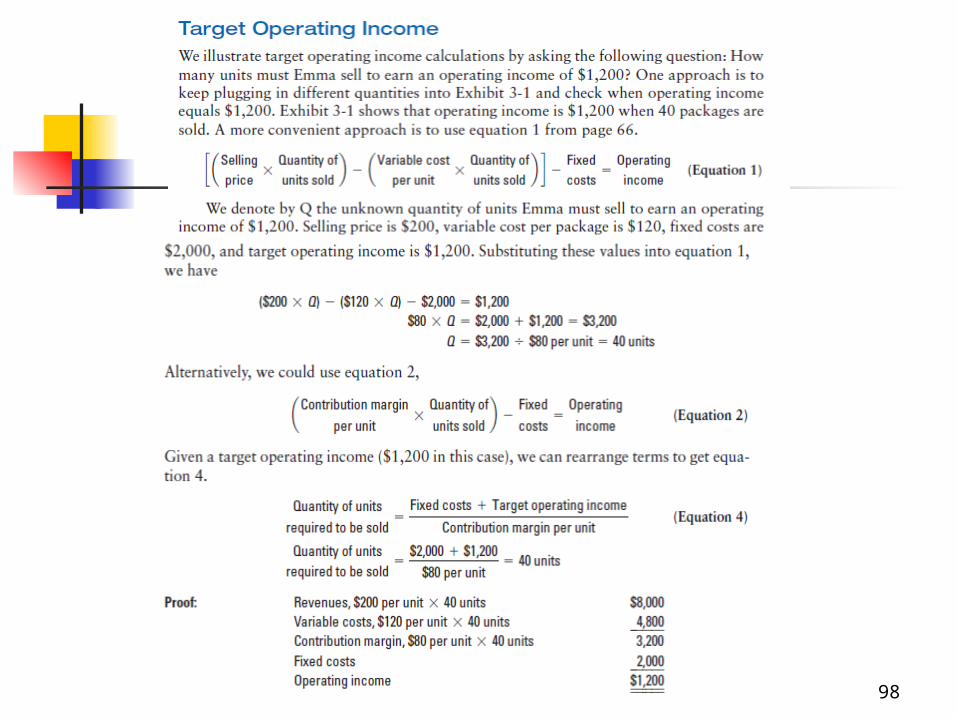

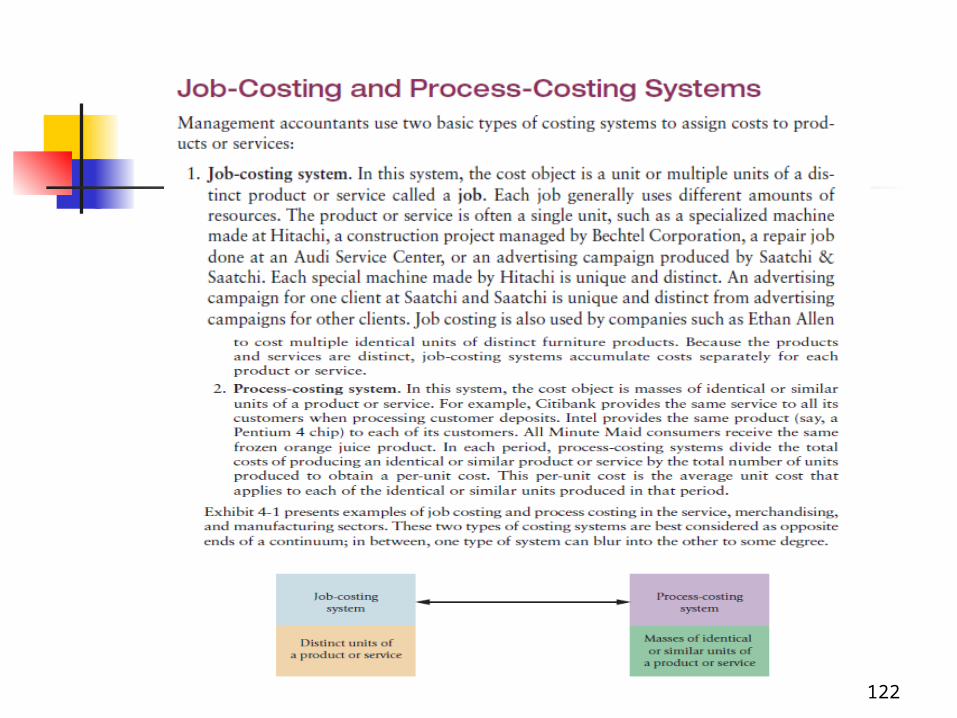

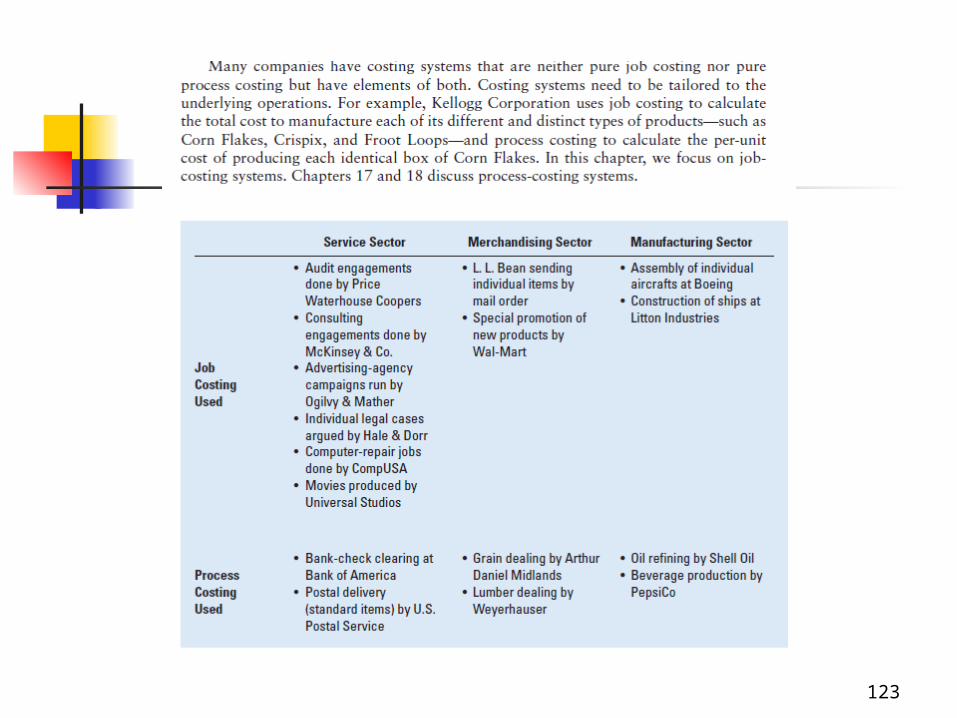

Job Costing, Job Costing System, Normal costing, ABC Costing

Upload

teresa-hinesCategory

view

227download

0

1

Chapter 1Costing Principles

Eng. MHMD RAWSHDH

2

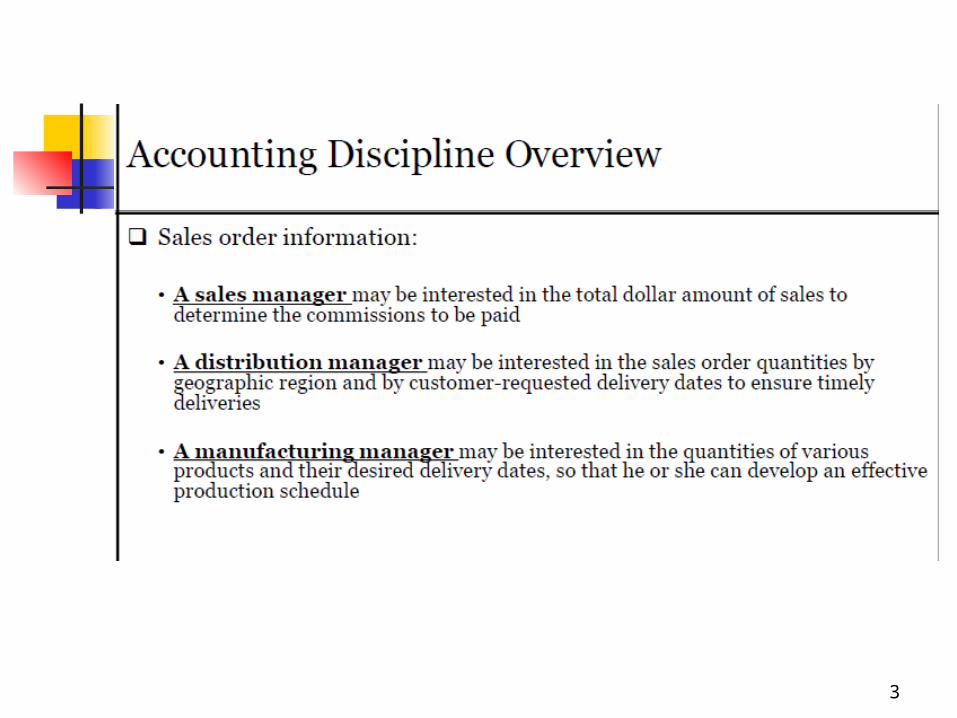

3

4

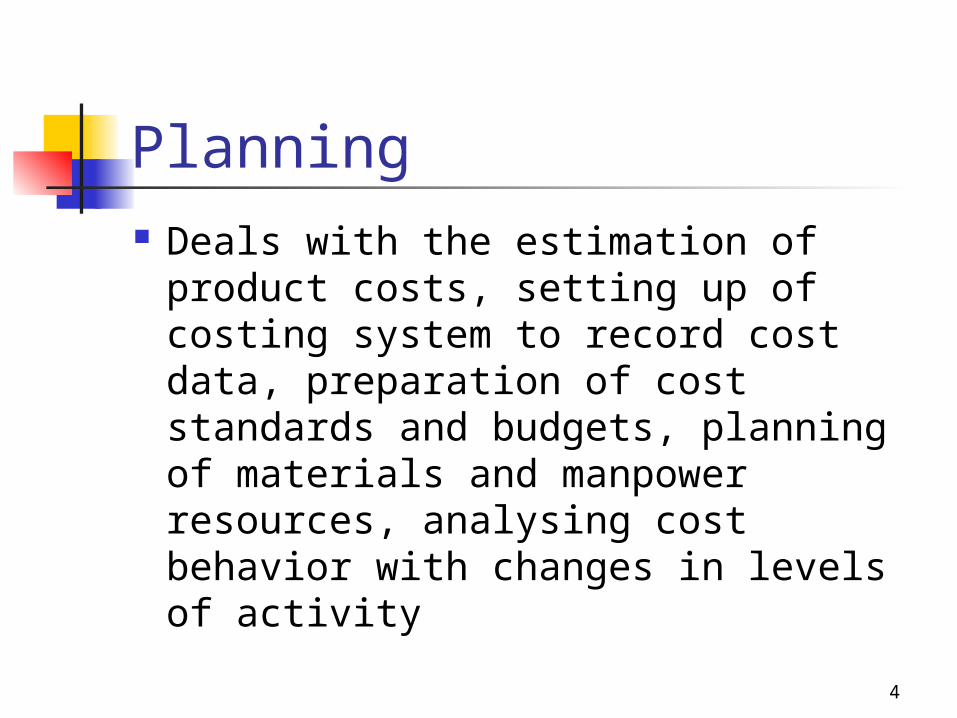

Planning Deals with the estimation of

product costs, setting up of costing system to record cost data, preparation of cost standards and budgets, planning of materials and manpower resources, analysing cost behavior with changes in levels of activity

5

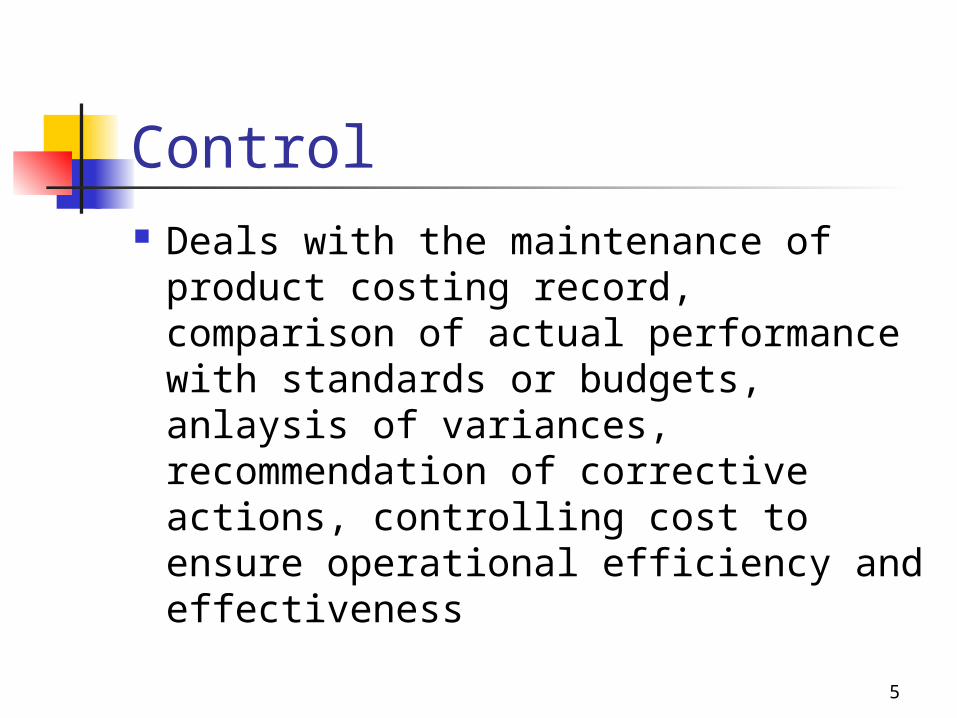

Control Deals with the maintenance of

product costing record, comparison of actual performance with standards or budgets, anlaysis of variances, recommendation of corrective actions, controlling cost to ensure operational efficiency and effectiveness

6

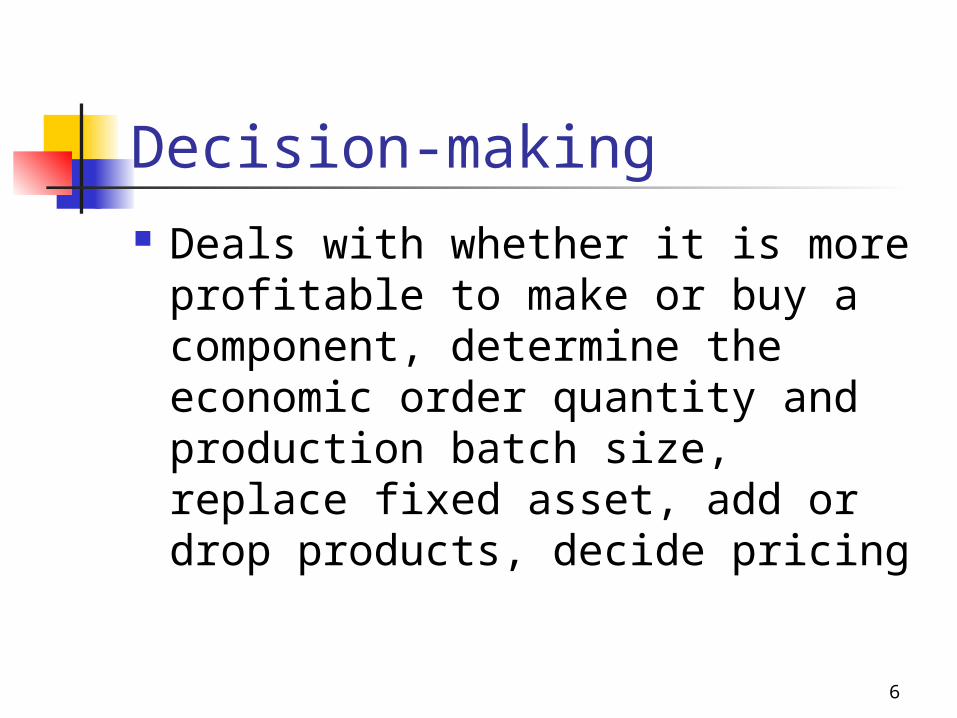

Decision-making Deals with whether it is more

profitable to make or buy a component, determine the economic order quantity and production batch size, replace fixed asset, add or drop products, decide pricing

7

Application Cost accounting has extended

from manufacturing operations to a variety of service industries such as hotels, bands, airline, etc

Cost accounting system should be flexible and adaptable to meet the new business environment and the changing nature of the company

8

Meanings Financial accounting Cost accounting Management accounting

9

Financial Accounting

Financial accounting measures and records business transactions and provides financial statements that are based on Generally Accepted Accounting Principles (GAAP)

Managers are responsible for the financial statements issued to investors, government regulators, and other parties outside the organization

Financial accounting focuses on external parties

Financial accounting reports on what happened in the past

10

Financial accounting Provides information to users who

are external to the business It reports on past transactions to

draw up financial statements The format are governed by law

and accounting standards established by the professional accounting policies

11

Cost Accounting

Cost accounting measures and reports information relating to the cost of acquiring and utilizing resources

Cost accounting provides information for management and financial accounting

Cost management describes the approaches and activities of managers in short-run and long-run planning and control decisions

These decisions increase value of customers and lower costs of products and services

Cost management is an integral part of a company’s strategy

12

Cost accounting Is concerned with internal users of

accounting information, such as operation managers

The generated reports are specific to the requirement of the management

The reporting can be in any format which suits the user

13

Cost Accounting

It provides information for both management accounting and financial accounting.

It measures and reports from financial and non financial data.

14

Management accounting Comprises all cost accounting

functions The accounting for product and

service costs, management accounting extends to use various internal accounting reports for planning, control and decision making

15

Cost and management accounting Provides management with costs

for products, inventories, operations or functions and compares actual to predetermined data

It also provides a variety of data for many day-to-day decision as well as essential information for long-range decisions

16

Functions of managerial accounting Determining the cost Providing relevant information for

better decision-making Providing information for planning,

control, decision-making and application

17

Comparison of cost, management and financial accounting

18

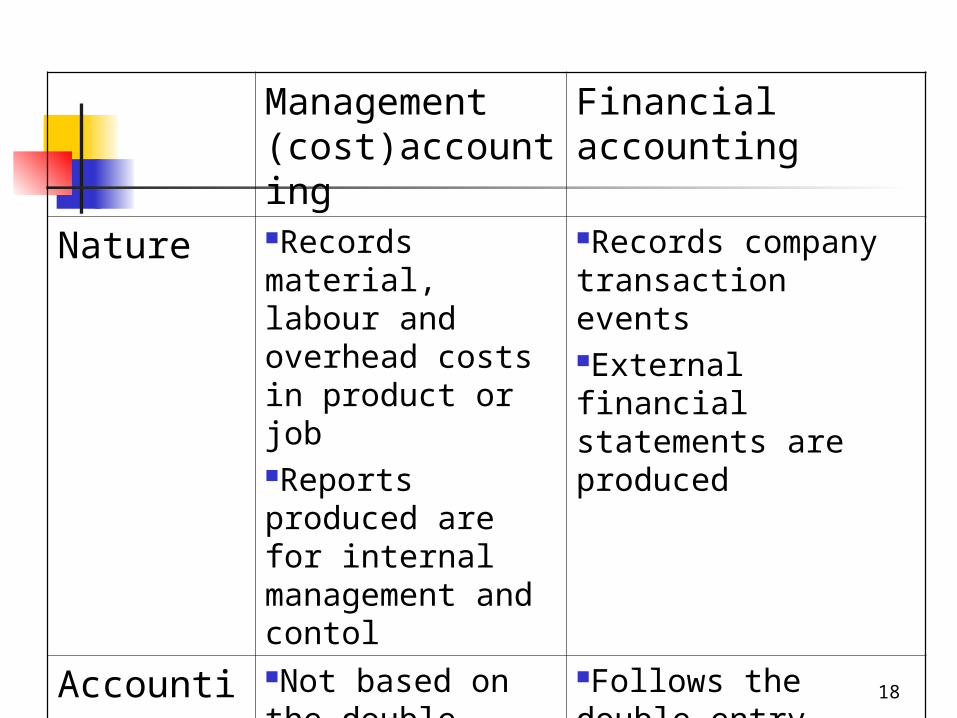

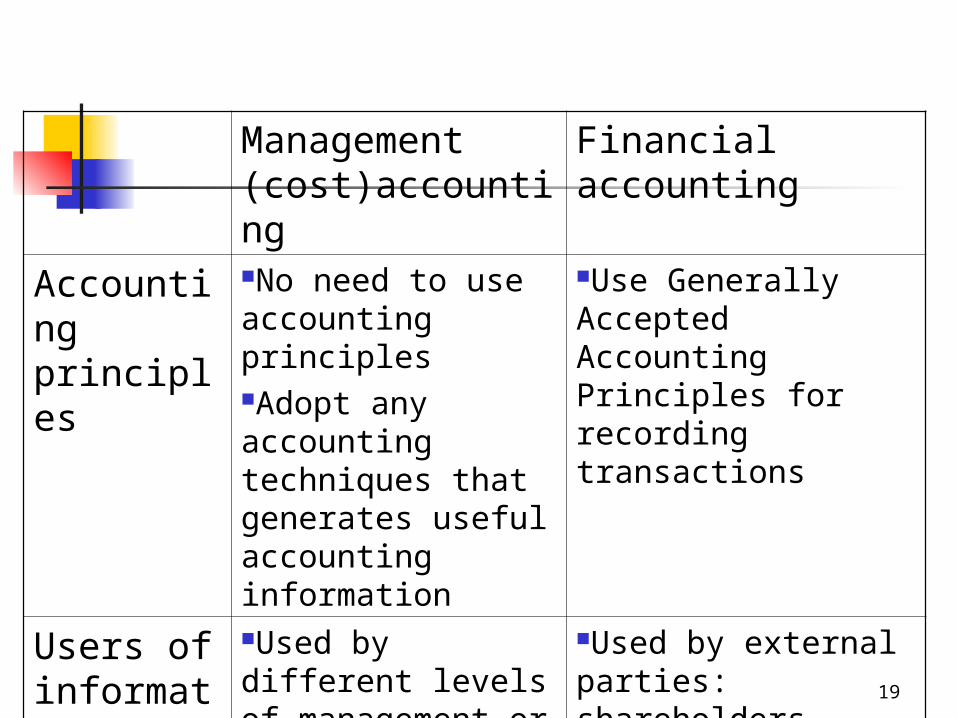

Management (cost)accounting

Financial accounting

Nature Records material, labour and overhead costs in product or jobReports produced are for internal management and contol

Records company transaction eventsExternal financial statements are produced

Accounting system

Not based on the double entry system

Follows the double entry system

19

Management (cost)accounting

Financial accounting

Accounting principles

No need to use accounting principlesAdopt any accounting techniques that generates useful accounting information

Use Generally Accepted Accounting Principles for recording transactions

Users of information

Used by different levels of management or departments responsible for respective activities

Used by external parties: shareholders, creditors, government, etc

20

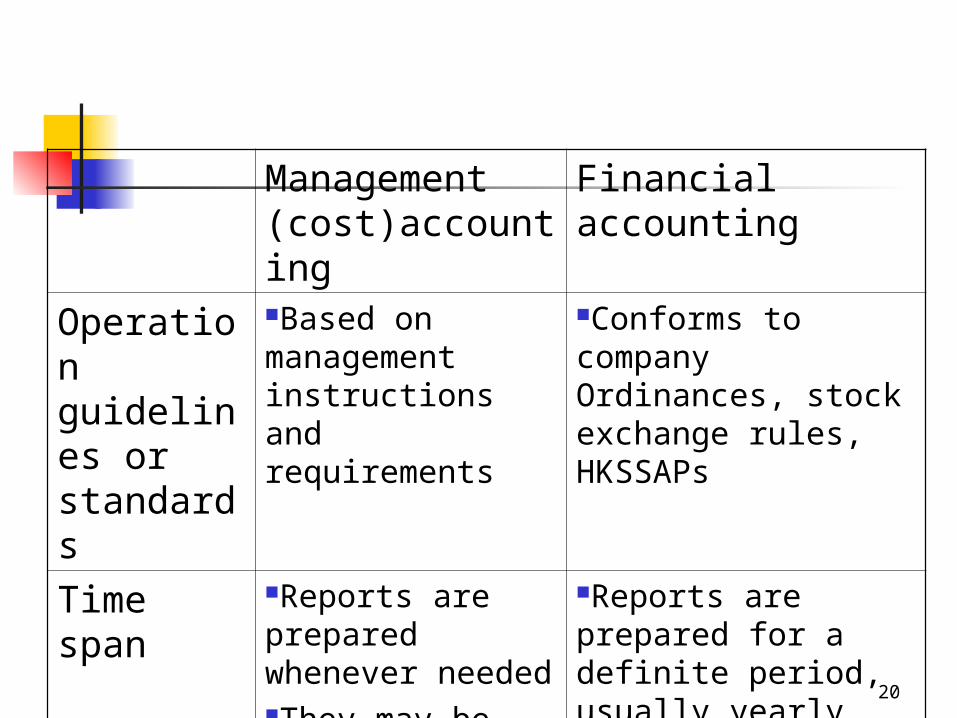

Management (cost)accounting

Financial accounting

Operation guidelines or standards

Based on management instructions and requirements

Conforms to company Ordinances, stock exchange rules, HKSSAPs

Time span

Reports are prepared whenever neededThey may be prepared on a weekly or daily basis

Reports are prepared for a definite period, usually yearly and half yearly

21

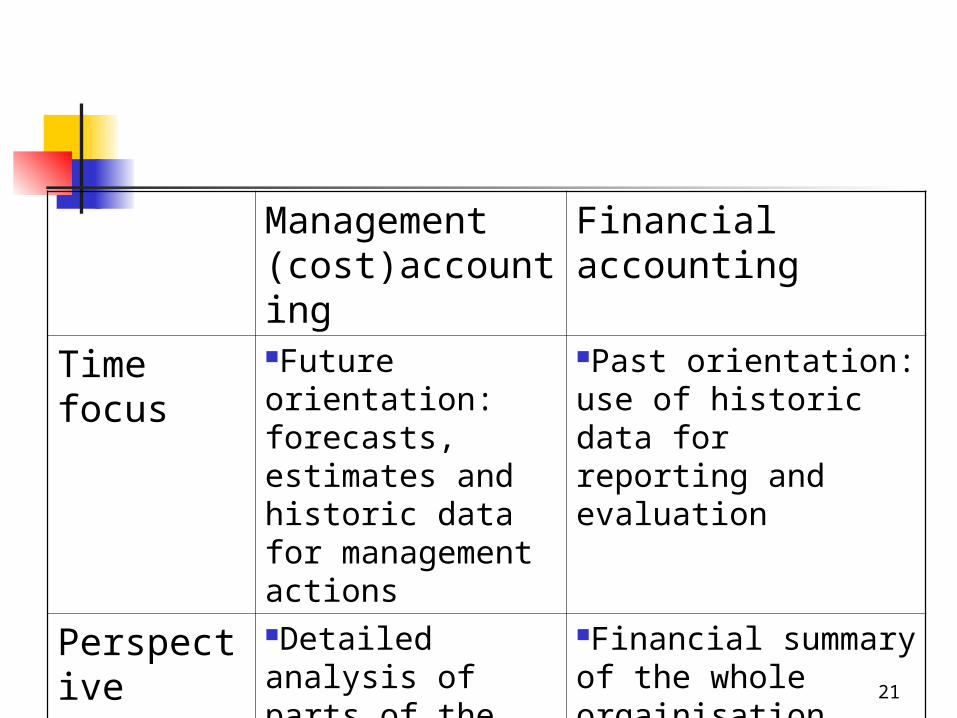

Management (cost)accounting

Financial accounting

Time focus

Future orientation: forecasts, estimates and historic data for management actions

Past orientation: use of historic data for reporting and evaluation

Perspective

Detailed analysis of parts of the entity, products, regions, etc

Financial summary of the whole orgainisation

22

Cost accountingvs.

Management accounting

23

Management accounting

Cost accounting

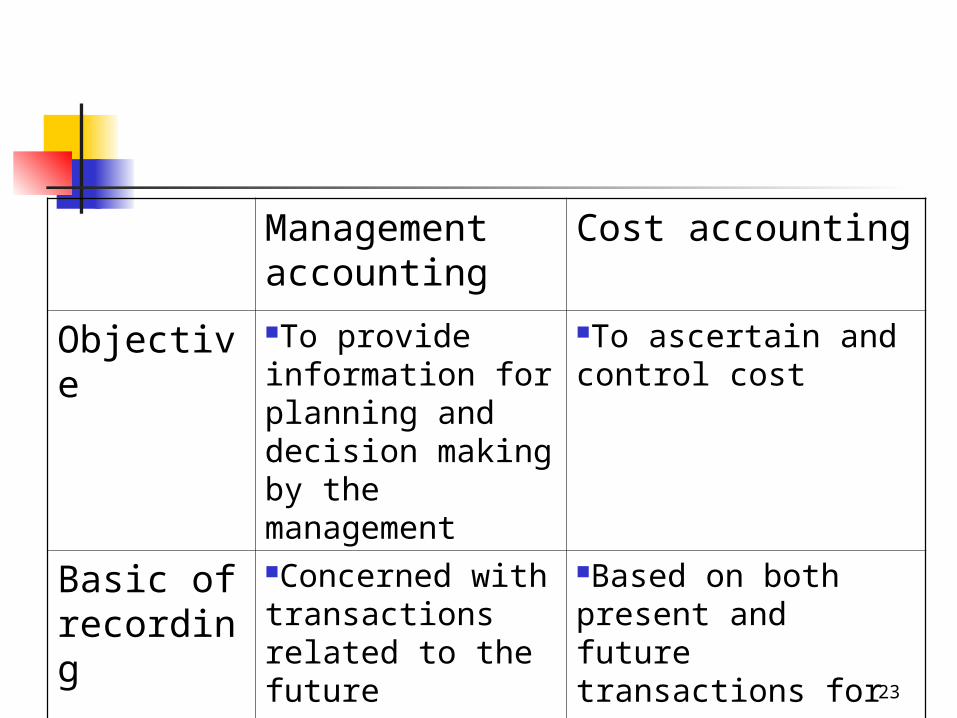

Objective To provide information for planning and decision making by the management

To ascertain and control cost

Basic of recording

Concerned with transactions related to the future

Based on both present and future transactions for cost ascertainment

24

Management accounting

Cost accounting

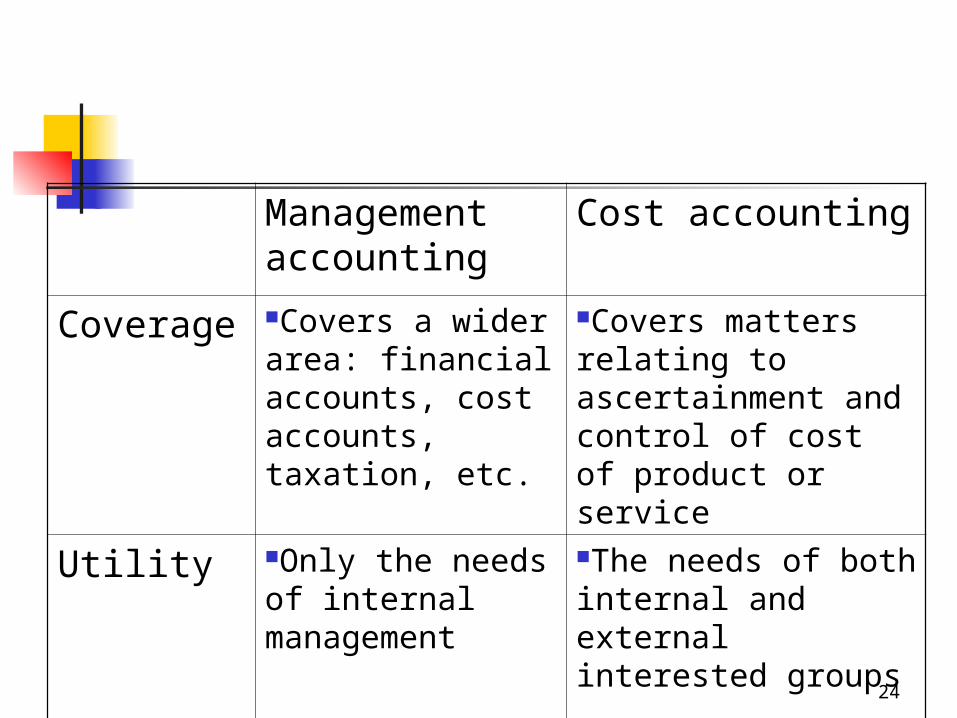

Coverage Covers a wider area: financial accounts, cost accounts, taxation, etc.

Covers matters relating to ascertainment and control of cost of product or service

Utility Only the needs of internal management

The needs of both internal and external interested groups

25

Management accounting

Cost accounting

Types of transactions

Deals with both monetary any non-monetary transactions, covering both quantitative and qualitative aspects

Deals only with monetary transactions, covering only quantitative aspect

26

27

28

29

30

31

32

33

34

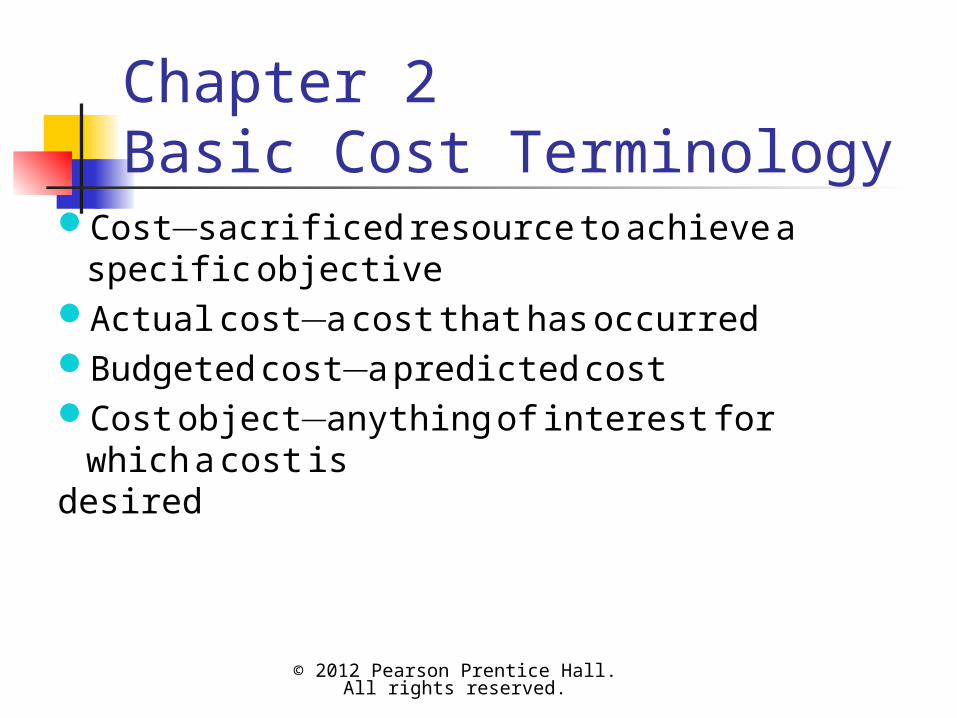

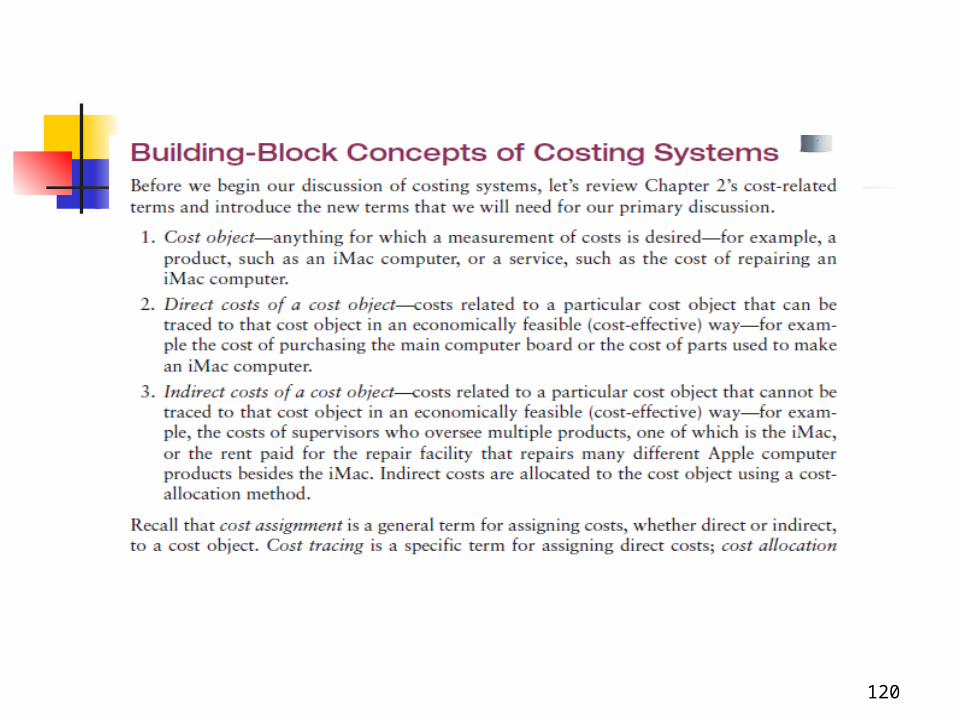

Chapter 2Basic Cost Terminology

© 2012 Pearson Prentice Hall. All rights reserved.

Cost—sacrificed resource to achieve a specific objective

Actual cost—a cost that has occurredBudgeted cost—a predicted costCost object—anything of interest for which

a cost isdesired

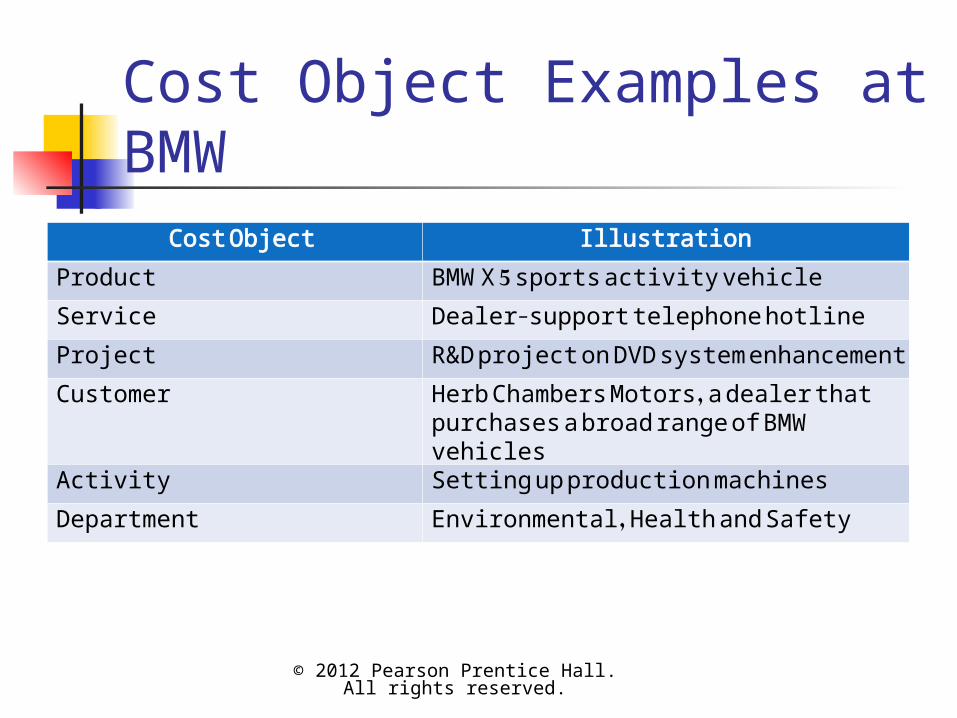

Cost Object Examples at BMW

© 2012 Pearson Prentice Hall. All rights reserved.

Cost Object IllustrationProduct BMW X 5 sports activity vehicleService Dealer-support telephone hotlineProject R&D project on DVD system

enhancementCustomer Herb Chambers Motors, a dealer that

purchases a broad range of BMW vehicles

Activity Setting up production machinesDepartment Environmental, Health and Safety

Basic Cost Terminology

© 2012 Pearson Prentice Hall. All rights reserved.

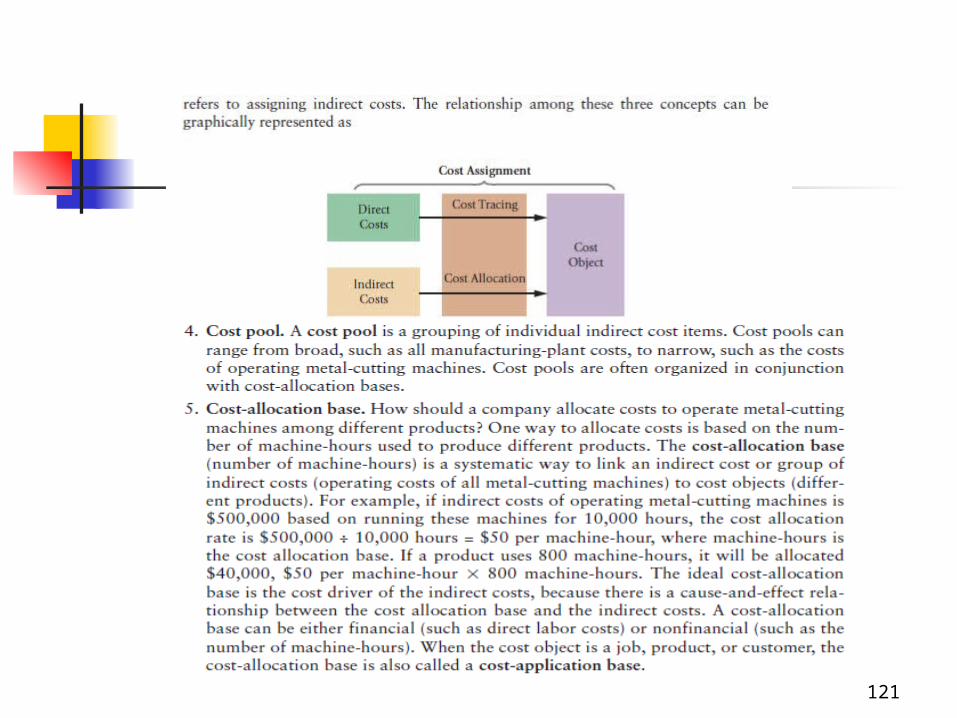

Cost accumulation—a collection of cost data in an organized manner

Cost assignment—a general term that includes gathering accumulated costs to a cost object. This includes:Tracing accumulated costs with a direct

relationship to the cost object andAllocating accumulated costs with an indirect

relationship to a cost object

Direct and Indirect Costs

© 2012 Pearson Prentice Hall. All rights reserved.

Direct costs can be conveniently and economically traced (tracked) to a cost object.

Indirect costs cannot be conveniently or economically traced (tracked) to a cost object. Instead of being traced, these costs are allocated to a cost object in a rational and systematic manner.

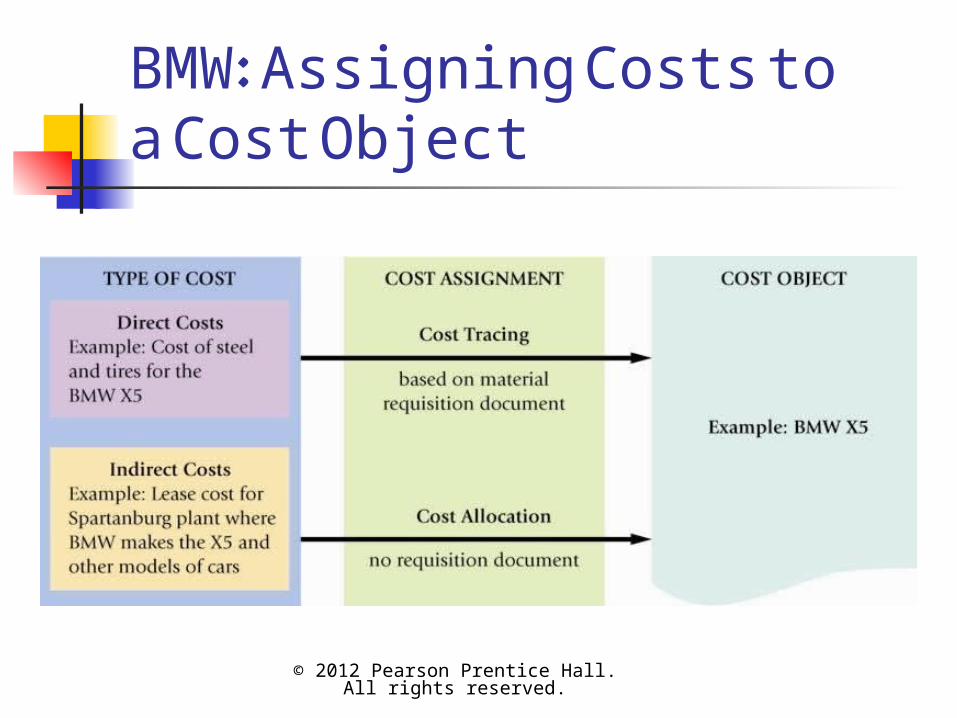

BMW: Assigning Costs to a Cost Object

© 2012 Pearson Prentice Hall. All rights reserved.

Cost Examples

© 2012 Pearson Prentice Hall. All rights reserved.

Direct CostsPartsAssembly line

wagesIndirect Costs

ElectricityRentProperty taxes

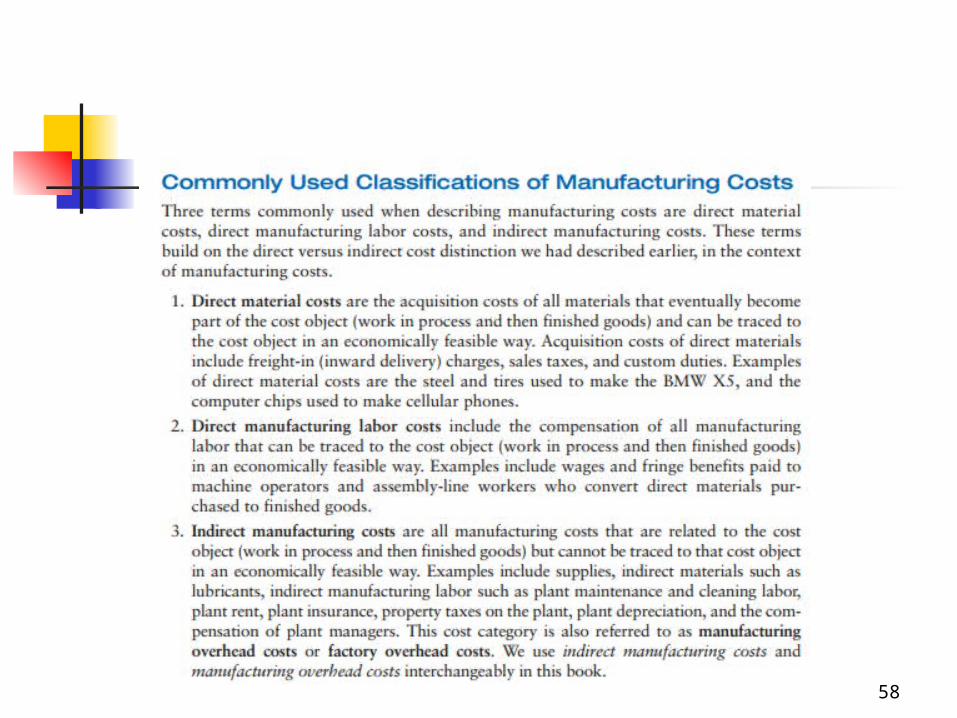

Factors Affecting Direct/Indirect Cost Classification

© 2012 Pearson Prentice Hall. All rights reserved.

Cost materialityAvailability of information-gathering

technologyOperational design

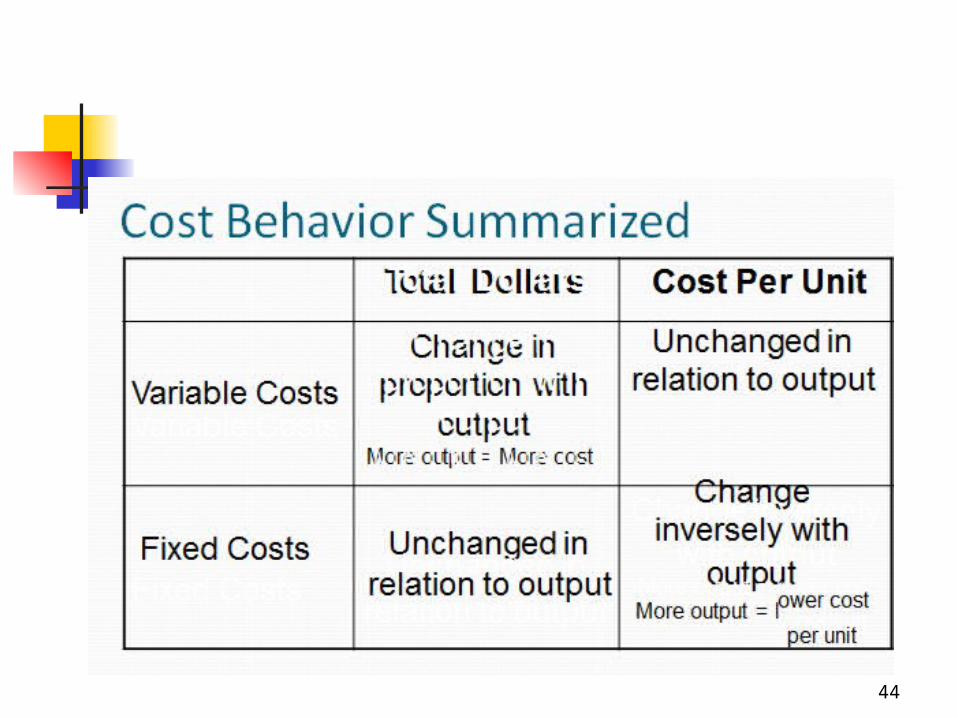

Cost Behavior

© 2012 Pearson Prentice Hall. All rights reserved.

Variable costs—changes in total in proportion to changes in the related level of activity or volume.

Fixed costs—remain unchanged in total regardless of changes in the related level of activity or volume.

Costs are fixed or variable only with respect to a specific activity or a given time period.

Cost Behavior

© 2012 Pearson Prentice Hall. All rights reserved.

Variable costs are constant on a per-unit basis. If a product takes 5 pounds of materials each, it stays the same per unit regardless if one, ten, or a thousand units are produced.

Fixed costs change inversely with the level of production. As more units are produced, the same fixed cost is spread over more and more units, reducing the cost per unit.

44

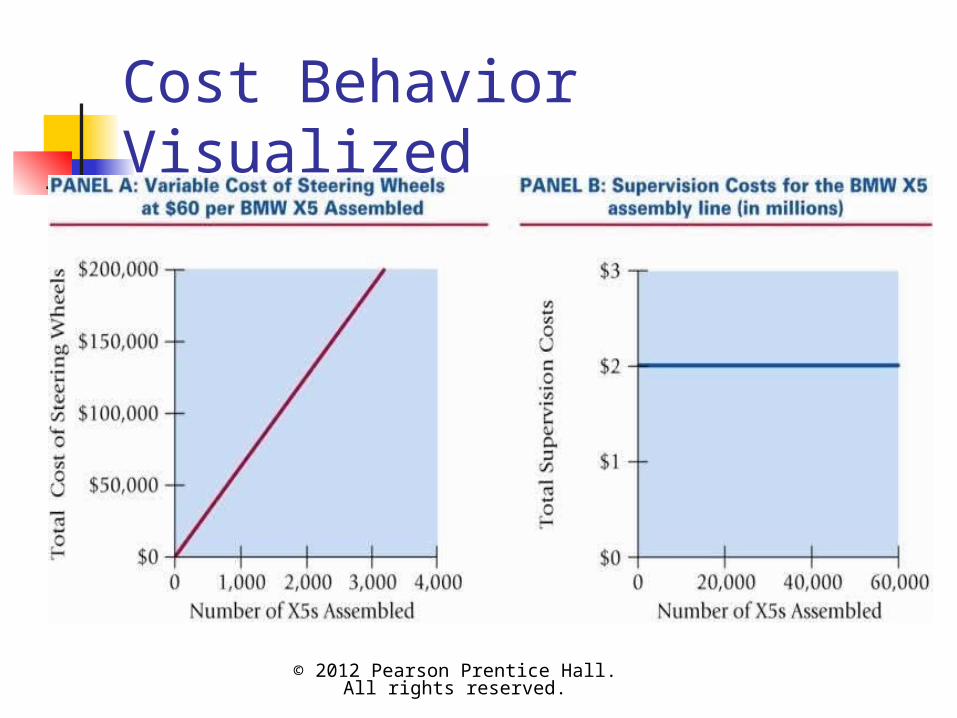

Cost Behavior Visualized

© 2012 Pearson Prentice Hall. All rights reserved.

Other Cost Concepts

© 2012 Pearson Prentice Hall. All rights reserved.

Cost driver—a variable that causally affects costs over a given time span

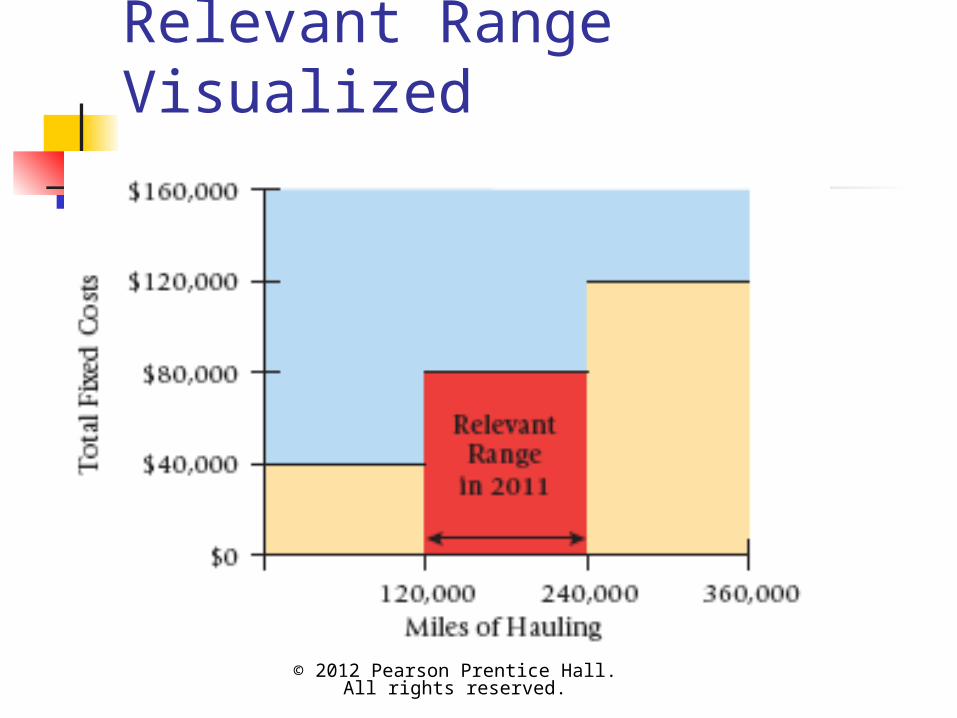

Relevant range—the band of normal activity level (or volume) in which there is a specific relationship between the level of activity (or volume) and a given costFor example, fixed costs are considered fixed

only within the relevant range.

Relevant Range Visualized

© 2012 Pearson Prentice Hall. All rights reserved.

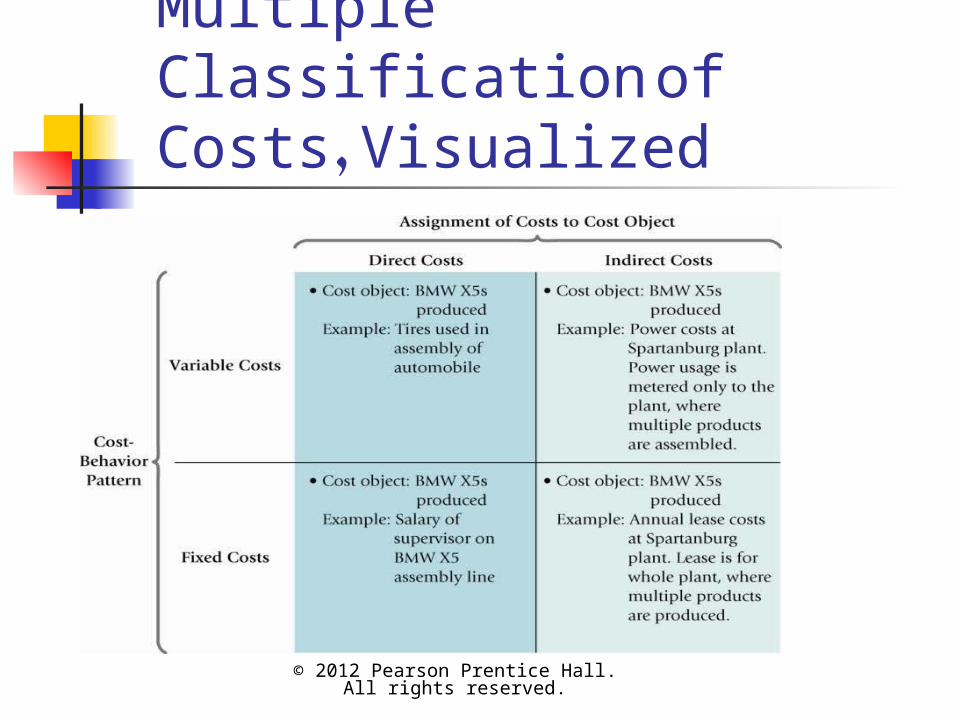

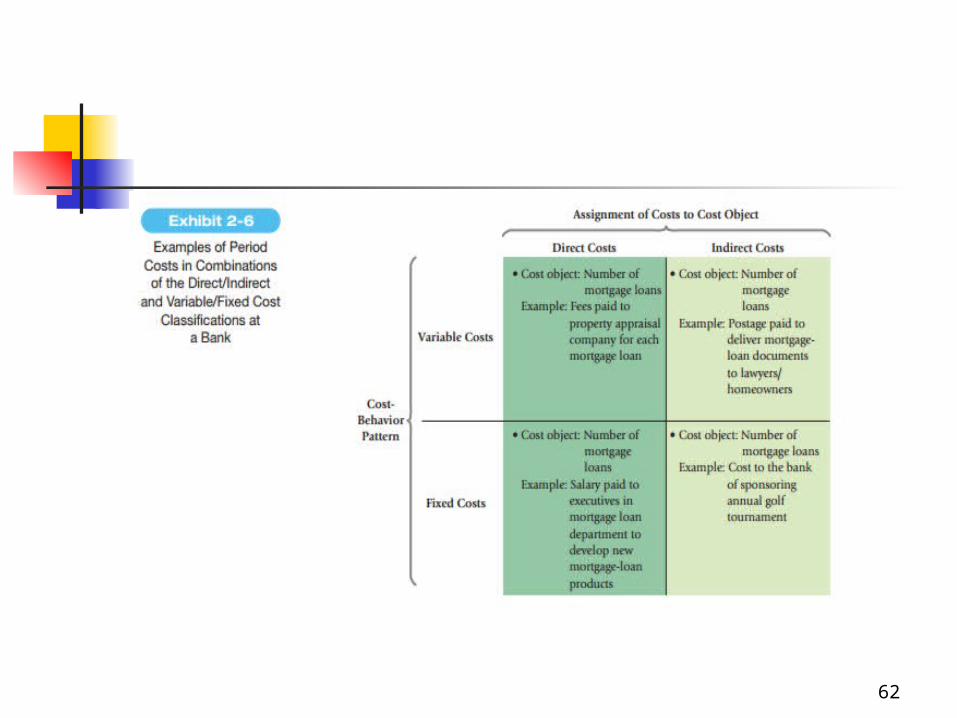

Multiple Classification of Costs

© 2012 Pearson Prentice Hall. All rights reserved.

Costs may be classified as:Direct/Indirect, andVariable/Fixed

These multiple classifications give rise to important

cost combinations:Direct and variableDirect and fixedIndirect and variableIndirect and fixed

Multiple Classification of Costs, Visualized

© 2012 Pearson Prentice Hall. All rights reserved.

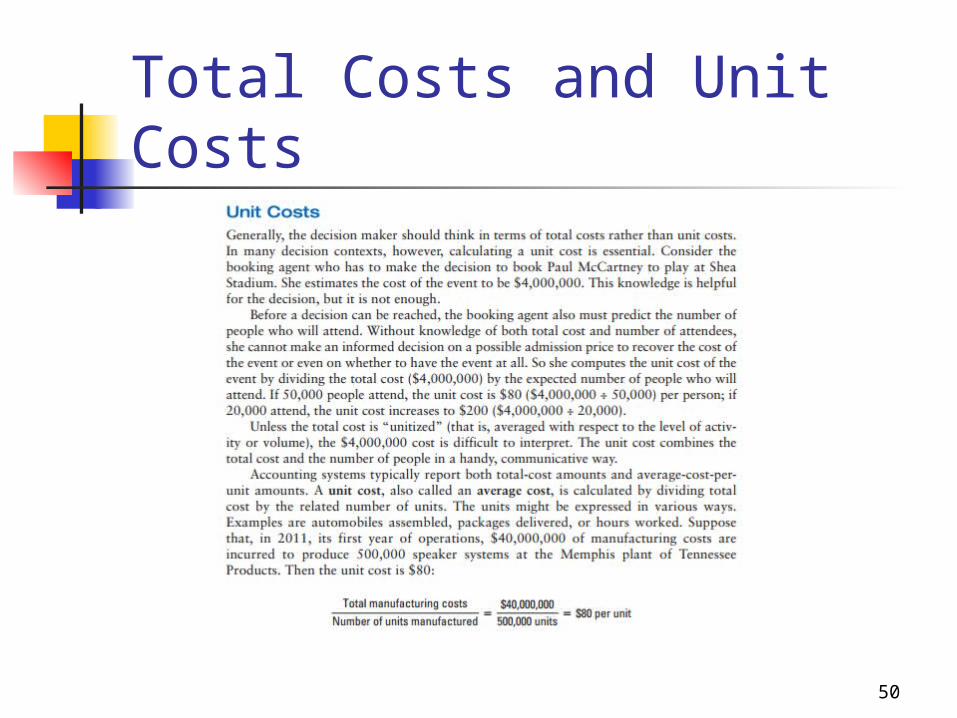

Total Costs and Unit Costs

50

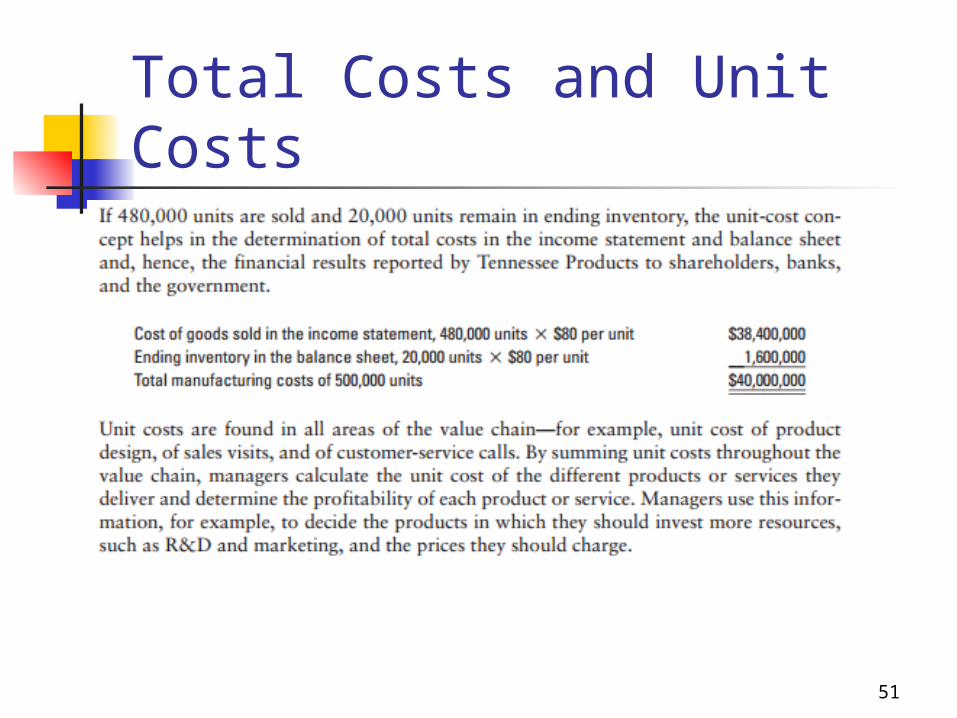

Total Costs and Unit Costs

51

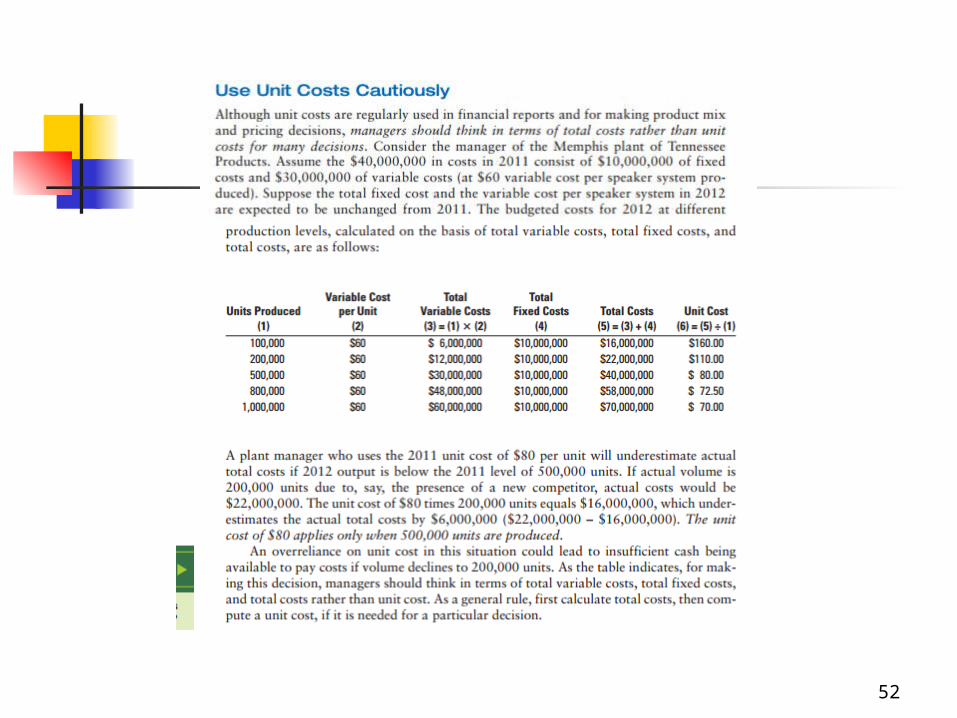

52

Total Costs and Unit Costs

© 2012 Pearson Prentice Hall. All rights reserved.

Unit costs should be used cautiously. Because unit costs change with a different level of output or volume, it may be more prudent to base decisions on a total dollar basis.Unit costs that include fixed costs should

alwaysreference a given level of output or activity.

Unit costs are also called average costs.Managers should think in terms of total costs

ratherthan unit costs.

54

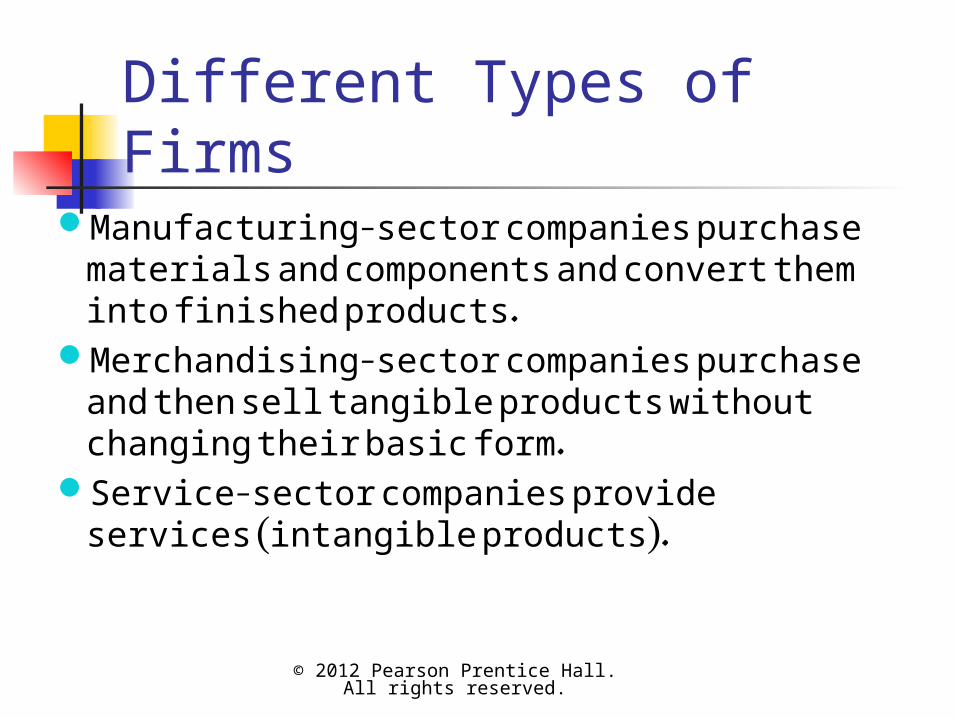

Different Types of Firms

© 2012 Pearson Prentice Hall. All rights reserved.

Manufacturing-sector companies purchase materials and components and convert them into finished products.

Merchandising-sector companies purchase and then sell tangible products without changing their basic form.

Service-sector companies provide services (intangible products).

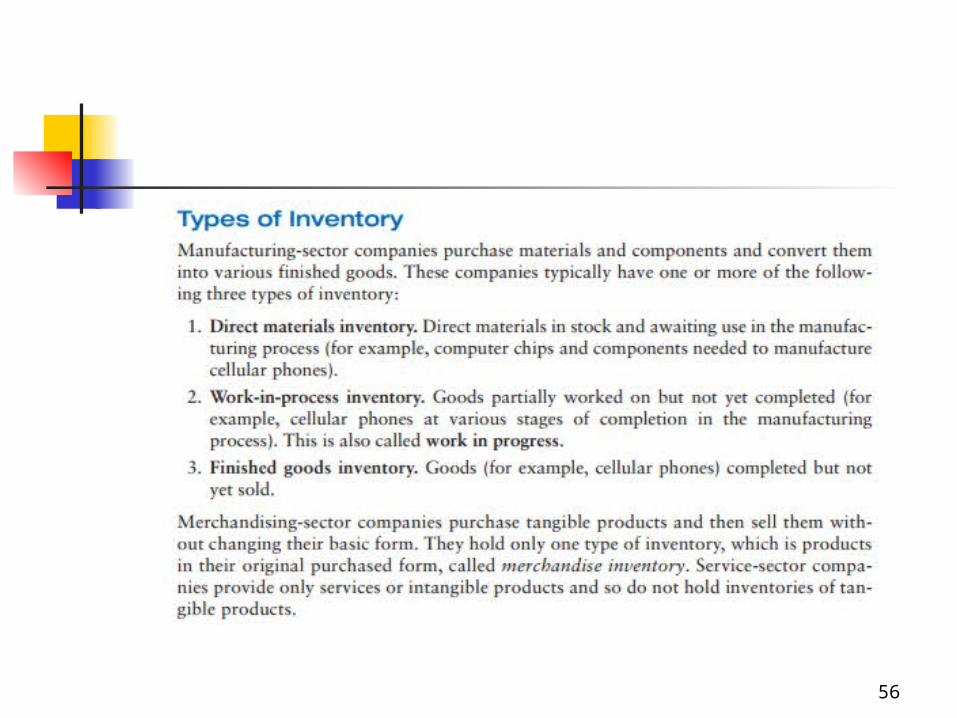

56

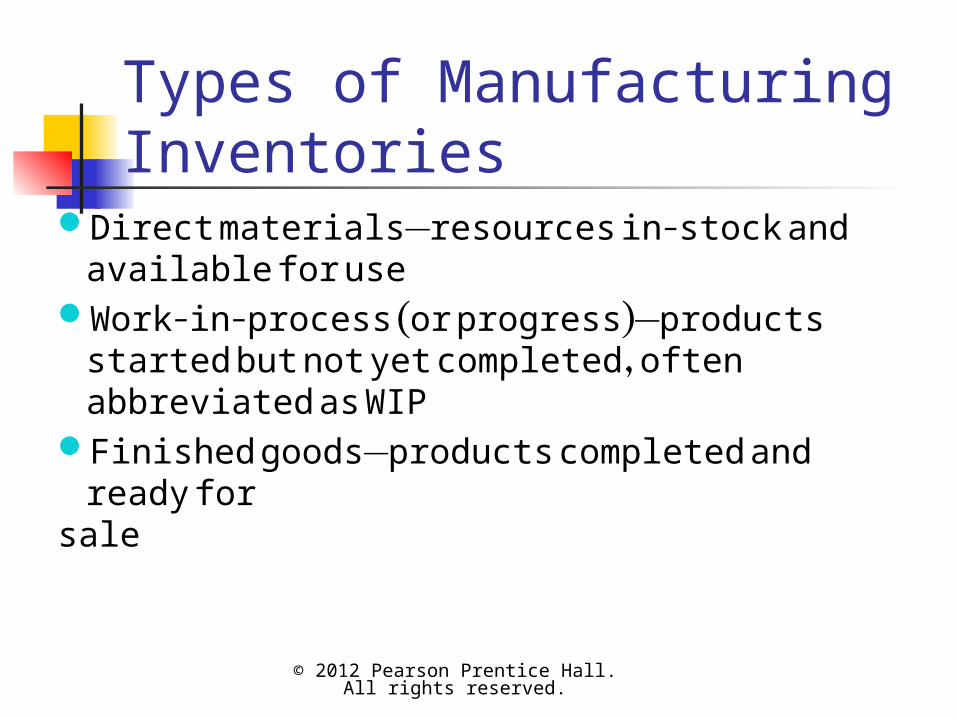

Types of Manufacturing Inventories

© 2012 Pearson Prentice Hall. All rights reserved.

Direct materials—resources in-stock and available for use

Work-in-process (or progress)—products started but not yet completed, often abbreviated as WIP

Finished goods—products completed and ready for

sale

58

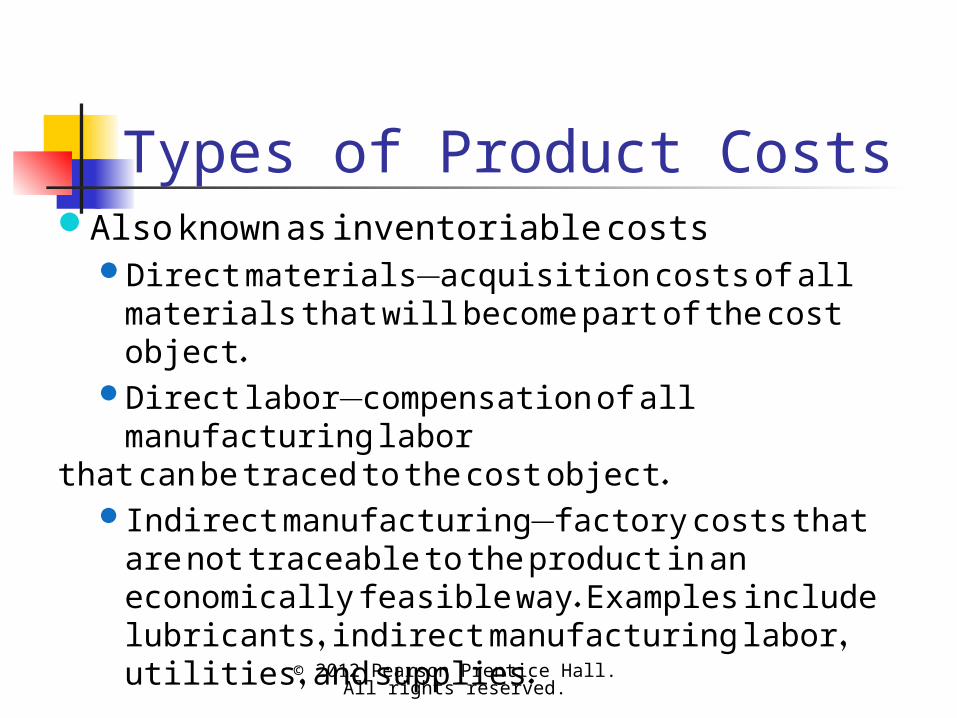

Types of Product Costs

© 2012 Pearson Prentice Hall. All rights reserved.

Also known as inventoriable costsDirect materials—acquisition costs of all

materials that will become part of the cost object.

Direct labor—compensation of all manufacturing labor

that can be traced to the cost object.Indirect manufacturing—factory costs that are

not traceable to the product in an economically feasible way. Examples include lubricants, indirect manufacturing labor, utilities, and supplies.

60

61

62

Accounting Distinction Between Costs

© 2012 Pearson Prentice Hall. All rights reserved.

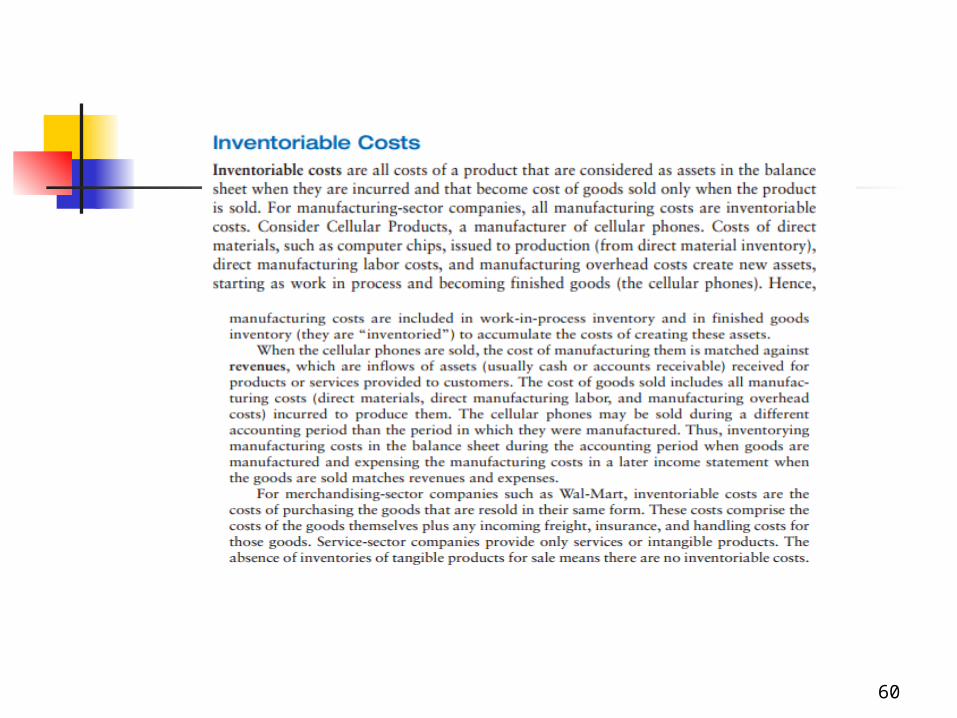

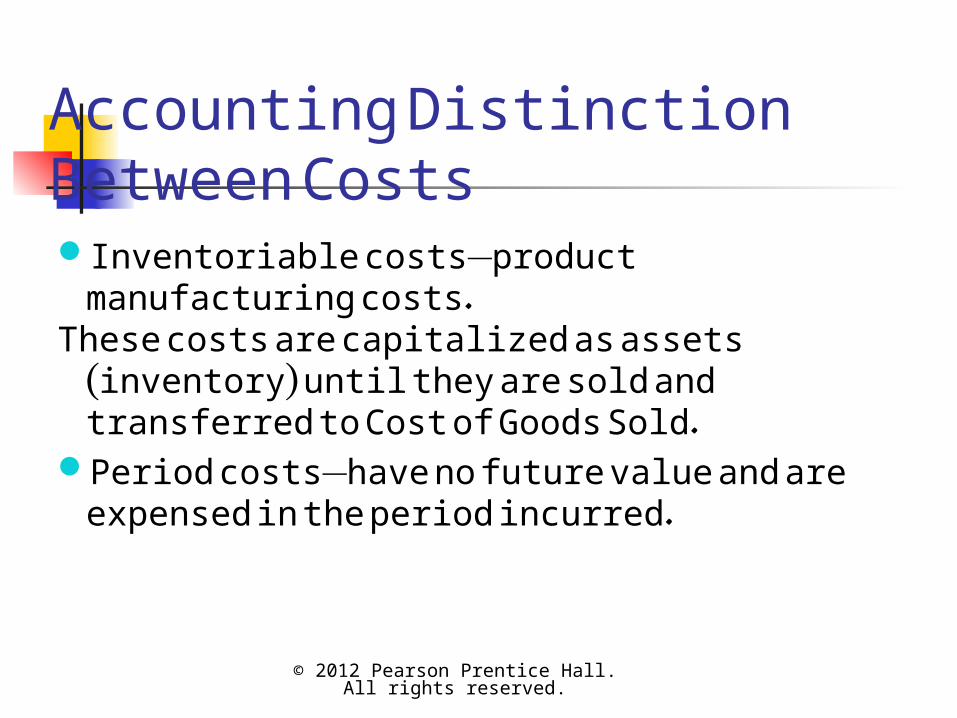

Inventoriable costs—product manufacturing costs.

These costs are capitalized as assets (inventory) until they are sold and transferred to Cost of Goods Sold.

Period costs—have no future value and are expensed in the period incurred.

64

65

66

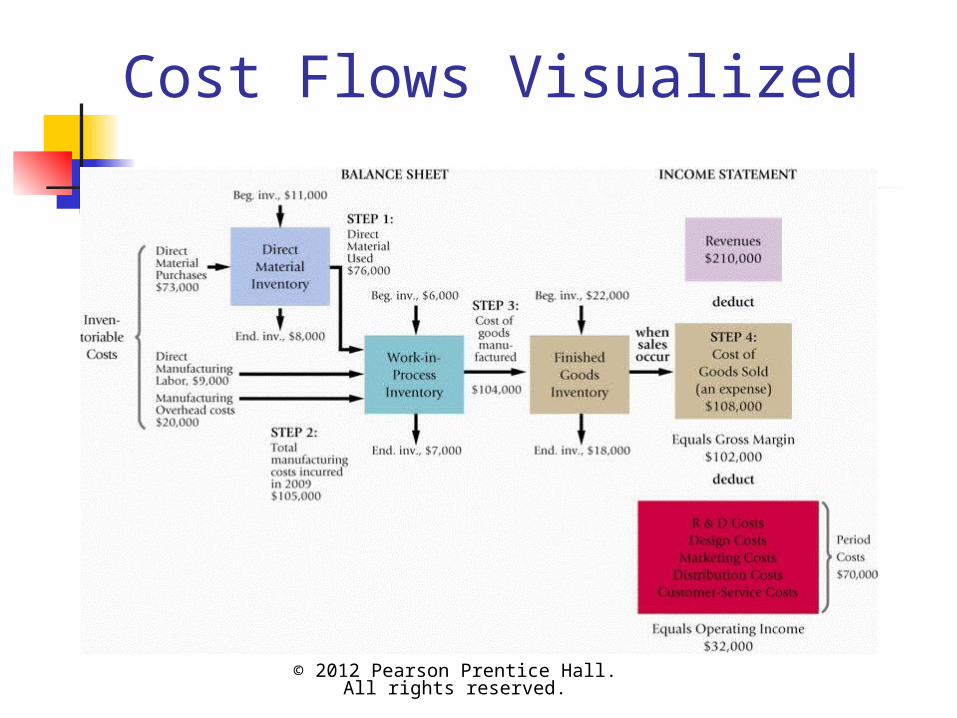

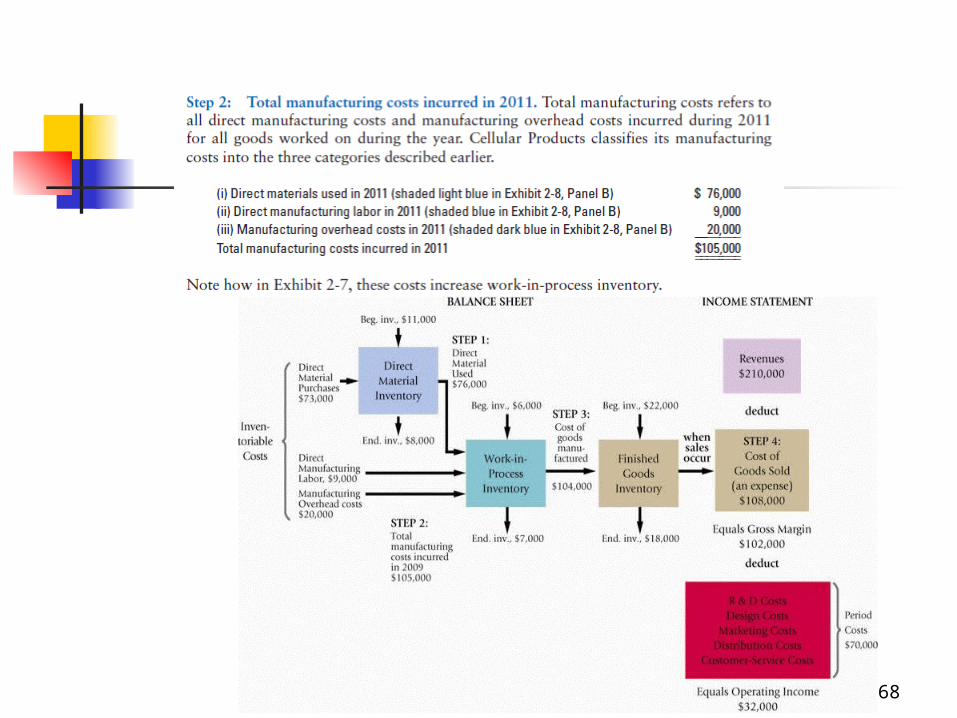

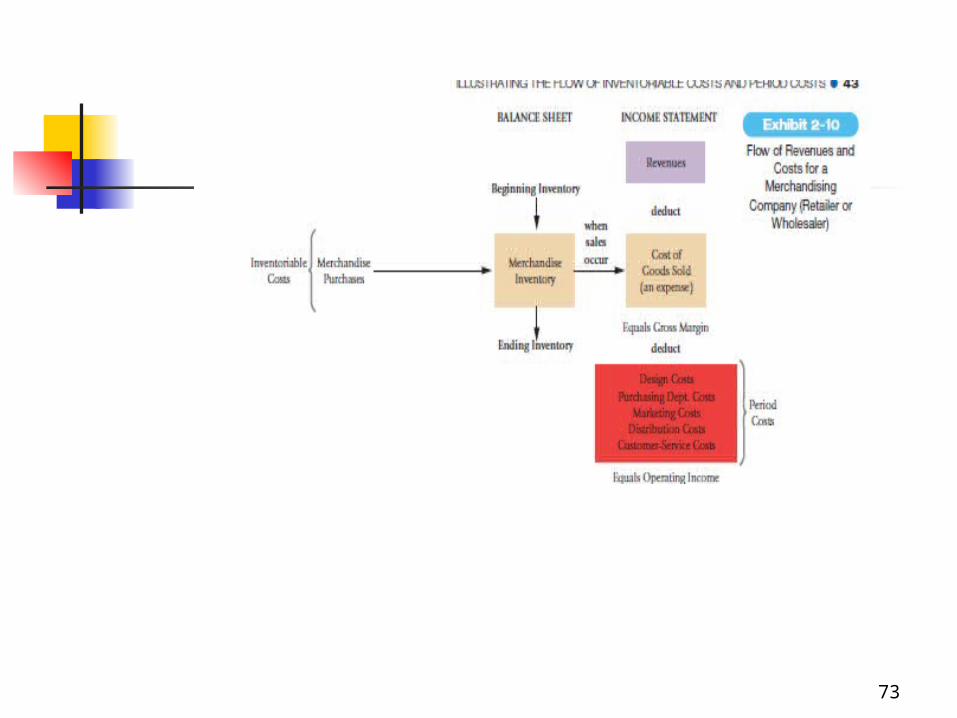

Cost Flows Visualized

© 2012 Pearson Prentice Hall. All rights reserved.

68

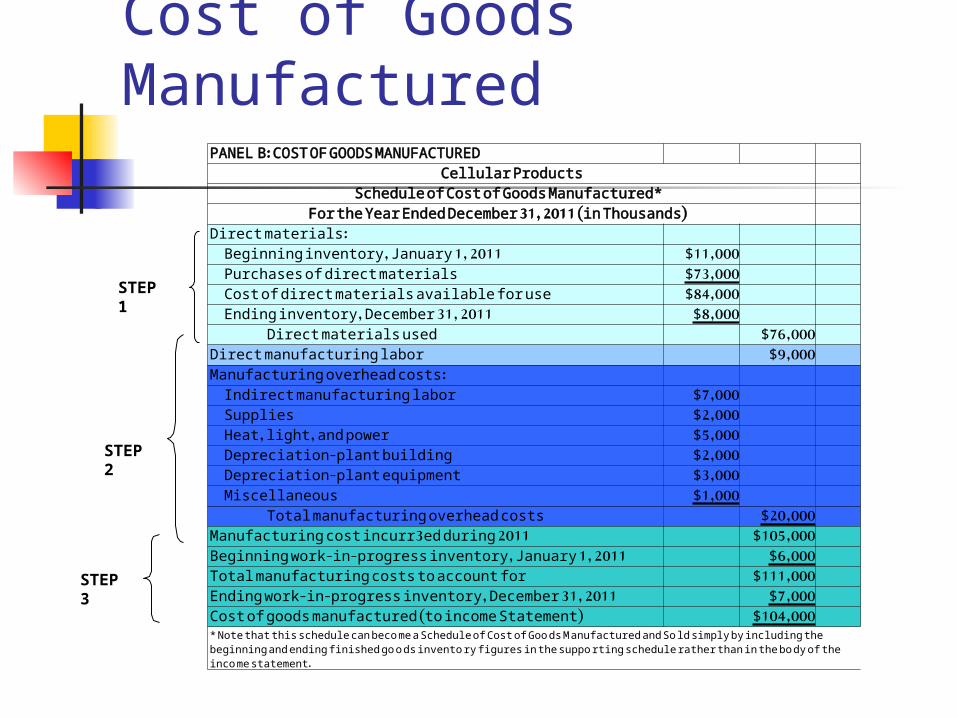

Cost of Goods Manufactured

STEP 1

STEP 3

STEP 2

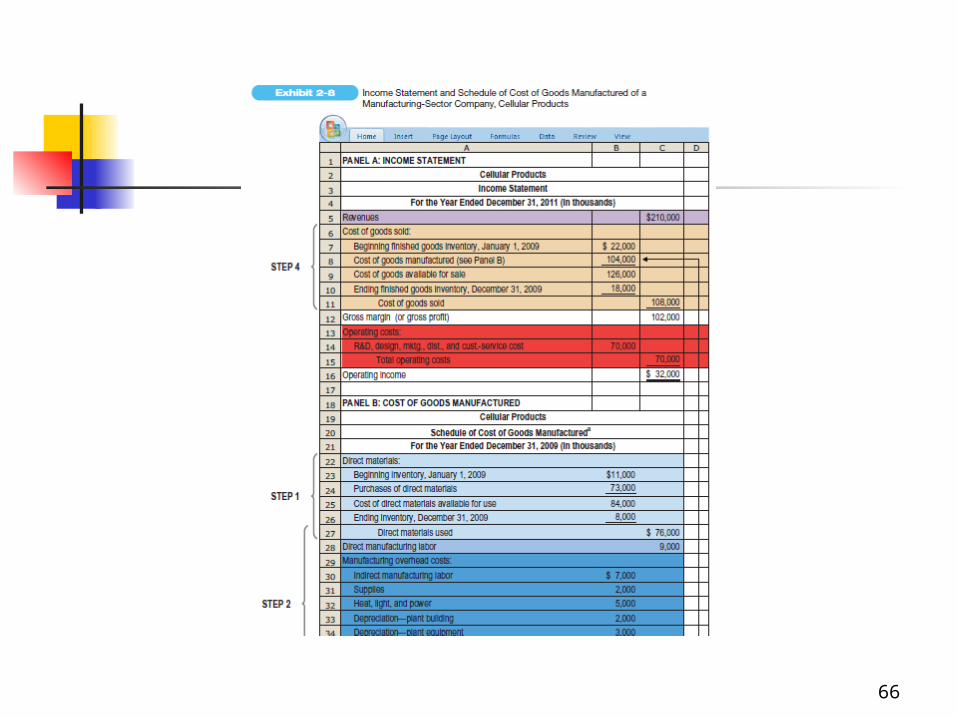

PANEL B: COST OF GOODS MANUFACTUREDCellular Products

Schedule of Cost of Goods Manufactured*For the Year Ended December 31, 2011 (in Thousands)

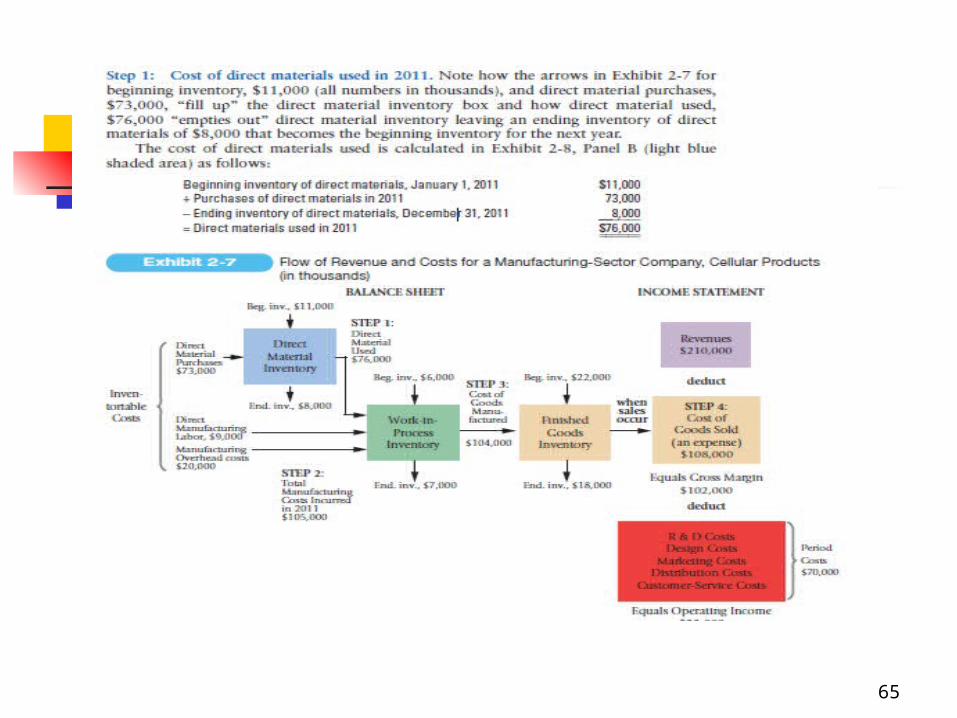

Direct materials:Beginning inventory, January 1, 2011 $11,000Purchases of direct materials $73,000Cost of direct materials available for use $84,000Ending inventory, December 31, 2011 $8,000

Direct materials used $76,000Direct manufacturing labor $9,000Manufacturing overhead costs:

Indirect manufacturing labor $7,000Supplies $2,000Heat, light, and power $5,000Depreciation-plant building $2,000Depreciation-plant equipment $3,000Miscellaneous $1,000

Total manufacturing overhead costs $20,000Manufacturing cost incurr3ed during 2011 $105,000Beginning work-in-progress inventory, January 1, 2011 $6,000Total manufacturing costs to account for $111,000Ending work-in-progress inventory, December 31, 2011 $7,000Cost of goods manufactured (to income Statement) $104,000* Note that this schedule can beco me a Schedule of Cost of Goo ds M anufactured and So ld simply by including the beginning and ending finished go o ds invento ry figures in the suppo rting schedule rather than in the bo dy of the inco me statement.

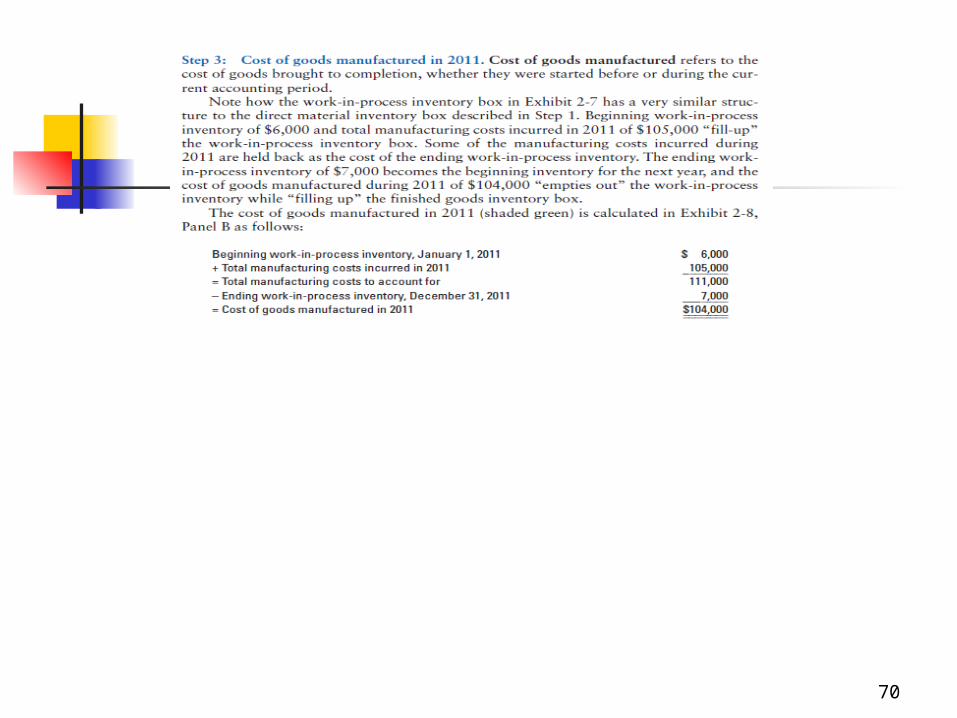

70

zz

71

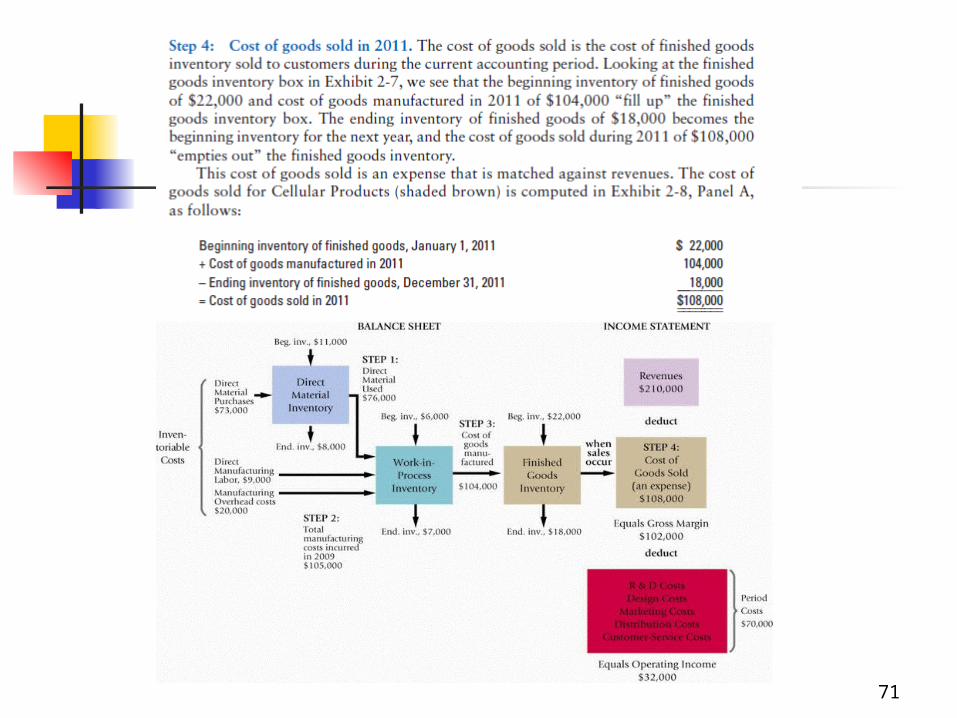

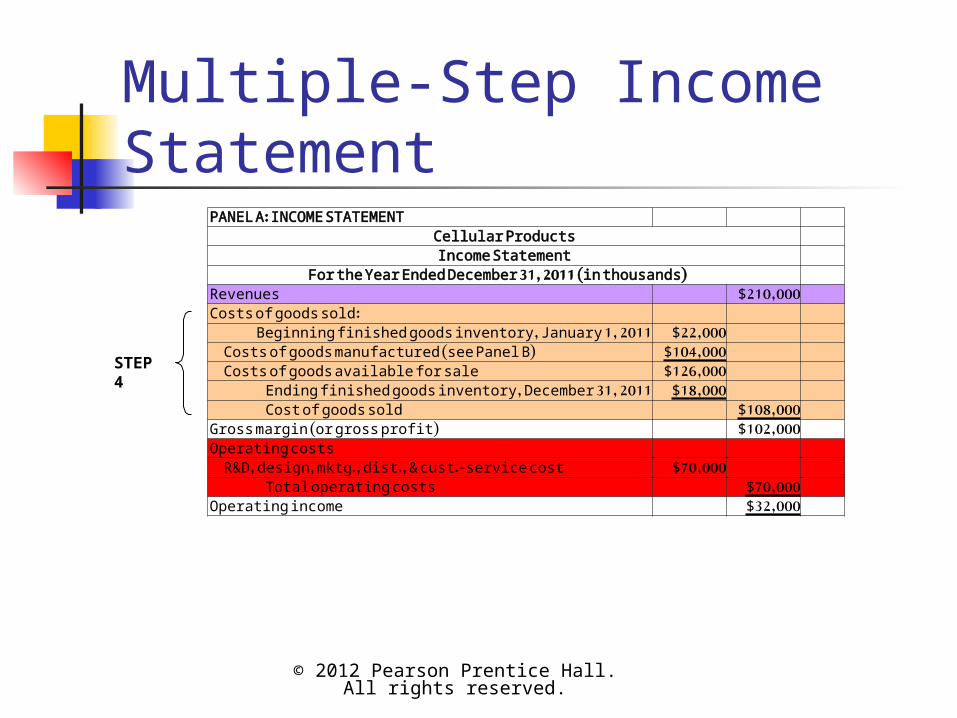

Multiple-Step Income Statement

STEP 4

© 2012 Pearson Prentice Hall. All rights reserved.

PANEL A: INCOME STATEMENTCellular ProductsIncome Statement

For the Year Ended December 31, 2011 (in thousands)Revenues $210,000Costs of goods sold:

Beginning finished goods inventory, January 1, 2011 $22,000Costs of goods manufactured (see Panel B) $104,000Costs of goods available for sale $126,000

Ending finished goods inventory, December 31, 2011 $18,000Cost of goods sold $108,000

Gross margin (or gross profit) $102,000Operating costs

R&D, design, mktg., dist., & cust.-service cost $70,000Total operating costs $70,000

Operating income $32,000

73

74

Other Cost Considerations

© 2012 Pearson Prentice Hall. All rights reserved.

Prime cost is a term referring to all direct manufacturing costs (materials and labor).

Conversion cost is a term referring to direct labor and indirect manufacturing costs.

Overtime labor costs are considered part of indirect

overhead costs.

76

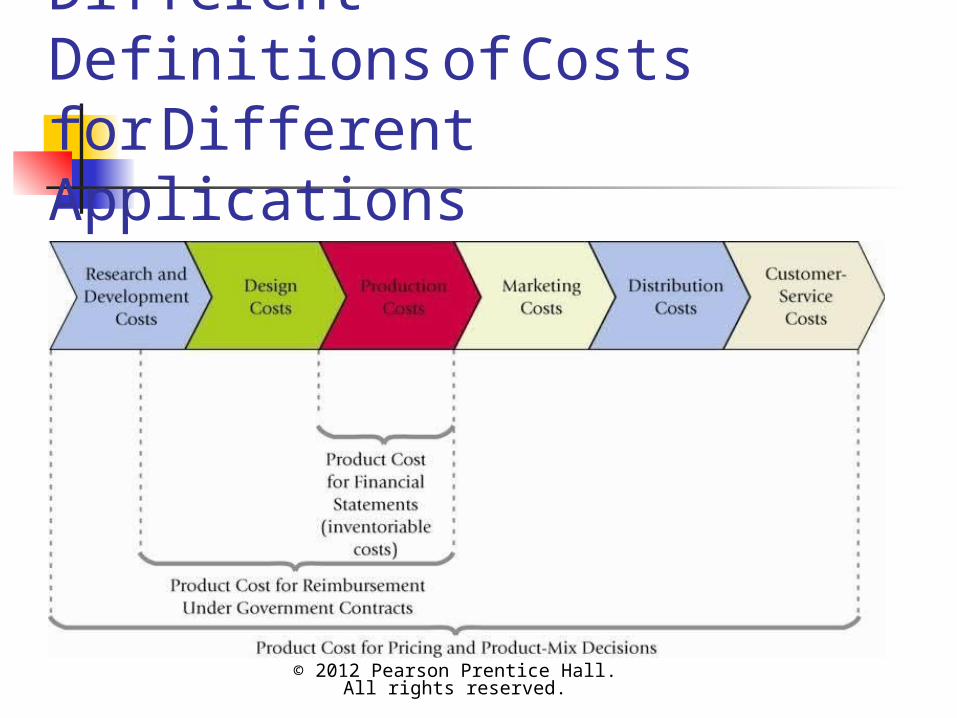

Different Definitions of Costs for Different Applications

© 2012 Pearson Prentice Hall. All rights reserved.

Pricing and product-mix decisions—decisions about pricing and maximizing profits

Contracting with government agencies—very specific definitions of allowable costs for “cost plus profit” contracts

Preparing external-use financial statements—GAAP- driven product costs only

Different Definitions of Costs for Different Applications

© 2012 Pearson Prentice Hall. All rights reserved.

Cost-Volume-Profit Analysis

© 2012 Pearson Prentice Hall. All rights reserved.

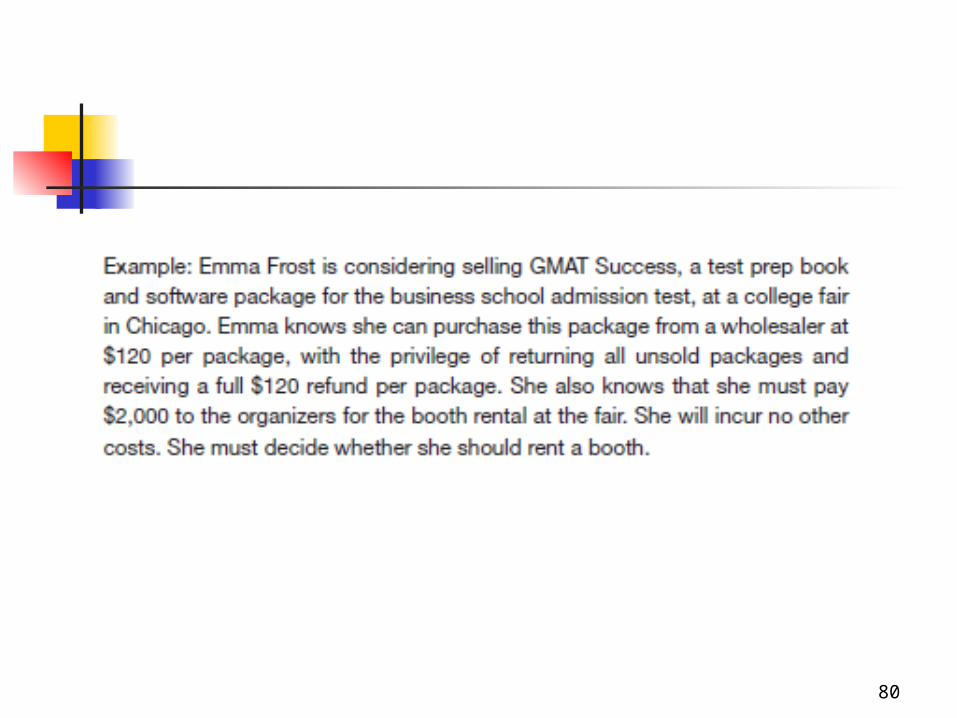

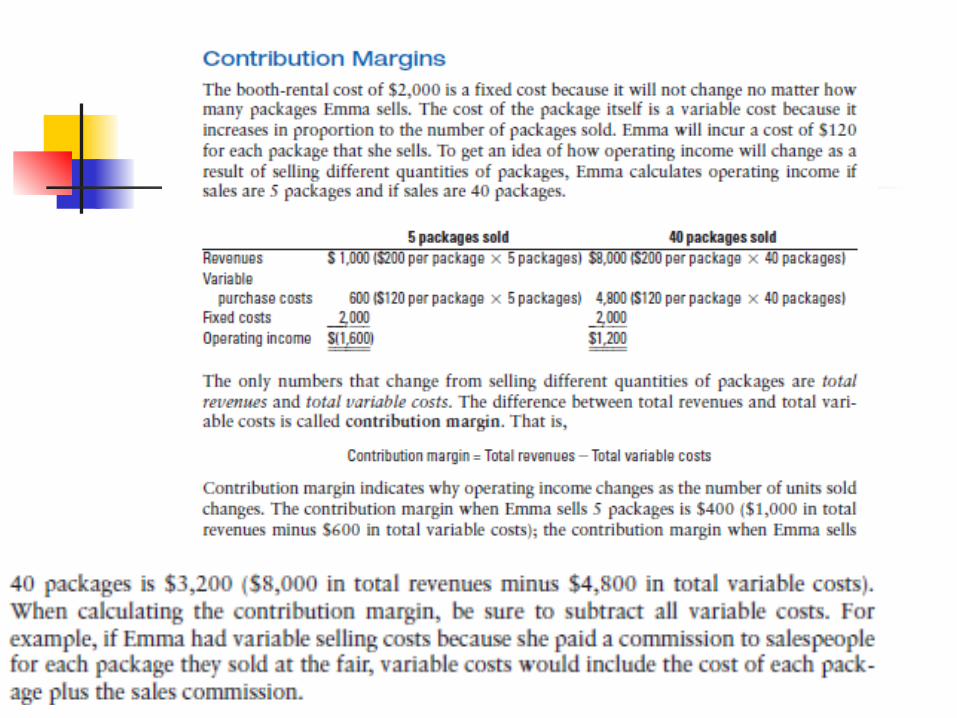

80

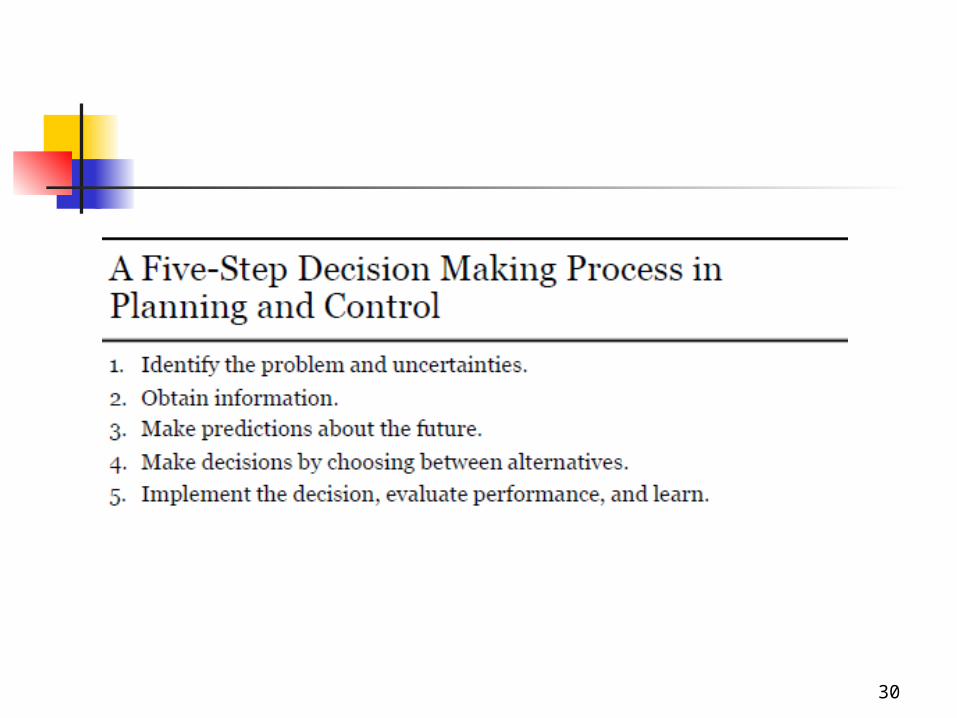

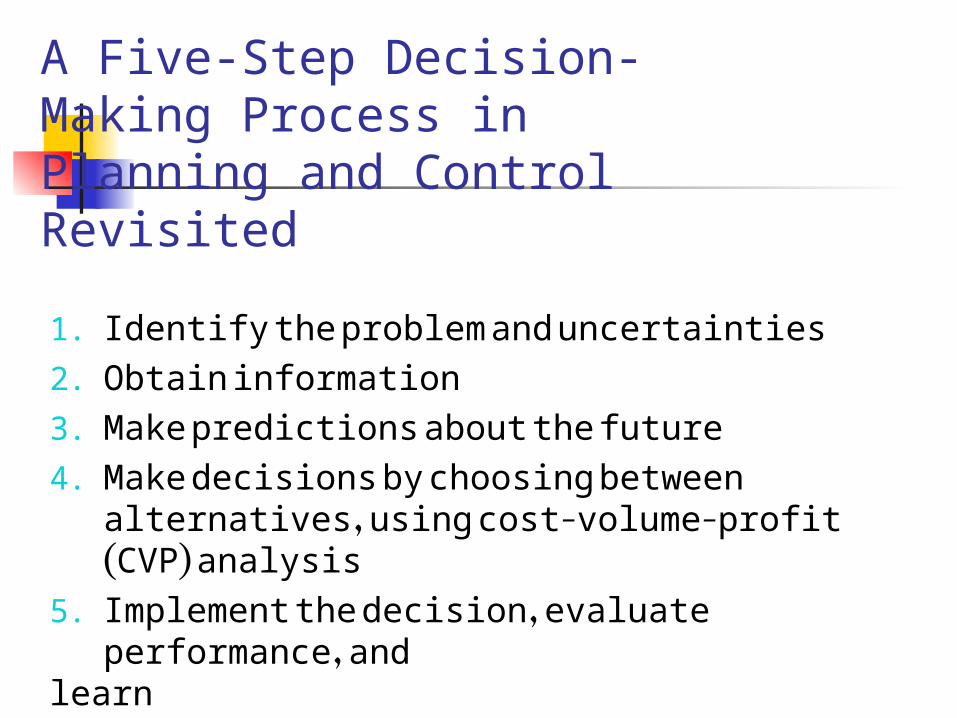

A Five-Step Decision-Making Process inPlanning and Control Revisited

1. Identify the problem and uncertainties2. Obtain information3. Make predictions about the future4. Make decisions by choosing between

alternatives, using cost-volume-profit (CVP) analysis

5. Implement the decision, evaluate performance, and

learn

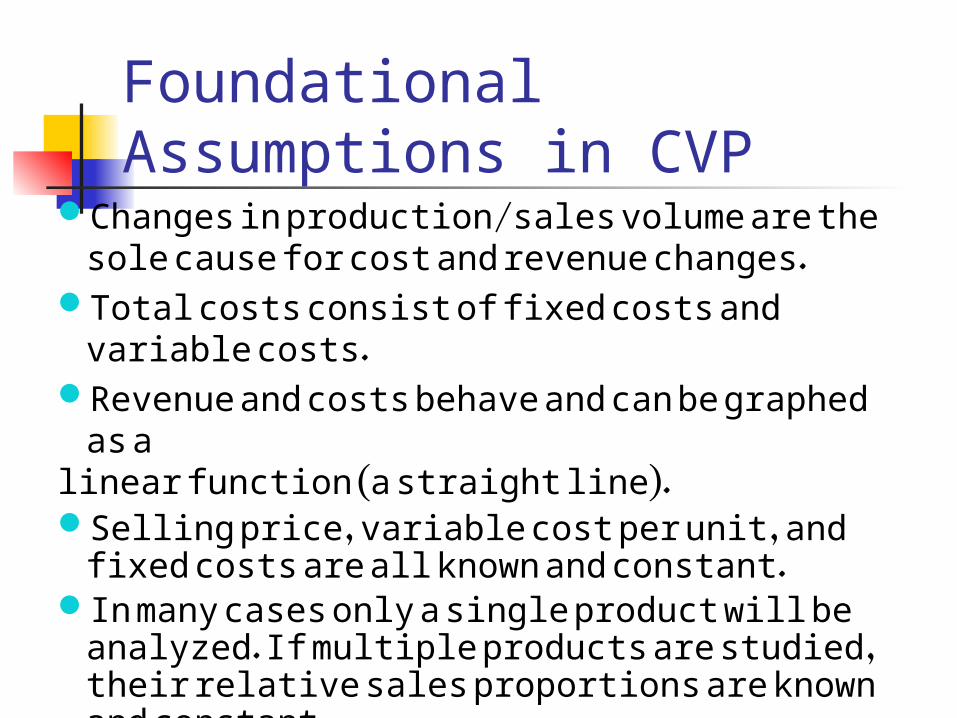

Foundational Assumptions in CVP

Changes in production/sales volume are the sole cause for cost and revenue changes.

Total costs consist of fixed costs and variable costs.

Revenue and costs behave and can be graphed as a

linear function (a straight line).Selling price, variable cost per unit, and fixed

costs are all known and constant.In many cases only a single product will be

analyzed. If multiple products are studied, their relative sales proportions are known and constant.

The time value of money (interest) is ignored.

83

84

85

86

87

88

89

90

Basic Formulae

© 2012 Pearson Prentice Hall. All rights reserved.

CVP: Contribution Margin

© 2012 Pearson Prentice Hall. All rights reserved.

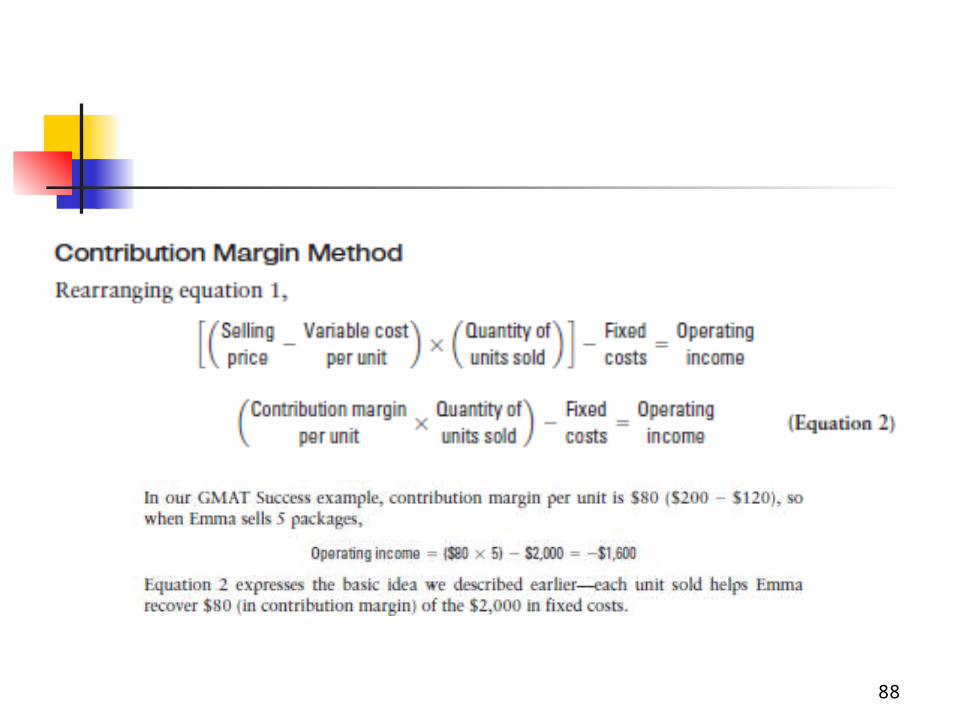

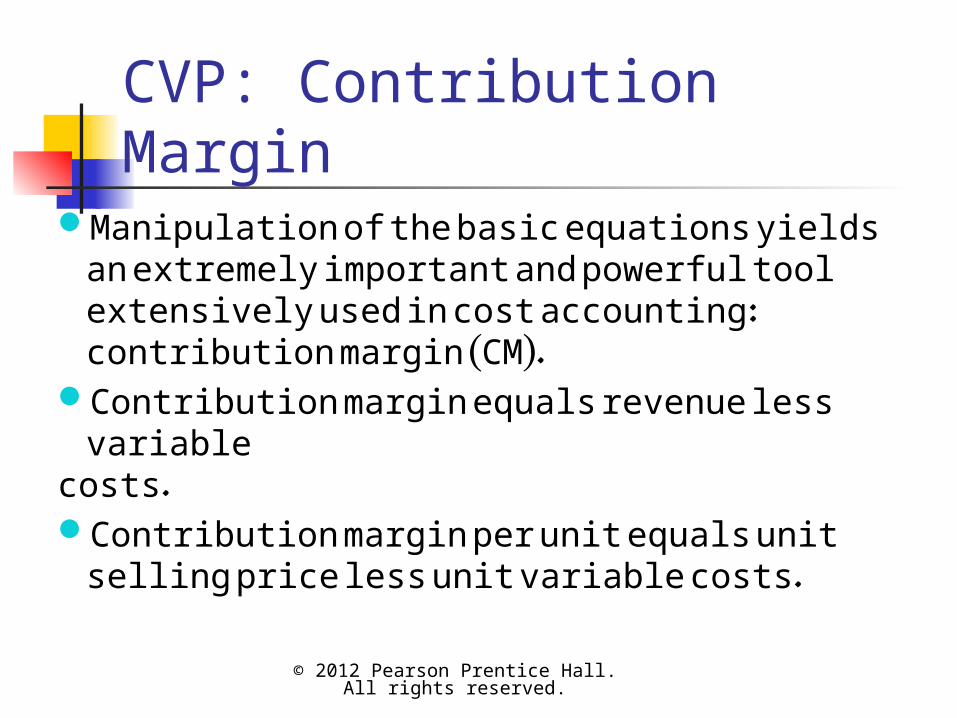

Manipulation of the basic equations yields an extremely important and powerful tool extensively used in cost accounting: contribution margin (CM).

Contribution margin equals revenue less variable

costs.Contribution margin per unit equals unit

selling price less unit variable costs.

Contribution Margin

© 2012 Pearson Prentice Hall. All rights reserved.

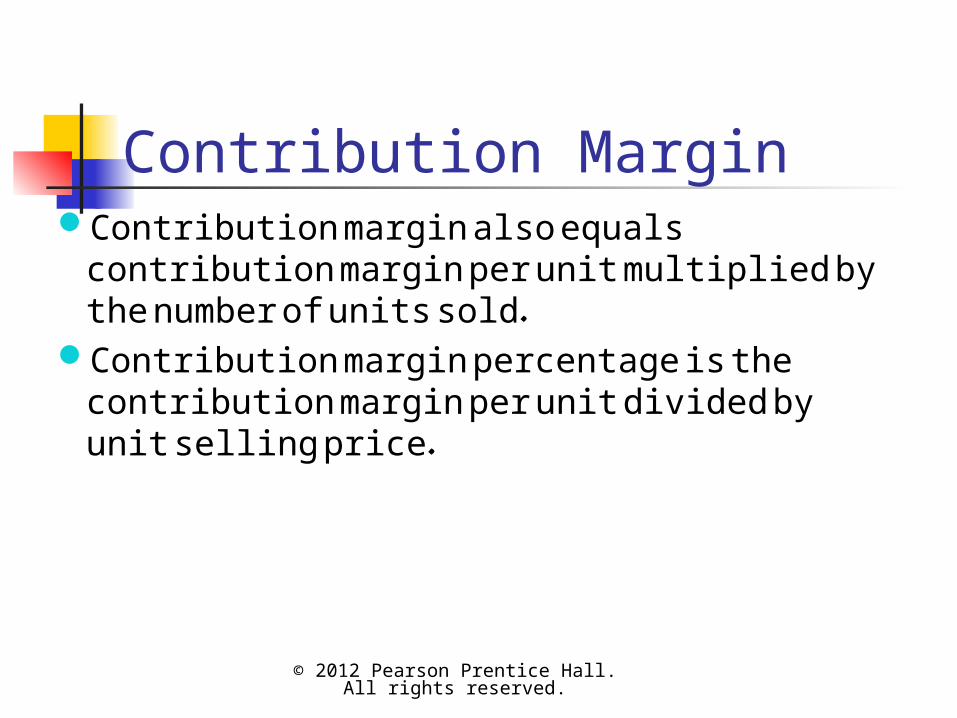

Contribution margin also equals contribution margin per unit multiplied by the number of units sold.

Contribution margin percentage is the contribution margin per unit divided by unit selling price.

Cost–Volume–Profit Equation

© 2012 Pearson Prentice Hall. All rights reserved.

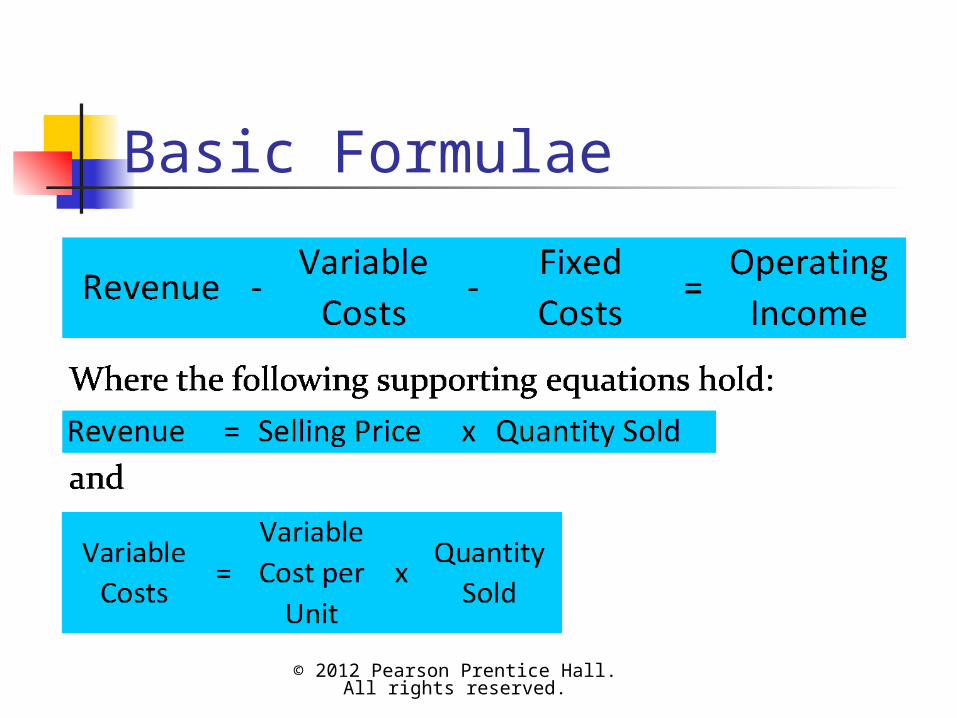

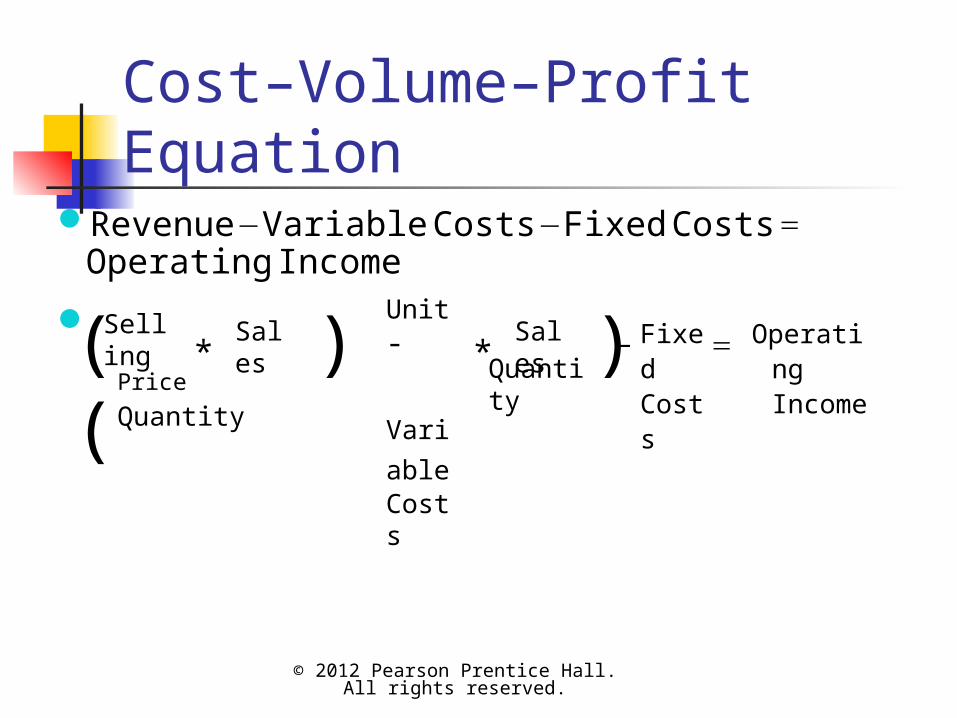

Revenue – Variable Costs – Fixed Costs = Operating Income

Selling

Sales

Price

Quantity

*( ) (

)*Unit-

Varia

bleCosts

SalesQuantit

y

- Fixed Costs

= Operating Income

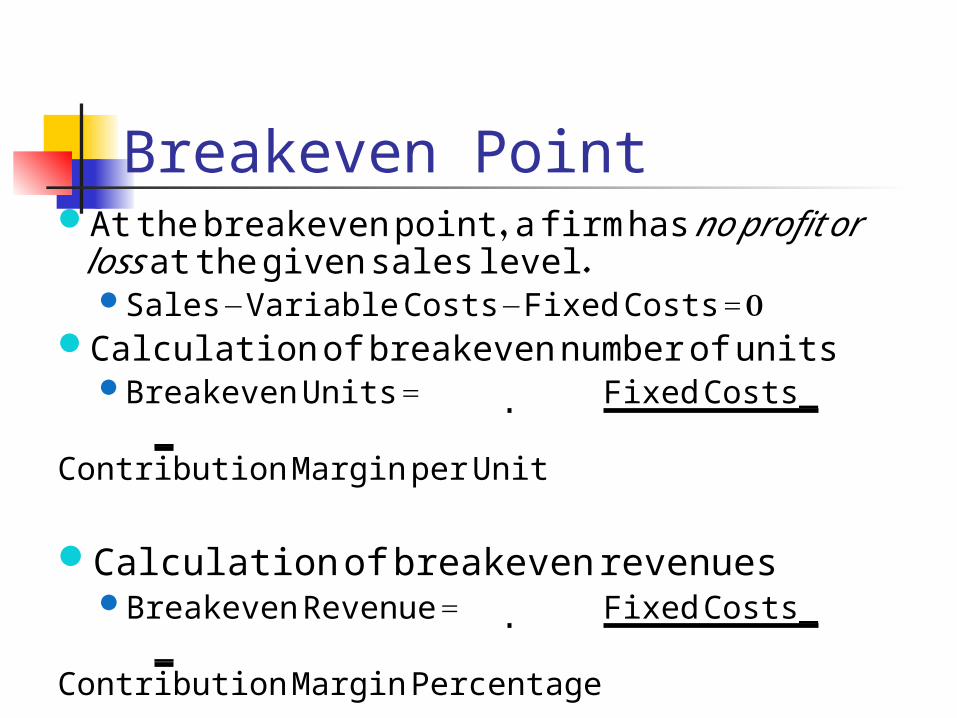

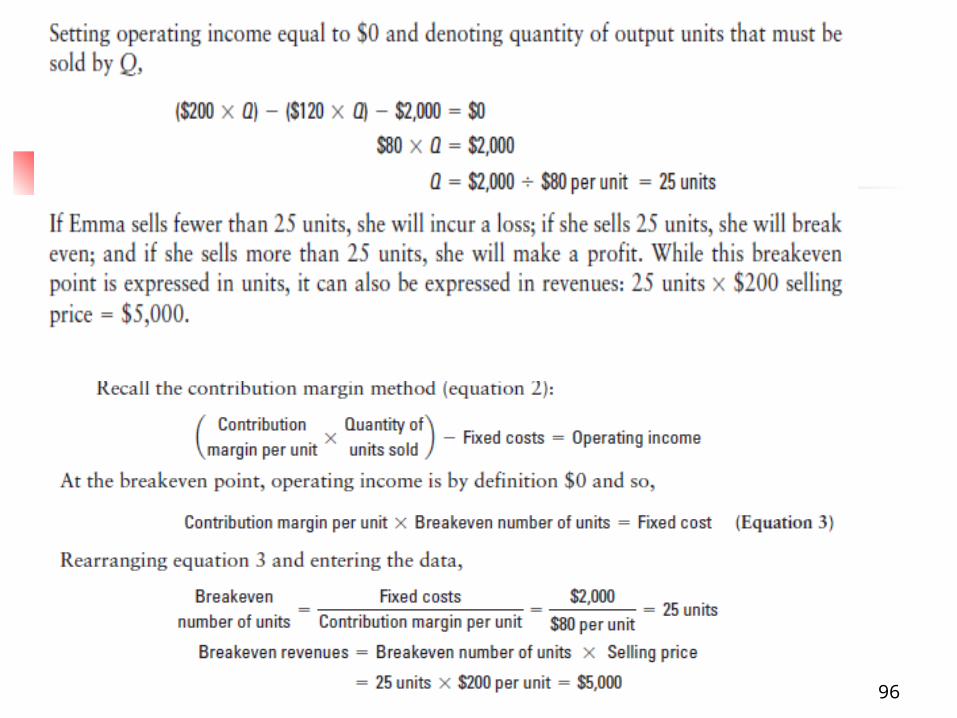

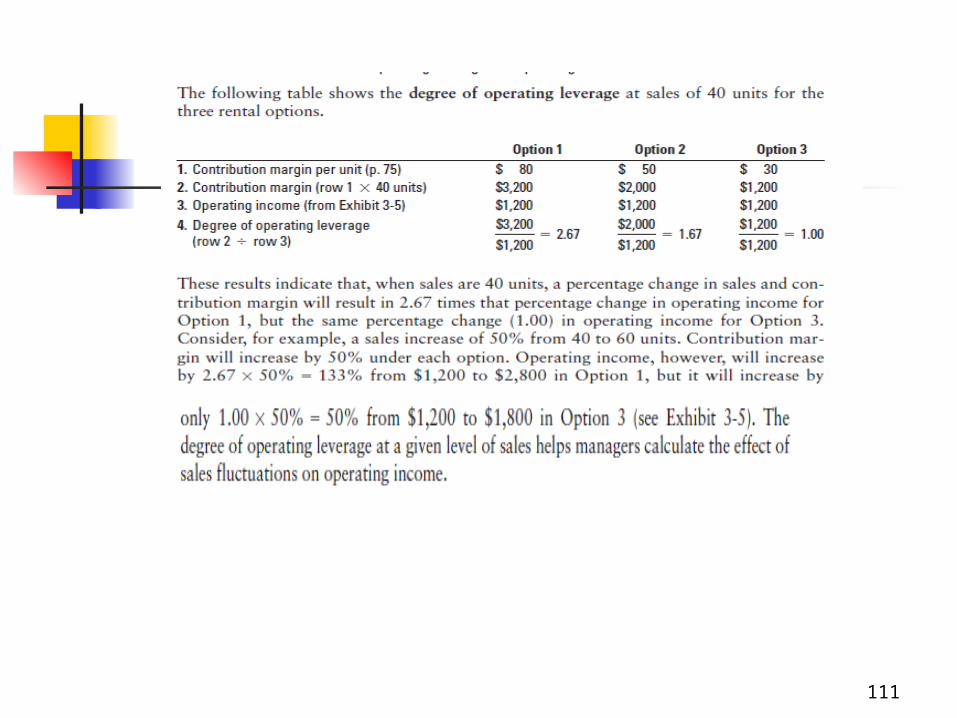

Breakeven PointAt the breakeven point, a firm has no profit or loss at the given sales level.

Sales – Variable Costs – Fixed Costs = 0Calculation of breakeven number of units

Breakeven Units = Fixed Costs__

Contribution Margin per Unit

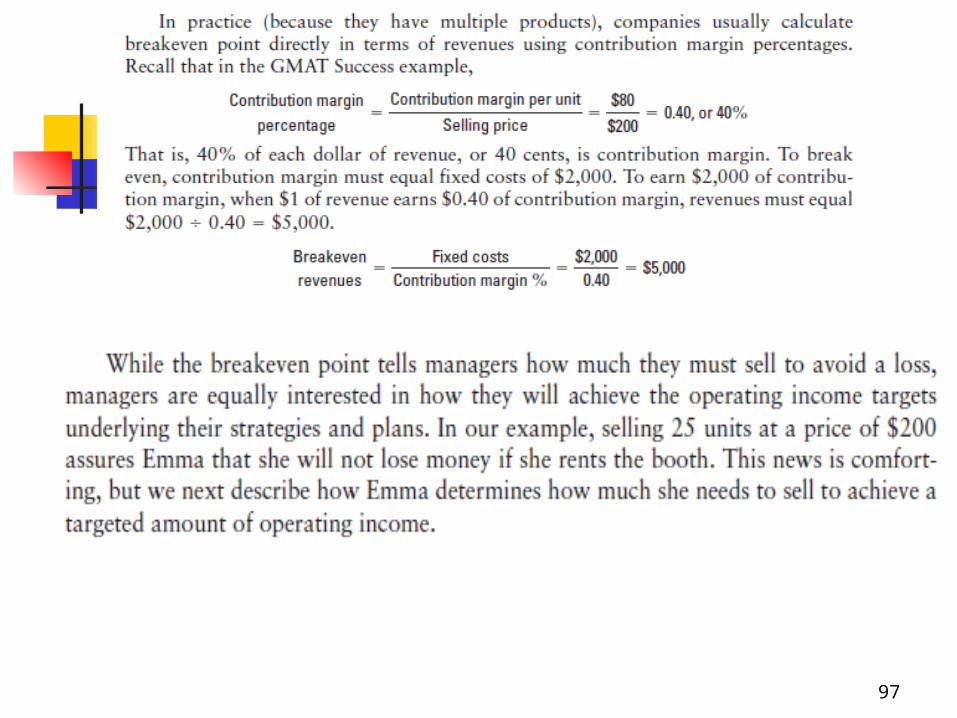

Calculation of breakeven revenuesBreakeven Revenue = Fixed Costs_

_Contribution Margin Percentage

96

97

98

99

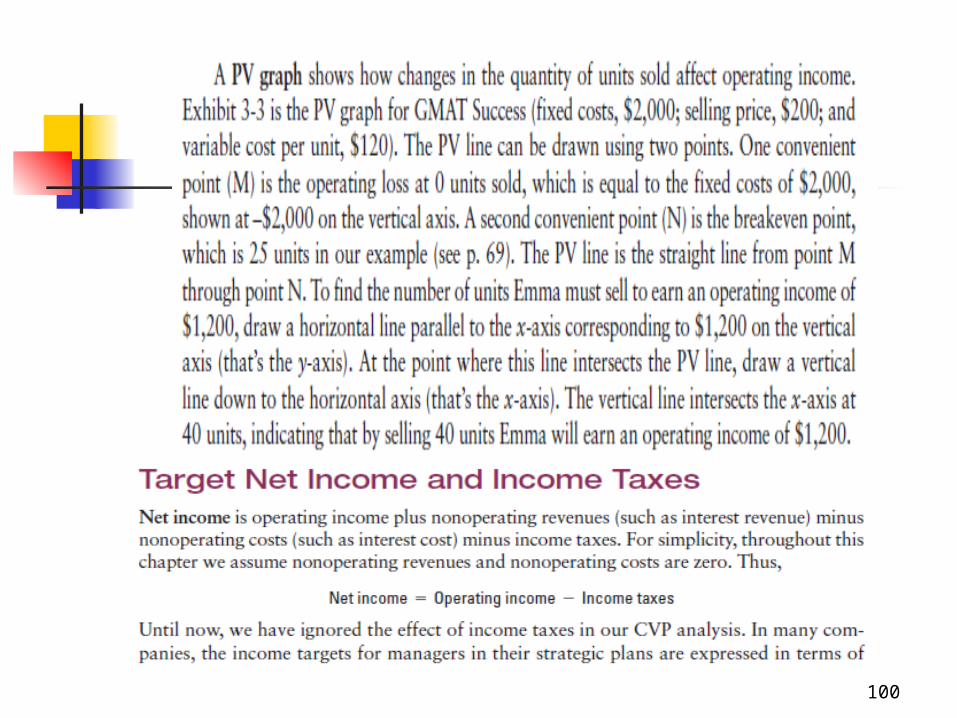

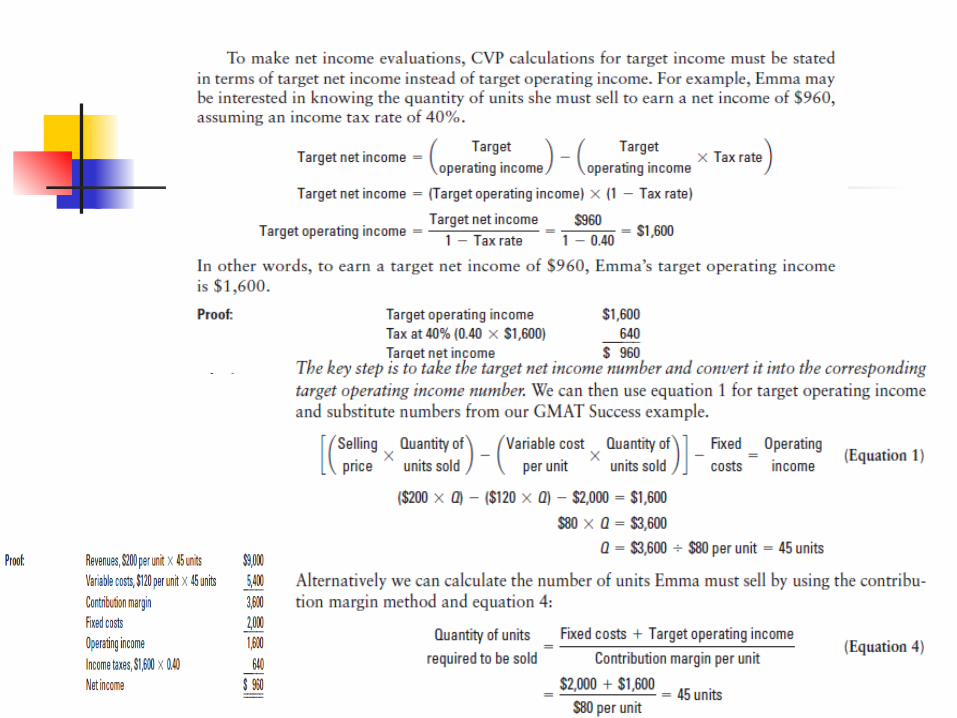

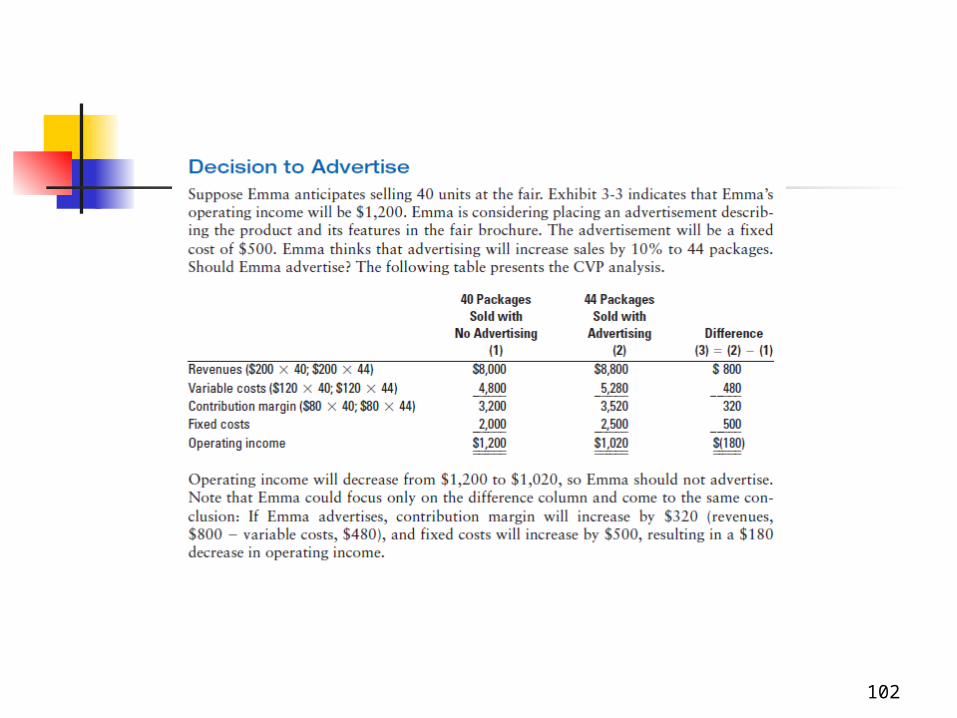

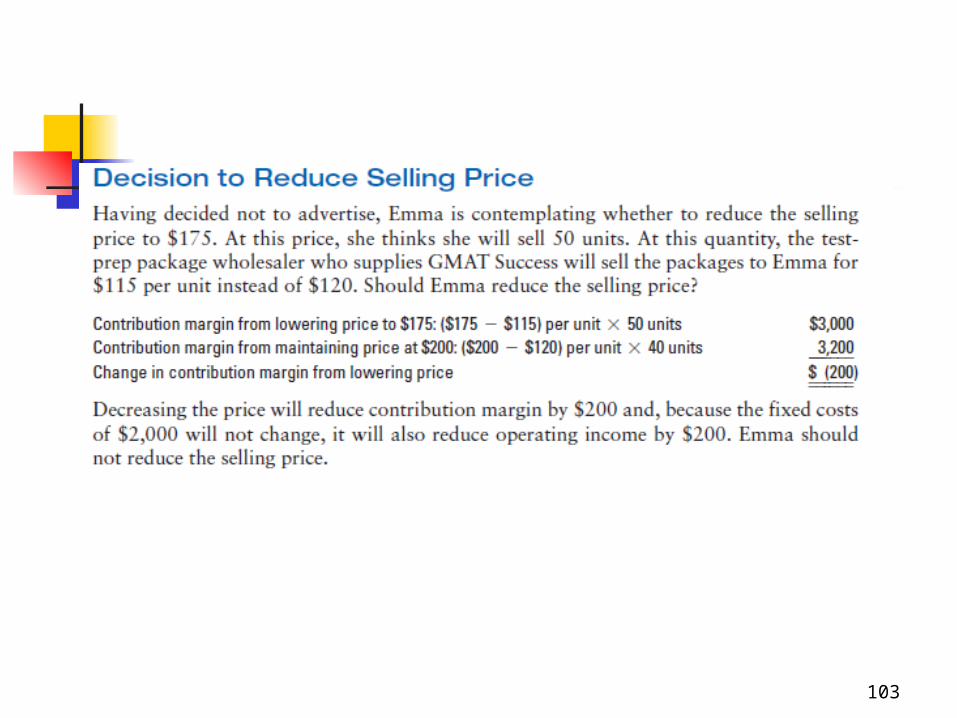

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

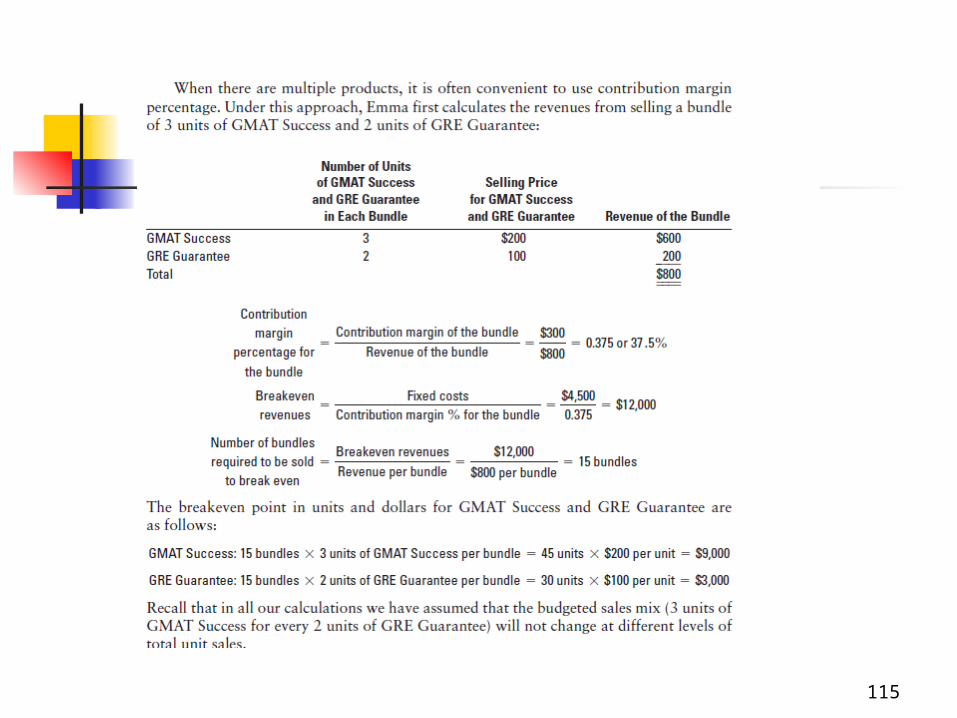

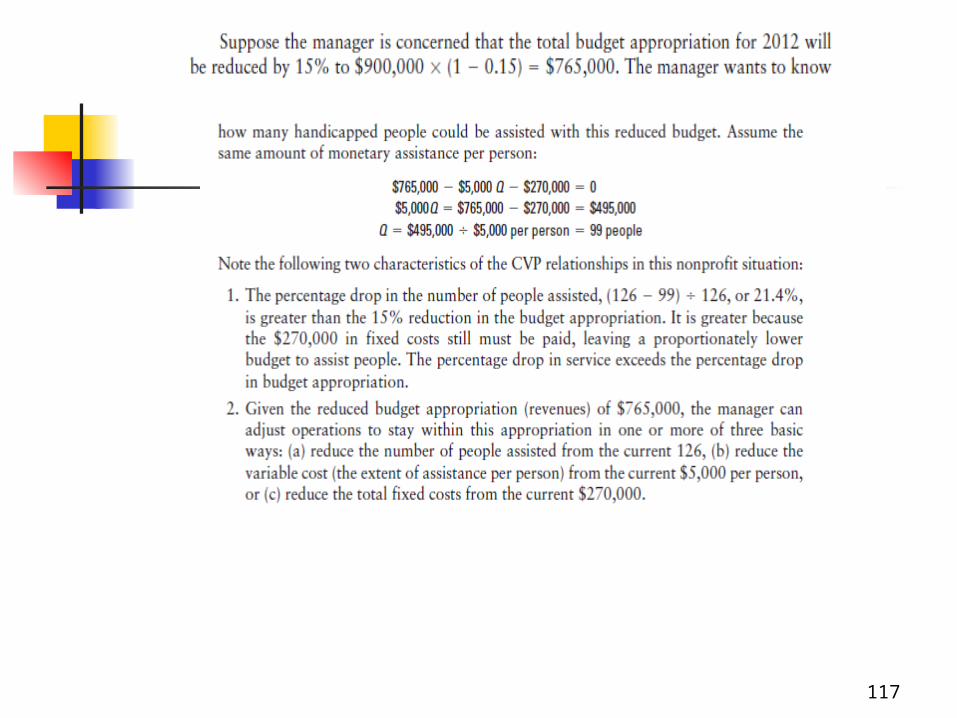

115

116

117

118

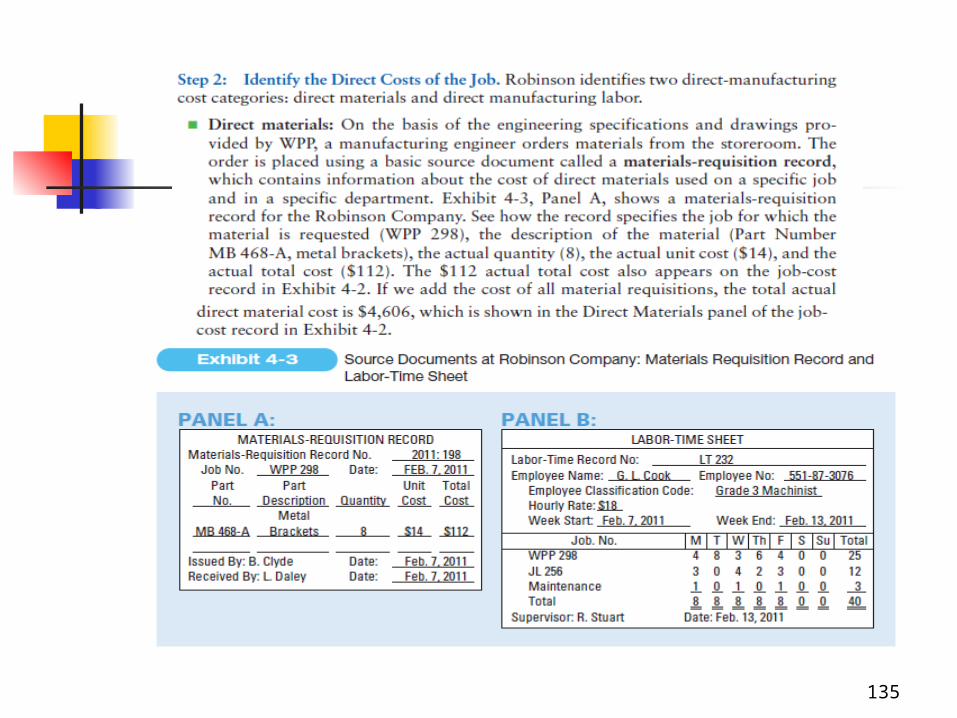

Job Costing

120

121

122

123

124

125

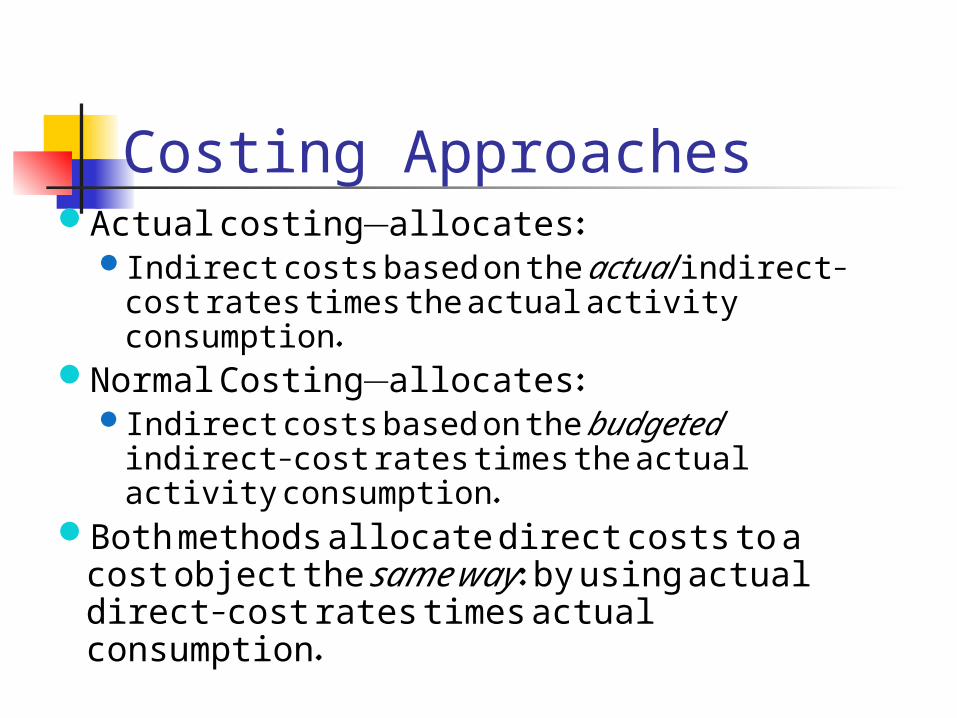

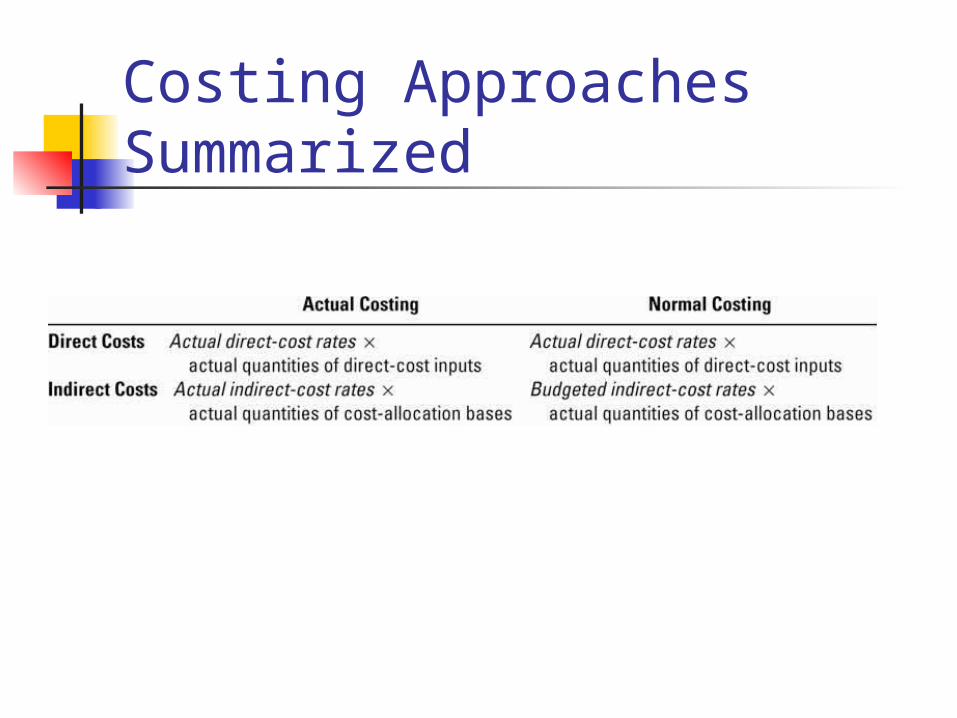

Costing ApproachesActual costing—allocates:

Indirect costs based on the actual indirect-cost rates times the actual activity consumption.

Normal Costing—allocates:Indirect costs based on the budgeted indirect-cost

rates times the actual activity consumption.Both methods allocate direct costs to a cost

object the same way: by using actual direct-cost rates times actual consumption.

127

Costing Approaches Summarized

…logically extendedCost pool—any logical grouping of related

cost objectsCost-allocation base—a cost driver is

used as a basis upon which to build a systematic method of distributing indirect costs.For example, let’s say that direct labor hours cause

indirect costs to change. Accordingly, direct labor hours will be used to distribute or allocate costs among objects based on their usage of that cost driver.

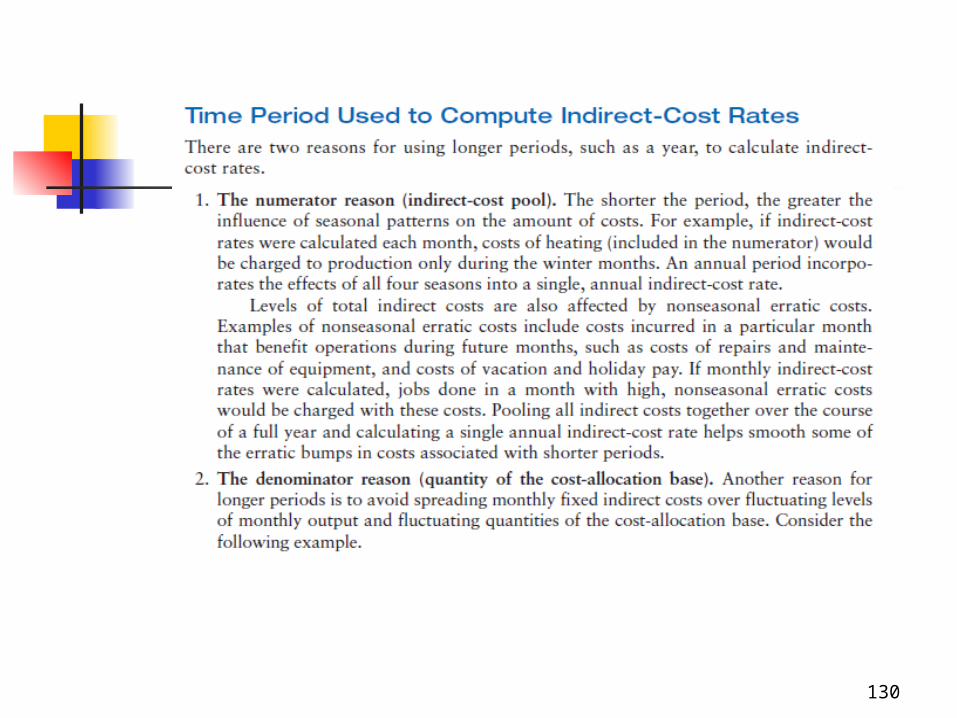

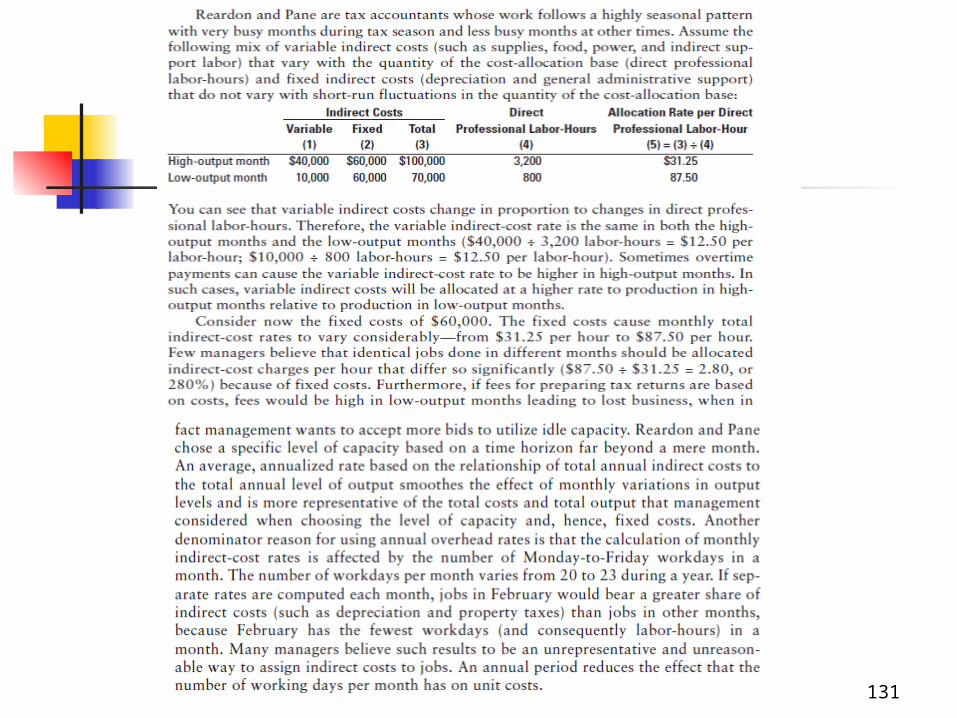

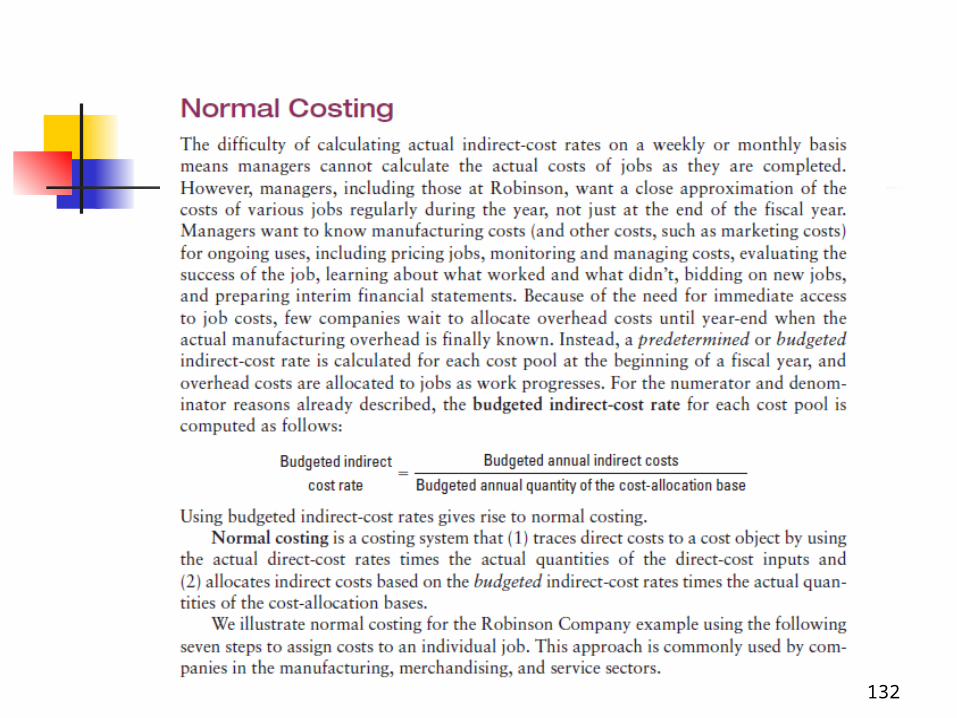

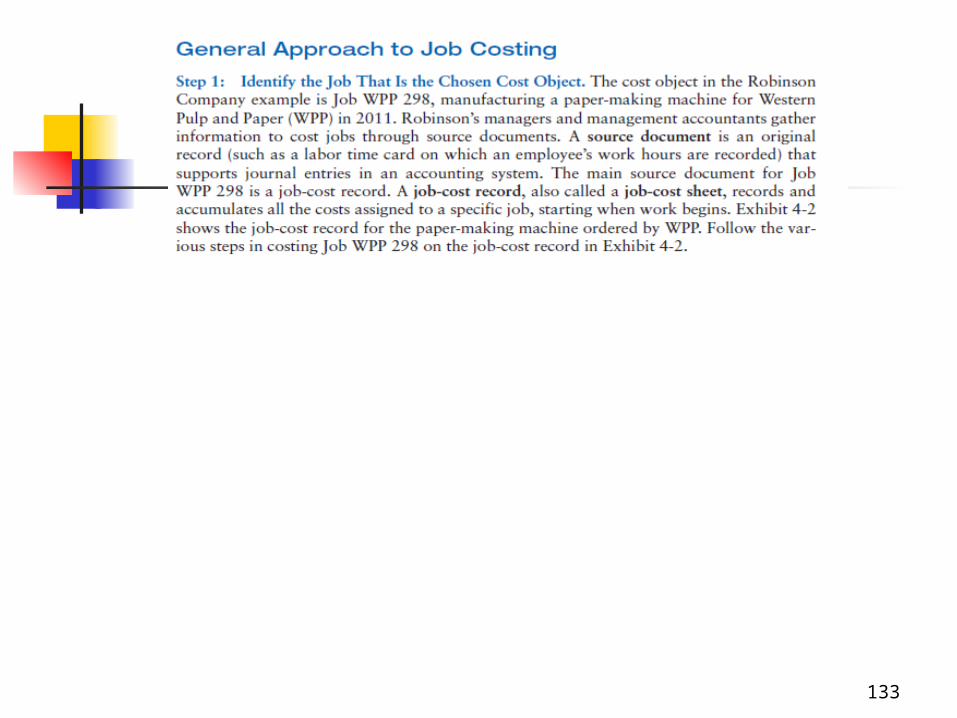

130

131

132

133

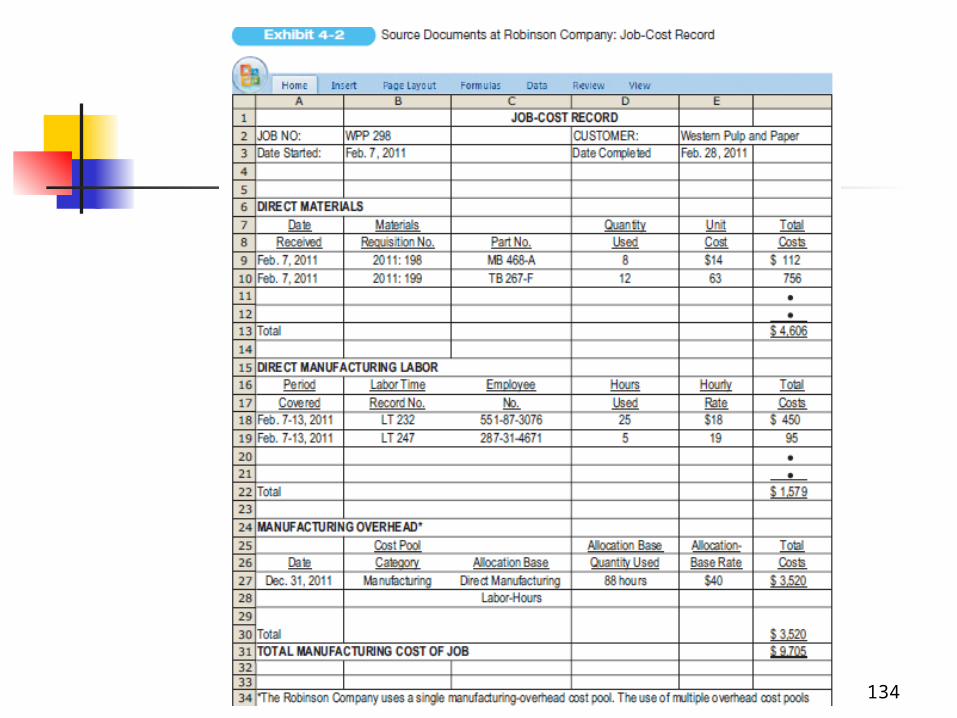

134

135

136

137

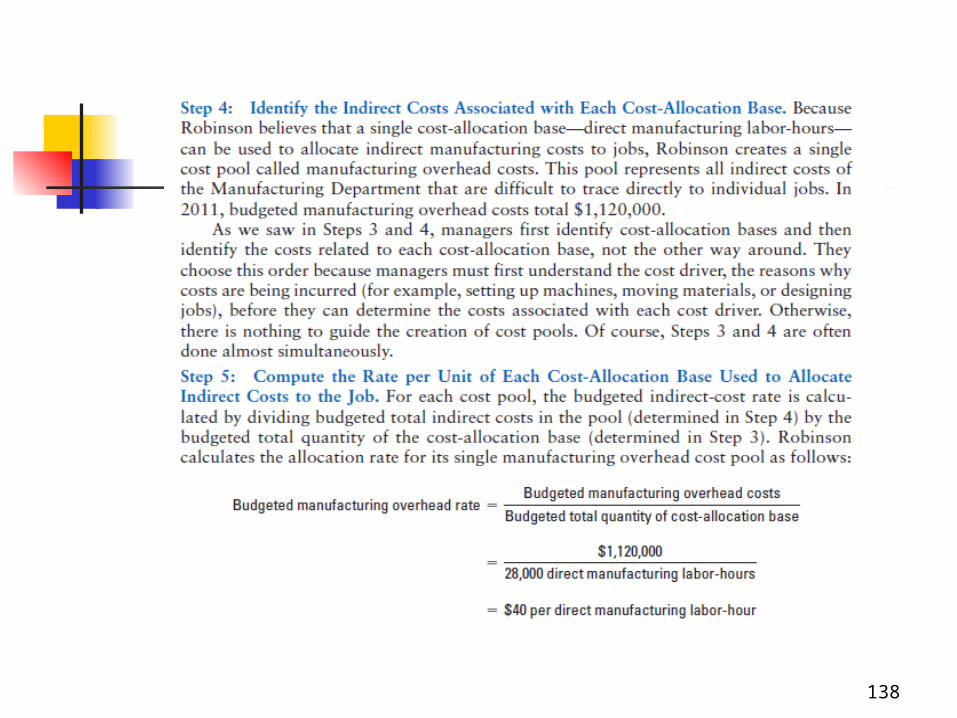

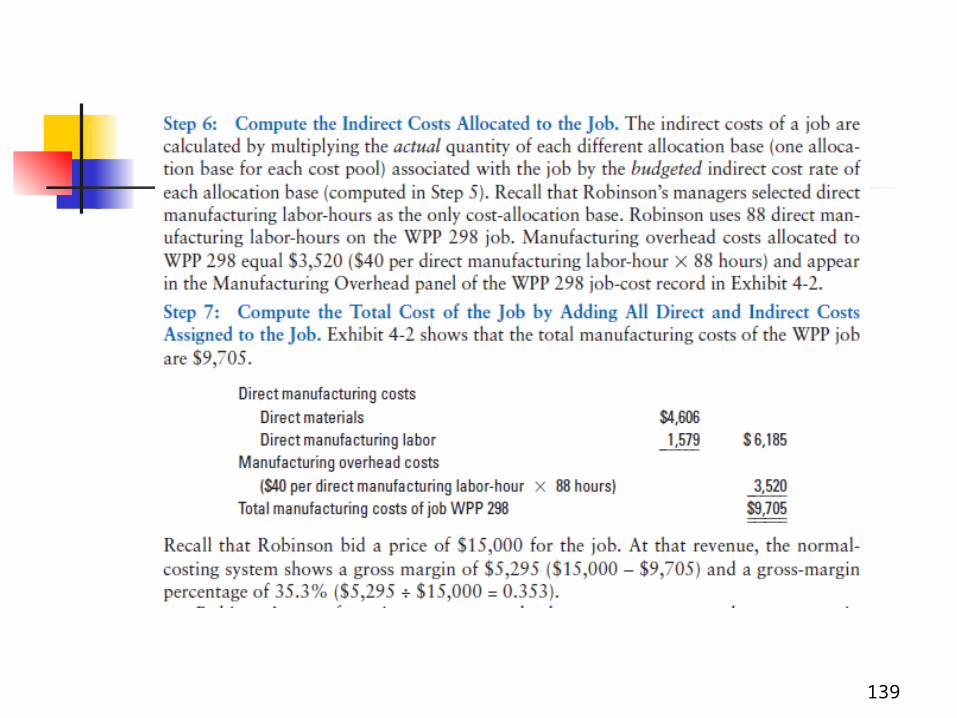

138

139