1 ( 1% 4%) Retirement Savings Plan - T. Rowe Price that you should read carefully before investing....

15

Retirement Savings Plan Dear BorgWarner Employee: Welcome to your Retirement Savings Plan—a great way to “take the wheel” and drive toward a more comfortable financial future. As a participant, you can take advantage of tax-deferred savings and a wide selection of investment opportunities. The enclosed “Take the Wheel” workbook includes essential information about the plan that will make it easier for you to get started. It walks you through simple steps to help you decide how much to save for your future and how to invest those savings. Included with this workbook are the following materials: • Plan features summary – outlines how the plan works, including information on contribution limits, vesting, and withdrawals. • Enrollment worksheet – is a handy way to record your decisions as you go through the materials. Use this worksheet as a guide when you contact T. Rowe Price about how much you contribute or how you invest your contributions. • Investment performance page – shows the short-term and long-term track record of each investment in the plan. • Fund fact sheets – give you information about each investment option, including investment objective, strategy, and risks. Please see the disclosure page that follows the fund fact sheets for important information, including the risks of investing in mutual funds and an explanation of the information available on the fund fact sheets. • Beneficiary form – allows you to name or update your beneficiaries. Important note: Please complete this form and return it to T. Rowe Price in the enclosed postage-paid, self-addressed envelope. Getting started is simple. That’s because 60 days after you become eligible to join the plan, you will be automatically enrolled in the plan. With automatic enrollment, 3% will be deducted from your Before-Tax pay and contributed to your plan account. This contribution along with a 100% Company Matching contribution will be invested in a Northern Trust Focus Fund with a “target” year most closely matching your anticipated retirement date. You can change your investment allocation or decide not to participate in the plan at any time. As a participant, you can take advantage of tax-deferred savings and a wide selection of investment opportunities. To enroll: 1. Call T. Rowe Price at 1-800-922-9945 or visit the website at rps.troweprice.com. 2. Complete the enclosed beneficiary form and return it to T. Rowe Price in the enclosed postage-paid, self-addressed envelope. Go ahead, turn the key and get going! Call 1-800-922-9945 to request a prospectus, which includes investment objectives, risks, fees, expenses, and other information that you should read carefully before investing. 105549_ltr_enr_0111 102988 OCQ18-BWEN 2/11

Transcript of 1 ( 1% 4%) Retirement Savings Plan - T. Rowe Price that you should read carefully before investing....

Retirement Savings Plan

Dear BorgWarner Employee:

Welcome to your Retirement Savings Plan—a great way to “take the wheel” and drive toward a more comfortable financial

future. As a participant, you can take advantage of tax-deferred savings and a wide selection of investment opportunities.

The enclosed “Take the Wheel” workbook includes essential information about the plan that will make it easier for you to get

started. It walks you through simple steps to help you decide how much to save for your future and how to invest those

savings. Included with this workbook are the following materials:

•Plan features summary – outlines how the plan works, including information on contribution limits, vesting, and

withdrawals.

•Enrollment worksheet – is a handy way to record your decisions as you go through the materials. Use this worksheet as

a guide when you contact T. Rowe Price about how much you contribute or how you invest your contributions.

• Investment performance page – shows the short-term and long-term track record of each investment in the plan.

• Fund fact sheets – give you information about each investment option, including investment objective, strategy, and

risks. Please see the disclosure page that follows the fund fact sheets for important information, including the risks of

investing in mutual funds and an explanation of the information available on the fund fact sheets.

•Beneficiary form – allows you to name or update your beneficiaries. Important note: Please complete this form and return it to T. Rowe Price in the enclosed postage-paid, self-addressed envelope.

Getting started is simple. That’s because 60 days after you become eligible to join the plan, you will be automatically enrolled

in the plan. With automatic enrollment, 3% will be deducted from your Before-Tax pay and contributed to your plan account.

This contribution along with a 100% Company Matching contribution will be invested in a Northern Trust Focus Fund with a

“target” year most closely matching your anticipated retirement date. You can change your investment allocation or decide

not to participate in the plan at any time.

As a participant, you can take advantage of tax-deferred savings and a wide selection of investment opportunities. To enroll:

1. Call T. Rowe Price at 1-800-922-9945 or visit the website at rps.troweprice.com.

2. Complete the enclosed beneficiary form and return it to T. Rowe Price in the enclosed postage-paid, self-addressed

envelope.

Go ahead, turn the key and get going!

Call 1-800-922-9945 to request a prospectus, which includes investment objectives, risks, fees, expenses, and other information that you should read carefully before investing.

105549_ltr_enr_0111

102988 OCQ18-BWEN 2/11

TAKE THEWHEEL Retirement Savings Plan

BorgWarner Inc. Retirement Savings Plan

Eligibility and Enrollment

You are immediately eligible to join the plan and may do so by calling T. Rowe Price at 1-800-922-9945 or by logging in to the website at rps.troweprice.com.

If you take no action, you will be automatically enrolled after 60 days of employment with BorgWarner.

With automatic enrollment, 3% will be deducted from your Before-Tax pay and deposited into the Savings Account of your Retirement Savings Plan (RSP) account. This contribution along with a 100% Company Matching contribution will be invested in a Northern Trust Focus Fund whose “target” year most closely matches your anticipated retirement date (as shown in the enclosed Investment Workbook). If you wish to change your investment mix allocation, log in to the website or call T. Rowe Price at 1-800-922-9945.

Company Retirement Account

After you have been employed by BorgWarner for 60 days, the Company will make a contribution to your account each payroll based on your years of service and your eligible pay, which is indicated in the chart below. The first 3% of your Company Retirement Contribution is a Safe Harbor contribution. For more information on this contribution, please refer to the vesting section of this document. The Company contributions made to this account are not available for a withdrawal or a loan.

Company Retirement Account Contributions

Years of vested service as of each January 1

Company contribution for compensation up to the Social Security wage base

Company contribution for compensation over the Social Security wage base

Less than or equal to 10 years 3% 6%

Over 10 years but less than or equal to 20 years

4% 8%

Over 20 years 5% 10%

The Social Security wage base is indexed at $110,100 for 2012.

Savings Account

You can contribute from 1% to 28% of your eligible pay to this account on a Before-Tax and/or After-Tax basis. (Your total contributions may not exceed 28%.) The Company will match 100% of the first 3% of your Before-Tax contributions. All employee contributions made to this account will be available for a withdrawal or a loan (subject to plan rules), though Company contributions are not available.

Catch-Up Contributions

If you will be age 50 or older on or before December 31 of the current year and defer the maximum you are allowed under the plan, you may also contribute an additional amount of “catch-up contributions” up to the IRS limit.

Retiree Health Account (RHA)

With health care costs continuing to climb, the RHA portion of the RSP is a valuable way to help you set aside money today—while earning RHA Company Matching contributions—for medical costs you may incur after you leave BorgWarner. You can contribute from 1% to 3% of your eligible pay on a before-tax basis and the Company will match those contribu-tions dollar for dollar up to $500 per year. All employee contributions made to this account will be available for a withdrawal or a loan (subject to plan rules), though Company contributions are not. RHA assets can be withdrawn even if the assets are not being used for health care expenses.

(over, please)

Your combined before-tax contributions made to your Savings Account and Retiree Health Account are subject to annual limits set by the Internal Revenue Service.

Vesting

Vesting refers to the portion of your account that you may take when you leave the Company or borrow from when you take a loan. You are always 100% immediately vested in the value of your own contributions and the contributions the Company makes to your Safe Harbor Company Retirement Contribution account. You will become 100% vested in all other contributions made to your account by the Company (e.g., any Company Retirement Contribution (CRC) allocated to your account above 3%; Savings Company Matching contributions, RHA Company Matching contribu-tions) after completing three years of service.

Loans

Your plan allows you to take a loan from the vested portion of your RSP account (with the exception of your Safe Harbor Company Retirement Contribution, Company Retirement, Savings Company Match, and RHA Company Match accounts) using the following guidelines:

•Theminimumloanamountis$500.Themaximumisthelesserof:(a)50%ofyourvestedbalance,or (b) $50,000 reduced by the highest outstanding loan balance in the last 12 months

•Youmaynothavemorethanoneloanoutstandingatatime •Loaninterestistheprimerateplus1% •Loansplusinterestmustbepaidbackwithinfiveyears •Thereisa$50loaninitiationfee

Withdrawals

While we encourage you to leave your money in the plan until you’re ready to retire, there are occasions when you may need to take a withdrawal while you are still employed. You may take up to two hardship and two non-hardship withdrawals per year, subject to plan rules. Here are the types of withdrawals available:

•Non-hardshipwithdrawal—includesAfter-TaxandRollover,plusearnings •Age591⁄2withdrawal—includesthevestedportionofyourRSPaccount(withtheexceptionofyourCompany

Retirement account, Savings Company Match, and RHA Company Match) •Hardshipwithdrawal—includesSavingsBefore-Taxcontributions,RHABefore-Taxcontributions,andcertain

earnings;availabletoemployeesunderage591⁄2 and is restricted to documented financial hardship. Reasons for hardship include:

•Unreimbursedmedicalexpenses •Purchaseofprimaryresidence •Tuitionandrelatedexpensesforpost-secondaryeducation •Preventionofevictionorforeclosure •Funeralexpenses •Damageofprincipalresidence

Just remember, there are serious consequences to taking a withdrawal:

•AnywithdrawalsofBefore-Taxoremployercontributionsandrelatedearningsaretaxableincomeforfederalandsometimes state taxes.

•Generally,a10%penaltyappliestotaxablewithdrawalstakenbeforeage591⁄2.

Most withdrawals are subject to a mandatory 20% federal withholding unless you make a direct rollover to a Traditional IRA or an eligible employer retirement plan. You may directly roll over a distribution from the plan into a Roth IRA. The amount rolled into the Roth IRA is considered taxable income to you in the year of the rollover. The earnings on any after-tax contributions you withdraw are taxed as income unless they are rolled over. After-tax con-tributions can be returned to you tax-free, or they may be rolled over to an individual retirement account (IRA) or an eligible employer retirement plan. Consult your tax advisor for details. Additional plan distribution rules apply.

This summary provides only a general overview of your plan. If any information in this summary conflicts with the plan document, the plan document will govern.

BW-B OCT74-BWEN 12/11105549_fly_fnd_0111111267

TAKE THEWHEEL Retirement Savings Plan

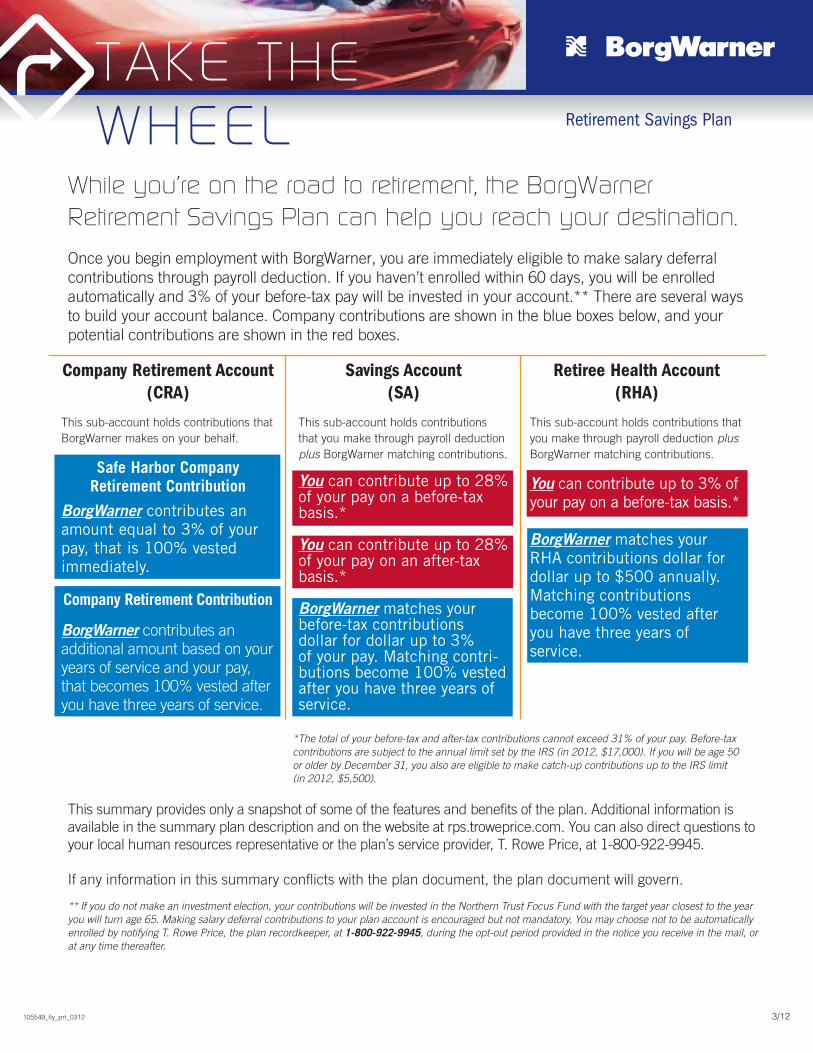

While you’re on the road to retirement, the BorgWarner

Retirement Savings Plan can help you reach your destination.

Once you begin employment with BorgWarner, you are immediately eligible to make salary deferral contributions through payroll deduction. If you haven’t enrolled within 60 days, you will be enrolled automatically and 3% of your before-tax pay will be invested in your account.** There are several ways to build your account balance. Company contributions are shown in the blue boxes below, and your potential contributions are shown in the red boxes.

This summary provides only a snapshot of some of the features and benefits of the plan. Additional information is available in the summary plan description and on the website at rps.troweprice.com. You can also direct questions to your local human resources representative or the plan’s service provider, T. Rowe Price, at 1-800-922-9945.

If any information in this summary conflicts with the plan document, the plan document will govern.

** If you do not make an investment election, your contributions will be invested in the Northern Trust Focus Fund with the target year closest to the year you will turn age 65. Making salary deferral contributions to your plan account is encouraged but not mandatory. You may choose not to be automatically enrolled by notifying T. Rowe Price, the plan recordkeeper, at 1-800-922-9945, during the opt-out period provided in the notice you receive in the mail, or at any time thereafter.

Company Retirement Account (CRA)

This sub-account holds contributions that BorgWarner makes on your behalf.

Safe Harbor Company Retirement Contribution

BorgWarner contributes an amount equal to 3% of your pay, that is 100% vested immediately.

Company Retirement Contribution

BorgWarner contributes an additional amount based on your years of service and your pay, that becomes 100% vested after you have three years of service.

Savings Account (SA)

This sub-account holds contributions that you make through payroll deduction plus BorgWarner matching contributions.

You can contribute up to 28% of your pay on a before-tax basis.*

You can contribute up to 28% of your pay on an after-tax basis.*

BorgWarner matches your before-tax contributions dollar for dollar up to 3% of your pay. Matching contri-butions become 100% vested after you have three years of service.

Retiree Health Account (RHA)

This sub-account holds contributions that you make through payroll deduction plus BorgWarner matching contributions.

You can contribute up to 3% of your pay on a before-tax basis.*

BorgWarner matches your RHA contributions dollar for dollar up to $500 annually. Matching contributions become 100% vested after you have three years of service.

105549_fly_prt_0312 3/12

*The total of your before-tax and after-tax contributions cannot exceed 31% of your pay. Before-tax contributions are subject to the annual limit set by the IRS (in 2012, $17,000). If you will be age 50 or older by December 31, you also are eligible to make catch-up contributions up to the IRS limit (in 2012, $5,500).

REQUIRED NOTICE TO PLAN PARTICIPANTS ***INFORMATION ONLY—NO ACTION REQUIRED***

Annual Notice

Safe Harbor, Automatic Enrollment and Default Investment Alternative Automatic Enrollment and Safe Harbor Contribution The BorgWarner Inc. Retirement Savings Plan (“Plan”) contains an “automatic contribution arrangement,” which is also known as automatic enrollment. With automatic enrollment, unless you elected otherwise, your employer (“Company”) automatically deducts 3% from your pay on a before-tax basis each pay period and deposits these amounts into your Plan account. The Company also matches, on a dollar-for-dollar basis, up to the first 3% of eligible pay you contribute each pay period. These matching contributions will be made regardless of whether your contributions are determined through automatic enrollment. You have the right at any time to change the contribution amount or to choose not to make any contribution at all. The change will be made as soon as administratively possible, but in most cases the change will apply to your first pay after you make the change. You may change your contribution amount by going to the Web site at rps.troweprice.com or by calling the Plan Account Line at 1-800-922-9945. Representatives are available to assist you from 7 a.m. to 10 p.m. Eastern time. Besides contributing the amounts taken from your pay, starting January 1, 2011, the Company began making a non-elective safe harbor contribution to the Plan for each plan year in the amount of 3% of your eligible pay. The Company intends to continue making this contribution for the 2012 Plan Year You can find a description of the other types of contributions the Company may make to your Plan account and an explanation of how your pay is determined for calculating contributions in the Contributions section of the Plan’s SPD. Terminated Participants If you are a terminated Participant in the Plan, the automatic enrollment and Company contribution information above does not apply to you. You are receiving this notice because it also contains information about the default investment alternatives for the amounts in your Plan account, if any, that you do not direct. Default Investment Alternative Regardless of whether you are an active employee or terminated participant, you have the right to direct the investment of your Plan account. If you do not choose an investment option for amounts in your Plan account, your Plan account (including any automatic enrollment contributions or Company contributions made on your behalf) will be invested in the Plan’s default investment fund until you change your investment election. The Plan’s default investment is the Northern Trust Focus Funds, and your account will be invested in the target year Focus Fund closest to the year in which you turn 65. A brief description of the existing and new default investments, including their investment objectives, risk and return characteristics, fees, and expenses is included in the booklet attached to this notice.

You have the right to change your investment election to any other investment alternative under the Plan at any time by calling the Plan Account Line at 1-800-922-9945 or by going to the Web site at rps.troweprice.com. You can obtain investment information about the Plan’s default fund and other investment options by calling the Plan Account Line or by going to the Web site at rps.troweprice.com. Vesting and Withdrawals You will always be fully vested in your contributions to the Plan and the non-elective safe harbor contributions the Company makes on your behalf. You will be fully vested in other Company contributions when you complete three years of service. To be fully vested in Plan contributions means that the contributions (together with any investment gain or loss) will always belong to you, and you will not lose them when you leave the Company. For more information about years of service, you can review the Vesting section of the Plan’s SPD.

There are limits on when you may withdraw your funds. These limits may be important to you in deciding how much, if any, to contribute to the Plan. You may withdraw all or any portion of your vested account if you are age 65 or over or you leave the Company. While you remain employed, you may withdraw the portion of your Plan account attributable to rollover or after-tax contributions, if any, up to two times per year. There is generally an extra 10% tax on distributions before age 59½. If you remain employed when you reach age 59½, you may also withdraw from your Plan account amounts attributable to your pre-tax contributions (including automatic enrollment contributions). Your Plan beneficiary can withdraw any vested amount remaining in your account when you die.

In addition to the above rules on withdrawals, you also can borrow certain amounts from your vested Plan account (referred to as a loan) or take a hardship withdrawal from certain amounts in your vested Plan account if you have a qualifying hardship. The amount of a hardship withdrawal is limited by the amount of your qualifying expenses. A hardship withdrawal may not be taken from Company contributions or from post-1988 earnings on your contributions. Hardship withdrawals may only be taken to pay qualifying expenses related to the following needs: medical, purchase of your principal residence, prevention of eviction from or foreclosure on your principal residence, repair of certain damages to your principal residence, post-secondary education, or burial or funeral. Before you can take a hardship distribution, you must have taken other permitted withdrawals and loans from qualifying Company plans. If you take a hardship withdrawal, you may not contribute to the Plan or other qualifying Company plans for six months. After six months, your contributions to the Plan will automatically resume at the rate you were contributing prior to the hardship withdrawal unless you elect otherwise.

To the extent anything in this notice is inconsistent with the terms of the Plan, the terms of the Plan govern. You can learn more about the Plan’s rules for enrollment, contributions, investments, and withdrawals in the Plan’s SPD. You can also learn more about the extra 10% tax in IRS Publication 575, Pension and Annuity Income. NOTE: IF YOU HAVE CHANGED YOUR CONTRIBUTION AMOUNT OR YOUR INVESTMENT OPTION FROM THE DEFAULTS NAMED ABOVE, YOU WILL REMAIN IN THE CONTRIBUTION AMOUNT AND THE INVESTMENT OPTION(S) YOU ELECTED UNTIL YOU OR THE COMPANY MAKES A FUTURE CHANGE.

1

Current Default Investment

Northern Trust Focus 2010 Fund The Northern Trust Focus 2010 Fund provides an asset allocation for people planning to retire between 2008 and 2012. Over time, the Fund’s asset allocation becomes more conservative as it approaches the target retirement date. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss. Northern Trust Focus 2015 Fund The Northern Trust Focus 2015 provides an asset allocation for people planning to retire between 2013 and 2017. Over time, the Fund’s asset allocation becomes more conservative as it approaches the target retirement date. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss. Northern Trust Focus 2020 Fund The Northern Trust Focus 2020 Fund provides an asset allocation for people planning to retire between 2018 and 2022. Over time, the Fund’s asset allocation becomes more conservative as it approaches the target retirement date. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss. Data provided by Northern Trust Corporation

2

Northern Trust Focus 2025 Fund The Northern Trust Focus 2025 Fund provides an asset allocation for people planning to retire between 2023 and 2027. Over time, the Fund’s asset allocation becomes more conservative as it approaches the target retirement date. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss.

Northern Trust Focus 2030 Fund The Northern Trust Focus 2030 Fund provides an asset allocation for people planning to retire between 2028 and 2032. Over time, the Fund’s asset allocation becomes more conservative as it approaches the target retirement date. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss. Northern Trust Focus 2035 Fund The Northern Trust Focus 2035 Fund provides an asset allocation for people planning to retire between 2033 and 2037. Over time, the Fund’s asset allocation becomes more conservative as it approaches the target retirement date. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss. Data provided by Northern Trust Corporation

3

Northern Trust Focus 2040 Fund The Northern Trust Focus 2040 Fund provides an asset allocation for people planning to retire between 2038 and 2042. Over time, the Fund’s asset allocation becomes more conservative as it approaches the target retirement date. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss. Northern Trust Focus 2045 Fund The Northern Trust Focus 2045 Fund provides an asset allocation for people planning to retire between 2043 and 2047. Over time, the Fund’s asset allocation becomes more conservative as it approaches the target retirement date. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss. Northern Trust Focus 2050 Fund The Northern Trust Focus 2050 Fund provides an asset allocation for people planning to retire between 2048 and 2052. Over time, the Fund’s asset allocation becomes more conservative as it approaches the target retirement date. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss. Data provided by Northern Trust Corporation

4

Northern Trust Focus 2055 Fund The Northern Trust Focus 2055 provides an asset allocation for people planning to retire between 2053 and 2057. Over time, the Fund’s asset allocation becomes more conservative as it approaches the target retirement date. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss. Target Retirement Income Fund The Target Retirement Income Fund provides an asset allocation for people already retired. The Fund invests in a broadly diversified portfolio of primarily passive investment funds comprised of U.S. and international stocks, securities that act as a hedge against inflation, U.S. bonds and U.S. Government cash reserves. The investment risks of the Fund changes over time as its allocation changes. The Fund is subject to the volatility of the financial markets including equity and fixed income investments in the U.S. and abroad and may be subject to risks associated with investing in high yield, small cap and foreign securities. Principal invested is not guaranteed at any time, including at or after the target date. Unit price and return will vary. The Fund’s holdings and asset allocation are subject to change. Asset allocation does not guarantee a profit, nor does it protect against loss.

Data provided by Northern Trust Corporation

11/10

TAKE THEWHEEL Retirement Savings Plan

BorgWarner Inc. Retirement Savings Plan

Make your decisions work for youYou are immediately eligible to join the plan. While the plan has made it easy to participate by automatically enrolling employees after 60 days of service, you may decide to enroll before your automatic enrollment takes place. Or you may want to make changes to how you would be automatically enrolled. For instance, you may want to change:

• How much you contribute, or• How your contributions and Company contributions are invested.

As you read through the enrollment materials, use this worksheet to keep track of your decisions. Then use it as a quick reference when you access your plan account either by phone at 1-800-922-9945 or by visiting the website at rps.troweprice.com.

COMPONENTS OF THE RETIREMENT SAVINGS PLAN (RSP)

Company Retirement Account

Company Retirement

Savings Account

Savings Before Tax

Savings After Tax

Savings Company Match

Rollover*

After-Tax Rollover*

Retiree Health Account (RHA)

RHA Before Tax

RHA Company Match

* Not a payroll contribution.

Company Retirement Account Savings

Account

Retiree Health Account

(over, please)

HOW MUCH TO CONTRIBUTE?

The Company will:

• Begin making Company retirement contributions after 60 days of service, and

• Immediately match certain contributions you make to the plan.

You must decide:

• How much you want to have taken out of your paycheck as your employee contributions. If you do nothing, you will be automatically enrolled after 60 days. With automatic enrollment, 3% will be deducted from your before-tax pay and contributed to your account.

Below is a listing of the various contribution sources (including contribution limits).

Your Employee Contribution Elections:

Contribution source Amount Your election

Savings Before Tax* 1%–28%** __________%

Savings After Tax 1%–28%** __________%

Catch-Up Before Tax up to the IRS limit (For employees age 50 or older by the end of the current year) __________%

RHA Before Tax* 1%–3% __________%

* Up to the IRS limit. ** Combined total not to exceed 28%.

Company Contributions:

Contribution source Amount

Company Retirement Automatic after 60 days from date of hire

Savings Company Match 100% of first 3% of Savings Before Tax

RHA Company Match 100% of RHA Before Tax, up to $500

HOW TO INVEST YOUR CONTRIBUTIONS?

INVESTMENT CATEGORIES STOCKS BONDS

MONEY MARKET/STABLE VALUE PRE-ASSEMBLED FUNDS

Investment Options

BorgWarner Inc. Stock***Buffalo Small Cap Harbor International Collective S&P 500 Index Fund Northern Trust InternationalVanguard Mid-Cap Index

Northern Trust Collective Aggregate Bond Index Fund

Stable Value Fund, Schedule N

Northern Trust Focus 2055 FundNorthern Trust Focus 2050 FundNorthern Trust Focus 2045 FundNorthern Trust Focus 2040 FundNorthern Trust Focus 2035 FundNorthern Trust Focus 2030 FundNorthern Trust Focus 2025 FundNorthern Trust Focus 2020 FundNorthern Trust Focus 2015 FundNorthern Trust Focus 2010 FundNorthern Trust Focus Income Fund

***Company stock2

The investment options offered in the Retirement Savings Plan are shown below:

With contributions coming soon into your account, you must decide how you want these contributions invested. The RSP offers you two ways to approach investing for your retirement:

1) Choose a pre-assembled, professionally managed portfolio, or

2) Choose the build-it-yourself approach where you will select your own combination of investments from the plan’s lineup.

These two investment methods are broken down below. As you review the enrollment materials and decide which approach best suits you, indicate how you would like to have future contributions invested. That way, you’ll have your choices at your fingertips when you contact T. Rowe Price to make your elections.

You must call T. Rowe Price at 1-800-922-9945 to make your investment choices, or you can make your election on the T. Rowe Price website at rps.troweprice.com. If you do not make an investment election, any contributions made to your account will be invested in a target-year Focus Fund closest to the year in which you turn 65.

Option 1: Pre-assembled portfolio

If you were born... This fund might be right for you...

In 1988 or after Northern Trust Focus 2055 Fund

1983 - 1987 Northern Trust Focus 2050 Fund

1978 - 1982 Northern Trust Focus 2045 Fund

1973 - 1977 Northern Trust Focus 2040 Fund

1968 - 1972 Northern Trust Focus 2035 Fund

1963 - 1967 Northern Trust Focus 2030 Fund

1958 - 1962 Northern Trust Focus 2025 Fund

1953 - 1957 Northern Trust Focus 2020 Fund

1948 - 1952 Northern Trust Focus 2015 Fund

1943 - 1947 Northern Trust Focus 2010 Fund

In 1942 or earlier Northern Trust Focus Income Fund

Each portfolio is designed with a target retirement date in mind.

Option 2: Build-it-yourself portfolio

The investments are grouped by investment type: stocks, bonds, and stable value. Once you have read about them and selected those that appeal to you:

• Check the percentage of your total contribution you want to invest in each investment type.

• Decide how to combine the investment options to complete the investment type. For example, if you decide you want 60% of your investment in the stock category, you will then need to decide how you want that 60% allocated across the stock funds that the plan offers.

NOTE: All investment options are available under the build-it-yourself approach. As you’ll see in the Investment Workbook, the pre-assembled funds are not included in the asset allocation pie charts. The Focus portfolios by design are diversified, made up of varying amounts of stocks, bonds, and stable value instruments.

(over, please)3

When building your own portfolio under Option 2 at T. Rowe Price:

• You may elect to assign the same investment allocation to all contribution sources, or you may elect to have these sources invested differently.

• If you choose to invest each contribution source differently (see the list of sources below), you will be required to make an investment option allocation for each source to which you are contributing.

• You will be required to make these choices again if you decide to change how your future contributions are allocated.

When making this election either online or via the toll-free phone number, the following options will be referenced:

• All sources

• Savings Before Tax

• RHA Before Tax

• RHA Company Match

• Savings After Tax

• After-Tax Rollover

• Company Retirement

• Savings Company Match

• Rollover

Call 1-800-922-9945 to request a prospectus, which includes investment objectives, risks, fees, expenses, and other information that you should read and consider carefully before investing.

105549_fly_inv_0511 OCX 106-BWEN106872 06/11

Stocks Your Election

Buffalo Small Cap Fund ________%Harbor International Fund, Instl. ________%Northern Trust Collective S&P 500 Index Fund ________%Vanguard Mid-Cap Index Fund, Instl. ________%

Total Stock ________%

Bonds

Northern Trust Collective Aggregate Bond Index Fund ________%Total Bond ________%

Money Market/Stable Value

Stable Value Fund, Schedule N ________%Total Stable Value ________%

Company Stock

BorgWarner Inc. Stock Fund ________%Total Company Stock ________%

Total Investment Allocation 100%

4

TAKE THEWHEEL Retirement Savings Plan

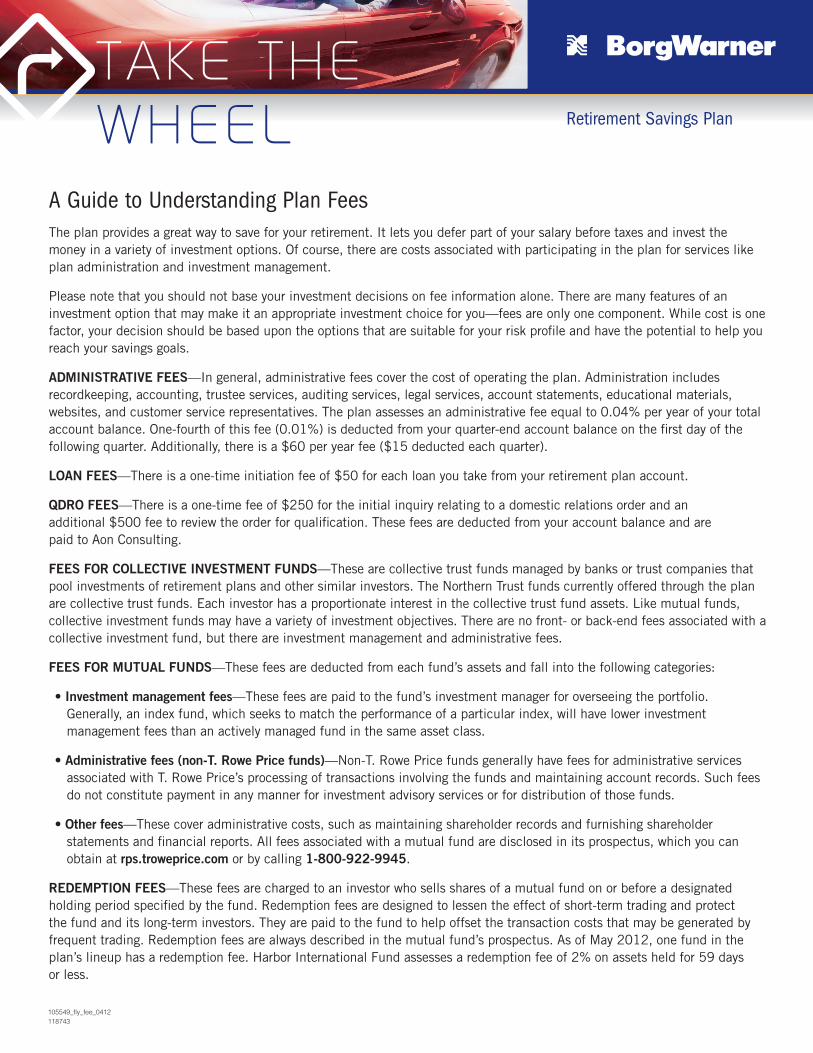

A Guide to Understanding Plan FeesThe plan provides a great way to save for your retirement. It lets you defer part of your salary before taxes and invest the money in a variety of investment options. Of course, there are costs associated with participating in the plan for services like plan administration and investment management.

Please note that you should not base your investment decisions on fee information alone. There are many features of an investment option that may make it an appropriate investment choice for you—fees are only one component. While cost is one factor, your decision should be based upon the options that are suitable for your risk profile and have the potential to help you reach your savings goals.

ADMINISTRATIVE FEES—In general, administrative fees cover the cost of operating the plan. Administration includes recordkeeping, accounting, trustee services, auditing services, legal services, account statements, educational materials, websites, and customer service representatives. The plan assesses an administrative fee equal to 0.04% per year of your total account balance. One-fourth of this fee (0.01%) is deducted from your quarter-end account balance on the first day of the following quarter. Additionally, there is a $60 per year fee ($15 deducted each quarter).

LOAN FEES—There is a one-time initiation fee of $50 for each loan you take from your retirement plan account.

QDRO FEES—There is a one-time fee of $250 for the initial inquiry relating to a domestic relations order and an additional $500 fee to review the order for qualification. These fees are deducted from your account balance and are paid to Aon Consulting.

FEES FOR COLLECTIVE INVESTMENT FUNDS—These are collective trust funds managed by banks or trust companies that pool investments of retirement plans and other similar investors. The Northern Trust funds currently offered through the plan are collective trust funds. Each investor has a proportionate interest in the collective trust fund assets. Like mutual funds, collective investment funds may have a variety of investment objectives. There are no front- or back-end fees associated with a collective investment fund, but there are investment management and administrative fees.

FEES FOR MUTUAL FUNDS—These fees are deducted from each fund’s assets and fall into the following categories:

• Investment management fees—These fees are paid to the fund’s investment manager for overseeing the portfolio. Generally, an index fund, which seeks to match the performance of a particular index, will have lower investment management fees than an actively managed fund in the same asset class.

• Administrative fees (non-T. Rowe Price funds)—Non-T. Rowe Price funds generally have fees for administrative services associated with T. Rowe Price’s processing of transactions involving the funds and maintaining account records. Such fees do not constitute payment in any manner for investment advisory services or for distribution of those funds.

• Other fees—These cover administrative costs, such as maintaining shareholder records and furnishing shareholder statements and financial reports. All fees associated with a mutual fund are disclosed in its prospectus, which you can obtain at rps.troweprice.com or by calling 1-800-922-9945.

REDEMPTION FEES—These fees are charged to an investor who sells shares of a mutual fund on or before a designated holding period specified by the fund. Redemption fees are designed to lessen the effect of short-term trading and protect the fund and its long-term investors. They are paid to the fund to help offset the transaction costs that may be generated by frequent trading. Redemption fees are always described in the mutual fund’s prospectus. As of May 2012, one fund in the plan’s lineup has a redemption fee. Harbor International Fund assesses a redemption fee of 2% on assets held for 59 days or less.

105549_fly_fee_0412118743