1 of 61 AIG / VALIC Retirement Services For Foothill - DeAnza Community College District May 2007.

46

1 of 61 of 61 AIG / VALIC Retirement Services AIG / VALIC Retirement Services For For Foothill - DeAnza Community Foothill - DeAnza Community College District College District May 2007 May 2007

-

Upload

jesse-norton -

Category

Documents

-

view

216 -

download

2

Transcript of 1 of 61 AIG / VALIC Retirement Services For Foothill - DeAnza Community College District May 2007.

11 of 61 of 61

AIG / VALIC Retirement ServicesAIG / VALIC Retirement ServicesForFor

Foothill - DeAnza CommunityFoothill - DeAnza CommunityCollege DistrictCollege District

May 2007May 2007

22 of 61 of 61

AgendaAgenda

Retirement today: What’s different?Retirement today: What’s different? Revisioning Retirement studyRevisioning Retirement study What have we learned?What have we learned? What’s next?What’s next? 403b and 457 Plan Information403b and 457 Plan Information

33 of 61 of 61

Retirement today: What’s different?Retirement today: What’s different?

65 is just a number.65 is just a number.

44 of 61 of 61

Birth Year Male Female

1900 46.3 years 48.3 years1950 65.6 71.11960 66.6 73.11970 67.1 74.71980 70.0 77.41990 71.8 78.82000 74.3 79.7

Retirement today: What’s different?Retirement today: What’s different?Average LifespanAverage Lifespan

Source: National Center for Source: National Center for Health Statistics from birthHealth Statistics from birth

55 of 61 of 61

Retirement today: What’s different?Retirement today: What’s different?

66 of 61 of 61

Retirement can last 20 - 30 yearsRetirement can last 20 - 30 years

The evolution of retirement planningThe evolution of retirement planning

1900 - 19351900 - 1935 Retirement was only for the wealthy and those Retirement was only for the wealthy and those few with pensionsfew with pensions

1935 - 19751935 - 1975 Social Security, pensions, defined contribution Social Security, pensions, defined contribution plans, IRAs, tax incentives to saveplans, IRAs, tax incentives to save

1975 - Present1975 - Present Living longer, retiring earlier, expecting more Living longer, retiring earlier, expecting more in retirementin retirement

77 of 61 of 61

Age 65 oryounger

Age 65-74 Age 75 andolder

Percentage ofnet disposableincome

Medical costs are increasing faster than Medical costs are increasing faster than inflationinflation

6.98%

16.75%

21.38%

25%

20%

15%

10%

5%

0%

88 of 61 of 61

Revisioning Retirement study Revisioning Retirement study

99 of 61 of 61

Ageless Ageless Explorers:Explorers:

• View retirement as an exciting new phase • Feel very financially prepared

• Developed an overall investment strategy to achieve financial independence

• Saved for an average of 24 years

• Have taken numerous steps to prepare for retirement

27% of those surveyed

1010 of 61 of 61

Comfortably Comfortably Contents:Contents:

• Are enjoying their golden years and the rewards of good financial planning

• Have saved and invested well and have an overall financial strategy

• Extremely satisfied with retirement

• Feel very financially prepared

• Saved for an average of 23 years19% of those surveyed

Live for Todays:Live for Todays:• Fun, active and adventuresome

• Are anxious about retirement due to lack of financial planning

• Worried they will not have enough money

• Saved for an average of 18 years

• Wish they could change how they prepared

22% of those surveyed

1212 of 61 of 61

Sick and Tireds:Sick and Tireds:• Have the worst possible retirement

• Are inactive, unfulfilled and worried about the future

• Saved very little for an average of 16 years

• Not financially prepared for retirement and do not have an overall strategy

• Little they can do to improve their situation - just trying to hang on

32% of those surveyed

1313 of 61 of 61

Average #years saved

24 years 23 years 18 years 16 years

Have aninvestment

strategy75% 68% 51% 27%

Receivedassistance

developing aplan

60% 47% 38% 22%

Retirementexperience

Mostsatisfied

Verysatisfied

Lesssatisfied

Leastsatisfied

1414 of 61 of 61

What can we learn from this study?What can we learn from this study?

Save more, save longerSave more, save longer Have a planHave a plan Get assistanceGet assistance

1515 of 61 of 61

0

5

10

15

20

25

By Years

Low financialpreparedness

Average financialpreparedness

High financialpreparedness

Lesson 1: Save more, save longer Lesson 1: Save more, save longer

11

19

24

1616 of 61 of 61

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

25-year-old 35-year-old 45-year-old

Lesson 1: Save more, save longer Lesson 1: Save more, save longer The cost to accumulate $300,000The cost to accumulate $300,000

$ This example compares the total out-of-pocket This example compares the total out-of-pocket costs required to fund the retirement goals of costs required to fund the retirement goals of three investors who started contributing $200 three investors who started contributing $200 a month at different ages. An additional $67 is a month at different ages. An additional $67 is deposited to the tax-qualified retirement plan deposited to the tax-qualified retirement plan each month as a result of current income tax each month as a result of current income tax savings, assuming a 25% federal income tax savings, assuming a 25% federal income tax bracket and an 8% annual ratebracket and an 8% annual rateof return. Tax-qualified plan accumulations are of return. Tax-qualified plan accumulations are taxed as ordinary income when withdrawn. taxed as ordinary income when withdrawn. Federal restrictions and tax penalties may Federal restrictions and tax penalties may apply to early withdrawals.apply to early withdrawals.

1717 of 61 of 61

0

50

100

150

200

10 years 20 years 30 years

Taxableaccount

Tax-qualifiedplan

Lesson 1: Save more, save longer Lesson 1: Save more, save longer (continued)(continued)Save tax deferredSave tax deferred

Thousands ($)

The chart assumes a 25% federal marginal income tax rate and an 8% annual rate of return. Fees and The chart assumes a 25% federal marginal income tax rate and an 8% annual rate of return. Fees and charges, if applicable, are not reflected in this example and would reduce the amount shown. Income taxes charges, if applicable, are not reflected in this example and would reduce the amount shown. Income taxes are payable upon withdrawal. Federal restrictions and tax penalties may apply to early withdrawals. are payable upon withdrawal. Federal restrictions and tax penalties may apply to early withdrawals. Investment values may fluctuate so that an investor’s shares, when withdrawn, may be worth more or less Investment values may fluctuate so that an investor’s shares, when withdrawn, may be worth more or less than the original cost.than the original cost.

1818 of 61 of 61

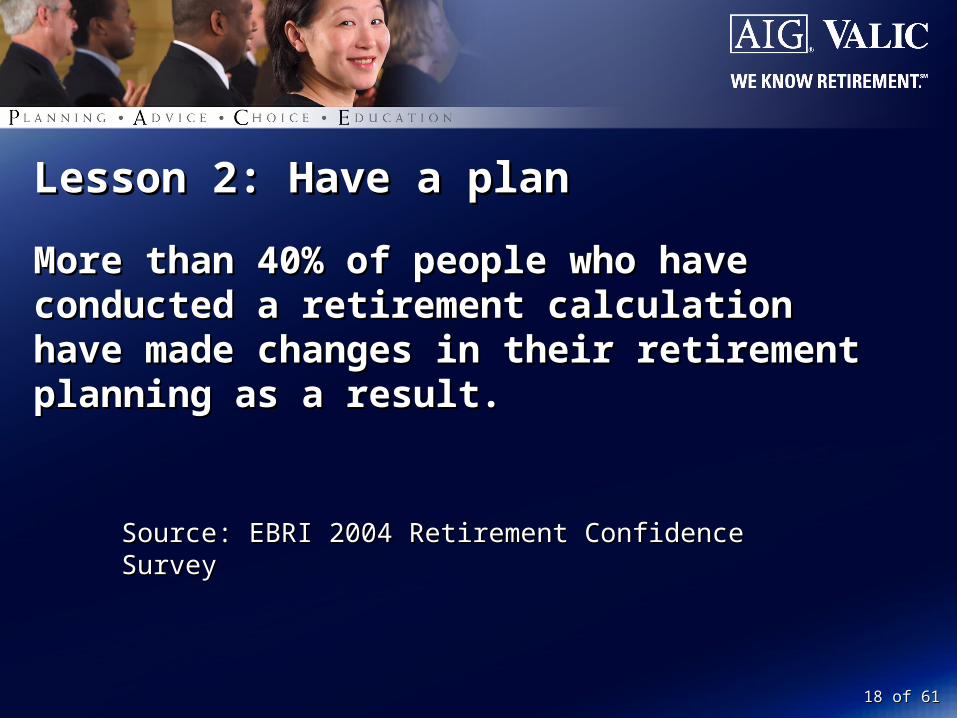

Lesson 2: Have a planLesson 2: Have a plan

More than 40% of people who have conducted a More than 40% of people who have conducted a retirement calculation have made changes in retirement calculation have made changes in their retirement planning as a result.their retirement planning as a result.

Source: EBRI 2004 Retirement Confidence SurveySource: EBRI 2004 Retirement Confidence Survey

1919 of 61 of 61

Lesson 2: Have a plan (continued)Lesson 2: Have a plan (continued)Does your asset allocation look like a goal post?Does your asset allocation look like a goal post?

2020 of 61 of 61

Lesson 2: Have a plan (continued)Lesson 2: Have a plan (continued)

Asset allocationAsset allocation

2121 of 61 of 61

Retirement summaryRetirement summary

2222 of 61 of 61

Lesson 3: Get assistanceLesson 3: Get assistanceRevisioning Retirement: Who received assistance?Revisioning Retirement: Who received assistance?

60% 38%

47% 22%

Ageless Explorers Live for Todays

Comfortably Contents Sick and Tireds

2323 of 61 of 61

Revisioning retirementRevisioning retirement

The secrets to financial freedom according to The secrets to financial freedom according to financially prepared retireesfinancially prepared retirees

Think positively toward retirementThink positively toward retirement Desire and achieve active goals in Desire and achieve active goals in

retirementretirement Work toward freedom and flexibilityWork toward freedom and flexibility

Start saving earlyStart saving early Develop an overall investment strategyDevelop an overall investment strategy Get professional assistance in developing a Get professional assistance in developing a

financial planfinancial plan

2424 of 61 of 61

In the past, planning for retirement meant:In the past, planning for retirement meant:

Saving moneySaving money Paying off the mortgagePaying off the mortgage Taking a tripTaking a trip

Today, planning for retirement means:Today, planning for retirement means: Creating and sticking to a financial planCreating and sticking to a financial plan Paying off the mortgage — or notPaying off the mortgage — or not Reinventing yourselfReinventing yourself

2525 of 61 of 61

In the past, planning for retirement meant:In the past, planning for retirement meant:

Relying on Medicare to cover large Relying on Medicare to cover large medical expensesmedical expenses

Today, planning for retirement means:Today, planning for retirement means: Saving more for higher medical costs Saving more for higher medical costs

and and long-term care expenseslong-term care expenses

2626 of 61 of 61

In the past, planning for retirement meant:In the past, planning for retirement meant:

Relying on pension and Social Relying on pension and Social Security to supplement retirement Security to supplement retirement income needsincome needs

Today, planning for retirement means:Today, planning for retirement means: Relying on a employer-sponsored retirement Relying on a employer-sponsored retirement

plan to supplement a significant portion of plan to supplement a significant portion of retirement incomeretirement income

More decisions to make; more More decisions to make; more choices availablechoices available

2727 of 61 of 61

What’s next?What’s next?

Have you enrolled in your retirement plan?Have you enrolled in your retirement plan? Are you contributing enough?Are you contributing enough? Is the money in your plan invested in the best Is the money in your plan invested in the best

possible way?possible way? Have you done your short-term and your long-term Have you done your short-term and your long-term

retirement calculations?retirement calculations? Is it time to seek assistance with your Is it time to seek assistance with your

retirement planning?retirement planning?

2828 of 61 of 61

These may be the most important These may be the most important years of your retirement.years of your retirement.

2929 of 61 of 61

Your 403b Program at Foothill-De Your 403b Program at Foothill-De Anza Community CollegeAnza Community College DistrictDistrict

3030 of 61 of 61

403b Contribution Limits403b Contribution Limits

100% of Includible Compensation up to 100% of Includible Compensation up to $15,500$15,500

Age Based Catch Up of $5,000 for employees Age Based Catch Up of $5,000 for employees age 50 and overage 50 and over

3131 of 61 of 61

403b Benefits to Employees403b Benefits to Employees

Contributions made on a “Pre-Tax” basisContributions made on a “Pre-Tax” basis Defer current income taxation on Defer current income taxation on

contributions and earningscontributions and earnings Salary Reduction -- Easy to participate!Salary Reduction -- Easy to participate!

3232 of 61 of 61

403(b) Withdrawal Restrictions403(b) Withdrawal Restrictions

Availability of funds generally subject to:Availability of funds generally subject to: Separation from serviceSeparation from service

Age 591/2Age 591/2

DisabilityDisability

DeathDeath

HardshipHardship

3333 of 61 of 61

403(b) Tax Penalties on Early Withdrawals403(b) Tax Penalties on Early Withdrawals

Withdrawals prior to age 591/2 generally subject to Withdrawals prior to age 591/2 generally subject to 10% federal tax penalty except:10% federal tax penalty except: Death Death

DisabilityDisability

Separation from service at age 55Separation from service at age 55

Payout through a substantially equivalent payment streamPayout through a substantially equivalent payment stream

Tax-Deductible Medical ExpensesTax-Deductible Medical Expenses

Qualified domestic relations order (QDRO)Qualified domestic relations order (QDRO)

Payment to IRS on account of federal tax levy Payment to IRS on account of federal tax levy

3434 of 61 of 61

403(b) Taxability403(b) Taxability

Pre-tax contributionsPre-tax contributions

Tax-deferred earningsTax-deferred earnings

Taxed as ordinary income when withdrawnTaxed as ordinary income when withdrawn

Subject to minimum distribution rules at age 70½ Subject to minimum distribution rules at age 70½

3535 of 61 of 61

Other Plan FeaturesOther Plan Features

Loans are available Loans are available Special Catch up provisions for employees with Special Catch up provisions for employees with

15 years of service who qualify15 years of service who qualify Portable to 403(b), 401(k) or IRAs at separation Portable to 403(b), 401(k) or IRAs at separation

from servicefrom service

3636 of 61 of 61

403b Contribution Example 403b Contribution Example

Employees less than 50 years old: $15,500Employees less than 50 years old: $15,500

Employees age 50+: $15,500 + $5,000 = $20,500Employees age 50+: $15,500 + $5,000 = $20,500

Employees age 50+ with 15 years of service that qualify Employees age 50+ with 15 years of service that qualify for cap expansion: $15,500 + $5,000 +$3,000 = $23,500 for cap expansion: $15,500 + $5,000 +$3,000 = $23,500

3737 of 61 of 61

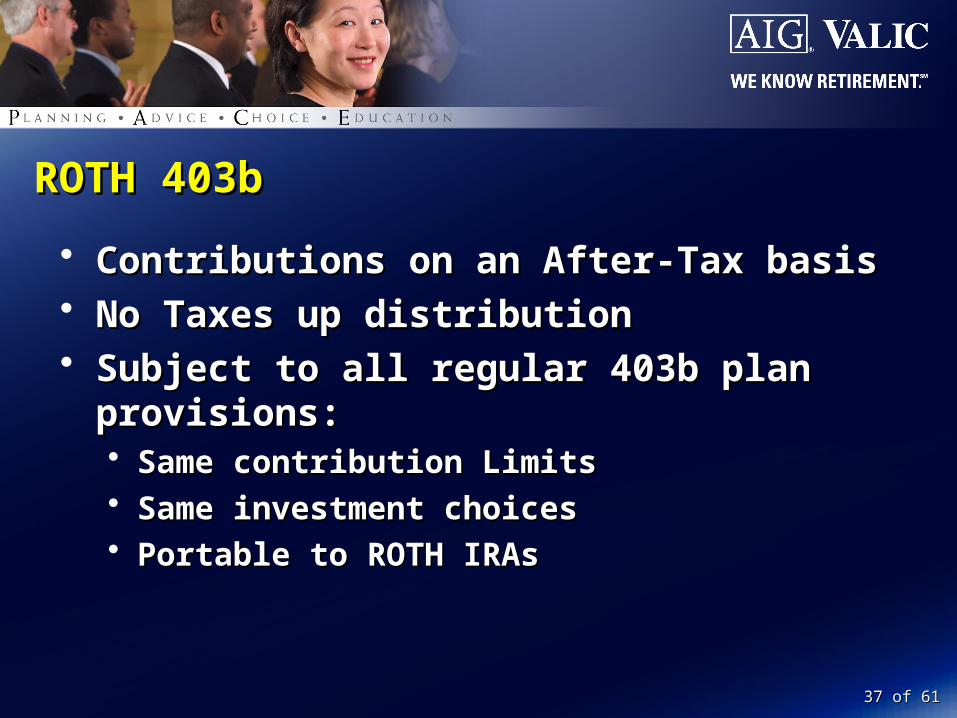

ROTH 403bROTH 403b

Contributions on an After-Tax basisContributions on an After-Tax basis No Taxes up distributionNo Taxes up distribution Subject to all regular 403b plan provisions:Subject to all regular 403b plan provisions:

Same contribution LimitsSame contribution Limits Same investment choicesSame investment choices Portable to ROTH IRAsPortable to ROTH IRAs

3838 of 61 of 61

Your 457 Program at Foothill-De Anza Your 457 Program at Foothill-De Anza Community CollegeCommunity College DistrictDistrict

3939 of 61 of 61

457 Benefits to Employees457 Benefits to Employees

Supplement retirement incomeSupplement retirement income Defer current income taxation on Defer current income taxation on

contributions and earningscontributions and earnings Able to “double up” on contribution deferrals - Able to “double up” on contribution deferrals -

Now can contribute to both 403b and 457 at Now can contribute to both 403b and 457 at the same time!the same time!

4040 of 61 of 61

457(b) Contribution Limits457(b) Contribution Limits

100% of compensation not to exceed $15,500 100% of compensation not to exceed $15,500 in 2007in 2007

Age 50 + catch up is $5,000 in 2007Age 50 + catch up is $5,000 in 2007

4141 of 61 of 61

457(b) Contribution Limits 457(b) Contribution Limits continuedcontinued

““3-year” catch-up prior to normal retirement 3-year” catch-up prior to normal retirement equal to 2 times the annual dollar limit equal to 2 times the annual dollar limit ($31,000 in 2007)($31,000 in 2007) Must have been eligible for this plan and must Must have been eligible for this plan and must

consider prior year pre-tax deferrals with this ERconsider prior year pre-tax deferrals with this ER Cannot use age 50 and 3 year catch up together Cannot use age 50 and 3 year catch up together

4242 of 61 of 61

457(b) Withdrawal Restrictions457(b) Withdrawal Restrictions

Availability of funds generally subject to:Availability of funds generally subject to: Attaining age 70½Attaining age 70½

Separation from service (any age with no pre-59 1/2 Separation from service (any age with no pre-59 1/2 withdrawal penalty)withdrawal penalty)

Unforeseen emergencyUnforeseen emergency

4343 of 61 of 61

457(b) Taxability457(b) Taxability

Pre-tax contributionsPre-tax contributions

Tax-deferred earningsTax-deferred earnings

Taxed as ordinary income when withdrawnTaxed as ordinary income when withdrawn

Subject to minimum distribution rules at age 70½ Subject to minimum distribution rules at age 70½

4444 of 61 of 61

Other Plan FeaturesOther Plan Features

Loans are available Loans are available Portable to 403(b), 401(k) or IRAs at separation Portable to 403(b), 401(k) or IRAs at separation

from servicefrom service Unforeseen Emergency Withdrawals are Unforeseen Emergency Withdrawals are

availableavailable

4545 of 61 of 61

Thank You!Thank You!

4646 of 61 of 61

Securities and investment advisory services are offered by VALIC Financial Advisors, Inc., member NASD, SIPC and an SEC-registered investment advisor.

AIG VALIC is the marketing name for the group of companies comprising VALIC Financial Advisors, Inc.; VALIC Retirement Services Company; and The Variable Annuity Life Insurance Company (VALIC); each of which is a member company of American International Group, Inc.

The information in this presentation is general in nature and may be subject to change. Neither AIG VALIC nor the financial advisors give legal or tax advice. Applicable laws and regulations are complex and subject to change. For legal or tax advice concerning your situation, consult your attorney or professional tax advisor.

Copyright © 2004 American International Group, Inc. All rights reserved.Houston, Texas

VL 16197 9/2004