1 Netherlands as a holding Jurisdiction 28.11.2007 West End Hotel, Mumbai Itzik Amiel, adv.

43

1 Netherlands as a holding Jurisdiction 28.11.2007 West End Hotel, Mumbai Itzik Amiel, adv.

-

Upload

claud-mason -

Category

Documents

-

view

216 -

download

0

Transcript of 1 Netherlands as a holding Jurisdiction 28.11.2007 West End Hotel, Mumbai Itzik Amiel, adv.

1

Netherlands as a holding Jurisdiction

28.11.2007

West End Hotel, Mumbai

Itzik Amiel, adv.

2

Agenda

ANT/AMACO Introduction;

Introduction - The Netherlands;

Traditional features of the Dutch tax system;

Dutch Tax Reform 2007;

Proven Tax Structuring opportunities with India.

QuickTime™ and aTIFF (Uncompressed) decompressor

are needed to see this picture.

3

ANT/AMACO

QuickTime™ and aTIFF (Uncompressed) decompressor

are needed to see this picture.

IntroductionIntroduction

4

ANT/AMACO Group’s Profile

About Us

Origin: ANT - 1897, Amaco - 1956;

Independent - maintain a position of absolute independence towards its business partners and clients;

International - international scope; strategically positioned to cater to the strong international growth in demand for our services;

In-Business - positioning ourselves as partner in business to help the strength and the growth of our clients;

Tradition of Trust - established track record and long-lasting relationship.

5

ANT/AMACO Group’s Profile

About Us

We are a genuinely international management, trust, corporate and asset administration group;

A growing global network - ANT Group continues to grow. To build extra capacity, we are investing heavily in human resources, technology and infrastructure, and in the next few years, we expect to increase the size of our network also to other jurisdictions;

Acts under supervision of the Dutch Central Bank as per the WTT (Act on Supervision Trust offices) and under the Netherlands Antilles central bank [while the NV is under the supervision of AFM];

Strong emphasis on professional skills, such as; Language skills (English, French, Dutch, German, Italian, Spanish, Portuguese, Greek,

Arabic, Croatian, Bulgarian, Chinese and Hebrew) at “operational level”; Qualifying (Tax) Legal degrees; Qualifying Accounting degrees.

6

The Added Value of ANT/AMACO

Reasons to involve ANT/AMACO:

The solid financial background and track-record; High commitment/ loyalty of clients; Close contacts with advisers and clients. Administration capabilities for Implementation of tax

planning (based on a tax lawyer’s advice); Administration capabilities for Implementation of

financial engineering advice (based on the financial advise);

Confidentiality; The global network (intermediaries; clients etc.). Proven successful experience with Indian clients.

7

The Added Value of ANT/AMACO

Benefits for client:

Global platform Geographical platform providing a range of services

for trust and fiduciary services from which to develop new business opportunities

Expertise High quality workforce with extensive experience in

rendering administration services for structuring of, private and corporate wealth/ transactions, and long commitment of employees to ANT/AMACO.

8

The Added Value of ANT/AMACO

Benefits for client:

Quality High level compliance and risk management

minimizing reputation risk for the business and its partners.

Independence Focused independent service provider with minimal

conflicts of interest with its partners or clients.

Inpersonal We know our clients and our clients know us.

9

Types of Clients

Main types of clients of ANT/AMACO:

Large-medium national and multinational companies;

Institutional clients;

High Net Worth Individuals.

We are proud to have the largest Indian clients portfolio

10

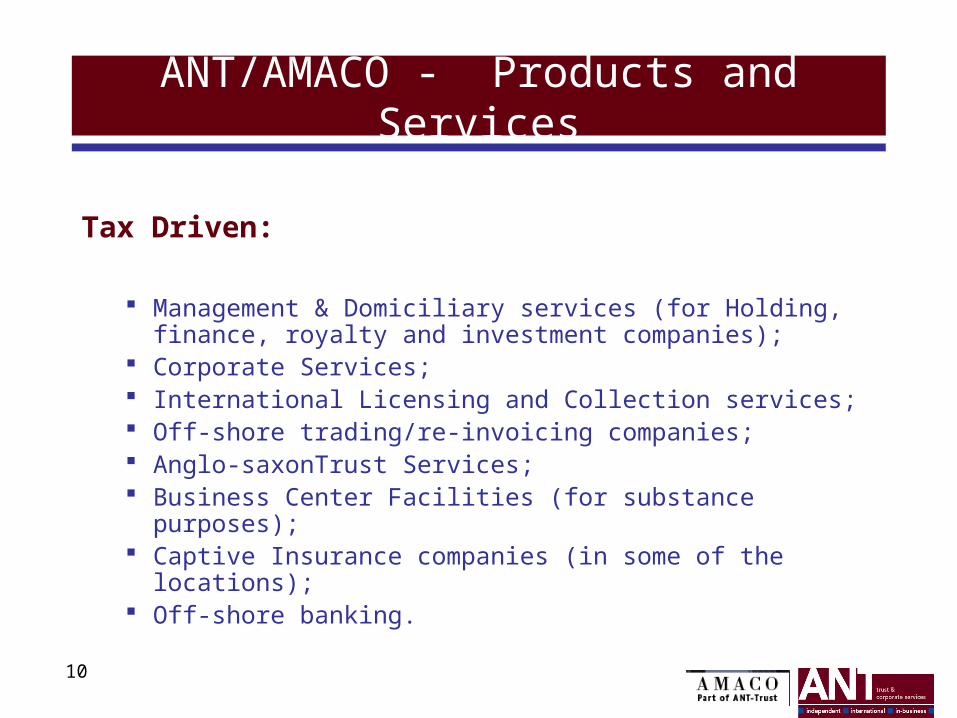

ANT/AMACO - Products and Services

Tax Driven:

Management & Domiciliary services (for Holding, finance, royalty and investment companies);

Corporate Services; International Licensing and Collection services; Off-shore trading/re-invoicing companies; Anglo-saxonTrust Services; Business Center Facilities (for substance purposes); Captive Insurance companies (in some of the

locations); Off-shore banking.

11

Licensing & Financial Services

Two dedicated subsidiaries:

A Dutch company focusing on the exploitation of intellectual property rights (“IP Rights”) and other intangible assets company incorporation or sale of existing companies.

NCS Universal Rights B.V.

NCS Finance B.V.

A Dutch company focusing on the rendering financial services like escrow arrangements and back-to-back loans and also focusing on the ownership of Special Purpose Vehicles.

12

ANT/AMACO - Products and Services

Non-Tax Driven:

Structured Finance Services: Securitization Deals; Special Purpose Vehicles; Other Special Products.

Escrow Services;

Custody services;

Trustee services;

Paying Agent services;

13

ANT/AMACO - Products and Services

Non-Tax Driven (continued):

Asset Administration Services: Electronic Voting; Employee Benefit Programs; Securities Investment systems; Custodian for Investment Funds.

Registrar and Shareholder Services: Administration of shareholders registers; Personal Consult and Support.

Fund Administration Services.

14

The Netherlands

IntroductionIntroduction

16

Introduction - The Netherlands

Interesting Facts About The NetherlandsDid you know that...?

• `the Netherlands' and 'Holland' are used to describe the same country?• the population density of the Netherlands is approximately 480 inhabitants per square km?• the Netherlands, covering a mere 0.008% of the world's surface, is the world's third biggest exporter of agricultural produce?• the Netherlands is one of the founding members of The European Union?• the Dutch are the tallest people in Europe?• the Netherlands is the eight biggest exporter in the world? • Amsterdam is the capital of the Netherlands, but The Hague is the seat of government?• most Dutch people speak at least one foreign language?• Amsterdam is home to almost 200 nationalities?• the Netherlands has one of the youngest populations in the EU?

[ Source: Dutch Ministry of Foreign Affairs]

17

Introduction - The Netherlands

For years, a reputable position as a good location for international tax planning of foreign groups. Generally recognized as having a positive impact on the Dutch investment climate:

Well educated, flexible, multilingual and motivated workforce and top professionals;

Central geographical position, combined with accessibility and excellent infrastructures such as the Port of Rotterdam and Schiphol Airport;

Strong international focus of the Dutch economy including open attitude of authorities.

18

Introduction - The Netherlands

Easy access to Stock markets via public listing at Euronext;

Currency is Euro (strong currency), no exchange control regulations;

Trading nation with long history: exposed to different cultures and open minded;

Internationally competitive tax rate;

Intra group finance/licensing activities;

Favorable international holding regime; Hardly ever blacklisted;

19

Introduction - The Netherlands

With the introduction of the 2007

amendments to the Dutch corporate income tax act, the Netherlands should be one of the first countries again to consider as a holding or financing location.

20

Traditional Features of the Dutch Tax System

The NetherlandsThe Netherlands

21

Traditional Features of the Dutch Tax System

No Corporate Income Tax (‘CIT’) on dividends and capital gains from (foreign) qualifying participations (‘participation exemption’);

No CIT on income from qualifying foreign permanent establishments;

No Withholding Taxes (‘WHT’) on interest and royalties paid by Dutch companies.

22

Traditional Features of the Dutch Tax System

Vast and favorable tax treaty and agreements network (over 80 tax treaties and more than 100 investment protection treaties)

Low or no WHT on foreign income received by Dutch companies, credits available. The tax treaty between the Netherlands and India is beneficial.

EU directives Provided certain conditions have been fulfilled: No withholding tax

on intra EU dividends, interest and royalties.

Domestic rules Good domestic rules for avoidance of double tax if no treaty

applies.

23

Dutch Tax Reform

20072007

24

2007 Dutch Tax Reform

Reduction of the Dutch CIT maximum rate from 29,6% to 25,5%;

Reduction of the Dutch dividend WHT rate from 25% to 15% (often lower in case tax treaty or EU directives applies);

Changes to the participation exemption;

Special tax regime on intra group interest income? – Subject to EU approval

25

2007 Dutch Tax Reform

Dutch Corporate Income Tax Rate

Overview of Dutch corporate tax rates during the past few years

Year Tax Rate first bracket(s) Tax rate on

remaining profit

…2004 29% (profits to € 22,689) 34.5%

2005 27% (profits to € 22,689) 31.5%

2006 25.5% (profits to € 22,689) 29.6%

2007 20% (profits to € 25,000)

23.5% (profits of € 25,000 to € 60,000)

25.5%

2008 20% (profits to € 40,000)

23% (profits of € 40,000 to € 200,000)

25.5%

26

2007 Dutch Tax Reform

Reduction of Dutch dividend withholding tax rate

Dutch dividend WHT rate to be reduced from 25% to 15%.

In practice often lower or nil as a result of tax treaties or EU law.

27

2007 Dutch Tax Reform

Dutch Participation Exemption

The participation exemption is a good tradition in Dutch corporate taxation. It is an exemption of Dutch corporate tax on dividends, capital gains and other benefits derived from shares that meet certain characteristics.

The 2007 legislation simplifies the rules and takes away some problems that were there previously.

28

2007 Dutch Tax Reform

Dutch Participation Exemption

On the basis of the proposed legislation:

It applies to shareholdings of 5% or more; It also applies if a group company owns 5% or more and the Dutch company holds less than 5% or to a so called “hybrid loan”.

Subsidiaries that are not ‘passive’ will not have to be subject to tax; The same applies to so called “real estate companies”.

It also applies to “passive” participations or passive group financing participations, provided their profits are taxed at 10% or more (profit determined on the basis of Dutch standards).

29

2007 Dutch Tax Reform

≥5%

>50%Passive

Tax rate>10%

Tax rate>10%

0% tax rate

Non EU

EU

No Dutch participation exemptionNo Dutch participation exemption

Fully exempt

Capital Gains

Dividends

≤50%Passive

<5%

30

2007 Dutch Tax Reform

Dutch Participation Exemption

• If tax haven ‘active’, e.g. performing (group) trading activities, participation exemption will be granted, irrespective of the level of taxation at tax haven.

• If tax haven ‘passive’ and not effectively taxed at 10%, participation exemption in principle will not apply

• Cyprus has a tax rate of 10%, but also various exemptions, so effective tax rate should be monitored closely.

31

2007 Dutch Tax Reform

Dutch Participation Exemption

100%100%

>5%<5%

32

2007 Dutch Tax Reform

Dutch Participation Exemption

The experience with the new regime:

New regime generally include more subsidiaries as qulifying subsidiaries;

Only in exceptional cases the new regime would cause the subsidiary to be no longer qualifying (have interest below 5%);

An (indirect) participation in an active business, generally participation exemption will apply;

An (indirect) participation in a passive real property company, generally participation exemption will apply;

Rules for exemption for PE income have not changes.

33

2007 Dutch Tax Reform

Dutch Interest Box• A special tax regime in respect of interest received from group companies has

been developed containing the following characteristics:

• Approximately 80% of inter-company interest income less expense to be exempt; the remainder will be taxable against 25,5% (effective tax rate approx. 5%);

• Taxpayer has to opt for application of the interest box together with all affiliated Dutch companies;

• Affiliated companies; shareholdings of at least 50% held by the tax payer or another group company.

• BUT, subject to certain conditions and restrictions

• Subject to EU approval

34

Proven Tax Structuring

With IndiaWith India

35

IndiaCo

DutchCo

LTSub1

10% WHT (article 10 Treaty)

0% CIT (participation exemption)

generally no WHT (domestic law) LTSub2

Holding- Dutch Intermediary Company

100%

100% 100%

36

IndiaCo

DutchCo

TaxHaven

Capital

Loan

Holding – use of losses

Interest

losses

37

IndiaCo

LuxCo

DutchCo

Capital

Hybrid Loan

Group Financing – Hybrid Loan [1]

Group Loans

38

DutchCo

Target

Loan

Group Financing – Hybrid Entity [1]

LP

39

IndiaCo

Target

Group Financing – Hybrid Entity [2]

Sub1

bank loan

BelgCo

equity

i/c loan

40

IndiaCo

DutchCo

Dividend/Interest/Royalty on sublicense

Loan/license

Foreign Sub

Finance/IP in low tax jurisdiction

100%

100%

Tax HavenCo.

100%

41

Caveat

ANT/AMACO does not advise on tax or legal matters. When structures are discussed, the purpose is to find a potential solution for a specific issue, which should subsequently be checked with the client’s tax or legal advisor.

This applies at the beginning of the relationship as well as during its lifetime. It also applies if and when NCS Universal Rights or NCS Finance is involved.

Before actually entering into a relationship ANT/AMACO needs to check and verify the background and the motives of the planned transaction(s) and the reputation and identity of the parties directly and ultimately involved.

WE ARE NOT TAX ADVISERS !

42

End Note.

QuickTime™ and aTIFF (Uncompressed) decompressor

are needed to see this picture.

Albert Einstein We owe a lot to the Indians, who taught us how to count, without which no worthwhile scientific discovery could have been made

43

Itzik Amiel, Adv. (LL.B., LL.M.)Director International Business Development

T: +31 20 5222 555M: +31 6 50801285F: +31 20 5222 500E: [email protected]

W: www.Ant-Trust.nl

Thank You!