1 Topic 24: Investment Vehicles CDs Money market funds Money market mutual funds temporarily...

40

1 Topic 24: Investment Vehicles CDs Money market funds Money market mutual funds temporarily insured T bills Commercial paper Bankers acceptances Bank guaranteed notes to assure payment for exports Eurodollars Dollar denominated deposits Municipal bonds No federal income tax on interest; cap gains taxed General obligation versus revenue bonds Treasury STRIPS Separates interest payments and principal payment

-

Upload

phoebe-payne -

Category

Documents

-

view

219 -

download

0

Transcript of 1 Topic 24: Investment Vehicles CDs Money market funds Money market mutual funds temporarily...

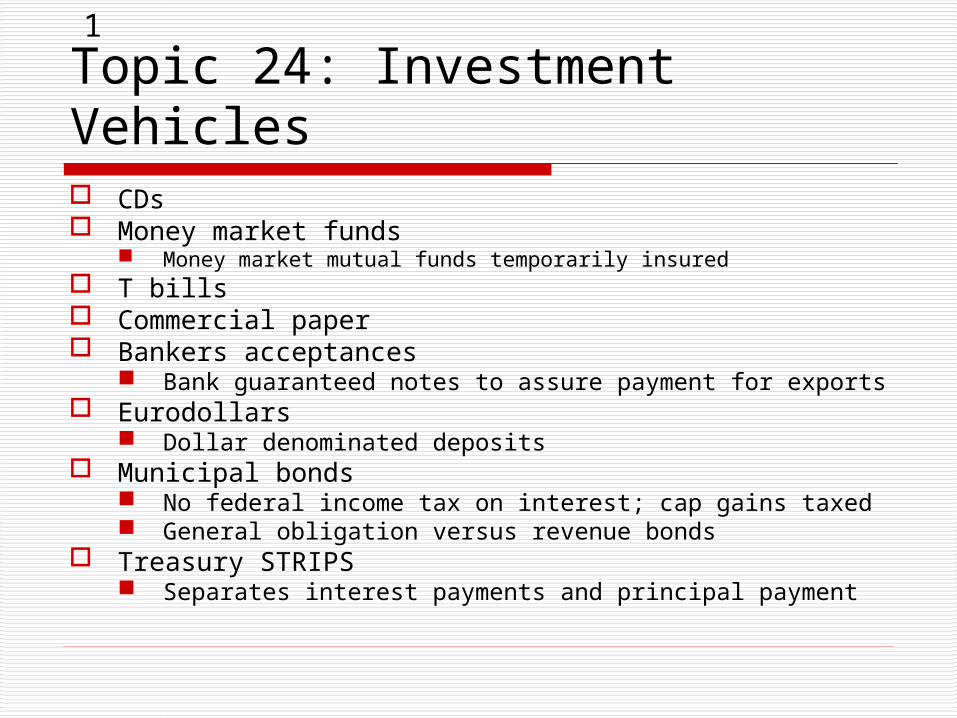

1

Topic 24: Investment Vehicles CDs Money market funds

Money market mutual funds temporarily insured T bills Commercial paper Bankers acceptances

Bank guaranteed notes to assure payment for exports Eurodollars

Dollar denominated deposits Municipal bonds

No federal income tax on interest; cap gains taxed General obligation versus revenue bonds

Treasury STRIPS Separates interest payments and principal payment

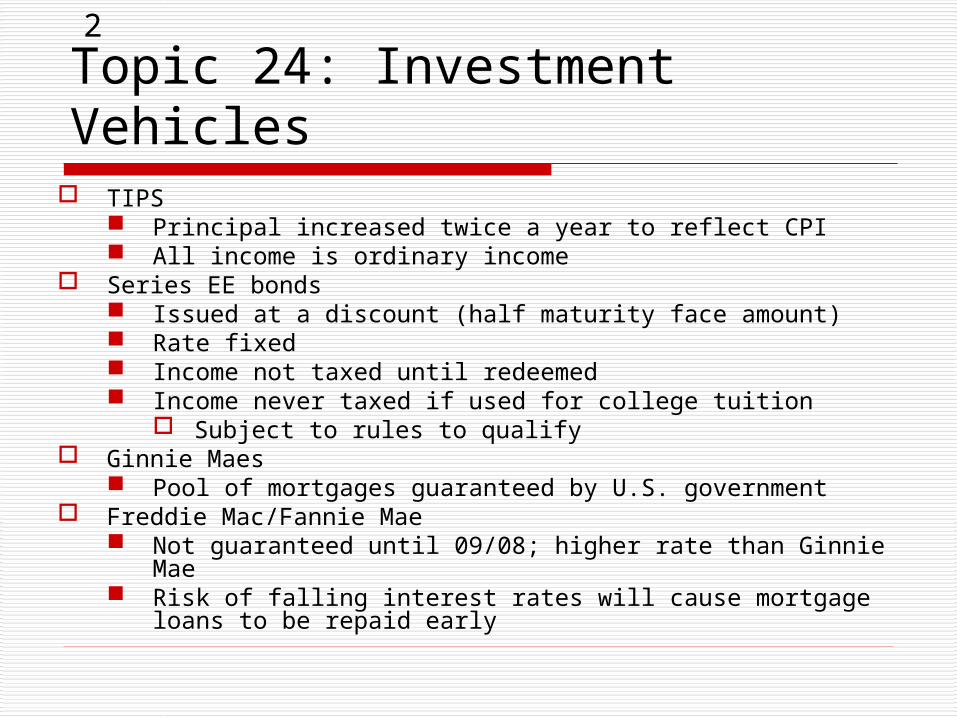

2

Topic 24: Investment Vehicles TIPS

Principal increased twice a year to reflect CPI All income is ordinary income

Series EE bonds Issued at a discount (half maturity face amount) Rate fixed Income not taxed until redeemed Income never taxed if used for college tuition

Subject to rules to qualify Ginnie Maes

Pool of mortgages guaranteed by U.S. government Freddie Mac/Fannie Mae

Not guaranteed until 09/08; higher rate than Ginnie Mae Risk of falling interest rates will cause mortgage loans to be

repaid early

3

Topic 24: Investment Vehicles CMOs

Investors can select tranches of various maturity, risk levels Zero coupon bonds

Pricing Use in retirement accounts

ADRs Foreign stocks trading on U.S. exchange Still have currency risk

Privately/separately managed accounts High minimum to start Actually own stocks, bonds (not mutual funds) More control over tax consequences

Precious metals ETFs versus physical possession

4

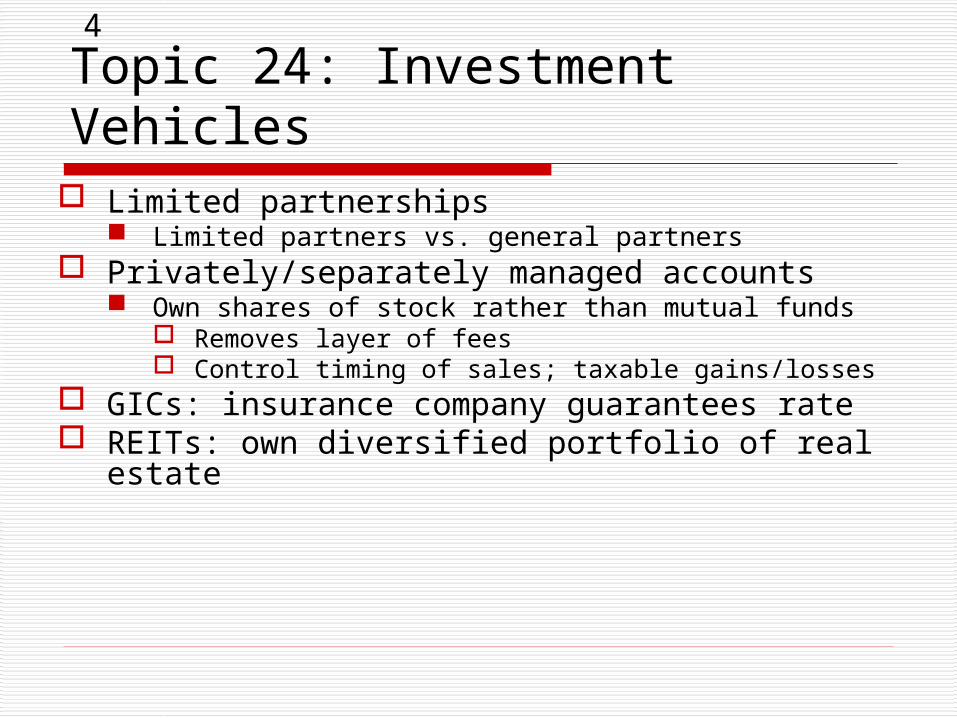

Topic 24: Investment Vehicles Limited partnerships

Limited partners vs. general partners Privately/separately managed accounts

Own shares of stock rather than mutual funds Removes layer of fees Control timing of sales; taxable gains/losses

GICs: insurance company guarantees rate REITs: own diversified portfolio of real estate

5

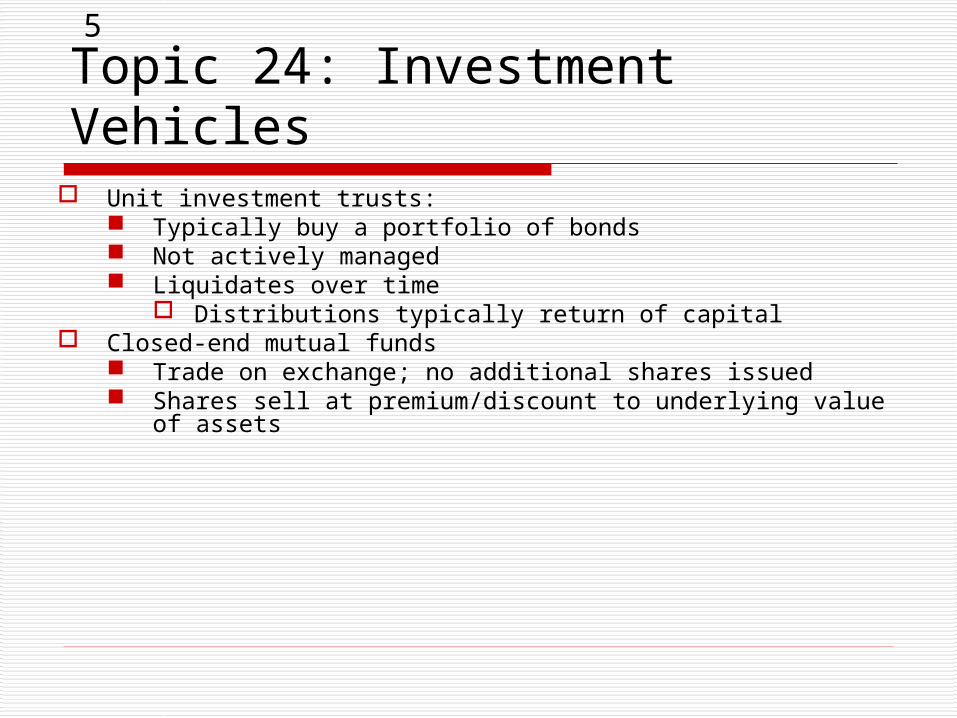

Topic 24: Investment Vehicles Unit investment trusts:

Typically buy a portfolio of bonds Not actively managed Liquidates over time

Distributions typically return of capital Closed-end mutual funds

Trade on exchange; no additional shares issued Shares sell at premium/discount to underlying value of assets

6

Topic 24: Investment Vehicles Mutual funds:

Pool funds from investors to invest in stocks, bonds and/or other types of securities

Each share represents investor’s proportionate interest in portfolio

Priced at the end of trading Advantages

Low minimum investments Automatic investment programs

Diversification Professional management

7

Topic 24: Investment Vehicles Open-end mutual funds

Grow by issuing shares Unless fund is closed if it gets too large

Costs Load

Class A: load but lower 12b-1 and annual expenses Class B: no front-end load but higher annual expenses Class C: lower load than Class A or B

No load Deferred sales charges

Holding of funds Management fees

Equities: 1 – 1.5%; bonds .5%, for example 12b-1 fees: brokers, advertising Portfolio turnover: commissions

8

Topic 24: Investment Vehicles Open-end mutual funds

Distributions of realized capital gains Generally in December Reinvest

Closed-end mutual funds Trade on exchange; no additional shares issued

Traditional open-end mutual funds grow by issuing shares Unit investment trusts:

Portfolio of bonds; not actively managed REITs: own diversified portfolio of real estate Privately/separately managed accounts

Own shares of stock rather than mutual funds Removes layer of fees Control timing of sales; taxable gains/losses

9

Topic 24: Investment Vehicles Corporate bonds

Debenture Convertible: income and growth Callable Yankee: issued by foreign banks in U.S. $

ETFs Match performance of index: S&P 500, GSCI

Diversification or specific industry Can be traded like stocks: limit order; short

Features not available with traditional mutual funds Hedge funds

Short/long; leveraged; principal protected notes High fees: 2 and 20. 2% fee plus 20% profits Low correlation with equities?

10

Topic 24: Investment Vehicles Puts

Right to sell at exercise price

Calls Right to buy at exercise price

Collar Buy put; sell call

LEAPs: long-term options Warrants: right to buy additional shares

11

Topic 25: Investment Risk Systematic: can’t diversify away Purchasing power: inflation; fixed income assets Interest rate: bonds; equities Unsystematic: can diversify away

Business: typewriters Financial: GM Liquidity: banks Marketability: 10,000 shares First-Mid Reinvestment: bonds

12

Topic 25: Investment Risk Political: Nigeria Exchange rate: international equities

Calculating return on foreign investments Impact of rising/falling dollar (Ending value in dollars – beginning value in

dollars) / beginning value in dollars Tax: increase in capital gains tax rates Investment manager: change/style drift

13

Topic 27: Quantitative Investment Concepts

Standard deviation: one: 68%; two: 95% Mean return 11%, how often fall in range of 8 – 14% if standard

deviation 3%? Computing standard deviation

Skewness: tails aren’t symmetrical Correlation coefficient:

1, 0, -1 R2:extent portfolio return explained by market return

.90 means only 10% of portfolio return not due to market (<.7 indicates lack of diversification)

Coefficient of Variation: Standard deviation/average return Measures risk to reward Same in efficient market?

14

Topic 27: Quantitative Investment Concepts

Beta: measures systematic risk. 1.0; 0; -1.0 Portfolio beta

Covariance: impact of security on portfolio’s risk Portfolio standard deviation: not weighted average

Semivariance: measures downside risk

15

Topic 27: Investment Returns Arithmetic average: sum/n Geometric mean:

Less than arithmetic as it factors in compounding Time weighted: evaluate portfolio manager

Ignores cash flows in/out of portfolio by investors Includes capital gains, and dividends received by portfolio Geometric average

Dollar weighted: evaluate investor’s performance Factors cash flows in/out of portfolio IRR calculation

Underperformance by mutual fund investors More frequent/pronounced in volatile funds

Holding period:

16

Topic 27: Investment Returns

Real return= Nominal return – Inflation rate Nominal 13% Inflation 3%

I = ((1+Nominal)/(1+Inflation))-1

Internal Rate of Return Present value of -0- If IRR>required return, present value positive Assumes cash flows reinvested at IRR Favors projects generating cash flows early

17

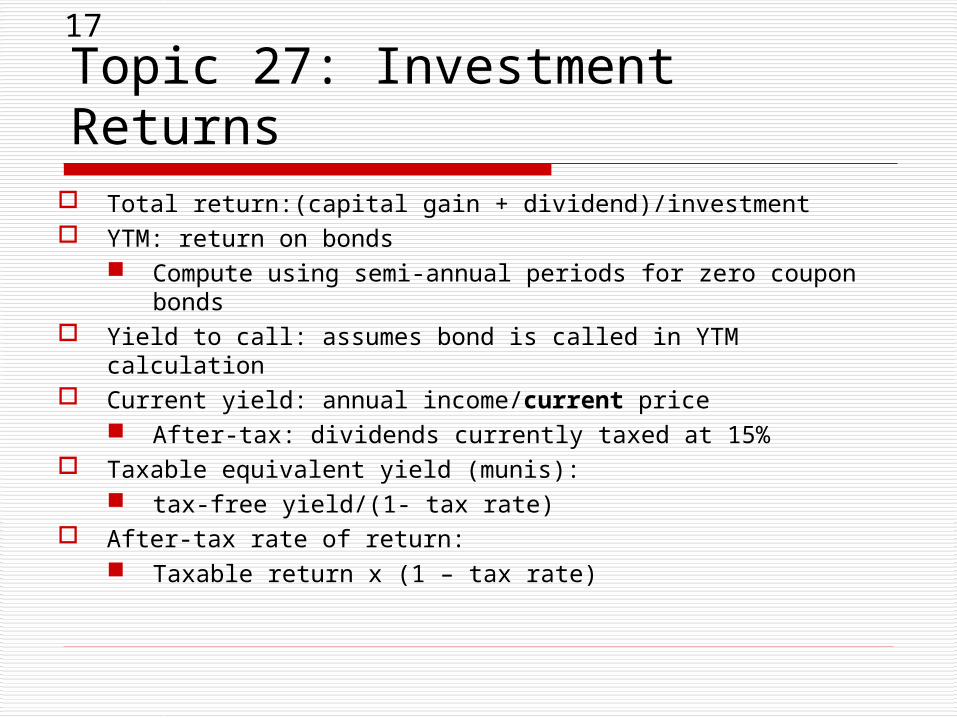

Topic 27: Investment Returns Total return:(capital gain + dividend)/investment YTM: return on bonds

Compute using semi-annual periods for zero coupon bonds Yield to call: assumes bond is called in YTM calculation Current yield: annual income/current price

After-tax: dividends currently taxed at 15% Taxable equivalent yield (munis):

tax-free yield/(1- tax rate) After-tax rate of return:

Taxable return x (1 – tax rate)

18

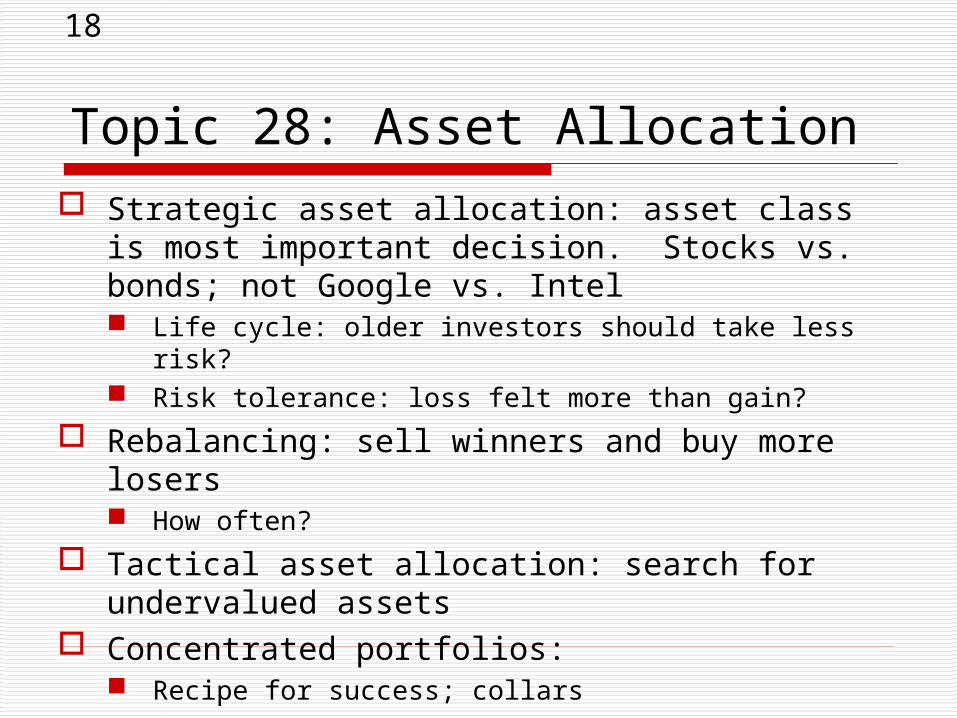

Topic 28: Asset Allocation Strategic asset allocation: asset class is most

important decision. Stocks vs. bonds; not Google vs. Intel Life cycle: older investors should take less risk? Risk tolerance: loss felt more than gain?

Rebalancing: sell winners and buy more losers How often?

Tactical asset allocation: search for undervalued assets

Concentrated portfolios: Recipe for success; collars

19

Topic 28: Asset Allocation Dynamic hedging strategy:

Move between risky assets and T bills

Correlations 1.0 vs. 0.0 vs -1.0 Stocks and bonds? Moderately low per book

20

Topic 29: Bond and Stock Valuation

Stocks: Value = PV of cash investor expects to receive Dividend growth model

No growth: Price = Dividend/Required Return Same as preferred stock valuation

Constant: Price = D1/Required Return – Growth Rate Multiple: Price = PV of Dividends

P/E ratio: high versus low PEG: high versus low Book value: Assets – Liabilities / Number of Shares

21

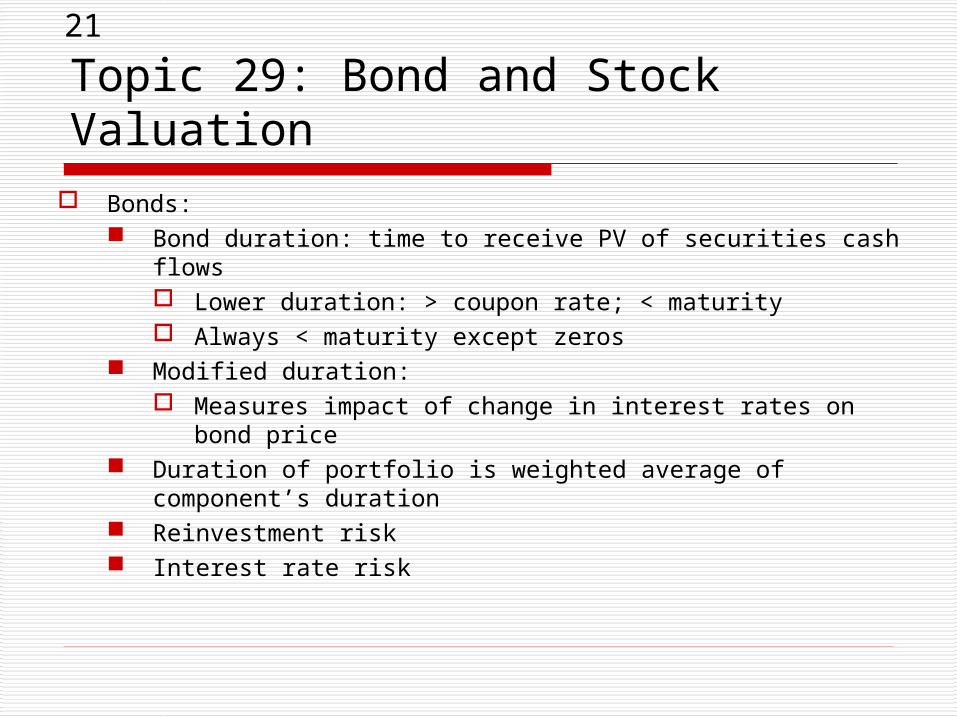

Topic 29: Bond and Stock Valuation Bonds:

Bond duration: time to receive PV of securities cash flows Lower duration: > coupon rate; < maturity Always < maturity except zeros

Modified duration: Measures impact of change in interest rates on bond price

Duration of portfolio is weighted average of component’s duration

Reinvestment risk Interest rate risk

22

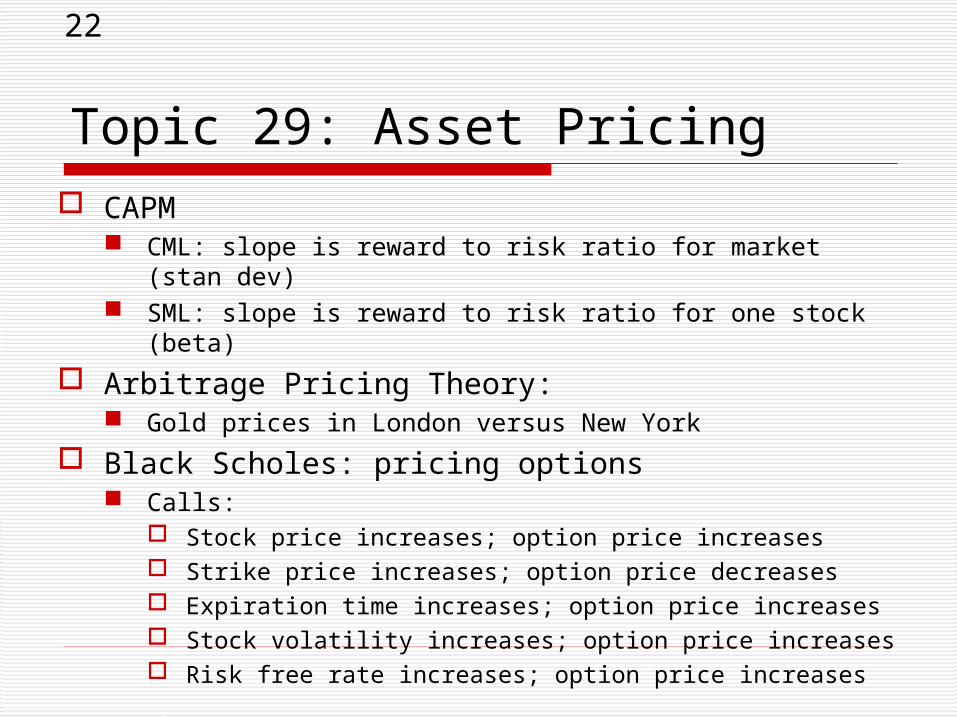

Topic 29: Asset Pricing CAPM

CML: slope is reward to risk ratio for market (stan dev) SML: slope is reward to risk ratio for one stock (beta)

Arbitrage Pricing Theory: Gold prices in London versus New York

Black Scholes: pricing options Calls:

Stock price increases; option price increases Strike price increases; option price decreases Expiration time increases; option price increases Stock volatility increases; option price increases Risk free rate increases; option price increases

23

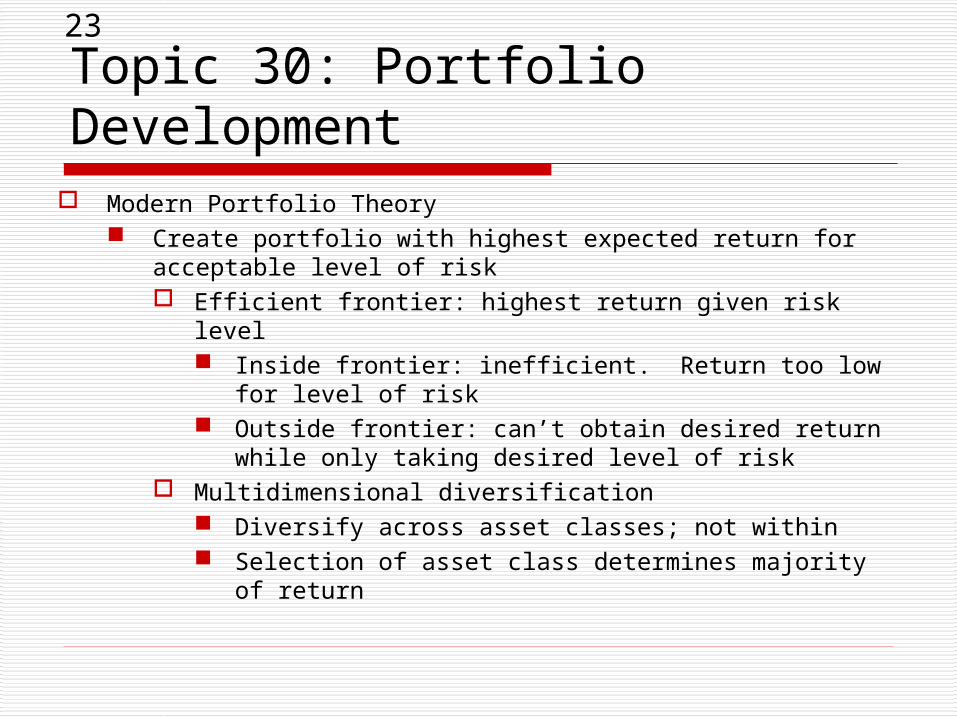

Topic 30: Portfolio Development Modern Portfolio Theory

Create portfolio with highest expected return for acceptable level of risk Efficient frontier: highest return given risk level

Inside frontier: inefficient. Return too low for level of risk

Outside frontier: can’t obtain desired return while only taking desired level of risk

Multidimensional diversification Diversify across asset classes; not within Selection of asset class determines majority of return

24

Topic 30: Portfolio Development Capital Market Line: Investor’s required return =

Risk free + Portfolio Stan Dev x (Market Ret – Risk Free) / Stan Dev Mkt

Formula provided Uses standard dev: includes systematic/unsystematic

25

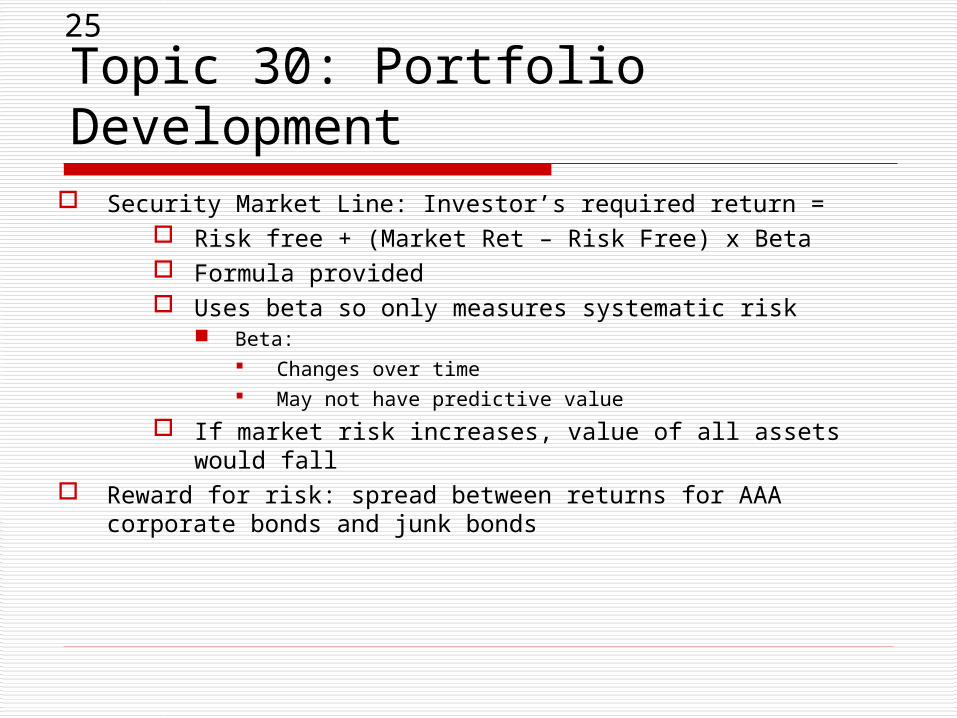

Topic 30: Portfolio Development Security Market Line: Investor’s required return =

Risk free + (Market Ret – Risk Free) x Beta Formula provided Uses beta so only measures systematic risk

Beta: Changes over time May not have predictive value

If market risk increases, value of all assets would fall Reward for risk: spread between returns for AAA corporate bonds

and junk bonds

26

Topic 30: Portfolio Development Efficient Market Hypothesis

Strong form Prices reflect public and insider info

Unable to outperform market All assets fairly priced reflecting all known info Index

Semi strong Prices reflect public info

Weak Prices reflect price/volume data Technical analysis has no value

But fundamental analysis can improve returns

27

Topic 30: Portfolio Development Market Anomalies

Strategy that seems to outperform market Low P/E ratios Small cap stocks January effect Value Line: 1 recommendations

Behavioral finance Investors are not rational

Loss avoidance Desire to break even Automatic 401(k) enrollment

28

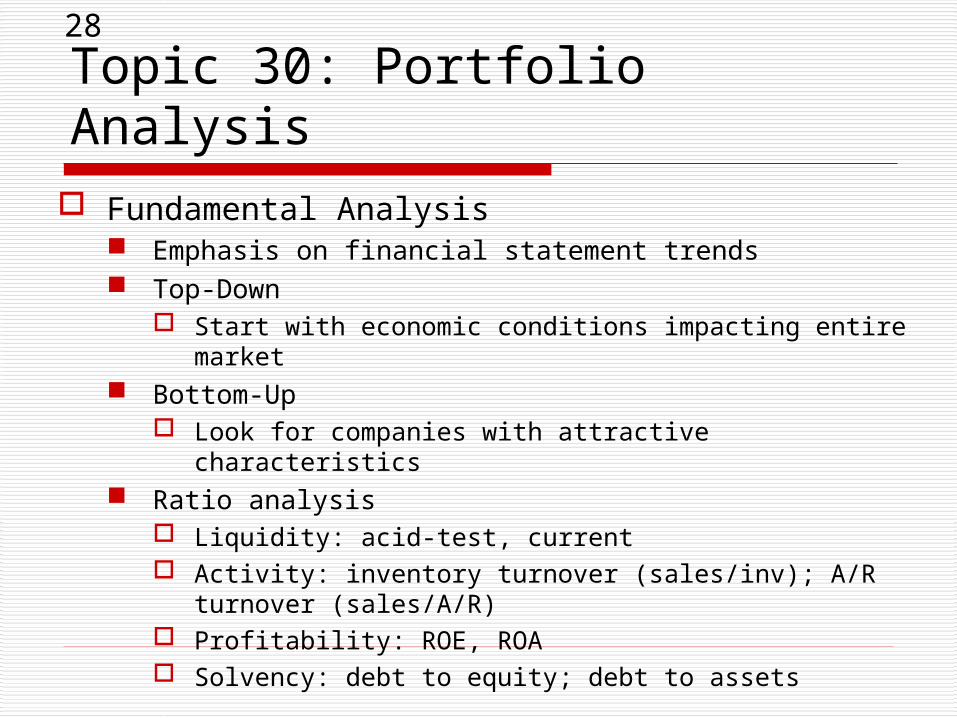

Topic 30: Portfolio Analysis Fundamental Analysis

Emphasis on financial statement trends Top-Down

Start with economic conditions impacting entire market Bottom-Up

Look for companies with attractive characteristics Ratio analysis

Liquidity: acid-test, current Activity: inventory turnover (sales/inv); A/R turnover

(sales/A/R) Profitability: ROE, ROA Solvency: debt to equity; debt to assets

29

Topic 30: Portfolio Analysis Technical Analysis

Past movement of security prices predict future Breaking through 50 day moving average Dow Theory: Transports confirm Industrials

Overall market Dow Transports confirms move in Dow Industrials Barron’s confidence index: spread between junk and

investment grade corporate debt Odd-lot: contrarian

Specific securities Moving average Put/call: contrarian Short-interest: future buyers

30

Topic 30: Portfolio Analysis Investment policy statement

Guidelines for selecting portfolio assets Appropriate levels of risk; bond duration, etc.

Benchmarks Comparable to portfolio’s objective/risk S&P 500; Wilshire 5000; EAFE

Monte Carlo Simulations generally using past price movements

Probability of outliving portfolio

31

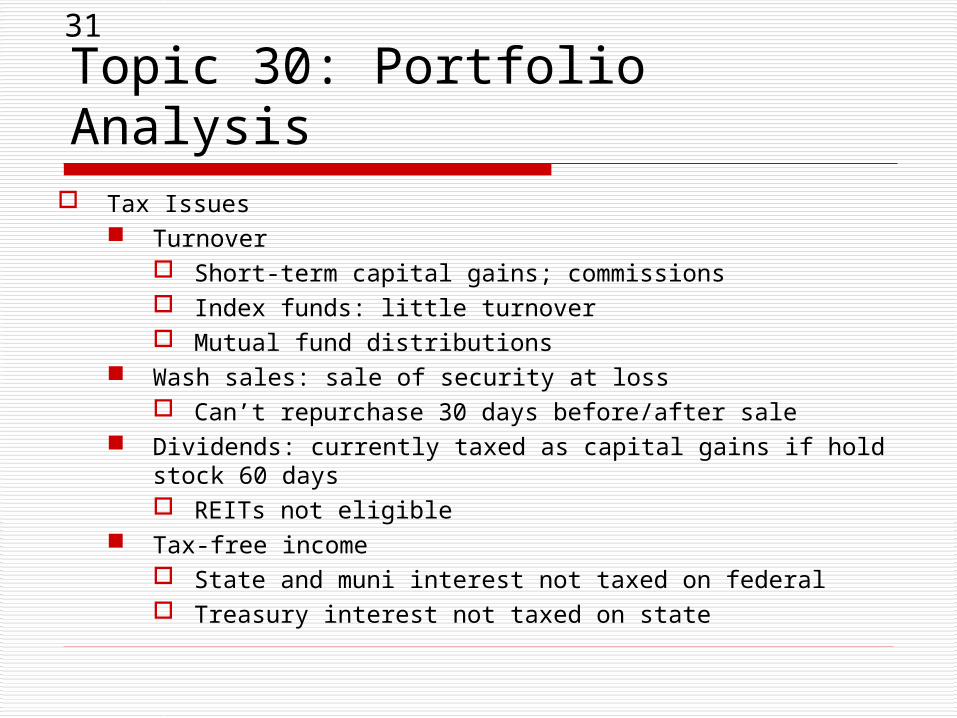

Topic 30: Portfolio Analysis Tax Issues

Turnover Short-term capital gains; commissions Index funds: little turnover Mutual fund distributions

Wash sales: sale of security at loss Can’t repurchase 30 days before/after sale

Dividends: currently taxed as capital gains if hold stock 60 days REITs not eligible

Tax-free income State and muni interest not taxed on federal Treasury interest not taxed on state

32

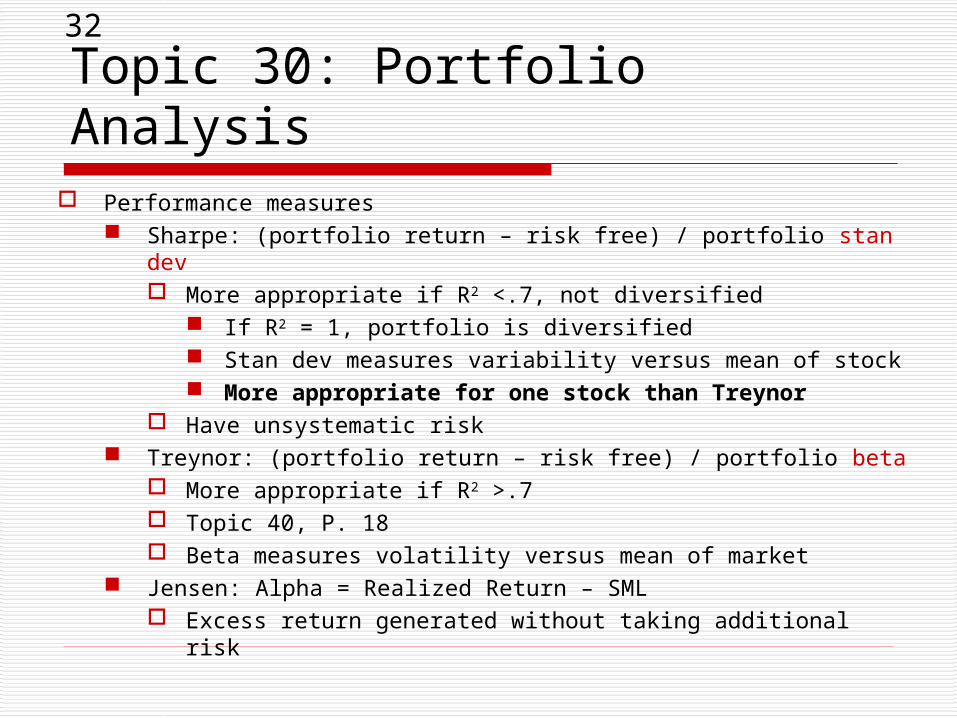

Topic 30: Portfolio Analysis Performance measures

Sharpe: (portfolio return – risk free) / portfolio stan dev More appropriate if R2 <.7, not diversified

If R2 = 1, portfolio is diversified Stan dev measures variability versus mean of stock More appropriate for one stock than Treynor

Have unsystematic risk Treynor: (portfolio return – risk free) / portfolio beta

More appropriate if R2 >.7 Topic 40, P. 18 Beta measures volatility versus mean of market

Jensen: Alpha = Realized Return – SML Excess return generated without taking additional risk

33

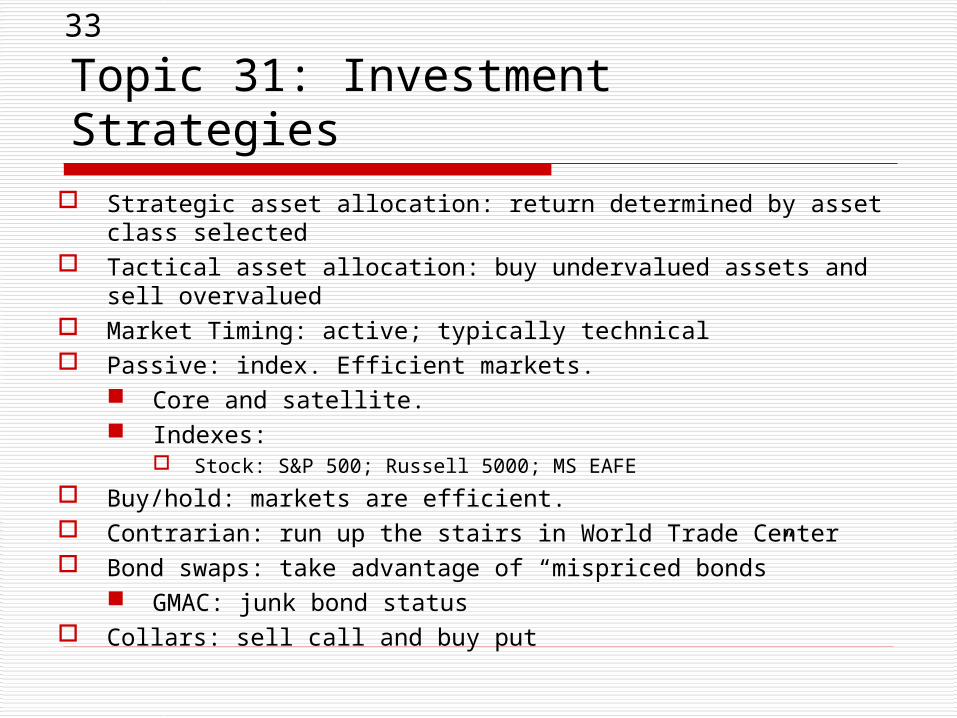

Topic 31: Investment Strategies Strategic asset allocation: return determined by asset class

selected Tactical asset allocation: buy undervalued assets and sell

overvalued Market Timing: active; typically technical Passive: index. Efficient markets.

Core and satellite. Indexes:

Stock: S&P 500; Russell 5000; MS EAFE

Buy/hold: markets are efficient. Contrarian: run up the stairs in World Trade Center Bond swaps: take advantage of “mispriced bonds”

GMAC: junk bond status Collars: sell call and buy put

34

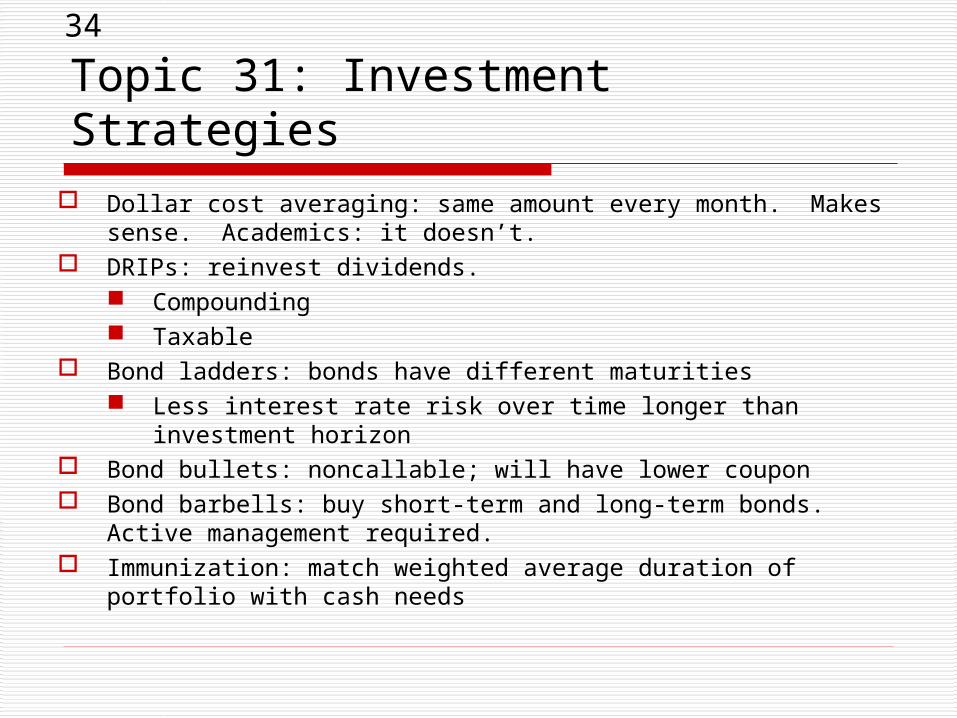

Topic 31: Investment Strategies Dollar cost averaging: same amount every month. Makes sense.

Academics: it doesn’t. DRIPs: reinvest dividends.

Compounding Taxable

Bond ladders: bonds have different maturities Less interest rate risk over time longer than investment

horizon Bond bullets: noncallable; will have lower coupon Bond barbells: buy short-term and long-term bonds. Active

management required. Immunization: match weighted average duration of portfolio with

cash needs

35

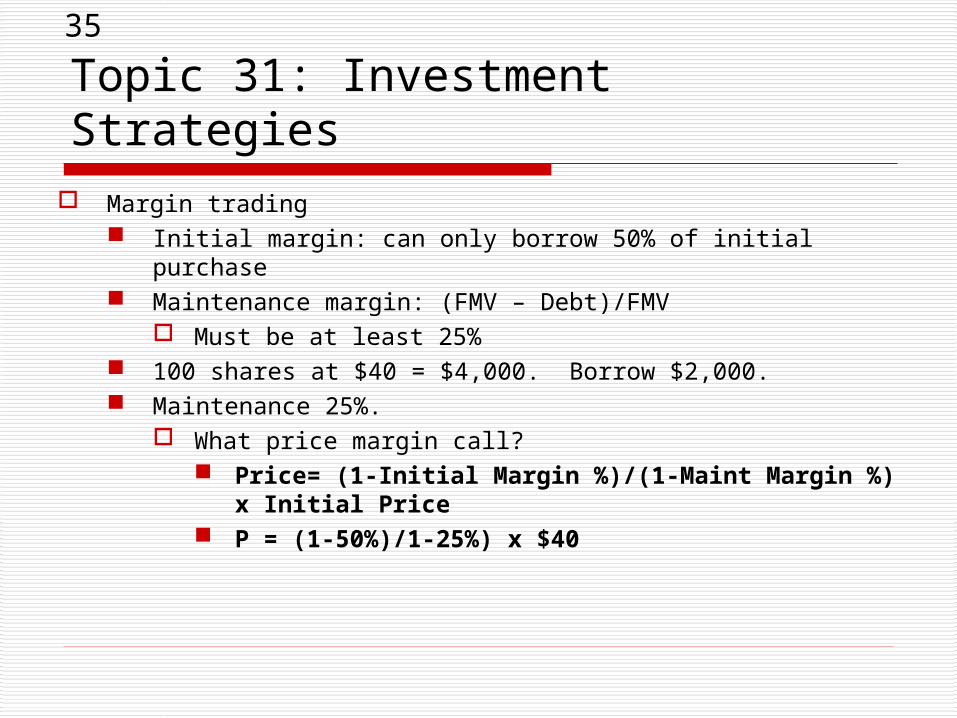

Topic 31: Investment Strategies Margin trading

Initial margin: can only borrow 50% of initial purchase Maintenance margin: (FMV – Debt)/FMV

Must be at least 25% 100 shares at $40 = $4,000. Borrow $2,000. Maintenance 25%.

What price margin call? Price= (1-Initial Margin %)/(1-Maint Margin %) x

Initial Price P = (1-50%)/1-25%) x $40

36

Topic 31: Investment Strategies Margin trading

Amount of margin call if price falls to $22? Current Value of Stock x Maint Margin % = Equity Needed $2,200 x 25% = $550 Present Equity = $2,200 Current Value - $2,000 Debt = $200 Margin Call = $550 - $200 =$350

37

Topic 31: Investment Strategies Short selling: sell borrowed stock; buy back at lower price

Uptick rule eliminated June 2007 Reinstated for financial stocks during 2008

Stock owner gets dividends Must have margin account; broker determines

maintenance margin

38

Topic 31: Investment Strategies

Hedging: protect against price moves in assets own. Buy a $3.50 put on December corn.

Options Puts: buy and sell

Naked Calls: buy and sell

Covered Topic 41, Problems 25 and 32

LEAPS: as long as three years

39

Topic 31: Investment Strategies

Straddle: buy put/call on same stock at same strike price Anticipate big move either way

Collar: sell call, buy put Concentrated positions

Spread: Buy and sell a call at different prices or expirations

Taxation of options Buy call, exercise: add to basis Buy call, expires: short-term capital loss Sell call, exercised: add to proceeds Sell call, expires: short-term capital gain

40

Topic 31: Investment Strategies

Taxation of options Buy put, exercise: add to basis Buy put, expires: short-term capital loss Sell put, exercised: reduce basis Sell put, expires: short-term capital gain