Today’s lesson will focus on Renewable Energy. So, what is Renewable Energy? Renewable Energy 2.

Upload

colin-randallCategory

view

214download

0

© OECD/IEA 2015

Business Models and Smart Policies for Scaling Up Renewable Energy

Dr. Paolo FranklHead, Renewable Energy DivisionInternational Energy Agency

Vienna Energy Forum, High Level Panel III, Vienna 18 June 2015

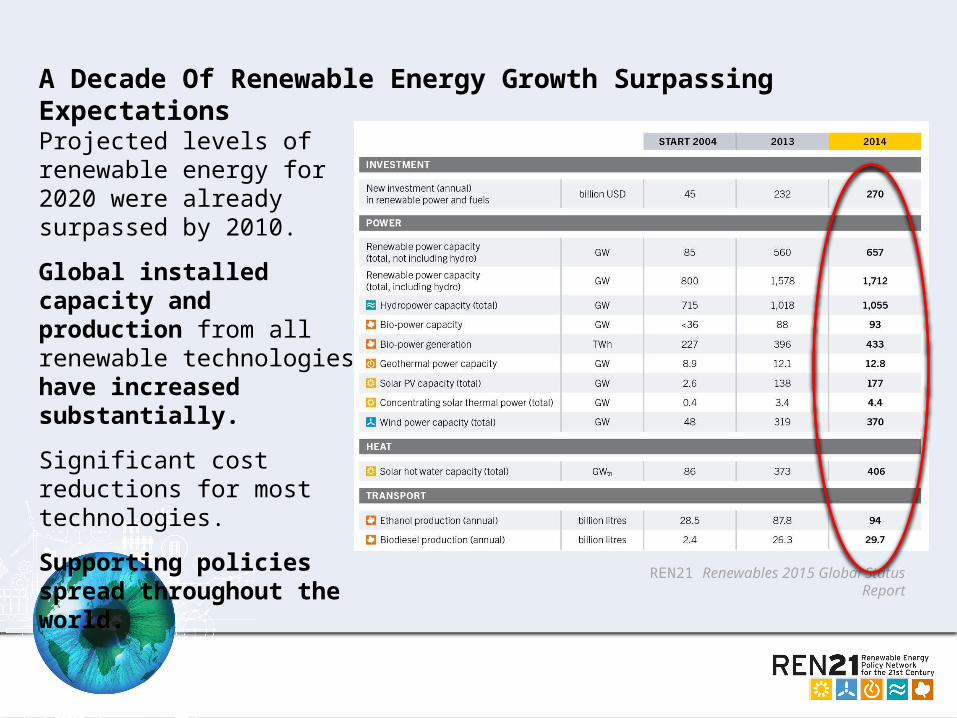

A Decade Of Renewable Energy Growth Surpassing Expectations

Projected levels of renewable energy for 2020 were already surpassed by 2010.

Global installed capacity and production from all renewable technologies have increased substantially.

Significant cost reductions for most technologies.

Supporting policies spread throughout the world.

REN21 Renewables 2015 Global Status Report

© OECD/IEA 2015

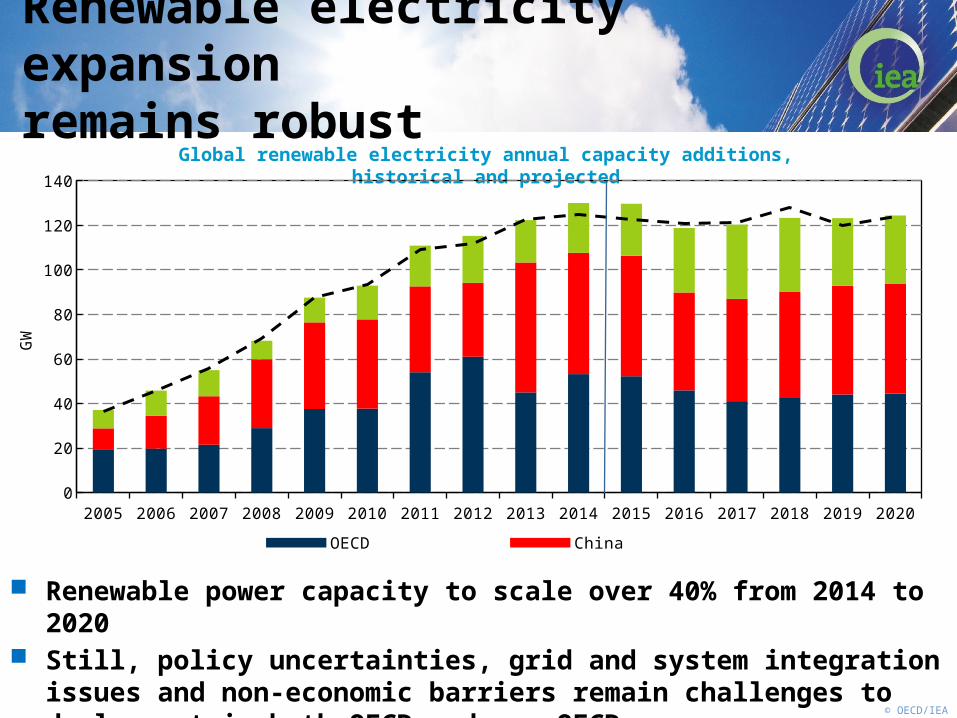

Renewable power capacity to scale over 40% from 2014 to 2020 Still, policy uncertainties, grid and system integration issues and non-economic

barriers remain challenges to deployment in both OECD and non-OECD Non-OECD markets face particular constraints accessing low cost finance

Renewable electricity expansion remains robust

Global renewable electricity annual capacity additions, historical and projected

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 0

20

40

60

80

100

120

140

OECD China Other non-OECD

GW

© OECD/IEA 2015

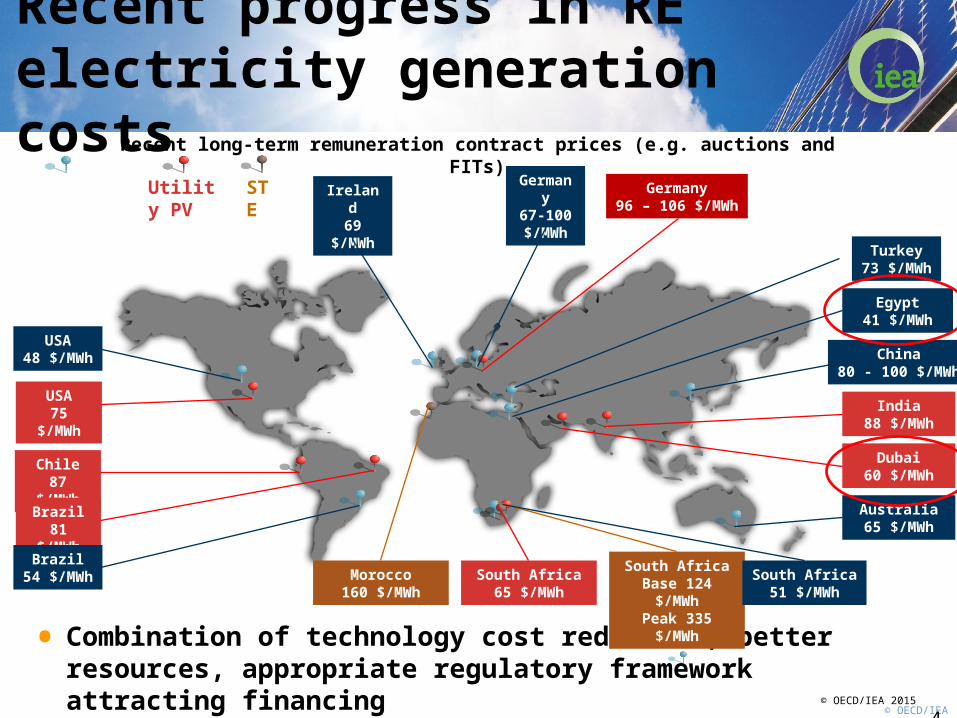

Recent progress in RE electricity generation costs

© OECD/IEA 2015 4

• Combination of technology cost reduction, better resources, appropriate regulatory framework attracting financing

• Long-term PPAs and price competition effective drivers for reducing costs

Utility PV

Recent long-term remuneration contract prices (e.g. auctions and FITs)

STE

India88 $/MWh

Chile87 $/MWh

USA75 $/MWh

South Africa65 $/MWh

Brazil81 $/MWh

Dubai60 $/MWh

Morocco160 $/MWh

South AfricaBase 124 $/MWhPeak 335 $/MWh

South Africa51 $/MWh

USA48 $/MWh China

80 - 100 $/MWh

Brazil54 $/MWh

Turkey73 $/MWh

Germany67-100 $/MWh

Ireland69

$/MWh

Australia65 $/MWh

Egypt41 $/MWh

Germany96 – 106 $/MWh

© OECD/IEA 2015

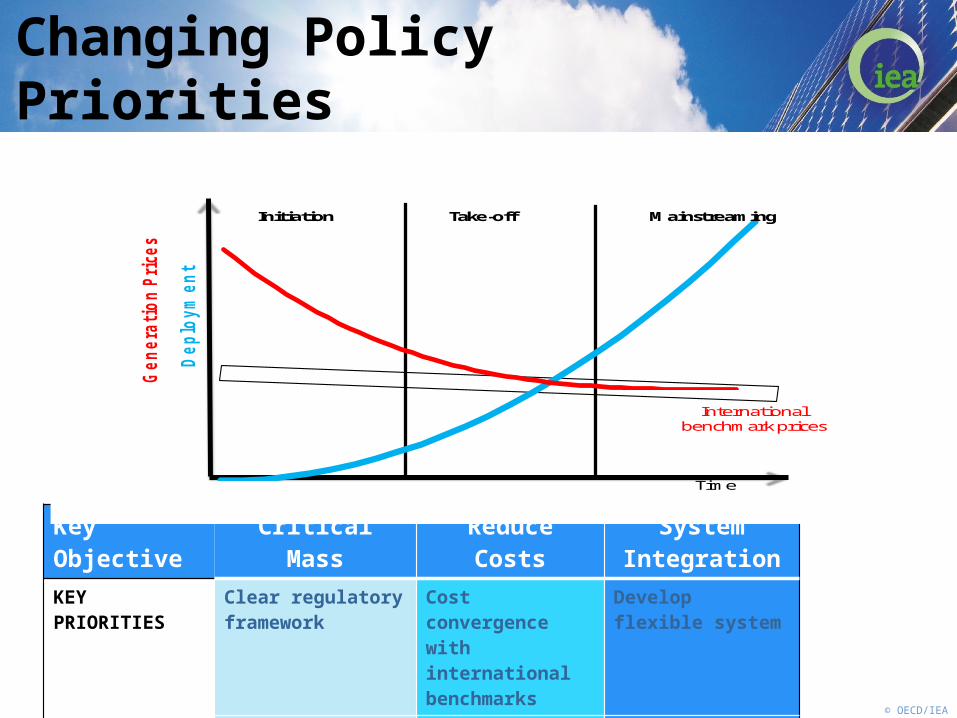

Changing Policy Priorities

• Predictable and rapidly adaptive incentives

• Focus on non-economic barriers

• Manage total support costs

• System integration Market design and expose RE to competition

• Publicacceptance

Time

De

plo

ym

en

t

Initiation Take-off Mainstreaming

Ge

ne

rati

on

Pri

ce

s

International benchmark prices

Key Objective Critical Mass Reduce Costs System Integration

KEY PRIORITIES Clear regulatory framework

Cost convergence with international benchmarks

Develop flexible system

Secure financial support

Introduce competition

Market reform

© OECD/IEA 2015

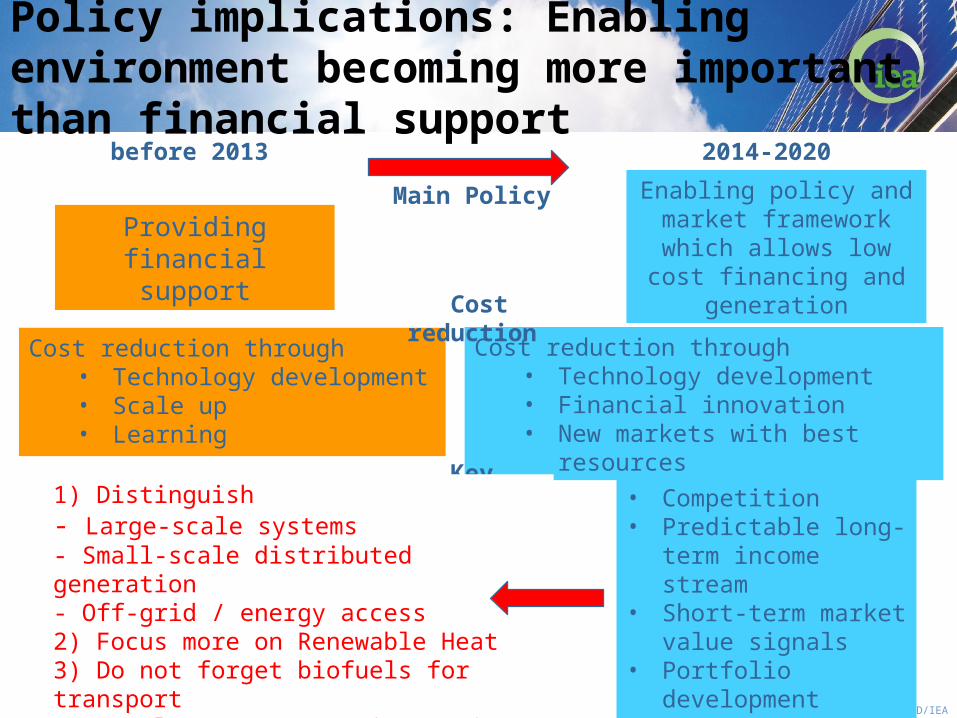

Policy implications: Enabling environment becoming more important than financial support

Providing financial support

Cost reduction through• Technology development• Scale up• Learning

before 2013

Enabling policy and market framework which allows low cost financing

and generation

• Competition• Predictable long-term

income stream• Short-term market

value signals• Portfolio development• System Integration

Cost reduction through• Technology development• Financial innovation• New markets with best resources

2014-2020

Main Policy

Key Characteristics

Cost reduction

1) Distinguish - Large-scale systems- Small-scale distributed generation- Off-grid / energy access2) Focus more on Renewable Heat3) Do not forget biofuels for transport4) Develop Energy Service Business Models

![[PPT]Chapter 18 Renewable Energy 18-1 Renewable …environmentalscienceclass.weebly.com/.../ch_18_notes.ppt · Web viewChapter 18 Renewable Energy 18-1 Renewable Energy Today Renewable](https://static.fdocuments.net/doc/165x107/5b029fb97f8b9a6a2e900bdf/pptchapter-18-renewable-energy-18-1-renewable-envir-viewchapter-18-renewable.jpg)