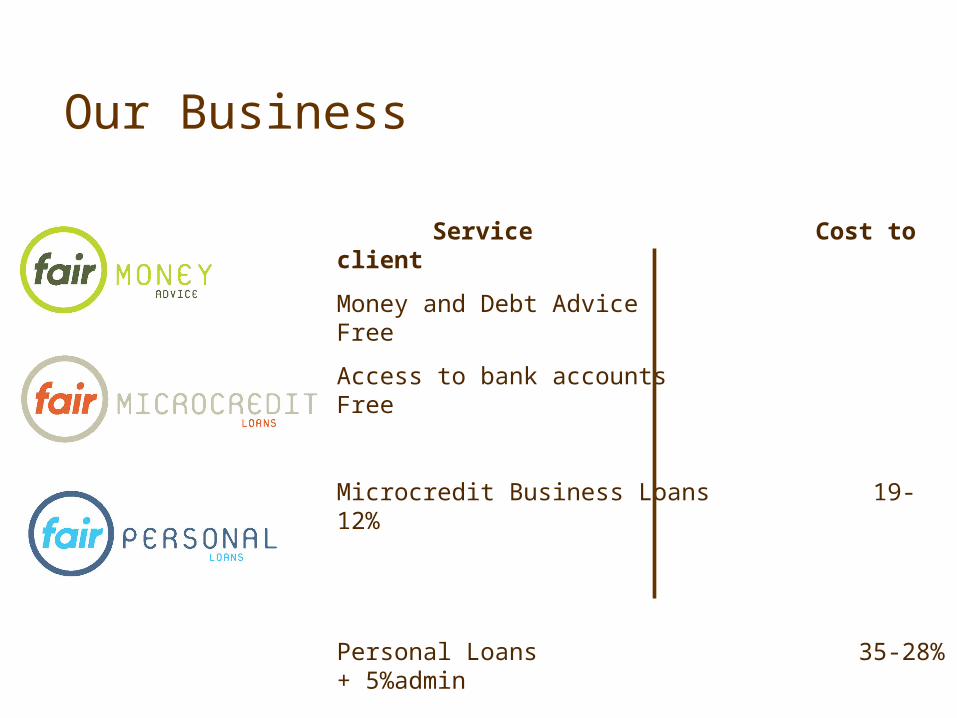

Service Cost to client

Money and Debt Advice Free

Access to bank accounts Free

Microcredit Business Loans 19-12%

Personal Loans 35-28% + 5%admin

Our Business

2005/06- 2008/9

Total number of clients seen and supported 5000

Personal Loans Made (1200) £1,100,000

Microcredit Loans Made (130)£500,000

Bad Debt Rate 7%

Debt Advice Given 1500

Overindebtedness managed£12m

Bank Accounts opened 120

Savings for clients £450,000

Statistics

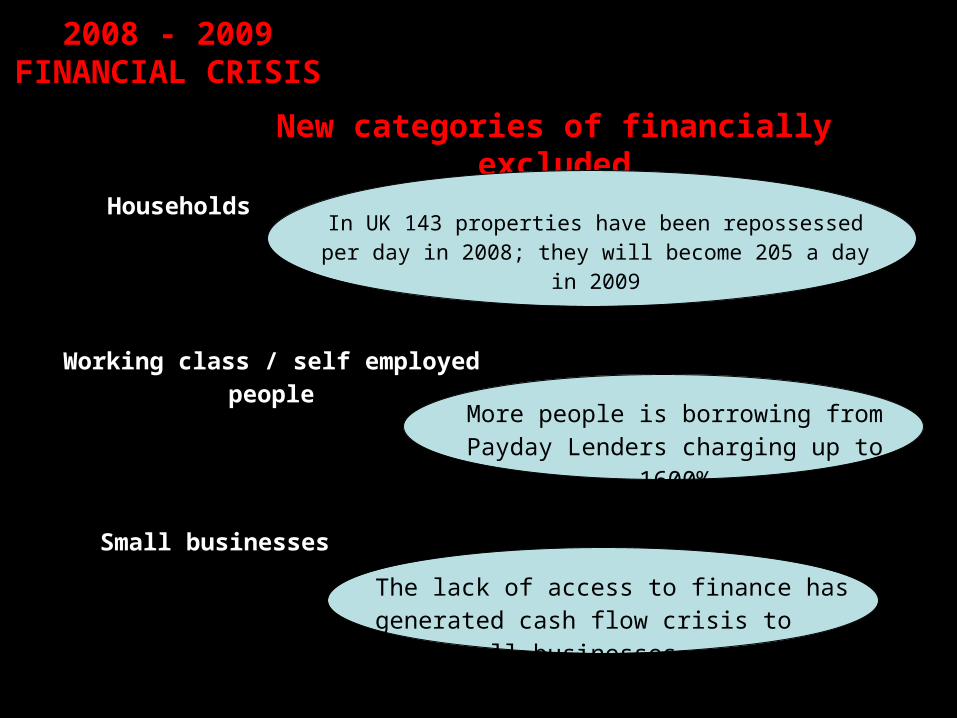

2008 - 2009FINANCIAL

CRISISNew categories of financially excluded

Households

Working class / self employed people

Small businesses

In UK 143 properties have been repossessed per day in 2008; they will become 205 a day in 2009

More people is borrowing from Payday Lenders charging up to 1600%

The lack of access to finance has generated cash flow crisis to many small businesses

Challenges of the new economic climate

New categories of financially excluded

New products/services needs

New delivery methods

HouseholdsQuick and professional

advice on remortgaging and debt problems

- Telephone advice- Preventative financial

capability programmes

Working class / self employed people

Consolidate high interest loans

- Telephone interviews (for repeated customers)

- Stricter connection with debt advice

Small businesses

Bigger and cash oriented loans for new category of

financially excluded businesses

- Referral partnerships with BSP

- Strong attention on repayment affordability

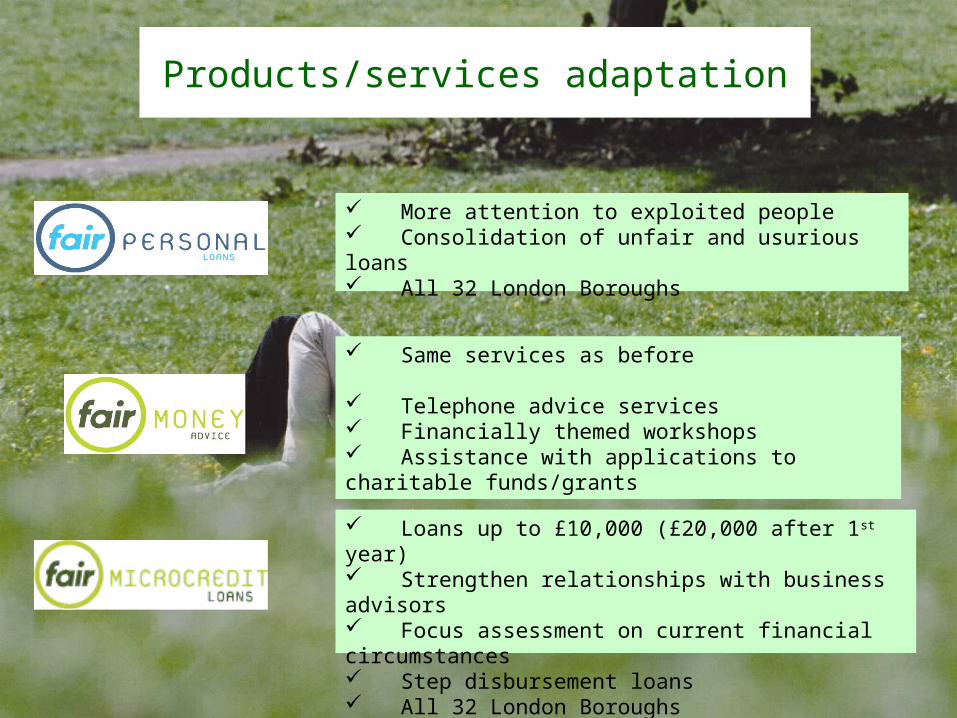

Products/services adaptation

More attention to exploited people Consolidation of unfair and usurious loans All 32 London Boroughs

Same services as before

Telephone advice services Financially themed workshops Assistance with applications to charitable funds/grants

Loans up to £10,000 (£20,000 after 1st year) Strengthen relationships with business advisors Focus assessment on current financial circumstances Step disbursement loans All 32 London Boroughs

Lessons learnt

• FF as Social enterprise look for solution in difficult times

• Innovated new products and services• Consulted with stakeholders and clients

to understand changing needs• Tightened existing systems and made

more efficient• Couldn’t have done this change so

quickly if primarily govt supported

Riccardo Aguglia Riccardo Aguglia Microcredit ManagerMicrocredit Managerwww.fairfinance.org.ukwww.fairfinance.org.uk47 Ben Jonson Road, Stepney, London E1 4SA47 Ben Jonson Road, Stepney, London E1 4SA18 Ashwin Street, Dalston, E8 3DL18 Ashwin Street, Dalston, E8 3DLT: 0207 780 1777 F: 0207 780 1999T: 0207 780 1777 F: 0207 780 1999E: [email protected]: [email protected]