1 Project I Econ 240c Spring 2006. 2 Issues Parsimonious models 2006: March or April 9.3 wks or...

68

1 Project I Project I Econ 240c Spring 2006 Econ 240c Spring 2006

-

date post

19-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of 1 Project I Econ 240c Spring 2006. 2 Issues Parsimonious models 2006: March or April 9.3 wks or...

11

Project IProject I

Econ 240c Spring 2006Econ 240c Spring 2006

22

IssuesIssues Parsimonious modelsParsimonious models 2006: March or April 9.3 wks or 8.9 wks2006: March or April 9.3 wks or 8.9 wks TrendTrend Residual seasonalityResidual seasonality Forecasts: sharp peaks or broad peaks?Forecasts: sharp peaks or broad peaks? Model selectionModel selection The labor marketThe labor market

TrendTrend Broad peaksBroad peaks

33

∆ ∆ durationduration : ar(1) ar(4) ar(24) ar(36): ar(1) ar(4) ar(24) ar(36) : ma(1) ma(4) ma(24) ma(36): ma(1) ma(4) ma(24) ma(36) : ar(1) ar(2) ma(1) ma(2): ar(1) ar(2) ma(1) ma(2)

44

∆ ∆ lndurationlnduration : ma(1) ma(4) sma(24) sma(36): ma(1) ma(4) sma(24) sma(36) : ma(1) ma(4) ar(24) ar(36): ma(1) ma(4) ar(24) ar(36) : ar(1) ar(2) ma(1) ma(2): ar(1) ar(2) ma(1) ma(2) : ar(1) ma(1) ma(2) ma(3): ar(1) ma(1) ma(2) ma(3)

55

OutlineOutline

Duration Model: trend and arma error, p.6Duration Model: trend and arma error, p.6 Dduration model: arma(2,2), p. 29Dduration model: arma(2,2), p. 29

66

Duration in LevelsDuration in Levels TrendTrend Duration = a + b*t +arma errorDuration = a + b*t +arma error IdentificationIdentification EstimationEstimation Model VerificationModel Verification Within Sample Forecasting, a Test of the Within Sample Forecasting, a Test of the

ModelModel ForecastsForecasts

77

2

4

6

8

10

12

14

70 75 80 85 90 95 00 05

DURATION

88

99

-4

-2

0

2

4

6

2

4

6

8

10

12

14

70 75 80 85 90 95 00 05

Residual Actual Fitted

Trend Model: Duration

1010

0

10

20

30

40

4 5 6 7 8 9 10 11 12

Series: DURATIONSample 1967:07 2006:04Observations 466

Mean 7.097639Median 6.900000Maximum 12.30000Minimum 4.000000Std. Dev. 1.651788Skewness 0.304644Kurtosis 2.365030

Jarque-Bera 15.03663Probability 0.000543

1111

1212

1313

1414

-2

-1

0

1

2

2

4

6

8

10

12

14

70 75 80 85 90 95 00 05

Residual Actual Fitted

ARMA-Trend Model for Duration

1515

1616

1717

Conditional Conditional Heteroskedasticity?Heteroskedasticity?

1818

1919

0

10

20

30

40

50

60

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

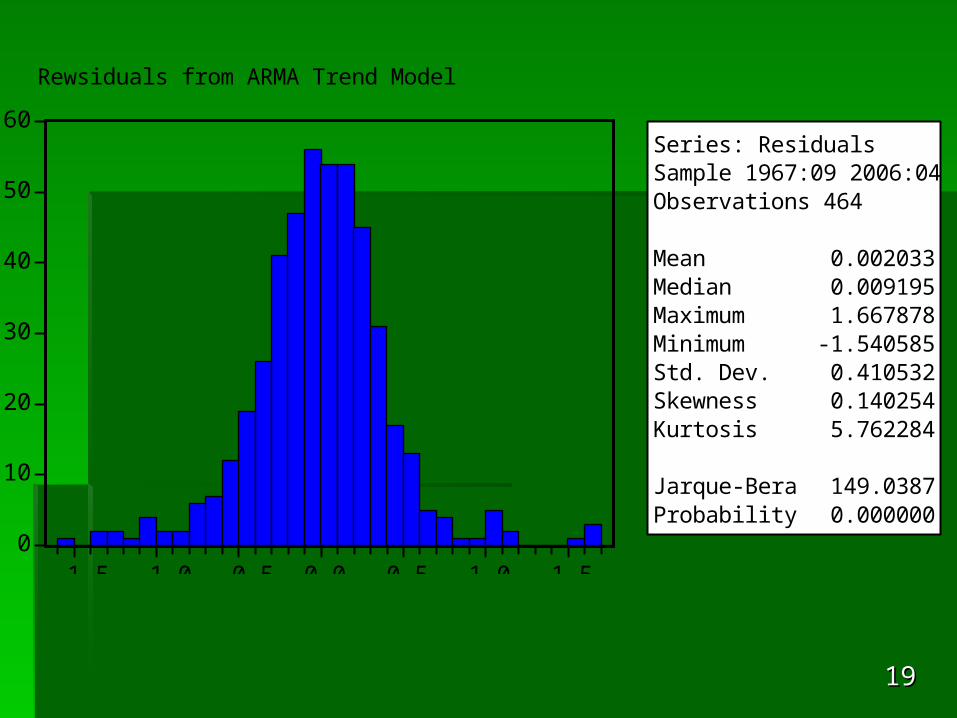

Series: ResidualsSample 1967:09 2006:04Observations 464

Mean 0.002033Median 0.009195Maximum 1.667878Minimum -1.540585Std. Dev. 0.410532Skewness 0.140254Kurtosis 5.762284

Jarque-Bera 149.0387Probability 0.000000

Rewsiduals from ARMA Trend Model

2020

Within Sample TestWithin Sample Test

2121

6

7

8

9

10

11

05:05 05:07 05:09 05:11 06:01 06:03

DURATIONF ± 2 S.E.

Forecast: DURATIONFActual: DURATIONSample: 2005:05 2006:04Include observations: 12

Root Mean Squared Error 0.242936Mean Absolute Error 0.196195Mean Abs. Percent Error 2.213545Theil Inequality Coefficient 0.013909 Bias Proportion 0.009928 Variance Proportion 0.618213 Covariance Proportion 0.371859

2222

2323

Quick Menu, ShowQuick Menu, Show

2424

2

4

6

8

10

12

14

70 75 80 85 90 95 00 05

DURATIONTEST

TEST+2*SEFTEST-2*SEF

Forecast: 2005.05-2006.04, ARMA Trend model

2525

Forecast: 2006.05-Forecast: 2006.05-2007.122007.12

5

6

7

8

9

10

11

12

06:07 06:10 07:01 07:04 07:07 07:10

DURATIONFF ± 2 S.E.

2626

2727

Quick Menu, ShowQuick Menu, Show

2828

2

4

6

8

10

12

14

70 75 80 85 90 95 00 05

DURATIONFORECASTFF

FORECASTFF+2*SEFFFORECASTFF-2*SEFF

Forecast 2006.04-2007.12, ARMA trend Model

2929

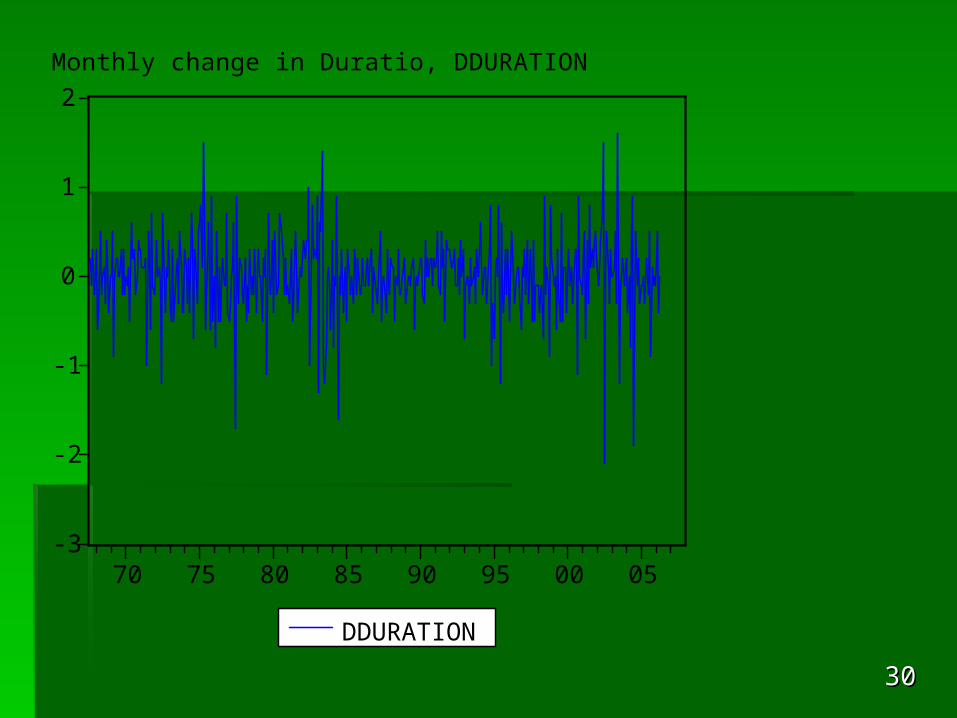

Monthly Change in Monthly Change in DurationDuration

3030

-3

-2

-1

0

1

2

70 75 80 85 90 95 00 05

DDURATION

Monthly change in Duratio, DDURATION

3131

0

10

20

30

40

50

60

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

Series: DDURATIONSample 1967:08 2006:04Observations 465

Mean 0.008602Median 0.000000Maximum 1.600000Minimum -2.100000Std. Dev. 0.443695Skewness -0.556232Kurtosis 6.021120

Jarque-Bera 200.8168Probability 0.000000

3232

3333

3434

3535

3636

3737

3838

Dduration: ar(1) ar(2), Dduration: ar(1) ar(2), ma(1)ma(1)

3939

Dduration: ar(1) ar(2), Dduration: ar(1) ar(2), ma(2)ma(2)

4040

Model Model

4141

DiagnosticsDiagnostics

-2

-1

0

1

2

-3

-2

-1

0

1

2

70 75 80 85 90 95 00 05

Residual Actual Fitted

ARMA(2,2) Model for DDuration

4242

4343

4444

4545

4646

0

10

20

30

40

50

60

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

Series: ResidualsSample 1967:10 2006:04Observations 463

Mean -0.001033Median 0.008725Maximum 1.657726Minimum -1.584772Std. Dev. 0.416357Skewness -0.111928Kurtosis 5.581513

Jarque-Bera 129.5305Probability 0.000000

Residuals from ARMA(2,2) Model of DDuration

4747

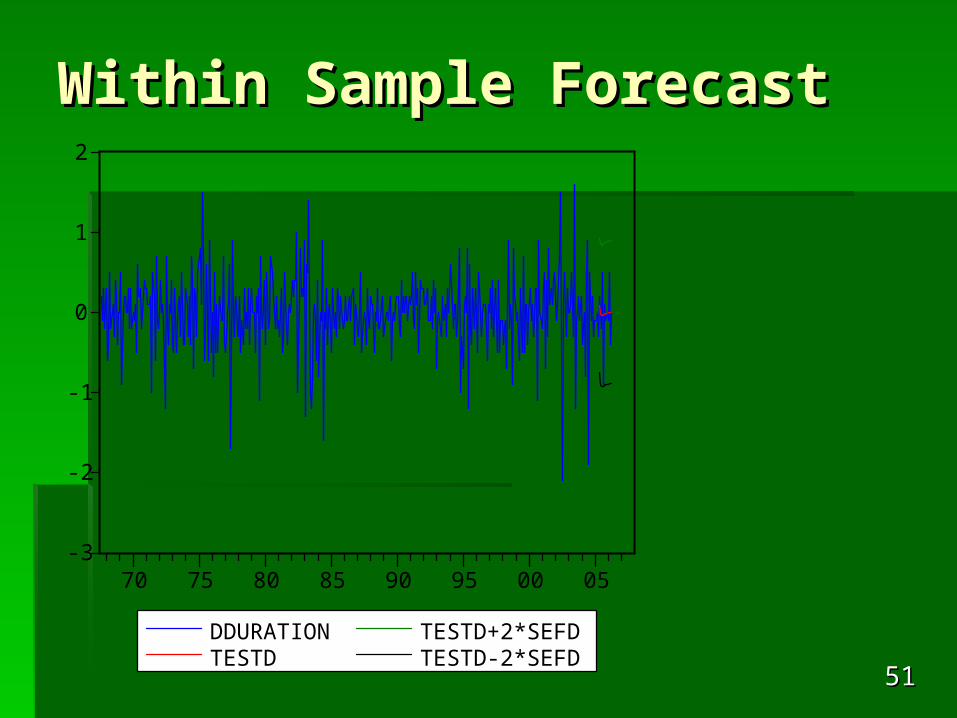

Within Sample ForecastWithin Sample Forecast

4848

-1.0

-0.5

0.0

0.5

1.0

05:05 05:07 05:09 05:11 06:01 06:03

DDURATIONF ± 2 S.E.

Forecast: DDURATIONFActual: DDURATIONSample: 2005:05 2006:04Include observations: 12

Root Mean Squared Error 0.357149Mean Absolute Error 0.242394Mean Abs. Percent Error 70.55898Theil Inequality Coefficient 0.901135 Bias Proportion 0.007489 Variance Proportion 0.843115 Covariance Proportion 0.149396

4949

5050

Quick menu, showQuick menu, show

5151

Within Sample ForecastWithin Sample Forecast

-3

-2

-1

0

1

2

70 75 80 85 90 95 00 05

DDURATIONTESTD

TESTD+2*SEFDTESTD-2*SEFD

5252

Out of Sample ForecastOut of Sample Forecast

5353

-1.0

-0.5

0.0

0.5

1.0

06:07 06:10 07:01 07:04 07:07 07:10

DDURATIONFF ± 2 S.E.

5454

5555

-3

-2

-1

0

1

2

70 75 80 85 90 95 00 05

DDURATIONDDURFORE

DDURFORE+2*SEFFDDDURFORE-2*SEFFD

Out of Sample Forecast for DDuration: 2006.05-2007.12

5656

5757

5858

5959

2

4

6

8

10

12

14

70 75 80 85 90 95 00 05

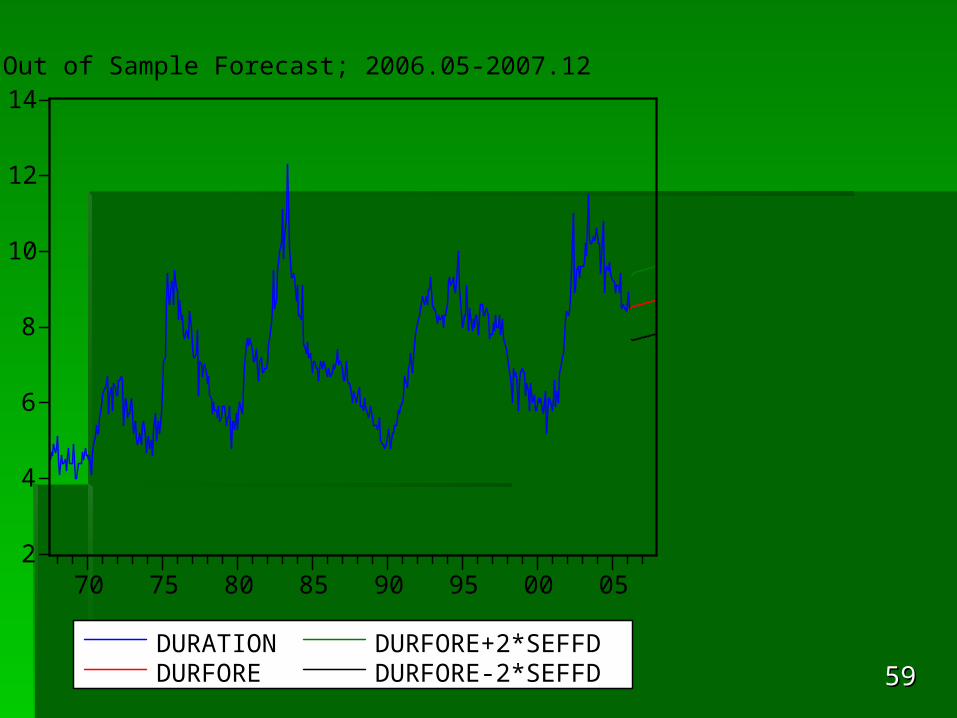

DURATIONDURFORE

DURFORE+2*SEFFDDURFORE-2*SEFFD

Out of Sample Forecast; 2006.05-2007.12

6060

2

4

6

8

10

12

14

70 75 80 85 90 95 00 05

DURATIONFORECASTFF

FORECASTFF+2*SEFFFORECASTFF-2*SEFF

Forecast 2006.04-2007.12, ARMA trend Model

2

4

6

8

10

12

14

70 75 80 85 90 95 00 05

DURATIONDURFORE

DURFORE+2*SEFFDDURFORE-2*SEFFD

Out of Sample Forecast; 2006.05-2007.12

6161

Fractional Change in Fractional Change in DurationDuration

6262

-0.3

-0.2

-0.1

0.0

0.1

0.2

70 75 80 85 90 95 00 05

DLNDURATION

Fractional change in duration

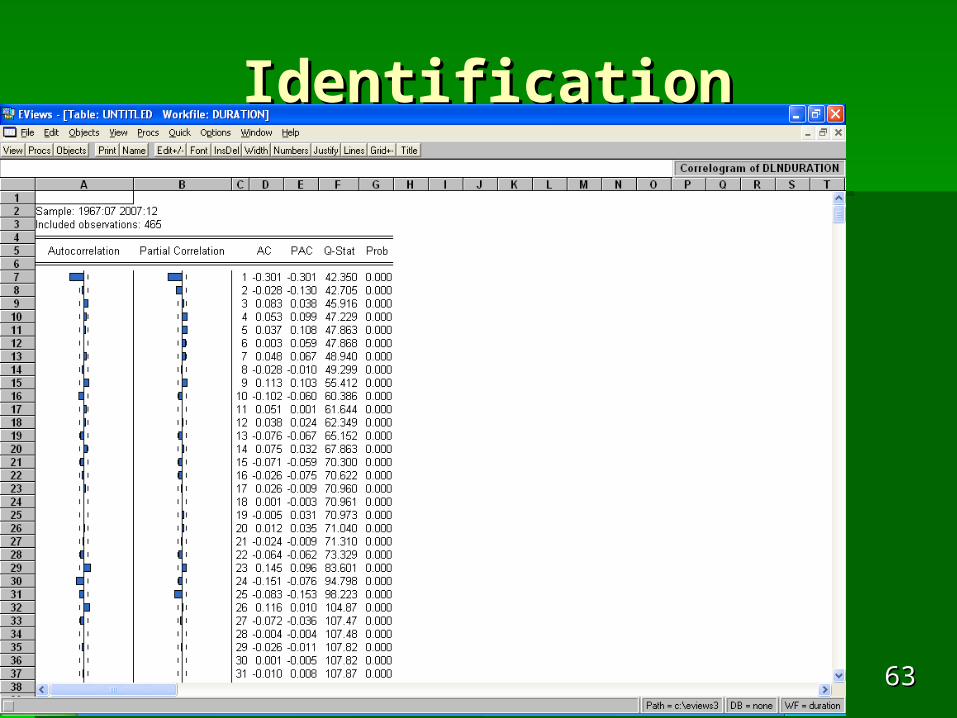

6363

IdentificationIdentification

6464

ModelModel

6565

Model verificationModel verification

6666

6767

6868