01 June 2020...3 Mediclaim –US$ 2.6k (ESC). Life Insurance –US$13.3k. No Cover. Dependent on...

24

Gaurava Gupta 01 June 2020 EVP – Health & Benefits Consulting

Transcript of 01 June 2020...3 Mediclaim –US$ 2.6k (ESC). Life Insurance –US$13.3k. No Cover. Dependent on...

Gaurava Gupta

01 June 2020

EVP – Health & Benefits Consulting

2

Based in Hyderabad, Gaurava is part of Health & Benefits

Consulting team at MMB India. He provides consulting support

to Hyderabad and Chennai offices and also leads Darwin and

Benefits Asia projects for India. Prior to taking up his current

role, he was Branch Leader for JLT’s Hyderabad office and has

also worked with various health and life insurance companies

in past as underwriter and pension fund manager.

Gaurava is a strong advocate of Shared Cost (Flexible) Model

for India and HR Automation. He also works on creating

bespoke wordings for new age covers for India like LGBTQ

inclusion, autism and mental health, gender reassignment

treatments and advanced cancer care, among others.

Gaurava has done Masters in business administration from IBS

and he his passion for continuous learning has taken him to

several other colleges like IIM – B, TU Delft and T.H. Chan

School of Public Health for business related studies.

Agenda

• Understanding India Today

- Some Interesting Statistics

- Economic reforms and GDP growth

Social Security and Employee Benefits in India

- Statutory and Voluntary Benefits

- Challenges

- Shared Cost Model

Covid-19 Updates

Introduction to Mercer Marsh Benefits India

3

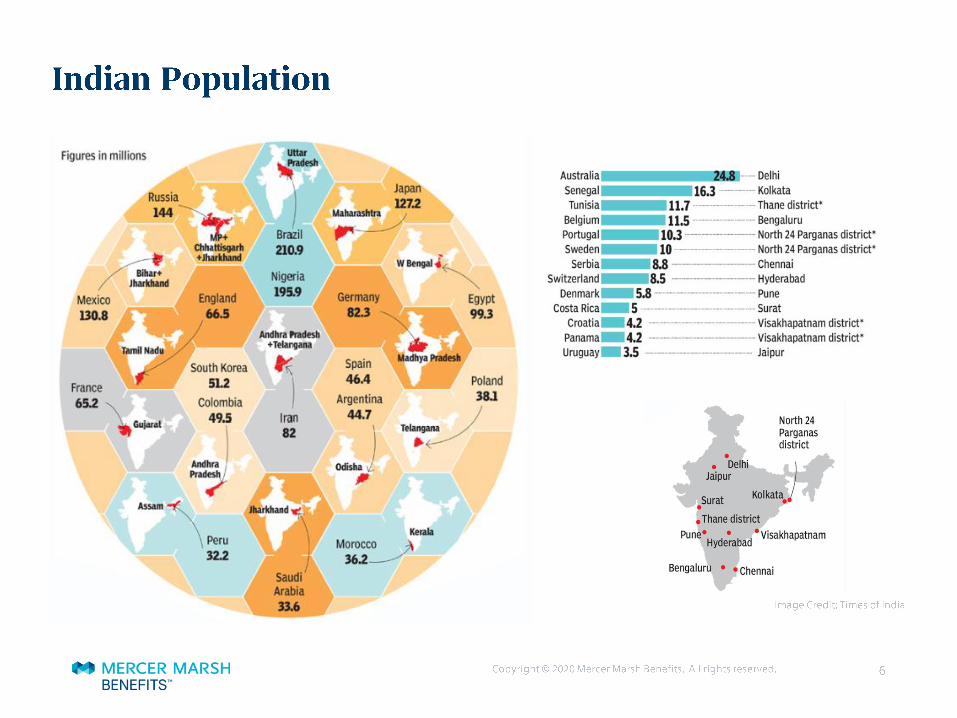

Understanding India Today

5th Largest

Economy –

Expected to be 3rd

largest by 2030

Main IndustriesIT & ITES, Textiles,

Pharmaceuticals, Iron &

Steel, Petrochemicals,

Automobile, Banking &

Insurance

Top ExportersUSA - $44.3bn, UAE -

$28bn, China - $14.8bn,

Hong Kong - 12.7bn

Top ImportersChina - $68.8bn, USA -

$22.8bn, UAE - $22.1bn,

Switzerland - $20.9bn,

Saudi Arabia - $19.4bn

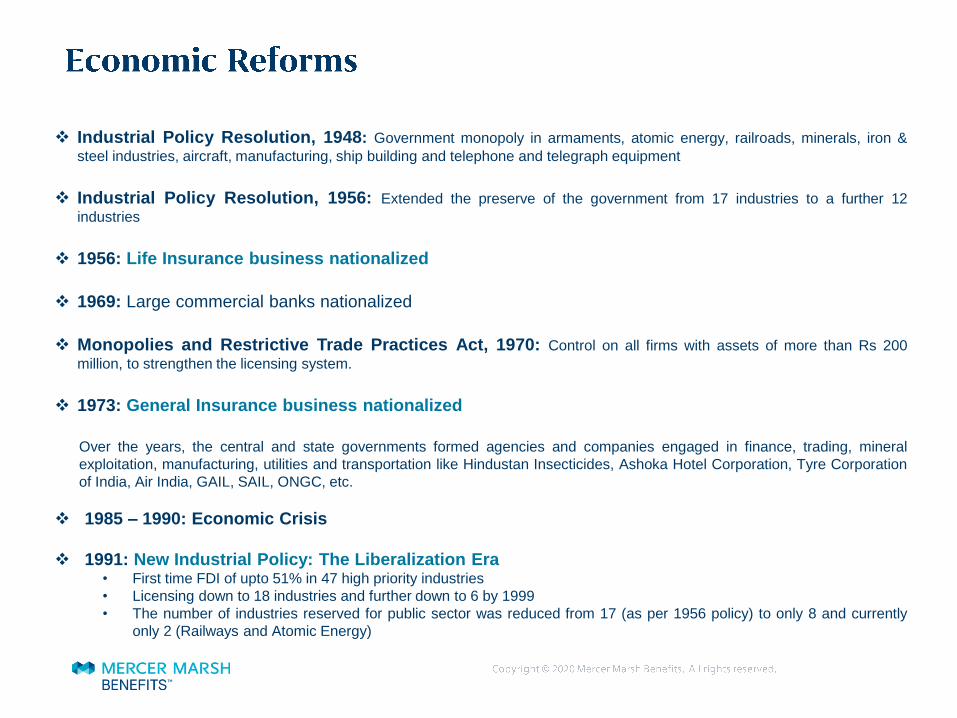

Industrial Policy Resolution, 1948: Government monopoly in armaments, atomic energy, railroads, minerals, iron &

steel industries, aircraft, manufacturing, ship building and telephone and telegraph equipment

Industrial Policy Resolution, 1956: Extended the preserve of the government from 17 industries to a further 12

industries

1956: Life Insurance business nationalized

1969: Large commercial banks nationalized

Monopolies and Restrictive Trade Practices Act, 1970: Control on all firms with assets of more than Rs 200

million, to strengthen the licensing system.

1973: General Insurance business nationalized

Over the years, the central and state governments formed agencies and companies engaged in finance, trading, mineral

exploitation, manufacturing, utilities and transportation like Hindustan Insecticides, Ashoka Hotel Corporation, Tyre Corporation

of India, Air India, GAIL, SAIL, ONGC, etc.

1985 – 1990: Economic Crisis

1991: New Industrial Policy: The Liberalization Era• First time FDI of upto 51% in 47 high priority industries

• Licensing down to 18 industries and further down to 6 by 1999

• The number of industries reserved for public sector was reduced from 17 (as per 1956 policy) to only 8 and currently

only 2 (Railways and Atomic Energy)

$2104

Social Security and Employee Benefits in India

Typical Family Structure

1No social security. Dependent on personal savings. Have spent earnings

on marriage, house, jewellery, children education and medical expenses.

3 Mediclaim – US$ 2.6k (ESC). Life Insurance – US$13.3k.

No Cover. Dependent on Employee.

Covered under Spouse’s mediclaim plan. Maternity excluded.

10

Father/

Father-in-law

Mother/

Mother-in-law

Spouse

Employee

Child 1

Child 2

Sibling

No social security. Housewife. Lifestyle related ailments.

Parents Mediclaim. Dependent upto 24yrs.

Parents Mediclaim. Dependent upto 24yrs.

Mortality Risk Covers Statutory plans and employer sponsored benefits

Employee Compensation

Act 2017(Workmen

Compensation Act 1923)

Group Term Life Insurance

Plan

(2x Annual Salary)

(74%)

Employee Deposit Linked

Insurance (Insurance Scheme

1976) – Max US$ 8k

Personal Accident Insurance

(3x Annual Salary) (94%)

Sta

tuto

ry B

en

efi

tsV

olu

nta

ry B

en

efits

Gratuity

(DB Plan)

(Payment of Gratuity Act 1972) – Max US$

26.67k in lifetime

Top-up

Spouse

Top-up

Spouse

Keyman

PMJJBY (US$ 2.67k –US$ 4.4/pa) –

55mn lives

Health Risk Covers Statutory plans and employer sponsored benefits

Employee Compensation

Act 2017 (Occupational

Disease)

Group Mediclaim Insurance

(US$1333 –13,333k)

(Mode – US$4.67k)

(100%)

Employee State

Insurance

(ESI Act 1948 – Start 1952)

Upto US$ 280/m

Critical Illness

Sta

tuto

ry B

en

efi

tsV

olu

nta

ry B

en

efits

ESI Employee Mini Plans

Contractua

l Staff

Retired

Employees

Global

Cover

Voluntary

Top-up

Voluntary

Personal

Plans

Parent’s

Plan

Self

Insurance

Plans

OPD Plans

Accident & Disability Covers Statutory plans and employer sponsored benefits

Employee Compensation

Act 2017

Group Term Life Insurance

Plan

Employee Deposit Linked

Insurance (Insurance

Scheme 1976) – Max US$ 8k

Personal Accident InsuranceS

tatu

tory

Ben

efi

tsV

olu

nta

ry B

en

efits

Gratuity

(DB Plan)

(Payment of Gratuity Act 1972) – Max US$

26.67k in lifetime

Partial Permanent Disability

Top-up

Spouse

Accidental Total

Permanent Disability

Accident & Sickness

Total Permanent Disability

• PTD

• PPD

• TTD – Weekly Benefits

• House/ Vehicle Modification

• Medical

• School Fee

• Dependent Travel

• Legal Fee

• Repatriation of remains

• Funeral Expenses

• Life Support Equipment

• External Aids

PMSBY (US$ 4k –US$ 16c) – 142mn

lives

Critical Illness

Terminal Illness

Retirement & Pension programs Statutory plans and employer sponsored benefits

Gratuity

(DB Plan)

(Payment of Gratuity Act 1972) – Max US$ 26.67k

in lifetime

Superannuation – Max 15% of Basic

Salary and upto INR 100k

Provident Fund

(Employees Provident Fund Act

1952)

(12% of Basic Salary from Employee + 12% of Basic Salary from

Employer)

Leave Encashment

– Tax free for central/ state govt.

employees and dependents of deceased employees. Least of the following tax

free for others:Amount notified by the Government

(300k)Actual leave encashment

Average basic salary for 10 months

Sta

tuto

ry B

en

efi

tsV

olu

nta

ry B

en

efits

National Pension System – Upto INR 200k/year

Voluntary Provident Fund

(Upto 88% of Basic Salary)

Gratuity linked GTLI

What is adding to healthcare costs

Medical Inflation

8.5%

Increase in Critical Illness

5%

Lifestyle related ailments

3%

Defensive Medicines

Advanced Medical Treatments

Expensive Medicines

Increase in Life Expectancy

Lack of Public Healthcare Infrastructure

0.5 beds/ 1000 – Global Avg 5.0

0.8 doctors / 1000 – Global Avg 3.4

Avg. Consultation Time – Under 2min

Hospital Acquired Infection – 20%+ (US 7 %– 11%)

Adverse Drug Reaction – 3%+

H&B – Changing Landscape/ Emerging Trends

Biggest challenge in benefit provision & engagement?

84% said it was ‘Rising Health care cost’

Cost Management Tool?

Co-pay on claims-34% Flexible Benefits-54%

Most important focus area for all employers?

Insurance (100%)

Health & Wellbeing (92%)

93% employers want

to enhance Employee Engagement &

Experience

72% employers want

to create a

Diverse and Inclusive work environment

Trending benefits

Preventive care, D&I,

Mental Well-being

Wellness strategy Improve awareness on

Health (83%) &

Enhance Employee Engagement (85%)

Source: Marsh Changing Landscape & The Emerging Trends 2019 – 20 Report

KEY INDUSTRIES- 161 PARTICIPANTS

ITeS

20%

HIGH TECH

16%

MANUFACTURING

13% 4%

RETAIL

73% with a base of

5000+ employees

How Benefit Marketplace (Flex) can help

C ON V E N T I ON AL B E N E F I T S

D e f i ne d B e ne f i t s

Similar coverages for all employees

Limited / No Choice to employees, for deciding their benefits

Limited to Health, Life and Accident Insurance

Employer decides on Benefits

Employer absorbs future cost increase

Employee often undervalues cost benefits

F L E X I B L E B E N E F I T S

Defined Contribution

Holistic approach on Health & Wellness

Option to select more appropriate family

definition

Option to select insurance cover limits

Benefit marketplace

Basic minimum cover for contingencies

Freedom to spend on plan of choice

insurance/ wellness/ other perks

Voluntary niche care covers

Employer retains spend control

OFFER CHOICE

ONE SIZE FITS ALL

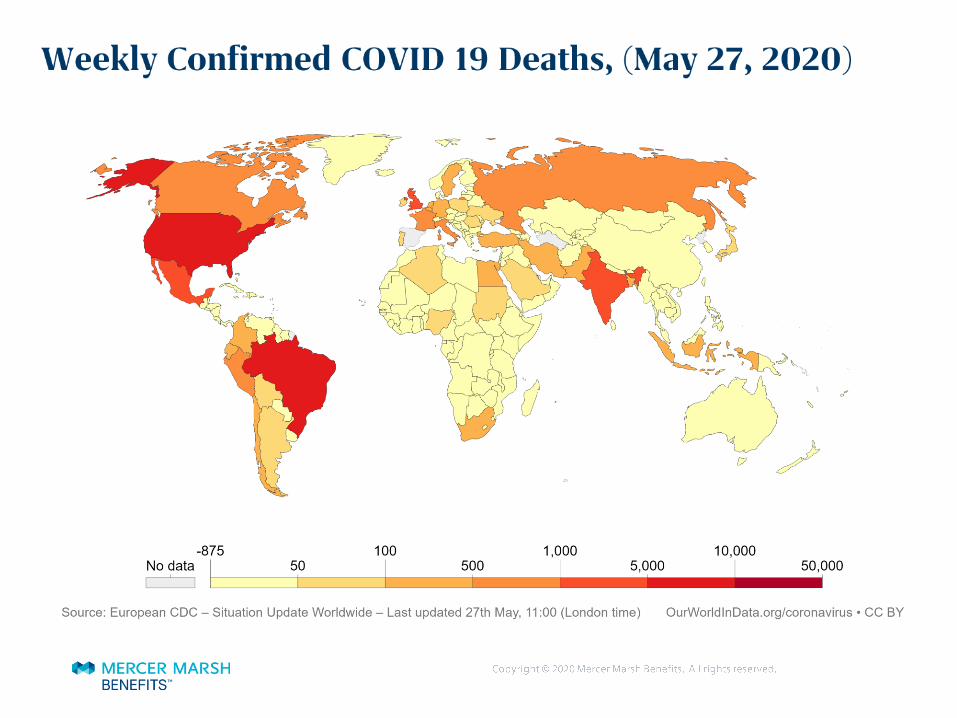

Covid-19 Latest Updates

Covid-19 Reminders

Cases in India –May 28

• Total accumulated confirmed # of cases: 158,333

• Last 1 day count # of cases: 6387

• # Deaths: 4,531

• # Cured: 67,692

Lockdown

• Phase 1:25 March 2020 –14 April 2020 (21 days)

• Phase 2: 15 April 2020 –3 May 2020 (19 days)

• Phase 3: 4 May 2020 –17 May 2020 (14 days)

• Phase 4: 18 May 2020 –ongoing (10 days); scheduled to end on 31 May 2020

Social

• 33% of workforce allowed with social distancing and sanitization norms

• Malls remain closed. Other shops and outlets open on odd-even basis or alternate day basis. Educational institutions remain closed

• Single rider on two wheeler and max two in a four wheeler. Flights resumed.

• Loan moratorium – 6 months , Insurance renewal extension, subsidized loans for SME

19

Cost of COVID-19 Treatment

Parameters Health Insurance Policies – India

In-patient Treatments Covered only for COVID – 19 positive cases. Upto Sum Insured

Out-patient Treatments Subject to individual policy terms. Negative cases can be covered if OPD plans are provided by the employer and

opted by employee during enrolment

Quarantine Chargers Covered only for COVID – 19 positive cases (at registered health facilities)

Confirmed COVID -19 Cases

Mild/ Pre Symptomatic

Regular temperature and

pulse oximetry monitoring.

Discharged post 10 days

of hospitalization

Treatment Cost

INR 85k – INR 120k

Moderate Severe

Discharged after 10 days of

symptom onset

• Absence of fever in 3 days

• Resolution of breathlessness

• Oxygen saturation above

95% for 4 consecutive days

Treatment Cost

INR 85k – INR 120k

Symptoms not resolved and

demand for oxygen therapy to

continue beyond 10 days

Discharged only after

• Resolution of clinical

symptoms

• Ability to maintain oxygen

saturation for 3 consecutive

days

Treatment Cost

INR 250k – INR 400k

Including immune

compromised cases (HIV,

Transplant, Malignancy)

Discharged only after

• Clinical recovery Patient

tested negative once by

RT – PCR (after

resolution of symptoms)

Treatment Cost

INR 500k – INR 1000k

7 days home isolation post

discharge

Teleconferencing – 14th

Day

7 days home isolation post

discharge

Introduction to MMB’s Capabilities in India

23

Clients including premier IT-

ITES BFSI, Life Science &

Core sector clients

M M B I N I N D I A W H AT D O E S I T M E A N F O R Y O U ?

Annual premium in

Employee Benefits

Employee Benefits Broker in

India by Premium placed

Years in India market

Health & Benefits experts

including Consulting, Account

Management, Flex, Health &

Wellness, Communication &

Operations

1st

1500+

US$ 320M+

No. 1*

17+

300+

• Wider experience across multiple

industry segments & managing large EB

programs

• Strong leverage for negotiation & ability

to design competitive benefits

• Thought leadership to support you on

consultative engagement to ensure you

stay ahead.

• Strong focus on Account Management

* Measured by value of insurance premiums under management.

M A R S H I N D I A

First Licensed Composite Broker in India

1 7 C I T I E S | $ 7 7 0 M N

P R E M I U M | 4 0 0 0 C L I E N T S

![Agito mediclaim turkish v1.0 20121031 [repaired]](https://static.fdocuments.net/doc/165x107/55899306d8b42a0b768b45b3/agito-mediclaim-turkish-v10-20121031-repaired.jpg)