PESCO | Power Plants, Oil & Gas, Substations EPC Contractors

Upload

mdlayeequeCategory

view

43download

2

®

EPC Contractors: Changing with the Industry

Larry Bolander

AIChE Management Division ConferenceApril 2007

HO20060444_001.ppt2®

AgendaAgenda

What makes EPC Contractors Successful?

The World Yesterday

The World Today

Where are the Resources?

Staying Up with the Changing Technologies

Market Uncertainty – Procurement Challenges

EPC Challenges

Future State of Industry

HO20060444_001.ppt3®

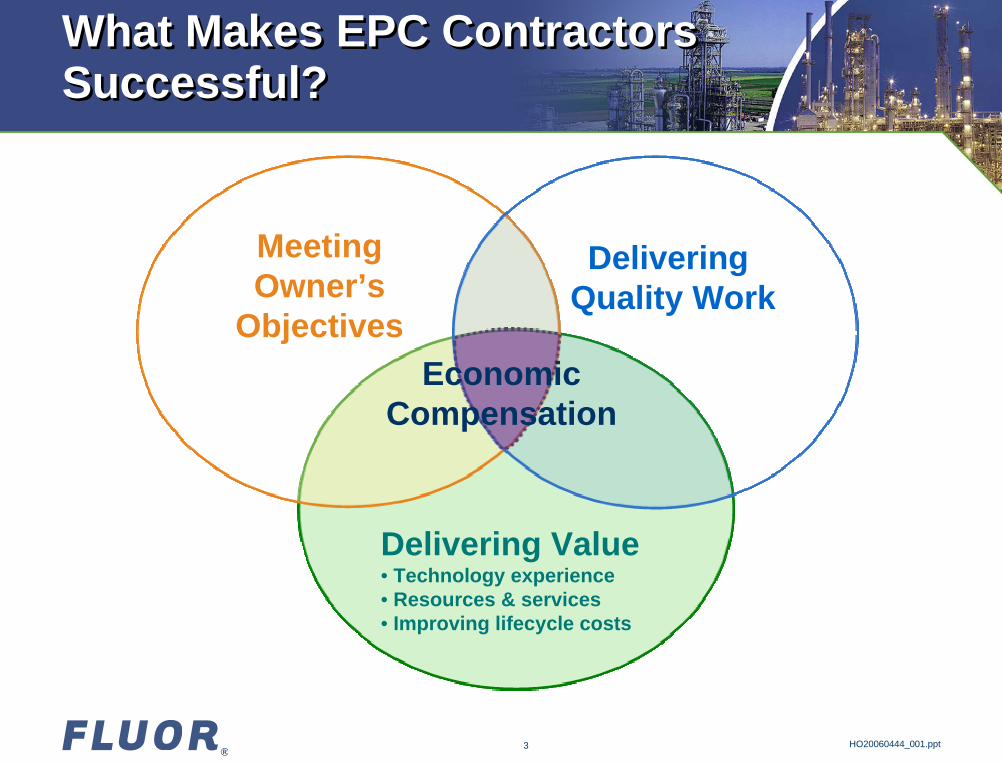

What Makes EPC Contractors Successful?What Makes EPC Contractors Successful?

Meeting Owner’s

Objectives

Delivering Value• Technology experience• Resources & services• Improving lifecycle costs

Delivering Quality Work

Economic Compensation

HO20060444_001.ppt4®

The Contractor’s World YesterdayThe Contractor’s World Yesterday

Few projectsSmall to medium size Mainly revampsSufficient supply in market

– Prices– Deliveries– Resources

Hungry contractorsSporadic mega projects

FEED by select contractorsMixed execution Competitively tendered EPC lump sum projects

Many took risky projects at low (or no) margin

Agreed to onerous contract termsIntegrated, client-led PMC

Previous Execution Strategies Resulting Execution Strategies

“Contractor margins were squeezed by owners from an average of 6 to 10 percent pre-1985 to 2 to 5 percent in the 1990 to 2002 period.”

Independent Project Analysis

HO20060444_001.ppt5®

The Contractor’s World TodayThe Contractor’s World Today

Current SituationDemand exceeds resourcesIncreased project size and complexity

– Mega projects up 900% since 2002

Unstable supply market– Prices– Deliveries– Resources

Shortage of qualified contractors

Execution Strategy for SuccessIncrease in sole source awardsPMC+ contractor FEED & EPC tied togetherNegotiated awards

– Based on contractor’s willingness to commit resources

Construction using multiple qualified contractorsOperating under a “Managed Growth” principle

“Contractor now demands 10-12 percent on a risk-free basis.”Independent Project Analysis

HO20060444_001.ppt6®

Workload DistributionWorkload Distribution

HO20060444_001.ppt7®

IPA Regional Risk Distribution(Regions Displaying Highest Risk Premiums)IPA Regional Risk Distribution(Regions Displaying Highest Risk Premiums)

HO20060444_001.ppt8®

Process Plant Industry Bookings(Sustained Demand Case)Process Plant Industry Bookings(Sustained Demand Case)

Graph compares process plant industry bookings expressed in man-hours compared to the available man-hours in the industry.

* Source is major oil companies including ExxonMobil, the Joint Industry Program, ENR, and Fluor

0

50

100

150

200

250

85 87 89 91 93 95 97 99 01 03 05 07 09Year

MM

MH

/Yr.

Refining Chem/Petrochem O/G Production Synthetic Fuels Effective Capacity

60% Growth between 2005 and 2009 – 3 of 5 new employees

HO20060444_001.ppt9®

Where Are the Resources? N. America Bachelor’s Degrees from 1999-2005Where Are the Resources? N. America Bachelor’s Degrees from 1999-2005

0

10000

20000

30000

40000

50000

60000

70000

80000

1999 2001 2003 2005

Total Disciplines EPC DisciplinesInformation from 334 USA & 7 Canadian Engineering Colleges

Source Michael T. GibbonsAmerican Society for Engineering Education

20% increase in Engineering Bachelor Degrees since 1999

3% increase in 5 major areas for EPC contractors since 1999

27% decrease in Chemical Engineering from 1999 to 2005

12% decrease in Civil Engineering from 1999 to 2005

HO20060444_001.ppt10®

Where Are the Resources? Global Graduates - 1990 vs. 2004Where Are the Resources? Global Graduates - 1990 vs. 2004

1.2 million/year engineers & scientists graduate from Chinese and Indian universities

Chinese & Indian graduates = USA, European & Japanese graduates

China & India = 3x the number 10 years ago

In 1970, USA accounted for 30% of worldwide university enrollment; now, USA is 12%

HO20060444_001.ppt11®

Where are the Resources?Fluor Support Of Educational ProgramsWhere are the Resources?Fluor Support Of Educational Programs

Actively recruit at 100 universities/technical institutes globally

Teaching at US, Kuwaiti, Poland & Chinese universities/schools

Developing global internship opportunities

Strategic partnerships with 15 US universities including:– Philanthropic contributions - engineering/construction departments,

student associations, scholarships– Participation in University Advisory Boards– Teaching & influencing curriculum development – Mentoring, summer internships & new grad recruiting

Commitment to diversity liaison programs– Society of Women Engineers (SWE)– National Society of Black Engineers (NSBE)– Society of Hispanic Professional Engineers (SHPE)

Outreach to 21,000+ elementary, middle school, high school students in 16 countries to raise profile / awareness of engineering

HO20060444_001.ppt12®

Industry Resources ChallengesIndustry Resources Challenges

Lead / management personnel agingLarge experience gap between leads and others

– Stretch / challenge employees– Offer opportunities to enhance skill sets

Recruiting– Higher salary offers to attract new employees– Hiring new grads – Tapping into other industries

Maximizing global resources– Standardizing work processes– Training

Retention– Reward to retain– Flexible company policies

HO20060444_001.ppt13®

Staying Up with the Changing TechnologiesStaying Up with the Changing Technologies

Schools teach “how it’s been done”

Contractors must anticipate trends before owners– Develop expertise– Begin process planning– Connect with licensors / suppliers

Investments shifting to non-petroleum-based plants– Ex. – Nuclear, coal gasification, bio-fuels

Writing the future on modifying processes – Ex. – CAD modified design / construction work processes

Large fabricators/suppliers doing more design work

HO20060444_001.ppt14®

Sharing Knowledge

Senior engineersRotation - Research

Young engineersRotation - Projects

StudentsProjects and Research

CommunityScholars and teachers

Global Execution CentersTraining & Development

RetireesGiving back

Individual Procedures Work processes Projects

All Disciplines

Government and industry collaborative skills initiatives

Training simulators

Operations excellence

Qatar China USA Spain Australia

Knowledge Management

Center

HO20060444_001.ppt15®

Procurement Challenges:Market Uncertainty

Extremely volatile commodity, material and equipment prices

Extending lead times

Higher shop loads

Reasons:– Sustained raw material supply

and demand imbalance– Constraints throughout the

supply chain– Capacity not being added– Consolidation of 21 key

suppliers down to 4

Major Equipment EscalationGeneral Fabricated Equipment

Bulk Materials EscalationFabricated Pipe

HO20060444_001.ppt16®

EPC ChallengesEPC Challenges

Employees’ market – People jumping from company to company– Salaries increasing exponentially– Must market industry better to attract workers

Sharing knowledge

Expand fabricator resource base– Train third-world fabricators– Help them be successful

Owners need contractors to be execution partners– Higher investments (mega projects) require more commitment– Greater investment for contractors to grow business

(salaries, real estate, equipment, training, etc.)– Higher fees – Wall Street expectations

HO20060444_001.ppt17®

Key Relationship Success CriteriaS

treng

th o

f rel

atio

nshi

p

Impact on business performance

Weak

Strong

HighLow

Partner

Trus

t; R

isk

& re

war

d

Added value

Alliance

Compatability

Trust

ClosenessDepth

Reliance

HO20060444_001.ppt18®

Future State of IndustryFuture State of Industry

EPC workload to peak in 2009 – Large drop in “lead” resources in 2-5 years– More projects awarded to less qualified contractor teams– More projects will miss on costs and schedules– Contractors with best teams / tools / processes will succeed– Promoting engineering careers in schools

Contractors / owners / suppliers teaming on new technologies

Continued volatility for commodities / material / equipment

Owners adopting contracting strategies to meet market realities will experience best results

Large fabricators/suppliers doing more design work

®

Questions?

Larry Bolander

AIChE Management Division ConferenceApril 2007