04B Retirement For Better Outcomes Start With a ... - ISCEBS · least $1.75M off of their total DC...

31

The opinions expressed in this presentation are those of the speaker. The International Society and International Foundation disclaims responsibility for views expressed and statements made by the program speakers. Retirement: For Better Outcomes, Start With a Better Design Marc Howell, FSA, EA Vice President, Intellectual Capital Retirement Plan Strategies Prudential Retirement Michele Talka, CEBS, SPHR Director Human Resources Operations Moffitt Cancer Center Tampa Florida 4B-1

Transcript of 04B Retirement For Better Outcomes Start With a ... - ISCEBS · least $1.75M off of their total DC...

The opinions expressed in this presentation are those of the speaker. The International Society and International Foundation disclaims responsibility for views expressed and statements made by the program speakers.

Retirement: For Better Outcomes, Start With a Better Design

Marc Howell, FSA, EAVice President, Intellectual Capital Retirement Plan Strategies Prudential Retirement

Michele Talka, CEBS, SPHRDirector Human Resources

OperationsMoffitt Cancer CenterTampa Florida

4B-1

Key Facts About the Plan Sponsor:Moffitt Cancer Center (MCC)

• NCI designated Comprehensive Cancer Center—only one in Florida • Academic Medical Center: provides cancer diagnosis and treatment on both in-patient

and out-patient basis; world class research facility; educational institution• Located in one metropolitan area—Tampa• Not-For Profit Organization• Employs 4,300 faculty & staff• 75% of population is female• Founded 28 years ago; experienced huge growth last 8 yrs• “Employer of Choice” in Tampa (Working Mothers Top 100, Included in multiple “Best

Places to Work” Lists Tampa & Florida• $290M in retirement assets • Complex retirement structure: 403(b), 401(a), 457(f) & (b), 401(k)• Some special groups with additional contributions “side benefits”

4B-2

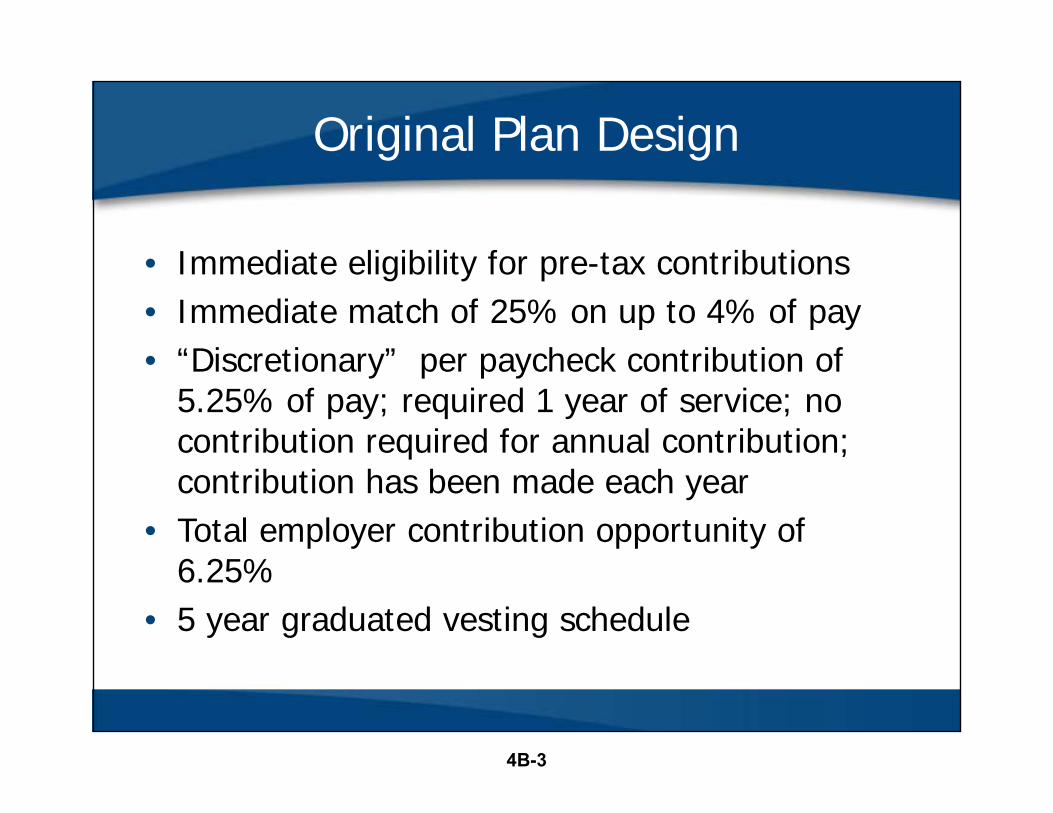

Original Plan Design

• Immediate eligibility for pre-tax contributions• Immediate match of 25% on up to 4% of pay• “Discretionary” per paycheck contribution of

5.25% of pay; required 1 year of service; no contribution required for annual contribution; contribution has been made each year

• Total employer contribution opportunity of 6.25%

• 5 year graduated vesting schedule

4B-3

Delayed Retirement in Organization

4B-4

Increasing Tenure On The Job

• Moffitt has a mixed population in terms of tenure• Tenure is not just time on the job. Instead a build up of

knowledge, contacts and skill from performing different jobs, experiences and circumstances with a variety of co-workers and clients in a career with one employer.

• Not all business models value or need tenure. If skills can be easily acquired by the available labor market-using contract or temporary labor.

• This model values current performance and knowledge and positions are easily filled by the outside.

• Delayed retirement in this case negatively impacts revenue and profits.

4B-5

Effect On Organization of Delayed Retirement

Although tenure may be held in high regard, there are potential conflicts if employees work longer than anticipated:• The next generation of workers may be depleted if, seeing

their prospects for advancement being put on hold, they look elsewhere for opportunities.

• Productivity may suffer if some employees continue to work merely because they cannot afford to retire.

• The cost of benefit programs may inch up if health and disability plan usage increases, as may be expected from older employees.

4B-6

Steps in the Right Direction2009 & 2010

• In 2009 added an “opt-out” auto enrollment feature.– Auto enrolled new hires at 4%; re-enrolled current participants at

4% unless they opt-out– Moved from 65% participation to 87% participation!

• Added an “opt-in” auto escalation feature– Scheduled to occur in July to coincide with our annual merit

process• In 2010 due to financial constraints moved to an annual,

year-end payment of the “discretionary” contribution. Reduced cost by $235k due to turnover forfeitures

4B-7

2012 Questions

4B-8

2012 Questions

Highest turnover in our Millennial Age

Group

Spending more each year but seem to be getting less Not enough team members

estimated to reach that optimal replacement ratio

4B-9

We Started Down the Path…

• Sought Executive buy in to making changes– Described the changing landscape of retirement– Described issues with the current plan not meeting

today’s objectives– Provided estimates of cost savings that could result

(generated in house)

• Complexity of our plans drove the need for outside expertise; we needed actuarial help for testing the options to ensure compliance.

4B-10

Doesn’t Have To Be A Lengthy Process

Week 1 – 2: Assess Current Retirement Program

Week 3 – 6: Define goals of Plan Redesign

Week 6 – 9: Compare current

program to redesign

alternatives

Week 9: Presentation of Results and Decision

4 meetings over 9 weeks

4B-11

Elements to Consider

Set Objectives

What is Working and What is Not?Develop guidelines for Change/Priorities

Establish Baseline

Assess Current ProgramCompetitive Market AnalysisReplacement Ratio AnalysisEmployer CostGap Analysis

Review & Refine Alternatives

Changes in replacement ratio analysisEmployer CostGap AnalysisNon‐discrimination testing implications and implementation

4B-12

What Is Working/What Isn’t?

• What is our organization’s philosophical view? – Who is responsible for retirement and why? – Where should we be positioned in the competitive landscape?

• Does the current plan provide a strong foundation to the overall employee retirement plan? Why or why not?

• Does it act as a significant recruiting and retention tool—is it still competitive?

• What sort of workforce behavior do we want to motivate?• Is it cost effective? What are its costs?• Is there a better alternative that will deliver the desired benefits?• Should the plan incentivize long service? How?• Who are my Competitors? Is my plan competitive?

4B-13

What Wasn’t Working!

• Our plan encouraged doing nothing about retirement!– No personal saving required for a substantial employer

contribution. Resulted in a lot of non-active participants– Our contribution amount (set 28 years ago) led people to

believe they would have enough for retirement without doing anything more (implicit communication)

• Once we got them in, we weren’t motivating them to save more over time– Auto-enrolled at 4% then nothing more– Match was the same regardless of how much you saved– Human Inertia meant most stayed at 4%

4B-14

Behavioral Finance

• Behavioral finance concepts in retirement plans can be used to overcome human inertia, information overload and procrastination in three key areas while still providing worker choice and achieving better long term outcomes:1. Participation2. Contribution/saving rate3. Investment choices

4B-15

Behavioral Finance

1. Participation– Default—no action then no personal savings– New Deal Solution

• 30 days to enroll pro-actively or auto enrolled at percentage to maximize matching contributions

2. Savings Rate– Default—employer contribution only– New Deal Solutions

• No personal savings, no employer contribution• Auto escalate % per year to a maximum• Increasing match with increased savings rate• Allow for loans

3. Investment Choice1. Default—Least risk/return Fund2. New Deal Solutions

• Diversified portfolio based on age with moderate risk• Rebalancing of portfolio to maintain diversification

4B-16

Objective RankingPredictable / Stable CostFunding FlexibilitySimplicityFacilitate Recruitment Younger / Early Career

Mid CareerExecutives

Foster Employee AppreciationEnsure Benefit AdequacyMinimize Employee and Investment RiskPromote Joint EE / ER ResponsibilityProvide Guaranteed BenefitsProvide Portable BenefitsProvide Competitive BenefitsIncentives for Targeted Employee GroupsCommunication and Employee UnderstandingEmployer AdministrationOther

Promote Retention Younger / Early CareerMid CareerExecutives

Prioritize Objectives

4B-17

It’s a Balancing Act….

Budgetary Constraints

4B-18

Our Goals For Defined Contribution Optimization

(DCO) Project

• Reduce Organization Cost• Improve Employee Retirement Outlook• Reduce Turnover in younger staff; facilitate

earlier (on-time) retirement for more senior staff• Better understand market practices to improve

recruiting value of plan

4B-19

Guiding Principles

1. Increase Employee Savings: Incentives provided to employees to increase savings. Use of behavioral finance principles—taken advantage of human inertia where appropriate via auto-enrollment/auto-escalation.

2. Reduce Current Cost by $1.75M at least, either structurally or through stretching employee deferrals: Moffitt would like to trim at least $1.75M off of their total DC expenditures if possible.

3. Maintain Vesting at appropriate length: This will allow Moffitt to continue to take advantage of forfeitures while taking into consideration the competitive environment.

4. Keep it Simple: Minimal changes if possible, ease of communication paramount.

5. Consider Safe Harbor where appropriate: The ability to avoid ADP testing is a worthwhile goal, if balanced against other considerations.

4B-20

Competitive Market Analysis

4B-21

Unknown Rules for St. Joseph and Cedars‐Sinai

Years o

f Service

* Source: Prudential Retirement, April 5, 2012 and August 23, 2012

Competitive Environment—Vesting Schedules*

4B-22

Current Program’s Projected Results

0-4 5-9 10-14 15-19 20-24 25-29 30-34 35+

<25 87% 91%

25-29 72% 73% 76%

30-34 63% 67% 69%

35-39 54% 56% 64% 61%

40-44 50% 49% 57% 64% 69%

45-49 44% 45% 49% 55% 56% 50%

50-54 42% 44% 47% 44% 52% 56%

55-59 39% 42% 46% 49% 44% 45%

60-64 40% 43% 45% 46% 46% 41% 11%

65+ 57% 45% 64% 39% 53% 37% 15%

Less than 40% Replacement Ratio

40% - 59% Replacement Ratio

60% - 79% Replacement Ratio

At Least 80% Replacement Ratio

AVERAGE REPLACEMENT RATIO AT AGE 65Years of Service

Age

4B-23

DC Optimization Option #1a

• Defined Contribution program has three distinct pieces– Safe Harbor Matching Employer contribution to all participants (post

PPA version) achieved through a matching program as follows:• First 3% of employee deferrals 100% Match• Next 7% of employee deferrals 50% Match

– For those employees for whom 10% deferrals would go beyond the deferral limit each year (and thus would reduce their possible match), all excess deferrals (and match) would be moved to the NQ program

– “Side Benefits” would be maintained in qualified program

• Auto Enrollment at 4%, both retroactively (once) and prospectively (ongoing)

• Auto-escalation 1% per year to 6%• 3-year Vesting for retirement program for all participants• All other plan provisions the same

4B-24

Option #1a

ADP Test deemed satisfied under ADP safe harbor (applicable to 401(k) plan only)

Required Tests*

ACP TestTop Heavy Test

(403(b) deferrals not included)

General Nondiscrimination

Test

* Minimum Coverage (except with regard to 403(b) deferrals), Annual Additions Limit, and 402(g) Limit testing are required of all plan designs.

Analysis of Projected Results:• ACP, Top Heavy and General Nondiscrimination tests are projected to pass by a comfortable margin.• It appears key employees hold less than 5% of plan assets, so becoming top heavy should not be a near

term concern.• Since the subset of employees receiving the “side benefits” is relatively small, the General

Nondiscrimination test may be sensitive to changes in demographics (e.g. average age) or classification (e.g. NHCE or HCE) of the benefitting employees. The plan’s formula is designed to allow for maximum flexibility in meeting the requirements.

DC Optimization Option #1aNondiscrimination Considerations

4B-25

Long term forfeitures estimated to be reduced by roughly $1M per year under this scenario

DC Optimization Option #1a—Cost Projections

4B-26

Assumes auto enrollment at 4% (retroactively and prospectively) and auto escalation to 6%All calculations as of 1/1/2012Includes all 401(k) contributions, investment earnings, and social security benefits

0-4 5-9 10-14 15-19 20-24 25-29 30-34 35+

<25 76% 85%

25-29 72% 72% 80%

30-34 65% 69% 74%

35-39 55% 58% 66% 66%

40-44 50% 51% 58% 66% 68%

45-49 45% 46% 50% 56% 58% 49%

50-54 42% 44% 48% 45% 52% 57%

55-59 39% 42% 46% 49% 45% 46%

60-64 40% 43% 45% 46% 46% 41% 11%

65+ 57% 45% 64% 39% 53% 37% 15%

AVERAGE REPLACEMENT RATIO AT AGE 65Years of Service

Age

Less than 40% Replacement Ratio

40% - 59% Replacement Ratio

60% - 79% Replacement Ratio

At Least 80% Replacement Ratio

DC Optimization Option #1a—Entire Employee Population

4B-27

Choose your path wisely

4B-28

Observations

1. By expanding implementation of the autos or otherwise increasing savings by employees, Moffitt cut employer costs while driving better employee outcomes

2. Any change from the current 5 year vesting schedule will be costly, but may be worthwhile given observed competitive behavior (and recent experience when recruiting)

3. Individuals will be the primary drivers of their own retirement success.

4B-29

Implementation

• Review options with benefits attorney• Amend retirement plan documents • Develop and distribute employee communications

– Lots of meetings!– Webinar online– Newsletter articles– Manager “huddle” notes

• Update administrative process • Implement new plan design

4B-30

Results To DateOn track to save $2M this fiscal year

4B-31