1 Implementing Risk Management: Adapting Normative Practice to Russian Specifics Adam Smith...

25

1 Implementing Risk Management: Adapting Normative Practice to Russian Specifics Adam Smith Conference – Russian Banking London 6 December 2005 Philip M Halperin Challenges and Compensatory Techniques

-

Upload

claud-scott -

Category

Documents

-

view

219 -

download

0

Transcript of 1 Implementing Risk Management: Adapting Normative Practice to Russian Specifics Adam Smith...

1

Implementing Risk Management: Adapting Normative Practice to Russian Specifics

Adam Smith Conference – Russian Banking

London 6 December 2005Philip M Halperin

Challenges and Compensatory Techniques

2

Alfa Bank snapshot

•112 branches in Russia, subsidiary banks in Ukraine and Kazakhstan, Holland, brokers in London and NYC•Universal bank - Retail, Commercial, Investment and Asset Management lines of business

3

Conceptual underpinning of Unified Risk Management

Credit RiskOperational Risk

Market Risk

Unified Risk Management – Overlapping skills sets, avoid silos!

Portfolio Management

Retail

4

Agenda

1) Institutional issues – transition economies (Russia, Kazakhstan, Ukraine):

2) Compensatory Technique – Implementation of Risk Management and RM Culture

3) Compensatory Technique – Adaptation of Normative Best Practice to Meet Challenges

Examples from Risk Management Areas – Market, Credit, Operational RM.

5

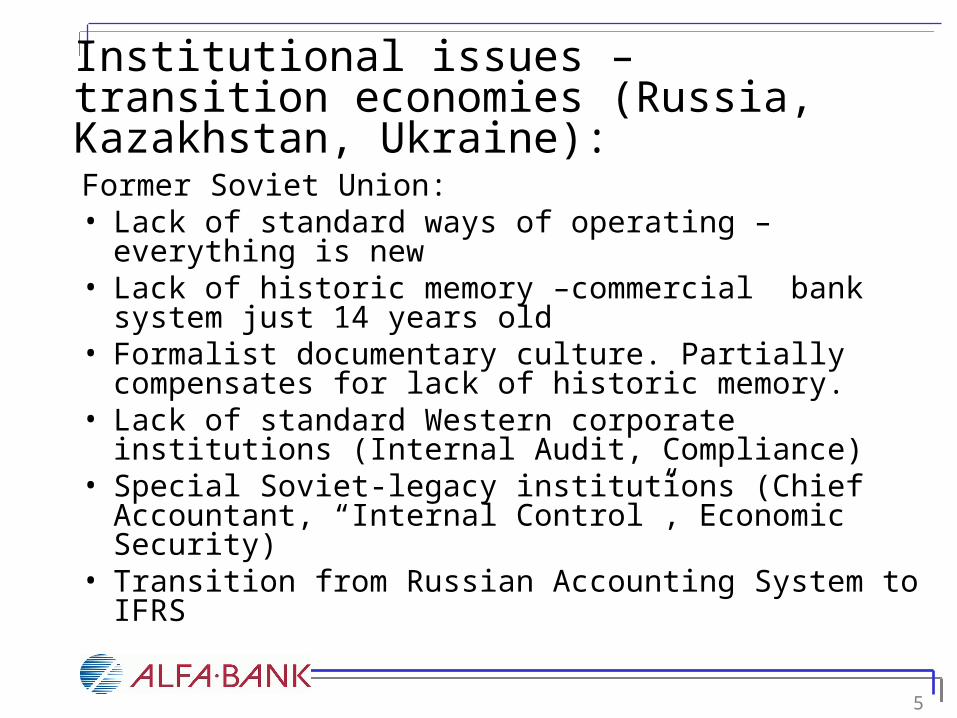

Institutional issues – transition economies (Russia, Kazakhstan, Ukraine):

Former Soviet Union:• Lack of standard ways of operating – everything is new• Lack of historic memory –commercial bank system just

14 years old• Formalist documentary culture. Partially compensates for

lack of historic memory.• Lack of standard Western corporate institutions (Internal

Audit, Compliance)• Special Soviet-legacy institutions (Chief Accountant,

“Internal Control”, Economic Security)• Transition from Russian Accounting System to IFRS

6

Institutional issues – transition economies (Russia, Kazakhstan, Ukraine):

• Information-poor environment• Lack of liquidity, transparency in markets

• Mismatch between risks and controls due to fast business, processes, and automation change

Most importantly … lack of risk culture … of managerial responsibility and systemic risks solutions

7

Institutional issues – transition economies (Russia, Kazakhstan, Ukraine):

• The environment and institutions of a transition economy are not conducive to standard technique only!

• One must be creative, and seek compensatory technique.

8

Achieving Management Buy-In – Document Ju-Jitsu

• Developed and promoted Group level Risk Policies

• Agreed and signed by every business leader

• Established business responsibility as Principle #1

• (Regulators like it as well!)

9

Examples of Compensatory Techniques - Implementation

• Use formal ‘Document Culture’ to implement new risk culture.

• Convert ‘Economic Security’ to be an active partner in the loss-collection process.– Threshold level to ensure business responsibility

• Use former-Soviet style collegial-bodies meetings to new goals.

10

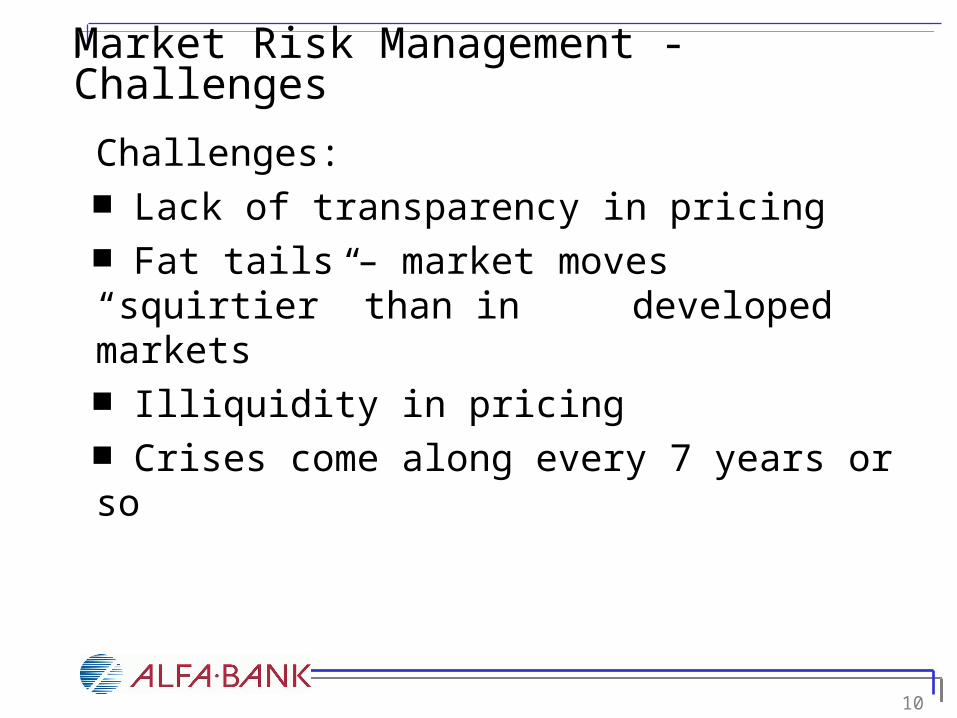

Market Risk Management - Challenges

Challenges: Lack of transparency in pricing Fat tails – market moves “squirtier” than in developed markets Illiquidity in pricing Crises come along every 7 years or so

11

Compensatory Techniques – Market RiskVaR (one day) vs. Liquidation Adjusted VaR

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

Equity M

oscow

Equity U

kr

Equity M

oscow+U

kr

FI Mosc

ow+Ukr

Forex

Turkey

Posi

tion

Deriv

ativ

es B

ook

Total M

oscow P

ositio

n

Total U

kr P

ositio

n

Total P

ositio

n

VaR

, LaV

aR (

mio

US

D) VaR (1% ql), mio USD

Liquidation adjustedVaR (1% ql), mio USD

12

Compensatory Techniques – Market RiskVaR (one day) vs. Stress Testing (one day)

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

Equity M

oscow

Equity U

kr

Equity M

oscow+Ukr

FI Mosc

ow+Ukr

Forex

Turkey

Posi

tion

Deriv

ativ

es B

ook

Total M

oscow P

ositio

n

Total U

kr P

ositio

n

Total P

ositio

n

Va

R,

Str

ess

(mio

US

D)

VaR (1% ql), mio USD

Stress Testing, mio USD

13

Compensatory Techniques – Market Risk

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

-7.00% -5.80% -4.60% -3.40% -2.20% -1.00% 0.20% 1.40% 2.60% 3.80% 5.00% 6.20%Return (%)

Fre

qu

ency

(%

)

Russian Trading System (RTS) Index: Empirical vs. Student's t Distribution

Empiricaldistribution

Normal distribution

Student's t (4 d.f.)

1% quantile (Normal)

1% quantile (Student's t)

14

Credit Risk Management - Challenges

Lack of reliable balance sheet data (IFRS desirable),

difficulty of correct factors choice

Lack of default data for calibration

Few borrowers have quoted liquid bonds

Few borrowers have liquid stocks

Asset market value and its volatility are usually

unobserved

15

Credit Expected Loss Estimation

1-PD

PD

CE

CE*RR

Credit is paid off: loss=0

Default: loss=CE*(1-RR)

Credit Expected Loss estimation:

Expected Loss = (1-PD)*0+PD*CE*(1-RR) = PD*CE*(1-RR)

«Event tree» of the credit:Components of credit risk estimation:

1. Credit exposure (CE)

2. Probability of default (PD)

3. Loss given default (LGD) or Recovery rate (RR)

LGD=1-RR

16

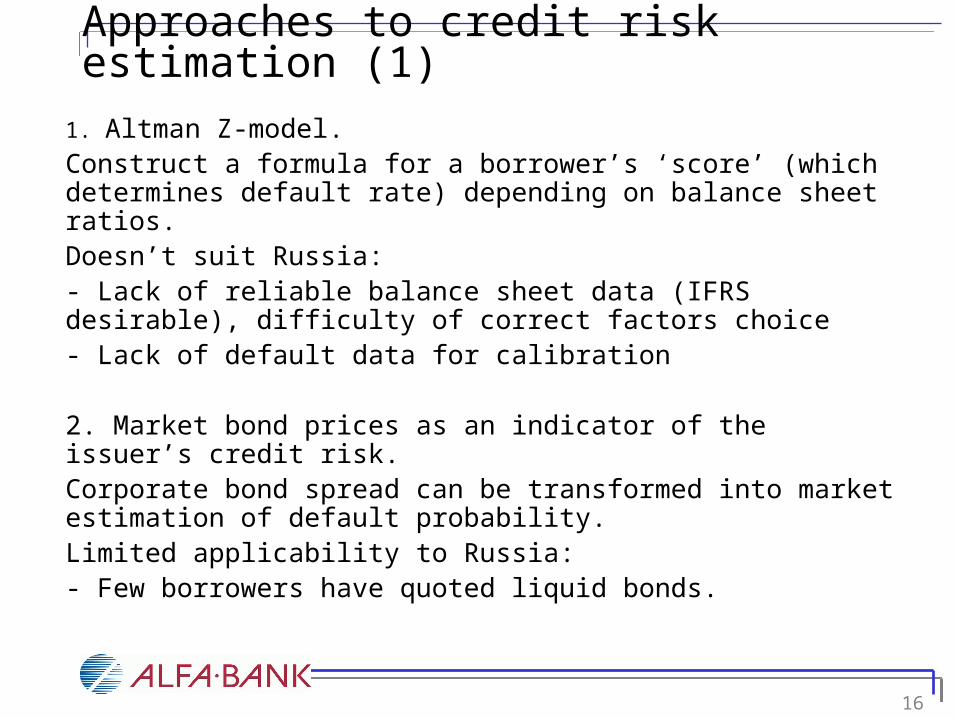

Approaches to credit risk estimation (1)

1. Altman Z-model.Construct a formula for a borrower’s ‘score’ (which determines default rate) depending on balance sheet ratios. Doesn’t suit Russia:- Lack of reliable balance sheet data (IFRS desirable), difficulty of correct factors choice - Lack of default data for calibration

2. Market bond prices as an indicator of the issuer’s credit risk.Corporate bond spread can be transformed into market estimation of default probability.Limited applicability to Russia:- Few borrowers have quoted liquid bonds.

17

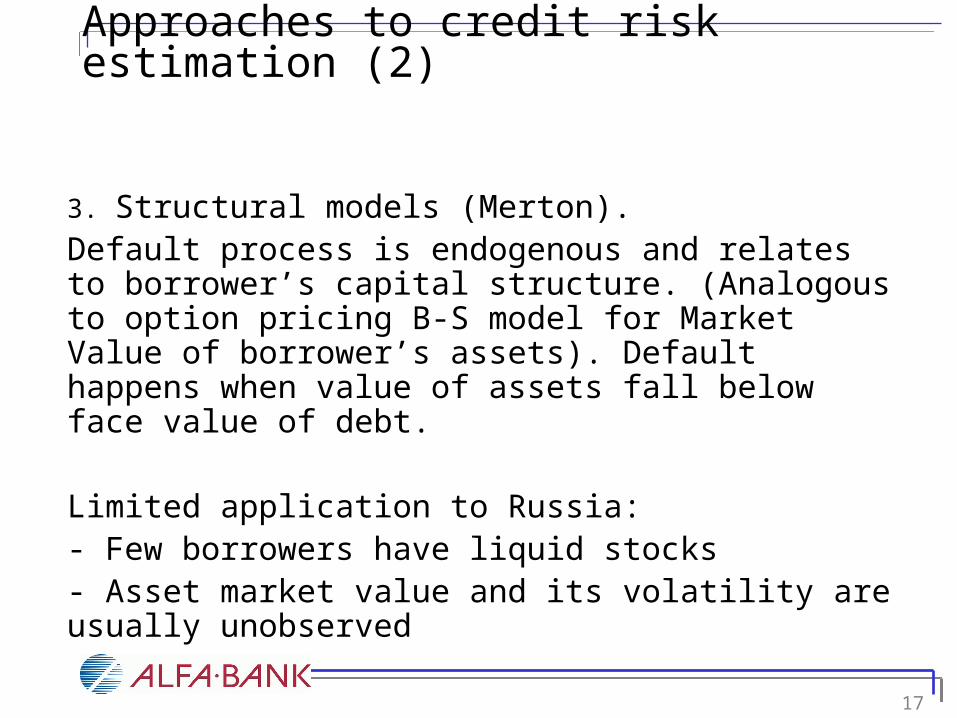

Approaches to credit risk estimation (2)

3. Structural models (Merton).Default process is endogenous and relates to borrower’s capital structure. (Analogous to option pricing B-S model for Market Value of borrower’s assets). Default happens when value of assets fall below face value of debt.

Limited application to Russia:- Few borrowers have liquid stocks- Asset market value and its volatility are usually unobserved

18

Credit RM – Compensatory Technique

4. Reduced-form models.Default probability depends on exogenous factors

(borrower’s characteristics, general economic variables); the dependency can be specified by logit or probit model.

This works in Russian environment. • Statistically significant estimates of default probability

were obtained using Bank’s proprietary credit portfolio payments and default information

19

Credit RM – Compensatory Technique Goal: Credit VaR Model: Loss Distribution

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

3.5

2

13

.5

23

.5

33

.5

43

.5

53

.5

63

.5

73

.5

83

.5

93

.5

10

4

11

4

12

4

13

4

14

4

15

4

16

4

17

4

18

4

19

4

20

4

21

4

22

4

23

4

24

4

Потери, $млн

Ча

сто

та

Квантиль 1% (3.9) Квантиль 5% (6.8) Квантиль 95% (104.0) Квантиль 99% (148.2) Среднее (39.6) Станд.откл. (31.5)

20

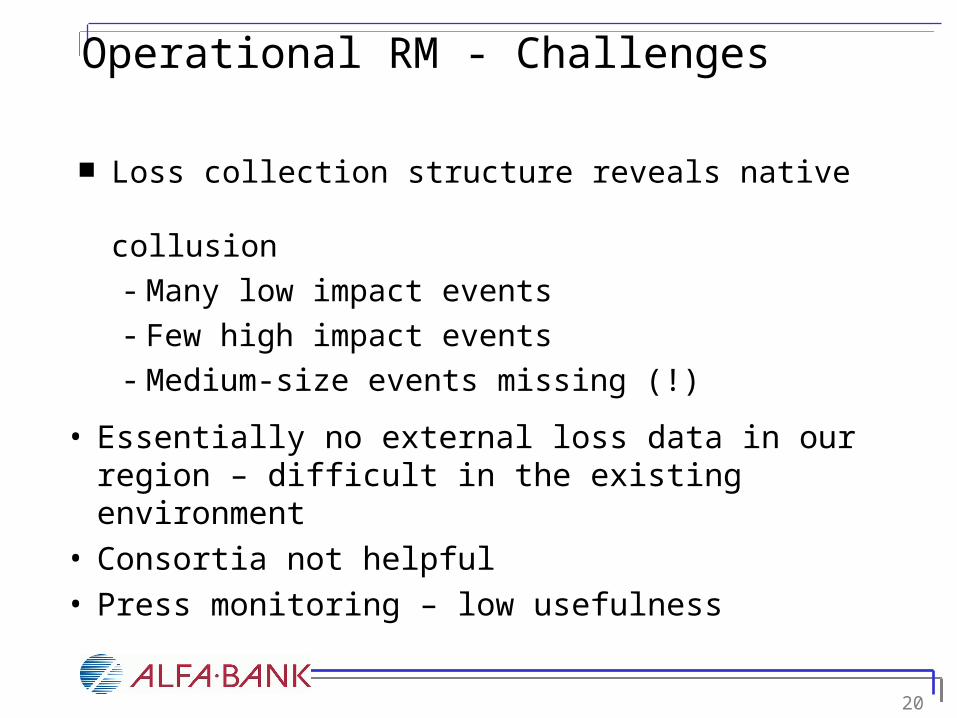

Operational RM - Challenges

Loss collection structure reveals native collusion- Many low impact events- Few high impact events- Medium-size events missing (!)

• Essentially no external loss data in our region – difficult in the existing environment

• Consortia not helpful• Press monitoring – low usefulness

21

Operational RM – Compensatory Techniques

Compensation:

We got External Data from

Insurance brokers:

22

Operational RM – Compensatory techniques

Compensation:

Work with ‘Economic Security Forces’

Patch and match external Insurance Broker sources

23

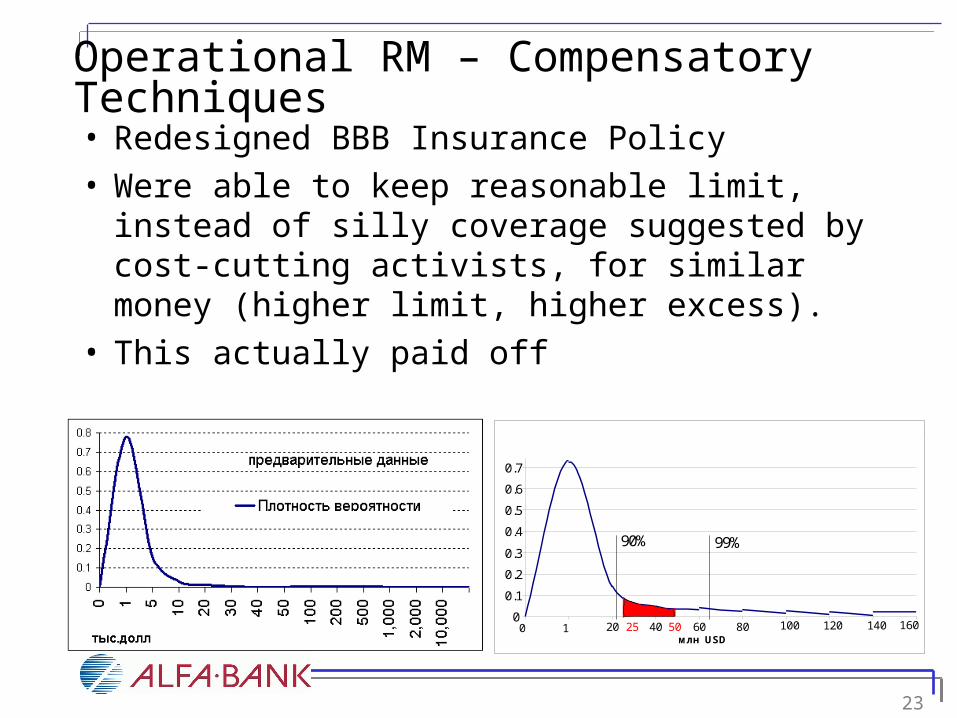

Operational RM – Compensatory Techniques

• Redesigned BBB Insurance Policy • Were able to keep reasonable limit, instead of silly

coverage suggested by cost-cutting activists, for similar money (higher limit, higher excess).

• This actually paid off

Разница цены – $214 000USD

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 1 20 40 60 80 100 120 140 160млн USD

5025

90% 99%

Разница цены – $214 000USD

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 1 20 40 60 80 100 120 140 160млн USD

5025

90% 99%

24

Summary• Russia is a market like any other market,

and different from all others like any other.• We must be

– creative in our implementation.– compensatory in our adaptation of

technique.

25

Contact InformationAlfa-Bank

http://www.alfabank.com/

http://www.alfabank.ru/

Philip M Halperin, Director of Risk Management

http://www.btinternet.com/~phalperin/