1 Investors’ appetite for real estate companies on AIM 18 February 2008 Zimmerman Adams...

28

1 Investors’ appetite for real Investors’ appetite for real estate companies on AIM estate companies on AIM 18 February 2008 18 February 2008 Zimmerman Adams International Ltd A Practitioner’s View A Practitioner’s View Zimmerman Adams International Limited Registered in England and Wales No. 5136014; Registered Office: One Threadneedle Street, London EC2R 8AW Authorised and Regulated by the Financial Services Authority Member of the London stock exchange

-

date post

19-Dec-2015 -

Category

Documents

-

view

219 -

download

0

Transcript of 1 Investors’ appetite for real estate companies on AIM 18 February 2008 Zimmerman Adams...

1

Investors’ appetite for real estate Investors’ appetite for real estate companies on AIMcompanies on AIM

18 February 200818 February 2008

Zimmerman Adams International Ltd

A Practitioner’s ViewA Practitioner’s View

Zimmerman Adams International LimitedRegistered in England and Wales No. 5136014; Registered Office: One Threadneedle Street, London EC2R 8AW

Authorised and Regulated by the Financial Services Authority

Member of the London stock exchange

2

Contents

AIM – A Viable Alternative for Real Estate

How liquid can you be?

What makes a Company Suitable

ZAI Unique Qualifications

Case Study: DUPD

Appendix: Recent article

3

AIM: A Viable Alternative for Real Estate

4

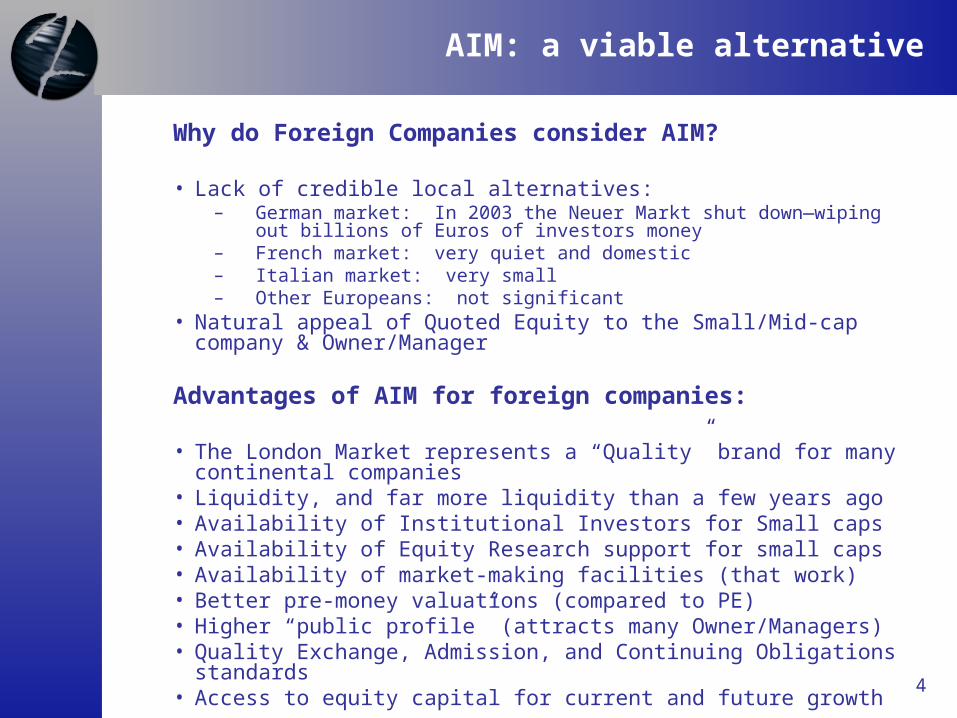

AIM: a viable alternative

Why do Foreign Companies consider AIM?

• Lack of credible local alternatives: – German market: In 2003 the Neuer Markt shut down—wiping out billions of

Euros of investors money– French market: very quiet and domestic– Italian market: very small– Other Europeans: not significant

• Natural appeal of Quoted Equity to the Small/Mid-cap company & Owner/Manager

Advantages of AIM for foreign companies:

• The London Market represents a “Quality” brand for many continental companies

• Liquidity, and far more liquidity than a few years ago• Availability of Institutional Investors for Small caps• Availability of Equity Research support for small caps• Availability of market-making facilities (that work)• Better pre-money valuations (compared to PE)• Higher “public profile” (attracts many Owner/Managers)• Quality Exchange, Admission, and Continuing Obligations standards• Access to equity capital for current and future growth

5

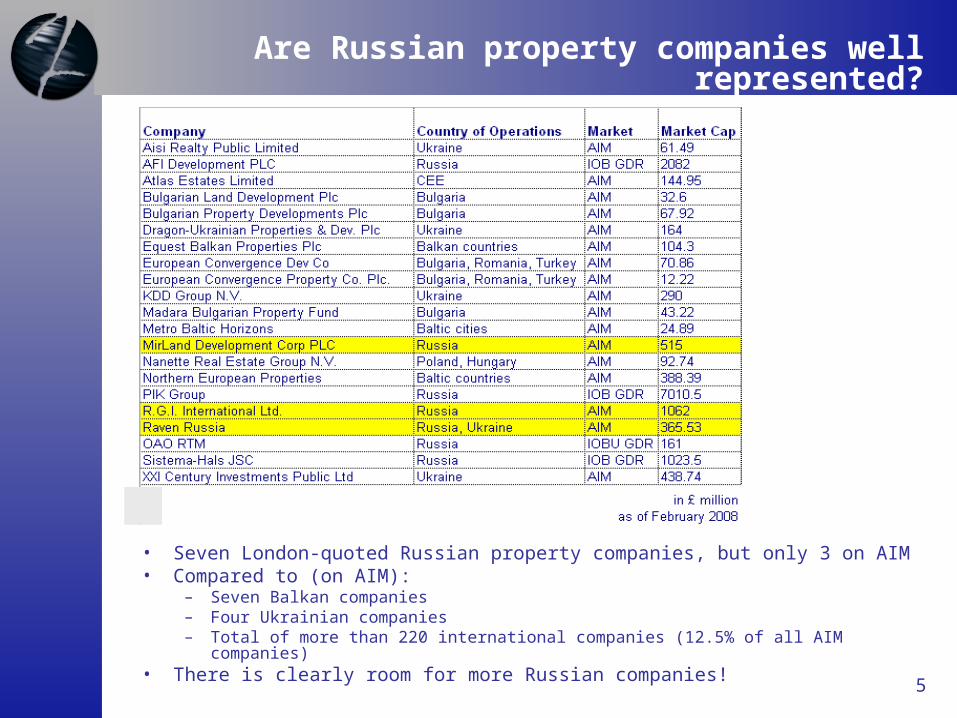

Are Russian property companies well represented?

• Seven London-quoted Russian property companies, but only 3 on AIM• Compared to (on AIM):

– Seven Balkan companies– Four Ukrainian companies– Total of more than 220 international companies (12.5% of all AIM companies)

• There is clearly room for more Russian companies!

6

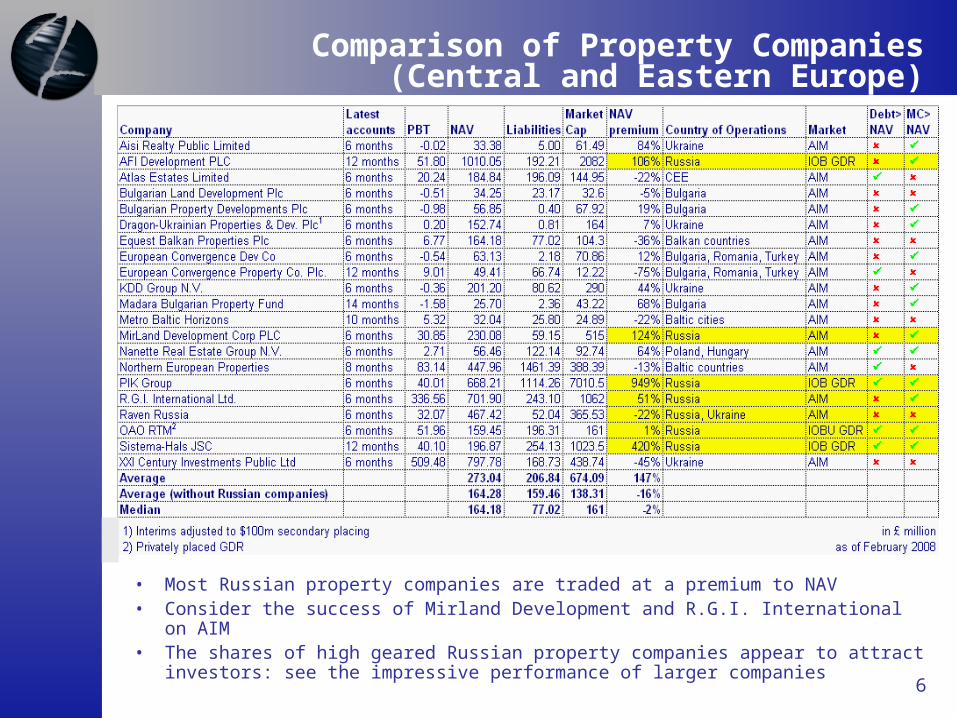

• Most Russian property companies are traded at a premium to NAV• Consider the success of Mirland Development and R.G.I. International on AIM• The shares of high geared Russian property companies appear to attract

investors: see the impressive performance of larger companies

Comparison of Property Companies(Central and Eastern Europe)

7

“It’s the economy, Stupid” (Bill Clinton 1992)

-i.e. The basic economic growth of the region, supported by sound fundamentals, outweighs the many risks investors face

1. Nominal GDP per capita of $14,000 in Russia (approximately 45% of Euro area) but well ahead of other BRIC countries

2. S&P awarded Russia “investment grade” status in 20073. GDP growth forecasted at above 5% for next 3 years in the CIS countries4. Robust economy will fuel corporate earnings in the medium term5. The first phase of London IPO’s have inevitably been natural resources

but...6. ZAI forecasts a growth of interest in mid cap property company IPO’s as

the property business in Russia matures and the population develops sustainable disposable income to be spent on housing

7. There is now an emerging private equity market in Russia, which signals the beginning of less risky business models

Why Invest in Russian Property companies: “it’s the economy, stupid” ?

8

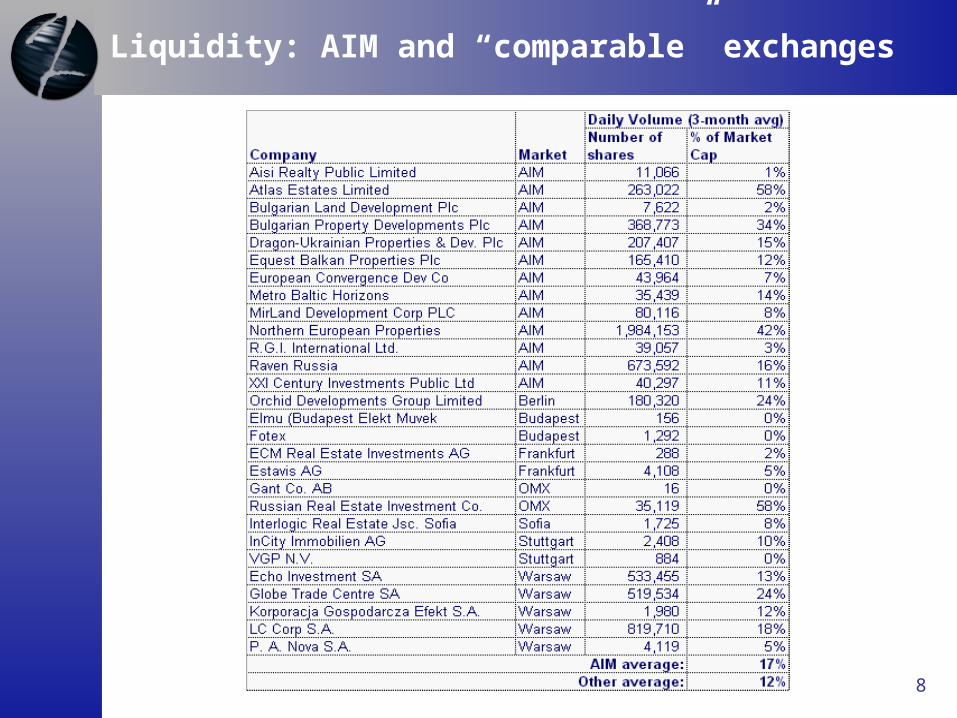

Liquidity: AIM and “comparable” exchanges

9

Availability of Equity Capital for International Companies in London:

(Don’t take my word for it – look at the empirical evidence)

10

0

500

1,000

1,500

2,000

2,500

3,000

Eq

uit

y a

ss

ets

un

de

r

ma

na

ge

me

nt

US

$b

n

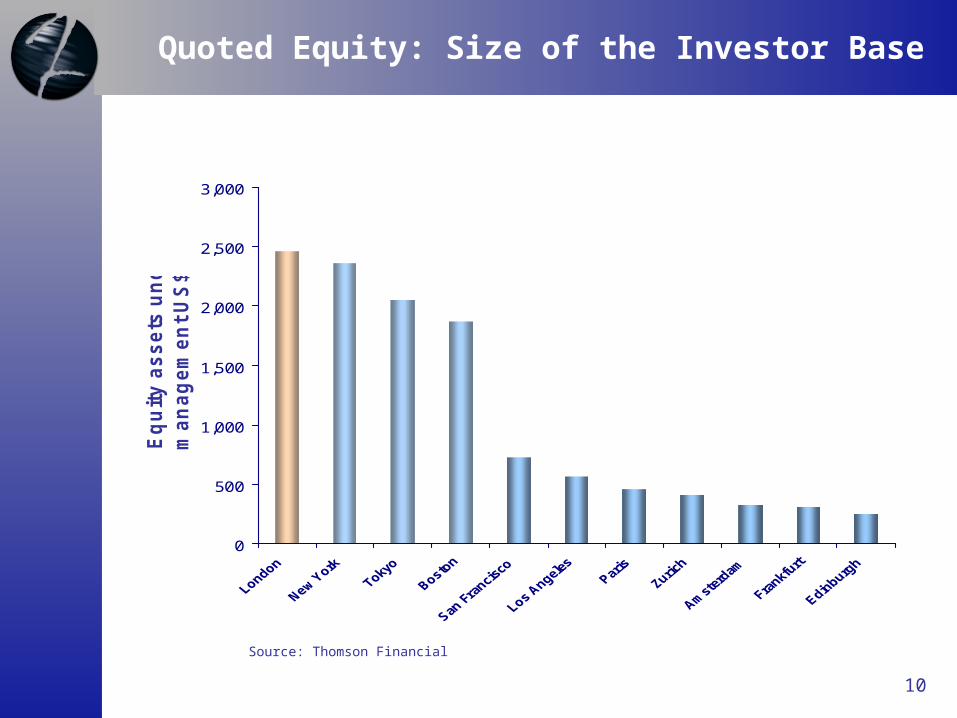

Source: Thomson Financial

Quoted Equity: Size of the Investor Base

11

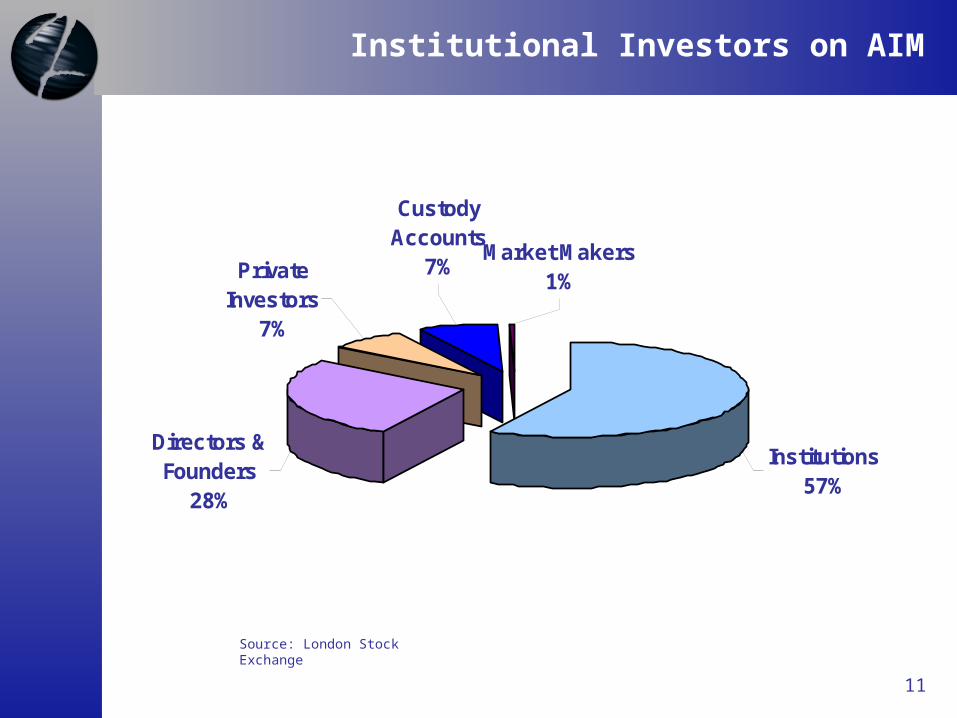

Source: London Stock Exchange

Institutional Investors on AIM

Market Makers1%

Custody Accounts

7%Private Investors

7%

Institutions57%

Directors & Founders

28%

12

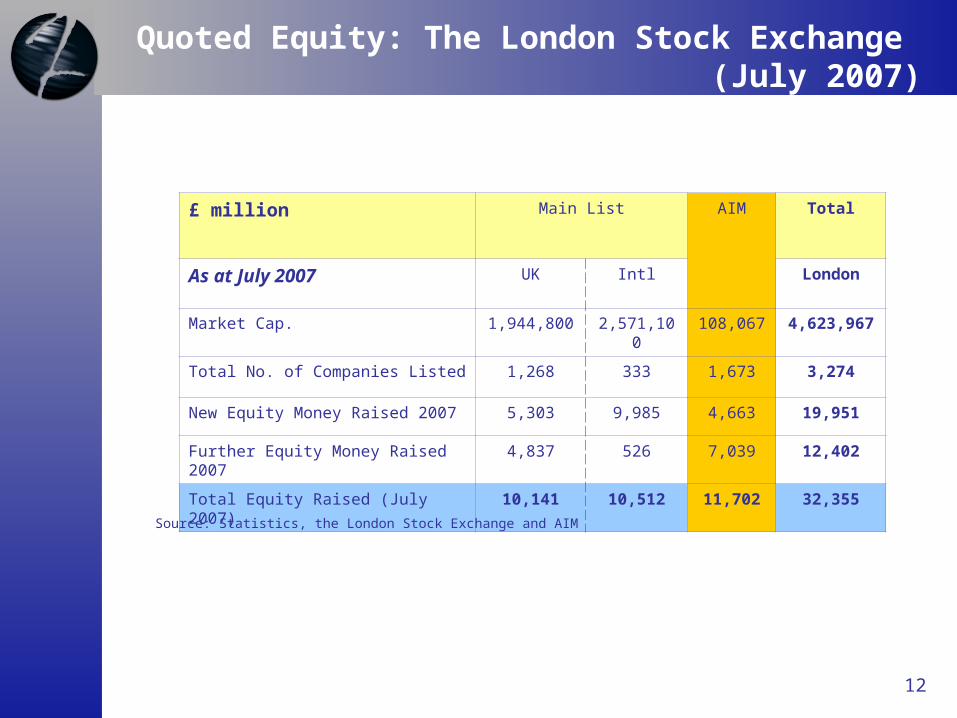

Quoted Equity: The London Stock Exchange

(July 2007)

£ million Main List AIM Total

As at July 2007 UK Intl London

Market Cap. 1,944,800 2,571,100 108,067 4,623,967

Total No. of Companies Listed 1,268 333 1,673 3,274

New Equity Money Raised 2007 5,303 9,985 4,663 19,951

Further Equity Money Raised 2007 4,837 526 7,039 12,402

Total Equity Raised (July 2007) 10,141 10,512 11,702 32,355

Source: Statistics, the London Stock Exchange and AIM

13

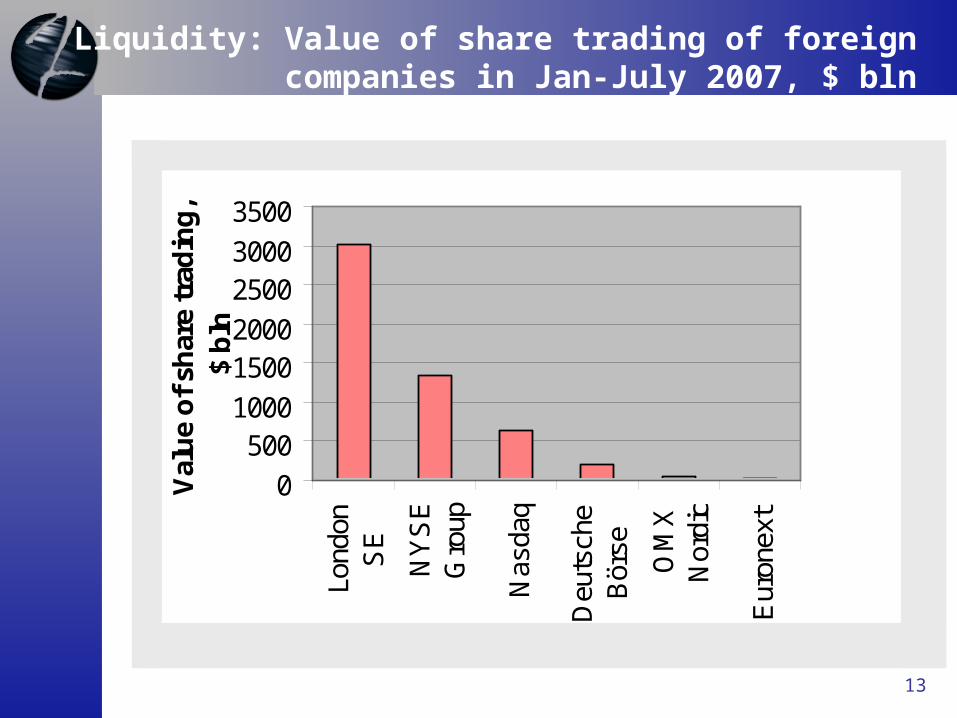

Liquidity: Value of share trading of foreign companies in Jan-July 2007, $ bln

0

5001000

15002000

25003000

3500

Lond

onS

E

NY

SE

Gro

up

Nas

daq

Deu

tsch

eB

örse

OM

XN

ordi

c

Eur

onex

t

Val

ue

of

shar

e tr

adin

g,

$ b

ln

14

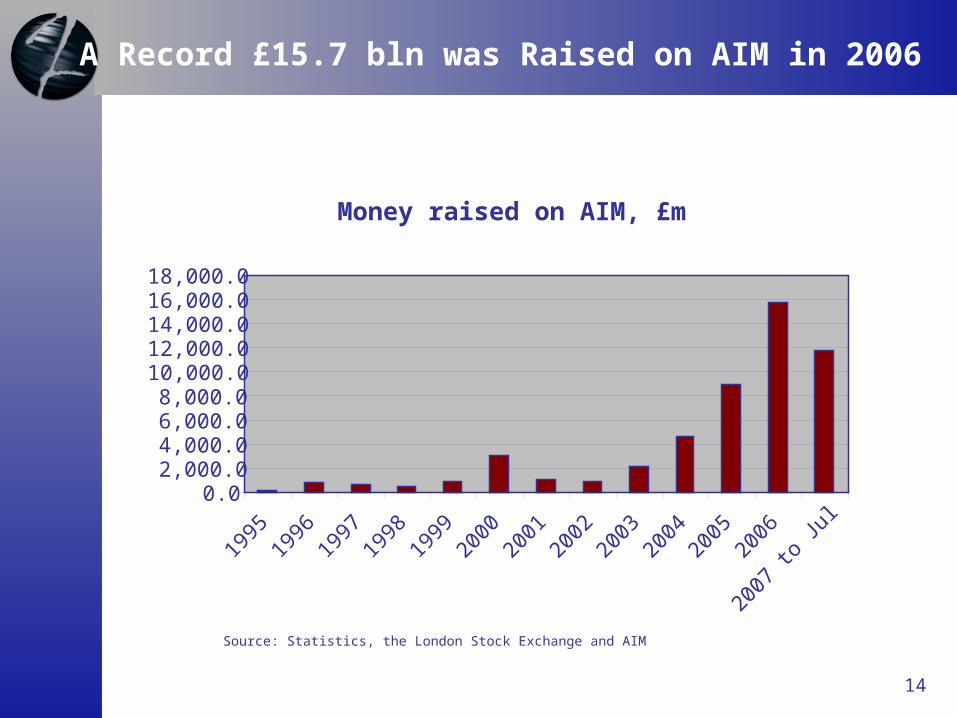

A Record £15.7 bln was Raised on AIM in 2006

Source: Statistics, the London Stock Exchange and AIM

Money raised on AIM, £m

0.02,000.04,000.06,000.08,000.0

10,000.012,000.014,000.016,000.018,000.0

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

to Ju

l

15

What makes a company suitable ?

16

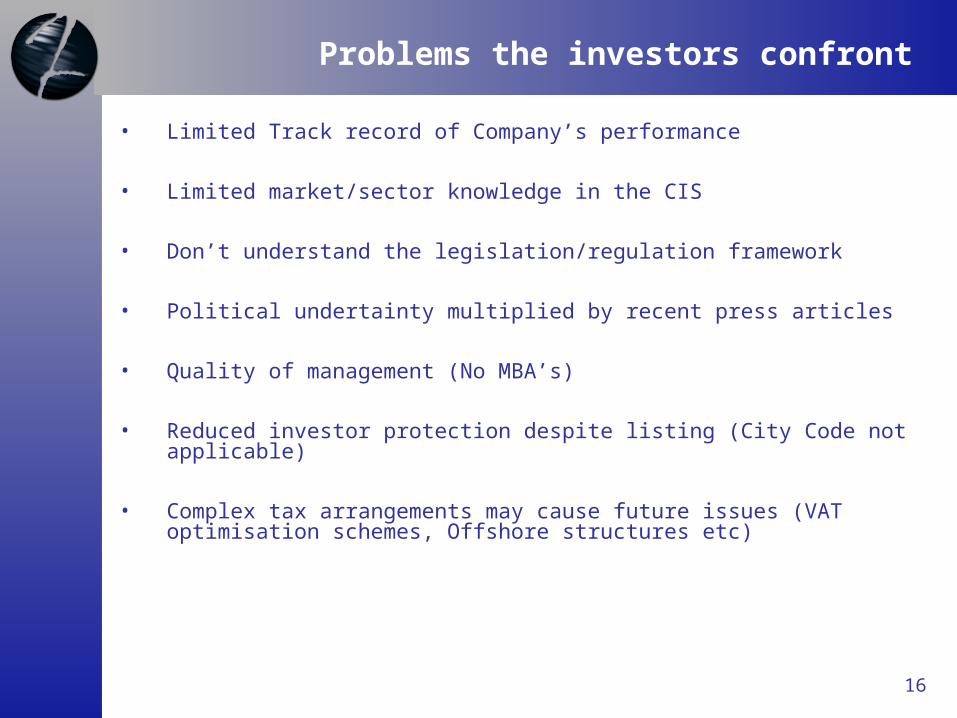

• Limited Track record of Company’s performance

• Limited market/sector knowledge in the CIS

• Don’t understand the legislation/regulation framework

• Political undertainty multiplied by recent press articles

• Quality of management (No MBA’s)

• Reduced investor protection despite listing (City Code not applicable)

• Complex tax arrangements may cause future issues (VAT optimisation schemes, Offshore structures etc)

Problems the investors confront

17

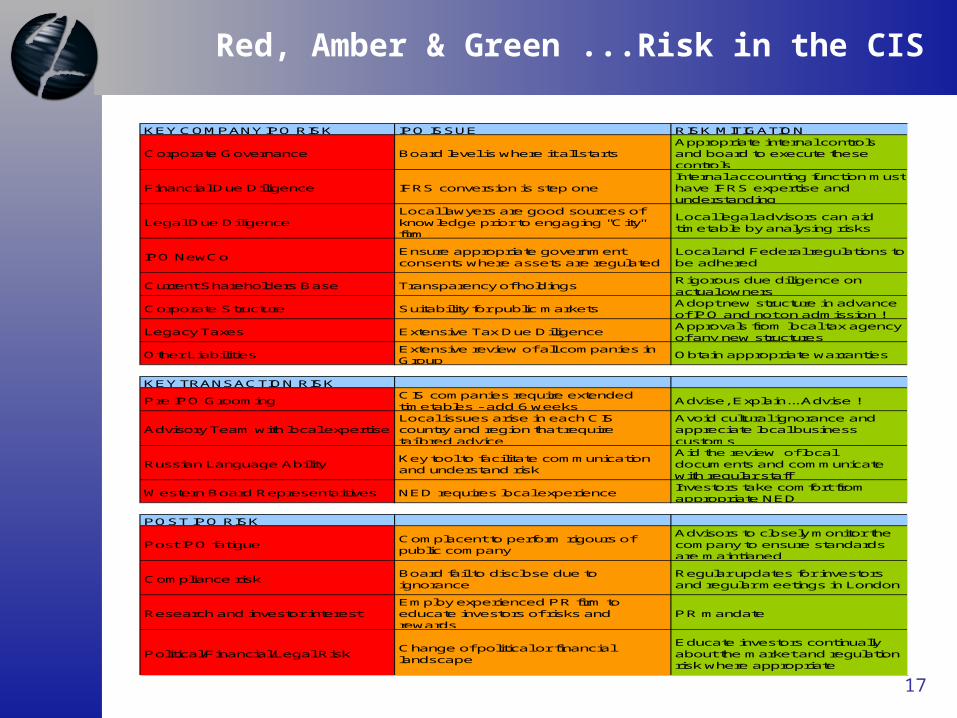

KEY COMPANY IPO RISK IPO ISSUE RISK MITIGATION

Corporate Governance Board level is where it all startsAppropriate internal controls and board to execute these controls

Financial Due Diligence IFRS conversion is step oneInternal accounting function must have IFRS expertise and understanding

Legal Due DiligenceLocal lawyers are good sources of knowledge prior to engaging "City" firm

Local legal advisors can aid timetable by analysing risks

IPO NewCo Ensure appropriate government consents where assets are regulated

Local and Federal regulations to be adhered

Current Shareholders Base Transparency of holdingsRigorous due diligence on actual owners

Corporate Structure Suitability for public marketsAdopt new structure in advance of IPO and not on admission !

Legacy Taxes Extensive Tax Due DiligenceApprovals from local tax agency of any new structures

Other LiabilitiesExtensive review of all companies in Group

Obtain appropriate warranties

KEY TRANSACTION RISK

Pre IPO Grooming CIS companies require extended timetables - add 6 weeks

Advise, Explain....Advise !

Advisory Team with local expertiseLocal issues arise in each CIS country and region that require tailored advice

Avoid cultural ignorance and appreciate local business customs

Russian Language AbilityKey tool to facilitate communication and understand risk

Aid the review of local documents and communicate with regular staff

Western Board Representaitives NED requires local experience Investors take comfort from appropriate NED

POST IPO RISK

Post IPO fatigueComplacent to perform rigours of public company

Advisors to closely monitor the company to ensure standards are maintianed

Compliance riskBoard fail to disclose due to ignorance

Regular updates for investors and regular meetings in London

Research and investor interestEmploy experienced PR firm to educate investors of risks and rewards

PR mandate

Political/Financial/Legal RiskChange of political or financial landscape

Educate investors continually about the market and regulation risk where appropriate

Red, Amber & Green ...Risk in the CIS

18

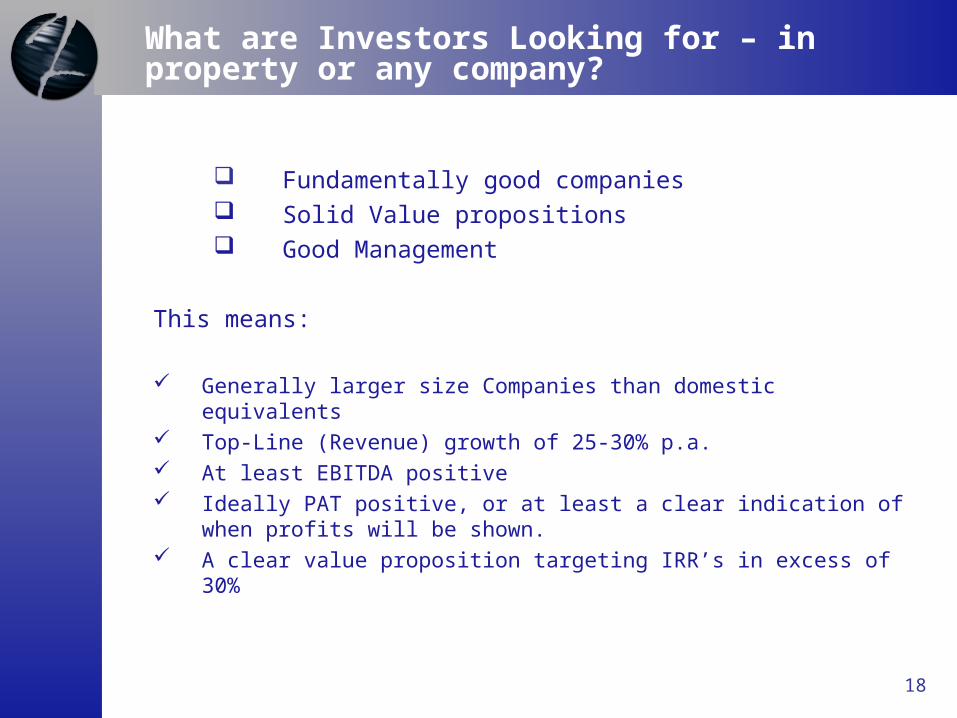

Fundamentally good companies Solid Value propositions Good Management

This means:

Generally larger size Companies than domestic equivalents Top-Line (Revenue) growth of 25-30% p.a. At least EBITDA positive Ideally PAT positive, or at least a clear indication of when profits will be

shown. A clear value proposition targeting IRR’s in excess of 30%

What are Investors Looking for – in property or any company?

19

elements of a successful flotation: A CASE STUDY- Dragon Ukrainian Properties and Development PLC

• Country of operation: Ukraine• Country of registration: Isle of Man• Sector: property investment and development• Assets: Commercial and residential property projects• Investors concerns and expectations: Ukrainian elections in 2008,

construction supply side issues due to surge in demand for materials and skills

• IPO and Secondary placing: • Further developments:

–IPO Price: $2.02 –Secondary placing: $100m

–Market Cap: $208.0m –Current share price: $2.20

–Capital raised: $205.1m –Current market cap: $330m

20

CASE STUDY- Dragon Ukrainian Properties and Development PLC

DUPD.L

100

105

110

115

120

125

130

135

140

01/06/07 01/07/07 01/08/07 01/09/07 01/10/07 01/11/07 01/12/07 01/01/08 01/02/08

£ pence

21

Key elements of a successful flotation

for an Emerging Markets Property Company

As illustrated by: Dragon Ukrainian Properties & Development (DUPD)

• Four key success factors:

– A strong market story, with reliable independent market research available

• DUPD is focussed on an interesting and to large extent undeveloped market, with significant upside potential

• The Kiev market, for office, commercial, and residential, is a compelling story • There was (and is) quality independent research available on the market, from the

leading western property consultants

– Strong management team – able to communicate with investors• good English language skills are essential• Experience with investor communications are essential• Credible independent Directors

– Track record of management in the specific asset class in question• The management team must have credible experience in the specific asset class in

question, and the ability to show track record

– Pipeline of projects• Investors want to understand the opportunities and risks of the types of projects the

company will invest in• The ability to get the money invested quickly in quality projects is a big factor

22

ZAI Unique Qualifications

23

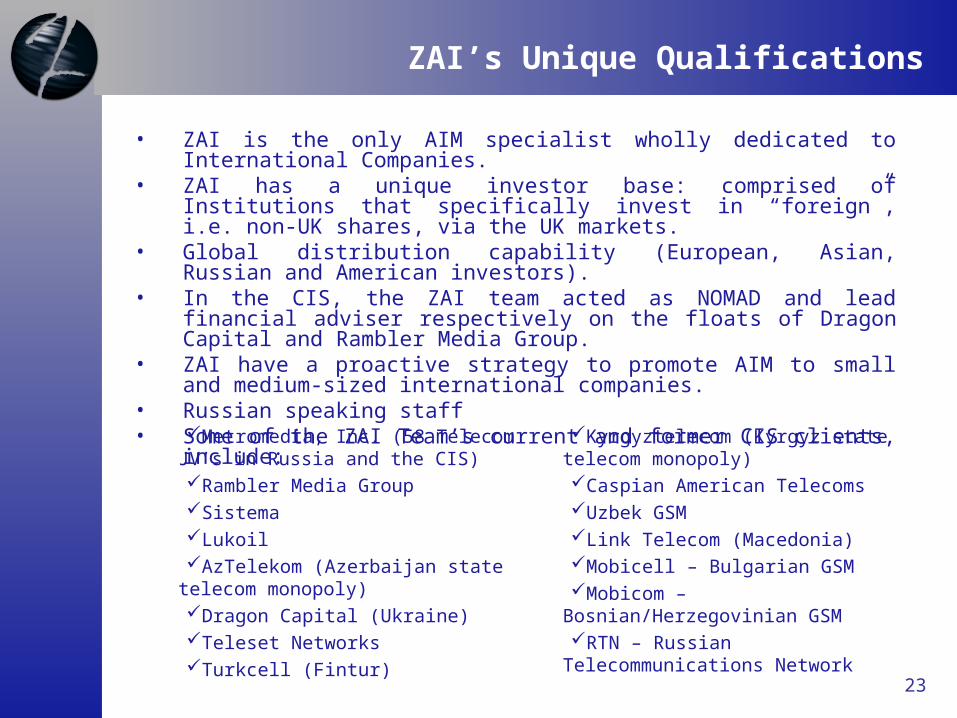

ZAI’s Unique Qualifications

• ZAI is the only AIM specialist wholly dedicated to International Companies.• ZAI has a unique investor base: comprised of Institutions that specifically

invest in “foreign”, i.e. non-UK shares, via the UK markets.• Global distribution capability (European, Asian, Russian and American

investors).• In the CIS, the ZAI team acted as NOMAD and lead financial adviser

respectively on the floats of Dragon Capital and Rambler Media Group. • ZAI have a proactive strategy to promote AIM to small and medium-sized

international companies.• Russian speaking staff • Some of the ZAI Team’s current and former CIS clients, include:

Metromedia, Inc. (58 Telecom JV’s in Russia and the CIS)Rambler Media GroupSistemaLukoilAzTelekom (Azerbaijan state telecom

monopoly)Dragon Capital (Ukraine)Teleset NetworksTurkcell (Fintur)

Kyrgyztelecom (Kyrgyz state telecom monopoly)Caspian American TelecomsUzbek GSMLink Telecom (Macedonia)Mobicell – Bulgarian GSMMobicom – Bosnian/Herzegovinian GSM RTN – Russian Telecommunications

Network

24

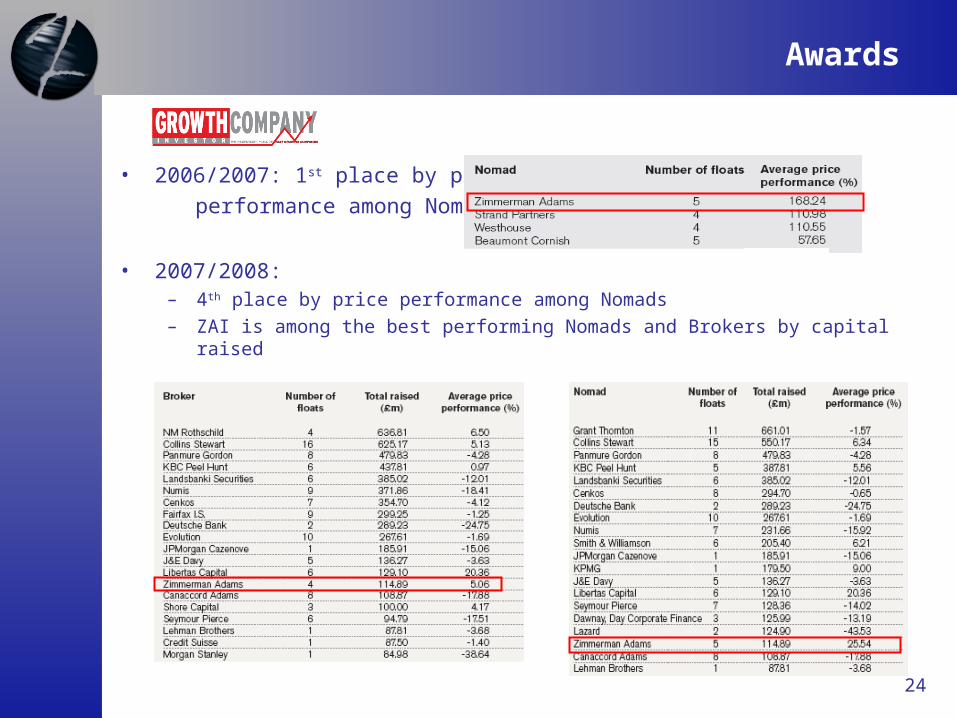

Awards

• 2006/2007: 1st place by price

performance among Nomads

• 2007/2008: – 4th place by price performance among Nomads

– ZAI is among the best performing Nomads and Brokers by capital raised

Brokers’ performance: Nomads’ performance:

25

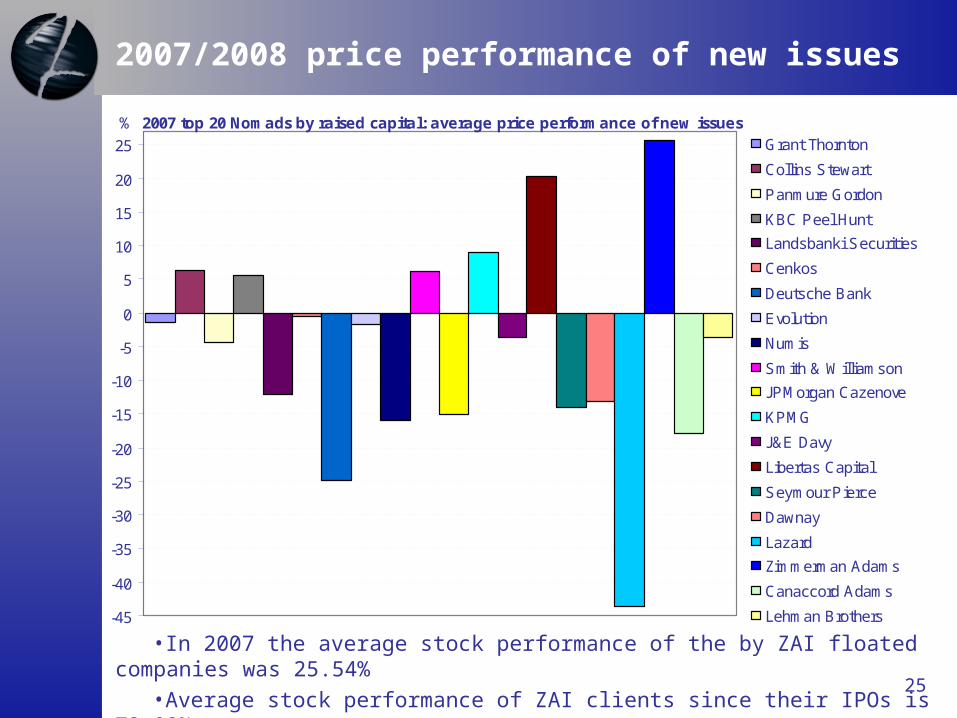

2007/2008 price performance of new issues

2007 top 20 Nomads by raised capital: average price performance of new issues

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

%Grant Thornton

Collins Stewart

Panmure Gordon

KBC Peel Hunt

Landsbanki Securities

Cenkos

Deutsche Bank

Evolution

Numis

Smith & Williamson

JPMorgan Cazenove

KPMG

J&E Davy

Libertas Capital

Seymour Pierce

Dawnay

Lazard

Zimmerman Adams

Canaccord Adams

Lehman Brothers

•In 2007 the average stock performance of the by ZAI floated companies was 25.54%•Average stock performance of ZAI clients since their IPOs is 73.02%

26

Conclusions

• The record shows: Foreign Issuers CAN benefit from AIM.

• Such deals CAN be done, and money can successfully be raised, if left to specialist firms.

• Zimmerman Adams International have the expertise to do successful floats

27

Contact Details

Zimmerman Adams InternationalNew Broad Street House35 New Broad StreetLondon EC2M 1NHUnited Kingdom

Ray ZimmermanAleksej KotiasviliPh: +44 20 7060 1760Fax: +44 20 7060 1761E-mail: [email protected]: [email protected]

Irina LomovaPh: +7 (926) 492 3424E-mail: [email protected]

Website: www.zimmint.com

28

Appendix

Non-UK listings on Aim increaseBy Robert Orr Published: January 30 2008 02:00 | Last updated: January 30 2008 02:00

The total value of international groups to list on London's junior equities market in the past quarter exceeded that of domesticcompanies for the first time.

The total market capitalisation of the 31 non-UK stocks that floatedon the alternative investment market (Aim) in the fourth quarter of 2007 totalled £1.9bn ($3.8bn) compared with £1.7bn forUK listings, according to figures from Deloitte, the professional services firm.

The number of companies joining Aim almost halved to 254 last year, while the total value of both UK and non-UK companies listing in the past quarter was well down on the same quarter of 2006. By contrast, the amount raised in the secondary market held up.

Recent Articles