1 Chapter 12 – The Financing Mix Key Sections: Business and Financial Risk Operating, financial...

21

1 Chapter 12 – The Financing Mix • Key Sections: • Business and Financial Risk • Operating, financial and combined leverage • Capital structure and financial structure • Saucer-shaped cost of capital curve • Management practices

-

date post

21-Dec-2015 -

Category

Documents

-

view

217 -

download

2

Transcript of 1 Chapter 12 – The Financing Mix Key Sections: Business and Financial Risk Operating, financial...

1

Chapter 12 – The Financing Mix

• Key Sections:

• Business and Financial Risk

• Operating, financial and combined leverage

• Capital structure and financial structure

• Saucer-shaped cost of capital curve

• Management practices

2

Risk

• Variability in revenue or income streams• Business risk affects EBIT

– Results from investment decisions (cost structure, competition, price elasticity, etc)

• Financial risk – use of fixed rate financing sources

• Variation in net income is due to both business and financial risk

3

Sources of Risk

• Risk results from the presence of fixed costs– Fixed operating and financing costs– If present, what happens to EBIT and EPS if

sales change?– EBIT will change more than sales change with

fixed operating costs– Changes in EPS will be even greater than the

change in EBIT if fixed-rate financing used

4

Breakeven Analysis

• Find amount of sales to produce EBIT of zero– Variable or direct costs vary as output

changes but are fixed per unit – Example: raw material costs

• Fixed costs do not vary as sales change– Example: depreciation

• Semi variable (over a range of output)

5

Contribution Margin

Per unit sales price $12

Variable cost per unit -7

Unit contribution margin 5

• Unit sales price less unit variable cost equals contribution margin (left over to cover fixed costs)

6

Percentage Change

• Percentage change = New Value less Old

Old Value

• Increase from 100 to 200 = 100% increase(200 – 100) / 100 = 100%

• Decrease from 200 to 100 = 50% decrease(100 - 200) / 200 = -.5 = -50%

7

Leverage

• In finance – presence of fixed operating costs and/or fixed financing costs cause sale changes to have a magnified impact on EBIT and EPS

• Degree of Operating Leverage (DOL) =• % change in EBIT divided by sales

change– Pierce +120% in EBIT/ +20% sales = 6 times

8

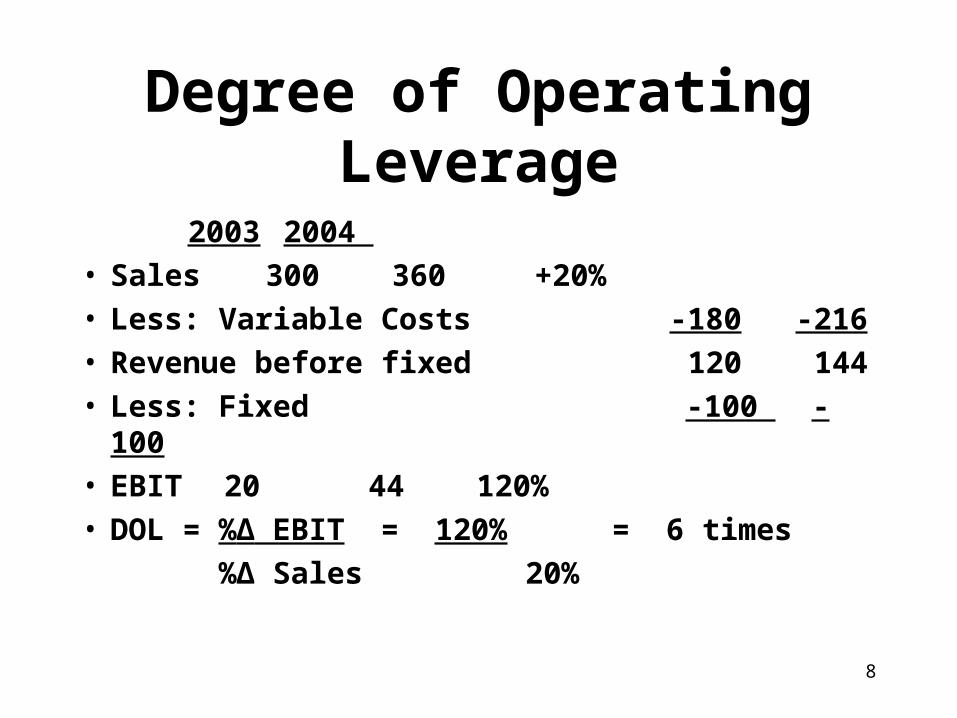

Degree of Operating Leverage

2003 2004 • Sales 300 360 +20%• Less: Variable Costs -180 -216• Revenue before fixed 120 144• Less: Fixed -100 -100• EBIT 20 44 120%• DOL = %Δ EBIT = 120% = 6 times

%Δ Sales 20%

9

Implications of DOL

• With DOL of 6 times, if sales increase 20%, EBIT will change by 120% (because the fixed costs don’t change)

• If sales fall 20% EBIT will decline 120% resulting in a $4,000 operating loss

• DOL falls as sales increase because fixed costs are spread over more units

10

Financial Leverage

• Financing a portion of the assets with fixed-rate financing (bonds, preferred stock)

• Degree of Financial Leverage = % change in EPS/ % change in EBIT, say 1.25 times

• Shows responsiveness of EPS to changes in EBIT

• Can have positive or negative effects but with greater leverage, greater changes occur

11

Degree of Financial Leverage DFL

2003 2004

EBIT 20 44 +120%

Less: Interest -4 -4

Before tax 16 40

Tax @ 50% -8 -20

Net Income 8 20 +150%

DFL = %Δ Net Inc = 150% = 1.25 times

%Δ EBIT 120%

12

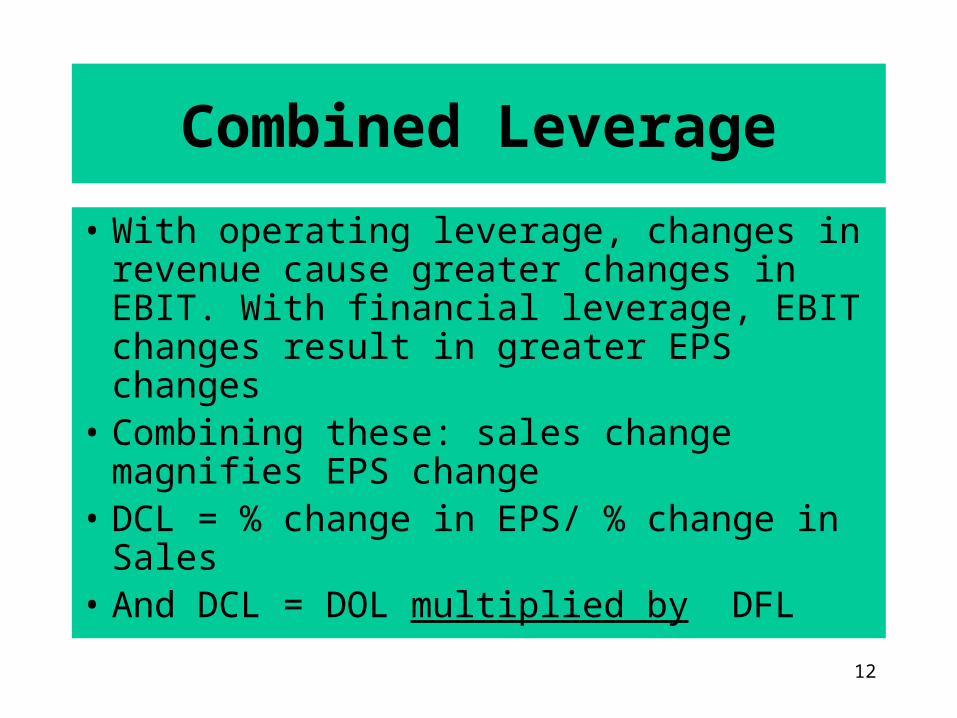

Combined Leverage

• With operating leverage, changes in revenue cause greater changes in EBIT. With financial leverage, EBIT changes result in greater EPS changes

• Combining these: sales change magnifies EPS change

• DCL = % change in EPS/ % change in Sales• And DCL = DOL multiplied by DFL

13

Combined Leverage

2003 2004

Sales 300 360 +20%

Net Income 8 20 +150%

DCL = %Δ Net Inc. = 150% = 7.50 times

%Δ Sales 20

Also = DOL * DFL = 6 X * 1.25X = 7.50 X

14

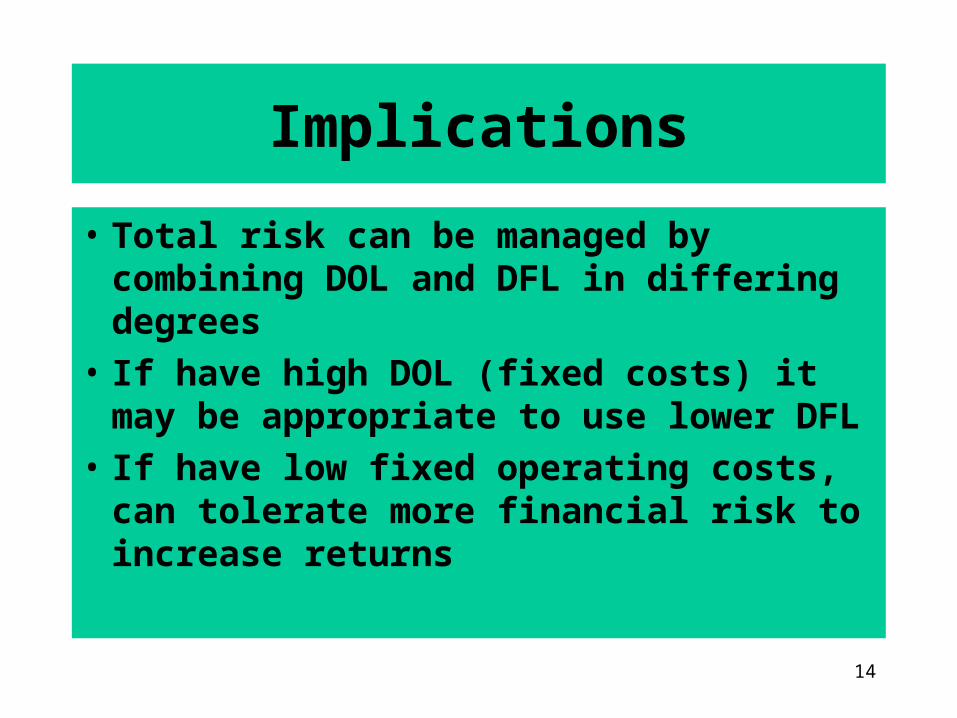

Implications

• Total risk can be managed by combining DOL and DFL in differing degrees

• If have high DOL (fixed costs) it may be appropriate to use lower DFL

• If have low fixed operating costs, can tolerate more financial risk to increase returns

15

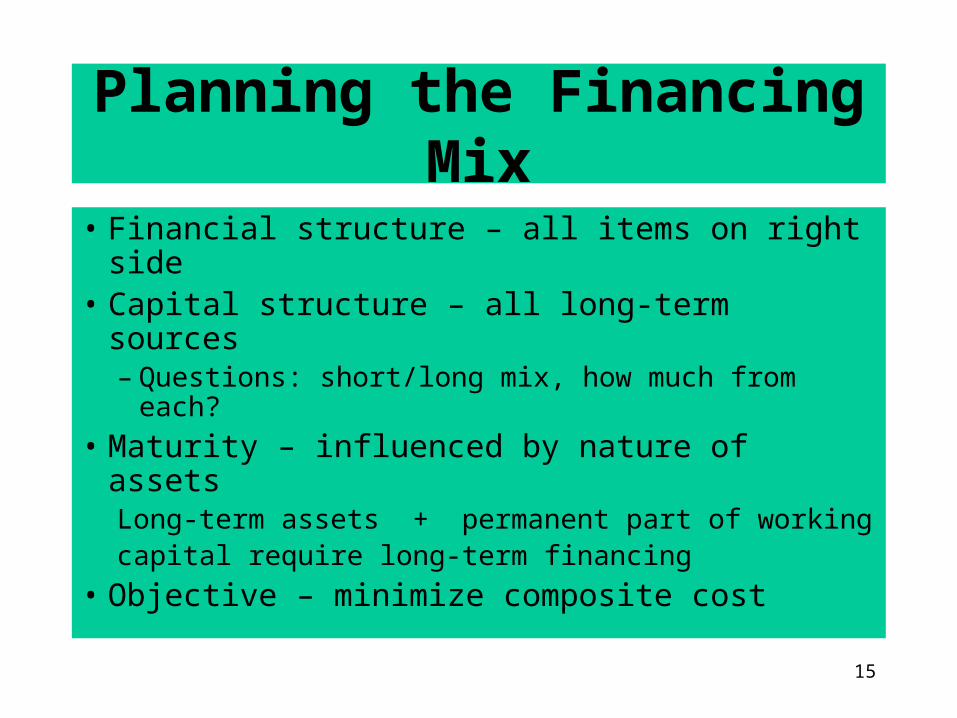

Planning the Financing Mix

• Financial structure – all items on right side• Capital structure – all long-term sources

– Questions: short/long mix, how much from each?

• Maturity – influenced by nature of assetsLong-term assets + permanent part of workingcapital require long-term financing

• Objective – minimize composite cost

16

Capital Structure Theory

• Can we affect cost by changing mix?

• Independence (Modigliani) – “no”– But assumptions may be unrealistic

• Moderate view – more realistic– Considers taxes and bankruptcy risk

• Debt encouraged by tax shield – Causes C of C to fall but only to a point

17

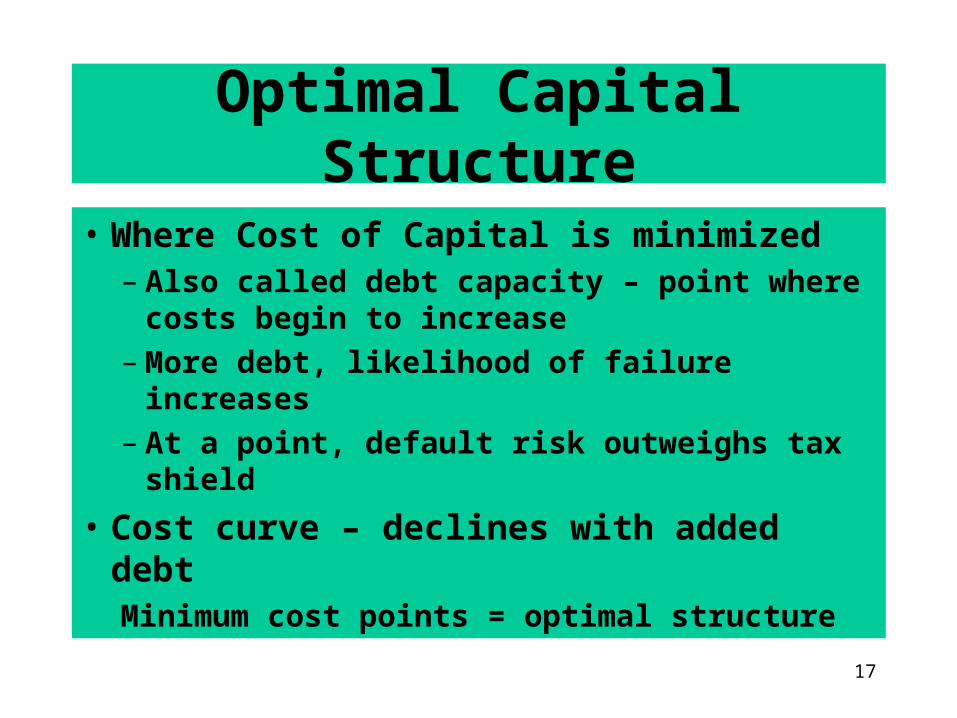

Optimal Capital Structure

• Where Cost of Capital is minimized– Also called debt capacity – point where costs

begin to increase– More debt, likelihood of failure increases– At a point, default risk outweighs tax shield

• Cost curve – declines with added debtMinimum cost points = optimal structure

18

Cost of Capital

0

2

4

6

8

10

12

14

100 90 80 70 60 50 40 30 20

Percent Financed by Equity

Co

st -

%

Optimal Range(Debt Capacity)

60 to 70% Equity

19

Saucer-Shaped Curve (Moderate)

• Before bankruptcy costs become detrimental, the tax shield causes share price to increase/ cost of capital to fall

• Need to find the optimal range of leverage

• Use caution in using fixed-charge capital, especially if there is operating leverage.

20

Summary of Financial Leverage

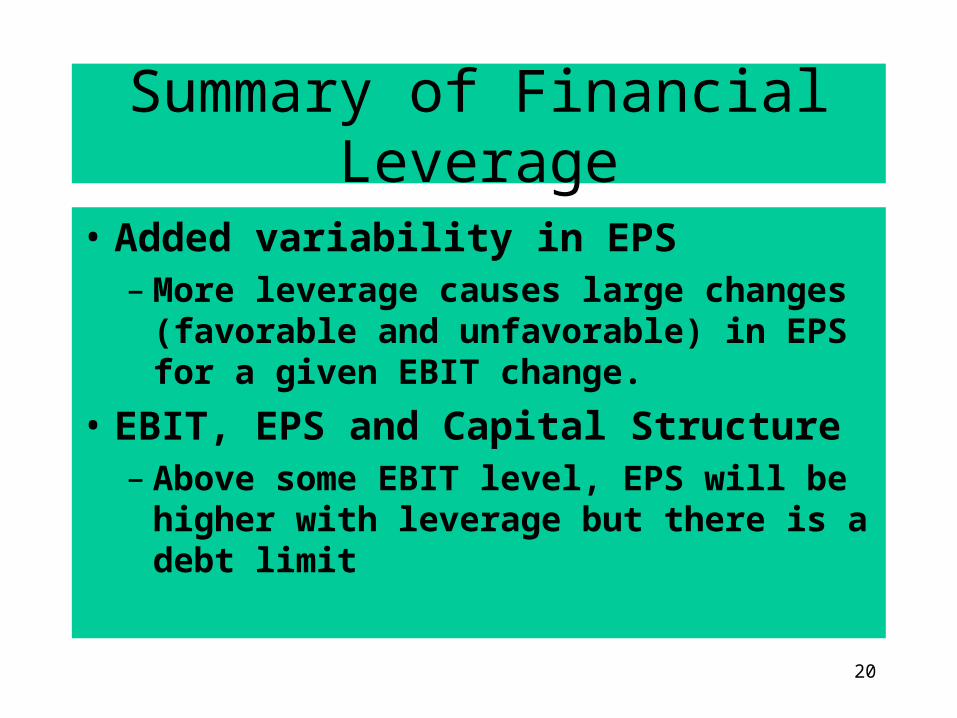

• Added variability in EPS– More leverage causes large changes

(favorable and unfavorable) in EPS for a given EBIT change.

• EBIT, EPS and Capital Structure– Above some EBIT level, EPS will be higher

with leverage but there is a debt limit

21

Management Practices

• Management sets debt targets based on evaluation of business risk (sales and EBIT variability). Influenced by– Desired bond rating– Having a borrowing reserve– Advantage of leverage

• Unwise to use large amounts of leverage with an uncertain income stream.