1 7 th Annual Gas & Power Institute September 4-5, 2008 Managing “Gap Risk” Between Standard...

51

1 7 th Annual Gas & Power Institute September 4-5, 2008 Managing “Gap Risk” Between Standard Form Trading Agreements Craig R. Enochs Craig R. Enochs [email protected] Jackson Walker L.L.P. 1401 McKinney, Suite 1900 Houston, Texas 77010 (713) 752-4200 phone

-

Upload

jayson-wilcox -

Category

Documents

-

view

218 -

download

0

Transcript of 1 7 th Annual Gas & Power Institute September 4-5, 2008 Managing “Gap Risk” Between Standard...

1

7th Annual Gas & Power Institute

September 4-5, 2008

Managing “Gap Risk” Between Standard FormTrading Agreements

Craig R. Enochs

Craig R. Enochs [email protected]

Jackson Walker L.L.P.1401 McKinney, Suite 1900

Houston, Texas 77010(713) 752-4200 phone

* 2

Selected Sources of “Gap Risk”

I. Issues Common to the NAESB, ISDA, EEI and CTAA. Notices

B. Events of Default

C. Setoff

II. Other Agreement Differences:A. Termination, Liquidation & Settlement: NAESB, ISDA and EEI

B. Confirmation Procedures: NAESB, ISDA and CTA

C. Netting: NAESB and ISDA

D. Transfer and Assignment: CTA and ISDA

3

I. Issues Common to the

NAESB, ISDA, EEI and CTA

A. Notices

B. Events of Default

C. Setoff

4

A. Notices1. NAESB § 9

Methods: Fax, mutually-accepted electronic means, overnight courier, first class mail or hand delivery

General Rule: deemed delivered when received on a Business Day

If no proof of actual receipt, the following presumptions apply: Fax: deemed delivered when sending party receives fax machine’s

confirmation of successful transmission. If after 5:00 p.m., deemed received the following Business Day

Overnight Courier or Mail: deemed delivered on following Business Day after sent, or earlier if confirmed by receiving party

First Class Mail: deemed delivered five (5) Business Days after mailing

5

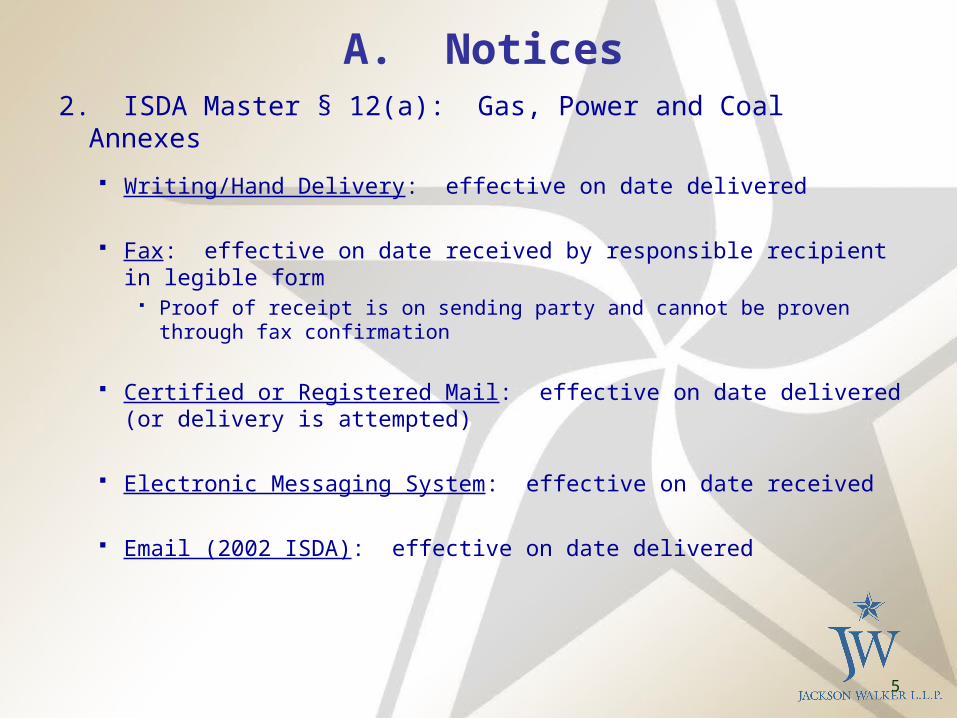

A. Notices2. ISDA Master § 12(a): Gas, Power and Coal Annexes

Writing/Hand Delivery: effective on date delivered

Fax: effective on date received by responsible recipient in legible form

Proof of receipt is on sending party and cannot be proven through fax confirmation

Certified or Registered Mail: effective on date delivered (or delivery is attempted)

Electronic Messaging System: effective on date received

Email (2002 ISDA): effective on date delivered

6

A. Notices

2. ISDA Master § 12(a): Gas, Power and Coal Annexes (cont.)

If notice (i) not delivered on Local Business Day, or (ii) is delivered after close of business, notice deemed delivered on following Local Business Day

Notices relating to Events of Default or Termination Events may not be sent by electronic messaging system (1992/2002), fax (1992) or email (2002 ISDA).

7

A. Notices

3. EEI § 10.7

Fax or Hand Delivery:

If received during business hours on a Business Day, notice deemed effective at the close of business on such day

If received after business hours, deemed effective at close of business on following Business Day

Overnight Courier or U.S. Mail:

Deemed effective on the following Business Day after sent

8

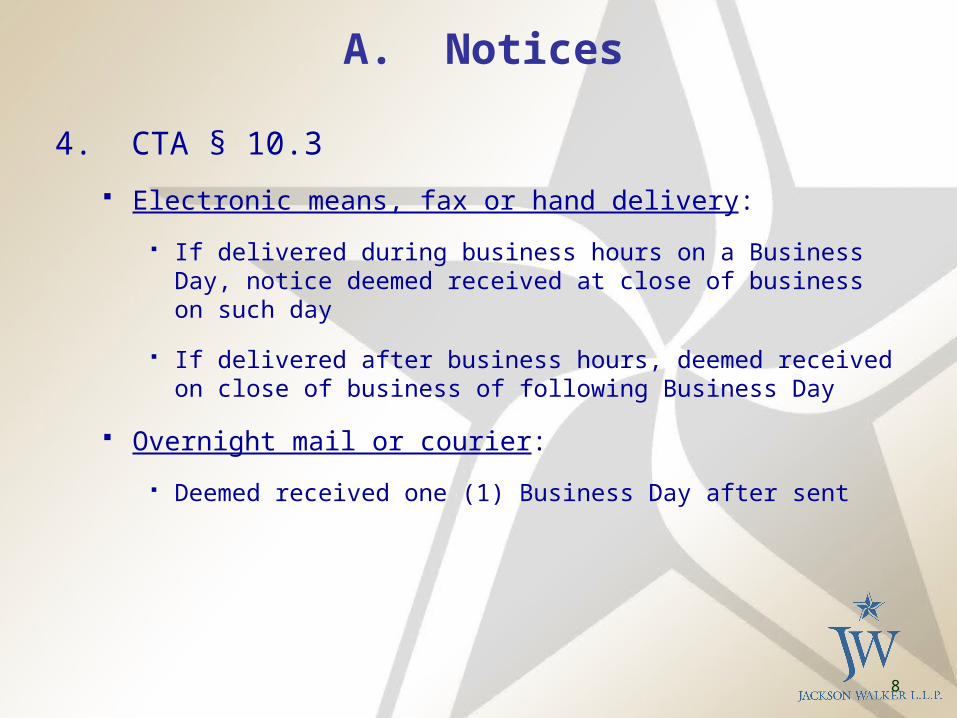

A. Notices

4. CTA § 10.3

Electronic means, fax or hand delivery:

If delivered during business hours on a Business Day, notice deemed received at close of business on such day

If delivered after business hours, deemed received on close of business of following Business Day

Overnight mail or courier:

Deemed received one (1) Business Day after sent

9

A. Notices

5. Risk Analysis

Operational Risk:

Various methods of notice permitted in trading contracts

Ex: ISDA contemplates electronic means, including email (2002 ISDA), but EEI does not contemplate electronic means unless otherwise elected by the parties

Inconsistent notice provisions across trading agreements

More likely that manner or method of notice may be insufficient

* 10

A. Notices5. Risk Analysis (cont.)

Credit and Payment Risk: Ineffective notice may create credit risk as to a defaulting

counterparty:

Ex: ISDA does not allow electronic means (1992/2002), fax (1992) or email (2002) notices with respect to Events of Default or Termination Events

If notice is ineffective, Non-Defaulting Party cannot declare an Early Termination Date

Parties should consider consistent notice provisions across trading contracts

* 11

B. Events of Default

1. 2002 v. 2006 NAESB: § 10.2

2002 and 2006 NAESB: each includes the following Events of Default:

Failure to pay Bankruptcy Default under Credit Support Obligations

2006 NAESB: adds “Additional Event of Default,” which may be elected on Cover Sheet

Indebtedness Cross Default: party or Guarantor defaults on agreements relating to indebtedness for borrowed money

Transactional Cross Default: party or Guarantor defaults under a Specified Transaction.

12

B. Events of Default

1. 2002 v. 2006 NAESB: § 10.2 (cont.)

Risk Analysis:

Additional Events of Default in 2006 NAESB mitigate credit and commercial risks by looking to performance of obligations outside the NAESB

2006 NAESB closes some “gap risk” by moving the 2002 NAESB closer to the EEI and ISDA

13

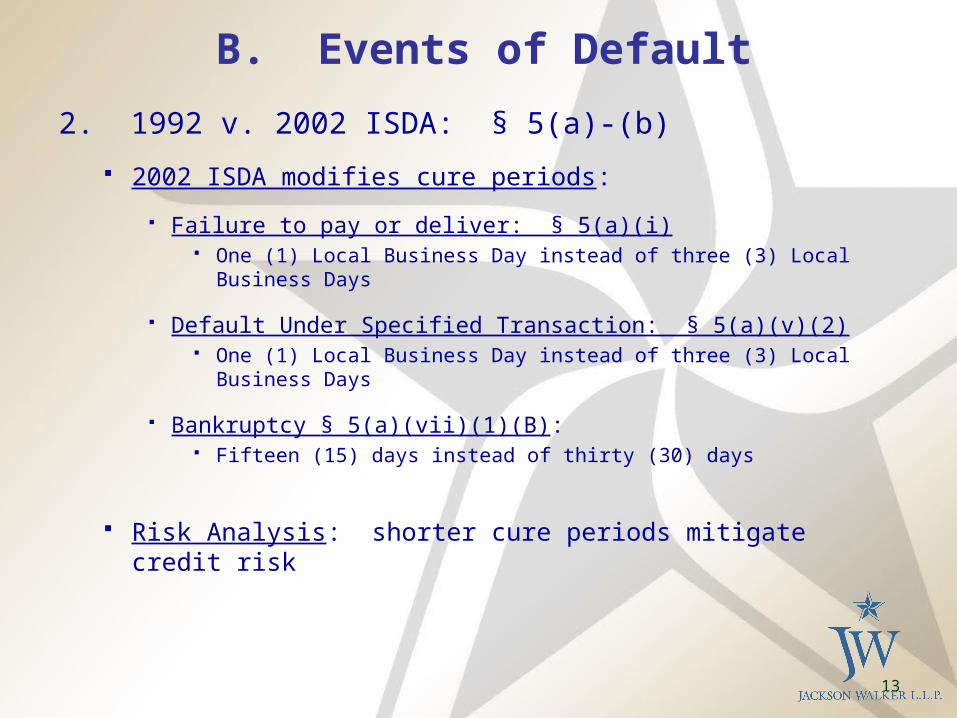

B. Events of Default

2. 1992 v. 2002 ISDA: § 5(a)-(b)

2002 ISDA modifies cure periods:

Failure to pay or deliver: § 5(a)(i) One (1) Local Business Day instead of three (3) Local Business Days

Default Under Specified Transaction: § 5(a)(v)(2) One (1) Local Business Day instead of three (3) Local Business Days

Bankruptcy § 5(a)(vii)(1)(B): Fifteen (15) days instead of thirty (30) days

Risk Analysis: shorter cure periods mitigate credit risk

14

B. Events of Default

2. 1992 v. 2002 ISDA (cont.)

Breach of Agreement: § 5(a)(ii)

2002 ISDA expands Breach of Agreement: Event of Default if a party “disaffirms, disclaims, repudiates or rejects…

or challenges the validity of” the ISDA

With respect to the 2002 language, the 30-day cure period in § 5(a)(ii) does not apply

Risk Analysis: allows swifter action when a counterparty clearly indicates it will not honor its ISDA obligations

15

B. Events of Default

2. 1992 v. 2002 ISDA (cont.)

Default Under Specified Transaction: § 5(a)(v)

2002 ISDA expands on events which constitute a default, including: Default under credit support arrangement relating to a Specified

Transaction Challenging the validity of a Specified Transaction

“Specified Transaction” includes “catch-all” clause to capture future derivatives products not otherwise stated

Risk Analysis: Avoids the risk that certain actions may not properly trigger the

Event of Default Avoids the risk that certain derivatives may be inadvertently

excluded from the laundry list of “Specified Transactions”

16

B. Events of Default

2. 1992 v. 2002 ISDA (cont.)

Cross Default: § 5(a)(vi)

2002 ISDA: To determine whether a party has exceeded Threshold Amount, party may look to both (i) principal of accelerated obligations, and (ii) unpaid amounts

1992 ISDA: Party cannot combine accelerated obligations and unpaid amounts to determine Threshold Amount

Risk Analysis: 2002 ISDA makes Cross Default much more sensitive and useful in situations where a counterparty commits multiple defaults, but some defaults are difficult to ascertain

17

B. Events of Default

2. 1992 v. 2002 ISDA (cont.)

Merger Without Assumption: § 5(a)(viii)

2002 ISDA expands to include reorganization, reincorporation and reconstitution

Risk Analysis: Mitigates credit risk by diminishing the ambiguity of what corporate action triggers this Event of Default

18

B. Events of Default

2. 1992 v. 2002 ISDA (cont.)

Credit Support Default: § 5(a)(iii)

2002 ISDA expands to include circumstances when a security interest granted under a Credit Support Document fails to be in full force and effect

Risk Analysis: Mitigates credit risk by expanding Event of Default upon failure under either (i) Credit Support Document, or (ii) security interest granted under such document.

19

B. Events of Default3. NAESB v. ISDA Gas Annex

Common Events of Default: NAESB § 10.2; ISDA § 5(a) Failure to pay when due Breach of credit obligations Insolvency and bankruptcy-related events

Events of Default in ISDA not found in NAESB: Breach of Agreement (other than failure to pay) Misrepresentations Default under Specified Transaction

Similar to Transactional Cross Default election in 2006 NAESB Cross Default

Similar to Indebtedness Cross Default election in 2006 NAESB Merger Without Assumption

* 20

B. Events of Default3. NAESB v. ISDA Gas Annex (cont.)

Termination Events in ISDA not found in NAESB: Illegality Force Majeure Event (2002) Tax Event and Tax Event Upon Merger Credit Event Upon Merger Additional Termination Event

21

B. Events of Default

4. EEI v. ISDA Power Annex

Common Events of Default: EEI § 5.1 and ISDA § 5(a):

Failure to pay when due

False or misleading representations

Breach of Agreement (other than failure to pay)

Insolvency and bankruptcy-related events

Breach of credit obligations

Merger without assumption

Cross Default

22

B. Events of Default

4. EEI v. ISDA Power Annex (cont.)

Events of Default and Termination Events in ISDA not found in EEI:

Default under Specified Transaction

Illegality

Force Majeure Event (2002 ISDA)

Tax Event and Tax Event Upon Merger

Credit Event Upon Merger

Additional Termination Event

23

B. Events of Default5. CTA v. ISDA Coal Annex

Common Events of Default: CTA § 8.1; ISDA § 5(a) Failure to Pay Breach of Agreement (other than failing to pay/deliver)

CTA: Cure Period of ten (10) Business Days, but potential extension of up to sixty (60) days

ISDA: Thirty (30)/Fifteen (15) Business Days (1992/2002) Credit Support Default Misrepresentation Cross Default Bankruptcy

ISDA triggering events more broad (e.g., passing resolutions for winding up or appointment of receiver)

Failure by Seller to provide reasonable assurances as to future coal shipments after non-conforming shipments are delivered

CTA § 8.1(e); Coal Annex, Appendix 1, § 13

24

B. Events of Default5. CTA v. ISDA Coal Annex (cont.)

Event of Default in CTA not found in ISDA: Material Adverse Change

Parties elect MAC definition on Cover Sheet: Credit Rating Trigger (as set by Parties) Event that has a material adverse effect on operations, financial condition

or business of a Party as a whole Even if MAC occurs, it is not an Event of Default if Defaulting Party

establishes and maintains Performance Assurance for the duration of the MAC

Risk Analysis: MAC provision mitigates credit risk by entitling a Party to either (i) receive

Performance Assurance, or (ii) declare Event of Default when the other Party shows signs of financial distress that may not fit cleanly in another Event of Default

25

B. Events of Default5. CTA v. ISDA Coal Annex (cont.)

Events of Default/Termination Events in ISDA not found in CTA:

Default Under Specified Transaction

Merger Without Assumption

Illegality

Force Majeure Event (2002)

Tax Event/Tax Event Upon Merger

Credit Event Upon Merger

26

B. Events of Default6. Automatic Early Termination under ISDA

How it works: Upon occurrence of certain bankruptcy events, an Early Termination

Date is deemed to occur Parties do not follow Early Termination Date notice procedures

Not in standard NAESB, EEI or CTA

May be useful in jurisdictions without U.S. Bankruptcy Code “safe harbor” provisions

Between U.S. counterparties, often not elected: Avoids risk of termination without Non-Defaulting Party’s knowledge Allows for cure and/or negotiation of better terms Avoids risk of unwanted Settlement Payments by Non-Defaulting Party

27

B. Events of Default7. Risk Analysis: Events of Default

Events of Default mitigate credit and payment risks with respect to the Defaulting Party

More ways to terminate under ISDA than under NAESB, EEI or CTA, but all may not be necessary for every transaction

Risks of underlying transaction help determine which Events of Default make sense

Short-Term v. Long-Term Index Price v. Fixed Price

Automatic Early Termination: May be beneficial under certain circumstances May create operational and credit risk if elected in some but not all contracts with a

counterparty

28

C. Setoff

1. 2002 v. 2006 NAESB: § 10.3.2

Elected on Cover Sheet of both 2002 and 2006 NAESB

2002 NAESB: Other Agreement Setoff

If Other Agreement Setoffs apply, bilateral setoff is the only option

Non-Defaulting Party sets off Net Settlement Amount against:

Margin or collateral held by Non-Defaulting Party

Any amounts payable by the Defaulting Party to the Non-Defaulting Party under any other agreement

29

C. Setoff

1. 2002 v. 2006 NAESB: § 10.3.2 (cont.)

2006 NAESB: Other Agreement Setoffs – 2 Options

Bilateral Setoff: Same as setoff in 2002 NAESB

Triangular Setoff: Same as setoff in 2002 NAESB, plus

Setoff Net Settlement Amount owed to Non-Defaulting Party against amount(s) owed by Non-Defaulting Party or Affiliates to Defaulting Party;

Setoff Net Settlement Amount owed to Defaulting Party against amount(s) owed by Defaulting Party to Non-Defaulting Party or Affiliates;

Setoff Net Settlement Amount owed to Defaulting Party against amount(s) owed by Defaulting Party or Affiliates to Non-Defaulting Party

30

C. Setoff

2. 1992 v. 2002 ISDA

1992 ISDA: No setoff provision

2002 ISDA: Setoff provision in § 6(f)

Non-defaulting Party may setoff Early Termination Amount against any other amounts owed between the parties

31

C. Setoff3. NAESB v. ISDA Gas Annex

NAESB § 10.3.2: Election on Cover Sheet

Other Agreement Setoffs Apply: 2002 NAESB: Bilateral 2006 NAESB: Bilateral or Triangular, as elected by the parties

Other Agreement Setoffs Do Not Apply Setoff limited to amounts owed under the NAESB.

ISDA Gas Annex:

2002 ISDA § 6(f): Setoff provision

Setoff amounts owed between the parties arising under ISDA or any other agreement

No cross-Affiliate setoff

Identical to setoff in 2002 NAESB

32

C. Setoff4. EEI v. ISDA Power Annex

EEI § 5.6: Setoff options elected on Cover Sheet

Option A: Non-Defaulting Party sets off obligations owed by Defaulting Party to Non-Defaulting Party under any agreements between the Parties

Options B: Non-Defaulting Party sets off obligations owed by Defaulting Party (or its Affiliates) to the Non-Defaulting Party (or its Affiliates) under any agreements between the Parties and/or their Affiliates

ISDA Power Annex:

2002 ISDA: Setoff provision in § 6(f)

Setoff amounts owed between the parties arising under ISDA or any other agreement

No cross-Affiliate setoff

33

C. Setoff5. CTA v. ISDA Coal Annex

CTA § 8.3

Upon an Event of Default, Non-Defaulting Party sets off amounts owed between the Parties under the CTA

ISDA: 2002: Setoff provision § 6(f)

Setoff amounts owed between the parties arising under ISDA or any other agreement

No cross-Affiliate setoff

34

C. Setoff6. Risk Analysis: Risks Mitigated by Setoff

Commercial Risks: Immediately extinguishes payment obligations Reduces involvement in bankruptcy proceedings

Credit Risks: Amounts owed by Defaulting Party are immediately setoff

Cash Flow Risk: No waiting for payments from Defaulting Party

Enterprise-wide risks among Affiliates: Manages risk of having to pay Termination Payments across trading contracts and

Affiliates

* 35

II. Other Agreement Differences

Potentially Creating “Gap Risk”

A. Termination, Liquidation & Settlement (NAESB, ISDA and EEI)

B. Confirmation Procedures (NAESB, ISDA and CTA)

C. Netting (NAESB and ISDA)

D. Transfer and Assignment (CTA and ISDA)

36

A. Termination, Liquidation & Settlement1. 2002 v. 2006 NAESB § 10.3: Terminating Transactions

2002 and 2006 NAESB: Upon designation of Early Termination Date, all transactions must be terminated and liquidated, except for “Excluded Transactions”

2002 NAESB: Excluded Transactions

May not be terminated and liquidated under law; and

Commercially impracticable to terminate in the reasonable opinion of Non-Defaulting Party

2006 NAESB: Excluded Transactions

May not be terminated or liquidated under law NOTE: does not include “commercially impracticable” transactions

37

A. Termination, Liquidation & Settlement

1. 2002 v. 2006 NAESB § 10.3: Terminating Transactions (cont.)

Risk Analysis:

Practical Risk: Inability to Liquidate Transactions

A Non-Defaulting Party under the 2006 NAESB may not be able to terminate and liquidate certain transactions as of the Early Termination Date if they are commercially impracticable

Example: Gas purchases at illiquid Delivery Points

38

A. Termination, Liquidation & Settlement

2. 1992 v. 2002 ISDA § 6: Calculation and Payment of Amounts Upon Termination

1992 ISDA § 6(e) Market Quotation or Loss calculation method One-way or two-way payment (First or Second method)

2002 ISDA § 6(d)-(e) Close-out Amount: Hybrid of Market Quotation and Loss

Calculation of gains, losses and costs incurred in replacing or realizing the economic equivalent of terminated transactions.

Determining Party may use internal valuations of its losses and costs, but also must use third-party quotations or market data in valuing transactions

39

A. Termination, Liquidation & Settlement

2. 1992 v. 2002 ISDA § 6: Calculation and Payment of Amounts Upon Termination (cont.)

Risk Analysis:

Close-out Amount mitigates risk of subjective valuations under Loss calculation method

Close-out Amount more flexible than Market Quotation because a party may look to internal data and estimated losses

Close-out Amount is more subjective than Market Quotation and more objective than Loss

40

A. Termination, Liquidation & Settlement3. NAESB v. ISDA Gas Annex: Calculation and Payments of

Amounts Owed Upon Termination

NAESB § 10.3.1

Non-Defaulting Party determines: Amount owed by each party for Gas delivered and received on or before the

Termination Date

All other applicable charges related to such deliveries and receipts for which payment has not yet been made

If “Additional Termination Damages” apply: Liquidation and acceleration of Terminated Transactions at Market Value

If Market Value greater than Contract Value, difference due to Buyer

If Market Value less than Contract Value, difference due to Seller

Default two-way payment

41

A. Termination, Liquidation & Settlement3. NAESB v. ISDA Gas Annex: Calculation and Payment of Amounts

Owed Upon Termination (cont.)

ISDA § 6(e): Market Quotation and Loss

Market Quotation: Value of Terminated Transactions based on quotations from Reference-Market

Makers plus any Unpaid Amounts owed to Non-Defaulting Party; minus

Unpaid Amounts owed to the Defaulting Party

Loss: Non-Defaulting Party’s total losses and costs resulting from early termination

and liquidation, including loss of bargain, costs of funding, and costs of terminating, liquidating or reestablishing any hedge

ISDA § 6(e): First and Second Method

One-way v. two-way payment

42

A. Termination, Liquidation & Settlement

4. EEI v. ISDA Power Annex: Calculation and Payment of Amounts Owed Upon Termination

EEI: § 5.2: Non-Defaulting Party calculates Settlement Amount for each

Terminated Transaction in a “commercially reasonable manner”

§ 5.3: Settlement Amounts netted into Termination Payment, payable either to or from the Non-Defaulting Party

Default two-way payment unless changed by parties

ISDA: § 6(e): Market Quotation or Loss, as elected by parties ISDA § 6(e): First or Second Method, as elected by the parties

(one-way or two-way payment)

43

A. Termination, Liquidation & Settlement

5. NAESB, EEI and ISDA: Risk Analysis

Inherent operational risks in various calculation methods:

NAESB method and Market Quotation are substantively similar, while EEI requires calculation in a “commercially reasonable manner”

Use of market quotes may not accurately reflect actual or anticipated value of transactions

Subjective nature of Loss calculation

Inconsistent Payment Risks to Defaulting Party:

NAESB and EEI are two-way payment

Potential exposure if one-way payment elected in ISDA

* 44

B. Confirmation Procedures

1. NAESB v. ISDA Gas Annex

NAESB § 1.2: Procedure elected on Cover Sheet

Oral Transaction Procedure Transaction is binding when parties orally agree upon terms Failure to send Transaction Confirmation does not affect performance

obligations

Written Transaction Procedure Parties must exchange non-conflicting Transaction Confirmation before

parties legally obligated to perform

45

B. Confirmation Procedures

1. NAESB v. ISDA Gas Annex (cont.)

ISDA § 9(e)(ii):

Parties legally bound from the moment they agree on commercial terms

Confirm Transaction terms by sending written Confirmations

No other specific terms or procedures in form ISDA

* 46

B. Confirmation Procedures

2. CTA v. ISDA Coal Annex

CTA § 1.1

Parties are bound when terms agreed upon (whether oral or written)

Buyer shall provide Confirmation with commercial terms

If Seller disputes terms, Parties use “commercially reasonable efforts” to resolve the dispute within ten (10) Business Days

If dispute cannot be resolved, Parties may seek “any other remedy” under the CTA

ISDA § 9.2(e)(ii)

Parties legally bound from the moment they agree on commercial terms, and confirm by sending written Confirmations

* 47

B. Confirmation Procedures

3. NAESB, CTA and ISDA: Risk Analysis

Confirmation procedures should conform to risk in underlying transactions

Short-term v. Long-term

Risk of disagreement regarding future performance obligations

Operational Risk in Confirming Transactions

Buyer confirms in CTA, Seller confirms in NAESB and ISDA does not specify

Inconsistent Dispute Resolution Procedures NAESB and CTA v. ISDA

* 48

C. Netting1. NAESB v. ISDA Gas Annex

NAESB § 7.7 All payments due and owing (or past due and owing) netted into single

amount The party owing the greater amount shall make a single payment to the other

party Not limited to amounts owed under a single transaction

ISDA § 2(c) Netting generally limited to amounts due (i) on the same date; (ii) in the same

currency; and (iii) in respect of the same Transaction. Can be modified by the parties in the Schedule

Risk Analysis: Inconsistent netting provisions across multiple agreements may create cash

flow and operational risks Cross-Transactional Netting: NAESB v. ISDA

49

D. Transfer and Assignment

1. CTA v. ISDA Coal Annex

General Rule: No transfer or assignment without prior written consent of other party (CTA § 10.1; ISDA § 7)

CTA: Consent cannot be unreasonably withheld or delayed ISDA: No “reasonableness” requirement

Exceptions in CTA:

Financing or financial arrangements

Affiliate at least as creditworthy as assignor

Person succeeding to all or substantially all of Party’s assets (merger, reorganization, or otherwise)

* 50

D. Transfer and Assignment

1. CTA v. ISDA Coal Annex (cont.)

Exceptions in ISDA:

Transfers of rights to receive Termination Payments from Defaulting Party

Consolidation, merger or transfer of all assets

Risk Analysis:

CTA provides more flexibility

ISDA may make transfers more difficult, time consuming and expensive

* 51

Conclusion

Differences exist between trading agreements

May be difficult to make all agreements consistent

Identify priority issues

Scope

Research paper

Craig R. Enochs

Jackson Walker L.L.P.

1401 McKinney, Suite 1900

Houston, Texas 77010

(713) 752-4200 phone

![James C. Enochs High School WASC Self-Study … WASC Self...[James C. Enochs High School WASC Self-Study Report] 2015-2016 BE SAFE, BE RESPONSIBLE, BE RESPECTFUL 3 Preface In the six](https://static.fdocuments.net/doc/165x107/5fa328cf6d32e112ef77abc0/james-c-enochs-high-school-wasc-self-study-wasc-self-james-c-enochs-high-school.jpg)