Corporate Self-Analysis Intelligent Business Analysis by Larraine D. Segil.

Upload

magdalen-coxCategory

view

218download

3

1

Corporate performance Corporate performance analysisanalysisFinancial ratio analysis and Financial ratio analysis and ratingrating

Helena SůvováHelena SůvováGuest lecture for the Czech University of Guest lecture for the Czech University of AgricultureAgricultureCourse: Corporate FinanceCourse: Corporate FinanceOctober, 2006October, 2006

2

Content of the lectureContent of the lecture

Sources of financial ratios (indicators), Sources of financial ratios (indicators), users of corporate performance users of corporate performance analysisanalysis

Basic groups of financial ratiosBasic groups of financial ratios Comprehensive systems of financial Comprehensive systems of financial

ratios, default prediction modelsratios, default prediction models Credit rating – external, internalCredit rating – external, internal Summary of the lectureSummary of the lecture Assignments for the tutorialAssignments for the tutorial

3

Sources of financial ratiosSources of financial ratios Financial statements: balance sheet, Financial statements: balance sheet,

income statement, statement of cash income statement, statement of cash flows, statement of retained earningsflows, statement of retained earnings

! Important: accounting /reporting ! Important: accounting /reporting standards standards • GAAPGAAP• IFRS or IFRS European versionIFRS or IFRS European version• CAS CAS

Accounting units registered on a regulated Accounting units registered on a regulated securities market in a EU Member State securities market in a EU Member State must report in IFRS – EU adjustedmust report in IFRS – EU adjusted

Accrual accounting – recognizes timing X Accrual accounting – recognizes timing X cash inflow – otflow: differences caused by: cash inflow – otflow: differences caused by: accrual principle, depreciation, taxesaccrual principle, depreciation, taxes

4

Sources of financial ratios, Sources of financial ratios, usersusers

Other sources: web pages of individual Other sources: web pages of individual firms, internet databases, paid firms, internet databases, paid databases – Magnus, Ariadnadatabases – Magnus, Ariadna

Users of corporate performance Users of corporate performance analysis:analysis:

stockholders, managers, employees, stockholders, managers, employees, business partners (customers, business partners (customers, suppliers), journalists, students, public suppliers), journalists, students, public generallygenerally

5

Basic groups of financial Basic groups of financial ratiosratios

Financial ratio = mathematical relationship Financial ratio = mathematical relationship among several variables (numbers), usually among several variables (numbers), usually stated in %, times, daysstated in %, times, days

Financial ratios are used to analyze firm´s Financial ratios are used to analyze firm´s financial performacefinancial performace

Ratios are not standardizedRatios are not standardized Ratios should not be analyzed in isolationRatios should not be analyzed in isolation Accounting standards affect the ratiosAccounting standards affect the ratios Comparisons: industry norms, key competitors, Comparisons: industry norms, key competitors,

previous periodprevious period

6

Basic groups of financial Basic groups of financial ratiosratios 5 basic groups:5 basic groups:

• liquidity ratiosliquidity ratios• debt management ratios (leverage ratios)debt management ratios (leverage ratios)• asset management ratios (activity ratios)asset management ratios (activity ratios)• profitability ratiosprofitability ratios• market value (valuation) ratiosmarket value (valuation) ratios

1) Liquidity ratios1) Liquidity ratiosfirm´s ability to pay its obligations in the short termfirm´s ability to pay its obligations in the short term

• current ratio = current assets/current liabilities (1,5)current ratio = current assets/current liabilities (1,5)• quick ratio = (current assets – inventory)/current liabilities (1)quick ratio = (current assets – inventory)/current liabilities (1)• cash ratio = (cash + near-cash)/current liabilities (0,25)cash ratio = (cash + near-cash)/current liabilities (0,25)• net working cap. to total assets = (curr.assets – curr. liab.)/total net working cap. to total assets = (curr.assets – curr. liab.)/total

assetsassets

7

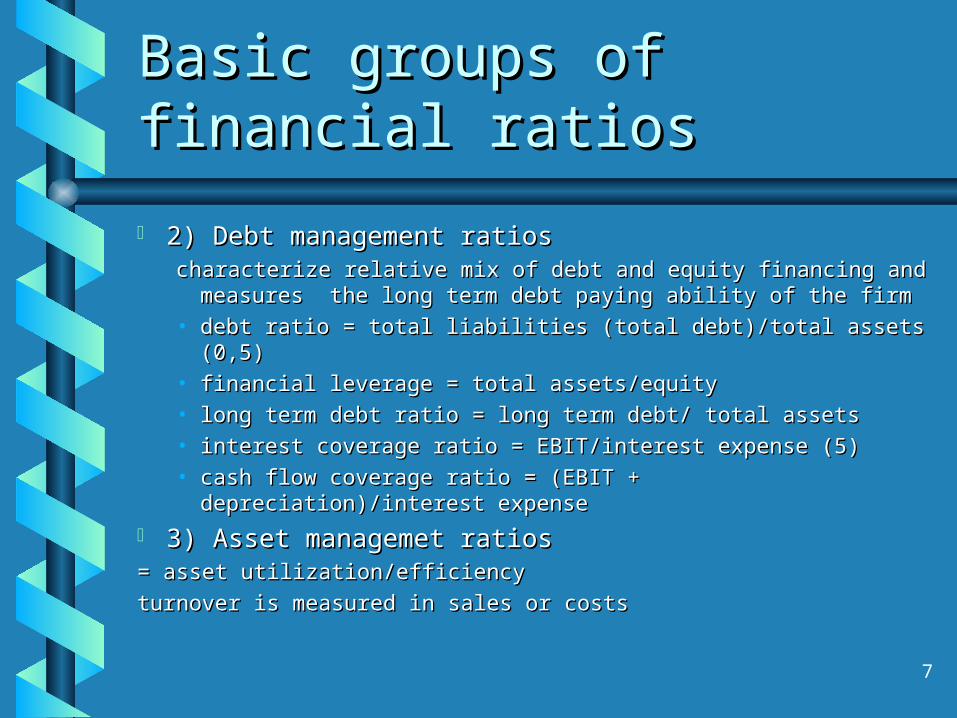

Basic groups of financial Basic groups of financial ratiosratios

2) Debt management ratios2) Debt management ratioscharacterize relative mix of debt and equity financing and characterize relative mix of debt and equity financing and

measures the long term debt paying ability of the firmmeasures the long term debt paying ability of the firm• debt ratio = total liabilities (total debt)/total assets (0,5)debt ratio = total liabilities (total debt)/total assets (0,5)• financial leverage = total assets/equityfinancial leverage = total assets/equity• long term debt ratio = long term debt/ total assetslong term debt ratio = long term debt/ total assets• interest coverage ratio = EBIT/interest expense (5)interest coverage ratio = EBIT/interest expense (5)• cash flow coverage ratio = (EBIT + depreciation)/interest cash flow coverage ratio = (EBIT + depreciation)/interest

expenseexpense 3) Asset managemet ratios3) Asset managemet ratios= asset utilization/efficiency= asset utilization/efficiency

turnover is measured in sales or coststurnover is measured in sales or costs

8

Basic groups of financial Basic groups of financial ratiosratios

• accounts receivable turnover = net credit sales/avrg accounts receivable turnover = net credit sales/avrg accounts receivable (60)accounts receivable (60)

• receivable collection period = 365/accounts receivable receivable collection period = 365/accounts receivable turnover (60)turnover (60)

• inventory turnover = cost of goods sold/ avrg inventoryinventory turnover = cost of goods sold/ avrg inventory• inventory collection period = 365/inventory turnover inventory collection period = 365/inventory turnover

ratio (60)ratio (60)• fixed assets turover = sales/ (net) fixed assetsfixed assets turover = sales/ (net) fixed assets

4) Profitability ratios4) Profitability ratiosfinal answer about the effevtivness of businessfinal answer about the effevtivness of business

• profit margin on sales = net income/ salesprofit margin on sales = net income/ sales• return on (total) assets ROA = EBIT/ total assetsreturn on (total) assets ROA = EBIT/ total assets• return on equity ROE = net income/ equityreturn on equity ROE = net income/ equity

9

Basic groups of financial Basic groups of financial ratiosratios

5) Market value ratios5) Market value ratios

most comprehensive measures of performancemost comprehensive measures of performance• P/E ratio = price of share/earnings per shareP/E ratio = price of share/earnings per share• market to book ratio = market value/book valuemarket to book ratio = market value/book value

10

Comprehensive systems of Comprehensive systems of financial ratios, default financial ratios, default prediction modelsprediction models

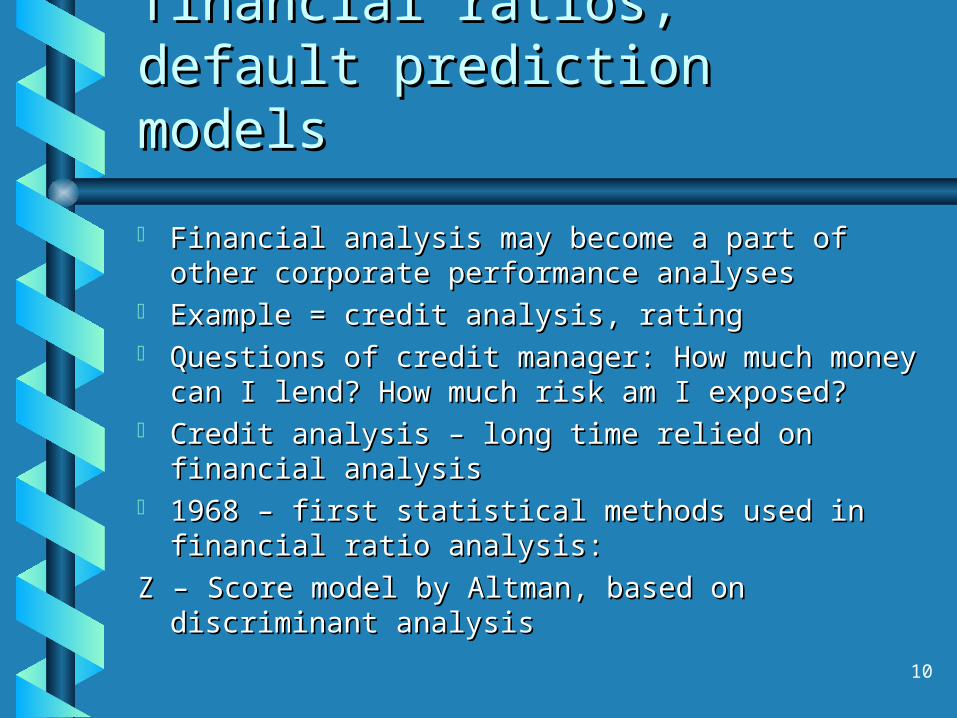

Financial analysis may become a part of other Financial analysis may become a part of other corporate performance analysescorporate performance analyses

Example = credit analysis, ratingExample = credit analysis, rating Questions of credit manager: How much money Questions of credit manager: How much money

can I lend? How much risk am I exposed?can I lend? How much risk am I exposed? Credit analysis – long time relied on financial Credit analysis – long time relied on financial

analysisanalysis 1968 – first statistical methods used in financial 1968 – first statistical methods used in financial

ratio analysis:ratio analysis:

Z – Score model by Altman, based on discriminant Z – Score model by Altman, based on discriminant analysisanalysis

11

Comprehensive systems of Comprehensive systems of financial ratios, default financial ratios, default prediction modelsprediction models

1977 – updated Zeta model1977 – updated Zeta model 1980 – KMV Corporation using modern portfolio 1980 – KMV Corporation using modern portfolio

theory → model Credit Monitor – default risk for theory → model Credit Monitor – default risk for publicly traded companies in North America and publicly traded companies in North America and EuropeEuropemodels like this are called „Merton“ modelsmodels like this are called „Merton“ models

1997 - J.P. Morgan developed Credit Metrics1997 - J.P. Morgan developed Credit Metrics 1999 - Moody´s introduced Risk Calc 1999 - Moody´s introduced Risk Calc 2002 - Kamakura Corporation credit risk models 2002 - Kamakura Corporation credit risk models

appeared – Merton type of models, reduced form appeared – Merton type of models, reduced form models (similar to Z-Score), hybrid combining both models (similar to Z-Score), hybrid combining both methodologiesmethodologies

12

Comprehensive systems of Comprehensive systems of financial ratios, default financial ratios, default prediction modelsprediction models

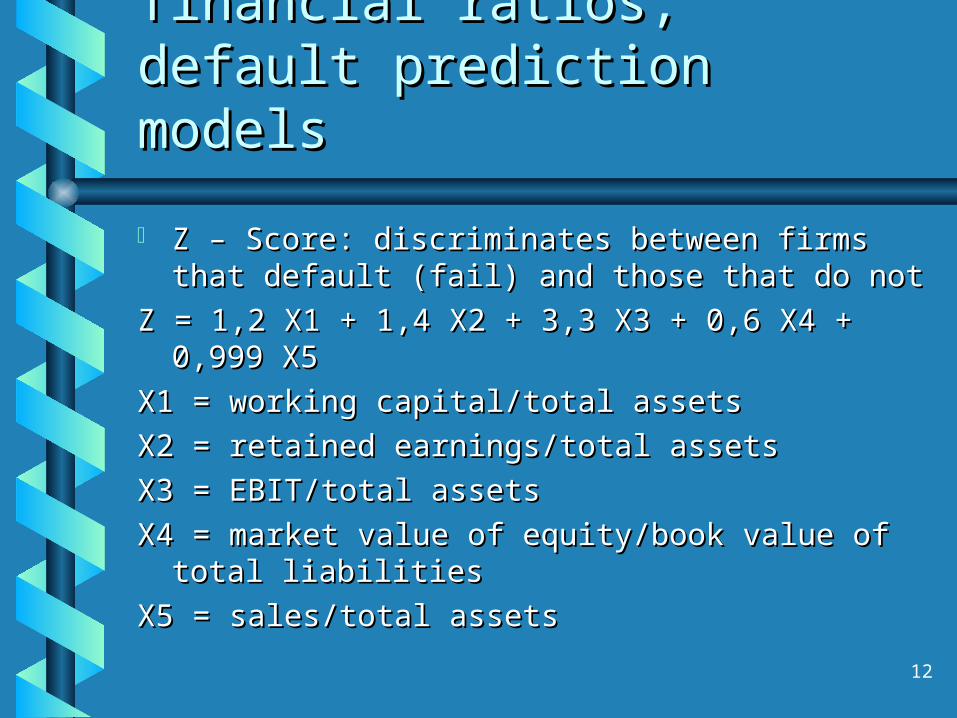

Z – Score: discriminates between firms that Z – Score: discriminates between firms that default (fail) and those that do notdefault (fail) and those that do not

Z = 1,2 X1 + 1,4 X2 + 3,3 X3 + 0,6 X4 + 0,999 Z = 1,2 X1 + 1,4 X2 + 3,3 X3 + 0,6 X4 + 0,999 X5X5

X1 = working capital/total assetsX1 = working capital/total assets

X2 = retained earnings/total assetsX2 = retained earnings/total assets

X3 = EBIT/total assetsX3 = EBIT/total assets

X4 = market value of equity/book value of total X4 = market value of equity/book value of total liabilitiesliabilities

X5 = sales/total assetsX5 = sales/total assets

13

Comprehensive systems of Comprehensive systems of financial ratios, default financial ratios, default prediction modelsprediction models

Czech index for assessment of the financial Czech index for assessment of the financial situation – IN index (index of Czech enterprise situation – IN index (index of Czech enterprise creditworthiness)creditworthiness)

Comprehensive financial analysis – using Comprehensive financial analysis – using organized system of financial ratios, e.g. Du organized system of financial ratios, e.g. Du Pont system or pyramid analysisPont system or pyramid analysis

14

M Z D T

M Z D T

M Z D T

M Z D T

M Z D T

M Z D T

M Z D T

+ + + +

:

L P K Z A V

L P A K T

K Z A V C K :

C K V K

N T

T Z A S

Z A S A K T

Z T

A K T V K

T A K T

Č Z

Z

Č Z V K

Č Z /VK – r en ta b ilita v la s t n íh o k ap it á lu Č Z /Z – p o d íl č is té h o zis k u n a zis ku k e zd a n ěn í Z /T – r en ta b ilita tr že b T /A K T – o b ra t a k tiv N /T – n á klad o v o s t t ržeb T /Z A S – o b ra t zá s o b Z A S /A K T – p o d íl zá s o b n a ak tiv e ch C K /VK – u k azat el zad lu že n o s ti

LP/ R ZA V – u k azat el ry c h lé lik v id ity M A T /T – m a te riá lo v á n ák la d n o s t M Z D /T – m zd o v á n ák la d n o s t O D P /T – p o d íl o d p is ů n a t ržb á ch F N /T – f in an č n í n ák la d n o s t O S TN / T – p o d íl o s ta tn íc h n ák la d ů n a tr žb á ch M Z D /P – p r ů m ěrn á m zd a p rac o v n ík a T /P – p ro d u kt iv ita p rá c e mě ře n á tr žb am i n a p ra co v n íka

O b r. č . 3- 3 : P y r a m ido v á s ou s ta v a fin a n č n íc h u k a z a te lů

Example of pyramid systemExample of pyramid system::

15

Credit rating – external, Credit rating – external, internalinternal

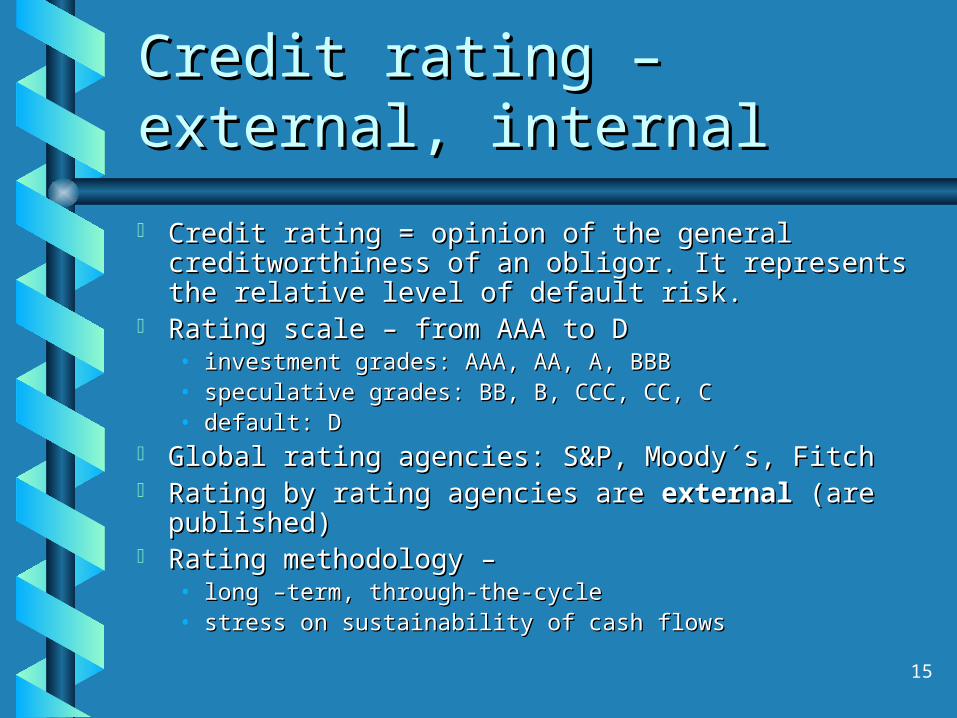

Credit rating = opinion of the general Credit rating = opinion of the general creditworthiness of an obligor. It represents the creditworthiness of an obligor. It represents the relative level of default risk.relative level of default risk.

Rating scale – from AAA to DRating scale – from AAA to D• investment grades: AAA, AA, A, BBBinvestment grades: AAA, AA, A, BBB• speculative grades: BB, B, CCC, CC, Cspeculative grades: BB, B, CCC, CC, C• default: Ddefault: D

Global rating agencies: SGlobal rating agencies: S&&P, Moody´s, FitchP, Moody´s, Fitch Rating by rating agencies are Rating by rating agencies are externalexternal (are (are

published) published) Rating methodology – Rating methodology –

• long –term, through-the-cyclelong –term, through-the-cycle• stress on sustainability of cash flowsstress on sustainability of cash flows

16

Credit rating – external, Credit rating – external, internalinternal

This is an ideal through-the-cycle rating:This is an ideal through-the-cycle rating:

17

Types of rating:Types of rating:• issue-specific X issuer ratingissue-specific X issuer rating• long-term X short-term ratinglong-term X short-term rating• international (foreign currency) X local ratinginternational (foreign currency) X local rating

Rating methodology usually includes the Rating methodology usually includes the assessment of:assessment of:• 1) Business risk1) Business risk

– Country risk– Industry characteristics– Company position– Product portfolio/Marketing– Technology– Cost efficiency– Strategic and operational management– competence– Profitability/Peer group comparisons

Credit rating – external, Credit rating – external, internalinternal

18

Credit rating – external, Credit rating – external, internalinternal

• 2) Financial risk2) Financial risk

– Accounting

– Corporate governance/Risk– tolerance/Financial policies– Cash-flow adequacy– Capital Structure/Asset Protection– Liquidity/Short-term factors

Ratings widely accepted by the financial Ratings widely accepted by the financial markets.markets.

Rating is an example of comprehensive Rating is an example of comprehensive assessment: financial factors (including ratio assessment: financial factors (including ratio analysis) must be completed by non-financial analysis) must be completed by non-financial factors + expert judgementfactors + expert judgement

19

Credit rating – external, Credit rating – external, internalinternal

Basic ratios used in rating methodology:Basic ratios used in rating methodology:• growth of EBITDAgrowth of EBITDA• growth of profit margingrowth of profit margin• debt ratiodebt ratio• interest coverage ratiointerest coverage ratio• liquidityliquidity

Interpretation of ratios is never straightforwardInterpretation of ratios is never straightforward „„Rating is as much art as it is a science.“Rating is as much art as it is a science.“

20

Credit rating – external, Credit rating – external, internalinternal

Internal ratingInternal rating systems – used for internal systems – used for internal purposes of financial institutionspurposes of financial institutions

similar basis as external rating by rating similar basis as external rating by rating agencies, but tailor-made for internal portfolio agencies, but tailor-made for internal portfolio and needsand needs

methodology based on model, completed by methodology based on model, completed by expert judgementexpert judgement

usage: credit approvals, limit setting, pricing, usage: credit approvals, limit setting, pricing, internal reporting, setting strategyinternal reporting, setting strategy

for homogenous portfolios (e.g. retail loans) – for homogenous portfolios (e.g. retail loans) – scoring systems (automatic assessment)scoring systems (automatic assessment)

21

Summary of the lectureSummary of the lecture

Financial statements are basic source of Financial statements are basic source of financial analysis which is based on financial financial analysis which is based on financial ratios.ratios.

Interpretation of ratios is not straigtforward, Interpretation of ratios is not straigtforward, for comprehensive view must be be completed for comprehensive view must be be completed by non-financial information and expert by non-financial information and expert judgement.judgement.

Financial analysis makes part of other Financial analysis makes part of other analyses – credit analysis, credit rating, default analyses – credit analysis, credit rating, default prediction – used by certain users for pre-prediction – used by certain users for pre-detrmined purposes.detrmined purposes.

22

Assignments for the Assignments for the tutorialtutorial

1.1. What are some important caveats to remember when What are some important caveats to remember when analyzing financial ratios?analyzing financial ratios?

2.2. For which business is inventory turnover important?For which business is inventory turnover important?• manufacturing (production) companymanufacturing (production) company• wholesalerwholesaler• retailerretailer• service sectorservice sector

3.3. How can a firm have a high current ratio and still be How can a firm have a high current ratio and still be unable to pay its bills? (Q 8.6.)unable to pay its bills? (Q 8.6.)

4.4. „„The higher the rates of return on assets, the better the The higher the rates of return on assets, the better the firm´s managament“. Is this true? (Q 8.7.)firm´s managament“. Is this true? (Q 8.7.)

5.5. What factors would you examine if a firm´s ROA was too What factors would you examine if a firm´s ROA was too low? (Q8.8)low? (Q8.8)

23

Assignments for the Assignments for the tutorialtutorial

6.6. Discover what is the current Fitch rating of the Czech Discover what is the current Fitch rating of the Czech Republic? What does this rating grade mean?Republic? What does this rating grade mean?

7.7. Calculate basic financial ratios for ČEZ company :Calculate basic financial ratios for ČEZ company :• current ratiocurrent ratio• debt ratiodebt ratio• cash flow coveragecash flow coverage• accounts receivable turnoveraccounts receivable turnover• ROAROA• ROEROE

Compare the results of the company in 2004 and 2005.Compare the results of the company in 2004 and 2005.

What do you think are the main economic factors influencing the What do you think are the main economic factors influencing the results of ČEZ?results of ČEZ?

Find out what is the current Long Term Issuer Default RatingFind out what is the current Long Term Issuer Default Rating of ČEZ?of ČEZ?

24

Assignments for the Assignments for the tutorialtutorial

8.8. Which banking client may be subject to scoring assessment?Which banking client may be subject to scoring assessment?

9.9. Look at the data on Wisconsin Furniture Company (see Look at the data on Wisconsin Furniture Company (see Problem 8.3, page 197 of the textbook) and indicate the Problem 8.3, page 197 of the textbook) and indicate the possible error in the management by calculating financial possible error in the management by calculating financial indicators.indicators.

How could the company improve its performance?How could the company improve its performance?