McGraw-Hill/Irwin Copyright © 2008 The McGraw-Hill Companies ...

Upload

horace-reevesCategory

view

221download

1

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-1

OPERATIONAL BUDGETING

Chapter

23

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-2

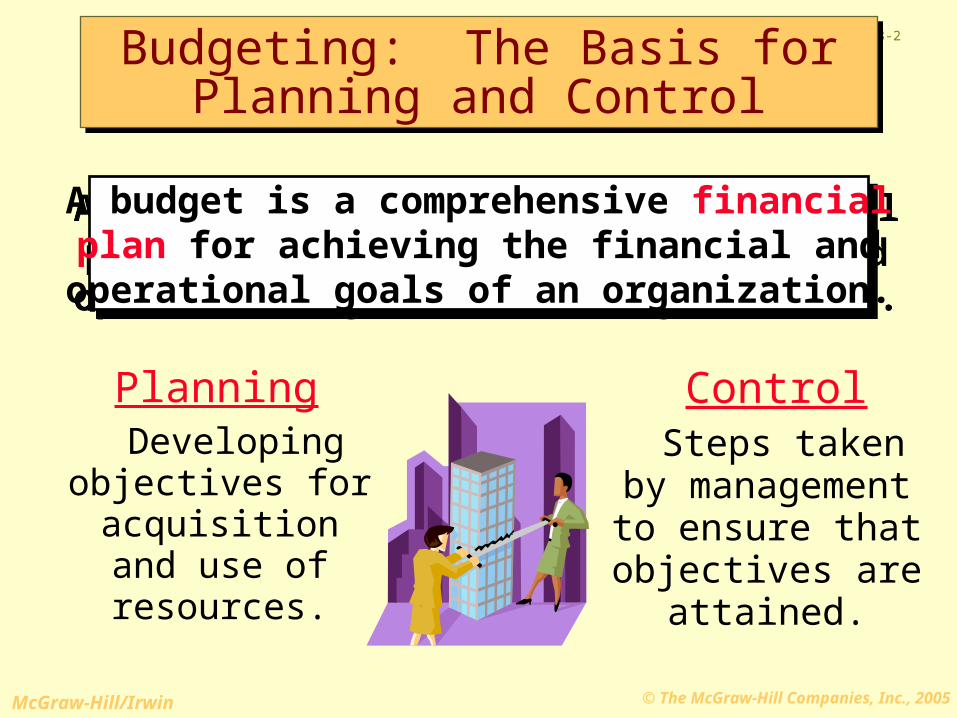

Control Steps taken by

management to ensure that

objectives are attained.

Planning Developing objectives for

acquisitionand use of resources.

A budget is a comprehensive financialplan for achieving the financial and

operational goals of an organization.

A budget is a comprehensive financialplan for achieving the financial and

operational goals of an organization.

Budgeting: The Basis forPlanning and Control

Budgeting: The Basis forPlanning and Control

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-3

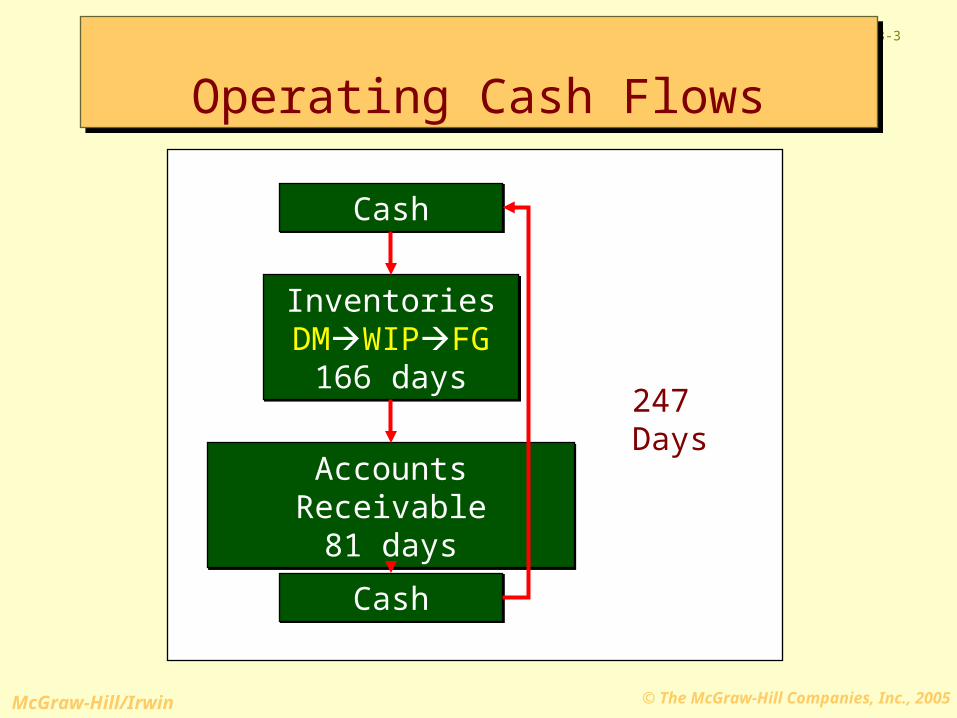

Operating Cash FlowsOperating Cash Flows

CashCash

InventoriesDMWIPFG

166 days

InventoriesDMWIPFG

166 days

Accounts Receivable81 days

Accounts Receivable81 days

CashCash

247 Days

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-4

BenefitsCoordinationof activities

Coordinationof activities

Performanceevaluation

Performanceevaluation

Enhanced managerialresponsibility

Enhanced managerialresponsibility

Assignment of decisionmaking responsibilitiesAssignment of decisionmaking responsibilities

Benefits Derived from BudgetingBenefits Derived from Budgeting

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-5

Budget Problems

Perceived unfair or unrealistic goals.

Poor management-employee communications.

Budget Problems

Perceived unfair or unrealistic goals.

Poor management-employee communications.

Solution

Reasonable and achievable budgets.

Employee participation in budgeting process.

Solution

Reasonable and achievable budgets.

Employee participation in budgeting process.

Establishing Budgeted Amounts: The “Behavioral” Approach

Establishing Budgeted Amounts: The “Behavioral” Approach

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

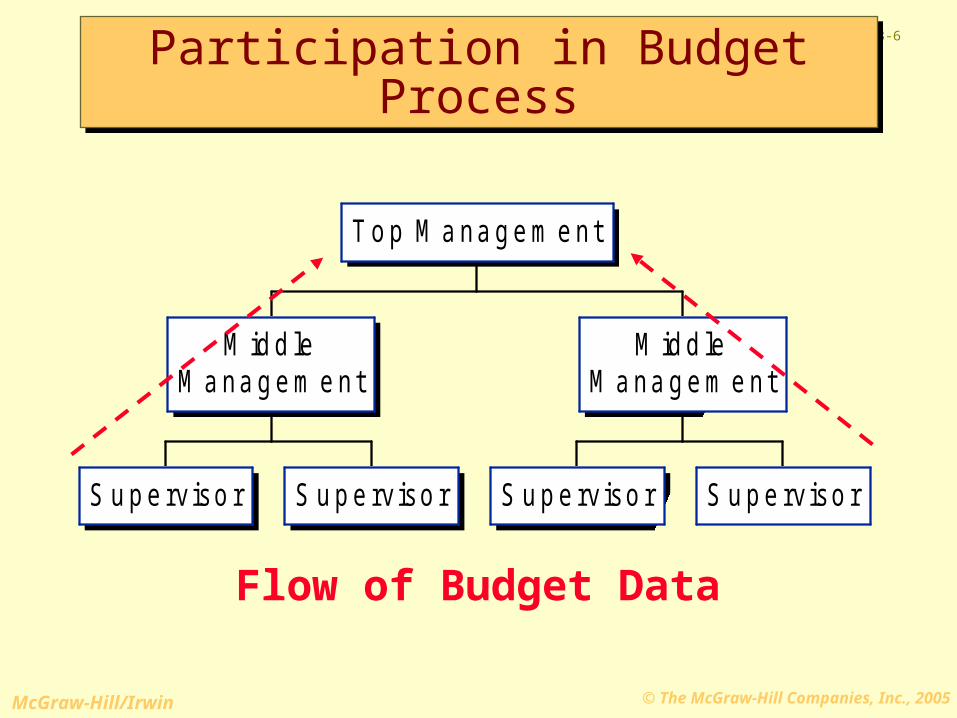

23-6

Flow of Budget Data

S u p e rv iso r S u p e rv iso r

M id d leM a na g e m e nt

S u p e rv iso r S u p e rv iso r

M id d leM a na g e m e nt

T o p M a na g e m e nt

Participation in Budget ProcessParticipation in Budget Process

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-7

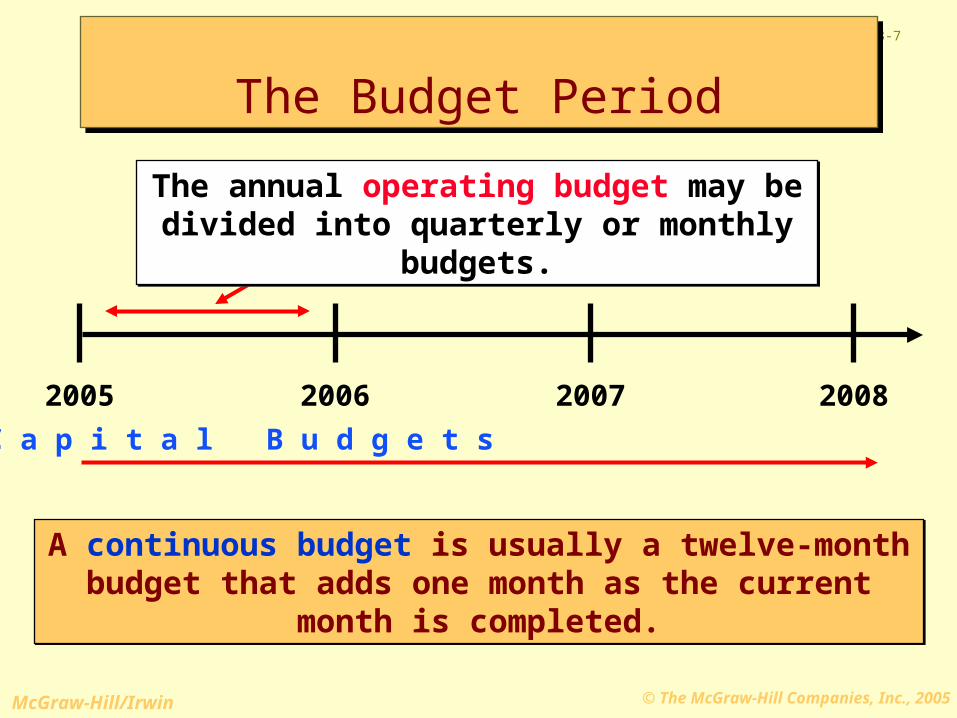

2005 2006 2007 2008

C a p i t a l B u d g e t s

A continuous budget is usually a twelve-month budget that adds one month as the current month is completed.A continuous budget is usually a twelve-month budget

that adds one month as the current month is completed.

The annual operating budget may be divided into quarterly or monthly budgets.

The annual operating budget may be divided into quarterly or monthly budgets.

The Budget PeriodThe Budget Period

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-8

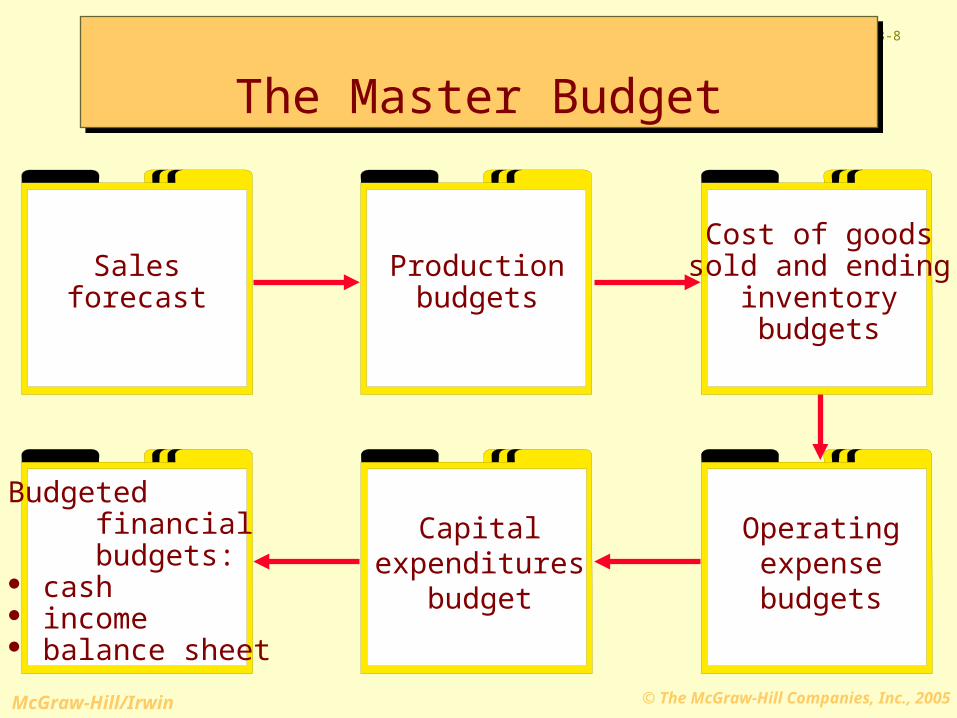

Salesforecast

Productionbudgets

Budgeted financial budgets: cash income balance sheet

Capitalexpenditures

budget

Operatingexpensebudgets

Cost of goodssold and ending

inventorybudgets

The Master BudgetThe Master Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-9

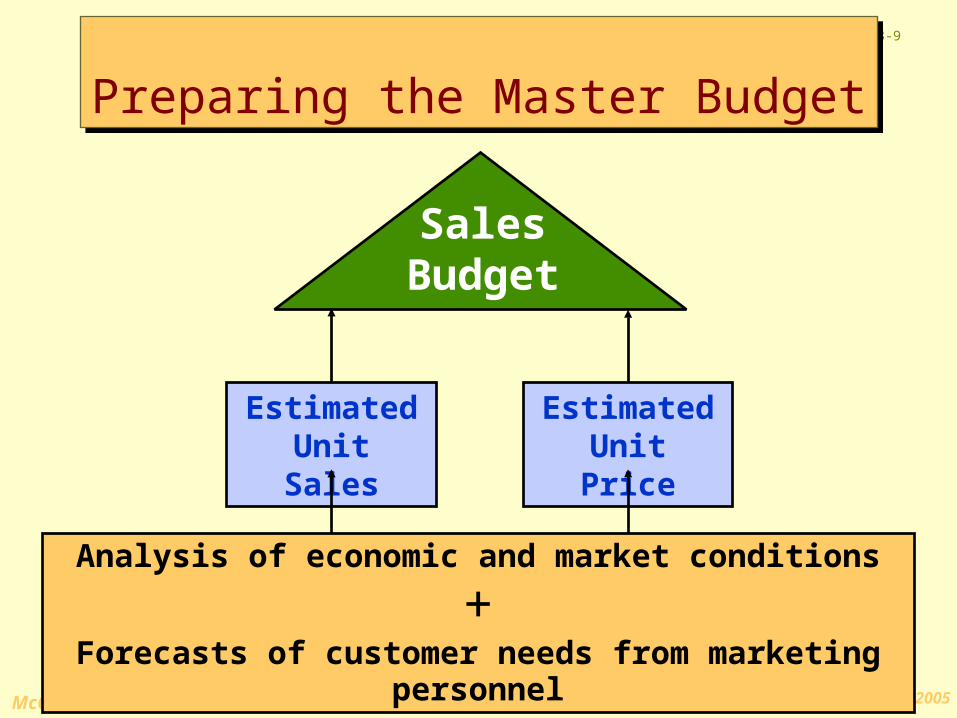

SalesBudget

EstimatedUnit Sales

EstimatedUnit Price

Analysis of economic and market conditions

+Forecasts of customer needs from marketing personnel

Preparing the Master BudgetPreparing the Master Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

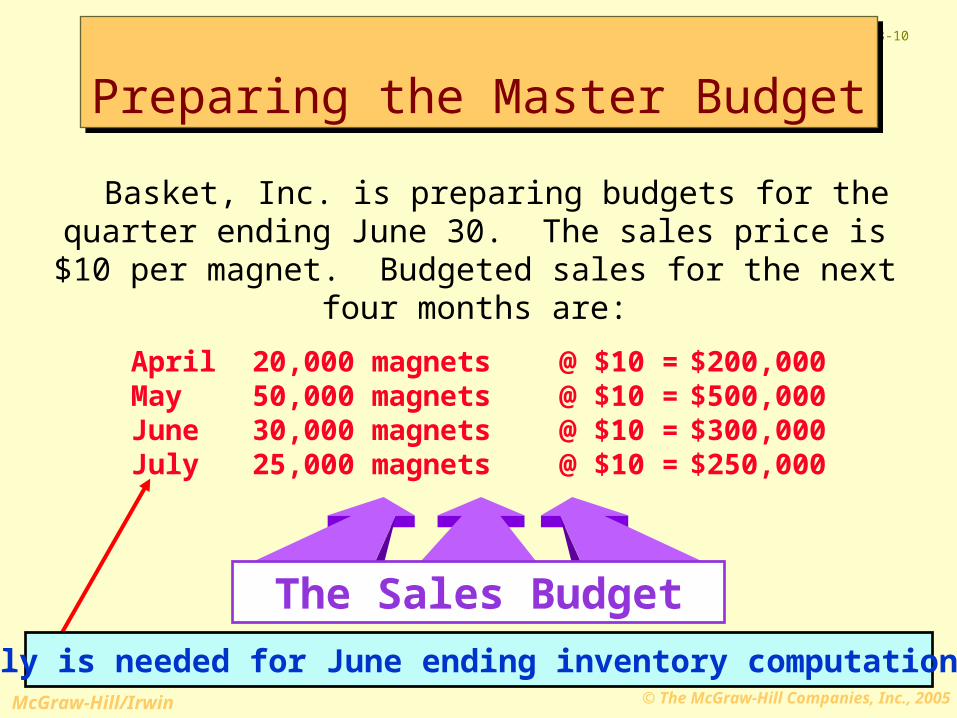

23-10

Basket, Inc. is preparing budgets for the quarter ending June 30. The sales price is $10 per magnet. Budgeted

sales for the next four months are:

April 20,000 magnets @ $10 = $200,000May 50,000 magnets @ $10 = $500,000June 30,000 magnets @ $10 = $300,000July 25,000 magnets @ $10 = $250,000

The Sales Budget

July is needed for June ending inventory computations.

Preparing the Master BudgetPreparing the Master Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-11

Sales Budget

Complete

d

ProductionBudgets

The Production BudgetThe Production Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-12

The management of Basket wants ending inventory to be 20 percent of the next

month’s budgeted sales in units.

4,000 units were on hand March 31.

Let’s prepare the production budget.

The management of Basket wants ending inventory to be 20 percent of the next

month’s budgeted sales in units.

4,000 units were on hand March 31.

Let’s prepare the production budget.

The Production BudgetThe Production Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-13

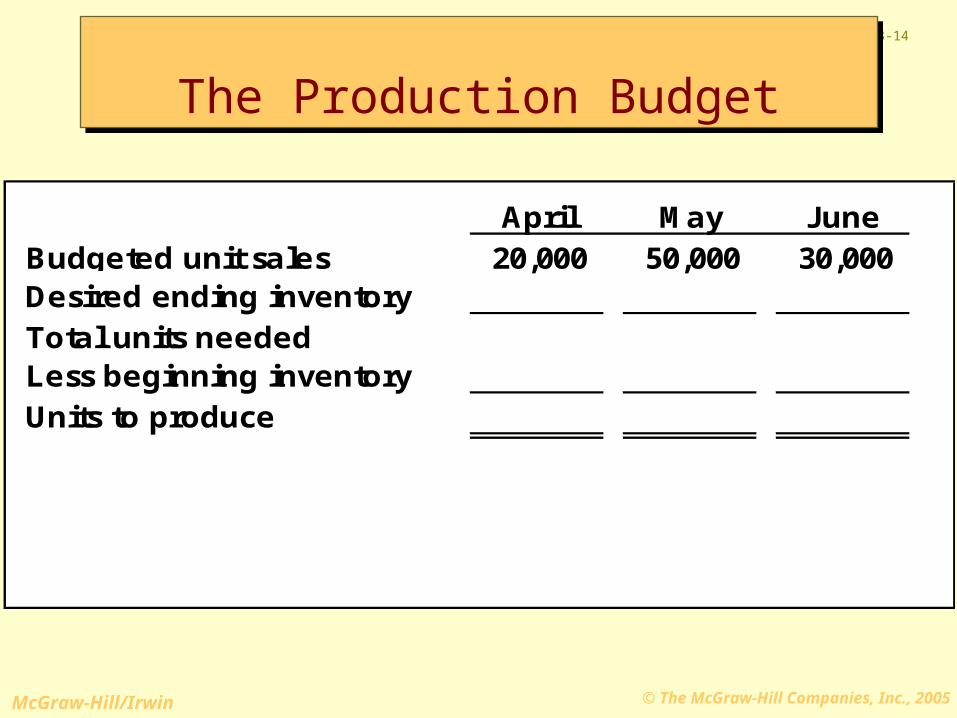

Production must be adequate to meet budgeted sales and to provide sufficient ending inventory.

Production must be adequate to meet budgeted sales and to provide sufficient ending inventory.

Budgeted product sales in units

+ Desired product units in ending inventory

= Total product units needed

– Product units in beginning inventory

= Product units to produce

The Production BudgetThe Production Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-14

April May JuneBudgeted unit sales 20,000 50,000 30,000Desired ending inventoryTotal units neededLess beginning inventoryUnits to produce

The Production BudgetThe Production Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-15

April May JuneBudgeted unit sales 20,000 50,000 30,000 Desired ending inventory 10,000 6,000 5,000 Total units needed 30,000 56,000 35,000 Less beginning inventoryUnits to produce

Ending inventory = 20% of next month's sales needs.June ending inventory = .20 × 25,000 July units = 5,000 units.

The Production BudgetThe Production Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-16

April May JuneBudgeted unit sales 20,000 50,000 30,000 Desired ending inventory 10,000 6,000 5,000 Total units needed 30,000 56,000 35,000 Less beginning inventory 4,000 10,000 6,000 Units to produce 26,000 46,000 29,000

Ending inventory = 20% of next month's sales needs.June ending inventory = .20 × 25,000 July units = 5,000 units.Beginning inventory is last month's ending inventory.

The Production BudgetThe Production Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-17

ProductionBudgetsMaterial

Purchases

Production BudgetUnits

Complete

d

The Production BudgetThe Production Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-18

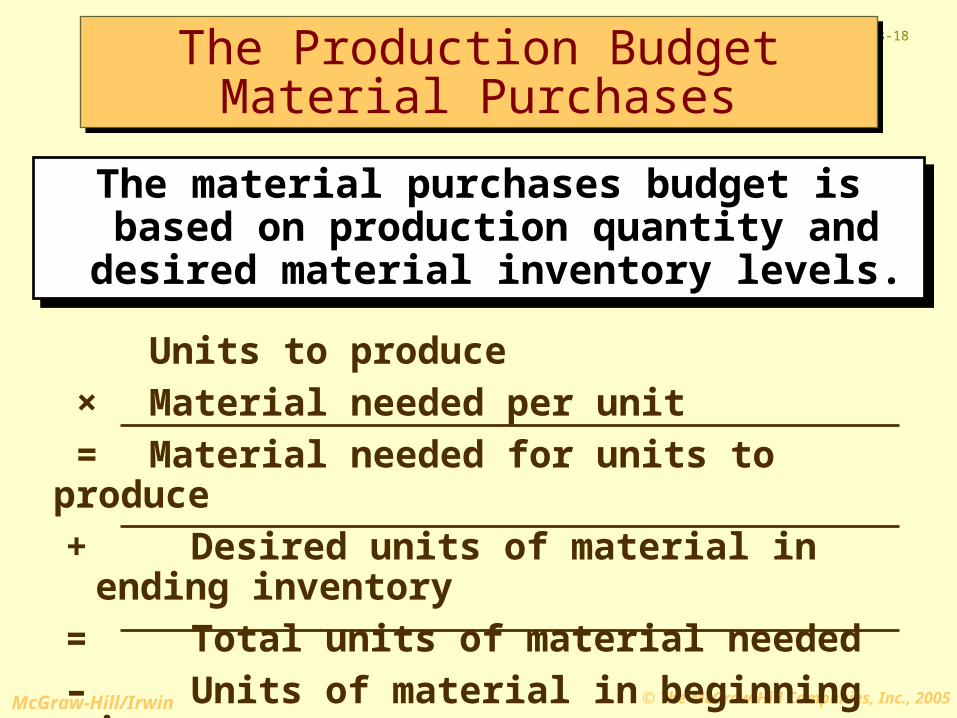

The material purchases budget is based on production quantity and desired material

inventory levels.

The material purchases budget is based on production quantity and desired material

inventory levels.

Units to produce × Material needed per unit = Material needed for units to produce+ Desired units of material in ending

inventory= Total units of material needed– Units of material in beginning inventory= Units of material to purchase

The Production BudgetMaterial Purchases

The Production BudgetMaterial Purchases

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-19

Five pounds of material are needed for each unit produced.

The management at Basket wants to have materials on hand at the end of each month equal to 10 percent of the following month’s

production needs.

The materials inventory on March 31 is 13,000 pounds. July production is budgeted for

23,000 units.

Five pounds of material are needed for each unit produced.

The management at Basket wants to have materials on hand at the end of each month equal to 10 percent of the following month’s

production needs.

The materials inventory on March 31 is 13,000 pounds. July production is budgeted for

23,000 units.

The Production BudgetMaterial Purchases

The Production BudgetMaterial Purchases

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-20

The Production BudgetMaterial Purchases

The Production BudgetMaterial Purchases

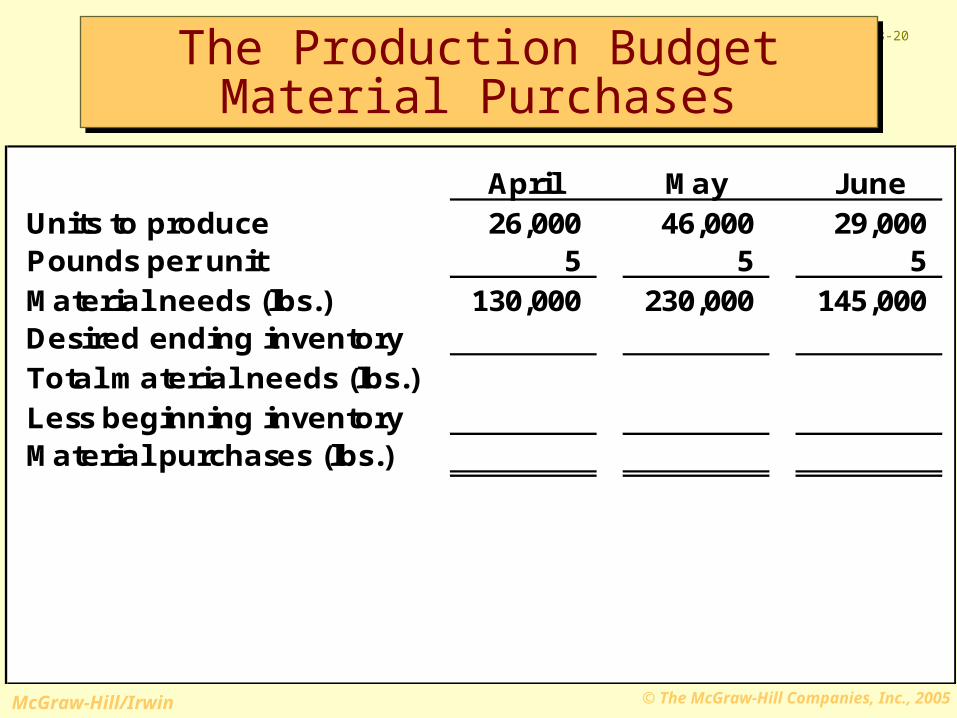

April May JuneUnits to produce 26,000 46,000 29,000 Pounds per unit 5 5 5 Material needs (lbs.) 130,000 230,000 145,000Desired ending inventoryTotal material needs (lbs.)Less beginning inventoryMaterial purchases (lbs.)

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-21

The Production BudgetMaterial Purchases

The Production BudgetMaterial Purchases

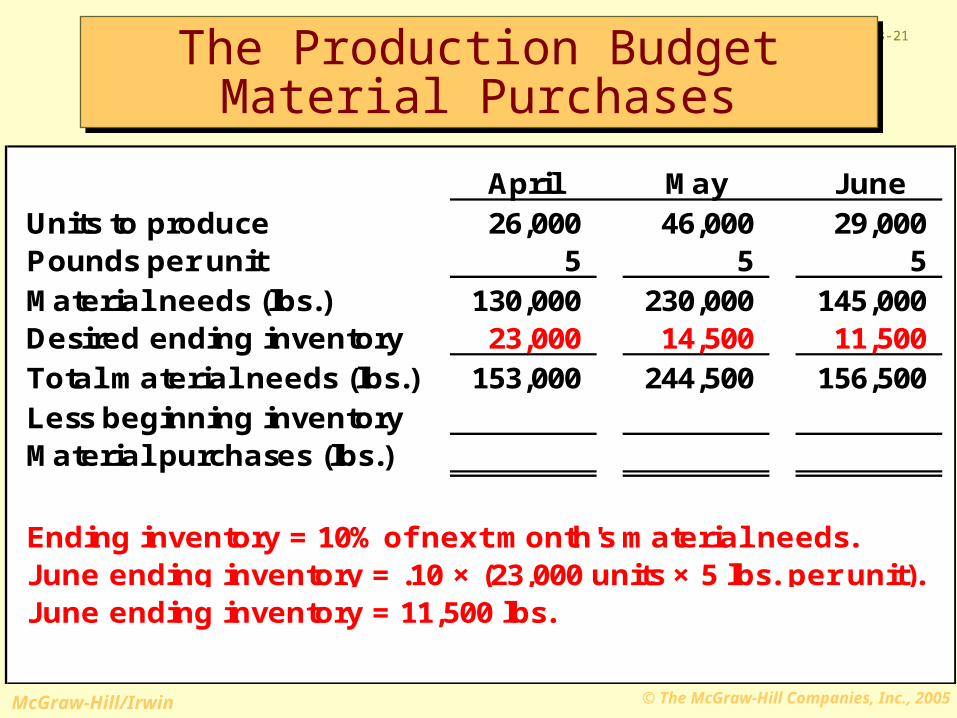

April May JuneUnits to produce 26,000 46,000 29,000 Pounds per unit 5 5 5 Material needs (lbs.) 130,000 230,000 145,000Desired ending inventory 23,000 14,500 11,500 Total material needs (lbs.) 153,000 244,500 156,500Less beginning inventoryMaterial purchases (lbs.)

Ending inventory = 10% of next month's material needs.June ending inventory = .10 × (23,000 units × 5 lbs. per unit).June ending inventory = 11,500 lbs.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-22

The Production BudgetMaterial Purchases

The Production BudgetMaterial Purchases

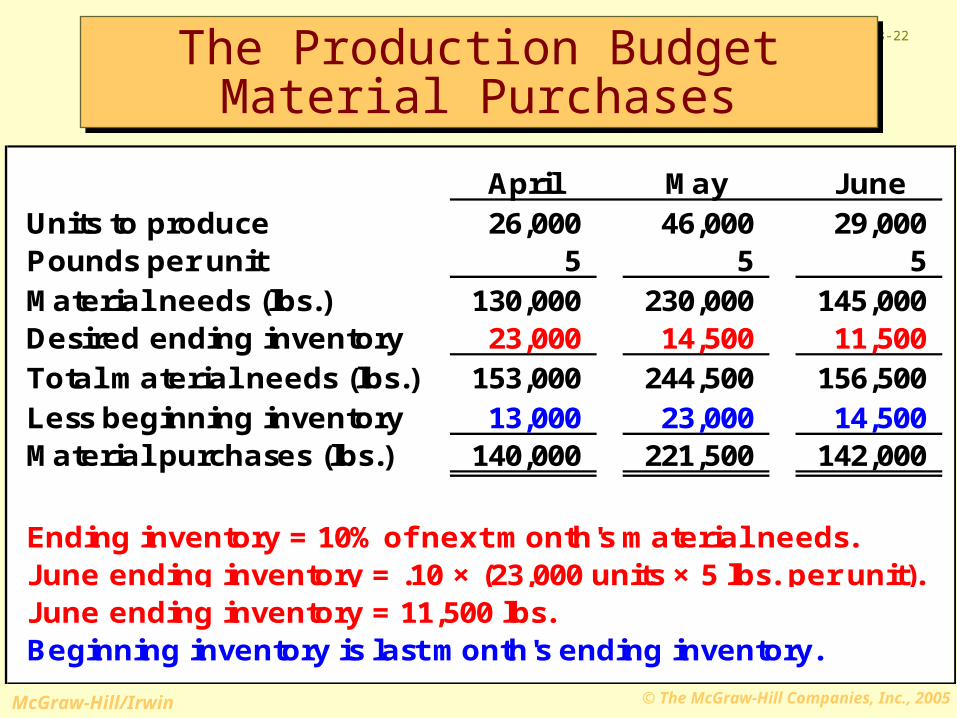

April May JuneUnits to produce 26,000 46,000 29,000 Pounds per unit 5 5 5 Material needs (lbs.) 130,000 230,000 145,000Desired ending inventory 23,000 14,500 11,500 Total material needs (lbs.) 153,000 244,500 156,500Less beginning inventory 13,000 23,000 14,500 Material purchases (lbs.) 140,000 221,500 142,000

Ending inventory = 10% of next month's material needs.June ending inventory = .10 × (23,000 units × 5 lbs. per unit).June ending inventory = 11,500 lbs.Beginning inventory is last month's ending inventory.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

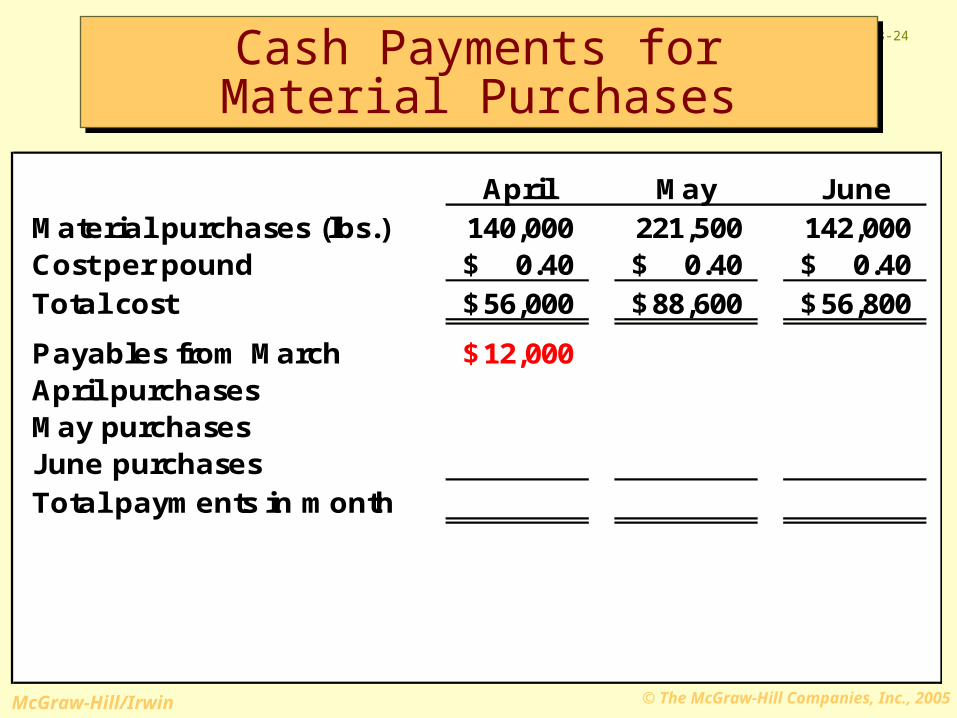

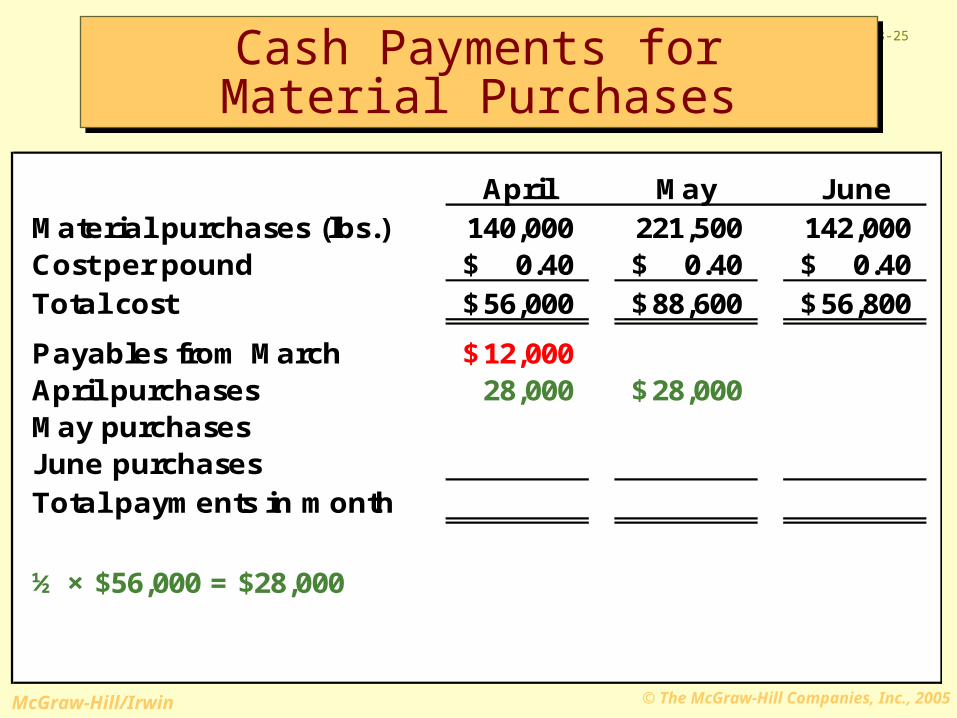

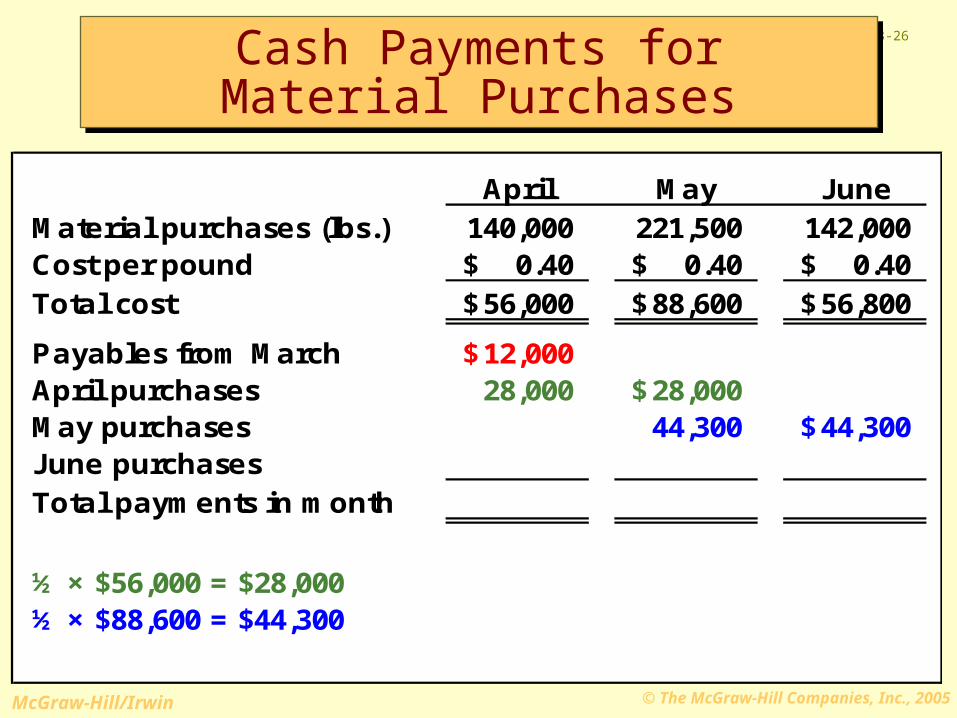

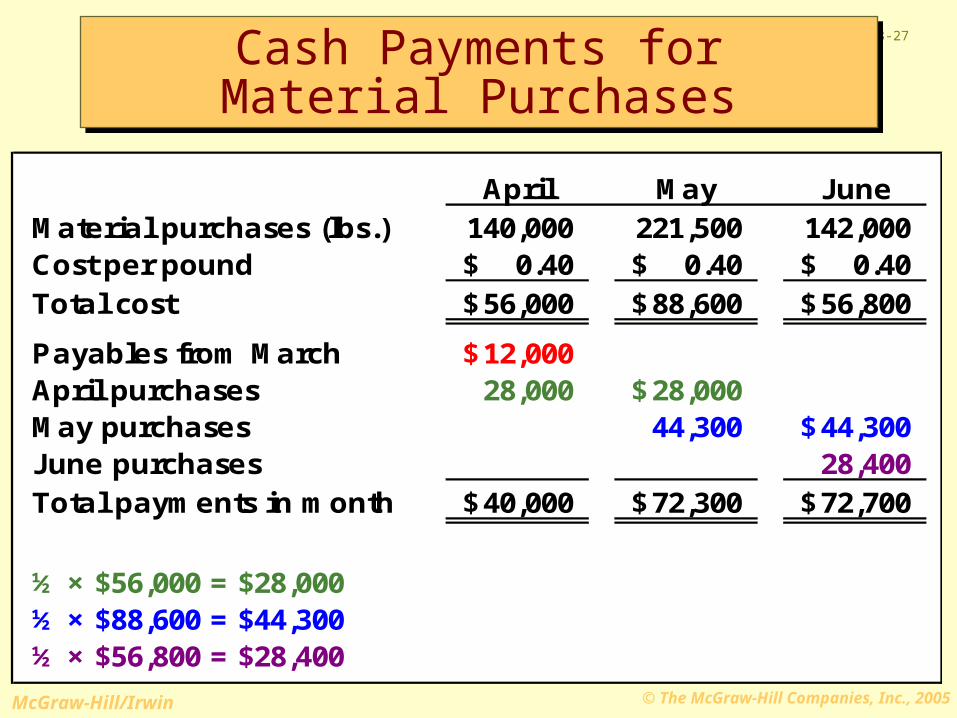

23-23

Cash Payments forMaterial PurchasesCash Payments forMaterial Purchases

Materials used in production cost $0.40per pound. One-half of a month’s

purchases are paid for in the month of purchase; the other half is paid for in the

following month.

No discount terms are available.

The accounts payable balance onMarch 31 is $12,000.

Materials used in production cost $0.40per pound. One-half of a month’s

purchases are paid for in the month of purchase; the other half is paid for in the

following month.

No discount terms are available.

The accounts payable balance onMarch 31 is $12,000.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-24

April May JuneMaterial purchases (lbs.) 140,000 221,500 142,000Cost per pound 0.40$ 0.40$ 0.40$ Total cost 56,000$ 88,600$ 56,800$

Payables from March 12,000$April purchasesMay purchasesJune purchasesTotal payments in month

Cash Payments forMaterial PurchasesCash Payments forMaterial Purchases

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-25

April May JuneMaterial purchases (lbs.) 140,000 221,500 142,000Cost per pound 0.40$ 0.40$ 0.40$ Total cost 56,000$ 88,600$ 56,800$

Payables from March 12,000$April purchases 28,000 28,000$May purchasesJune purchasesTotal payments in month

½ × $56,000 = $28,000

Cash Payments forMaterial PurchasesCash Payments forMaterial Purchases

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-26

April May JuneMaterial purchases (lbs.) 140,000 221,500 142,000Cost per pound 0.40$ 0.40$ 0.40$ Total cost 56,000$ 88,600$ 56,800$

Payables from March 12,000$April purchases 28,000 28,000$May purchases 44,300 44,300$June purchasesTotal payments in month

½ × $56,000 = $28,000½ × $88,600 = $44,300

Cash Payments forMaterial PurchasesCash Payments forMaterial Purchases

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-27

April May JuneMaterial purchases (lbs.) 140,000 221,500 142,000Cost per pound 0.40$ 0.40$ 0.40$ Total cost 56,000$ 88,600$ 56,800$

Payables from March 12,000$April purchases 28,000 28,000$May purchases 44,300 44,300$June purchases 28,400 Total payments in month 40,000$ 72,300$ 72,700$

½ × $56,000 = $28,000½ × $88,600 = $44,300½ × $56,800 = $28,400

Cash Payments forMaterial PurchasesCash Payments forMaterial Purchases

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-28

ProductionBudgetLabor

Production BudgetUnits

Material

Complete

d

The Production BudgetThe Production Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-29

Each unit produced requires 3 minutes (.05 hours) of direct labor. Basket employs 30

persons for 40 hours each week at a rate of $10 per hour. Any extra hours needed are

obtained by hiring temporary workers also at $10 per hour.

Each unit produced requires 3 minutes (.05 hours) of direct labor. Basket employs 30

persons for 40 hours each week at a rate of $10 per hour. Any extra hours needed are

obtained by hiring temporary workers also at $10 per hour.

The Production BudgetDirect Labor

The Production BudgetDirect Labor

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-30

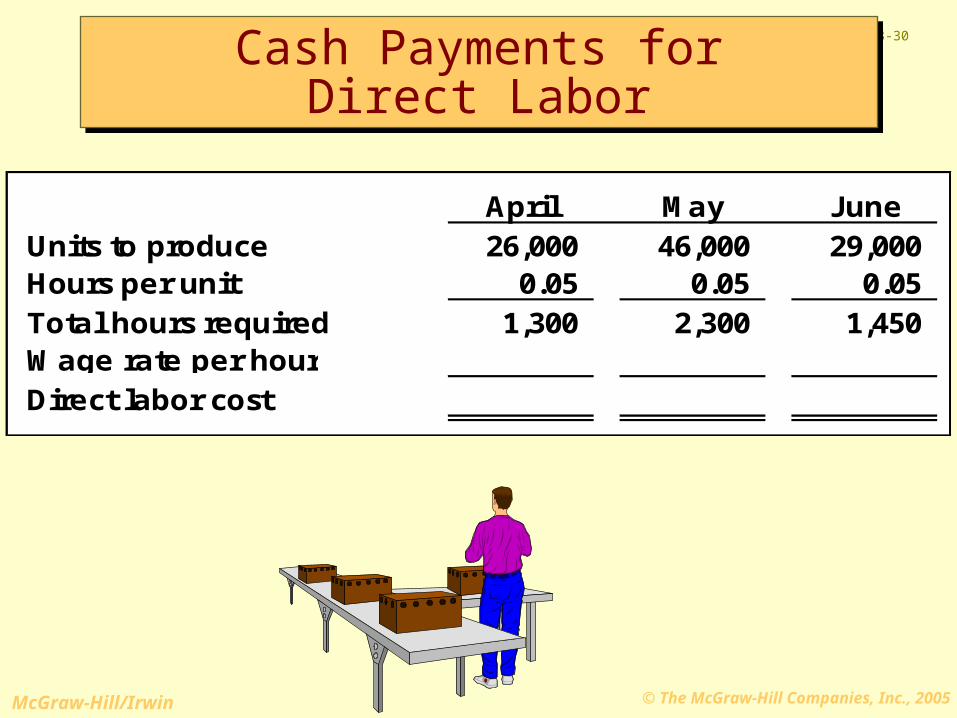

April May JuneUnits to produce 26,000 46,000 29,000 Hours per unit 0.05 0.05 0.05 Total hours required 1,300 2,300 1,450 Wage rate per hourDirect labor cost

Cash Payments forDirect Labor

Cash Payments forDirect Labor

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-31

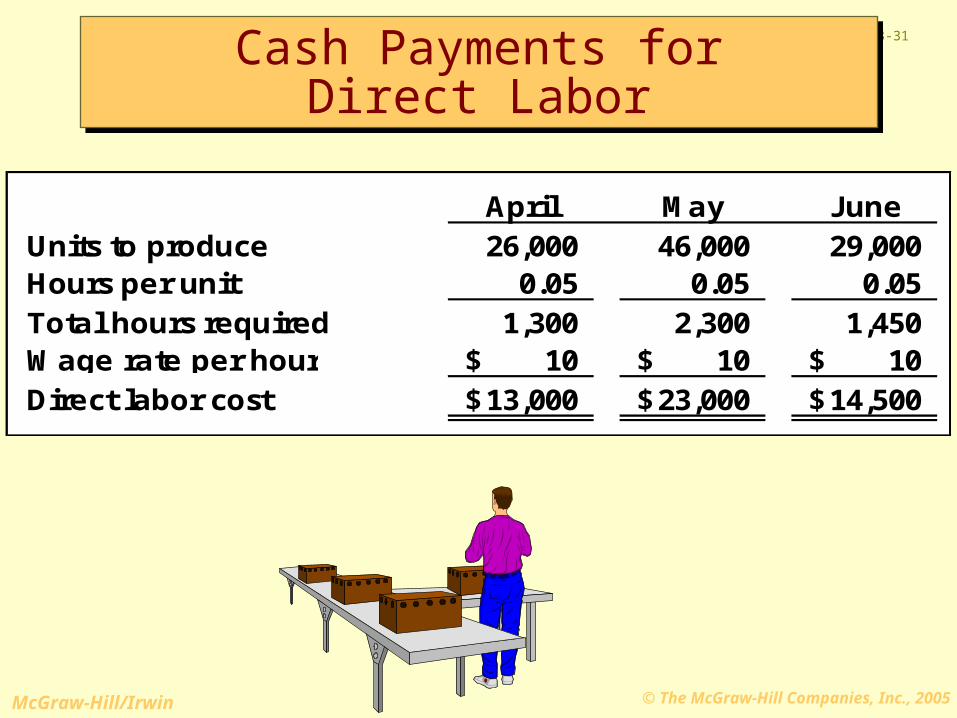

April May JuneUnits to produce 26,000 46,000 29,000 Hours per unit 0.05 0.05 0.05 Total hours required 1,300 2,300 1,450 Wage rate per hour 10$ 10$ 10$ Direct labor cost 13,000$ 23,000$ 14,500$

Cash Payments forDirect Labor

Cash Payments forDirect Labor

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-32

Production Budget

UnitsMaterialLabor

Complete

d

ProductionBudget

ManufacturingOverhead

The Production BudgetThe Production Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-33

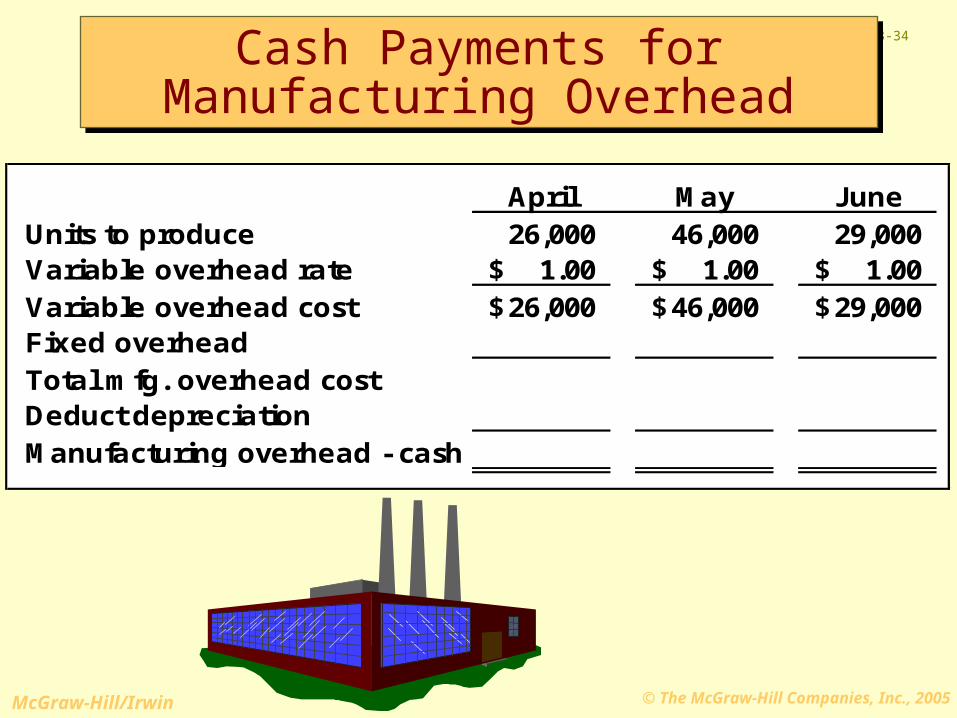

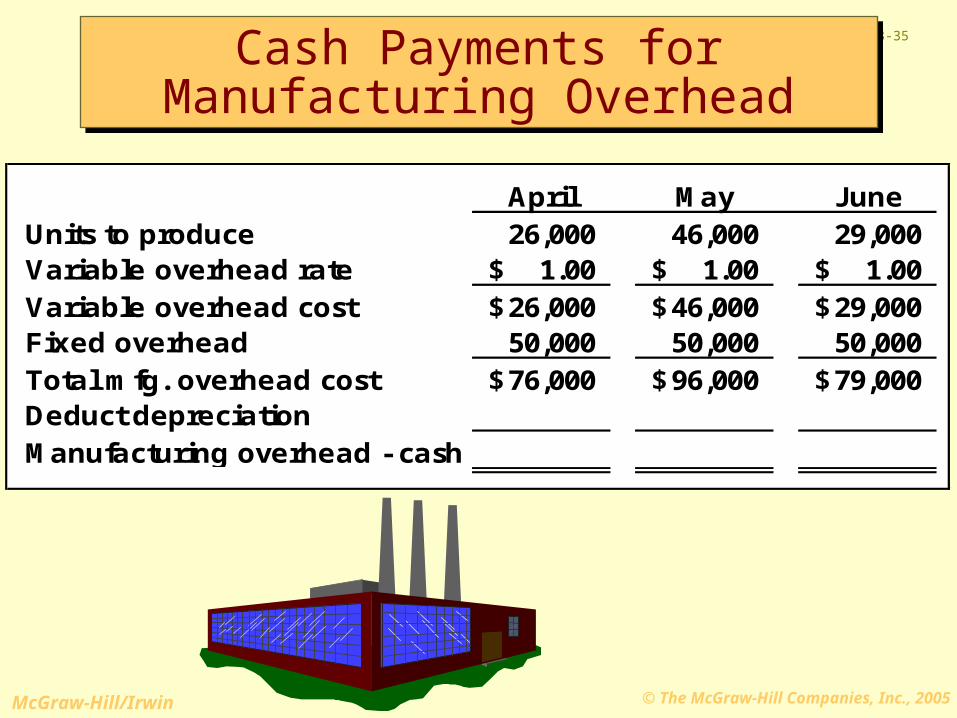

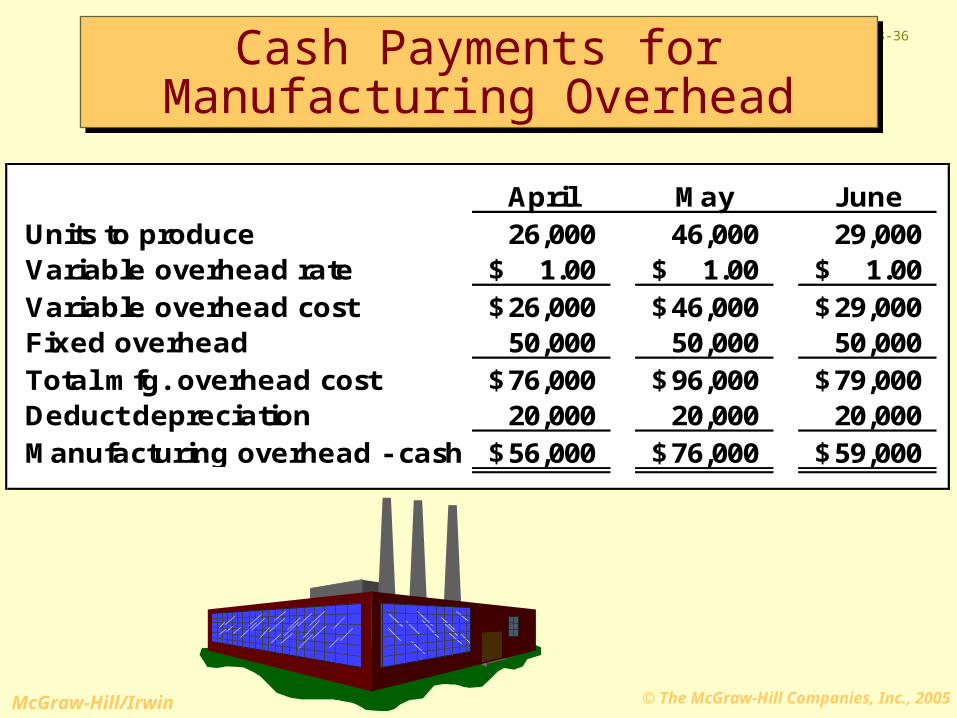

Variable manufacturing overhead is $1 per unit produced and fixed manufacturing overhead is

$50,000 per month.

Fixed manufacturing overhead includes $20,000 in depreciation which does not require

a cash outflow.

Variable manufacturing overhead is $1 per unit produced and fixed manufacturing overhead is

$50,000 per month.

Fixed manufacturing overhead includes $20,000 in depreciation which does not require

a cash outflow.

The Production BudgetManufacturing OverheadThe Production Budget

Manufacturing Overhead

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-34

April May JuneUnits to produce 26,000 46,000 29,000 Variable overhead rate 1.00$ 1.00$ 1.00$ Variable overhead cost 26,000$ 46,000$ 29,000$Fixed overheadTotal mfg. overhead costDeduct depreciationManufacturing overhead - cash

Cash Payments forManufacturing Overhead

Cash Payments forManufacturing Overhead

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-35

April May JuneUnits to produce 26,000 46,000 29,000 Variable overhead rate 1.00$ 1.00$ 1.00$ Variable overhead cost 26,000$ 46,000$ 29,000$Fixed overhead 50,000 50,000 50,000 Total mfg. overhead cost 76,000$ 96,000$ 79,000$Deduct depreciationManufacturing overhead - cash

Cash Payments forManufacturing Overhead

Cash Payments forManufacturing Overhead

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-36

April May JuneUnits to produce 26,000 46,000 29,000 Variable overhead rate 1.00$ 1.00$ 1.00$ Variable overhead cost 26,000$ 46,000$ 29,000$Fixed overhead 50,000 50,000 50,000 Total mfg. overhead cost 76,000$ 96,000$ 79,000$Deduct depreciation 20,000 20,000 20,000 Manufacturing overhead - cash 56,000$ 76,000$ 59,000$

Cash Payments forManufacturing Overhead

Cash Payments forManufacturing Overhead

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-37

Production Budget

Complete

d

Sellingand

AdministrativeExpenseBudget

Selling and Administrative(S&A) Expense Budget

Selling and Administrative(S&A) Expense Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-38

Selling expense budgets contain both variable and fixed items.

Variable items: shipping costs and sales commissions.

Fixed items: advertising and sales salaries.

Administrative expense budgets contain mostly fixed items.Executive salaries and depreciation on company

offices.

Selling expense budgets contain both variable and fixed items.

Variable items: shipping costs and sales commissions.

Fixed items: advertising and sales salaries.

Administrative expense budgets contain mostly fixed items.Executive salaries and depreciation on company

offices.

Selling and Administrative(S&A) Expense Budget

Selling and Administrative(S&A) Expense Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-39

Variable selling and administrative expenses are $0.50 per unit sold and fixed

selling and administrative expenses are $70,000 per month.

Fixed selling and administrative expenses include $10,000 in depreciation which does

not require a cash outflow.

Variable selling and administrative expenses are $0.50 per unit sold and fixed

selling and administrative expenses are $70,000 per month.

Fixed selling and administrative expenses include $10,000 in depreciation which does

not require a cash outflow.

Cash Payments for(S&A) Expenses

Cash Payments for(S&A) Expenses

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-40

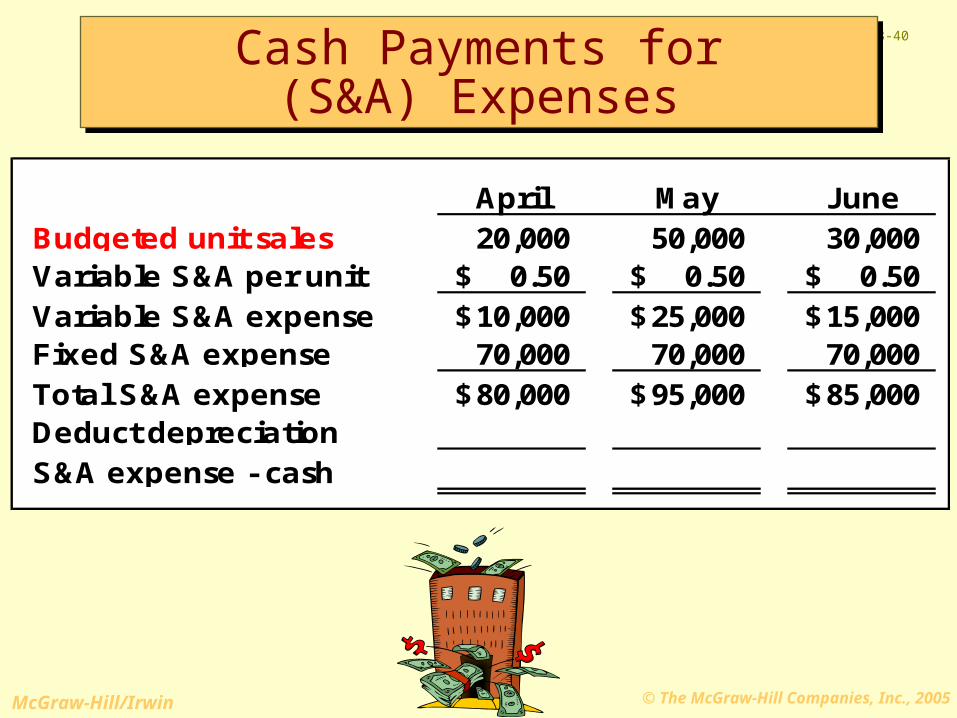

April May JuneBudgeted unit sales 20,000 50,000 30,000 Variable S&A per unit 0.50$ 0.50$ 0.50$ Variable S&A expense 10,000$ 25,000$ 15,000$Fixed S&A expense 70,000 70,000 70,000 Total S&A expense 80,000$ 95,000$ 85,000$Deduct depreciationS&A expense - cash

Cash Payments for(S&A) Expenses

Cash Payments for(S&A) Expenses

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-41

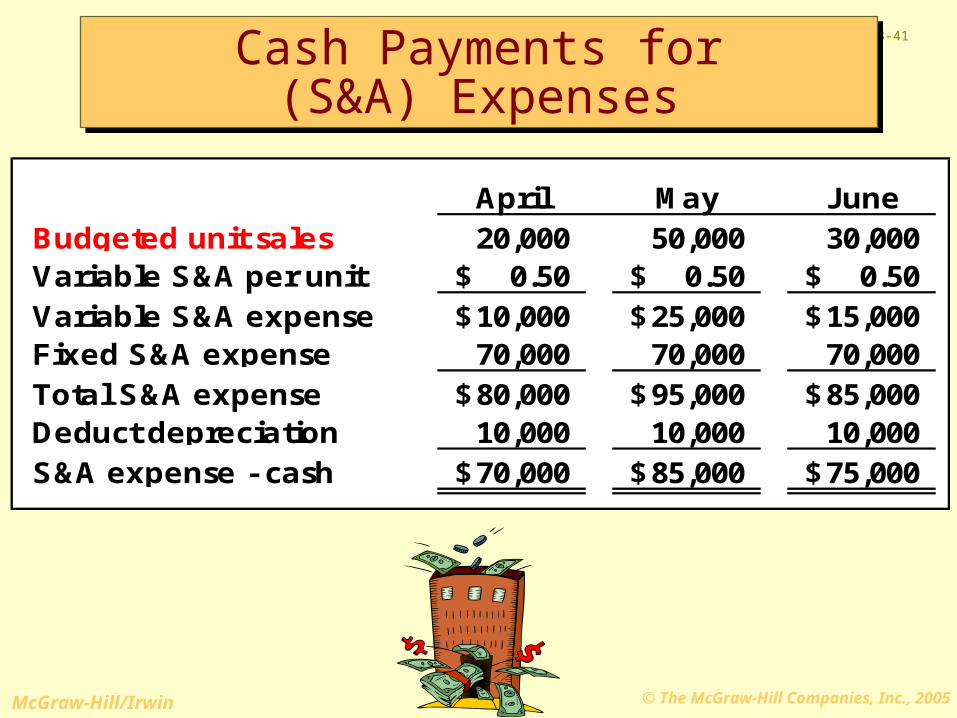

April May JuneBudgeted unit sales 20,000 50,000 30,000 Variable S&A per unit 0.50$ 0.50$ 0.50$ Variable S&A expense 10,000$ 25,000$ 15,000$Fixed S&A expense 70,000 70,000 70,000 Total S&A expense 80,000$ 95,000$ 85,000$Deduct depreciation 10,000 10,000 10,000 S&A expense - cash 70,000$ 85,000$ 75,000$

Cash Payments for(S&A) Expenses

Cash Payments for(S&A) Expenses

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-42

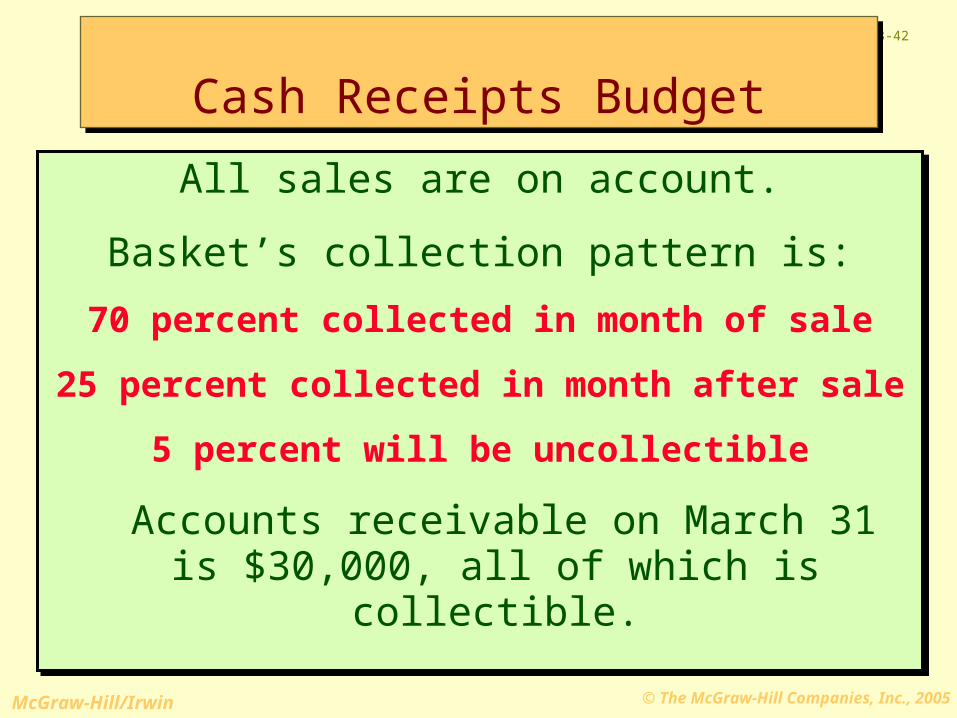

All sales are on account.

Basket’s collection pattern is:

70 percent collected in month of sale

25 percent collected in month after sale

5 percent will be uncollectible

Accounts receivable on March 31 is $30,000, all of which is collectible.

All sales are on account.

Basket’s collection pattern is:

70 percent collected in month of sale

25 percent collected in month after sale

5 percent will be uncollectible

Accounts receivable on March 31 is $30,000, all of which is collectible.

Cash Receipts BudgetCash Receipts Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-43

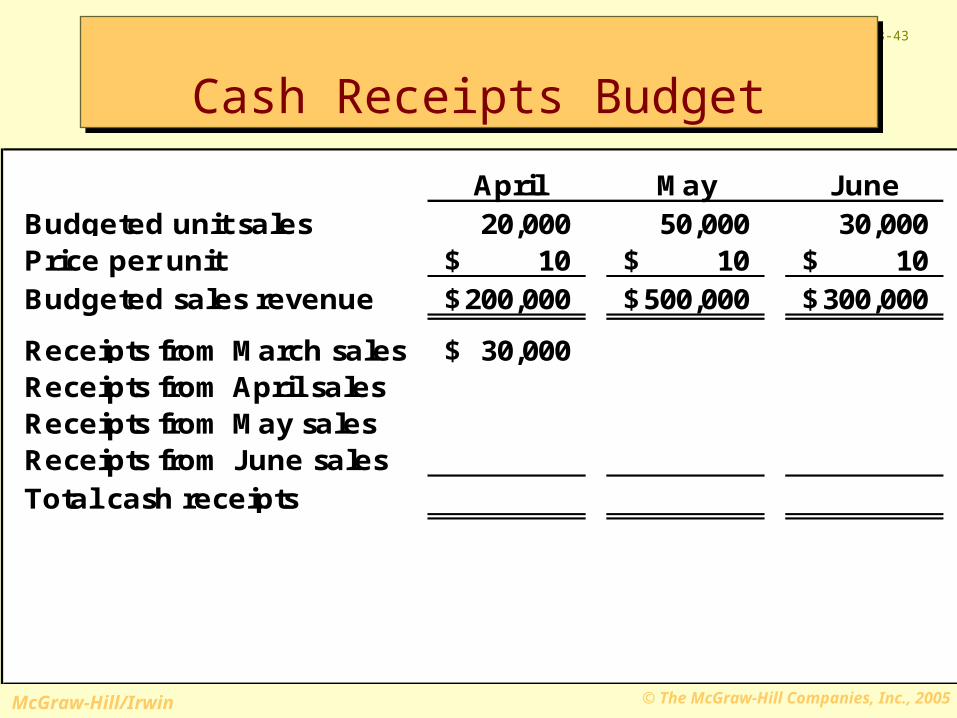

April May JuneBudgeted unit sales 20,000 50,000 30,000 Price per unit 10$ 10$ 10$ Budgeted sales revenue 200,000$ 500,000$ 300,000$

Receipts from March sales 30,000$ Receipts from April salesReceipts from May salesReceipts from June salesTotal cash receipts

Cash Receipts BudgetCash Receipts Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-44

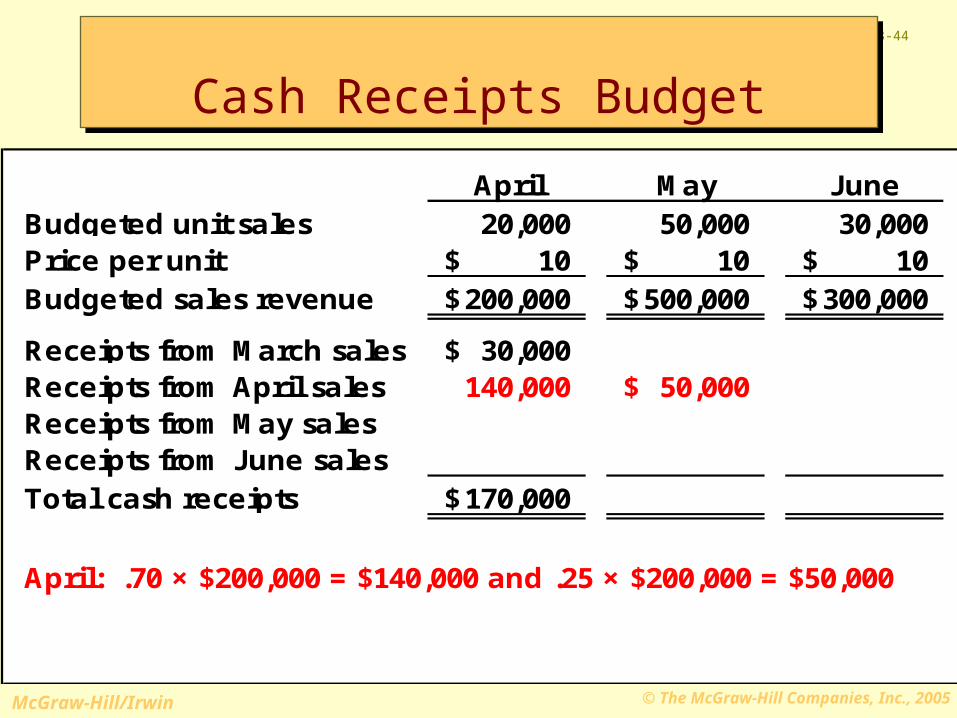

April May JuneBudgeted unit sales 20,000 50,000 30,000 Price per unit 10$ 10$ 10$ Budgeted sales revenue 200,000$ 500,000$ 300,000$

Receipts from March sales 30,000$ Receipts from April sales 140,000 50,000$ Receipts from May salesReceipts from June salesTotal cash receipts 170,000$

April: .70 × $200,000 = $140,000 and .25 × $200,000 = $50,000

Cash Receipts BudgetCash Receipts Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-45

April May JuneBudgeted unit sales 20,000 50,000 30,000 Price per unit 10$ 10$ 10$ Budgeted sales revenue 200,000$ 500,000$ 300,000$

Receipts from March sales 30,000$ Receipts from April sales 140,000 50,000$ Receipts from May sales 350,000 125,000$Receipts from June salesTotal cash receipts 170,000$ 400,000$

April: .70 × $200,000 = $140,000 and .25 × $200,000 = $50,000 May: .70 × $500,000 = $350,000 and .25 × $500,000 = $125,000

Cash Receipts BudgetCash Receipts Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-46

April May JuneBudgeted unit sales 20,000 50,000 30,000 Price per unit 10$ 10$ 10$ Budgeted sales revenue 200,000$ 500,000$ 300,000$

Receipts from March sales 30,000$ Receipts from April sales 140,000 50,000$ Receipts from May sales 350,000 125,000$Receipts from June sales 210,000 Total cash receipts 170,000$ 400,000$ 335,000$

April: .70 × $200,000 = $140,000 and .25 × $200,000 = $50,000 May: .70 × $500,000 = $350,000 and .25 × $500,000 = $125,000 June: .70 × $300,000 = $210,000

Cash Receipts BudgetCash Receipts Budget

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-47

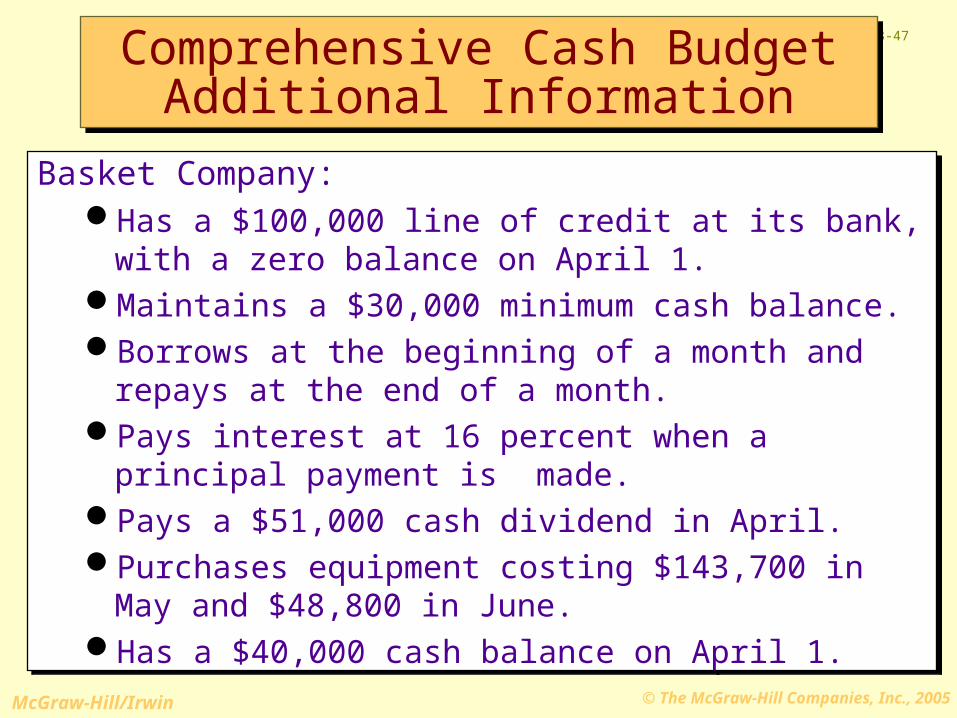

Basket Company:Has a $100,000 line of credit at its bank, with a zero

balance on April 1.Maintains a $30,000 minimum cash balance.Borrows at the beginning of a month and repays at the

end of a month.Pays interest at 16 percent when a principal payment is

made.Pays a $51,000 cash dividend in April.Purchases equipment costing $143,700 in May and

$48,800 in June.Has a $40,000 cash balance on April 1.

Basket Company:Has a $100,000 line of credit at its bank, with a zero

balance on April 1.Maintains a $30,000 minimum cash balance.Borrows at the beginning of a month and repays at the

end of a month.Pays interest at 16 percent when a principal payment is

made.Pays a $51,000 cash dividend in April.Purchases equipment costing $143,700 in May and

$48,800 in June.Has a $40,000 cash balance on April 1.

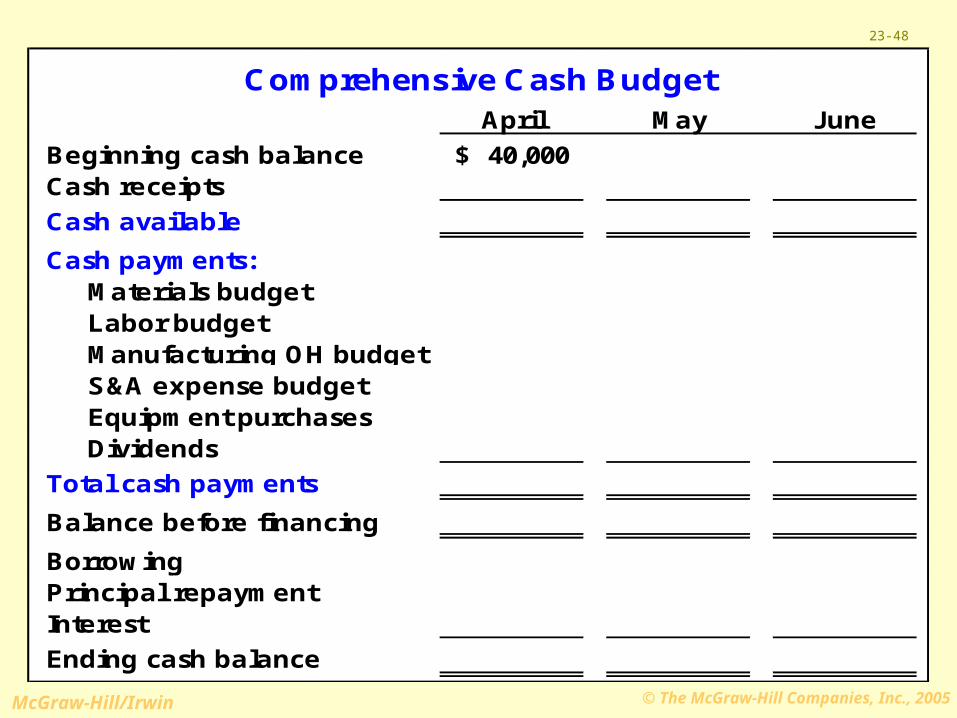

Comprehensive Cash BudgetAdditional Information

Comprehensive Cash BudgetAdditional Information

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-48

Comprehensive Cash BudgetApril May June

Beginning cash balance 40,000$ Cash receipts

Cash available

Cash payments: Materials budget Labor budget Manufacturing OH budget S&A expense budget Equipment purchases Dividends

Total cash payments

Balance before financing

BorrowingPrincipal repaymentInterest

Ending cash balance

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-49

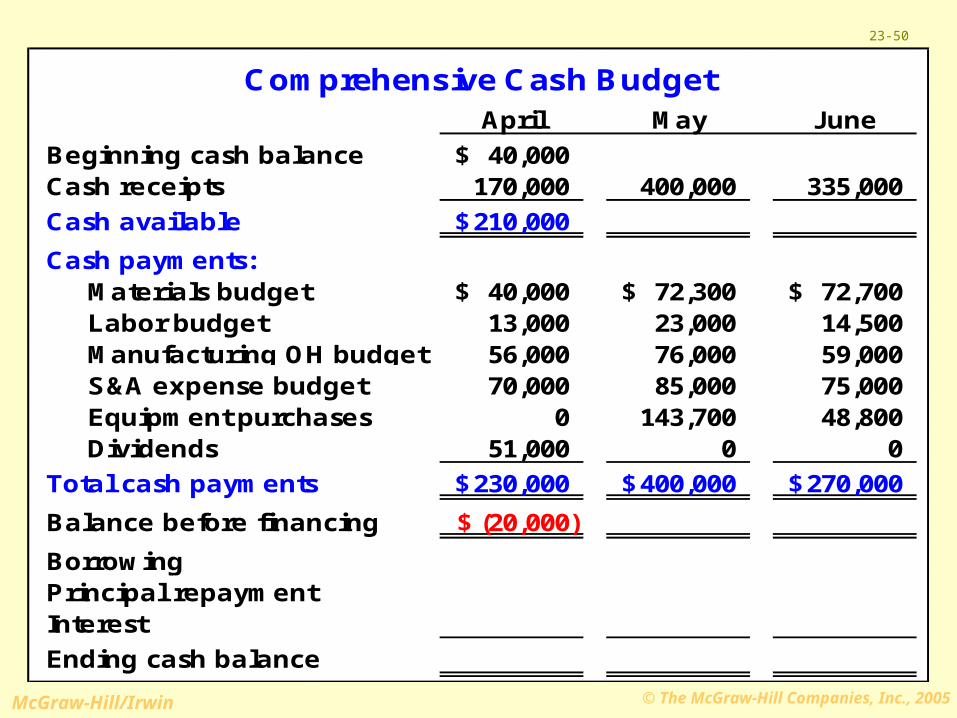

Comprehensive Cash BudgetApril May June

Beginning cash balance 40,000$ Cash receipts 170,000 400,000 335,000

Cash available 210,000$

Cash payments: Materials budget Labor budget Manufacturing OH budget S&A expense budget Equipment purchases Dividends

Total cash payments

Balance before financing

BorrowingPrincipal repaymentInterest

Ending cash balance

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-50

Comprehensive Cash BudgetApril May June

Beginning cash balance 40,000$ Cash receipts 170,000 400,000 335,000

Cash available 210,000$

Cash payments: Materials budget 40,000$ 72,300$ 72,700$ Labor budget 13,000 23,000 14,500 Manufacturing OH budget 56,000 76,000 59,000 S&A expense budget 70,000 85,000 75,000 Equipment purchases 0 143,700 48,800 Dividends 51,000 0 0

Total cash payments 230,000$ 400,000$ 270,000$

Balance before financing (20,000)$

BorrowingPrincipal repaymentInterest

Ending cash balance

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-51

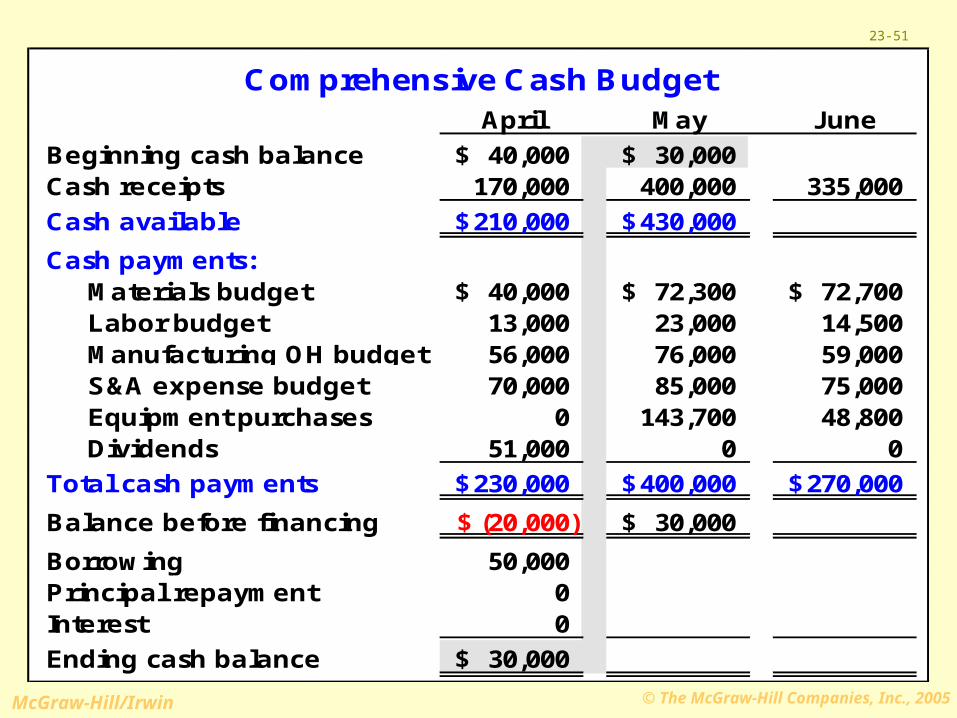

Comprehensive Cash BudgetApril May June

Beginning cash balance 40,000$ 30,000$ Cash receipts 170,000 400,000 335,000

Cash available 210,000$ 430,000$

Cash payments: Materials budget 40,000$ 72,300$ 72,700$ Labor budget 13,000 23,000 14,500 Manufacturing OH budget 56,000 76,000 59,000 S&A expense budget 70,000 85,000 75,000 Equipment purchases 0 143,700 48,800 Dividends 51,000 0 0

Total cash payments 230,000$ 400,000$ 270,000$

Balance before financing (20,000)$ 30,000$

Borrowing 50,000 Principal repayment 0Interest 0

Ending cash balance 30,000$

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-52

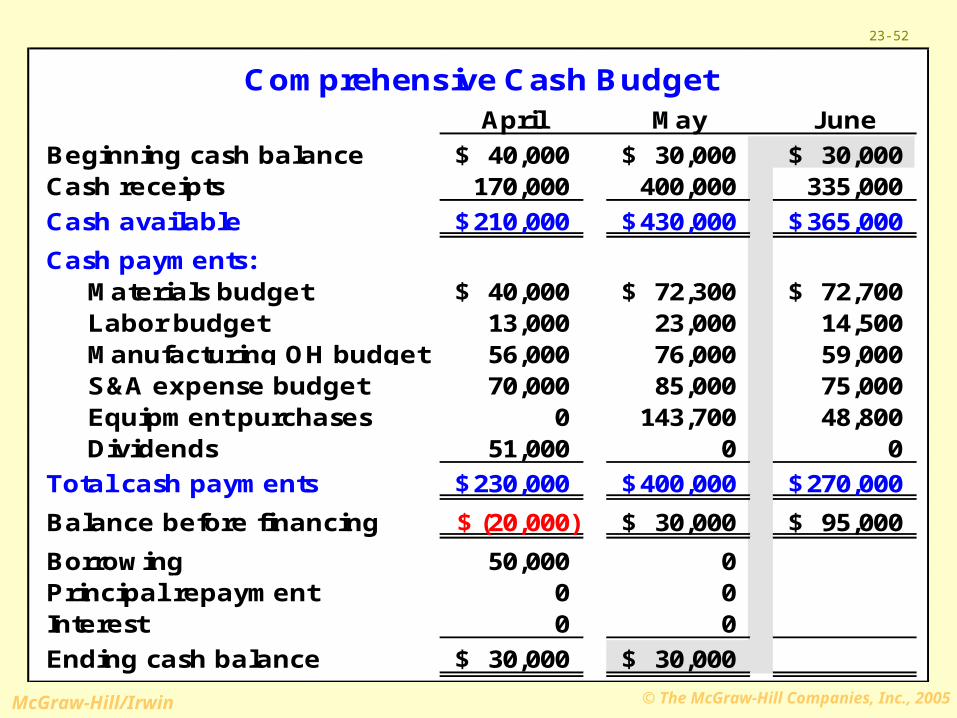

Comprehensive Cash BudgetApril May June

Beginning cash balance 40,000$ 30,000$ 30,000$ Cash receipts 170,000 400,000 335,000

Cash available 210,000$ 430,000$ 365,000$

Cash payments: Materials budget 40,000$ 72,300$ 72,700$ Labor budget 13,000 23,000 14,500 Manufacturing OH budget 56,000 76,000 59,000 S&A expense budget 70,000 85,000 75,000 Equipment purchases 0 143,700 48,800 Dividends 51,000 0 0

Total cash payments 230,000$ 400,000$ 270,000$

Balance before financing (20,000)$ 30,000$ 95,000$

Borrowing 50,000 0Principal repayment 0 0Interest 0 0

Ending cash balance 30,000$ 30,000$

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

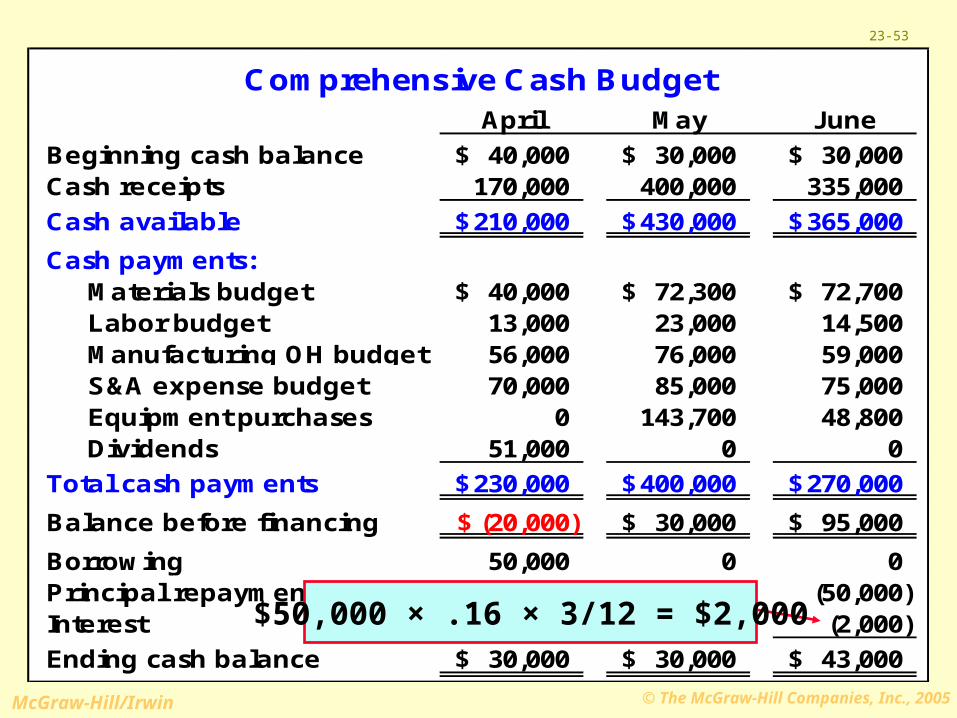

23-53

Comprehensive Cash BudgetApril May June

Beginning cash balance 40,000$ 30,000$ 30,000$ Cash receipts 170,000 400,000 335,000

Cash available 210,000$ 430,000$ 365,000$

Cash payments: Materials budget 40,000$ 72,300$ 72,700$ Labor budget 13,000 23,000 14,500 Manufacturing OH budget 56,000 76,000 59,000 S&A expense budget 70,000 85,000 75,000 Equipment purchases 0 143,700 48,800 Dividends 51,000 0 0

Total cash payments 230,000$ 400,000$ 270,000$

Balance before financing (20,000)$ 30,000$ 95,000$

Borrowing 50,000 0 0Principal repayment 0 0 (50,000) Interest 0 0 (2,000)

Ending cash balance 30,000$ 30,000$ 43,000$

$50,000 × .16 × 3/12 = $2,000

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-54

BudgetedIncome

Statement

Cash Budget

Complete

d

The BudgetedIncome Statement

The BudgetedIncome Statement

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

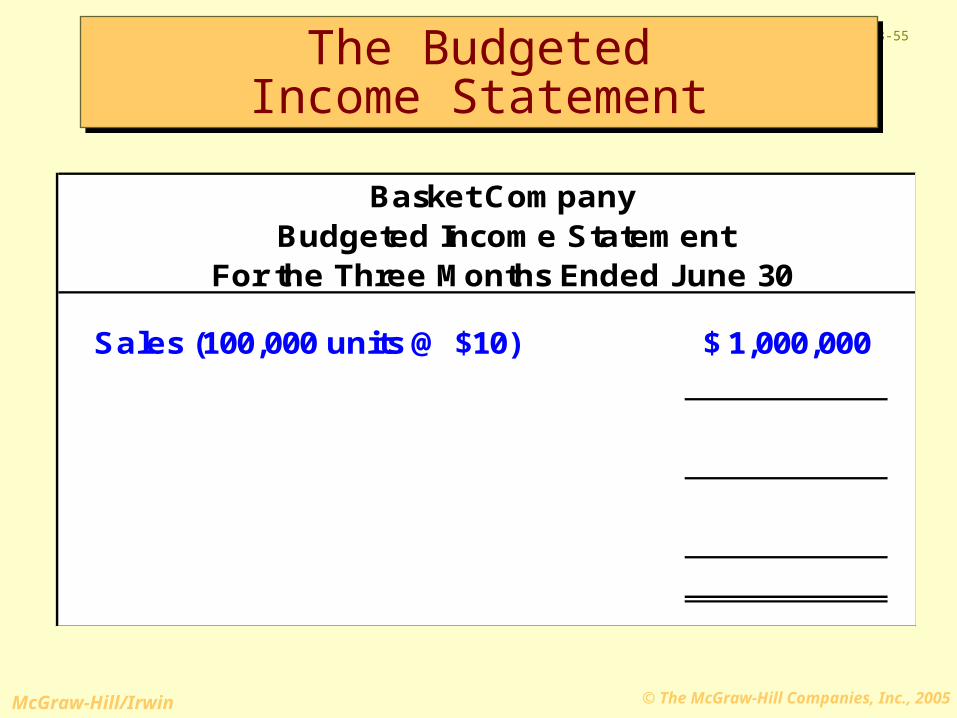

23-55

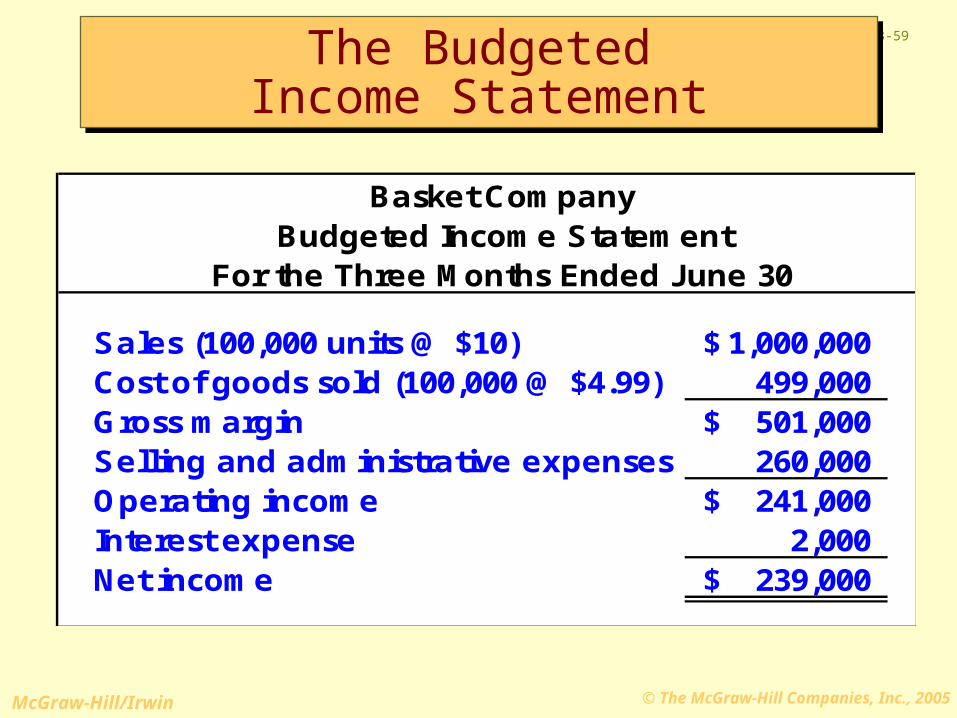

Basket CompanyBudgeted Income Statement

For the Three Months Ended June 30

Sales (100,000 units @ $10) 1,000,000$

The BudgetedIncome Statement

The BudgetedIncome Statement

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-56

Basket CompanyBudgeted Income Statement

For the Three Months Ended June 30

Sales (100,000 units @ $10) 1,000,000$ Cost of goods sold (100,000 @ $4.99) 499,000 Gross margin 501,000$

Computation of unit cost follows

The BudgetedIncome Statement

The BudgetedIncome Statement

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-57

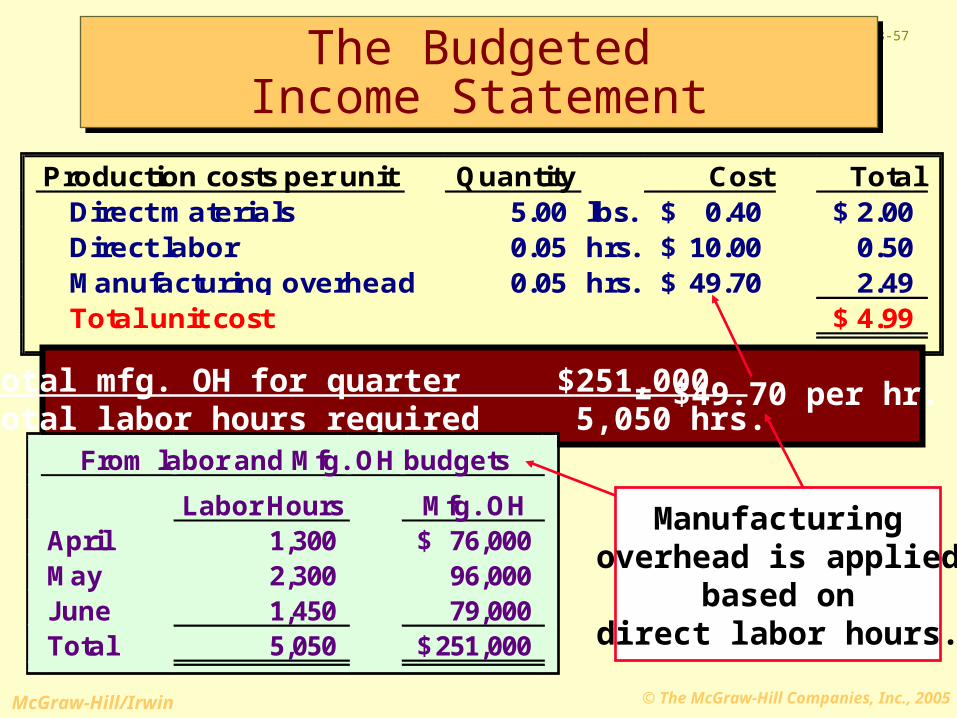

Production costs per unit Quantity Cost Total Direct materials 5.00 lbs. 0.40$ 2.00$ Direct labor 0.05 hrs. 10.00$ 0.50 Manufacturing overhead 0.05 hrs. 49.70$ 2.49 Total unit cost 4.99$

Total mfg. OH for quarter $251,000 Total labor hours required 5,050 hrs.

= $49.70 per hr.

From labor and Mfg. OH budgets

Labor Hours Mfg. OHApril 1,300 76,000$ May 2,300 96,000 June 1,450 79,000 Total 5,050 251,000$

Manufacturingoverhead is applied

based ondirect labor hours.

The BudgetedIncome Statement

The BudgetedIncome Statement

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-58

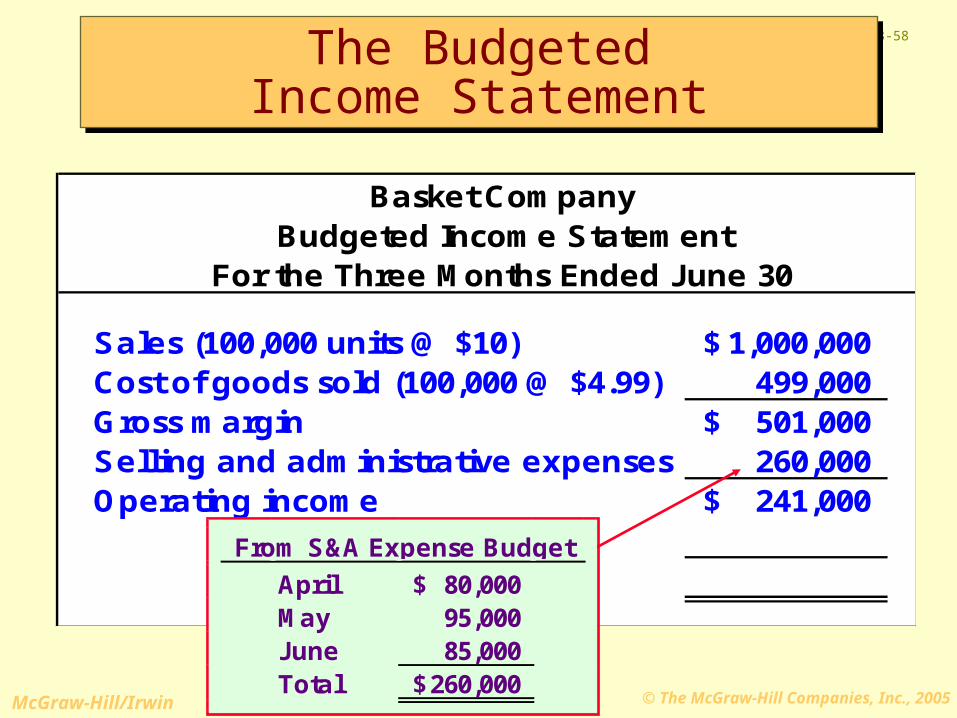

Basket CompanyBudgeted Income Statement

For the Three Months Ended June 30

Sales (100,000 units @ $10) 1,000,000$ Cost of goods sold (100,000 @ $4.99) 499,000 Gross margin 501,000$ Selling and administrative expenses 260,000 Operating income 241,000$

From S&A Expense Budget

April 80,000$ May 95,000 June 85,000 Total 260,000$

The BudgetedIncome Statement

The BudgetedIncome Statement

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-59

Basket CompanyBudgeted Income Statement

For the Three Months Ended June 30

Sales (100,000 units @ $10) 1,000,000$ Cost of goods sold (100,000 @ $4.99) 499,000 Gross margin 501,000$ Selling and administrative expenses 260,000 Operating income 241,000$ Interest expense 2,000 Net income 239,000$

The BudgetedIncome Statement

The BudgetedIncome Statement

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-60

BudgetedBalance

Sheet

Complete

d

BudgetedIncome

Statement

The BudgetedBalance SheetThe BudgetedBalance Sheet

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-61

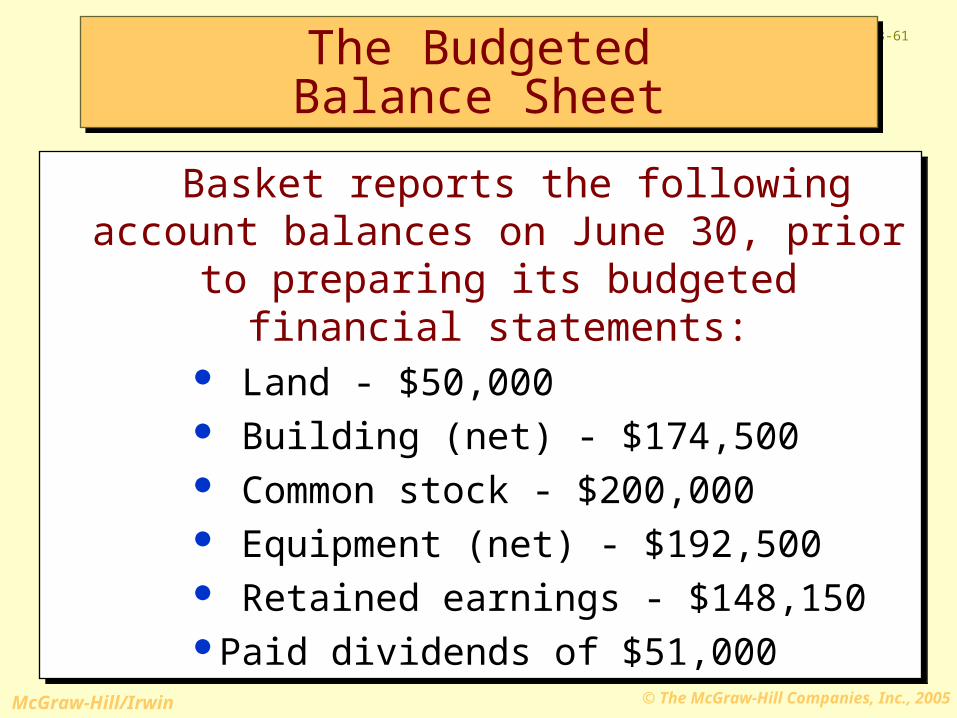

Basket reports the following account balances on June 30, prior to preparing its budgeted

financial statements: Land - $50,000 Building (net) - $174,500 Common stock - $200,000 Equipment (net) - $192,500 Retained earnings - $148,150Paid dividends of $51,000

Basket reports the following account balances on June 30, prior to preparing its budgeted

financial statements: Land - $50,000 Building (net) - $174,500 Common stock - $200,000 Equipment (net) - $192,500 Retained earnings - $148,150Paid dividends of $51,000

The BudgetedBalance SheetThe BudgetedBalance Sheet

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-62Basket CompanyBudgeted Balance Sheet

June 30, 2004Current assets Cash 43,000$ Accounts receivable 75,000 Raw materials inventory 4,600 Finished goods inventory 24,950

Total current assets 147,550$ Property and equipment Land 50,000$ Building 174,500 Equipment 192,500 Total property and equipment 417,000$

Total assets 564,550$

Liabilities and Equities Accounts payable 28,400$ Common stock 200,000 Retained earnings 336,150 Total liabilities and equities 564,550$

25% of Junesales of $300,000

25% of Junesales of $300,000

11,500 lbs. @ $.40 per lb.11,500 lbs.

@ $.40 per lb.

50% of Junepurchases of $56,800

50% of Junepurchases of $56,800

5,000 units@ $4.99 each5,000 units

@ $4.99 each

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-63Basket CompanyBudgeted Balance Sheet

June 30, 2004Current assets Cash 43,000$ Accounts receivable 75,000 Raw materials inventory 4,600 Finished goods inventory 24,950

Total current assets 147,550$ Property and equipment Land 50,000$ Building 174,500 Equipment 192,500 Total property and equipment 417,000$

Total assets 564,550$

Liabilities and Equities Accounts payable 28,400$ Common stock 200,000 Retained earnings 336,150 Total liabilities and equities 564,550$

Beginning balance 148,150$Add: net income 239,000 Deduct: dividends (51,000) Ending balance 336,150$

Beginning balance 148,150$Add: net income 239,000 Deduct: dividends (51,000) Ending balance 336,150$

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-64

Performance evaluation is difficult when actual

activity differs from the activity originally

budgeted.

Flexible BudgetingFlexible Budgeting

Hmm! Comparingcosts at differentlevels of activity is like comparing

apples with oranges.

Consider the followingcondensed examplefrom Barton, Inc. . . .

Consider the followingcondensed examplefrom Barton, Inc. . . .

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

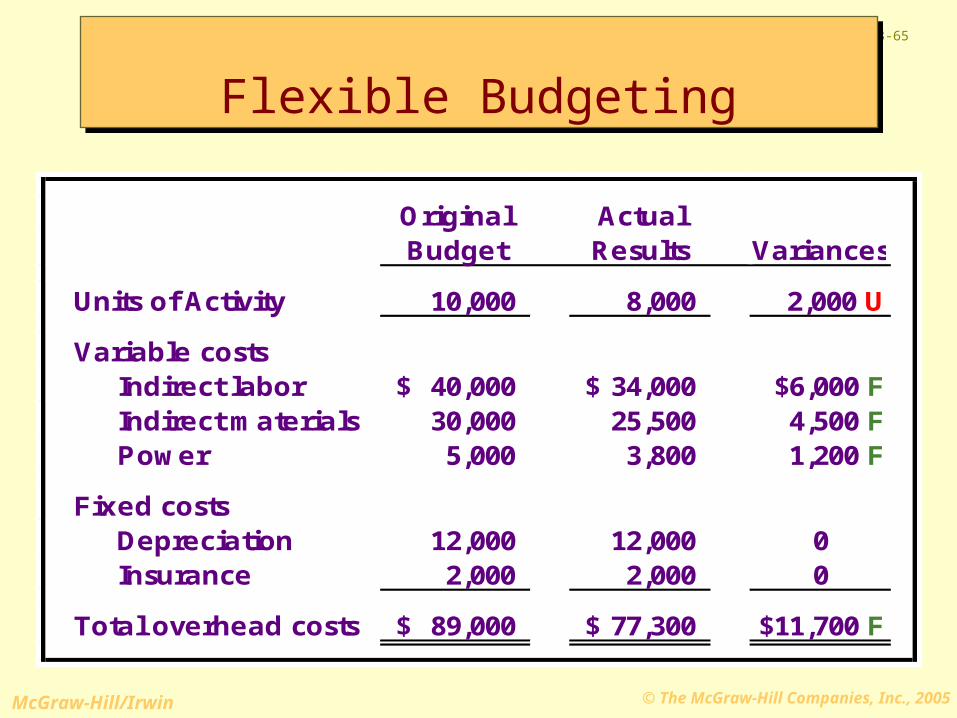

23-65

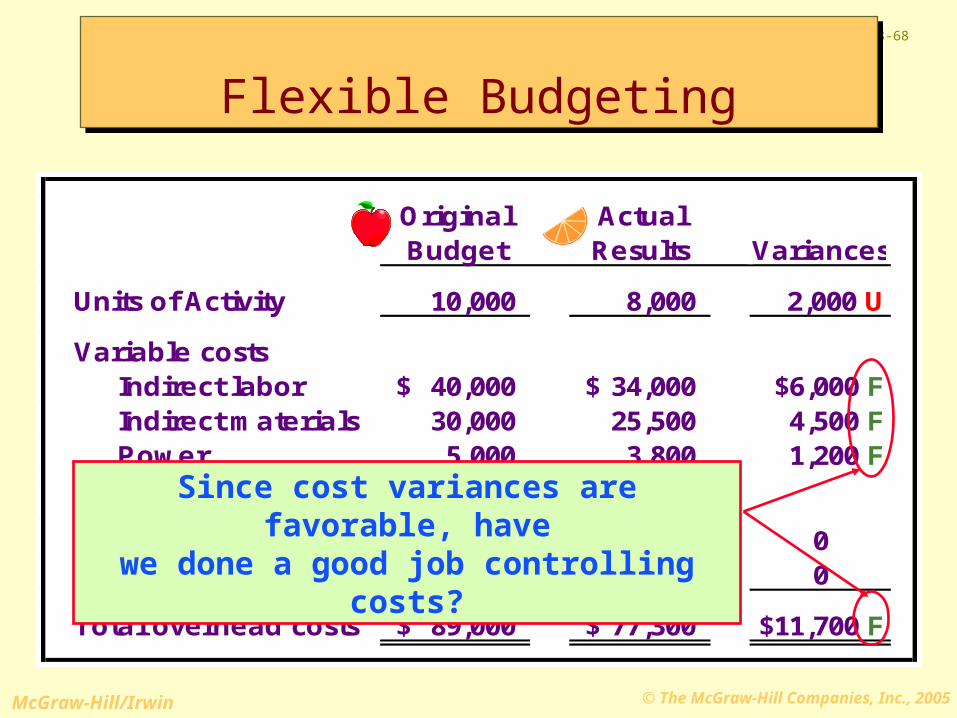

Flexible BudgetingFlexible Budgeting

Original ActualBudget Results Variances

Units of Activity 10,000 8,000 2,000 U

Variable costs Indirect labor 40,000$ 34,000$ $6,000 F Indirect materials 30,000 25,500 4,500 F Power 5,000 3,800 1,200 F

Fixed costs Depreciation 12,000 12,000 0 Insurance 2,000 2,000 0

Total overhead costs 89,000$ 77,300$ $11,700 F

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-66

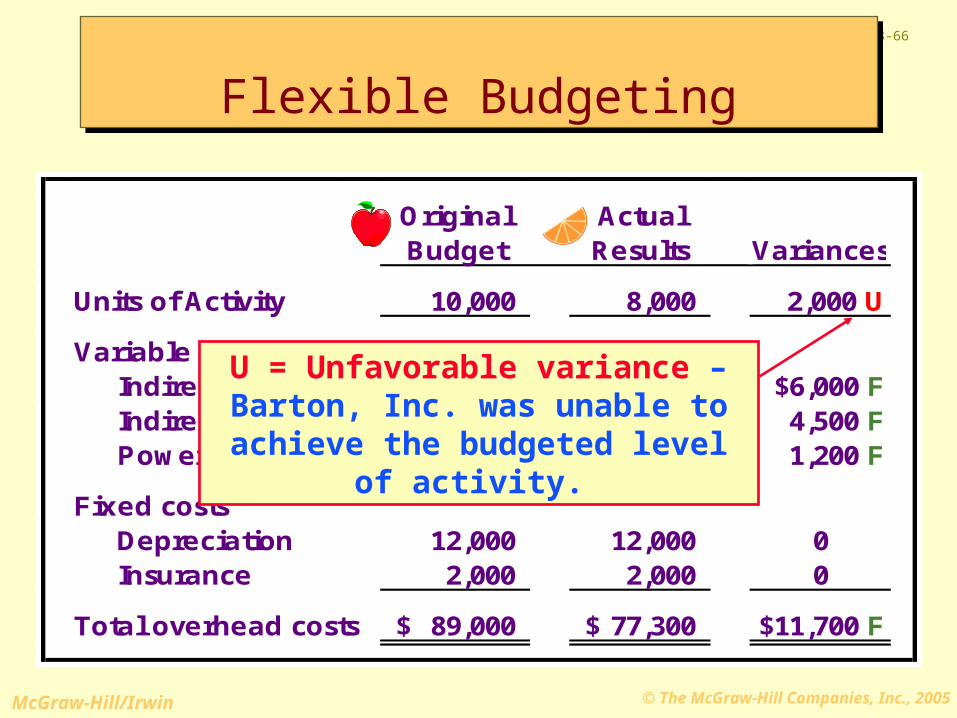

Original ActualBudget Results Variances

Units of Activity 10,000 8,000 2,000 U

Variable costs Indirect labor 40,000$ 34,000$ $6,000 F Indirect materials 30,000 25,500 4,500 F Power 5,000 3,800 1,200 F

Fixed costs Depreciation 12,000 12,000 0 Insurance 2,000 2,000 0

Total overhead costs 89,000$ 77,300$ $11,700 F

U = Unfavorable variance – Barton, Inc. was unable to achieve the

budgeted level of activity.

Flexible BudgetingFlexible Budgeting

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-67

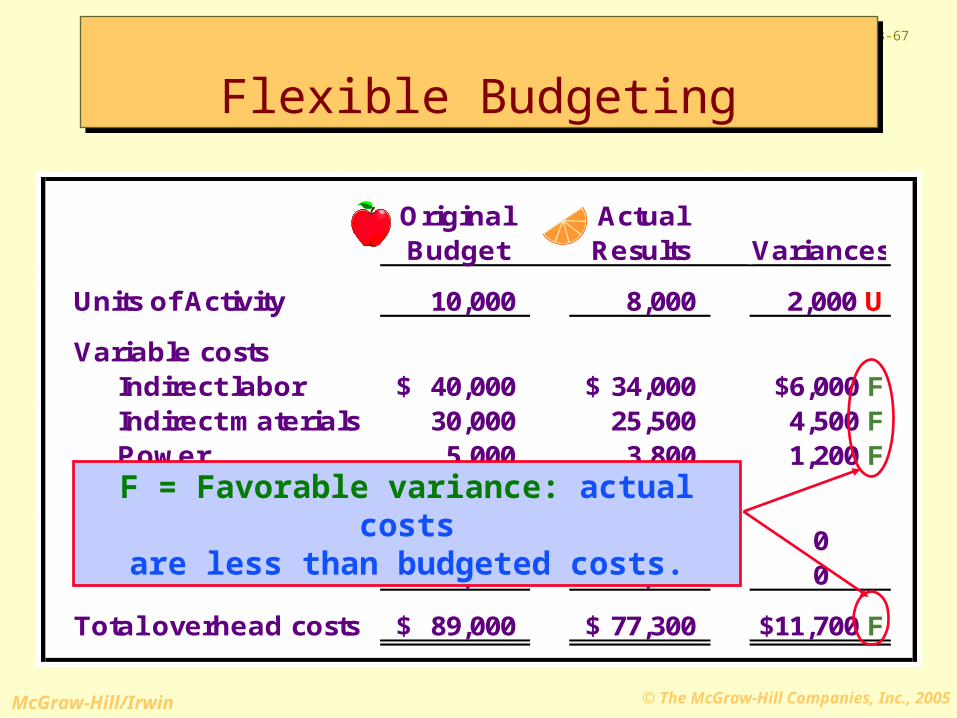

Original ActualBudget Results Variances

Units of Activity 10,000 8,000 2,000 U

Variable costs Indirect labor 40,000$ 34,000$ $6,000 F Indirect materials 30,000 25,500 4,500 F Power 5,000 3,800 1,200 F

Fixed costs Depreciation 12,000 12,000 0 Insurance 2,000 2,000 0

Total overhead costs 89,000$ 77,300$ $11,700 F

F = Favorable variance: actual costs are less than budgeted costs.

Flexible BudgetingFlexible Budgeting

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-68

Original ActualBudget Results Variances

Units of Activity 10,000 8,000 2,000 U

Variable costs Indirect labor 40,000$ 34,000$ $6,000 F Indirect materials 30,000 25,500 4,500 F Power 5,000 3,800 1,200 F

Fixed costs Depreciation 12,000 12,000 0 Insurance 2,000 2,000 0

Total overhead costs 89,000$ 77,300$ $11,700 F

Since cost variances are favorable, havewe done a good job controlling costs?

Flexible BudgetingFlexible Budgeting

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-69

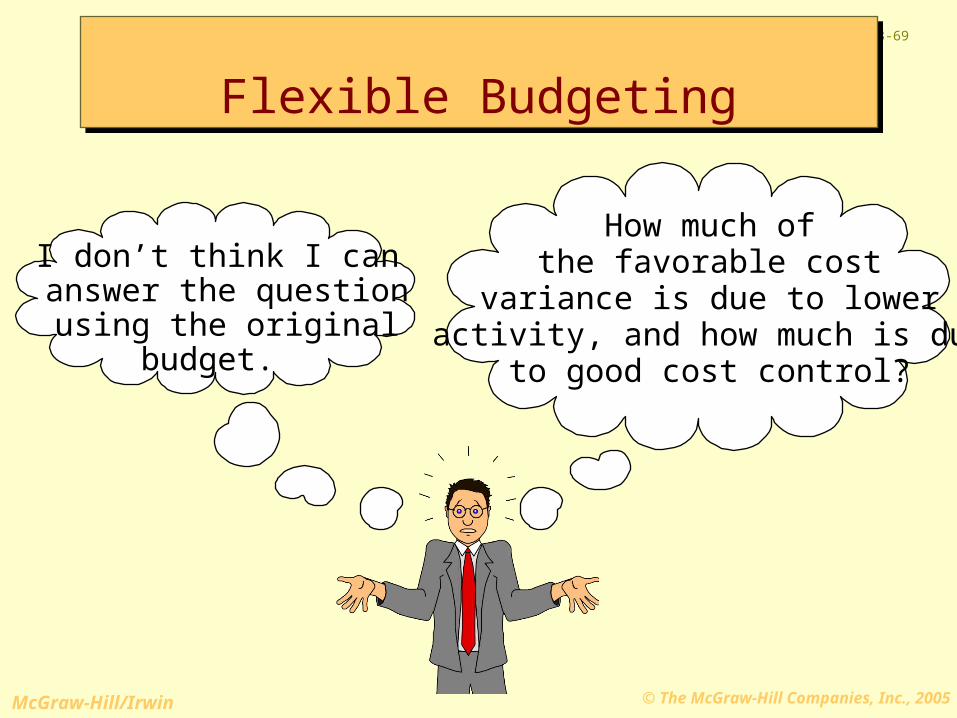

I don’t think I can answer the question

using the originalbudget.

How much ofthe favorable cost

variance is due to loweractivity, and how much is due

to good cost control?

Flexible BudgetingFlexible Budgeting

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-70

Flexible BudgetingFlexible Budgeting

I don’t think I can answer the question

using the originalbudget.

How much ofthe favorable cost

variance is due to loweractivity, and how much is due

to good cost control?

To answer the question, we mustthe budget to the actual level of activity.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-71

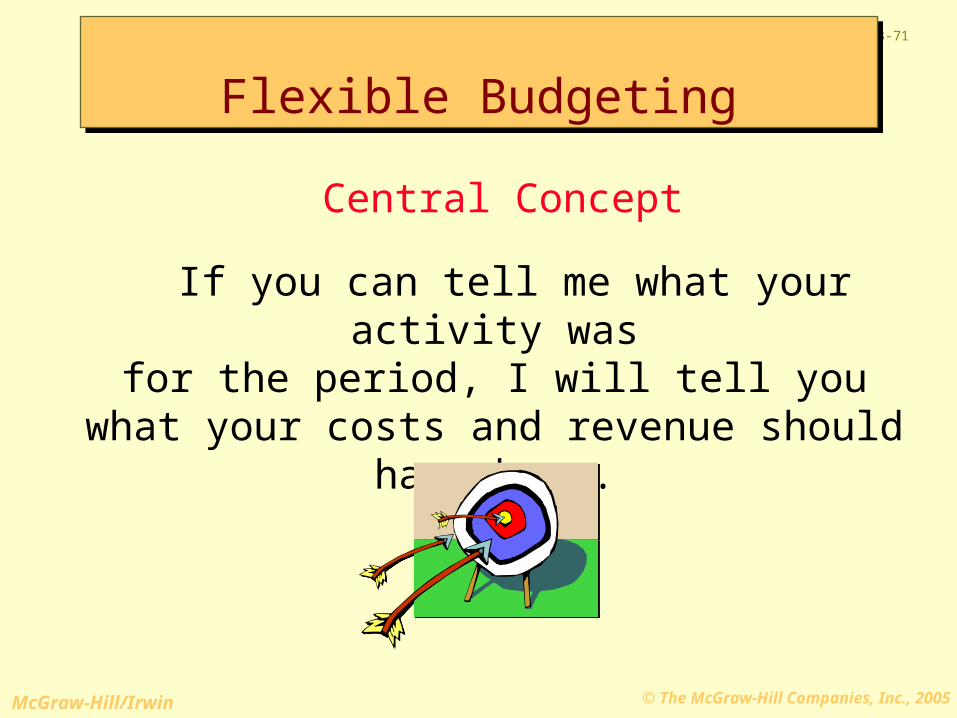

Central Concept

If you can tell me what your activity wasfor the period, I will tell you what your costs

and revenue should have been.

Flexible BudgetingFlexible Budgeting

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-72

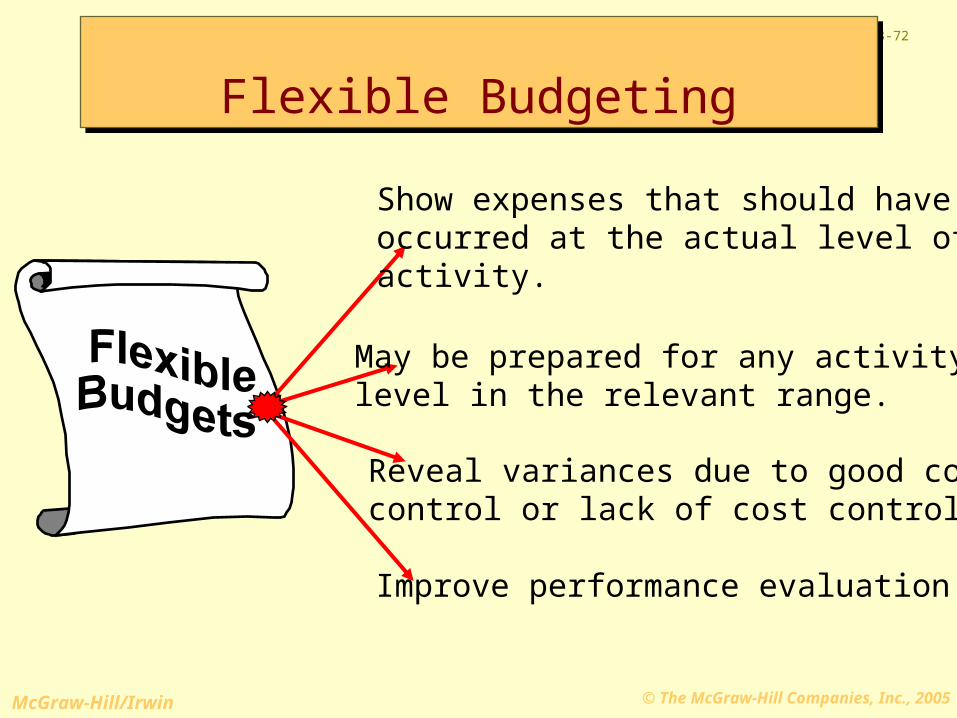

Improve performance evaluation.

May be prepared for any activity level in the relevant range.

Show expenses that should haveoccurred at the actual level ofactivity.

Reveal variances due to good costcontrol or lack of cost control.

Flexible BudgetingFlexible Budgeting

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-73

To a budget for different activity levels, we must know how costs behave with changes in activity levels.Total variable costs change

in direct proportion to changes in activity.

Total fixed costs remainunchanged within therelevant range.

FixedVaria

ble

Flexible BudgetingFlexible Budgeting

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-74

Let’s prepare budgetsBarton, Inc.

Flexible BudgetingFlexible Budgeting

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-75

Flexible BudgetingFlexible Budgeting

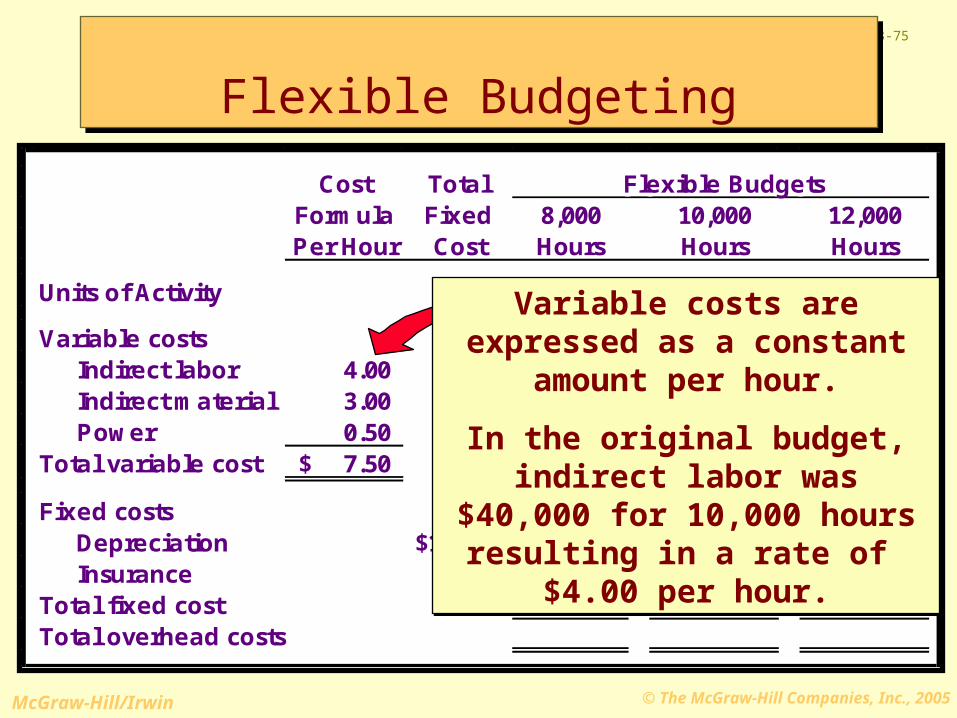

Cost Total Flexible BudgetsFormula Fixed 8,000 10,000 12,000Per Hour Cost Hours Hours Hours

Units of Activity 8,000 10,000 12,000

Variable costs Indirect labor 4.00 32,000$ Indirect material 3.00 24,000 Power 0.50 4,000 Total variable cost 7.50$ 60,000$

Fixed costs Depreciation 12,000$ Insurance 2,000 Total fixed costTotal overhead costs

Variable costs are expressed as a constant amount per hour.

In the original budget, indirect labor was $40,000 for 10,000 hours resulting in a rate of

$4.00 per hour.

Variable costs are expressed as a constant amount per hour.

In the original budget, indirect labor was $40,000 for 10,000 hours resulting in a rate of

$4.00 per hour.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-76

Flexible BudgetingFlexible Budgeting

Cost Total Flexible BudgetsFormula Fixed 8,000 10,000 12,000Per Hour Cost Hours Hours Hours

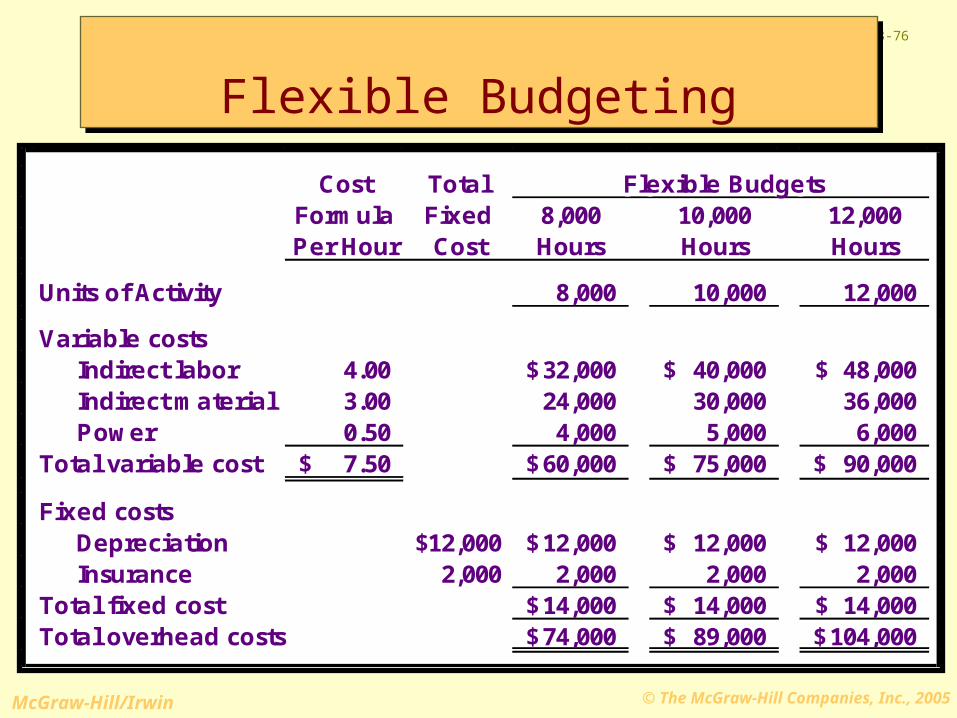

Units of Activity 8,000 10,000 12,000

Variable costs Indirect labor 4.00 32,000$ 40,000$ 48,000$ Indirect material 3.00 24,000 30,000 36,000 Power 0.50 4,000 5,000 6,000 Total variable cost 7.50$ 60,000$ 75,000$ 90,000$

Fixed costs Depreciation 12,000$ 12,000$ 12,000$ 12,000$ Insurance 2,000 2,000 2,000 2,000 Total fixed cost 14,000$ 14,000$ 14,000$ Total overhead costs 74,000$ 89,000$ 104,000$

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

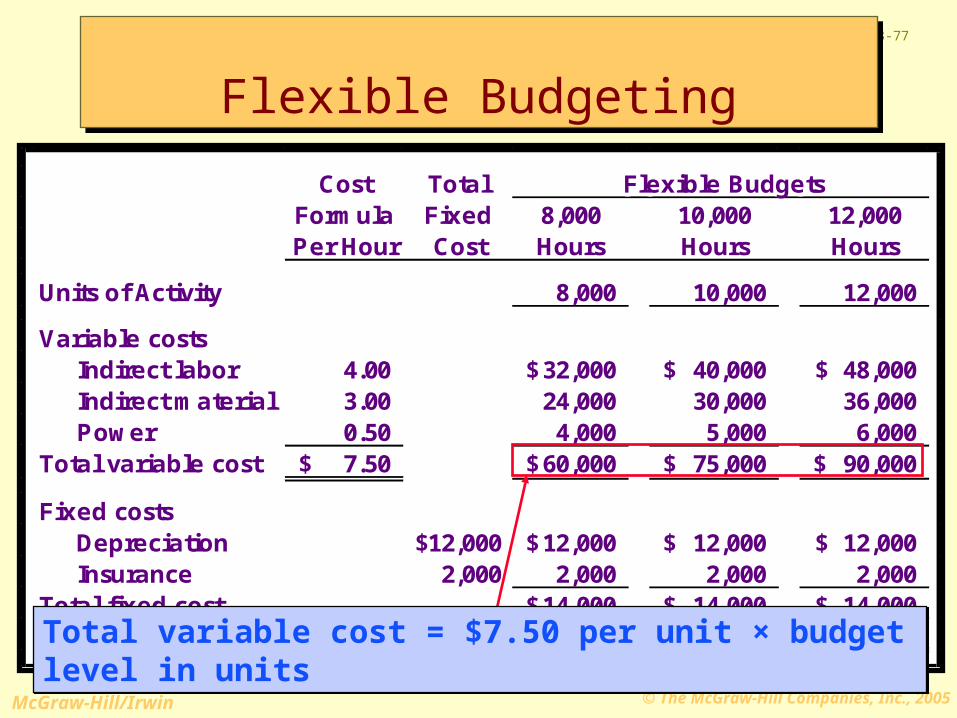

23-77

Cost Total Flexible BudgetsFormula Fixed 8,000 10,000 12,000Per Hour Cost Hours Hours Hours

Units of Activity 8,000 10,000 12,000

Variable costs Indirect labor 4.00 32,000$ 40,000$ 48,000$ Indirect material 3.00 24,000 30,000 36,000 Power 0.50 4,000 5,000 6,000 Total variable cost 7.50$ 60,000$ 75,000$ 90,000$

Fixed costs Depreciation 12,000$ 12,000$ 12,000$ 12,000$ Insurance 2,000 2,000 2,000 2,000 Total fixed cost 14,000$ 14,000$ 14,000$ Total overhead costs 74,000$ 89,000$ 104,000$

Flexible BudgetingFlexible Budgeting

Total variable cost = $7.50 per unit × budget level in unitsTotal variable cost = $7.50 per unit × budget level in units

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-78

Flexible BudgetingFlexible Budgeting

Cost Total Flexible BudgetsFormula Fixed 8,000 10,000 12,000Per Hour Cost Hours Hours Hours

Units of Activity 8,000 10,000 12,000

Variable costs Indirect labor 4.00 32,000$ 40,000$ 48,000$ Indirect material 3.00 24,000 30,000 36,000 Power 0.50 4,000 5,000 6,000 Total variable cost 7.50$ 60,000$ 75,000$ 90,000$

Fixed costs Depreciation 12,000$ 12,000$ 12,000$ 12,000$ Insurance 2,000 2,000 2,000 2,000 Total fixed cost 14,000$ 14,000$ 14,000$ Total overhead costs 74,000$ 89,000$ 104,000$

Fixed costs are expressed as a total amount that does not change within the relevant

range of activity.

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-79

Now let’s prepare a budget performance report at 8,000 actual machine hours for Barton, Inc.

Flexible BudgetingPerformance ReportFlexible BudgetingPerformance Report

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-80

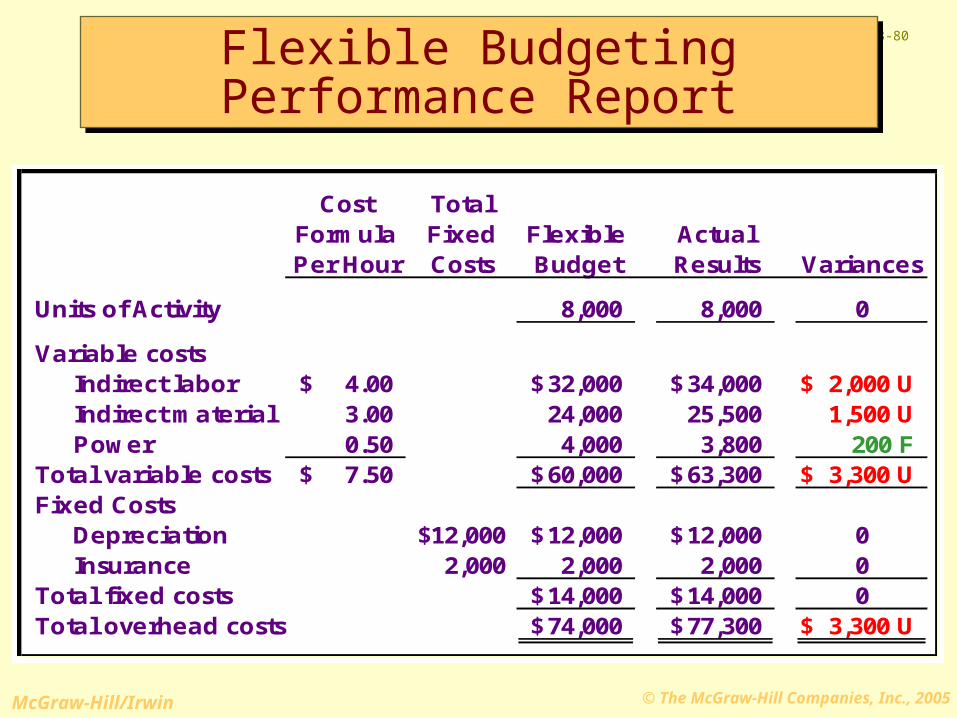

Flexible BudgetingPerformance ReportFlexible BudgetingPerformance Report

Cost TotalFormula Fixed Flexible ActualPer Hour Costs Budget Results Variances

Units of Activity 8,000 8,000 0

Variable costs Indirect labor 4.00$ 32,000$ 34,000$ $ 2,000 U Indirect material 3.00 24,000 25,500 1,500 U Power 0.50 4,000 3,800 200 FTotal variable costs 7.50$ 60,000$ 63,300$ $ 3,300 UFixed Costs Depreciation 12,000$ 12,000$ 12,000$ 0 Insurance 2,000 2,000 2,000 0Total fixed costs 14,000$ 14,000$ 0Total overhead costs 74,000$ 77,300$ $ 3,300 U

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-81

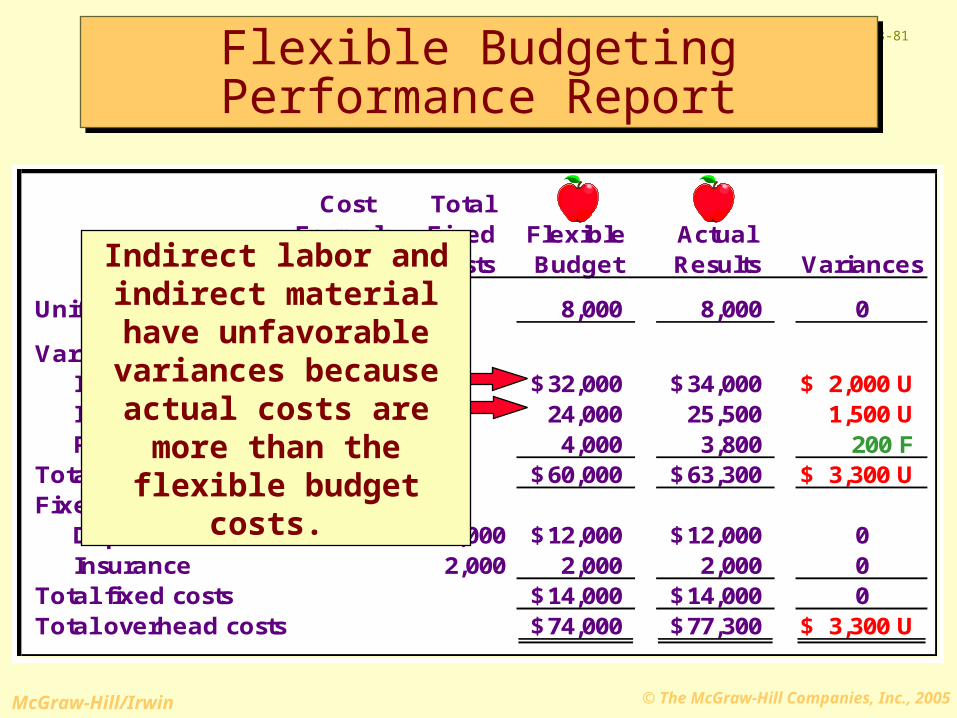

Cost TotalFormula Fixed Flexible ActualPer Hour Costs Budget Results Variances

Units of Activity 8,000 8,000 0

Variable costs Indirect labor 4.00$ 32,000$ 34,000$ $ 2,000 U Indirect material 3.00 24,000 25,500 1,500 U Power 0.50 4,000 3,800 200 FTotal variable costs 7.50$ 60,000$ 63,300$ $ 3,300 UFixed Costs Depreciation 12,000$ 12,000$ 12,000$ 0 Insurance 2,000 2,000 2,000 0Total fixed costs 14,000$ 14,000$ 0Total overhead costs 74,000$ 77,300$ $ 3,300 U

Indirect labor and indirect material have unfavorable variances because actual costs

are more than the flexible budget costs.

Flexible BudgetingPerformance ReportFlexible BudgetingPerformance Report

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-82

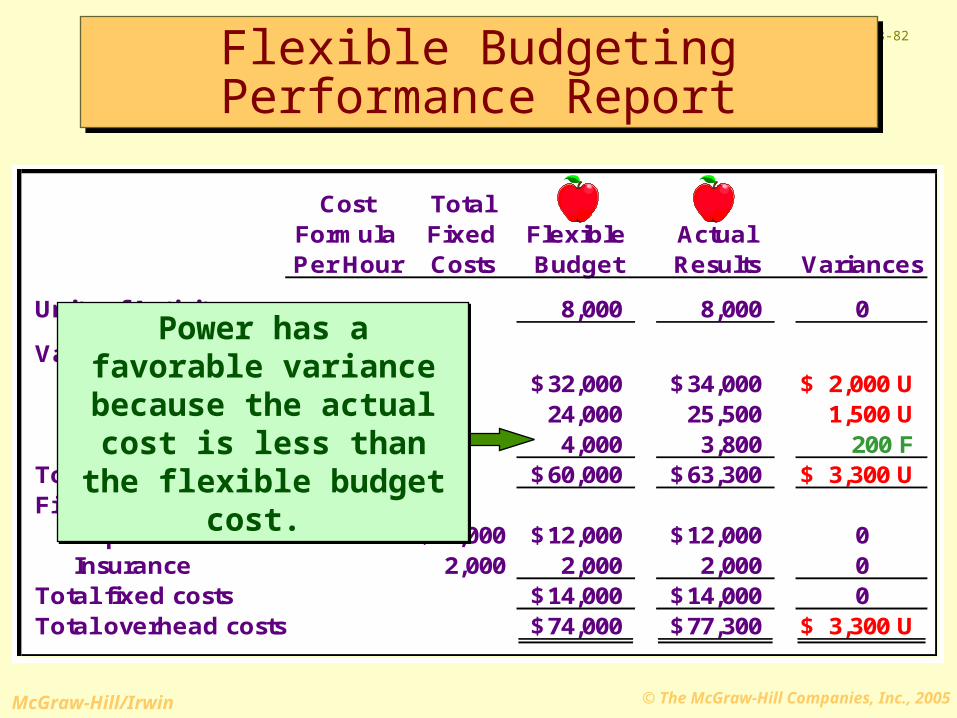

Cost TotalFormula Fixed Flexible ActualPer Hour Costs Budget Results Variances

Units of Activity 8,000 8,000 0

Variable costs Indirect labor 4.00$ 32,000$ 34,000$ $ 2,000 U Indirect material 3.00 24,000 25,500 1,500 U Power 0.50 4,000 3,800 200 FTotal variable costs 7.50$ 60,000$ 63,300$ $ 3,300 UFixed Costs Depreciation 12,000$ 12,000$ 12,000$ 0 Insurance 2,000 2,000 2,000 0Total fixed costs 14,000$ 14,000$ 0Total overhead costs 74,000$ 77,300$ $ 3,300 U

Power has a favorable variance because the

actual cost is less than the flexible budget cost.

Power has a favorable variance because the

actual cost is less than the flexible budget cost.

Flexible BudgetingPerformance ReportFlexible BudgetingPerformance Report

© The McGraw-Hill Companies, Inc., 2005McGraw-Hill/Irwin

23-83

End of Chapter 23End of Chapter 23