1 ITTO MARKET DISCUSSION Libreville - Gabon | November, 2013 Ivan Tomaselli .

24

1 TRENDS IN BRAZIL’S PRODUCTION AND INTERNATIONAL TRADE ITTO MARKET DISCUSSION Libreville - Gabon | November, 2013 Ivan Tomaselli www.stcp.com.b r

-

Upload

dominik-cornish -

Category

Documents

-

view

223 -

download

1

Transcript of 1 ITTO MARKET DISCUSSION Libreville - Gabon | November, 2013 Ivan Tomaselli .

1

TRENDS IN BRAZIL’S PRODUCTION AND

INTERNATIONAL TRADE

ITTO MARKET DISCUSSION

Libreville - Gabon | November, 2013

Ivan Tomaselliwww.stcp.com.br

2

CONTENTS

FORESTS AND RAW MATERIAL SUPPLY

INDUSTRIAL DEVELOPMENTS

MARKETS AND TRADE

PERSPECTIVES

3

FORESTS AND RAW MATERIAL SUPPLY

4

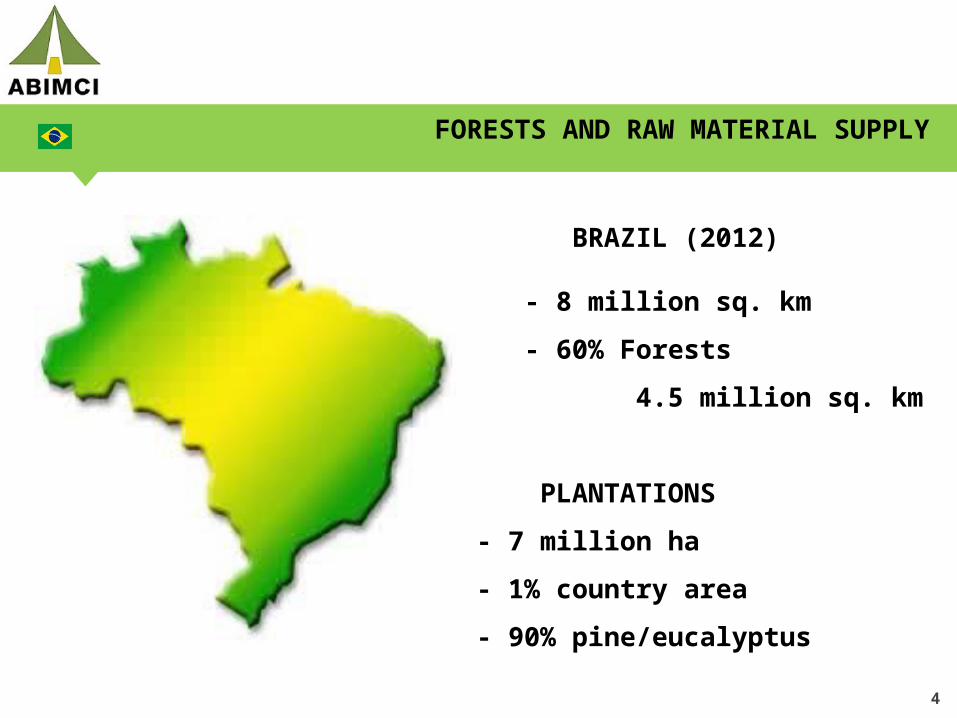

FORESTS AND RAW MATERIAL SUPPLY

BRAZIL (2012)

- 8 million sq. km

- 60% Forests

4.5 million sq. km

PLANTATIONS

- 7 million ha

- 1% country area

- 90% pine/eucalyptus

5

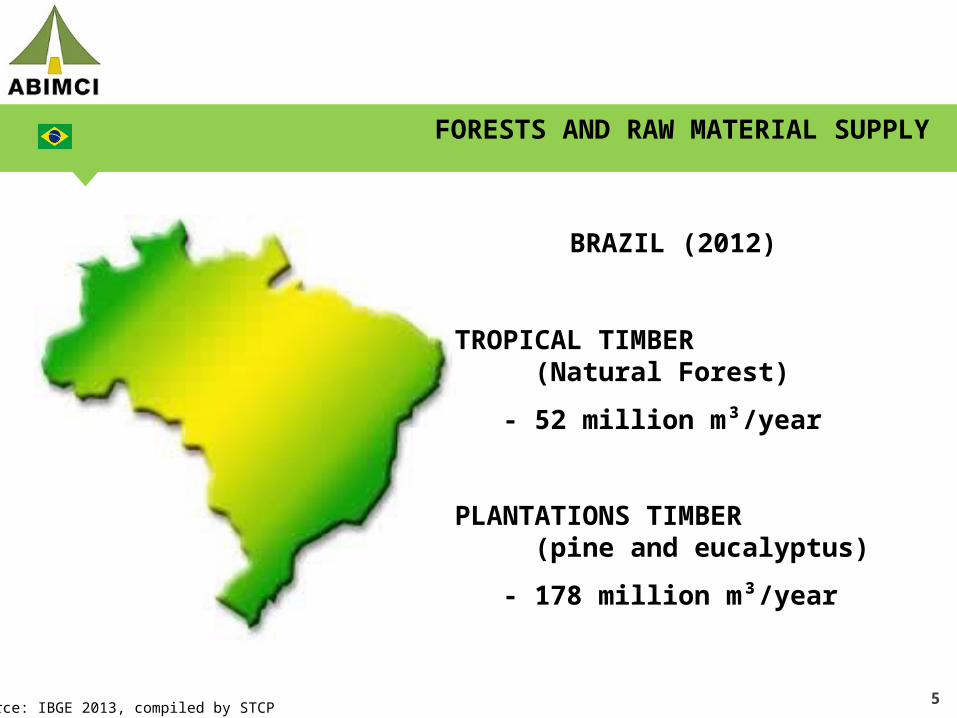

FORESTS AND RAW MATERIAL SUPPLY

BRAZIL (2012)

TROPICAL TIMBER (Natural Forest)

- 52 million m³/year

PLANTATIONS TIMBER (pine and eucalyptus)

- 178 million m³/year

Source: IBGE 2013, compiled by STCP

6

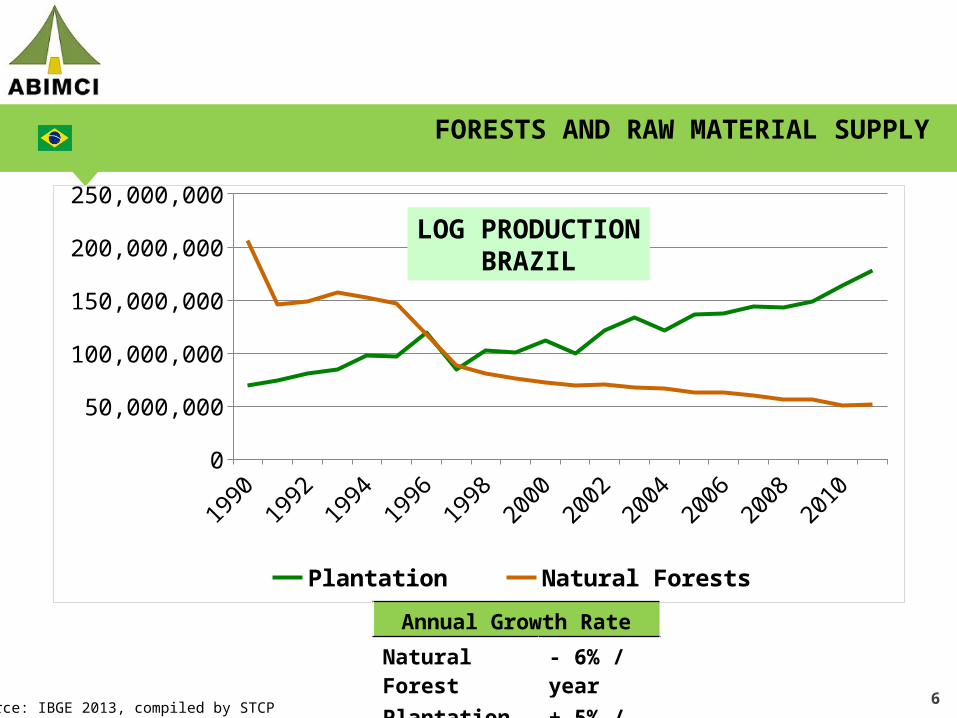

FORESTS AND RAW MATERIAL SUPPLY

19901992

19941996

19982000

20022004

20062008

20100

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

Plantation Natural Forests

LOG PRODUCTIONBRAZIL

Source: IBGE 2013, compiled by STCP

Annual Growth Rate

Natural Forest - 6% / year

Plantation + 5% / year

7

INDUSTRIAL DEVELOPMENTS

8

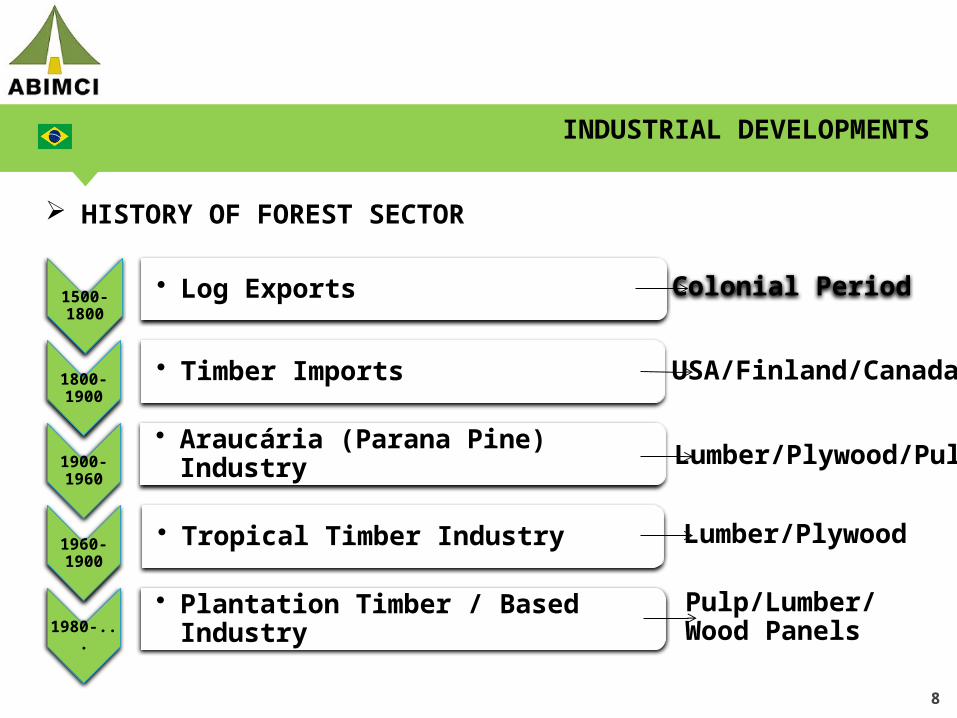

INDUSTRIAL DEVELOPMENTS

HISTORY OF FOREST SECTOR

1500-

1800

• Log Exports

1800-

1900

• Timber Imports

1900-

1960

• Araucária (Parana Pine) Industry

1960-

1900

• Tropical Timber Industry

1980-...

• Plantation Timber / Based Industry

Colonial Period

USA/Finland/Canada

Lumber/Plywood/Pulp

Lumber/Plywood

Pulp/Lumber/Wood Panels

9

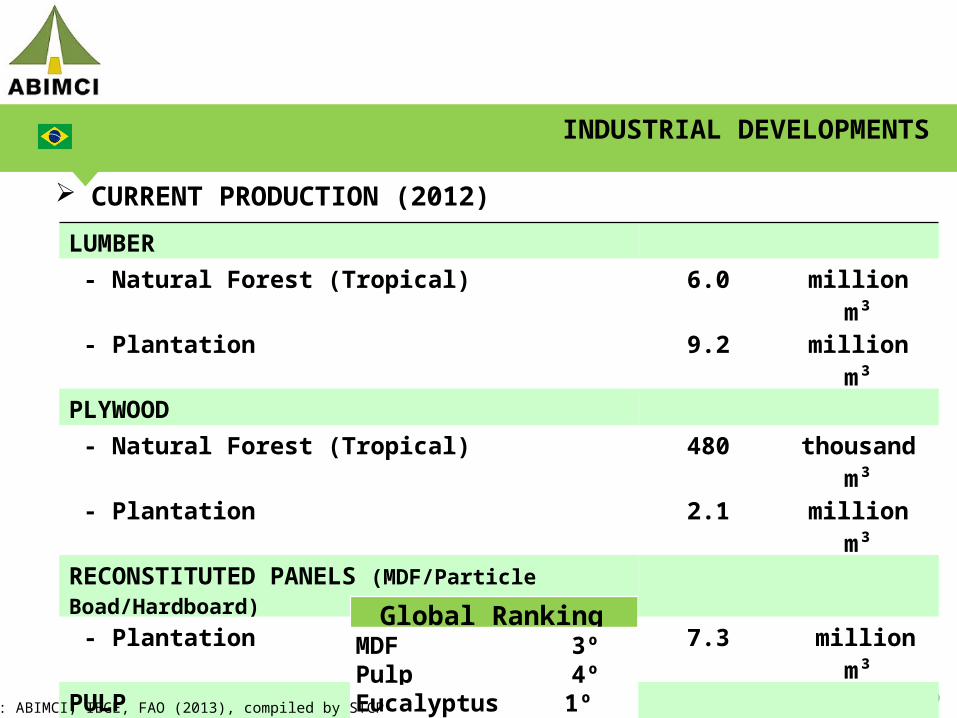

INDUSTRIAL DEVELOPMENTS

CURRENT PRODUCTION (2012)LUMBER - Natural Forest (Tropical) 6.0 million m³ - Plantation 9.2 million m³PLYWOOD - Natural Forest (Tropical) 480 thousand m³ - Plantation 2.1 million m³RECONSTITUTED PANELS (MDF/Particle Boad/Hardboard)

- Plantation 7.3 million m³PULP - Plantation 14.0 million tons

Global RankingMDF 3ºPulp 4ºEucalyptus Pulp 1º Source: ABIMCI, IBGE, FAO (2013), compiled by STCP

10

MARKETS AND TRADE

11

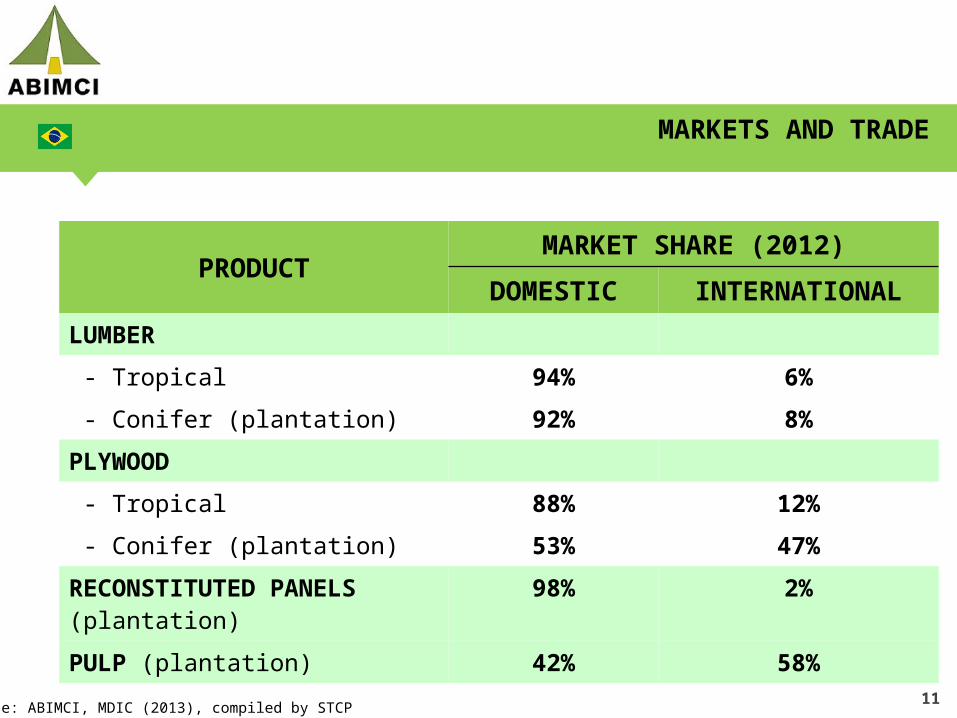

MARKETS AND TRADE

PRODUCTMARKET SHARE (2012)

DOMESTIC INTERNATIONALLUMBER - Tropical 94% 6% - Conifer (plantation) 92% 8%PLYWOOD - Tropical 88% 12% - Conifer (plantation) 53% 47%RECONSTITUTED PANELS (plantation) 98% 2%PULP (plantation) 42% 58%

Source: ABIMCI, MDIC (2013), compiled by STCP

12

MARKETS AND TRADE

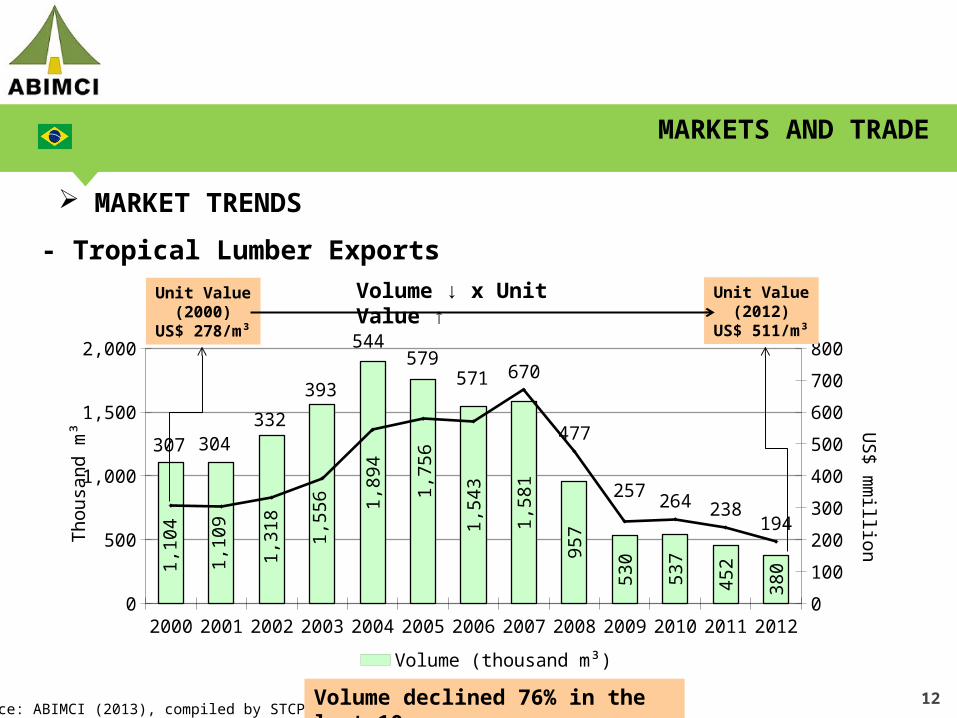

MARKET TRENDS

- Tropical Lumber Exports

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 20120

200400600800

1,0001,2001,4001,6001,8002,000

0

100

200

300

400

500

600

700

800

1,10

4

1,10

9

1,31

8

1,55

6 1,89

4

1,75

6

1,54

3

1,58

1

957

530

537

452

380

307 304332

393

544579

571 670

477

257264 238

194

Volume (thousand m³) Value (US$ million)

Thou

sand

m³ U

S$ mm

illion

Unit Value(2000)

US$ 278/m³

Unit Value(2012)

US$ 511/m³

Volume ↓ x Unit Value ↑

Volume declined 76% in the last 10 yearsSource: ABIMCI (2013), compiled by STCP

13

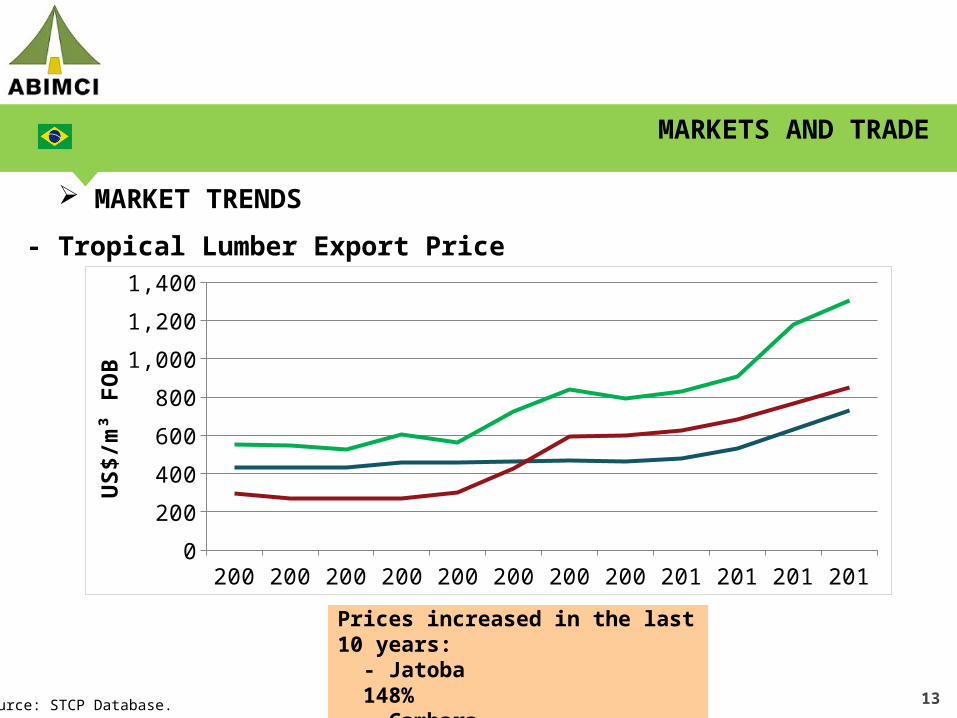

MARKETS AND TRADE

MARKET TRENDS

- Tropical Lumber Export Price

Source: STCP Database.

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

200

400

600

800

1,000

1,200

1,400Jatoba (Green) Cambara KD Angelim Pedra (Green)

US$

/m³ F

OB

Prices increased in the last 10 years: - Jatoba 148% - Cambara 70% - Angelim Pedra 216%

14

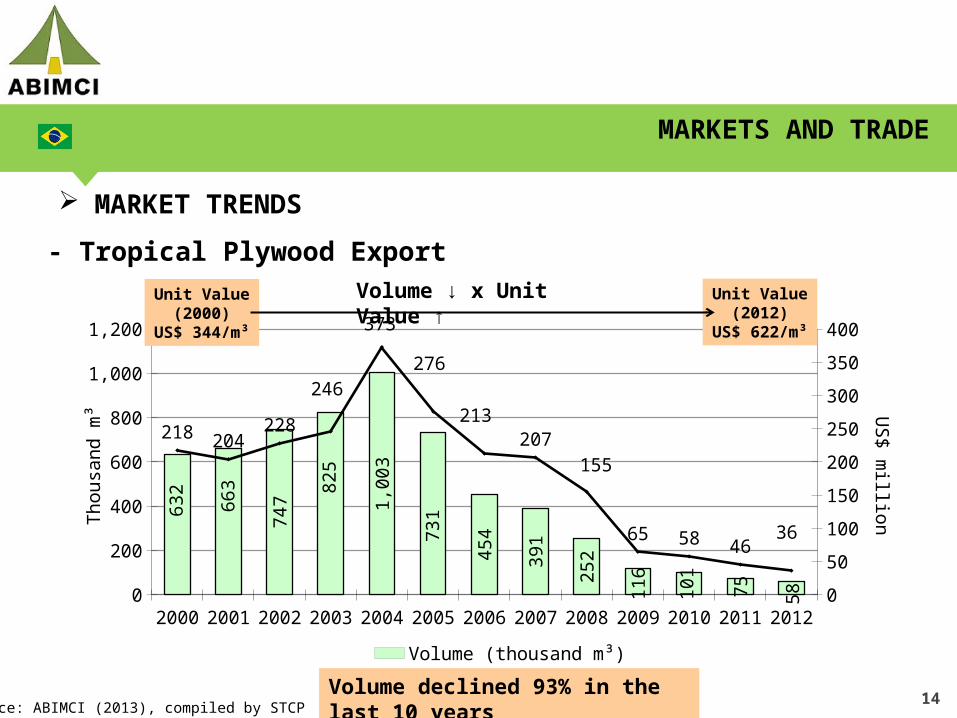

MARKETS AND TRADE

MARKET TRENDS

- Tropical Plywood Export

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 20120

200

400

600

800

1,000

1,200

0

50

100

150

200

250

300

350

400

632

663

747

825

1,00

3

731

454

391

252

116

101

75 58

218 204228

246

373

276

213207

155

65 58 4636

Volume (thousand m³) Value (US$ million)

Thou

sand

m³ U

S$ million

Unit Value(2000)

US$ 344/m³

Unit Value(2012)

US$ 622/m³

Volume ↓ x Unit Value ↑

Volume declined 93% in the last 10 yearsSource: ABIMCI (2013), compiled by STCP

15

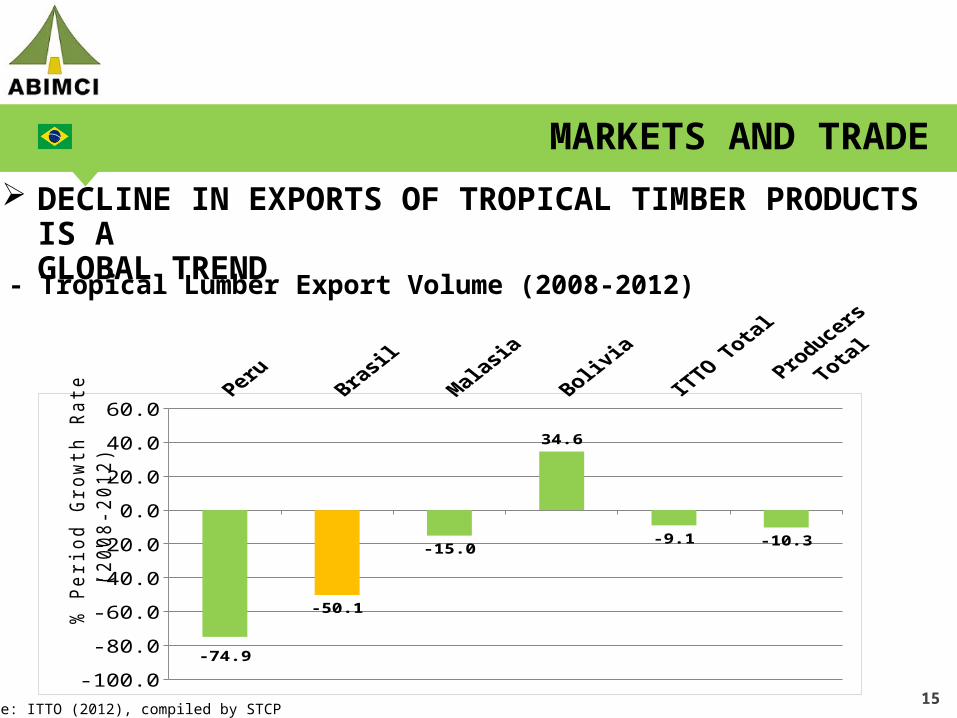

DECLINE IN EXPORTS OF TROPICAL TIMBER PRODUCTS IS A GLOBAL TREND

MARKETS AND TRADE

Peru Brasil Malasia Bolivia ITTO TotalProducers

Total

-100.0

-80.0

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

-74.9

-50.1

-15.0

34.6

-9.1 -10.3

% P

erio

d G

row

th R

ate

(200

8-20

12)

Source: ITTO (2012), compiled by STCP

- Tropical Lumber Export Volume (2008-2012)

16

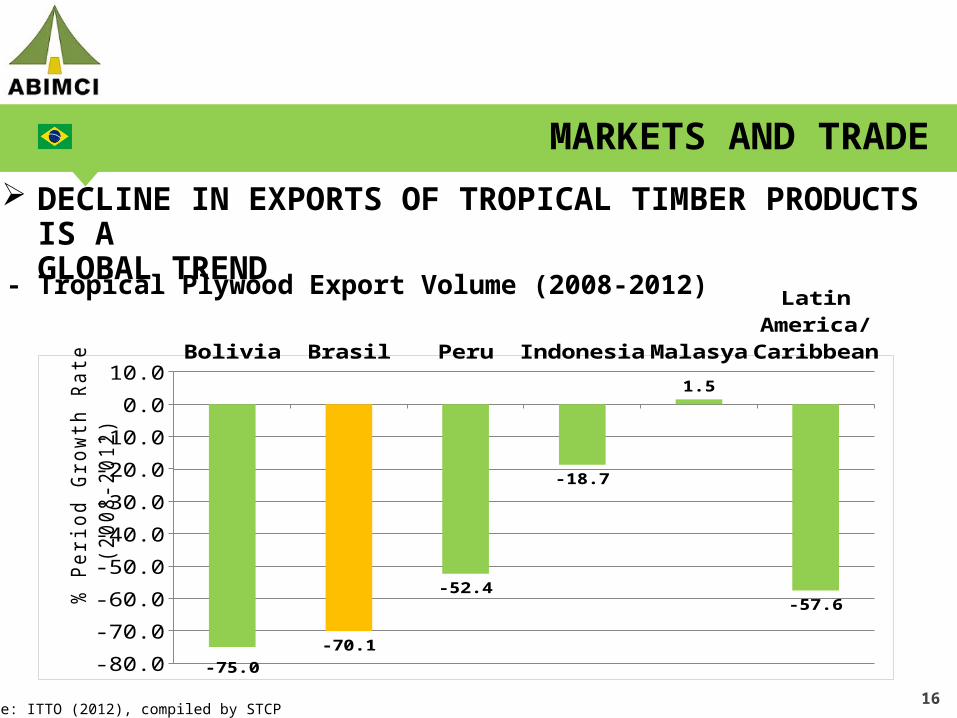

DECLINE IN EXPORTS OF TROPICAL TIMBER PRODUCTS IS A GLOBAL TREND

MARKETS AND TRADE

Bolivia Brasil Peru Indonesia Malasya

LatinAmerica/Caribbean

-80.0

-70.0

-60.0

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

-75.0-70.1

-52.4

-18.7

1.5

-57.6

% P

erio

d G

row

th R

ate

(200

8-20

12)

Source: ITTO (2012), compiled by STCP

- Tropical Plywood Export Volume (2008-2012)

17

PERSPECTIVES

18

PERSPECTIVES

TRADE IS EXPECTED TO CONTINUE TO DECLINE…

The international trade of tropical timber products has been affected by:

- Competition with other timber products (plantations);- Development of new competitive products and finishing materials;- Increase in the logistics costs for tropical timber;- Increase in transaction costs (local and international- EU FLEFT, United States’

Lacey Act, Australia’s Illegal Logging Act, etc); - Market access: barriers and impediments;- Lack of market promotion and product image- Reduction and restrictions on supply;- Lack of investments on technology developments to increase competitiveness.

19

PERSPECTIVES

TROPICAL PLANTATION TIMBER IS AN ALTERNATIVE…

There are successful tropical plantations that can enhance competitiveness of tropical timber products in the global market

- Teak- Acacia- Eucalyptus- African Mahogany- Others

Efforts are needed to maintain competitiveness: - Increase productivity of plantations and industrial operations - Develop and improve products performance

20

PERSPECTIVES

TO ENSURE THAT TROPICAL FORESTS ARE SUSTAINABLY MANAGED AND TROPICAL TIMBER INDUSTRY CONTINUE TO CONTRIBUTE TO IMPROVE THE SOCIAL-ECONOMIC CONDITIONS OF TROPICAL COUNTRIES IS FUNDAMENTAL A GLOBAL COORDINATED EFFORT TO INCREASE THE COMPETITIVENESS OF TROPICAL TIMBER PRODUCTS IN THE MARKET

It is important to consider:- Reduction of transaction costs and market barriers / impediments- Technology developments to improve use of resources and products

performance- Market promotion to improve image

21

PERSPECTIVES

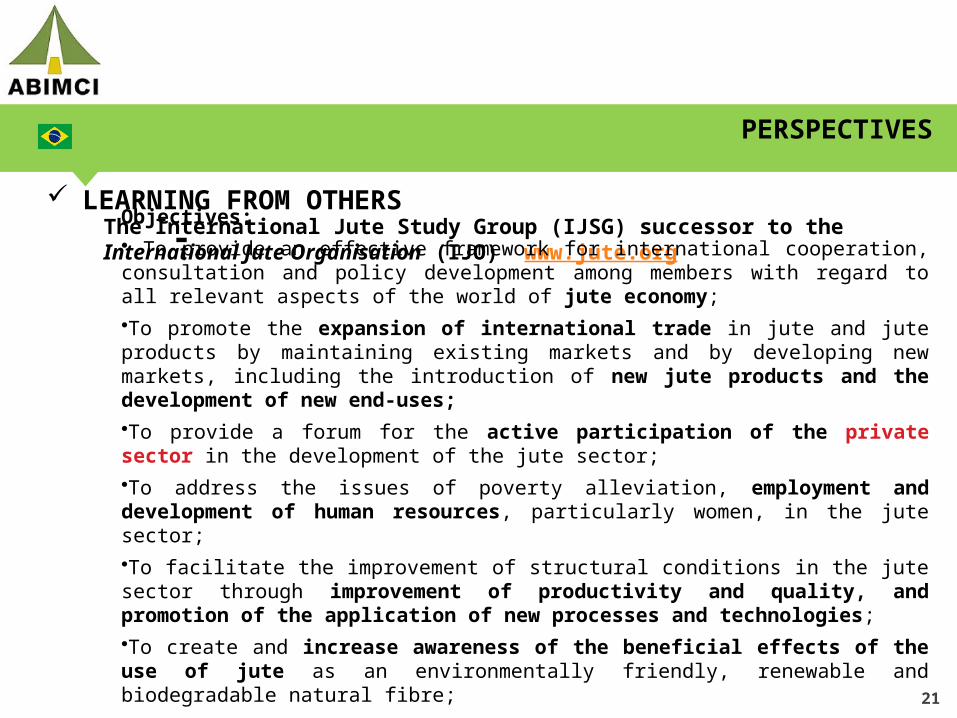

LEARNING FROM OTHERS - The International Jute Study Group (IJSG) successor to the International Jute Organisation (IJO)

www.jute.org

Objectives: • To provide an effective framework for international cooperation, consultation and policy development among members with regard to all relevant aspects of the world of jute economy;•To promote the expansion of international trade in jute and jute products by maintaining existing markets and by developing new markets, including the introduction of new jute products and the development of new end-uses;•To provide a forum for the active participation of the private sector in the development of the jute sector;•To address the issues of poverty alleviation, employment and development of human resources, particularly women, in the jute sector;•To facilitate the improvement of structural conditions in the jute sector through improvement of productivity and quality, and promotion of the application of new processes and technologies;•To create and increase awareness of the beneficial effects of the use of jute as an environmentally friendly, renewable and biodegradable natural fibre;•To improve market intelligence with a view to ensuring greater transparency in the international jute market in collaboration with other organizations, including the Food and

22

PERSPECTIVES

LEARNING FROM OTHERS - The International Coffee Organization (established in 1963)

Private Sector Consultative Board

The Private Sector Consultative Board (PSCB) is an ICO body which provides a platform for the representatives of private sector organizations of producing and consuming countries. Established in 1999, it consults with and advises the Council on issues relevant to the coffee sector, either on request or on its own initiative.The PSCB comprises 16 leading industry representatives from producing and consuming countries, along with their alternates and advisers. It generally meets at the time of the International Coffee Council meetings in March and September each year and its Chairperson reports to the Council on the outcome of its meeting. At the meetings, PSCB representatives review a range of coffee issues including sustainability initiatives, food safety aspects, quality and coffee and health. The PSCB has agreed that its main mission and objective should be to increase the world coffee market in value and volume. One of the constraints for increasing coffee consumption was the misconception that coffee is bad for your health held by part of the population. On the contrary, there is significant scientific information available on various positive health benefits associated with coffee drinking.www.ico.org

23

PERSPECTIVES

WHY WE ARE WE MOVING TO ANOTHER DIRECTION?

24

THANK YOU !

Presentation available inwww.stcp.com.br