1 USF Reform— Getting It Right, Getting it Fair Dr. Brian K. Staihr Regulatory Economist –...

17

1 USF Reform— Getting It Right, Getting it Fair Dr. Brian K. Staihr Regulatory Economist – Embarq July 16, 2007 [email protected]

-

Upload

claude-arnold -

Category

Documents

-

view

214 -

download

0

Transcript of 1 USF Reform— Getting It Right, Getting it Fair Dr. Brian K. Staihr Regulatory Economist –...

1

USF Reform—Getting It Right, Getting it Fair

Dr. Brian K. Staihr

Regulatory Economist – Embarq

July 16, [email protected]

2

Overview - Getting it Right, Getting it Fair

Quick reiteration of why the

needfor

USF supportmust be

determinedat a

more granularlevel.

Brief discussion of how this

granularapproachcan be

implementedright now…

today…with no

roadblocks!

A couple of minutes

to addresswhat this means

for reverseauction

proposals andfor

broadbandproposals.

The “WHY” The “HOW” The “WHAT”

3

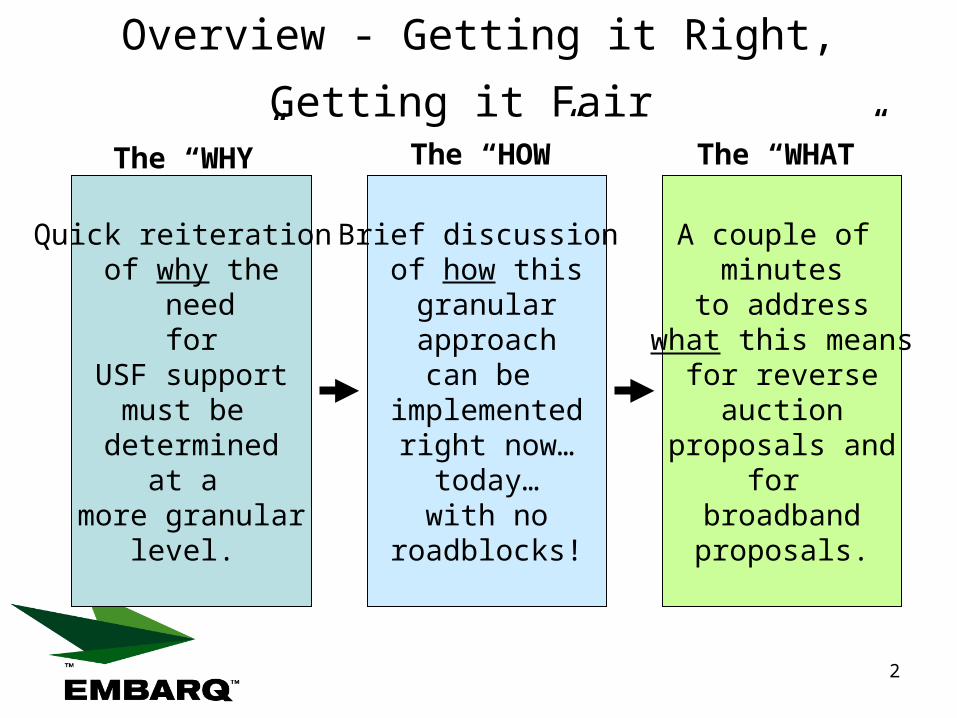

Paterson, WashingtonMonthly Cost: $228.60

Mount Charleston, NevadaMonthly Cost: $318.18

Waldorf, MinnesotaMonthly Cost: $137.86

Urbana, IndianaMonthly Cost: $106.73

Ceres, VirginiaMonthly Cost: $127.14

Westville, FloridaMonthly Cost: $200.49

Iona, MissouriMonthly Cost: $174.37

NO SUPPORT

4

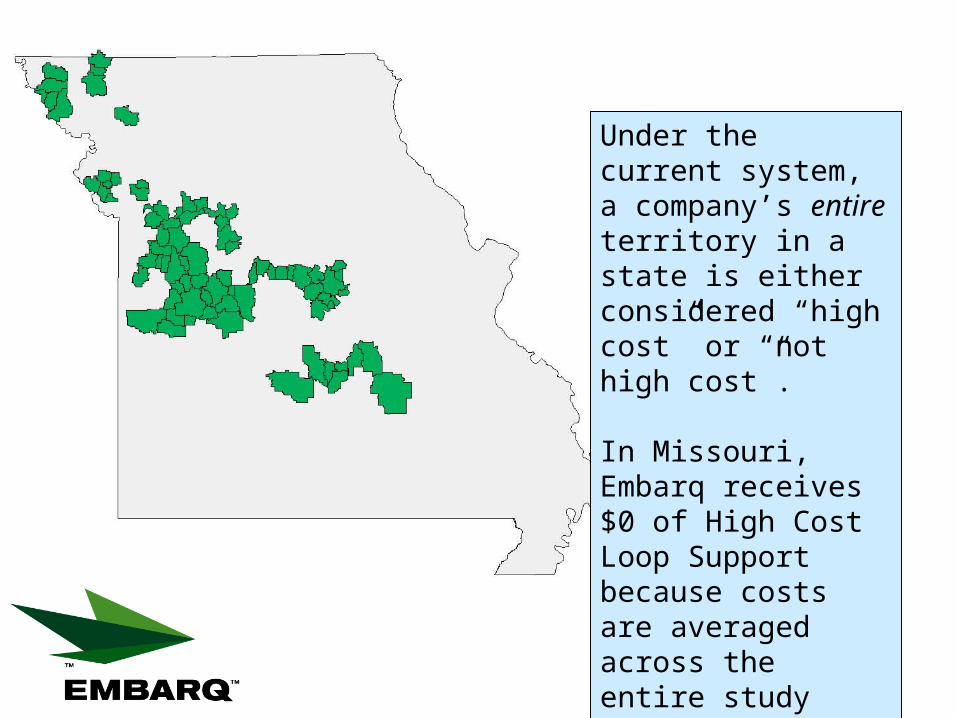

Under the current system, a company’s entire territory in a state is either considered “high cost” or “not high cost”.

In Missouri, Embarq receives $0 of High Cost Loop Support because costs are averaged across the entire study area.

5

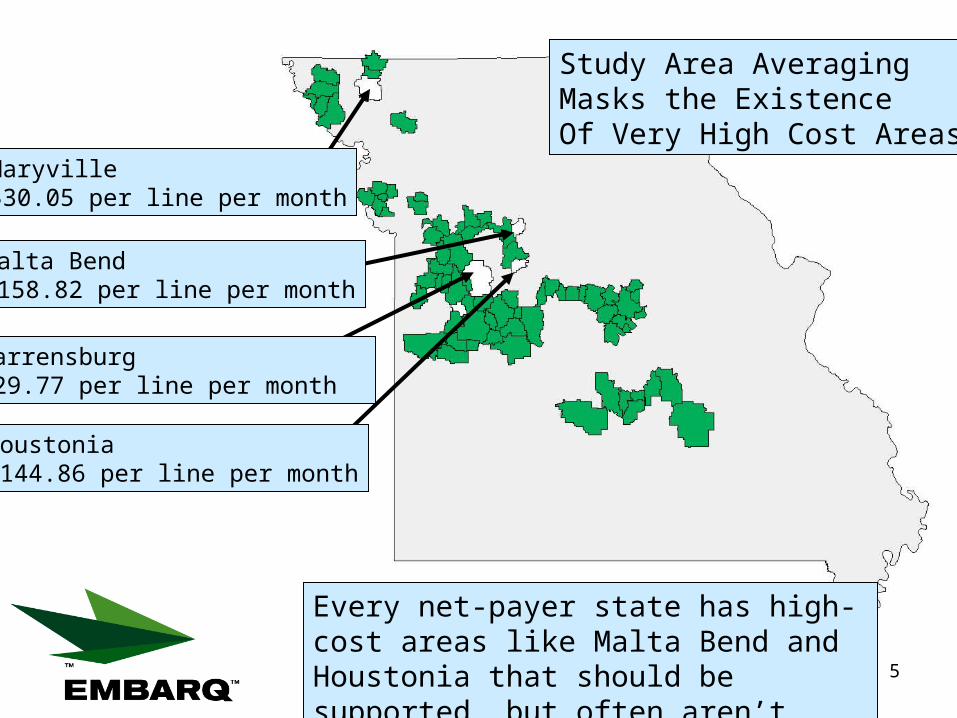

Maryville$30.05 per line per month

Malta Bend$158.82 per line per month

Houstonia$144.86 per line per month

Warrensburg$29.77 per line per month

Study Area AveragingMasks the ExistenceOf Very High Cost Areas

Every net-payer state has high-cost areas like Malta Bend and Houstonia that should be supported, but often aren’t.

6

Bethel, North Carolina: City Center

7

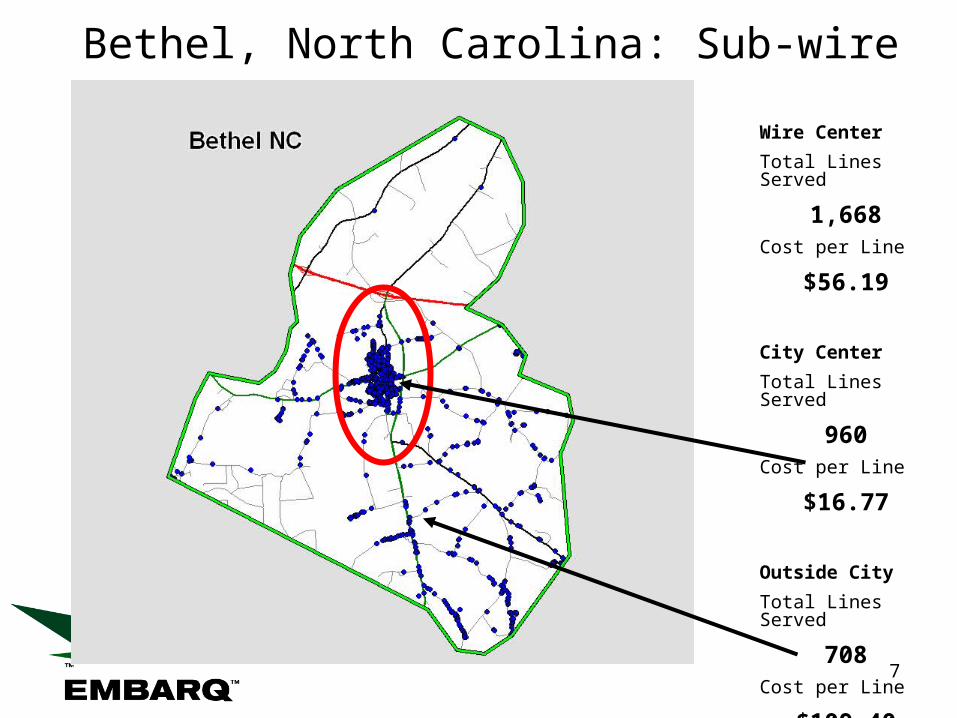

Bethel, North Carolina: Sub-wire center

Wire Center

Total Lines Served

1,668Cost per Line

$56.19

City Center

Total Lines Served

960Cost per Line

$16.77

Outside City

Total Lines Served

708Cost per Line

$109.40

8

• Recently filed study on Texas USF—co-sponsored by Embarq, Windstream, CenturyTel and Consolidated—documents impacts of “donut-and-hole” phenomenon.

• Competitors serve only low-cost, economic, in-town areas, ignoring higher-cost out-of-town regions.

• Competition, rather than solving the problem, increases the need for explicit support.

Wire Center Boundary

Service Locations

Central Office

9

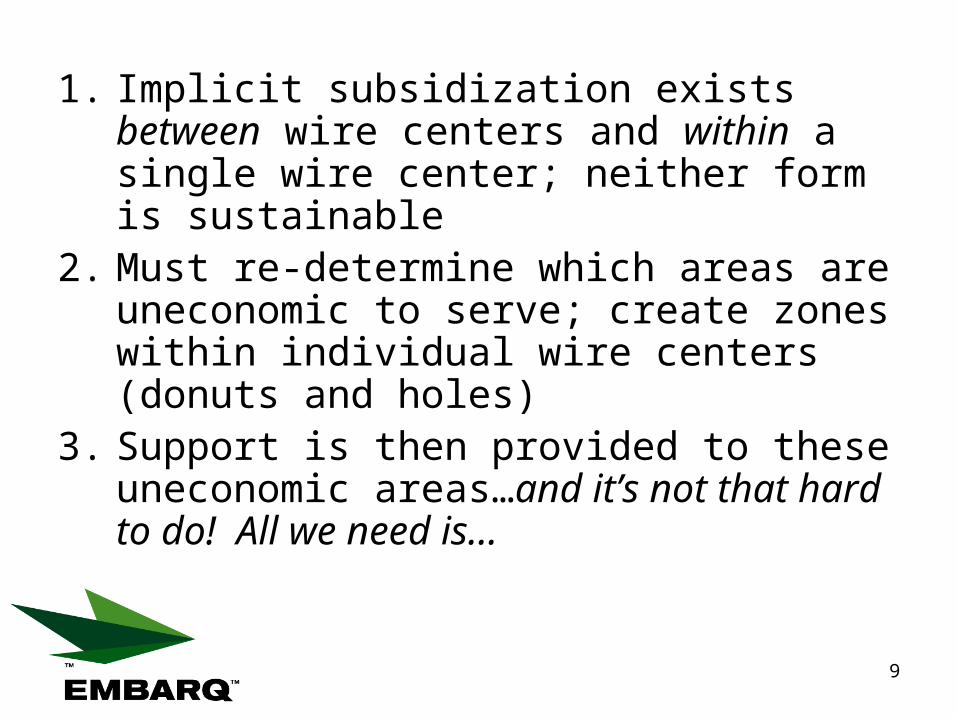

1. Implicit subsidization exists between wire centers and within a single wire center; neither form is sustainable

2. Must re-determine which areas are uneconomic to serve; create zones within individual wire centers (donuts and holes)

3. Support is then provided to these uneconomic areas…and it’s not that hard to do! All we need is…

10

Oh no! Not…a cost model!!!

11

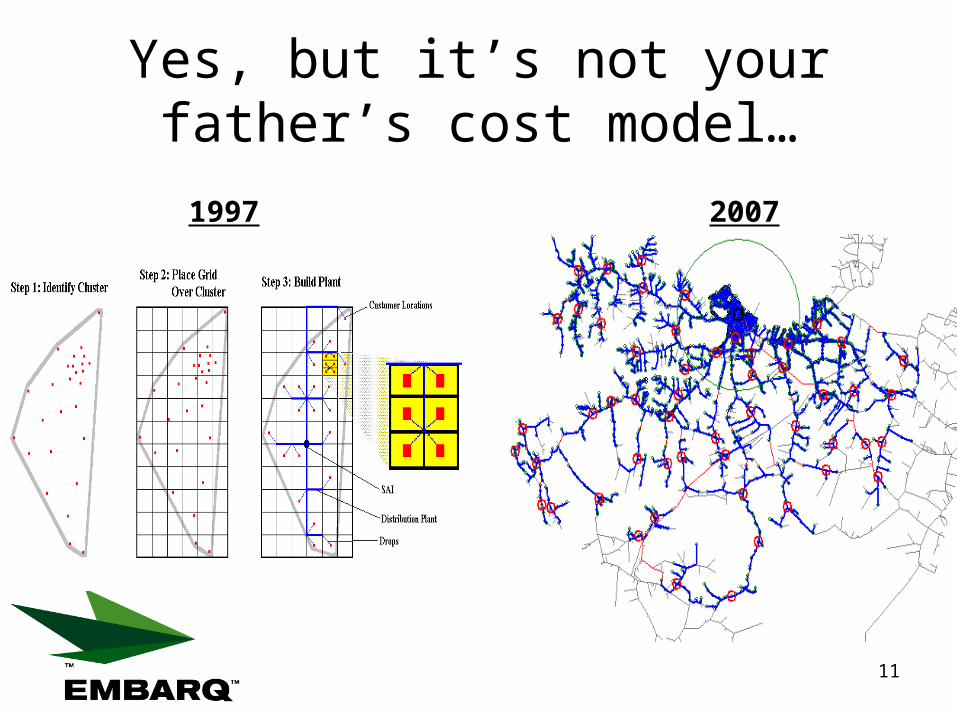

Yes, but it’s not your father’s cost model…

1997 2007

12

Increased Granularity Does Require a Model. But…

• Models available now that can calculate need for support at wire center (or sub wire center) levels…– Any company that has customers’ addresses and wire

center boundaries can have granular costs calculated in a matter of weeks

– Two years not needed to “produce” a model• Commission’s past experience with model controversies is not

prelude…– No repeat of the “Model Wars” of the late 90s

• Smaller companies—whose study areas do not exhibit variations in costs—would not require increased granularity.

13

Fund Size Can Be Controlled Even With Increased Granularity

• Fund size function of numerous variables, including benchmark

• Illustrative Example:1. Take benchmark currently found in H.R. 2054: 2.75X national

average cost

2. Apply this benchmark at a wire center level to all areas that make up wire centers served by large and mid-sized LECs

3. Support 75% of the difference between the benchmark and the cost at a wire center level

4. That amount is LESS than annual support dollars currently going to redundant competitive ETCs serving the same areas.

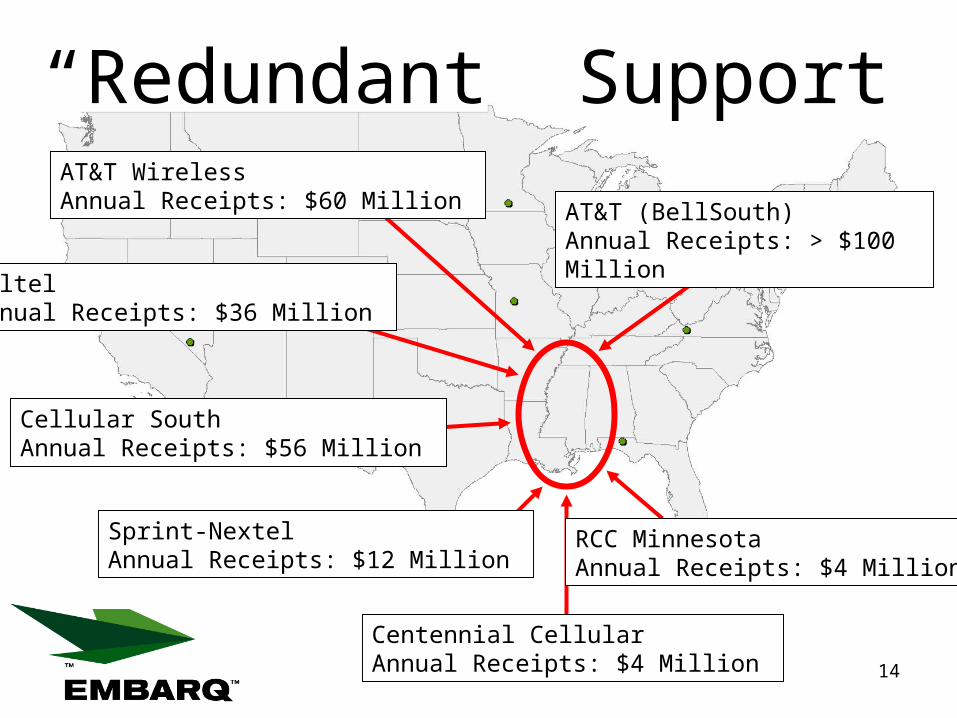

14

“Redundant” Support

AT&T (BellSouth)Annual Receipts: > $100 Million

AT&T WirelessAnnual Receipts: $60 Million

AlltelAnnual Receipts: $36 Million

Cellular SouthAnnual Receipts: $56 Million

Sprint-NextelAnnual Receipts: $12 Million

Centennial CellularAnnual Receipts: $4 Million

RCC MinnesotaAnnual Receipts: $4 Million

15

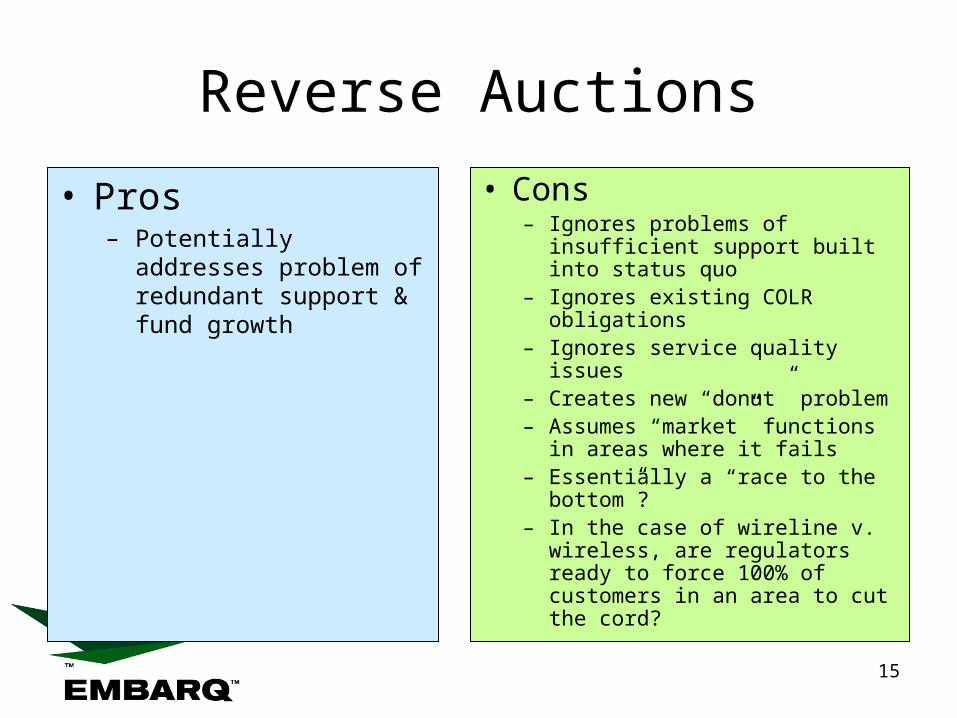

Reverse Auctions

• Pros– Potentially addresses

problem of redundant support & fund growth

• Cons– Ignores problems of insufficient

support built into status quo– Ignores existing COLR

obligations– Ignores service quality issues– Creates new “donut” problem– Assumes “market” functions in

areas where it fails– Essentially a “race to the

bottom”?– In the case of wireline v.

wireless, are regulators ready to force 100% of customers in an area to cut the cord?

16

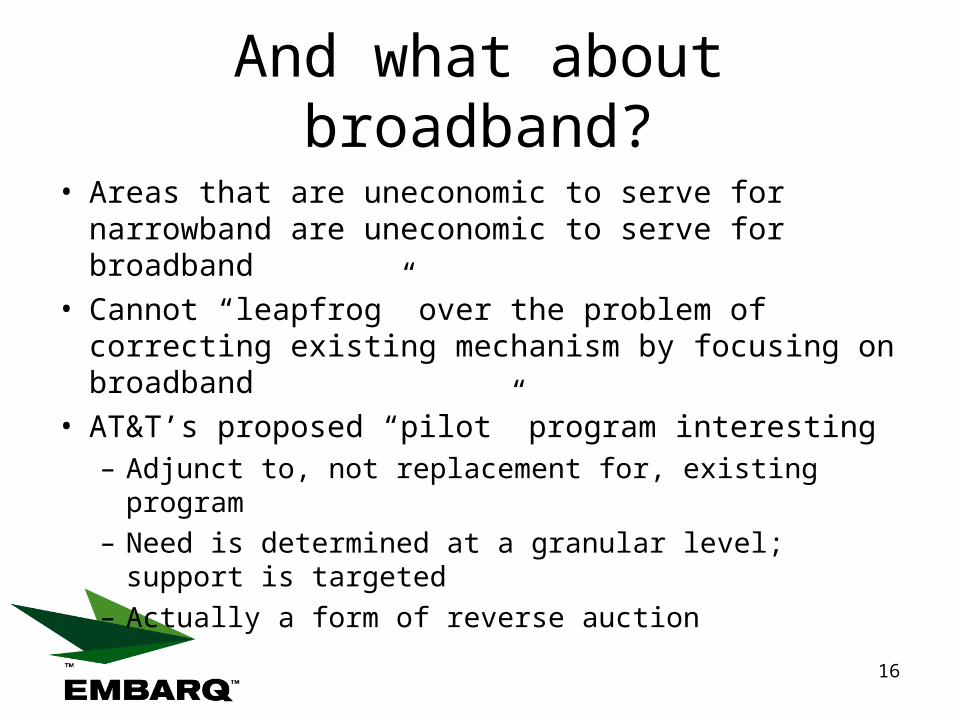

And what about broadband?

• Areas that are uneconomic to serve for narrowband are uneconomic to serve for broadband

• Cannot “leapfrog” over the problem of correcting existing mechanism by focusing on broadband

• AT&T’s proposed “pilot” program interesting– Adjunct to, not replacement for, existing program– Need is determined at a granular level; support is

targeted– Actually a form of reverse auction

17

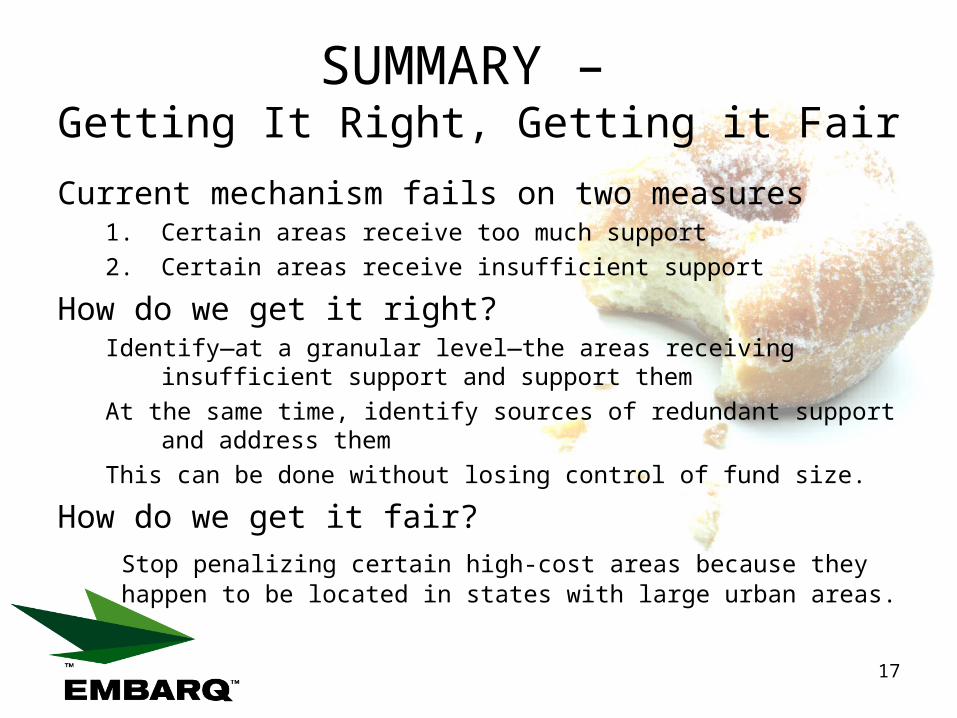

SUMMARY – Getting It Right, Getting it Fair

Current mechanism fails on two measures1. Certain areas receive too much support

2. Certain areas receive insufficient support

How do we get it right?Identify—at a granular level—the areas receiving insufficient support and

support them

At the same time, identify sources of redundant support and address them

This can be done without losing control of fund size.

How do we get it fair?Stop penalizing certain high-cost areas because they happen to be located in states with large urban areas.