1 Published Account. 2 Introduction Limited liability companies are governed by Companies Ordinance...

39

1 Published Account

-

Upload

rosalyn-chambers -

Category

Documents

-

view

217 -

download

3

Transcript of 1 Published Account. 2 Introduction Limited liability companies are governed by Companies Ordinance...

1

Published Account

2

Introduction

Limited liability companies are governed by Companies Ordinance (Cap.32 Tenth Schedule) to prepare and publish accounts annually which should have to comply with Hong Kong Statements of Standard Accounting Practice (HKSSAP) issued by Hong Kong Society of AccountantsPublished accounts set out in standardized format

3

Components of Published Accounts

Components need special attention:

- Extraordinary items- Exceptional items- Prior year adjustments- Post balance sheet events - Contingencies

4

Exceptional items

5

Exceptional ItemsDefinition

Items related to the ordinary activities of the businessbut due to exceptional size, nature or incidenceItems must be material in size, unusual in nature and expected not to recur frequently and regularly

Exampleexceptional bad debts are written off profits or losses related to discontinued operations

e.g. loss on the closure of a transport depotexceptional bad debts are written off profits or losses on the disposal of long-term investments

e.g. profit on the disposal of a subsidiary company

6

Exceptional ItemsExample (cont’l)

exceptional bad debts are written off profits or losses on the disposal of fixed assets

e.g. loss on the disposal of land, machinery or equipmentexceptional bad debts are written off

e.g. a major debtor is declared bankruptexceptional stock is written off

e.g. a large amount of obsolete stockamortization of intangible fixed assets which had been capitalized previously

e.g. write off goodwill at 2% per annumincome or expenses arising from the restructuring of the activities of a businessamounts transferred to employee share schemesamounts of litigation settlements

7

Disclosure requirement:

Disclosed in the published profit and loss account as follows:$ $

Profit before taxation is arrived at X after charging:

Depreciation XDirector’s remuneration XAudit fee XHire of plant XInterest XExceptional loss X

And after crediting:Income from investment XRental income XExceptional gain X

Exceptional Items

8

Extraordinary items

9

Extraordinary Items

Definitionthose items which are derived from events or transactions outside the ordinary activities of the businessitems which are material and expected not to recur frequently and regularly.Events which are completely outside the control of the management

Examples:- Losses arising from a natural catastrophe- Losses arising from the expropriation of assets

10

Extraordinary Items

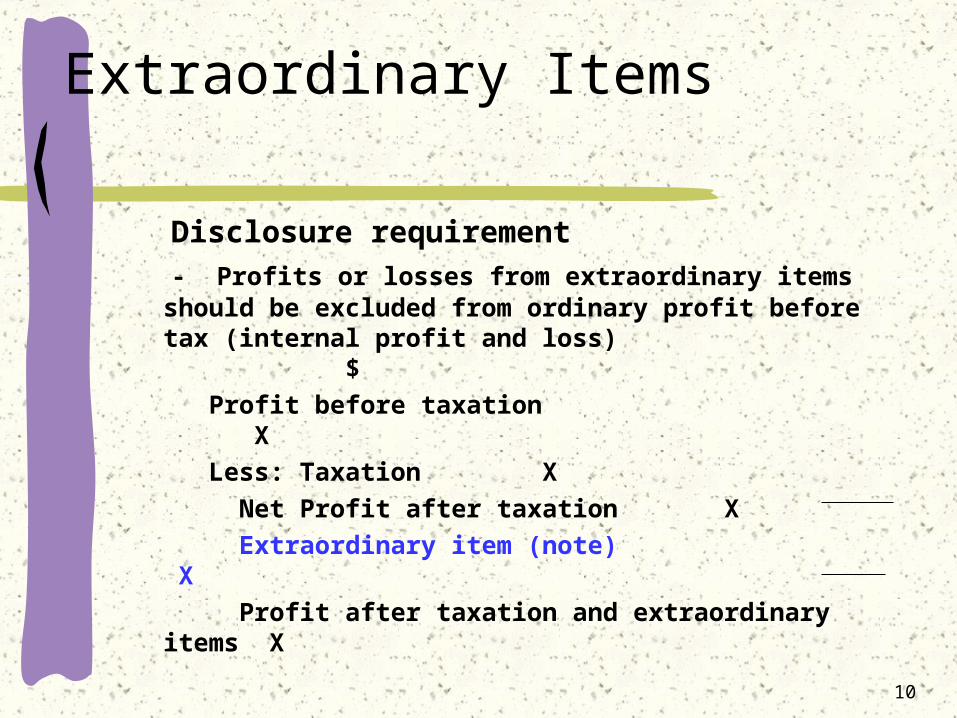

Disclosure requirement - Profits or losses from extraordinary items

should be excluded from ordinary profit before tax (internal profit and loss) $

Profit before taxation X Less: Taxation X

Net Profit after taxation X Extraordinary item (note) X Profit after taxation and extraordinary items X

11

Prior Year Adjustment

12

Prior Year Adjustments

DefinitionMaterial adjustments made to the previous year’s retained profits of there is a fundamental error in one of the previous year’s accounts or a change in the accounting policy

Example- fundamental error in previous year

- the omission of a significant amount of purchases in the previous year.

13

Prior Year Adjustments

Example- change in accounting policy- Completely written off intangible fixed assets

(research and development expenditures or goodwill) which had been capitalized previously

- Change in stock valuation method- Change in depreciation method

14

Disclosure RequirementOpening retained profits should be adjusted:

$ $Profit before taxation XLess: Taxation X

XAdd/less: Extraordinary item XProfit after tax and extraordinary item XLess: Appropriation X

Retained profits for the year XAdd: Retained profit bought forward XRetained profits brought forward XAdd/Less: Prior year adjustment X X

Prior Year Adjustments

•A note is required to show the nature of the prior yearadjustment

15

Contingencies

16

Contingencies

Definitioncondition which exists at the balance sheet date, where the outcome will be confirmed only on the occurrence or non occurrence of one or more uncertain future events

17

Contingencies

Possibility of Occurrence

For Contingent Gain

For Contingent

LossWith certainty Accruals Accruals

Probable A contingency(to be disclosed in

notes)

Accruals

Possible Not to disclose A Contingency(to be disclosed

in notes)

With a slight chance Not to disclose Not to disclose

Accounting treatment- depending on the degree of contingency

18

Contingencies

Examples of contingent losses:- A discounted bill of exchange- A guarantee given for a borrowing by another company- A pending legal claim

Example of a contingent gain:- A pending litigation settlement from another company

Disclosure requirement:Contingencies should not be recognized in the accounts. A note is required to describe the nature of a contingency.

19

Post Balance Sheet Events

20

Post Balance Sheet Events

Definition:Those events, both favourable and unfavourable, which occur between the balance sheet date and the date on which the financial statements are approved by the board of directors

21

Post Balance Sheet Events

Adjusting EventsNon-adjusting Events

22

Adjusting Events

Definition:Those events, both favourable or unfavourable, which occur between the balance sheet date and the date on which the financial statements are approved by the board of directors

23

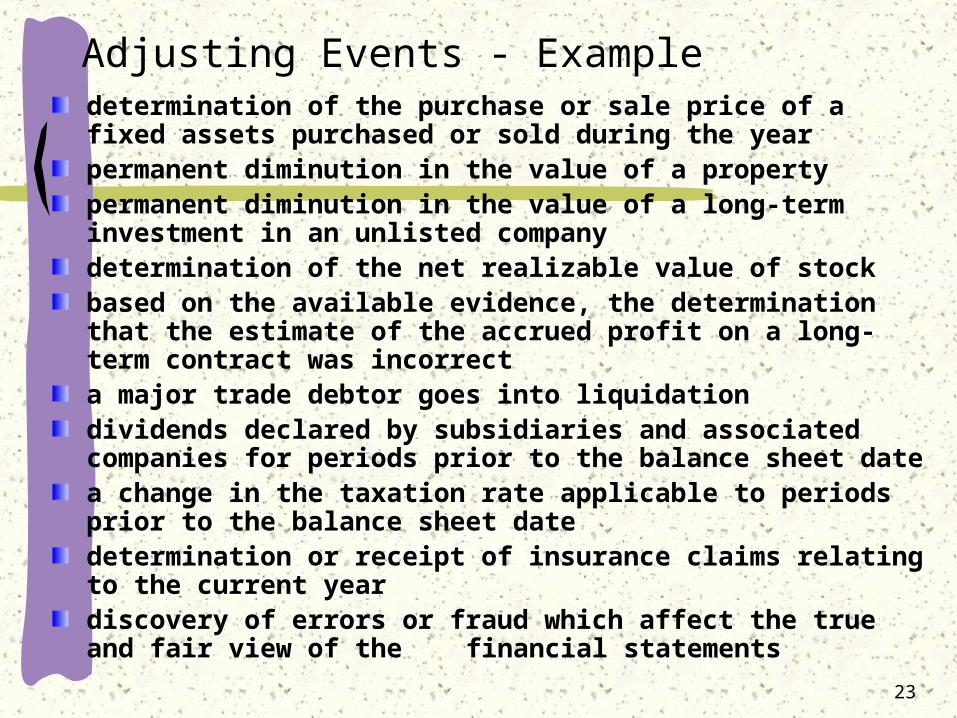

Adjusting Events - Exampledetermination of the purchase or sale price of a fixed assets purchased or sold during the yearpermanent diminution in the value of a propertypermanent diminution in the value of a long-term investment in an unlisted companydetermination of the net realizable value of stockbased on the available evidence, the determination that the estimate of the accrued profit on a long-term contract was incorrecta major trade debtor goes into liquidationdividends declared by subsidiaries and associated companies for periods prior to the balance sheet datea change in the taxation rate applicable to periods prior to the balance sheet datedetermination or receipt of insurance claims relating to the current yeardiscovery of errors or fraud which affect the true and fair view of the financial statements

24

Non-adjusting Events

DefinitionThose events which concern conditions that did not exist at the balance sheet date.

25

Non-adjusting Events - Example

mergers and acquisitionsreconstructions and proposed reconstructionsissuance of shares and debenturespurchases and sales of fixed assets and investmentslosses of fixed assets as a result of a disaster such as fire or floodextending trading activities or starting new activitieschanges in foreign exchange ratesgovernment actions such as the expropriation of assetsstrikes and industrial actionschanges in pension benefits

26

Example

Refer to textbook P. 159

27

Harbour Ltd.Profit and Loss Account for the year ended 31 December 1994

$ $

after charging:

and after crediting:

Turnover (note 1) 1,881,600Profit before taxation is arrived at (working) 111,600

Fire loss (2) 20,000

Auditor’s remuneration (2) 1,000Directors’ remuneration (25600+5000) (2) 30,600Goodwill written off (2) 1,500Debenture interest ($200,000 x 4%) (2,12) 8,000

Loss on disposal (trial) 2,000Exceptional bad debts (13) 70,000

Depreciation (note 1,3) 29,600

Income from quoted investments 3,000Income from unquoted investments 1,000

Profit tax for the year (1) 44,000Less: overprovision in previous year (1) 2,200 41,800

69800

28

Adjustment for profit before tax:

Original 185600Less disposal loss (trial) 2000

Bad debt (13) 70000Debenture interest (8000-6000) (12,2) 2000

11600

Working:

29

Cont’

$ $ 69,806

Appropriations:

Debenture redemption reserve (trial) 50,000Dividends (400000*0.0402) (1) 16,080 66,080

Retained profits for the year 3,720Retained profits brought forward (trial) 86,200

Less: Prior year adjustment (note 2) 1,200 85,00088,720

30

Harbour Ltd.Balance Sheet as at 31 December 1994

$ $ $

Intangible Fixed Assets

Investments

Fixed Assets (note 3)1,149,000

Goodwill (trial) 4500

Quoted investments, at cost (market value: $57,000) (4, trial) 50,000Current Assets

Stocks (5, trial) 108,460Debtors (80000-70000-1200) (13, trial) 8,800

Bills Receivable (trial) 22000Prepayment (trial) 7600

Short-term investment, at cost (director’s valuation: $38,000) (14, trial) 30,000Called up capital not paid (250*0.6) (14) 150

Cash at bank (trial) 285,670462,680

31

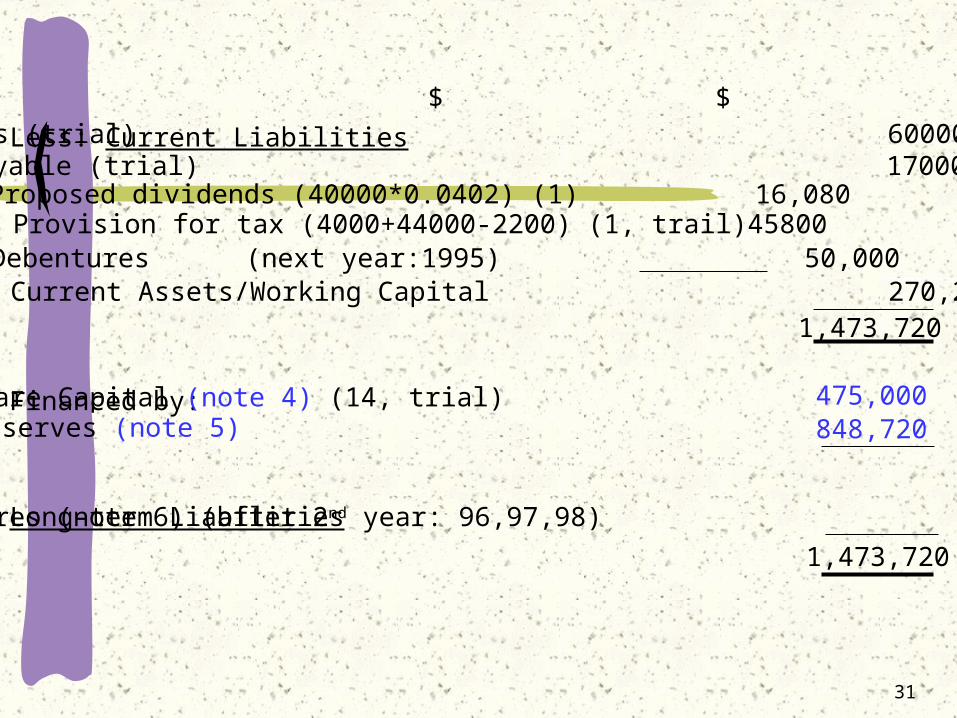

$ $

Less: Current Liabilities

Financed by:

Long-term Liabilities

Creditors (trial) 60000Bills Payable (trial) 17000

Proposed dividends (40000*0.0402) (1) 16,080Provision for tax (4000+44000-2200) (1, trail)458004% Debentures (next year:1995) 50,000

Net Current Assets/Working Capital 270,2201,473,720

Share Capital (note 4) (14, trial)Reserves (note 5)

475,000848,720

4% Debentures (note 6) (after 2nd year: 96,97,98) 150,0001,473,720

32

Harbour Ltd.Notes to the Accounts

1. Principal Accounting Policies(a)Turnover

Turnover represents the invoiced amount of goods sold less returns.(b)Depreciation

Depreciation is calculated to write off the cost of fixed assets over their estimated useful lives on a straight line basis at the following annual rates:

Buildings 2%Plant and machinery 10%Office equipment 15%

No depreciation is provided on leasehold land.( c )Stocks

Stocks are valued at the lower of cost and net realizable value. Cost is determined on a first-in-first-out basis. Work in progress and finished goods include an appropriate proportion of production overhead expenses.(d)Goodwill

Goodwill is amortized over a period of 5 years in equal instalments.

33

2. Prior Year AdjustmentThe prior year adjustment relates to a change of accounting policy in the treatment of development expenditures.

34

3. Fixed assets

Aggregate DepAt 1 Jan 94DisposalsCharge for the year(3)At 31 Dec 94 (trial)

Net book valueAt 31 Dec 93At 31 Dec 94

Land

$000

Buildings

$000

Plant andMachiner

y$000

OfficeEquipme

nt$000

Total$000

2.3100.0

108.0(12.0)24.0

120.0

4.7

3.38.0

210.4(12.0)29.6

228.0

400.01,000.0

17.315.0

192.0120.0

17.314.0

626.61,149.

115000*2% 24000*10% 22000*15%

400.0 300.0115.0

600.0115.01000.0

(60.0)

240.0

22.0

22.0

837.0(60.0)600.0

1,377.0

240+60 (11, trial)

Cost

At 1 Jan 94

Disposals (11)

Revaluation (3)

At 31 Dec 94

35

During the year, the leasehold land was revalued to $1,000,000 and the surplus on revaluation of $600,000 was credited directly to the revaluation reserve. The valuation was made by a firm of independent valuers.

36

4. Share Capital$

Authorized:1,000,000 ordinary shares of $1 each 1,000,000Issued and called up:475,000 ordinary shares of $1 each 475,000

In March 1994, 75,000 ordinary shares were offered to the public at

1.8 per share payable as follows:On application $1.2 per share including premiumOn allotment $0.6 per shareThese new shares rank pari passu in all respects with the existingshares except that they are not entitled to receive the final divide

nd declared for the year.

37

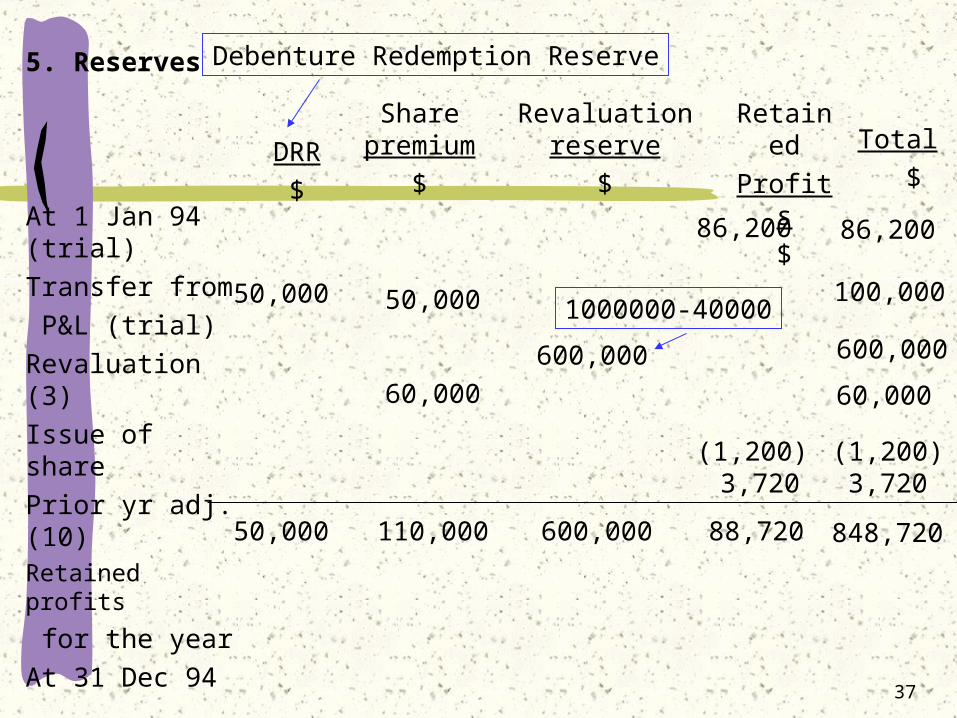

5. Reserves

At 1 Jan 94 (trial)Transfer from P&L (trial)Revaluation (3)Issue of sharePrior yr adj. (10)Retained profits

for the yearAt 31 Dec 94

DRR$

Share premium

$

Revaluation reserve

$

Retained

Profits$

Total $

Debenture Redemption Reserve

50,000

50,000 50,000

60,000

110,000

600,000

600,000

86,200

(1,200)3,720

88,720

100,000

86,200

600,00060,000

(1,200)3,720

848,720

1000000-40000

38

6. 4% Debentures (12)The company redeemed $50,000 4% debentures on 1 Jan. 94 at par.

7. Capital Commitments (6)Commitments outstanding at 31 Dec. 1994 not provided for in the financial statement were as follows:

$Contracted for

200,000Authorized but not contracted for 300,000

500,000

250000/5

39

8. Contingent Liabilities (7)At 31 Dec. 1994, there was an unsecured guarantee given by the company for the bank overdraft facility of a supplier in the amount of $95,000.

9. Post Balance Sheet Event (8)On 3 Jan. 1995, the company acquired the business of Foreign Company for a cash consideration of $139,000.