Chapter 1 Accounting in Action Accounting Principles, 7 th Edition Weygandt Kieso Kimmel.

Upload

john-bensonCategory

view

248download

0

1

Accounting Changes and Error Analysis

Chapter 22

Intermediate Accounting12th & 13th Editions

Kieso, Weygandt, and Warfield

KWW slides Prepared by Coby Harmon, University of California, Santa Barbara as modified by Teresa Gordon,

University of Idaho

4

Restatements are common!

5

Accounting Changes & Corrections

ASC Topic 250 (SFAS No. 154) discusses 3 types of accounting changes plus correction of errors

1. Changes in Accounting Principle

2. Changes in Accounting Estimates

3. Changes in Reporting Entity

4. Errors in Financial Statements

6

Change in accounting principle A change from one generally accepted

principle to another generally accepted accounting principle Only possible where GAAP permits more than

one acceptable choice Definition includes a change in the method of

applying an accounting principle Must be applied consistently after adopted

IMPORTANT NOTE: The change must be justified on the basis that it is preferable to the principle previously followed.

7

Change in accounting principle

A change in accounting principle does NOT include Initial adoption of an accounting principle for a

new event or transaction Modification of an accounting principle made

necessary by transactions clearly different in substance from those previously occurring

A change to a generally accepted principle from an incorrect principle (This is considered the correction of an error)

8

Reporting a change in principle

Retrospective application to all prior periods unless this is impracticable Cumulative DIRECT effect of the change on periods prior

to those presented is reflected on the balance sheet in the amounts reported for assets and liabilities

The offsetting adjustment (if any) is made to the beginning balance of retained earnings for the earliest period presented

Financial statements will be re-stated as though the new principle had been in use

Direct effects include income tax impact

Indirect effects (if actually incurred) are recognized in the period during which the accounting change is made

9

Earliest Year Presented (or affected by change)

Retained Earnings account is shown as follows:

Balance at beginning of year $ XXX

Adjustment for the cumulative

effect on prior years (net of tax) $ XX

Balance at beginning (as adjusted) $ XX

Net Income $ XXX

Less dividends declared - XX

Balance at end of year $ XXX

10

When is a Change in Accounting Principle Appropriate?

Changes are appropriate when the new principle is preferable to the existing accounting principle.

The new principle should result in improved financial reporting.

A change is considered preferable if a FASB standard: creates a new accounting principle, or expresses preference for a new principle, or rejects a specific accounting principle

11

Motivations for Change

Managers and others may have a self- interest in adopting principles or standards: Companies may want to be less politically visible

to avoid regulation A company’s capital structure may affect its

selection of accounting standards Managers may select accounting standards to

maximize their performance-related bonuses Companies have an incentive to manage or

smooth earnings

Illustration: Denson Company has accounted for its income

from long-term construction contracts using the completed-

contract method. In 2010 the company changed to the

percentage-of-completion method. Management believes this

approach provides a more appropriate measure of the income

earned. For tax purposes, the company uses the completed-

contract method and plans to continue doing so in the future.

(We assume a 40 percent enacted tax rate.)

LO 3 Understand how to account for retrospective accounting changes.

Retrospective Accounting Change: Long-Term Contracts

Changes in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting Principle

LO 3

Income statements for 2008–2010

Changes in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting Principle

Illustration 22-1Illustration 22-1

Data for Retrospective Change Example

Changes in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting Principle

Illustration 22-2Illustration 22-2

Construction in Process 220,000

Deferred Tax Liability

88,000

Retained Earnings

132,000LO 3 Understand how to account for retrospective accounting changes.

Journal entry to record change at beginning of 2010:

Reporting a Change in Principle

Changes in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting Principle

LO 3 Understand how to account for retrospective accounting changes.

Major disclosure requirements are as follows.

1. Nature and reason for the change in accounting principle.

2. The method of applying the change, and:

a. A description of the prior-period information that has been

retrospectively adjusted, if any.

b. The effect of the change on income from continuing

operations, net income, any other affected line items.

c. The cumulative effect of the change on retained earnings

or other components of equity or net assets as of the

beginning of the earliest period presented.

Reporting a Change in Principle

Changes in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting Principle

LO 3 Understand how to account for retrospective accounting changes.

Illustration 22-3Illustration 22-3

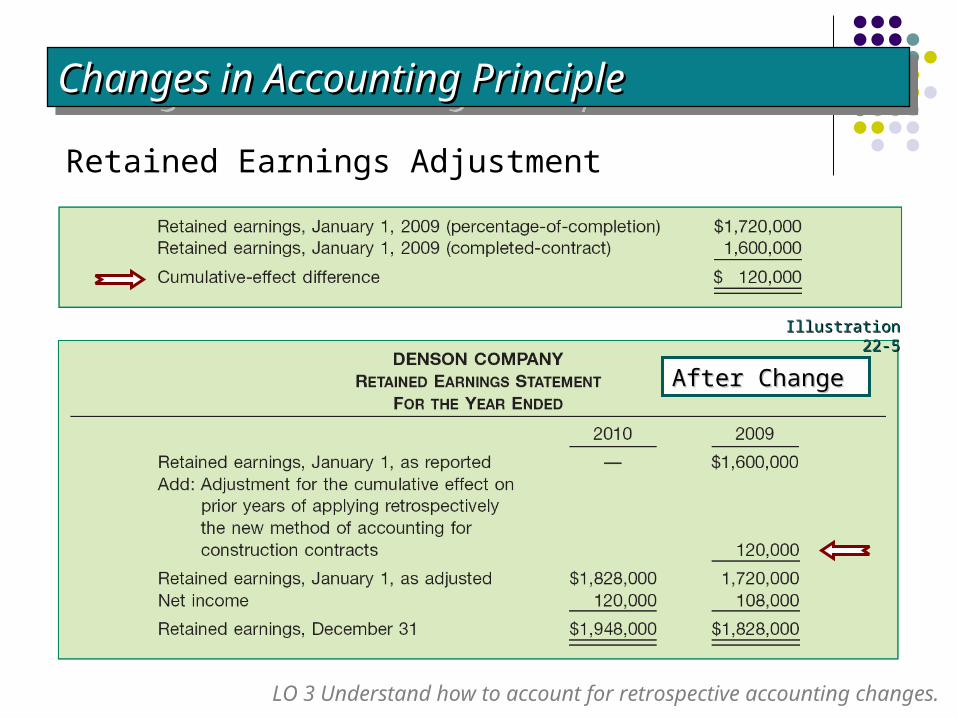

Retained Earnings Adjustment

Changes in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting Principle

LO 3 Understand how to account for retrospective accounting changes.

Illustration 22-4Illustration 22-4

Assuming a retained earnings balance of $1,360,000 at the

beginning of 2008.

Before ChangeBefore Change

Retained Earnings Adjustment

Changes in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting PrincipleChanges in Accounting Principle

LO 3 Understand how to account for retrospective accounting changes.

Illustration 22-5Illustration 22-5

After ChangeAfter Change

19

Changes in accounting estimates

Current and prospective method

20

Many amounts on FS involve estimates, including:Many amounts on FS involve estimates, including:

1. Uncollectible receivables.

2. Inventory obsolescence.

3. Useful lives and salvage values of assets.

4. Periods benefited by deferred costs.

5. Liabilities for warranty costs and income taxes.

6. Recoverable mineral reserves.

7. Change in depreciation methods.

21

Change in Estimate

Estimates that are later determined to be incorrect should be corrected as changes in estimates Result from availability of new or additional

information

Companies report prospectively changes in accounting estimates.

22

Change in Estimate

Sometimes effected in the form of a change in accounting principle Bad debt accounting – change from percentage of

sales method to aging of accounts receivable (allowance) method

Fixed assets – change from sum-of-year’s-digits depreciation to straight-line depreciation

23

Changes in Accounting Estimates

Are handled with what used to be called the current and prospective method This means that we do not go back and change

previously reported numbers on the financial statements (no retroactive restatement)

We make changes to current and future years only

Two numeric examples Depreciation expense Depletion expense

24

Asset cost $240,000Estimated residual value $40,000Estimated service life 5 years

Depreciation Example

Consider these facts related to an asset acquired January 1, 2010:

The company uses straight-line depreciation Assume that after 2 years, it becomes obvious that the

asset will be used for a total of 8 years At the end of 8 years, it will be worth $10,000 What depreciation expense should be recorded for 2012?

25

160,000 -10,000 = 6

$240,000

YearDepreciation

Book value at end of year

2010 40,000$ $200,0002011 40,000$ $160,000

2012 25,000$ $135,000

2013 25,000$ $110,0002014 25,000$ $85,0002015 25,000$ $60,0002016 25,000$ $35,0002017 25,000$ $10,000

$240,000 - 40,000- 40,000 =$160,000

Carrying Value

Solution

8 - 2

new estimate

$ 25,000

26

Alternate treatment

If we had originally known new facts:

We would have had $57,500 in accumulated depreciation at end of 2011.

Actually in acc’d depreciation = $80,000 Make adjusting JE and then continue with

$28,750 depreciation for remaining useful life

240,000 -10,000 = $28,750 8

27

Alternate treatment

2012Correcting JE:

Acc’d Depr 22,500 Depr Exp 22,500

Record 2012 depreciation:

Depr Exp 28,750

Acc’d Depr 28,750

240,000 -10,000 = $28,750 8

$240,000

YearDepreciation

Book value at end of year

2010 40,000$ $200,0002011 40,000$ $160,000

2012 6,250$ $153,750

2013 28,750$ $125,0002014 28,750$ $96,2502015 28,750$ $67,5002016 28,750$ $38,7502017 28,750$ $10,000

28

Example - Coal Mine Cost of property $9,000,000 Cost to restore property $1,200,000* Value after restoration $1,000,000 Recoverable resources 4,000,000 tons First year production 150,000 tons Sold for $30 per ton

* Present value (asset retirement obligation measured in accordance with SFAS No. 143)

Statutory depletion rate for tax purposes = 10%

29

Cost basis + cost to restore - residual value after restoration Total estimated recoverable units

$9,000,000 + 1,200,000 - 1,000,000 = 4,000,000 tons $2.30 per ton

Sold 150,000 tons, therefore cost depletion = 150,000 * 2.30 = $345,000

Coal mine example:

30

Coal mine example, continued

Assume that 250,000 tons of coal were produced and sold during the second year of operation

However, new EPA regulations increased the projected restoration costs to $2,000,000 (asset retirement obligation)

At the beginning of the second year of production, geologist estimate 4,050,000 tons remain

We start over estimating the depletion rate per ton -- using the current BOOK VALUE instead of cost

31

Coal Mine Example

Cost basis + cost to restore - residual value after restoration Remaining recoverable units (estimated)

Cost basis is now $9,000,000 - $345,000 = $8,655,000

The cost to restore is now $2,000,000

The new estimate of recoverable units (including 2nd year’s production) is 4,050,000 tons(3,800K left + 250K mined this year)

$8,655,000 + $2,000,000 - $1,000,000 = $2.38 per ton 4,050,000

250,000 tons * $2.38 = $595,000 depletion expense

32

Statutory Depletion

Note that the tax deduction would be much higher using statutory depletion allowance (a permanent difference between accounting and tax return)

Year 1 - 150,000 tons * $30 per ton = $4,500,000 revenue * 10% statutory rate = $450,000 on tax deduction vs. $345,000 on income statement

Year 2 - 250,000 tons * $33 per ton = $8,250,000 Revenue * 10% statutory rate =

$825,000 tax deduction vs. $595,000 on income statement

33

Disclosure of Changes in Estimate

Not required for routine changes in estimate that happen every year Allowance for uncollectible accounts Inventory obsolescence Warranty obligations

UNLESS material If material, the change in estimate should be

discussed in footnotes to financial statements with per share disclosures

34

Other Changes & Corrections

Change in Entity

Correction of Error

35

Reporting a Change in Entity

The reporting entity changes Financial statements are restated for all prior

periods presented Examples of a change in reporting entity are:

Consolidated statements in lieu of individual financials

Loss in control of formerly consolidated subsidiary Acquisition or sale of subsidiaries

36

Reporting the Correction of an Error

Corrections are treated as prior period adjustments to retained earnings for the earliest period being reported

Examples of accounting errors include: A change from an accounting principle that is not generally

accepted to one that is accepted Mathematical errors Changes in estimates that were not prepared in good faith A failure to properly accrue or defer expenses or revenues A misapplication or omission of relevant facts

37

Restatement Example

ASC 250-10-55-2 (SFAS No. 154, Appendix A)

Illustration 1 - detailed example of a change from LIFO to FIFO inventory method

Shows extensive disclosures that would be needed to communicate impact on balance sheet, income statement, and statement of cash flows

38

Error Analysis in General

Firms do not correct errors that are insignificant. Three questions must be answered in this regard:

1. What type of error is involved?

2. What correcting entries are needed?

3. How are financial statements to be restated? Error corrections are reported as prior period

adjustments to the beginning retained earnings balance in the current year

39

A. Change in Accounting Estimate (prospectively)B. Change in Accounting Principle (retroactively or

disclosed)C. Change in Accounting Entity (retroactively)D. Correction of an Error (retroactively)

1. Change in a plant asset’s salvage value.

2. Change due to overstatement of inventory

4. Change from presenting unconsolidated financial statements to consolidated financial statements

5. Change from LIFO to FIFO inventory method

Accounting ChangesAccounting Changes

3. Change from sum-of-years’-digits to straight-line depreciation method

6. Change in rate used to compute warranty costs

40

7. Change from an unacceptable to an acceptable accounting principle

9. Change from completed contract to percentage of completion accounting for long-term contracts

10. Change from FIFO to LIFO inventory method

Accounting ChangesAccounting Changes

8. Change in a patent’s amortization period

11. Change from allowance method to the percentage of sales method to account for bad debt expense

A. Change in Accounting Estimate (prospectively)B. Change in Accounting Principle (retroactively or

disclosed)C. Change in Accounting Entity (retroactively)D. Correction of an Error (retroactively)