1 CHAPTER M7 The Capital Budget: Evaluating Capital Expenditures © 2007 Pearson Custom Publishing.

63

1 CHAPTER M7 CHAPTER M7 The Capital Budget: The Capital Budget: Evaluating Capital Evaluating Capital Expenditures Expenditures © 2007 Pearson Custom Publishing © 2007 Pearson Custom Publishing

-

Upload

cori-edwards -

Category

Documents

-

view

213 -

download

0

Transcript of 1 CHAPTER M7 The Capital Budget: Evaluating Capital Expenditures © 2007 Pearson Custom Publishing.

1

CHAPTER M7CHAPTER M7

The Capital Budget:The Capital Budget:

Evaluating Capital Evaluating Capital ExpendituresExpenditures

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

2

Learning Objective 1:Learning Objective 1:

Describe the overall Describe the overall business planning business planning process and where process and where

the capital budget fits the capital budget fits in that process.in that process.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

3

Capital InvestmentsCapital Investments

Acquisitions of significant long-term assets Acquisitions of significant long-term assets are called are called capital investments (or capital capital investments (or capital projects).projects).

Due to the large amount of money being Due to the large amount of money being spent and the relative importance of these spent and the relative importance of these expenditures, managers spend a great deal expenditures, managers spend a great deal of time evaluating the viable alternatives of time evaluating the viable alternatives available to them. available to them.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

4

Capital BudgetingCapital Budgeting The decision-making process that The decision-making process that

encompasses such expenditures is encompasses such expenditures is called called capital budgeting.capital budgeting.

Individuals practice their own form of Individuals practice their own form of capital budgeting when they decide to capital budgeting when they decide to buy a new car, house, or make some buy a new car, house, or make some other major purchaseother major purchase..

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

5

Business Planning Business Planning ProcessProcess

An organization needs to have a system ofAn organization needs to have a system of planning and controlplanning and control in order to achieve its in order to achieve its goals.goals.

Organization goalsOrganization goals represent the company’s represent the company’s long-term aspirations as determined by upper long-term aspirations as determined by upper management. Goal setting is management. Goal setting is THE WHYTHE WHY of the of the business.business.

WHY WHAT HOW WHO

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

6

Nonfinancial GoalsNonfinancial Goals

A company typically has many goals that A company typically has many goals that are not centered around money.are not centered around money.

The The nonfinancial goalsnonfinancial goals are often are often highlighted in a highlighted in a mission statementmission statement or a or a similar document.similar document.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

7

Financial GoalsFinancial Goals The main The main financial goalfinancial goal for most for most

businesses is to turn a profit. Business businesses is to turn a profit. Business owners have substantial amounts of owners have substantial amounts of capital at risk in most ventures, so they are capital at risk in most ventures, so they are concerned with earning an adequate concerned with earning an adequate return.return.

This might be stated as fulfilling earnings This might be stated as fulfilling earnings potential, building shareholder value, or potential, building shareholder value, or something similar.something similar.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

8

Mission StatementMission Statement The mission statement for The mission statement for

Procter&Gamble is quoted below:Procter&Gamble is quoted below:

PURPOSEWe will provide products of superior quality and value

that improve the lives of the world’s consumers.As a result, consumers will reward us with leadership

sales and profit growth, allowing our people, ourshareholders, and the communities in which we live

and work to prosper.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

9

Strategic PlanStrategic Plan After goals have been set, a After goals have been set, a strategic planstrategic plan

or long-range budget need to be set.or long-range budget need to be set. This plan will identify those actions that the This plan will identify those actions that the

firm will take to achieve its goals. It is firm will take to achieve its goals. It is important that these plans support, rather important that these plans support, rather than conflict with, the company’s goals.than conflict with, the company’s goals.

This is This is THE WHATTHE WHAT of doing business. of doing business.

WHY WHAT HOW WHO

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

10

Preparing the Capital Preparing the Capital BudgetBudget

The The capital budgetcapital budget identifies scarce resource identifies scarce resource allocations over the next several years. A allocations over the next several years. A budget period of five years, ten years, or even budget period of five years, ten years, or even longer is not unusual.longer is not unusual.

This is This is THE HOWTHE HOW of the business. of the business. The capital budget focuses on acquiring and The capital budget focuses on acquiring and

replacing the significant long-lived assets.replacing the significant long-lived assets.

WHY WHAT HOW WHO © 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

11

The Operating BudgetThe Operating Budget The day-to-day operations of the company The day-to-day operations of the company

also must be planned for and budgeted.also must be planned for and budgeted. An An operating budgetoperating budget is used for this type of is used for this type of

short-term planning, usually one year at a short-term planning, usually one year at a time, but possibly for more than one year.time, but possibly for more than one year.

The operating budget is The operating budget is THE WHOTHE WHO of the of the business.business.

WHY WHAT HOW WHO © 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

12

Planning Planning InterrelationshipsInterrelationships

Goals

WHY

StrategicPlan

WHAT

CapitalBudget

HOW

OperatingBudget

WHO

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

13

Learning Objective 2:Learning Objective 2:

Explain the process of Explain the process of capital budgeting.capital budgeting.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

14

Capital AssetsCapital Assets Long-lived assets are commonly referred Long-lived assets are commonly referred

to as to as capital assets.capital assets. Whenever an Whenever an expenditure is made to purchase expenditure is made to purchase something, the cost of that item will either something, the cost of that item will either be shown as an expense or as an asset.be shown as an expense or as an asset.

CapitalizingCapitalizing the expenditure is the the expenditure is the process of recording the expenditure as an process of recording the expenditure as an asset rather than an expense.asset rather than an expense.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

15

Capitalization ThresholdCapitalization Threshold Not all long-lived assets will be capitalized. Not all long-lived assets will be capitalized.

This is essentially an application of the This is essentially an application of the materiality principle in accounting.materiality principle in accounting.

For very large companies, an asset may For very large companies, an asset may have to cost $5,000 or more before it will have to cost $5,000 or more before it will be capitalized. Smaller companies would be capitalized. Smaller companies would have a significantly lower threshold, have a significantly lower threshold, maybe something in the vicinity of $500.maybe something in the vicinity of $500.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

16

Learning Objective 3:Learning Objective 3:

Discuss the four Discuss the four shared characteristics shared characteristics of all capital projects.of all capital projects.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

17

Characteristics of Characteristics of Capital ProjectsCapital Projects

Long Lives: Capital projects are more than Long Lives: Capital projects are more than one year in length. For example, a new office one year in length. For example, a new office building may have an expected useful life of building may have an expected useful life of fifty years or more.fifty years or more.

High Cost: The cost needs to be high enough High Cost: The cost needs to be high enough to exceed the company’s threshold for to exceed the company’s threshold for capitalization. Long-lived items with a small capitalization. Long-lived items with a small cost will be expensed immediately.cost will be expensed immediately.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

18

Characteristics of Characteristics of Capital ProjectsCapital Projects

Quickly Sunk Costs: Expenditures involved in Quickly Sunk Costs: Expenditures involved in capital projects typically become capital projects typically become sunk costssunk costs at an early stage. Sunk costs are costs that at an early stage. Sunk costs are costs that cannot be recovered.cannot be recovered.

High Degree of Risk: Due to the High Degree of Risk: Due to the uncertainty in the long-range planning uncertainty in the long-range planning process, capital projects are inherently risky.process, capital projects are inherently risky.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

19

Learning Objective 4:Learning Objective 4:

Describe the cost of Describe the cost of capital and the capital and the

concept of scarce concept of scarce resources.resources.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

20

Cost of CapitalCost of Capital A business cannot raise funds without A business cannot raise funds without

incurring a cost. The incurring a cost. The cost ofcost of capitalcapital represents a firm’s cost of acquiring debt or represents a firm’s cost of acquiring debt or equity financing.equity financing.

The cost of capital is often used as a The cost of capital is often used as a minimum desired rate of return on projects.minimum desired rate of return on projects.

Also called the Also called the cost of capital rate, cost of capital rate, required rate of return,required rate of return, or theor the hurdle rate.hurdle rate.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

21

Blended Cost of Blended Cost of CapitalCapital

Many companies rely on Many companies rely on financing from both debt and financing from both debt and equity sources.equity sources.

Combining the cost of debt Combining the cost of debt financing with the cost of financing with the cost of equity financing is called the equity financing is called the blended cost of capital.blended cost of capital.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

22

Cost of Debt CapitalCost of Debt Capital

The The cost of debt capitalcost of debt capital is basically equal is basically equal to the effective interest rate on the long-to the effective interest rate on the long-term debt. The debt is typically in the form term debt. The debt is typically in the form of either notes payable or bonds payable.of either notes payable or bonds payable.

If a company issues bonds, there is a cost If a company issues bonds, there is a cost involved in making the bond issuance, and involved in making the bond issuance, and this cost should also be included when this cost should also be included when determining the cost of debt capital.determining the cost of debt capital.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

23

Cost of Equity CapitalCost of Equity Capital The The cost of equity capitalcost of equity capital can be a rather can be a rather

complicated concept. There is a cost of complicated concept. There is a cost of issuing the equity securities, but most of the issuing the equity securities, but most of the cost is related to the rate of return on the cost is related to the rate of return on the securities for the investor.securities for the investor.

Dividends paid are included in the cost of Dividends paid are included in the cost of capital, as is the investors’ expected amount capital, as is the investors’ expected amount of appreciation in the stock value.of appreciation in the stock value.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

24

Example of Blended Example of Blended Cost of CapitalCost of Capital

The following example illustrates the The following example illustrates the calculation of the blended cost of capital:calculation of the blended cost of capital:

FinancingFinancing % of Total% of Total Cost RateCost Rate WeightedWeighted Debt Debt 30%30% X X 9% 9% = 2.7% = 2.7% Equity Equity 70%70% X X 18%18% = = 12.6%12.6%

Weighted cost of capital = 15.3% Weighted cost of capital = 15.3%

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

25

Scarce ResourcesScarce Resources

If you have ever had the desire to spend If you have ever had the desire to spend or invest more money that you have or invest more money that you have available, then you understand the available, then you understand the concept of scarce resources.concept of scarce resources.

A very important management job is to A very important management job is to properly allocate the scarce resources that properly allocate the scarce resources that the company has available to them.the company has available to them.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

26

Learning Objective 5 :Learning Objective 5 :

Determine the Determine the information relevant information relevant

to the capital to the capital budgeting decision.budgeting decision.© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

27

Evaluating Potential Evaluating Potential ProjectsProjects

Managers will evaluate capital projects by:Managers will evaluate capital projects by: Identifying possible capital projects.Identifying possible capital projects. Determining the relevant cash flows for the Determining the relevant cash flows for the

alternative projects.alternative projects. Selecting a method of evaluating the projects.Selecting a method of evaluating the projects. Evaluating the projects and selecting one or Evaluating the projects and selecting one or

more of the acceptable alternatives.more of the acceptable alternatives.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

28

Identifying Possible Identifying Possible ProjectsProjects

A potential capital project is one that has the A potential capital project is one that has the possibility of increasing revenues, decreasing possibility of increasing revenues, decreasing expenses, or some combination of both. In expenses, or some combination of both. In other words, a capital project should have a other words, a capital project should have a positive impact on profits.positive impact on profits.

Occasionally, a project is considered that will Occasionally, a project is considered that will have a negative impact on profits. Some have a negative impact on profits. Some projects may even be forced upon the projects may even be forced upon the company.company.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

29

Evaluation MethodsEvaluation Methods We will consider three different methods for We will consider three different methods for

evaluating capital projects:evaluating capital projects: Net Present ValueNet Present Value Internal Rate of ReturnInternal Rate of Return Payback PeriodPayback Period

These three methods will often produce These three methods will often produce conflicting results regarding acceptability of conflicting results regarding acceptability of the capital projects under consideration.the capital projects under consideration.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

30

Selecting Capital ProjectsSelecting Capital Projects The first step in selecting a capital The first step in selecting a capital

budgeting project is to determine which budgeting project is to determine which projects are acceptable and which are not. projects are acceptable and which are not. This step is often called This step is often called screening.screening.

The next step would be to rank the The next step would be to rank the acceptable alternatives according to some acceptable alternatives according to some criteria. Typically, the first choice would be criteria. Typically, the first choice would be the project with the highest ranking.the project with the highest ranking.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

31

Discounted Cash FlowsDiscounted Cash Flows Since these projects are long term in nature, Since these projects are long term in nature,

it is wise to consider the time value of money it is wise to consider the time value of money in the capital budgeting analysis.in the capital budgeting analysis.

Determining the present value of future cash Determining the present value of future cash flows is called flows is called discounting cash flows.discounting cash flows.

The discounted cash flows methods are:The discounted cash flows methods are: Net present valueNet present value Internal rate of returnInternal rate of return

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

32

Net Present ValueNet Present Value

The The net present value (NPV)net present value (NPV) of a capital of a capital project is calculated by subtracting the project is calculated by subtracting the present value of future cash outflows from present value of future cash outflows from the present value of future cash inflows.the present value of future cash inflows.

The future cash flows will be discounted to The future cash flows will be discounted to present value using the firm’s blended cost present value using the firm’s blended cost of capital (unless the project will be funded of capital (unless the project will be funded solely by debt or by equity).solely by debt or by equity).

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

33

Net Present ValueNet Present Value Generally speaking, any project that has a Generally speaking, any project that has a

positive or net present value will be positive or net present value will be considered to be an acceptable project.considered to be an acceptable project.

Even with an NPV of zero, the project is Even with an NPV of zero, the project is earning the company’s cost of capital. If the earning the company’s cost of capital. If the company wants to ensure that they will earn company wants to ensure that they will earn more than the cost of capital, then the cash more than the cost of capital, then the cash flows should be discounted at a higher rate.flows should be discounted at a higher rate.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

34

Learning Objective 6 :Learning Objective 6 :

Evaluate potential Evaluate potential capital investments capital investments using three capital using three capital budgeting decision budgeting decision

models.models.© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

35

CautionCaution When we analyze capital projects, the When we analyze capital projects, the

capital budgeting project analyses give capital budgeting project analyses give analysts analysts quantitativequantitative financial information financial information to help them make decisions. This is only to help them make decisions. This is only part of the decision.part of the decision.

QualitativeQualitative issues weigh heavily on the issues weigh heavily on the final determination of which projects will be final determination of which projects will be funded. funded.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

36

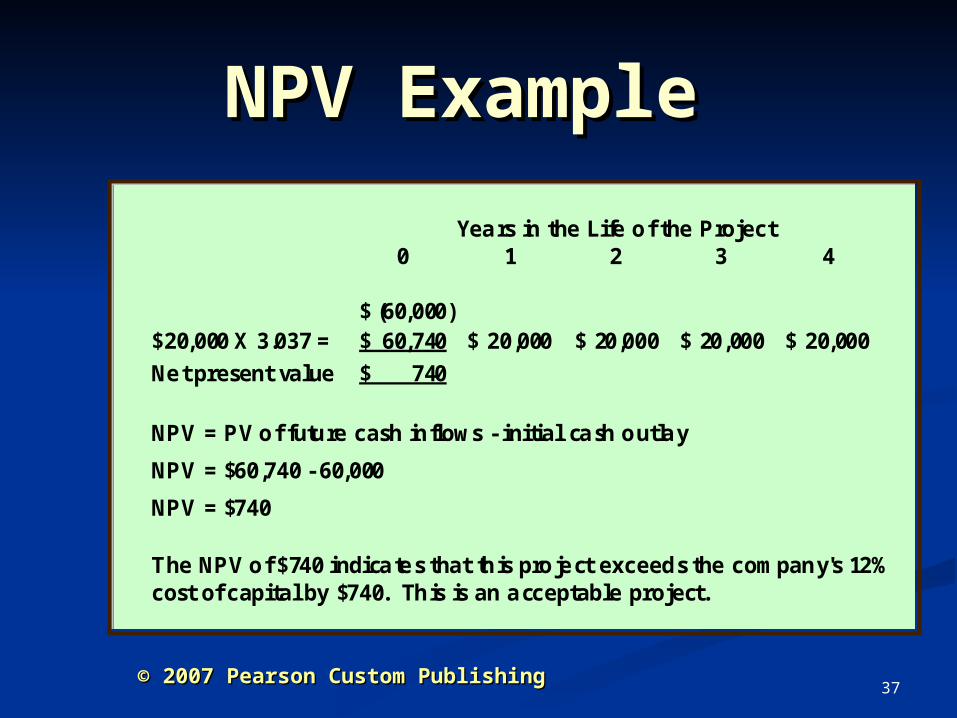

NPV ExampleNPV Example Assume that the ASU Company is Assume that the ASU Company is

considering a capital outlay of $60,000. considering a capital outlay of $60,000. This project should result in net cash This project should result in net cash inflows of $20,000 per year for the next inflows of $20,000 per year for the next four years.four years.

ASU has a blended cost of capital equal to ASU has a blended cost of capital equal to 12%. We will discount the future cash 12%. We will discount the future cash flows at the 12% discount rate.flows at the 12% discount rate.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

37

NPV ExampleNPV Example

Years in the Life of the Project0 1 2 3 4

(60,000)$ $20,000 X 3.037 = 60,740$ 20,000$ 20,000$ 20,000$ 20,000$

Ne t present value 740$

NPV = PV of future cash inflows - initial cash outlay

NPV = $60,740 - 60,000

NPV = $740

The NPV of $740 indica tes that this project exceeds the company's 12% cost of capital by $740. This is an acceptable project.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

38

Extended NPV Extended NPV ExampleExample

Most capital projects don’t have equal Most capital projects don’t have equal cash inflows as illustrated in the previous cash inflows as illustrated in the previous example.example.

ASU expects to generate only $15,000 in ASU expects to generate only $15,000 in year one, with the cash inflow increasing year one, with the cash inflow increasing by $5,000 in each of the succeeding three by $5,000 in each of the succeeding three years. Now the uneven cash flows must years. Now the uneven cash flows must be separately discounted.be separately discounted.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

39

Extended NPV Extended NPV ExampleExample

Years in the Life of the Project0 1 2 3 4

Initial investment (60,000)$ Annual cash inflow 15,000$ 20,000$ 25,000$ 30,000$ Present values:

$15,000 X .893 = 13,395$ $20,000 X .797 = 15,940 $25,000 X .712 = 17,800 $30,000 X .636 = 19,080

6,215$

The NPV of $6,215 indicates tha t this project exceeds the company's 12% cost of capital by $6,215. This is an acceptable project.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

40

Profitability IndexProfitability Index Using NPV to compare different Using NPV to compare different

projects is appropriate if the projects projects is appropriate if the projects require equal or similar amounts of require equal or similar amounts of initial investment.initial investment.

However, if the initial investments are However, if the initial investments are not comparable, then the NPVs should not comparable, then the NPVs should be used to calculate the be used to calculate the profitability profitability index (PI)index (PI) for each project. for each project.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

41

Profitability Index Profitability Index ExampleExample

Project #1 has future cash inflows with a Project #1 has future cash inflows with a present value of $110,500 and an initial present value of $110,500 and an initial investment of $100,000. Thus, the NPV is investment of $100,000. Thus, the NPV is $10,500 on project #1.$10,500 on project #1.

Project #2 has future cash inflows with a Project #2 has future cash inflows with a present value of $79,000 and an initial present value of $79,000 and an initial investment of $70,000. Thus, the NPV is investment of $70,000. Thus, the NPV is $9,000 on project #2.$9,000 on project #2.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

42

Profitability Index Profitability Index ExampleExample

Project #1 appears to be the best investment Project #1 appears to be the best investment because it has a higher NPV. However, the because it has a higher NPV. However, the PI for each project should be calculated PI for each project should be calculated since the investments required are unequal.since the investments required are unequal.

PI #1 = $110,500 / $100,000 = 1.105PI #1 = $110,500 / $100,000 = 1.105 PI #2 = $ 79,000 / $ 70,000 = 1.129PI #2 = $ 79,000 / $ 70,000 = 1.129 Using this measure, #2 is the project which Using this measure, #2 is the project which

offers the highest rate of return.offers the highest rate of return.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

43

Internal Rate of Internal Rate of ReturnReturn

The NPV method provides a dollar The NPV method provides a dollar answer, but it is impossible to tell what answer, but it is impossible to tell what the percentage rate of return is on the the percentage rate of return is on the project.project.

The The internal rate of return (IRR)internal rate of return (IRR) is is the expected percentage return the expected percentage return promised by a capital project. It is also promised by a capital project. It is also called the called the real rate of returnreal rate of return or the or the time-adjusted rate of return.time-adjusted rate of return.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

44

IRR ExampleIRR Example

BYU Company is considering two alternative BYU Company is considering two alternative projects. projects. Project A1 requires an initial investment of Project A1 requires an initial investment of

$50,000 and has expected annual cash inflows $50,000 and has expected annual cash inflows of $15,750 for four years.of $15,750 for four years.

Project B2 requires an initial investment of Project B2 requires an initial investment of $75,000 and has expected annual cash inflows $75,000 and has expected annual cash inflows of $25,750 for four years.of $25,750 for four years.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

45

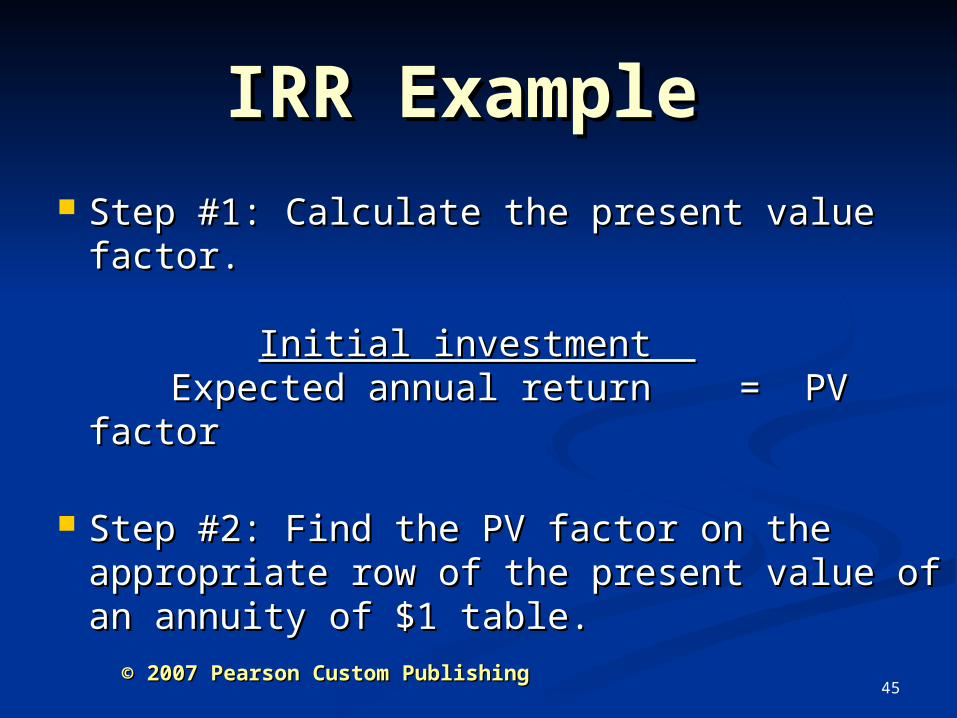

IRR ExampleIRR Example

Step #1: Calculate the present value factor.Step #1: Calculate the present value factor.

Initial investment Initial investment Expected annual return = PV factorExpected annual return = PV factor

Step #2: Find the PV factor on the Step #2: Find the PV factor on the appropriate row of the present value of an appropriate row of the present value of an annuity of $1 table.annuity of $1 table.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

46

IRR ExampleIRR Example Project A1: $50,000

$15,750 = 3.175For 4 years, the factor 3.175 is very close to the factor for the 10% rate of return.

Project B2: $75,000$25,750 = 2.913

For 4 years, the factor 2.913 is very close to the factor for the 14% rate of return.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

47

Comparing NPV Comparing NPV and IRRand IRR

If a capital project has a positive NPV, then If a capital project has a positive NPV, then the IRR will be above the company’s the IRR will be above the company’s required rate of return.required rate of return.

If a capital project has a negative NPV, then If a capital project has a negative NPV, then the IRR will be below the company’s required the IRR will be below the company’s required rate of return.rate of return.

If a capital project has an NPV of zero, then If a capital project has an NPV of zero, then the IRR equals the required rate of return.the IRR equals the required rate of return.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

48

Non-Discounted Cash Non-Discounted Cash Flow MethodFlow Method

Discounted cash flow methods are generally Discounted cash flow methods are generally considered to be the preferable methods for considered to be the preferable methods for capital budgeting. However, one capital budgeting. However, one non-non-discounted cash flow methoddiscounted cash flow method is also used. is also used.

A non-discounted cash flow method does not A non-discounted cash flow method does not factor the time value of money into the factor the time value of money into the analysis. analysis.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

49

Payback Period MethodPayback Period Method

The The payback period methodpayback period method is a measure is a measure of the time that will pass before a capital of the time that will pass before a capital project will have generated cash inflows project will have generated cash inflows equal to the amount of cash outflows.equal to the amount of cash outflows.

Since the major cash outflow is typically the Since the major cash outflow is typically the initial investment in the project, the payback initial investment in the project, the payback period is calculated by dividing the initial period is calculated by dividing the initial investment by the annual cash inflow.investment by the annual cash inflow.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

50

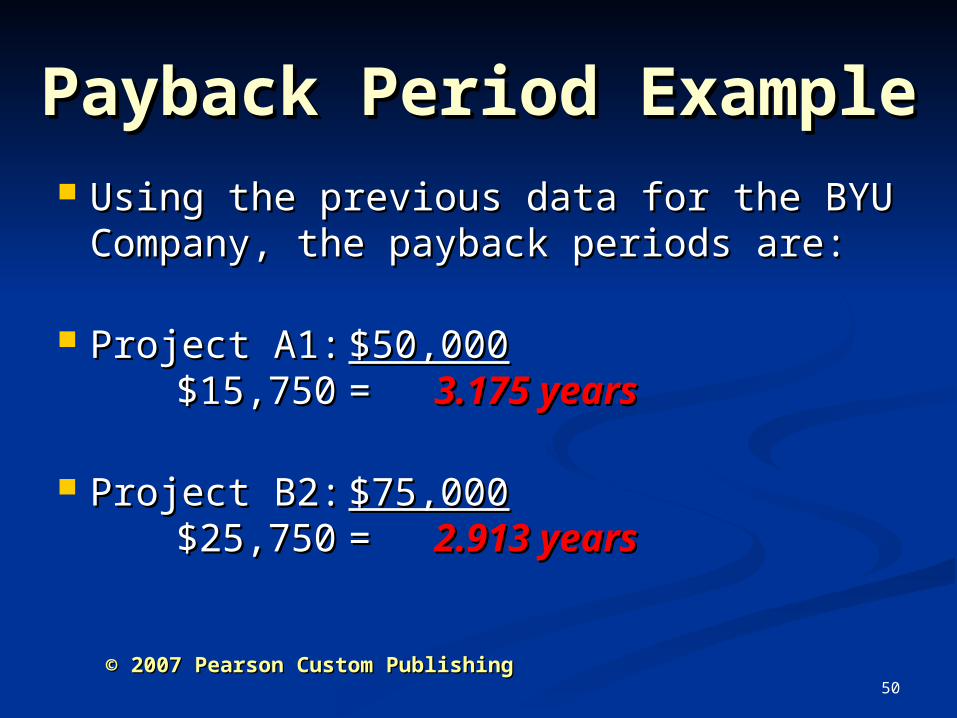

Payback Period ExamplePayback Period Example Using the previous data for the BYU Using the previous data for the BYU

Company, the payback periods are:Company, the payback periods are:

Project A1:Project A1: $50,000$50,000$15,750$15,750 == 3.175 years3.175 years

Project B2:Project B2: $75,000$75,000$25,750$25,750 == 2.913 years2.913 years

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

51

Factors Leading to Poor Factors Leading to Poor Capital Project SelectionCapital Project Selection Due to the Due to the natural optimismnatural optimism that managers that managers

often possess, they tend to overestimate often possess, they tend to overestimate future cash inflows and underestimate future future cash inflows and underestimate future cash outflows.cash outflows.

Some managers play Some managers play capital budgeting capital budgeting gamesgames by manipulating the numbers to put a by manipulating the numbers to put a more favorable light on the projects that have more favorable light on the projects that have been proposed.been proposed.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

52

Learning Objective 7 :Learning Objective 7 :

Determine present and Determine present and future values using future values using present value and present value and

future value tables.future value tables.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

53

Appendix: Time Value Appendix: Time Value of Moneyof Money

If you have a dollar in hand today, you can If you have a dollar in hand today, you can invest it and earn a return on it in the future. invest it and earn a return on it in the future. This is the concept of interest and is the basis This is the concept of interest and is the basis for the for the time value of money.time value of money.

To properly understand the time value of To properly understand the time value of money, you first must be able to distinguish money, you first must be able to distinguish between between simple interestsimple interest and and compound compound interest.interest.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

54

Interest ExampleInterest Example

You go to the bank and negotiate a five-year loan. You go to the bank and negotiate a five-year loan. They will loan you $5,000 at 10% annual interest. They will loan you $5,000 at 10% annual interest. Principal plus interest is due at the end of the term Principal plus interest is due at the end of the term (five years from now).(five years from now).

Your parents agree to match the offer from the Your parents agree to match the offer from the bank. You will choose between the bank loan and bank. You will choose between the bank loan and the family loan. The only difference is that the bank the family loan. The only difference is that the bank charges compound interest and your parents charges compound interest and your parents charge simple interest.charge simple interest.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

55

Compound Interest Compound Interest on a Loanon a Loan

The following schedule shows how much The following schedule shows how much interest will accrue on the bank loan, and interest will accrue on the bank loan, and the final payoff amount in five years.the final payoff amount in five years.

Bank Loan with 10% Compound Interest

Year 1 Year 2 Year 3 Year 4 Year 5Loan balance 5,000 5,500 6,050 6,655 7,321Interest 500 550 605 666 732Total due 5,500 6,050 6,655 7,321 8,053

Total due to repay loan

Interest each year equals loan balance times 10%.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

56

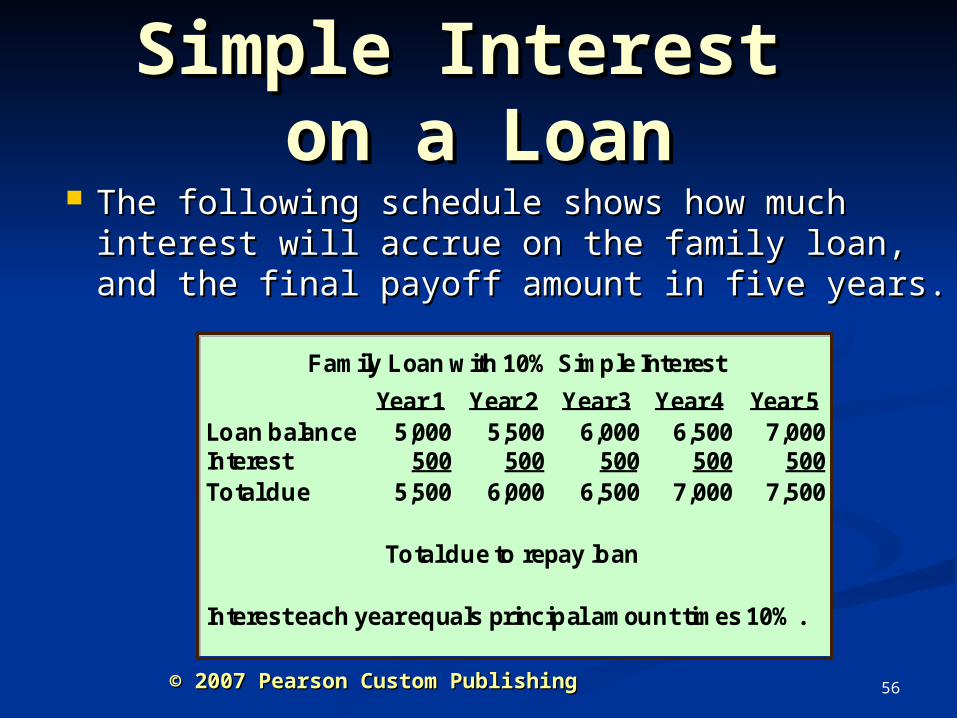

Family Loan with 10% Simple Interest

Year 1 Year 2 Year 3 Year 4 Year 5Loan balance 5,000 5,500 6,000 6,500 7,000Interest 500 500 500 500 500Total due 5,500 6,000 6,500 7,000 7,500

Total due to repay loan

Interest each year equals principal amount times 10% .

Simple Interest Simple Interest on a Loanon a Loan

The following schedule shows how much The following schedule shows how much interest will accrue on the family loan, and the interest will accrue on the family loan, and the final payoff amount in five years.final payoff amount in five years.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

57

Future ValueFuture Value

In each of the previous examples, the payoff In each of the previous examples, the payoff amount at the end of five years could be amount at the end of five years could be called the called the future valuefuture value of the loan. of the loan.

In all of the business examples, we will In all of the business examples, we will assume that interest is compounded unless assume that interest is compounded unless specifically told otherwise. Additionally, the specifically told otherwise. Additionally, the four time-value tables that are provided are four time-value tables that are provided are all based on compound interest.all based on compound interest.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

58

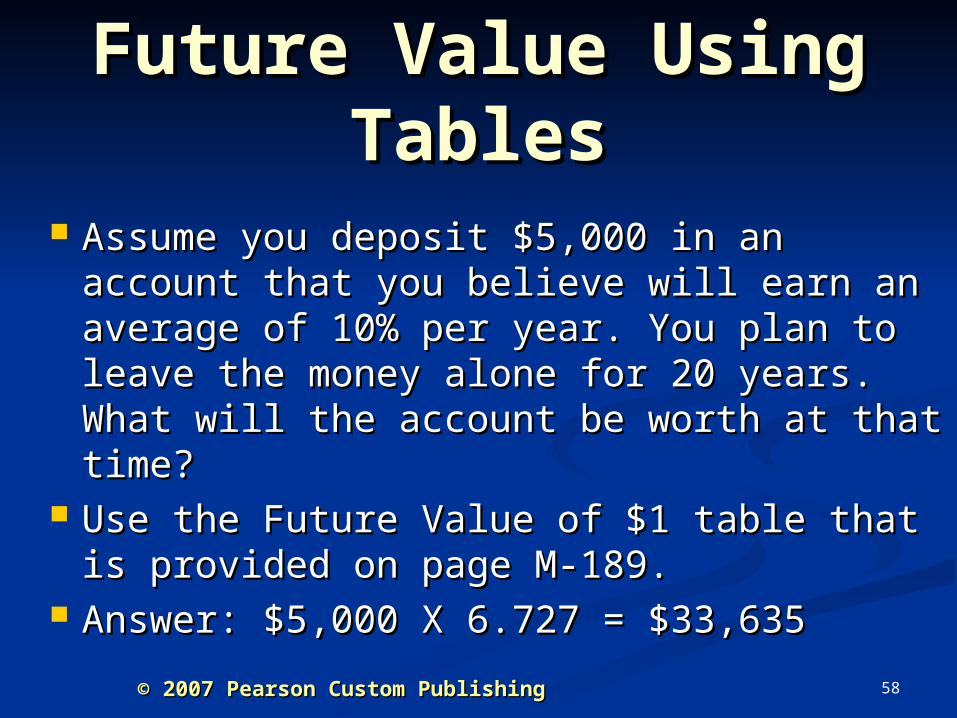

Future Value Using Future Value Using TablesTables

Assume you deposit $5,000 in an account Assume you deposit $5,000 in an account that you believe will earn an average of 10% that you believe will earn an average of 10% per year. You plan to leave the money alone per year. You plan to leave the money alone for 20 years. What will the account be worth for 20 years. What will the account be worth at that time?at that time?

Use the Future Value of $1 table that is Use the Future Value of $1 table that is provided on page M-189.provided on page M-189.

Answer: $5,000 X 6.727 = $33,635Answer: $5,000 X 6.727 = $33,635

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

59

Future Value of an Future Value of an AnnuityAnnuity

AnAn annuityannuity is a series of equal cash is a series of equal cash payments. Assume that instead of investing payments. Assume that instead of investing $5,000 all at once, you decide to deposit $5,000 all at once, you decide to deposit $500 per year for 20 years into the account.$500 per year for 20 years into the account.

Use the table on page M-190. At a 10% Use the table on page M-190. At a 10% return, what is the account worth after 20 return, what is the account worth after 20 years?years?

Answer: $500 X 57.275 = $28,637.50Answer: $500 X 57.275 = $28,637.50

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

60

Present ValuePresent Value Using the same investment account, assume Using the same investment account, assume

that you want a total equal to $50,000 at the that you want a total equal to $50,000 at the end of the 20th year. How much would you end of the 20th year. How much would you have to deposit in the account right now?have to deposit in the account right now?

This is a This is a present valuepresent value problem. You need problem. You need to discount $50,000 to be received 20 years to discount $50,000 to be received 20 years from now, to its current value, at a 10% from now, to its current value, at a 10% annual rate.annual rate.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

61

Present ValuePresent Value

To solve this problem, use the table on To solve this problem, use the table on page M-191. The factor for 20 years at page M-191. The factor for 20 years at 10% interest is 0.149. In other words, if 10% interest is 0.149. In other words, if you multiply the desired future amount by you multiply the desired future amount by 14.9%, you will see the size of deposit 14.9%, you will see the size of deposit required now.required now.

Answer = $50,000 X 0.149 = $7,450Answer = $50,000 X 0.149 = $7,450

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

62

Present Value of Present Value of an Annuityan Annuity

As a final example, assume that you will As a final example, assume that you will want to withdraw $2,500 per year from the want to withdraw $2,500 per year from the account for 20 years. How much should account for 20 years. How much should you deposit into the account?you deposit into the account?

Use the present value of an annuity table Use the present value of an annuity table on page M-193.on page M-193.

Answer: $2,500 X 8.514 = $21,285Answer: $2,500 X 8.514 = $21,285

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

63

End of Chapter M7End of Chapter M7

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing