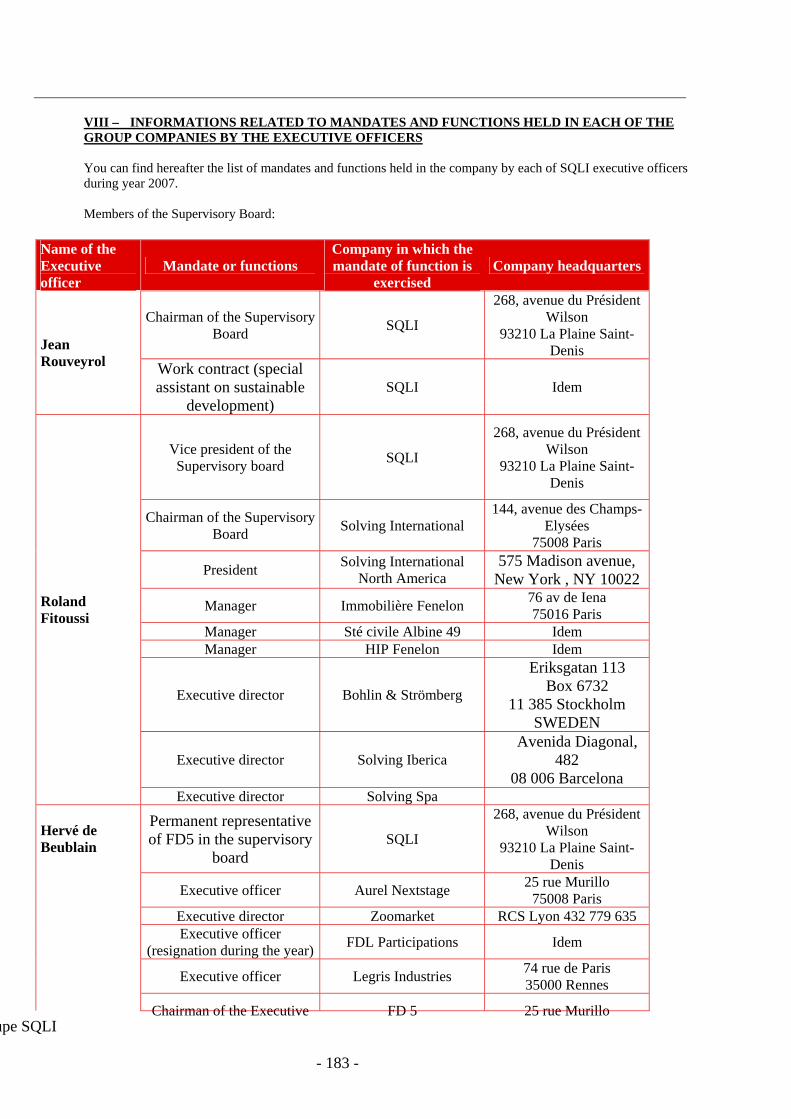

· Groupe SQLI - - 1 REFERENCE DOCUMENT AND FINANCIAL YEAR REPORT 2007 This reference document was...

200

Groupe SQLI - - 1 REFERENCE DOCUMENT AND FINANCIAL YEAR REPORT 2007 This reference document was filed with the Financial Markets Authority on 25 Avril 2008, pursuant to article 212- 3 of the FMA General Rules and Regulations. It may be used in support of a financial transaction only if it is supplemented by an operation note approved by the Financial Markets Authority. The document has been signed by the issuer and commits the signatories. Copies of the present document can be found free of charge at SQLI headquarters (La Plaine Saint Denis, Immeuble Le Pressensé - 268, avenue du Président Wilson - 93210 La Plaine-Saint-Denis), on SQLI website (www.sqli.com ) and on the French FMA website (www.amf-france.org)

Transcript of · Groupe SQLI - - 1 REFERENCE DOCUMENT AND FINANCIAL YEAR REPORT 2007 This reference document was...

Groupe SQLI - - 1

REFERENCE DOCUMENT

AND FINANCIAL YEAR REPORT

2007

This reference document was filed with the Financial Markets Authority on 25 Avril 2008, pursuant to article 212-3 of the FMA General Rules and Regulations.

It may be used in support of a financial transaction only if it is supplemented by an operation note approved by

the Financial Markets Authority. The document has been signed by the issuer and commits the signatories. Copies of the present document can be found free of charge at SQLI headquarters (La Plaine Saint Denis, Immeuble Le Pressensé - 268, avenue du Président Wilson - 93210 La Plaine-Saint-Denis), on SQLI website (www.sqli.com) and on the French FMA website (www.amf-france.org)

Groupe SQLI - - 2

1 RESPONSIBLE PERSON............................................................................................................................. 4 1.1 Person responsible for the reference document..........................................................................................4 1.2 Responsible person’s attestation.................................................................................................................4

2 STATUTORY AUDITORS ........................................................................................................................... 5 2.1 Incumbent statutory auditors.......................................................................................................................5 2.2 Auxiliary statutory auditors........................................................................................................................6

3 SELECTED FINANCIAL DATA................................................................................................................. 7 3.1 2007 : Achievement of a new stage of the business plan ..........................................................................7 3.2 2007 : Enforcement of the results improvements ......................................................................................7 3.3 Brief presentation of the main financial data..............................................................................................8

4 RISKS FACTORS........................................................................................................................................ 10 4.1 Liquidity risks ......................................................................................................................................... 10 4.2 Market-related risks (interest rates, exchange rates, shares and loans) ................................................... 11 4.3 Business-related risks.............................................................................................................................. 12 4.4 Legal risks ……………………………………………………………………………………………….14

5 INFORMATION ABOUT THE ISSUER .................................................................................................. 16 5.1 History and evolution of the company.....................................................................................................;16 5.2 Investments................................................................................................................................................18

6 GENERAL SURVEY OF THE COMPANY’S ACTIVITIES ................................................................. 23 6.1 Main activities...........................................................................................................................................23 6.2 Main markets.............................................................................................................................................29 6.3 Exceptional events that influenced the activities or the markets of the company ................................... 31 6.4 The company’s dependence upon patents, licences and other ............................................................... 32 6.5 The company’s competitive environment ............................................................................................... 32

7 ORGANIZATION CHART ........................................................................................................................ 35 7.1 Functional Organization Chart ................................................................................................................ 35 7.2 Legal Organization Chart ........................................................................................................................ 36

8 REAL ESTATE OWNERSHIP, FACTORIES AND EQUIPMENT....................................................... 39 8.1 premises assigned to operations................................................................................................................39 8.2 Environment issue.....................................................................................................................................39

9 ANALYSIS OF FINANCIAL SITUATION AND EARNINGS............................................................ 40 39.1 Analysis of financial situation .................................................................................................................40 9.2 Operating result .......................................................................................................................................40

10 FUNDS AND CAPITAL...............................................................................................................................41 10.1 Shareholder’s equity.................................................................................................................................41 10.2 Source and total amount of cash flows during 2005, 2006, 2007............................................................41 10.3 Loan conditions and financing structure...................................................................................................41 10.4 Possible restrictions on the use of capital .................................................................................................41 10.5 Expected sources of funding needed to meet the commitments...............................................................41

11 RESEARCH AND DEVELOPMENT, PATENT LICENCE................................................................. .. 42 11.1 trademarks, domain names, copyrights, intellectual property..................................................................42 11.2 Activity related to Research and Development........................................................................................42

12 INFORMATION ABOUT THE TRENDS...................................................................................... ........... 43 12.1 Trends that affected the issuer’s activity since last year-end....................................................................43 12.2 Elements that may affect the issuer’s perspectives...................................................................................43

13 PROFIT FORECAST AND ESTIMATION.................................................................................... .......... 44 13.1 Forecast hypothesis...................................................................................................................................44 13.2 Report by the statutory auditors on the conformity of the accouting methods used by the compagny....44

14 ADMINISTRATIVE, MANAGERIAL AND SUPERVISORY ORGANS..............................................46 14.1 General information about the managers and the directors......................................................................46 14.2 Conflicts of interest in the administrative and managerial organs...........................................................46

15 COMPENSATIONS AND BENEFITS.......................................................................................... ............. 47 15.1 Compensation and benefits in kind of the Executive officers during last year........................................47 15.2 Funds estimated or recorded by SQLI that were allocated to the Executive officers for pensions and other benefits……................................................................................................................................................47

16 ORGANIZATION OF EXECUTIVE AND SUPERVISORY ORGANS................................................ 48 16.1 The company’s management....................................................................................................................48 16.2 Contracts between the officers and the company.....................................................................................48 16.3 Audit and Compensation Committees......................................................................................................51 16.4 Corporate governance...............................................................................................................................51

17 EMPLOYEES..................................................................................................................................................60

Groupe SQLI - - 3

17.1 Number and distribution of employees....................................................................................................60 17.2 Participation of Executive officers in stock option..................................................................................60 17.3 Participation of employees in the company’s capital...............................................................................61

18 MAIN SHAREHOLDERS........................................................................................................................... 62 18.1 Breakdown of capital and voting rights....................................................................................................62 18.2 Main shareholders’ voting rights..............................................................................................................64 18.3 Internal management.................................................................................................................................64 18.4 Agreements that may bring a change in the company’s management......................................................64

19 OPERATIONS WITH RELATED FIRMS.................................................................................................65 19.1 Inter-company current agreements...........................................................................................................65

20 FINANCIAL INFORMATION ABOUT THE ISSUER’S NET WORTH FINANCIAL SITUATION AND RESULTS ................................................................................................................................................... 67

20.1 Historical financial statement...................................................................................................................67 20.2 Financial information pro forma.............................................................................................................103 20.3 Consolidated accounts at 31 December 2007..........................................................................................103 20.4 Checking of the annual historical financial information...........;............................................................132 20.5 Intermediate financial information and other.........................................................................................135 20.6 Payment of dividends policy..................................................................................................................136 20.7 Judicial and arbitration procedures.........................................................................................................136 20.8 Significant change of the financial or commercial position...................................................................136

21 FURTHER INFORMATION.................................................................................................................... 137 21.1 Share capital ...........................................................................................................................................137 21.2 Deed of foundation and articles of incorporation.................................................................................142

22 MAJOR CONTRACTS ............................................................................................................................. 155 23 INFORMATION COMING FROM OUTSIDERS, EXPERT DECLARATIONS OR DECLARATIONS OF INTEREST......................................................................................................................................................... 156 24 DOCUMENTS OPEN TO PUBLIC INSPECTION ............................................................................... 157

24.1 Communication rights of the shareholders (Art. 32 of status)...............................................................157 24.2 Financial communication.......................................................................................................................157

25 INFORMATIONS ON THE CONTRIBUTIONS……………………………………………………….158 26 CONCORDANCE TABLE WITH THE ANNUAL FINANCIAL REPORT.........................................159 27 APPENDICE : MANAGEMENT REPORT..............................................................................................160

Groupe SQLI - - 4

1 RESPONSIBLE PERSON In application of Article 28 of Regulation (EC) No 809/2004 of 29 April 2004 related to the prospectus, the following pieces of information are included in the Reference document: ♦ The company’s consolidated accounts and the statutory auditors’ report on the consolidated accounts for financial year ended 31 December 2006, as described on pages 88 to 118 and 159 to 160 respectively of the reference document deposited with the Financial Markets Authority on 24 July 2007 under the number D.07-735. ♦ The social accounts of SQLI Inc and the statutory auditors’ general report on social accounts for financial year ended 31 December 2005, as described on pages 119 to 158 and 161 to 162 respectively of the reference document deposited with the Financial Markets Authority on 24 July 2007 under the number D. 07-735, ♦ The company’s consolidated accounts and the statutory auditors’ report on consolidated accounts for financial year ended 31 December 2005, as described on pages 80 to 116 and 152 to 154 respectively of the reference document deposited with the Financial Markets Authority on 13 July 2005 under the number D.06-729,

♦ The social accounts of SQLI Inc and the statutory auditors’ general report on social accounts for financial year ended 31 December 2005, as described on pages 117 to 151 and 155 to 156 respectively of the reference document deposited with the Financial Markets Authority on 13 July 2005 under the number D.06-729.

The pieces of information included in these two reference documents that differ from those above mentioned have, if necessary, been corrected and/or updated by new statements included in the present reference document.

The two reference documents given above are available on the company’s website, www.sqli.com, or on the Financial Markets Authority’s, www.amf-France.org.

1.1 PERSON RESPONSABLE FOR THE REFERENCE DOCUMENT Monsieur Yahya EL MIR Chairman of SQLI’s Executive Board.

1.2 RESPONSIBLE PERSON’S ATTESTATION “After having taken all reasonable measure to this end, I attest that the pieces of information presented in this reference document fairly reflect the current situation and I certify that no information likely to have a material impact on the interpretation of this document has been omitted. I attest that, to my knowledge, the accounts are drawn up in compliance with the applicable accountancy standards and reflect faithfully the capital, the financial situation and the result of the company and its consolidated firms. The management report presented page 156 includes a table showing the evolution of the activities, the results and the financial situation for both the company and its consolidated firms, as well as a description of the main risks and uncertainties they have to face.

The statutory auditors gave me a notice of completion of work that guarantees both the audit of the financial situation and the accounts presented in this reference document, and the reading of this very document.”

La Plaine Saint-Denis, 24 July 2007

Yahya EL MIR

Groupe SQLI - - 5

2 STATUTORY AUDITORS The table below shows the audit and counselling fees of the incumbent statutory auditors appointed by SQLI for 2007. Missions FIDUCIAIRE DE LA TOUR CONSTANTIN ASSOCIES

2007 2006 N en % N-1 en % 2007 2006 N en % N-1 en %

AUDIT

· Statutory auditors and certification of consolidated annual accounts

Issuer 74 750 € 74 750 €

Fully integrated subsidiaries 20 160 €

75 500 €

95% 73%

27 100 €

84 900 €

82% 70%

· Secondary missions 5 000 € 28 500 € (1) 5% 27% 22 100 € 37 220 € (1) 18% 30%

TOTAL 99 910 € 104 000 € 100% 100% 123 950 € 122 120 € 90%

OTHER SERVICES

· Others 21 600 € (1) 13 296 € (2) Legal, financial, social

17% 10%

TOTAL 99 910 € 104 000 € 100% 100% 123 950 € 135 416 € 100% 100%

(1) Missions of external contractual audit (2) Fees paid to the foreign partners of Constantin Associés for their counselling about the American subsidiary and the auditing of the Moroccan subsidiaries’ accounts.

2.1 INCUMBENT STATUTORY AUDITORS Fiduciaire de la Tour Represented by Monsieur Claude FIEU. 28, rue Ginoux 75015 Paris Statutory Auditors registered under number 2060 in the Paris Region’s list of Accountancy Firms and a member of « la Compagnie Régionale des Commissaires aux Comptes de Paris », a Paris-based Accounting and Auditing body.

First appointed: 30 July 1995. Mandate renewed on 15 June 2007. Mandate expiry date: mandate for six financial years which will expire following the Ordinary Shareholders’

Meeting called to assess the financial statements for the financial year ending 31 December 2012. Constantin Associés Represented by Monsieur Michel Bonhomme. 26, rue de Marignan 75008 Paris

First appointed: 21 March 2000. Mandate renewed on 15 June 2007 Mandate expiry date: mandate for six financial years which will expire following the Ordinary Shareholders’

Meeting called to assess the financial statements for the financial year ending 31 December 2011.

Groupe SQLI - - 6

2.2 AUXILIARY STATUTORY AUDITORS

Monsieur Dominique BEYER 40 bis, rue Boissière 75116 Paris First appointed: 30 July 1995. 28 February 2000, replacing Mr Jean-Marc Robinet, 53, rue Eugène Carrière,

75018 Paris, the former auxiliary auditor to the Company. This mandate was renewed on 15 June 2007 Mandate expiry date: mandate for six financial years to expire following the Ordinary General Shareholders'

Meeting called to assess the financial statements for the financial year ending 31 December 2012. Monsieur François-Xavier AMEYE 114, rue Marius Aufan 92532 Levallois-Perret Cedex First appointed: 21 March 2000, renewal of mandate on 16 June 2006. Mandate expiry date: mandate for six financial years to expire following the Ordinary General Shareholders'

Meeting called to assess the financial statements for financial year ended 31 December 2011.

Groupe SQLI - - 7

3 SELECTED FINANCIAL DATA En K€ IFR

3.1 2007: A NEW STAGE OF THE BUSINESS PLAN IS ACHIEVED

Turnover (in M€) Net Result (in M€) Equity capital (in M€)

45,8

59,3

91,1

115,4

0

20

40

60

80

100

120

2004 2005 2006 2007

1,6

2,5

6,5

5,3

0

1

2

3

4

5

6

7

2004 2005 2006 2007

6,8

23,5

33

45,8

0

10

20

30

40

50

2004 2005 2006 2007

In September 2005, SQLI displayed its business plan for 2006-2008. After a good performance in 2006 for the first stage of this plan (turnover of 90 M€, operating margin of 6%), the group carried on its expansion in 2007 (turnover of 115.4 M€ and operating margin of 7.2%). The company experienced a real change of dimension during the last years: the turnover has has been multiplied by 2.5 since 2004, the net result has been multiplied by 3.3 in three years and the Equity capital has been multiplied by 6.7. SQLI perfectly achieved the two first stages of its plan in 2006 and 2007 by increasing significantly its organic growth and by gathering uniting complementary firms on its project.

3.1.1 TURNOVER INCREASE OF 27% IN 2007

The consolidated revenues reached 115.4 M€ and grew by 27% since 2006. The group clearly increased its organic growth which reached 16% in 2007 (exceeding the objective of 15%) while

it reached 12% in 2006. The 6 companies or activities (Clear Value, Alcyonix, Iconeweb, Amphaz, Urbanys et Eozen) added in 2007

participated only for 9 M€ on the year results (41 M€ for a full year). All integrations have been done as expected and helped to develop new commercial, technical and administrative synergies. The group has started 2008 whith a proforma business volume exceeding 145 M€.

3.2 2007: HIGH IMPROVEMENT OF THE RESULTS 3.2.1 STRONG IMPROVEMENT OF THE CURRENT OPERATING RESULT

The current operating result increased by 47.4% to reach 8.3 M€ in 2007 after a 162% growth in 2006. The current operating margin reached 7.2% that is 1,0% more than in 2006. The operating result has a non

recurrent cost of 0.6 M€ already registered in the first half of the year and due to a commercial strategy negotiation. Without this cost, the current operating margin would reach 7.7% in 2007.

SQLI keeps improving its margin half year after half year: the group registered a 7.9% current operating margin for the second half of 2007, while it reached 6.4% in the first half of 2007 and 6.2% in 2006.

These results are due to the big improvement in the industrialisation of CMMI and offshore processes.

T x2,5NR x 3.3

EC x6,7

Groupe SQLI - - 8

3.2.2 THE NET PROFIT PER SHARE HAS MORE THAN DOUBLED DURING THE LAST TWO YEARS

The consolidated net result increased by 112% since 2004, to reach 5.3M€ in 2007. The decrease noticed in the last year (-17.8 %) is not significant since the group registered a non payable tax of

2.7M€ which accounts for the activation of the deficit taxes reports for last years in compliance with IFRS standards.

In K€ 2004 2005 2006 Variation 2006/2005

Turnover 45 776 59 344 91 148 54% Current operating result 1 782 2 153 5 649 162% Current operating margin 3,89% 3,60% 6,20% Non ordinary incomes and expenses 45 -688 Operating Result 1 827 1 465 5 649 285% Net financial debt -27 -48 -135 Taxes on result -166 1 146 1 019 Net result, group’s share 1600 2 501 6 452 158% Net margin 3,5% 4,20% 7,10% Net diluted profit per share (in cents of euros)

0,07 0,1 0,22 120%

3.3 BRIEF PRESENTATION OF THE MAIN FINANCIAL DATA 3.3.1 SIMPLIFIED CONSOLIDATED RESULTS ACCOUNTS

In K € 2005 2006 2007 Variation

2007/2006 Turnover 59 344 91 148 115 362 +27 % Current operating result 2 153 5 649 8 328 +47 %

Current operating margin 3,6 % 6,2 % 7,2 % Non ordinary incomes and expenses -688 223 Operating result 1 465 5 649 8 551 +51 % Net financial debt -48 -135 -458 Taxes on result 1 146 1 019 -2 668* Net result, group’s share 2 501 6 452 5 303 ns*

Net Margin 4,2 % 7,1 % 4,6 % Net diluted profit per share (in euro) 0,1 0,22 0,17 ns* * : The variation of the net result is not significant, since the group registered a non payable tax of 2.7M€ which accounts for the activation of the deficit taxes reports for last years in compliance with IFRS standards.

Groupe SQLI - - 9

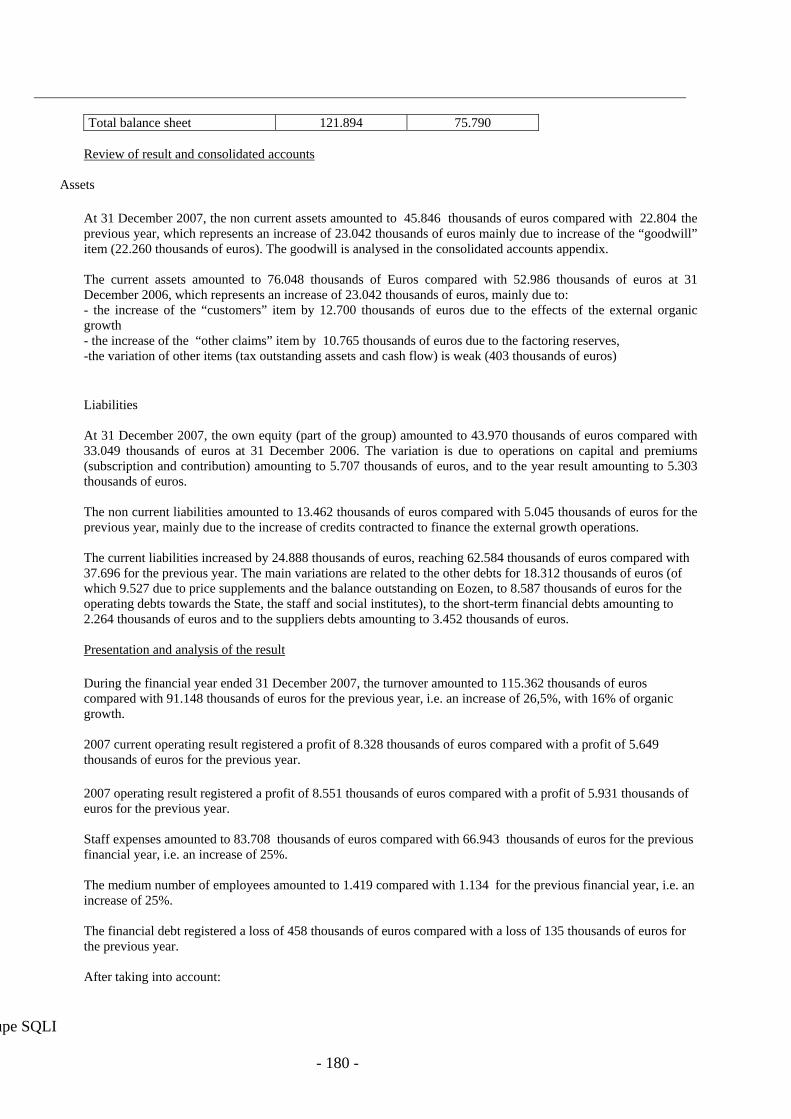

3.3.2 SIMPLIFIED BALANCE SHEET

ASSETS (M€) 31/12/2006 31/12/2007 LIABILITIES (M€) 31/12/2006 31/12/2007 Goodwill 16,3 38,6 Equity capital 33,0 45,8 Fixed assets 4,3 7,0 Long term liabilities 4,1 12,3 Deferred fixed assets 2,3 0,3 Long term funds 0,7 0,8 Non current assets 22,8 45,9 Other non current liabilities 0,2 0,2 Deferred taxes liabilities* 0,1 0,2 Credits 43,4 66,9 Non current liabilities 5,0 13,5 Eligible deferred taxes 0,3 0,5 Short term liabilities 1,8 4,1 Cash positions & équivalents 9,3 8,7 Other debts 35,8 57,5

Eligible burden taxes* 0,0 0,8 Current assets 53,0 76,0 Short term funds 0,0 0,1 Current liabilities 37,7 62,6 Total Assets 75,8 121,9 Total liabilities 75,8 121,9 * The 2006 balance sheet has been modified in order to specify the deffered taxes and the elgibile deferred taxes ans burden taxes which had before been included in the categories « other credits » and « other debts » .

Groupe SQLI - - 10

4 RISK FACTORS

The company does not acknowledge any strategy or factor of a government economic, financial, monetary or political nature which could noticeably influence directly or indirectly the issuer’s operations.

The company is not in a position to assess the relative importance of the risks factors listed below. The order in which they are presented does not take account of their importance. When it is possible to estimate quantitatively the risks, or when measures have been taken to ensure the supervising and watching of these risks, these procedures are mentioned in the following paragraphs. The company assessed the potential risks and maintains that there are no other existing risks than those presented thereafter.

4.1 LIQUIDITY RISKS

The direction reckons liquidity risk is weak because of the following facts:

The financial structure of the company is healthy : the consolidated equity capital amounts to 45.8 M€ and the available funds to 8.7 M € (financial debt non included) at 31 December 2007 (whereas the Equity capital amounted to 33 M € and the available funds to 9.3 M € at the end of 2006)

The financial debt at 31 December 2006, amounting to 16.3M€ , includes:

A 4,5M€ medium-term loan repayable over a period of 4 years contracted in October 2005 with a bank pool for the acquisition of Aston securities

a 1,3 M € loan contracted in December 2006 with a banking pool for the refinancing of Procea acquisitions and Inlog goodwill

an authorised credit line reaching a maximum of 17.2 M€ contracted with a banking pool in June and December 2007

This credit line is aimed at refinancing the acquisition of Alcyonix, Iconeweb, Clear Value and Eozen as well as other future external growth operations. The fund-raising was done in June 2007 for 5200 K€ and in December 2007 for 7 427 K€. The surplus of 4 573 K€ is payable before the 31 July 2008. The credit line is guaranteed by the share pledge of Alcyonix, Iconeweb, Clear Value and Eozen, the goodwill pledge of SQLI for 1.4 M €, as well as by a delegation of profit from liabilities guarantees granted by the sellers and a delegation of the keyman insurance contract. This loan includes a certain number of covenants and financial ratios exposed below. At 31 December 2007, the group has respected these covenants and ratios.

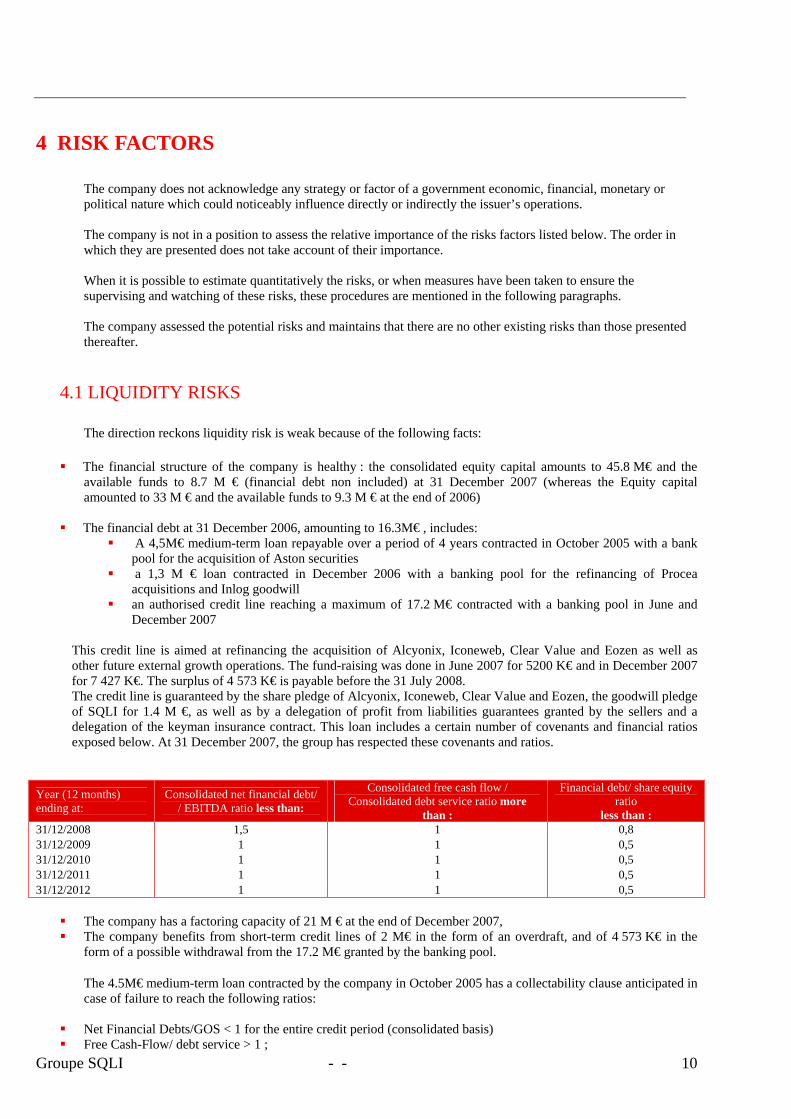

Year (12 months) ending at:

Consolidated net financial debt/ / EBITDA ratio less than:

Consolidated free cash flow / Consolidated debt service ratio more

than :

Financial debt/ share equity ratio

less than : 31/12/2008 1,5 1 0,8 31/12/2009 1 1 0,5 31/12/2010 1 1 0,5 31/12/2011 1 1 0,5 31/12/2012 1 1 0,5

The company has a factoring capacity of 21 M € at the end of December 2007, The company benefits from short-term credit lines of 2 M€ in the form of an overdraft, and of 4 573 K€ in the

form of a possible withdrawal from the 17.2 M€ granted by the banking pool.

The 4.5M€ medium-term loan contracted by the company in October 2005 has a collectability clause anticipated in case of failure to reach the following ratios:

Net Financial Debts/GOS < 1 for the entire credit period (consolidated basis) Free Cash-Flow/ debt service > 1 ;

Groupe SQLI - - 11

CIF > 2 M€ ; Medium and long term Debt/shareholders' equity and quasi own funds < 1.

The following transactions, if done without the lenders’ provisional authorization, could also lead to the anticipated collectability of the loan:

The Investments higher than 1M€ a year; External growth transactions amounting to more than 0.5 M€ a year. By way of an exception, the lenders’

provisional authorization is not required for external growth transactions that had been financed for at least 40% by a capital increase (cash or in kind) and whose cash price given for the part exceeding the capital increase is lower or equal to 3,5 M€.

All the covenants are fully respected by SQLI company. The chart below presents the company’s net financial debt at 31 December 2007

Net Financial Debt at 31 December 2006 In K€ A. Revenues 3 492 B. Equivalent tools 5 209 C. Investment securities D. Liquid assets (A+B+C) 8 701 E. Short-term financial receivables F. Sort-term banking debts 164 G. Less-than-a-year-share of mid-term and long-term debts 3 828 H. Other short-term financial debts (*) 114 I. Short-term financial debts (F+G+H) 4 106 -J. Short-term net financial debt (I-E-D) -4 595 K. Banking loans of more than one year 11 863 L. issued bonds M. Other loans of more than one year 405 N. Net financial debt tat mid-term and long term (K+L+M) 12 268 O. Net Financial Debt (J+N) 7 673

The invoicing depends on a seasonal fluctuation according to the number of working days in the month, and a year fluctuation in December related to the closing of the customers’ annual budgets. Regarding costs, there is a peak in costs on the first day of every half-year term related to pension and insurance periodic rents and costs.

4.2 MARKET-RELATED RISKS (INTEREST RATES, EXCHANGE RATES, SHARES AND LOANS)

4.2.1 EXCHANGE RISKS

To refer to the appendix VII “Further information on the balance sheet and the result account” of SQLI 2007 consolidated accounts; and more specifically to paragraph 27 of this appendix named “currency rates and exchange risk exposure”.

4.2.2. INTEREST RATES RISKS

To refer to the appendix VII “Further information on the balance sheet and the result account” of SQLI 2007 consolidated accounts; and more specifically to paragraph 19 of this appendix named “ derivative instruments related to the interest rate risk”.

Groupe SQLI - - 12

4.3 BUSINESS RELATED RISKS 4.3.1 CUSTOMER RISKS

While expanding its activity, SQLI tries carefully to keep both diversified customers (1628 active customers) and diversified business fields related to the company, in order to limit the concentration risk on a restricted number of customers. In 2007, the importance of main SQLI customers was as follows:

The first customer (Airbus) accounted for 4.5% of the consolidated turnover ;

The first 5 customers accounted for 19.5% of the consolidated turnover;

The first 10 customers accounted for 31.5% of the consolidated turnover.

The company resorts to a factoring company (credit insurance, reflection, conflicts) on the main part of its business in France. Furthermore, since the group works only for major accounts, the insolvency risk is limited.

Finally, the credit management and collection procedures that have been set allow the company to control the customer risk (advance check of the prospects solvency, monitoring outstanding invoices, follow-up on customer payment periods, customer reminders and legal proceedings). The risks related to the execution of package projects will be presented at paragraph 4.4 below.

4.3.2 SUPPLIERS RELATED RISKS

The first supplier accounts for 10.1% in SQLI purchases. The first 5 suppliers account for 27.8% in SQLI purchases. The first 10 suppliers account for 37.4% in SQLI purchases. The share made by the group with its subcontractor’s accounts for 6.2% of the turnover.

4.3.3 COMPETITION RISKS

SQLI Group reckons that the competition in the sector will intensify as the current players have become consolidated, as new Foreign Service providers have entered the market and as customer quality requirements are increasing.

But competition still remains sharp. SQLI intends to strengthen its competitive positions by industrialising its trade approach: with CMM-I, the solution approach and the offshore sector, SQLI has gained some real competitive advantages. SQLI also benefits from an increasingly strong position on the specialized market, thanks to its strong organic growth and its recent acquisitions.

4.3.4 KEY PERSONS RISKS The direction thinks that the risk of having key persons leaving is weak because SQLI Group is organised into profit centres governed by a manager, who freely runs the centre. These responsibility and freedom for operations mean that managers are heavily involved in the running of the company, creating synergies between various profit centres (commercial synergies and skills….). This organisation favours long term managerial commitment and a network organisation, by relying on other members of the group to reinforce the notion of true team. The group management checks that managers pay attention to detecting talented employees and to their career progress, so as to have potential managers available. To reinforce this cohesion, managers are involved in the capital of SQLI group. Effectively, the management team and key staff members benefit from important benefits and incentives scheme (BSPCE or stock-options).

4.3.5 TECHNOLOGY RISKS

Groupe SQLI - - 13

SQLI Group operates in an environment where technology change is particularly fast moving. Ever since its creation, the group has focused on helping its customers to take benefit from this technology. SQLI group has always been a precursor when it comes to adaptation and integration of new technologies. The move from the client/server model to the Internet in 1995 and the positioning of the Group on the Open Source model in 2000 are two good illustrations of the ability of SQLI group to use the technology changes. Although SQLI group cannot guarantee that it will always be able to quickly identify and build up knowledge for every change in technology, this ability is part of the company culture and constitutes one of its strong points.

4.3.6 RISKS RELATED TO THE EXTERNAL GROWTH POLICY

SQLI carried out three external growth operations in 2005 (LNET, ASTON and SYSDEO), two in 2006 (PROCEA and INLOG) and three in 2007 (CLEAR VALUE, ALCYONIX, INCONEWEB). This external growth strategy established by the group involves some risks. Even if these risks are hardly measurable, SQLI thinks that the risk of goodwill depreciation will exist (amounting to 16M € at the end of 2006) if the profitability does not reach the expected amount. Integration difficulties: It is considered as the major risk by the company’s managers all the more since the group tends to favour a strong degree of integration of acquired companies, in order to boost the development of commercial, technical and administrative synergies. For each future acquisition the company’s management carefully assesses the risk factors of an integration failure in order to complete the operations without guaranteeing the success of the integration. Today, the managers believe there are no specific failures regarding the integration of the recent acquisitions. Key men leaving: When the acquired companies’ managers or shareholders are considered as essential in the cooperation success, there are asked by SQLI to commit themselves to remaining in the group for at least two to three years after the acquisition. However, this commitment is not considered as essential when the only goal of these managers is to reach the price supplement objective. If SQLI is covered by the commitments subscribed, the company does not have any legal resort to secure the employees’ services. The risk can be important (in theory, SQLI could lose up to 100% of the staff and thus of the purchased companies). Until today the company hasn’t registered any difference between the manpower rotation of the purchased companies and that of SQLI. Partners leaving: Since SQLI is a services firm, its partners represent its real potential manpower. The integration of new partners in the group is thus carefully followed, and the harmonisation of working conditions is generally favourably considered. The change of working places can also create difficulties. However as most partners work in the customer offices, the headquarters move does not modify their main workplace. The announcement of the companies merger can also lead to a questioning period for some partners, and lead to a departure from the group because of the current market situation. Customer loss: SQLI group, the acquired companies and the targeted companies mostly work for major accounts. For a few years these customers have carried out an active referencing policy aiming to reduce the number of service providers. These acquisitions have thus been positively considered both by the customers of SQLI and by those of recently acquired companies, as they take part in the sector consolidation wanted by the major accounts. Today, SQLI does not register any loss of major customers related to recent acquisitions. Emergence or detection of conflicts: Even if the group carries out judicial, tax, accounting and operating due diligences on external growth transactions in order to finalize definitive agreements, an uncertainty still remains about the existence of conflicts that would not have been mentioned or translated in the accounts. The agreements relating to the acquisitions provide consequently the conventional assets and liabilities guarantees as well as the mode of paying them if they are invoked. The managers consider there is no existing conflict involving one or more of the companies purchased during 2005, 2006, except for a exceeding project of PROCEA for which the transferors have given SQLI 200K€ in compensation for the guarantee. Difference on expected results and price supplements (Earn out) : A clause allowing the payment of a price supplement if the objective expected have been met is usually inserted in the protocols of agreement related to firm acquisitions.

Groupe SQLI - - 14

Price supplements related to the objectives of turnover and margin have been decided in agreement with the transferors for the acquisitions made in 2007: IconeWeb, Urbanys, Amphaz, Clear Value, Alcyonix and Eozen. . According to the managers, there is no existing substantial difference on the results likely to have an effect on the price supplement which will be paid for IconeWeb, Urbanys, Amphaz, Clear Value, Alcyonix and Eozen. .

4.4 LEGAL RISK The SQLI Group is not subject to any particular regulatory body. More than half of the company’s business is carried out through fixed price contracts with outcome obligation (45% of the pro forma consolidated revenues). Even if the group has contract management experience for this type of contract and rarely suffers excesses, the outcome obligation resulting from these commitments can involve significant risks. To limit the range of these commitments, the company, for the majority of contracts, ensures that it: obtains a contractual penalty ceiling for late payment commits to carrying out its deliveries in conformance with the detailed specifications established by its

needs on the basis of the reference terms prepared by customers limits its responsibility in the amount of the contract or the ceiling covered by its third party insurance

SQLI SL is not integrated in the consolidated accounts of the SQLI group as its non significant nature does not imply any contractual obligation or any particular risk for the group. There is no existing government, legal or arbitrary measure, including every procedure known by the company, which is on hold or threatening the company, and which is likely to have or to have had an effect on the financial situation and the profitability of the company or the group during last 13 months.

4.4.1 REGULATION There is no specific regulation applicable to the group and its activities.

4.4.2 ENVIRONMENT RISKS

SQLI did not acknowledge any specific risk related to its activity in the industrial or environment fields, especially regarding the natural resources consumption (water, energy), the rejections in the water, the air or the soil… Consequently, no funds or guarantee against environment risks have been created. Given the nature of the group activity, no specific impact on the company’s close environment, whether good or bad, has been witnessed. In particular, the company business does not have any significant influence on the local economic development.

4.4.3 CURRENT CONFLICTS

SQLI Morocco was submitted to a tax inspection from the Moroccan tax authorities related to years 2002 to 2006. On 5 March 2008, the company has thus been notified with a few tax adjustment grounds for a total of 319 K€, related to the formal aspects of some deducting charges. The company opposed these adjustments considering them irrelevant. Without prejudice to the conclusions of the appeal brought, the company thinks that the settlement of this procedure won’t have any major impact on its results and its financial situation. No provision was then registered on this ground.

4.4.4 INSURANCE RISKS

The SQLI Group has adequate professional risk cover and is not currently implicated in any conflict related to activities not covered by its insurance policies. Risks relating to losses due to contact termination or late payment

Groupe SQLI - - 15

penalties not covered by third party insurance are covered by provisions for risks and costs in the company's accounts. The SQLI Group has a third party insurance policy with AXA company which covers any damages caused by third parties to its activities up to a maximum amount: - per accident of 7,500,000€ - per accident and year of insurance of 10,000,000€ The third party liability of the company’s representatives relating to the exercising of their mandate is covered by an insurance policy with AXA. The guarantee amounts to 10,000,000. The business loss risk is a major risk for which the company is not covered and whose management is ensured by the company itself.

Key man insurances for the Chairman of the Executive Board amounting to 1,100,000€ and 3,057,000€ have been subscribed in favour of the company. If levied, the money would be allocated to the anticipated reimbursement of the bank loans.

Table of main insurance policies in 2007

Type of risk Compagny Annual cost Extent of coverage Professional multi-risk AXA 32 K € Fire, explosion, theft, additional cost

Professional Third Party liability

AXA 0,106% of the Turnover

Operating legal liability ceiling of 7500K€ per accident Legal liability for product with ceiling of 10,000K€ per accident and per insurance year

Corporate officers and manager’s responsibilities

AXA 25 K € Fault of oversight on behalf of managers, guarantee of 10,000K€ per accident

Car fleet AXA 140 K € All Professional travelling risks

The total amount of insurance premiums paid in 2007 amounts to 207 K€.

4.4.5 DEPENDENCE UPON PATENTS AND LICENCES

SQLI does not have any dependence on patents or licences essential for its activity. The Group’s main brands (SQLI, TEchmetrix, Interligo) are protected in Europe and in the United States. All the brands belong to SQLI. There is no element owned by the company’s managers or their families. All legal forms of protection of the trademarks, domain names and the copyright have been carried out to the benefit of SQLI or its subsidiaries.

SQLI and its subsidiaries benefit from the copyright protection, enforced by the law of 3 July 1985, on all their software solutions and training aids. Major works have been deposited with a bailiff or with specialized depositories.

Groupe SQLI - - 16

5 INFORMATION ABOUT THE ISSUER

5.1 HISTORY AND EVOLUTION OF THE COMPANY

5.1.1 CORPORATE NAME AND TRADE NAME OF THE COMPANY

The company name is « SQLI »

5.1.2 LOCATION AND REGISTRATION NUMBER OF THE COMPANY

SQLI is registered in the Bobigny Commercial Register under number 353 861 909.

5.1.3 DATE OF INCORPORATION AND DURATION OF THE COMPANY 5.1.3.1 Date of incorporation SQLI was incorporated on 22 March 1990. 5.1.3.2 Legal duration (article 5) The legal duration of the Company is fixed at 99 years as from 22 March 1990, unless it is prolonged or dissolved beforehand in accordance with the Company’s articles of incorporation

5.1.4 HEADQUARTERS, LEGAL FORM AND LEGAL PROCEDURES OF THE COMPANY

5.1.4.1 Headquarters (article 4) Immeuble Le Pressensé 268, avenue du Président Wilson 93210 La Plaine-Saint-Denis Phone number: +33 (0)1 55 93 26 00 5.1.4.2 Legal form and legal procedures (article 1) SQLI is a corporation (a French "Société Anonyme"), with an Executive Board ("directoire") and a Supervisory Board ("conseil de surveillance"), under French law. It is subject to the requirements of the French Commercial Code (Code de Commerce).

5.1.5 MAJOR EVENTS IN THE DEVELOPMENT OF THE COMPANY’S ACTIVITIES

SQLI, created to accompany businesses in their use of new technologies, has specialised in realising new-generation information systems. Starting at the time of its creation in 1990, SQLI based its development on advanced technological expertise and on its intense policy of monitoring developments and R&D. The company recruits high-level engineers and experts in complex assignments, and invests large amounts in training. Strengthened by its expertise, SQLI has been able to anticipate all major computer trends and to determine their potential for the company's information system and performance.

Groupe SQLI - - 17

Being positioned on the most buoyant segments of the computer services market, SQLI keeps strengthening its leading position in e-business, SAP and Business projects and solutions.

5.1.5.1 1990 – 1995: The user-server years

Jean Rouveyrol and Alain Lefebvre created the company, focusing on the new technologies. Creation of a department of R&D and publication of comparative studies on the user-server development tools. 5.1.5.2 1995 - 1998: From user-server to the Internet

A shift is made towards Internet technologies, that help the R&D teams to resolve the problems of user-server application deployment (in 1995 the Internet is considered as the universal user-server). Creation of the « Web Agency ». Publication of an ergonomics guideline for Internet applications. Beginning of a regional development with the creation of an agency in Lyon 5.1.5.3 1999 - 2001 : Acceleration of the company’s development in order to reach the critical size Capital uplift thanks to the company’s initial public offering (listed on the new market in 2000). The company has more than 700 customers for a turnover of 45,3M€ in 2001. Purchase of Sudisim, Abcial, InVerso and Cari. Opening of a subsidiary in Switzerland. Development of the regional network (Toulouse, Bordeaux, Nantes…) 5.1.5.4 2002 - 2004: New board of directors and new development project The company’s founders form a new board of directors with an Executive board directed by Yahya El Mir. In order to meet the customers’ expectations « better, faster, and cheaper » SQLI launches the industrialization project with CMMI, which is the spearhead of the company’s strategy. The group obtains certification CMMI 2 in 2004. Industrialisation of the technical capitalization with CMMI in order to offer turnkey contracts. In 2003 is created IdeoPass the patient identity server, that will quickly be completed by a range of products in the health sector.

In 2003 is created an offshore development centre in Morocco. Totally owned by SQLI, the centre follows all methods and processes projected by the company.

5.1.5.5 2005 – Today: SQLI has become the leader of e-business projects The industrialization strategy is going on: all agencies have obtained CMMI level 3 certification in 2006. SQLI wants to reach CMMI level 5 before 2008. The range of turnkey products has improved with Ideoproject, a management and project regulation tool (result of the experience gained with CMMI). With the acquisition of Iconeweb in 2007, the range gains new job solutions for the real estate sector and in particular a promising e-data room product. With the purchase of Lnet Multimédia, Aston and Sysdeo in 2005, PROCEA and Inlog’s hospital assets in 2006, Clear Value, Alcyonix, Iconeweb, Amphaz goodwill, IconeWeb, Urbanys and Eozen in 2007, SQLI confirms his leading position in e-business sector in France; 1500 associates pool their assessments to help customers transform their information systems thanks to new technologies. To continue its development, SQLI decided to focus its efforts on:

Groupe SQLI - - 18

Strengthening its e-business company status by continuing to broaden the range of intervention so as to offer its customers a complete accompaniment while maintaining the depth of its expert skills and offering high-value added.

Developing a customer-centred sales organisation to benefit from the sole agency network for a specialised company in innovation (geographical proximity) and to accompany it over time with all of the group services. Carrying out CMM business program in 2007 should help improving the quality of the commercial relationship management.

Le développement d'une organisation commerciale centrée sur le client pour profiter du réseau d'agence unique pour une société spécialisée dans l'innovation (proximité géographique) et l'accompagner dans la durée avec l'ensemble des prestations du groupe. La mise en place du programme business CMM au cours de l’exercice 2007 a contribué à améliorer la qualité de la gestion de la relation commerciale.

Continuing to carry out of a service industrialisation strategy combining: o Total control of the sotftware development process (CMM-I approach). The acquisition of Alcyonix in

2007 helps reinforce SQLI offer (support and tools) ) throughout high quality advice, and authorization for CMMI certification. (SEI partner)

o Offshore development centre (meant to cut production costs). The subsidiaries in Morocco have 130 employees in June 2007 and should keep on increasing their staff. The construction of an offshore center on Mohamed 1er university campus in Oujda is planned for 2007 in order to accelerate the development.

o Turnkey software solutions (Solutions programme). SQLI keeps on building its solutions portfolio: local authorities, health care, (reinforced by Inlog hospital activity in 2006), Ideoproject (SQLI program used to implement CMMI), company estate with the acquisition of Iconeweb.

o Developing commercial, job and administrative synergies with the companies purchased in 2005. o Accelerating the company development with external growth operations targeted on firms able to

reinforce the range of e-business competences, the catalogue of software solutions, or the regional establishment. o The development of an e o The development of an expertise around SAP (through the acquisition of Eozen and Clear Value). SQLI is

becoming a major actor of SAP support in Europe and covers all the demands of the major accounts.

5.2 INVESTMENTS 5.2.1 DESCRIPTION OF SQLI’S MAJOR INVESTMENTS DURING THE LAST THREE YEARS Excepted the external growth operations carried out in 2005, the group did not make any major investment during the last three years. The production equipment mainly consists in premises taken out on commercial lease, computer hardware, and hired vehicles, and does not require any investment from the company.

5.2.1.1 EXTERNAL GROWTH OPERATIONS CARRIED OUT IN 2005

LNET Multimédia Company became associated with SQLI after having been put in receivership in October 2004. Supported by SQLI, LNET administrators suggested a continuation plan that was accepted by the Commercial Court of Nantes on 16 March 2005. Within the framework of this plan SQLI purchased for 6 euros all the shares of LNET and recapitalized the company up to 200K€. The goodwill of 494 K€ represents the difference between the purchase price of the securities of SARL LNET Multimédia, LNET Morocco and IROKO.net, and their net assets ended 28 February 2005 on the basis of IAS/IFRS standards. Given the net result of 154K€ performed by LNET in 2005 and 189K€ in 2006, this external growth operation is already a financial success. Lnet Morocco and SQLI Morocco merged in 2007 in order to make the local administration easier. Lnet Multimedia is in charge of the whole R&D open source for the group. This explains why the net results amounts to –204 k€. A transfer of the R&D from Lnet Multimedia to SQLI is planned for 2008. Aston has been purchased in cash for 50% of its securities, i.e. 774,149 securities at a price of 3.994€ per share; the 50% remaining have been given in kind and paid with SQLI securities according to the exchange rate of 2 SQLI shares for 1 ASTON share. The transfers in cash and in kind have been made between 29 July 2005 and 7 November 2005. The final price of 8,942 K€ contains a price supplement of 2,339 K€ calculated in relation to the 2005 results obtained by ASTON and that was due on 31 December 2005. This price supplement has been paid in April 2006, and consisted in 1.459K€ in cash and 434.953 SQLI shares in kind.

Groupe SQLI - - 19

The acquisition charges have been integrated in the purchasing costs for 282K€. During ASTON entry in the group’s perimeter on 1st November 2005 a goodwill of 10,037K€ representing the difference between the acquisition value of Aston securities and its net assets on 31 October 2005 on the basis of IAS/IFRS standard has been recorded. This goodwill has been slightly diminished at the end of 2006 reaching 9.954K€. The economies of scale related to the move of Aston teams in SQLI premises in Paris, Lyon and Toulouse, to the steering groups, to the cut of administrative staff should result in a saving of 1.5M€ per year from 2006. Moreover, Aston Education activity which was in deficit left the group sphere on 31 October 2005. From 1st January 2006, Aston activity has been transferred to SQLI throughout a management lease contract that allowed a total operational merger of the team. Aston is by now structurally in benefit: the company does not bear any operating charges and gets the management lease fees from SQLI.

Aston has been consolidated since 1st November 2005. Aston company has been dissolved in 2007, by consequence of a universal transfer of assets. Sysdeo has been purchased in application of the protocol provisions signed on 9 November 2005: 60% of securities that is 60,502 securities have been purchased in cash for 39.27 euros per share, and the 40% remaining securities have been given in kind and paid with SQLI securities according to the exchange rate of 17.45 SQLI shares for 1 Sysdeo share. The acquisition charges have been integrated in the purchasing costs for 235 KE. The final price of 4,915 KE contains a price supplement of 720 KE calculated in relation to the 2005 results obtained by Sysdeo. This price supplement has been paid in April 2006 for the amount of 431K€ in cash and 127.983 SQLI shares in kind in June 2006. The goodwill amounts to 4.282K€ and the net result at the end of 2006 to 186K€. Sysdeo has been consolidated since 1st November 2005. The lease of Sysdeo came to terms at 1st January 2007. The company has then been dissolved by consequence of a universal transfer of assets.

5.2.1.2 EXTERNAL GROWTH OPERATIONS MADE IN 2006

PROCEA was purchased on 10th August 2006 and consolidated from 1st July 2006. 5°% of the shares i.e. 1250 shares have been purchased in cash for 560€ per share and 1250 shares in kind paid with 273.435 SQLI shares according to a share ratio of 218, 75 SQLI shares for one PROCEA share.

The acquisition charges have been integrated in the acquisition price for 128k€.

The guarantors agreed to give SQLI 200K€ deducted from the acquisition charges as a compensation for the commitments subscribed for the assets and liabilities guarantee. According to PROCEA results in 2007, a price supplement amounting to 600K€ at the most will be able to give rise to a payment from SQLI. The temporary acquisition price amounts to 1.327K€, the goodwill to 1438K€. Procea company has been dissolved in 2007, by consequence of a universal transfer of assets.

Groupe SQLI - - 20

Inlog hospital assets have been purchased on 26th October 2006 and have been integrated on 1st October 2006 (date of entry in SQLI’s perimeter) for the following values: - Vigilink/Jurilink businesses assessed at 280K€ and paid in cash - Image Pharma business assessed at 720K€ and paid in cash for 220K€ and in kind for 500K€ trough the issue of 190.114 SQLI shares. A price supplement for Image Pharma licences until of June 2007 has been paid at 28 September 2007 by SQLI. This price supplement amounted to 104 K€ under deduction of the issue cost of 10K€, charged on the issue premium.

The acquisition costs amount to 153K€.

5.2.1.3 EXTERNAL GROWTH OPERATIONS MADE IN 2007

The group CLEAR VALUE consists in CLEAR VALUE based in Paris and its subsidiaries (owned at 100%), APPIA CONSULTING, a company whose headquarters are located in Paris, and CLEAR VISION INTERNATIONAL, a company incorporated in Luxembourg, which owns 100% of CLEAR VISION capital. This group has developed an advanced expertise on SAP solutions in the three sectors of the SRM (relationship with the supplier), the CRM (relationship with the customer) and FSCM (electronic invoicing). The group has been purchased according to the procedure signed on 15 December 2006, modified by additional clauses on 31 January 2007. The fixed share of the acquisition price amounts to 6.016K€, 189.040 Clear Value’s shares (22% of Clear Value shares) have been paid in cash for 1.324K€; 670.235 Clear Value (78% of the capital’s shares) have been given in kind and paid by the issue of: - 1 116 633 SQLI’s ordinary ABSA, divided for the need of the price supplement in 955 221 shares category A allowing to the subscription of ordinary shares (ABSA A) and in 161 412 shares category B allowing to the subscription of ordinary shares (ABSA B). - 621 311 SQLI’s ordinary shares 1.737.944 new SQLI shares according to the exchange rate of 2,593 SQLI share for one Clear Value share. A price supplement amounting at the most to 1.000K€ (22% in cash and 78% in SQLI new shares at the current value) will possibly lead to a payment from SQLI if the result objectives for 2007 are reached. According to the information currently available, the price supplement is totally owed to the founders. The group’s activity focuses on advices for SAP architectures especially for new open tools on the internet. In 2007, the combined turnover reached 5 975 K€ for a combined net profit of 860 K€. The company has 46 employees. The acquisition costs amounted to 95 K€. Clear Value has been consolidated from 1st January 2007. Alcyonix group (which consists in Alcyonix Inc in Canada and Alcyonix France SARL) has been purchased on 30 April 2007. The group activity focuses on advices and certification with CMMI, Capability Maturity Model Integration. The acquisition of 100% of the two companies’ capitals has been paid in cash for 1.053K€. A price supplement of 187K€ will be possibly given if the objectives for 2007 are reached. It WILL be paid before the 30 June 2008. The consolidated turnover for 2007 amounted to 1 812 K€ for a net consolidated profit of 33 K€. The group has 9 employees. The acquisition costs (legal fees, registration fees..) related to this acquisition amount to 89 K€.

Groupe SQLI - - 21

This acquisition will be consolidated from 1st May 2007. Its contribution to SQLI results amounts to a profit of 120 K€. Iconeweb Group (which consists in Iconeweb multimedia SAS and its subsidiary Iconeweb Maroc) has been purchased on 31 May 2007. The group’s activity focuses on the conception and selling of company estate solutions (websites dedicated to the promotion of building complexes, electronic e-data room..). The acquisition of 100% of the two companies’ capitals has been paid in cash for an amount of 3.115K€. A price supplement amounting up to 435K€ (and at the most 565K€ if the objectives are surpassed) will possibly be paid according to the turnover and the margin in 2007 and 2008. In 2007, no price supplement has been registered as the conditions have not been fulfilled. The acquisition costs (legal fees, audit, contribution commissioner, business contributor, registration fees..) related to this acquisition amount to 41 K€. The group’s turnover reached 1 785K€ in 2007 for a net result in deficit of 292K€. The company has 35 employees. This acquisition has been consolidated on 1st June 2007. Its contribution to SQLI results is a loss of 330K€. URBANYS group. SQLI took control of URBANYS company. Based in Suresnes, URBANYS has developed a complete consulting offer going from consulting in architecture and governance of the information system MOAP aiming at improving the performance of information systems in order to match the jobs and economy objectives of the company. Operating in France and in Luxembourg, URBANYS is also famous for its consulting offer on the accompaniment for processing improvement related to the referentials CMMI, ISO, 9001, ITIL, COBIT… This acquisition has been made according to the procedure signed on 23 November207. 8 890 shares, that is 100% of the capital, have been purchased in cash for a fixed price of 2000K€. According to the procedure, a price supplement of at the most 600K will be possibly paid from SQLI if the turnover growth objectives are reached for 2008 and 2009 (subject to certain result levels). The acquisition costs (legal fees, registration fees…) related to this acquisition amount to 129K€. The company’s turnover amounted to 2 875K€ in 2007 and the net result to a profit of 190K€. It has 20 employees. URBANYS and its subsidiary, the company EASYLINK (owned for 99.2% from URBANYS) were consolidated on 1st December 2007. There contribution to SQLI results amounts to a profit of 26K€. The assets of Amphaz company, subsidiary of Altitude have been purchased on 16 November 2007, and take effect on 30 November 2007 (date of integration in the group). Created in 2000 , Amphaz is specialised in consulting and integration of databases and decision making tools. It thus performed the integration of Business Object solutions for more than 1000 clients since the beginning. Amphaz has been primed in 2007 by Business Object for the best progress in 2006. The company relies today on 75 partners, located in Paris, Toulouse and Rouen. With this acquisition, SQLI has strengthened its Business Intelligence department, Which is now made of 150 people offering a complete offer for various types of customers. The price of the acquisition is made as follows:

Goodwill acquisition price 1 500 K€ Price adjustment on the basis of 0.35 times the turnover amount in 2007 535 K€ Value of tangible assets 133 K€ Acquisition fees 78 K€ Total 2 246 K€

The acquisition costs amount to 78K€.

Groupe SQLI - - 22

Eozen group is made of Eozen Belgium, a limited company under Belgian law, of EOZEN, a limited company under Luxembourg law which owns 100% of EOZEN France’s capital, and of EOZEN SINGAPOR. SQLI made an acquisition of majority holding (51%) of Eozen with an agreement signed on 19 December 2007, and integrated Eozen company on 31 December 2007. EOZEN is a top-end consulting firm dealing with all types of SAP offers, with a strong competence in the retail sale industry, the media and the energy distribution. EOZEN is one of the 4 major members of SAP Council in Benelux. Eozen’s imports value amounts to 15.2 M€ for 100% of capital and vote rights. This acquisition price is equal to 0.7 times the amount of Eozen 2007 turnover that is 21.8M€. The acquisition of 51% of both companies’ capitals has been made in cash for an amount of 7.8M€. The takeover of the remaining 49% will be done before 30 June 2008 through a payment in kind of the minority holders’ shares with the attribution of SQLI securities for the price firm part, and with the issue of equity-warrant securities for the price variable part. According to the agreement, Eozen acquisition price was set on the basis of a minimum of 0.7 times until a maximum of 1.2 times the consolidated revenues amount for 2007. The final rate will be set according to the EBIT growth rate and the consolidated revenues for 2008 and 2009 made by the group CLEAR VALUE and EOZEN together inside SQLI group.

5.2.2 DESCRIPTION OF MAJOR CURRENT INVESTMENTS SQLI wants to start the building of an offshore platform on Mohammed 1er university’s technology campus in Oujda. The university would provide the site for free and SQLI would have to finance the construction of a building for an amount of 500K€ for a first site of 1500M2 on average.

5.2.3 DESCRIPTION OF MAJOR FUTURE INVESTMENTS After three years of intensive acquisition policy towards value-added companies, SQI external growth policy should now slow down in order to consolidate its position. However SQLI doesn’t exclude to make new acquisitions in case of interesting propositions being offered. The presentation of the new three years plan will be done in the fall and should give more indications about the company’s future strategy.

Groupe SQLI - - 23

6 GENERAL SURVEY OF THE COMPANY ACTIVITIES

6.1 MAIN ACTIVITIES 6.1.1 JOBS AND CUSTOMERS

6.1.1.1 Jobs SQLI focuses its activity on e-business projects, which consist in all the projects in connection with the information systems integrating the use of internet technologies. As Architects of e-business solutions, SQLI accompanies its customers on the basis of two main assignments:

Modernisation of the information system in order to make it more productive, more flexible and more agile to

be able to cope with the company’s strategic evolution. This modernisation mainly relies on the integration of the internet technologies into the existing applications in order to upgrade the performance of the trade process;

The use of internet technologies to offer new web services in the objective to promote new marketing channels

(e-commerce websites), to improve the customer relations (customer portal), to boost the services offered to partners (extranet partners), to adapt the company communication (institutional websites and intranet communication…)

In order to help companies use internet technologies, SQLI offers a global accompaniment throughout the

entire project lifecycle: advisory services to help the customers make the good choices, the concrete fulfilment of these choices throughout integration and an accompaniment in the project deployment and the skill transfer.

UNDERSTANDING BUILDING ACCOMPANYING SI consulting

• Development of the SI (SOA, BPM, MCO, Mobility…) • Software factory and project industrialization • Project governance • SI indicators and pilots

Projects • Integration and specific developments • 100% ebusiness: Java/J2EE, Microsoft, OpenSource and NetWeaver SAP • 45% of package projects Quality approach: 100% CMMI 3

Skill Transfer •150 seminars and ebusiness lectures • eLearning and lessons • books, White Paper, Blogs • Publications in specialized medias

IdeoFactory IdeoProject IdeoPtima

OUR SOLUTIONS IdeoFactory IdeoProject IdeoPtima

e-business consulting • ebusiness services (CRM, SCM, BI, e-commerce…) • dematerialisation of the flows (FS, Extranet partners…) • Company portal and knowledge management •Communication sites

Web Agency • Visual identity (graphic design, brand image…) • Respect of the standards (Web 2.0, Rich media, accessibility…) • Front-office intuitive interface (usability, ergonomics, performance, user)

Qualification & monitoring • SI performance (audt, optimisation, architecture, reliability…) • Operational condition maintenance (TMA & MCO) • Functional validation (TRA) • Websites mastering

UNDERSTANDING BUILDING ACCOMPANYING

Groupe SQLI - - 24

Information system consulting SQLI helps computer departments improve performance of the company's Information System. To that end, SQLI offers a set of services necessary to the success of projects. SQLI consulting activity is based on the field experiment of its consultants. They offer an operational help based on their knowledge of the project management which they adapt to the company needs, in order to give the customers realistic solutions which combine technological expertise with operational pragmatism. Each consulting mission aims at identifying personalised solutions which integrate the constraints of the project with the information system components. SQLI consultants operate on the basis of a functional and sector-based expertise. Their knowledge of the job and their understanding of the stakes of the customer activity sector are the base of the consulting approach. SQLI consultants offer consulting in the three following fields: Technological SI consulting

By carrying a continuous watch policy, SQLI consultants assist the customer in their technology choices. They give advice on the architecture and technologies available in order to increase the performance and to consolidate the system with capitalizing the experience and optimising the investments at the same time. Assistance to set the architecture and the technology options: Analysis, choices and studies of scenarios, objectification of the choices. Architecture audits, technical audits: Carrying out of audits during the realisation phase or the takings phase in order to measure the performance of the customer’s system and applications. ( code quality, response time, etc.). Performance tests Adapt the customer’s technical architecture by being aware of its limits in order to anticipate its future evolution: SQLI performance tests aim at adapting the current and future needs of the customer’s activity with the real capacity of its architecture. SI decision consulting

Fully exploiting your data In a competitive and changing environment, it is important for the company to rely on accurate information allowing it to quickly take the good decisions at every level. The strategic exploitation of the data represents a complex process in front of the multiplication of information sources. Since 1995, SQLI has developed an advanced expertise and is accompanying its customers from the beginning to the end in the choice and the implementation of solutions which help make decisions. A both functional and operational approach Decision-making solutions are firstly based on a approach of functionality and job. In order to always bring a good answer, SQLI consultants focus on the users when they decide of the right expression and expectation approach. SQLI approach is based on a perfect appropriation of the customer functional stake. It includes: - an analysis of its demands in close collaboration with the General management, the Operational management and the computer management; - a help in the choice of architecture and solutions - the implementation of confirmed architecture The intervention sectors - Consolidation of the status and the management - Analytical CRM - Referential management - Guidance system: finance, HR, Marketing, purchases

Groupe SQLI - - 25

SI functional consulting Creation of a dialogue between technicians and users Beyond the technical feasibility, implementing a computer project demands the integration of mall the functional and organisation stakes of the company as well as the expectations of the users. This is the only condition which can allow the new technologies make the business easier and not more complicated. This is why SQLI accompany you through a operation mastering assistance. SQLI helps its customers define explicit and implicit needs for their users which correspond to the company’s cultural, technical and organisational knowledge. Organisation and modelling of the processes Dematerialising is the last step of a complex process. From clarification to formalisation, SQLI helps its customers through an approach which is totally focused on their partners and their activities. The conduct of change From the conception, SQLI integrates the customs, the culture and the resistance to changes of its partners trough a participative approach. SQLI has been carrying pedagogical and consciousness-raising actions as well as training actions to develop the project and make its integration easier. Marketing web ♦ SQLI helps in the conception of the customer e-marketing strategy and the positioning of its website. The

company puts up strong value-added services and animation plans in order to conquest and keep the customer’s targets.

E-business consulting

SQLI helps the functional departments offer new web services by making the company’s job processes evolve in the purpose of guaranteeing the return on investment of new web services. SQLI offers its customers: ♦ The creation of an e-commerce strategy consisting in e-commerce websites, optimisation of internet services

(e-mailing, multi channel dispositive system, services traffic analysis...); ♦ Complete services focused on the information communication to unite the company’s partners (company

portal, intranet...) and to strengthen the relation between the company and its targets (websites, institutional and events)

♦ Control of the key elements affecting the ergonomic performance of the trade applications: work station comfort and productivity, harmonisation of interfaces, observance of the W3C standards (HTML, accessibility…)…

♦ Know-how with respect to the tools and methods to be applied to control the users/customers targets and its competitive universe: competition watch, auditing, on line questionnaires, "focus groups", user tests…

Integration and projects

The integration of the new technologies into the customers’ information systems at the base of SQLI’s activities. The whole activity is based on a complete understanding of the customer’s activity, of its goals and burdens in order to help him implement reliable solutions which perfectly match the organisation and the values of its company. SQLI has a strict approach based on the anticipation of the customer’s needs in order to guarantee the continuity of the solutions. SQLI helps the project teams to materialise the recommendations made by SQLI consultants. 100% of its projects and missions rely on internet technologies. SQLI has a real ability to make projects succeed: with more than 50% of its turnover made without recourse, SQLI adopted a pragmatic project approach based on the CMM-I software quality model, that permits a commitment in time limits, budgets, and customer satisfaction in the projects carried out. The SQLI project teams can call on CMMI project management tools (IdeoProject), designed and developed by the SQLI teams in connection with integration of the CMMI model).

Groupe SQLI - - 26

Each integration project applies CMMI (Capability Maturity Integrated) standards. As a top-end software approach, CMMI brings a complete result guarantee on: - The collecting of explicit and implicit functional demands of the users - The respect of technical specifications during the whole project - The reliability of developed applications - The respect of costs and deadlines The types or know-how displayed by the project teams are the following: Project procedure adopted to the new technologies and centred around CMMI: management of requirements, certified project approach (CMMI, RUP, UML…), object/relational mapping (Castor, TopLink), risk analysis and management, internal project management tools (IdeoProject);

Quality of development by use of the market framework (Struts, JSF, Blue Martini…) or SQLI's framework (Bornéo, Interligo…)

Mastery of the main development environments: Java (J2EE, WebLogic, Websphere…), Microsoft (DNA, DotNet), Open Source tools (Php, Tomcat, Jonas…)

Integration of technical and applicative software solutions: EAI (Mercator, WebMethod, Seebeyond…), Portal (IBM WebSphere Portal, Oracle Portal, BEA WebLogic Portal, BEA Aqualogic User Interaction, Vignette Portal, Microsoft SharePoint…), Web Content Management (Microsoft Content Management Server , Tridion, Documentum…) ERP (SAP, Siebel, Peoplesoft…)

Decision-making solutions: ETL (Genio, Sunopsis, Datastage…), analytic reporting (Cognos, Business Object…)…

Creation and Web Design SQLI cares about the users’ satisfaction and about the conquest of new customers throughout an ergonomic interface, target-adapted contents and a differentiated brand image. SQLI offers its customers strong value-added web consulting in order to favour innovation, creativity and ROI through : a strategy of e-business positioning, an ergonomics performance consulting, a knowledge of the user, a generation of traffic as well as services of creation, conception, accompaniment and e-business training, marketing e-mail offer. In term of front office, that is the visible part of information systems and websites, SQLI has assessments and a know-how that helps to create intuitive user interfaces: ♦ Know-how with respect to the "usability" of the interfaces, emphasising intuitive navigation

(indicators…), speedy display (weight of the pages…), ergonomics of the functions (operating logic, effectiveness…), readability (organisation of the pages…), uniformity and stability (standards accounting…)