© Fasano Associates October 31, 20081 Securitization of LS Cash Flows Michael Fasano Founder &...

33

© Fasano Associates October 31, 2008 1 Securitization of LS Cash Flows Michael Fasano Founder & President Fasano Associates Securitization of Life Settlement Cash Flows

-

Upload

cecil-hudson -

Category

Documents

-

view

214 -

download

1

Transcript of © Fasano Associates October 31, 20081 Securitization of LS Cash Flows Michael Fasano Founder &...

© Fasano Associates October 31, 2008 1 Securitization of LS Cash Flows

Michael Fasano Founder & PresidentFasano Associates

Securitization of Life Settlement Cash Flows

© Fasano Associates October 31, 2008 2 Securitization of LS Cash Flows

• Seller realizes immediate value on the sale.

• Buyer pays up front lump sum, followed by periodic premium payments to keep policy in force.

• Buyer receives the policy Death Benefit at the Insured’s death.

Definition: A Life Settlement is the sale of a life insurance policy in the secondary market.

© Fasano Associates October 31, 2008 3 Securitization of LS Cash Flows

Economic Basis for Life Settlement

• U.S. Insurance Regulations do not allow differentiation in

cash surrender values based on health of Insured

• Insurance contract guarantees cash surrender values based

on conservative (low) interest rate assumptions

Market value of life insurance contract for older,

impaired life is greater than guaranteed cash surrender

value

• Reduction in U.S. estate taxes has created added financial

incentive to liquidate life insurance contracts

© Fasano Associates October 31, 2008 4 Securitization of LS Cash Flows

Characteristics of U.S. Life Settlement Market

• Age 65 and older; Average age approximately 77

• 2/3rds of policies are male; 1/3 female

• Average face amount between $1 million and $2 million; significantly higher for premium financed policies

• Premium financed component of market has been facilitated by unrealistically short life expectancy estimates available in market. Policies issued, financed during 2-year contestability period, then resold.

• Realistic expected portfolio duration in the range of 12 years

© Fasano Associates October 31, 2008 5 Securitization of LS Cash Flows

Cash Flows

• For a portfolio of Life Settlements, significant cash outflow in the first year, due to acquisition cost

• Then increasing cash flow through portfolio duration

• Then decreasing cash flow as portfolio winds down

• In some scenarios cash flow can be negative in first couple of years

© Fasano Associates October 31, 2008 6 Securitization of LS Cash Flows

(30,000,000)

(25,000,000)

(20,000,000)

(15,000,000)

(10,000,000)

(5,000,000)

0

5,000,000

10,000,000

15,000,000

20,000,000

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

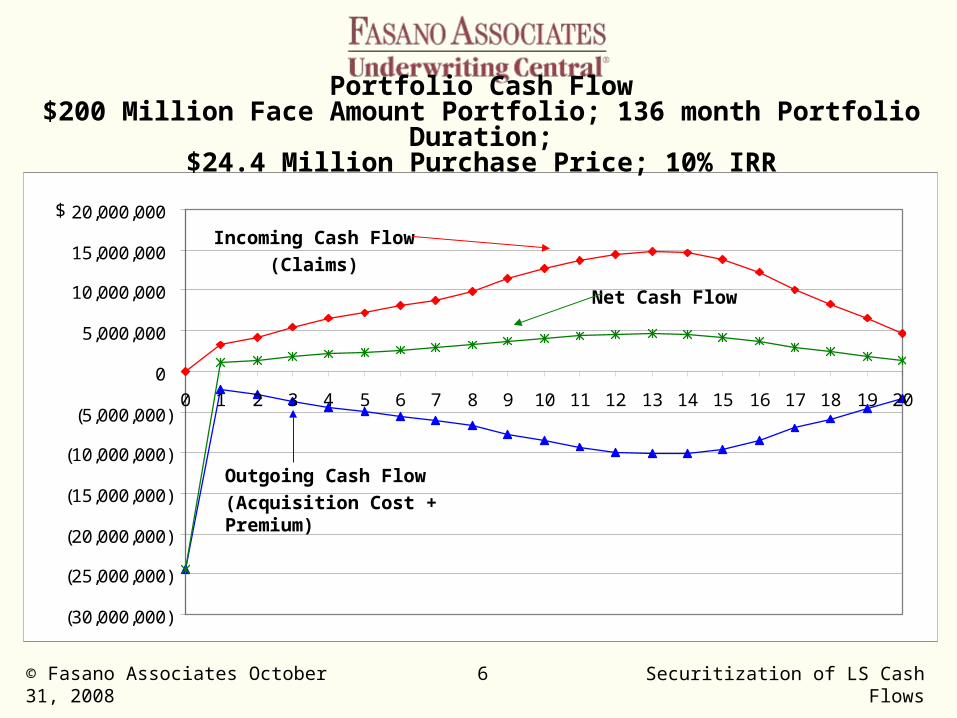

Portfolio Cash Flow$200 Million Face Amount Portfolio; 136 month Portfolio Duration;

$24.4 Million Purchase Price; 10% IRR

Outgoing Cash Flow

(Acquisition Cost + Premium)

Incoming Cash Flow

(Claims)

Net Cash Flow

$

© Fasano Associates October 31, 2008 7 Securitization of LS Cash Flows

(200,000,000)

(150,000,000)

(100,000,000)

(50,000,000)

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

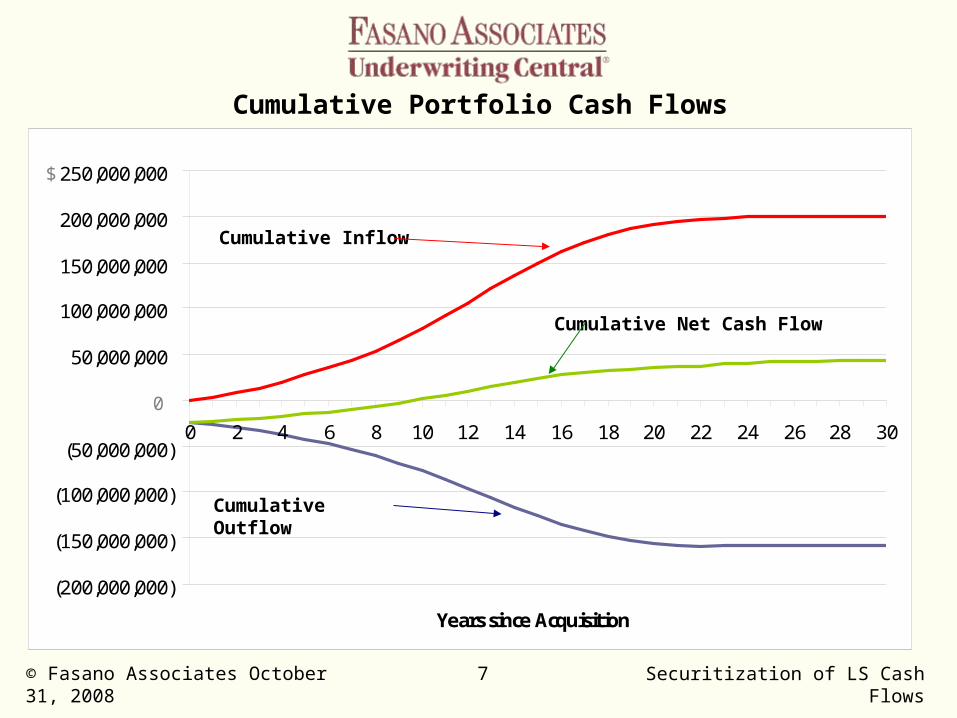

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30

Years since Acquisition

Cumulative Portfolio Cash Flows

Cumulative Outflow

Cumulative Inflow

Cumulative Net Cash Flow

0

$

© Fasano Associates October 31, 2008 8 Securitization of LS Cash Flows

Possible Portfolio Requirements

• Short Term Line of Credit

• Stop Loss Longevity Protection

• Credit Enhancement

© Fasano Associates October 31, 2008 9 Securitization of LS Cash Flows

Current Investors – Primary Life Settlement Market• AIG

• Hedge funds

• Bond Funds

• Some Pension Funds

• Investment and Commercial Banks have served mostly as intermediaries

• Most European interest has been from Germany; however, UK, Switzerland, Sweden and other countries have participated. Interest from Japan, Korea and Australia.

© Fasano Associates October 31, 2008 10 Securitization of LS Cash Flows

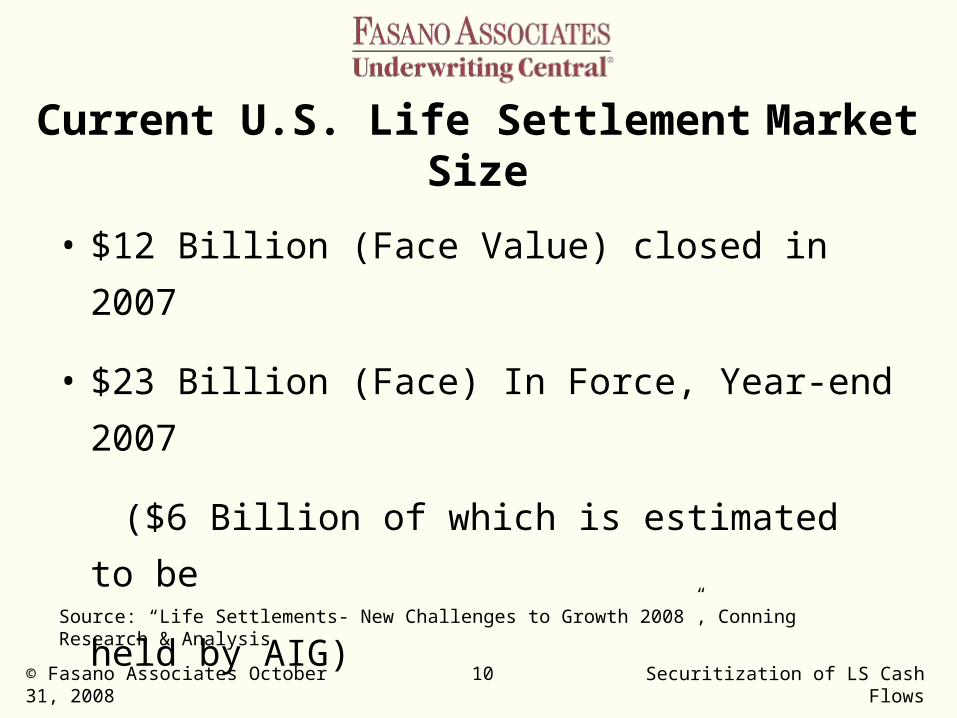

Current U.S. Life Settlement Market Size

• $12 Billion (Face Value) closed in 2007

• $23 Billion (Face) In Force, Year-end 2007

($6 Billion of which is estimated to be

held by AIG)

Source: “Life Settlements- New Challenges to Growth 2008”, Conning Research & Analysis

© Fasano Associates October 31, 2008 11 Securitization of LS Cash Flows

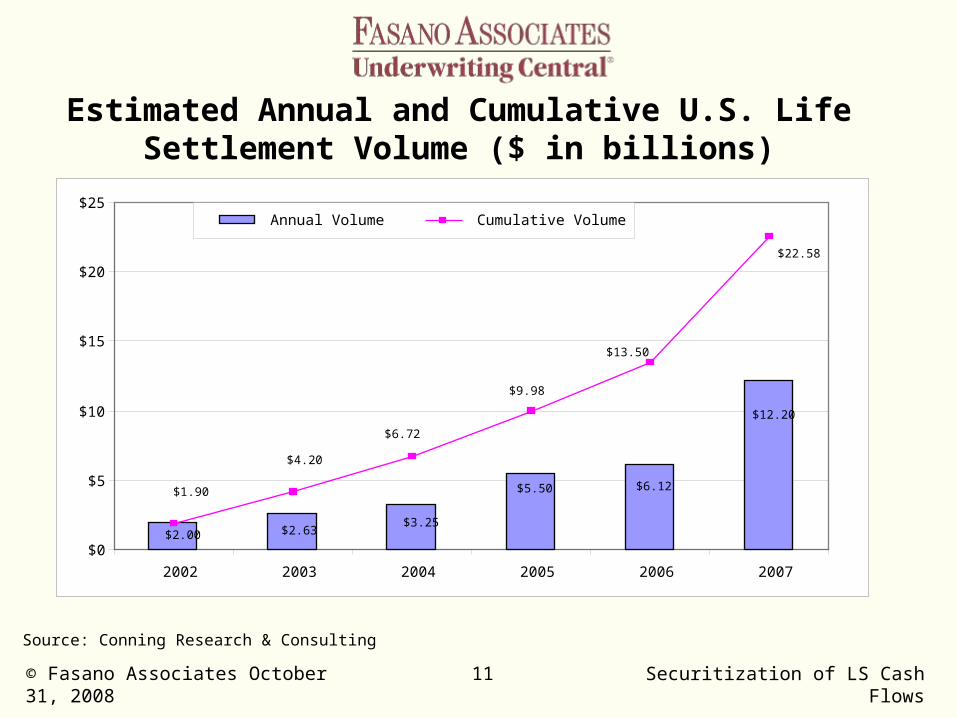

Estimated Annual and Cumulative U.S. Life Settlement Volume ($ in billions)

Source: Conning Research & Consulting

$12.20

$2.00 $2.63$3.25

$5.50 $6.12

$22.58

$13.50

$9.98

$6.72

$4.20

$1.90

$0

$5

$10

$15

$20

$25

2002 2003 2004 2005 2006 2007

Annual Volume Cumulative Volume

© Fasano Associates October 31, 2008 12 Securitization of LS Cash Flows

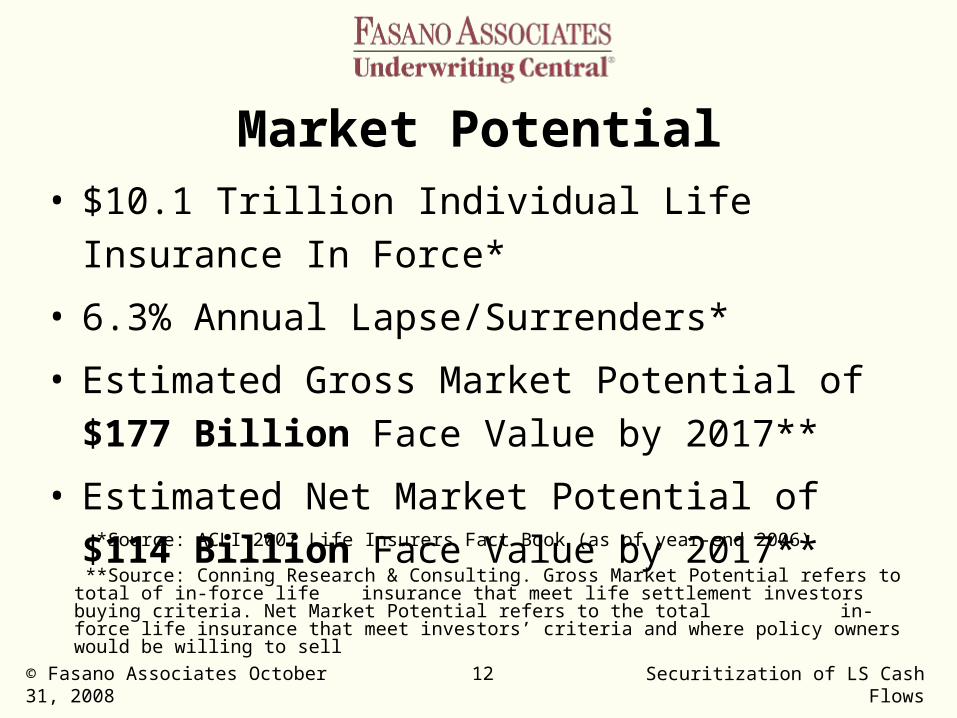

Market Potential• $10.1 Trillion Individual Life Insurance In Force*

• 6.3% Annual Lapse/Surrenders*

• Estimated Gross Market Potential of $177 Billion

Face Value by 2017**

• Estimated Net Market Potential of $114 Billion

Face Value by 2017** *Source: ACLI 2007 Life Insurers Fact Book (as of year-end 2006)

**Source: Conning Research & Consulting. Gross Market Potential refers to total of in-force life insurance that meet life settlement investors buying criteria. Net Market Potential refers to the

total in-force life insurance that meet investors’ criteria and where policy owners would be willing to sell

© Fasano Associates October 31, 2008 13 Securitization of LS Cash Flows

Market Impediments• Resistance from life insurance industry, ostensibly due to

concerns over manufactured transactions (Speculator Originated purchase/sales). This has resulted in restrictive regulatory proposals; and also has limited sourcing of policies.

• Excessive intermediary fees from brokers and portfolio aggregators, which can average more than 20% gross proceeds*

• Misalignment of interests between intermediaries purchasing policies (Providers) and funding sources shopping for short life expectancy estimates and irrational pricing.

• The absence of meaningful longevity risk protection*Conning Research has estimated Agent, Broker and Provider Fees to be 9.5% of Face Amount

© Fasano Associates October 31, 2008 14 Securitization of LS Cash Flows

History of Life Settlement Securitizations• Not much to speak of

• January 2004: Tarrytown Second, LLC $63 Million Class A Life Settlement Securitization backed by $195 million face value of life insurance policies

• April 2004: Legacy Benefits $70 Million Life Settlement Securitization; Moody’s Rated: $61.5 Million Class A Notes, rated A1; $8.5 Million Class B Notes, rated Baa2

• Ritchie Capital Deal would have $1.2 Billion Face Amount ($340 Million Market Value). Moody’s rated securitization (A3 Rating on Senior Securities). Rating pulled and deal fell through after packager of pool, Coventry, sued by New York Attorney General

• Most securitizations have been small and private

© Fasano Associates October 31, 2008 15 Securitization of LS Cash Flows

Limits to Securitization

• Market Impediments to Underlying Life Settlement Market

• Lack of Longevity Risk Protection

• Premature to consider tranching of cash flows; We need to demonstrate basic ability to pool assets and resell as securitized interests

© Fasano Associates October 31, 2008 16 Securitization of LS Cash Flows

Potential from Securitization• Substantial and potentially transformative

• Current investors seek equity returns, 10% or greater

• Life Settlements currently seen as a niche, uncorrelated asset

• Substantial potential as an alternative fixed income investment

• This will lower return expectation significantly and correlate with opening of market to pension funds, endowments and other logical long term investors

• If so, Conning market projections might be conservative

© Fasano Associates October 31, 2008 17 Securitization of LS Cash Flows

Similar Potential to Mortgage Backed Securities

• Pre-1970’s mortgage investing was localized in thrift institutions

• Securitization opened mortgage market to wide range of institutional investors

• Similar potential for Life Settlements

• Prepayment risk was significant consideration in early MBS transactions. Longevity risk is the primary risk for life settlement transactions.

© Fasano Associates October 31, 2008 18 Securitization of LS Cash Flows

• Longevity Risk

• Wrong Mortality Tables

• Credit Risk needs to be dealt with, but a

lesser consideration

Real Impediments to Life Settlement Securitization

© Fasano Associates October 31, 2008 19 Securitization of LS Cash Flows

Longevity Risk

• Life Expectancy estimates have been

inconsistent and often wrong

• A.M. Best Study of 909 life portfolio underwritten

by the 3 major Life Expectancy Underwriters

– Average spread of 8 months between longest and

second longest L.E. Provider

– Average spread of 24 months between longest and

shortest L.E. Provider

© Fasano Associates October 31, 2008 20 Securitization of LS Cash Flows

• Fasano has consistently been the longest of the L.E. Providers

• Fasano Actual to Expected accuracy has been established at 96%, suggesting an A/E Ratio of 90% for the second longest, and 79% for the shortest LE Provider

• Yet because of misalignment of interest between the portfolio aggregators and the funders, many portfolios have been assembled based on the shorter, less accurate life expectancy estimates

• Market recently shocked when the shortest of L.E. Providers announced plans to extend life expectancies by 20 to 25%.

• This clearly is a developing market

© Fasano Associates October 31, 2008 21 Securitization of LS Cash Flows

Ramifications for IRR

• Portfolio priced at 12.4% based on the shortest L.E. Underwriter would =>

– IRR of 8.3% based on second longest L.E.

Underwriter;

– IRR of 6.5% based on longest of L.E.

Underwriters

Source: A.M. Best

© Fasano Associates October 31, 2008 22 Securitization of LS Cash Flows

Solutions to Longevity Risk• First Step is for Life Expectancy Underwriters to get

better and for Market to get smarter

• Encouraging Developments: Recent announcement of

shortest of L.E. Underwriters to extend LE’s by 20 to

25%; follow-up announcement of second longest to

extend by estimated 5 to 10%

• Investment Banks have promoted synthetic transactions

to hedge longevity risk

• More traditional stop loss product is more appealing

© Fasano Associates October 31, 2008 23 Securitization of LS Cash Flows

Traditional Longevity Risk Products• Lloyd’s (Goshawk Syndicate) developed L.E. + 2 product

in the 1990’s: Would purchase life settled or viaticated policy back if person lived 2 years beyond the 85th percentile. Premium charged of 4% of face value

• Product failed due to:

– Anti-selection (Investor could choose which policies to buy cover for.)

– Poor control of underwriting function

– No life settlement model will work with wrong LE estimate

© Fasano Associates October 31, 2008 24 Securitization of LS Cash Flows

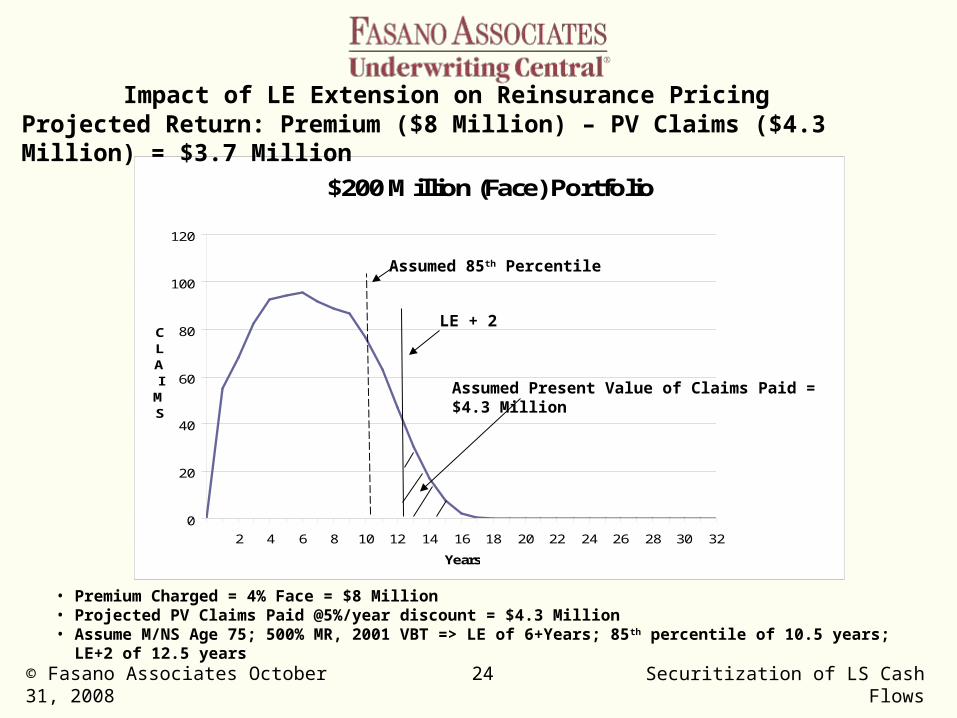

$200 Million (Face) Portfolio

0

20

40

60

80

100

120

2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32

Years

CLAI

MS

Impact of LE Extension on Reinsurance Pricing

Assumed Present Value of Claims Paid = $4.3 Million

LE + 2

Assumed 85th Percentile

• Premium Charged = 4% Face = $8 Million• Projected PV Claims Paid @5%/year discount = $4.3 Million• Assume M/NS Age 75; 500% MR, 2001 VBT => LE of 6+Years; 85 th percentile of 10.5 years; LE+2 of 12.5 years

Projected Return: Premium ($8 Million) – PV Claims ($4.3 Million) = $3.7 Million

© Fasano Associates October 31, 2008 25 Securitization of LS Cash Flows

0

20

40

60

80

100

120

2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32

Years

CLAI

MS

PV of Actual Claims Paid = $38.7 Million

Assumed LE + 2

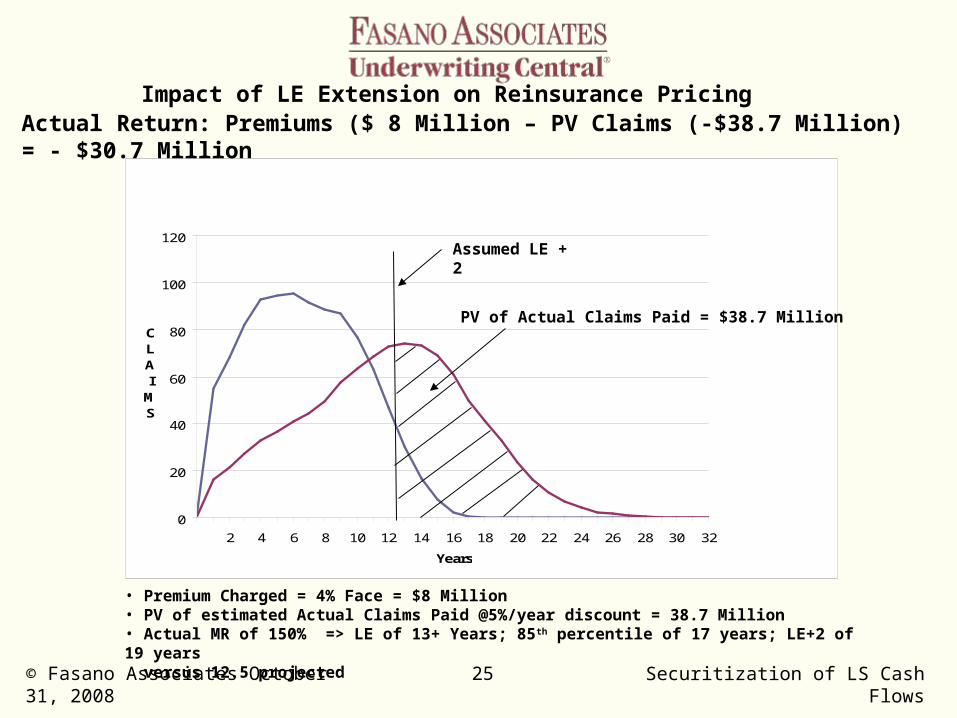

• Premium Charged = 4% Face = $8 Million• PV of estimated Actual Claims Paid @5%/year discount = 38.7 Million• Actual MR of 150% => LE of 13+ Years; 85th percentile of 17 years; LE+2 of 19 years versus 12.5 projected

Impact of LE Extension on Reinsurance PricingActual Return: Premiums ($ 8 Million – PV Claims (-$38.7 Million) = - $30.7 Million

© Fasano Associates October 31, 2008 26 Securitization of LS Cash Flows

FAIRE• Joint venture between Fasano Associates, U.S.

underwriting firm, and Augur Capital, a German investment manager of life insurance and life settlement assets

• Will offer both individual and portfolio extension risk products, priced off of Fasano Life Expectancy estimates

• Preliminary interest strong; current market unsettled

© Fasano Associates October 31, 2008 27 Securitization of LS Cash Flows

Impediments to Securitization: Mortality Tables

• Shape of the Mortality Curve is important for modeling cash flows, although not as important as getting the midpoint life expectancy estimate right

• Industry has used 2001 VBT and now 2008 VBT Tables: Both based on Life Insurance, not Life Settlement experience.

• VBT 2001 and 2008 exclude impaired lives, assume too long of a select period and don’t adjust for Mortality Rating

© Fasano Associates October 31, 2008 28 Securitization of LS Cash Flows

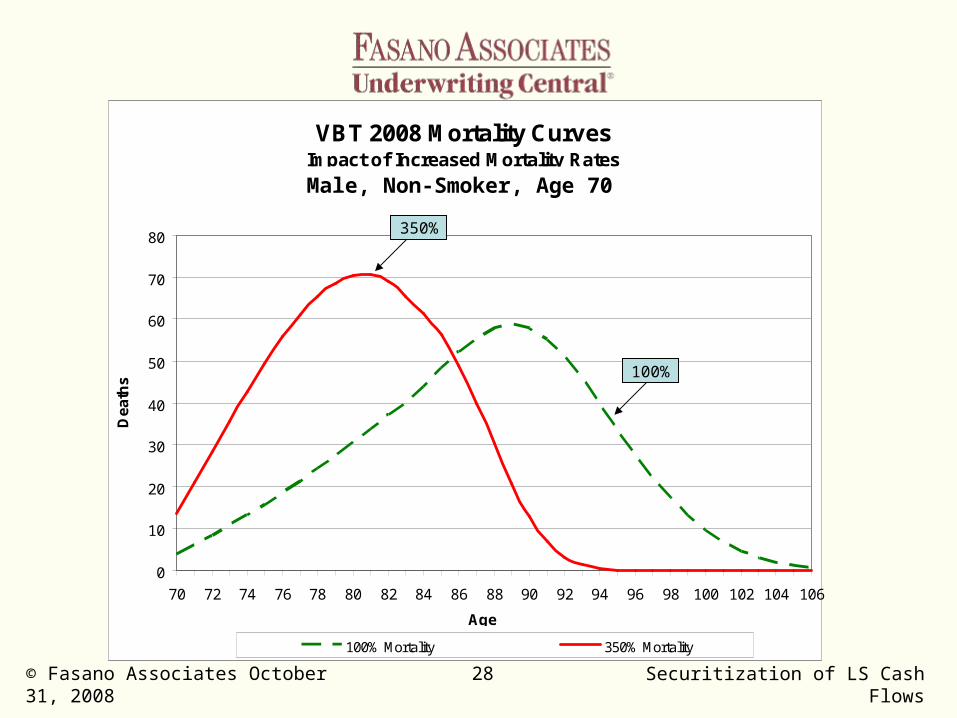

VBT 2008 Mortality CurvesImpact of Increased Mortality Rates

0

10

20

30

40

50

60

70

80

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 100 102 104 106

De

ath

s

100% Mortality 350% Mortality

Age

350%

100%

Male, Non-Smoker, Age 70

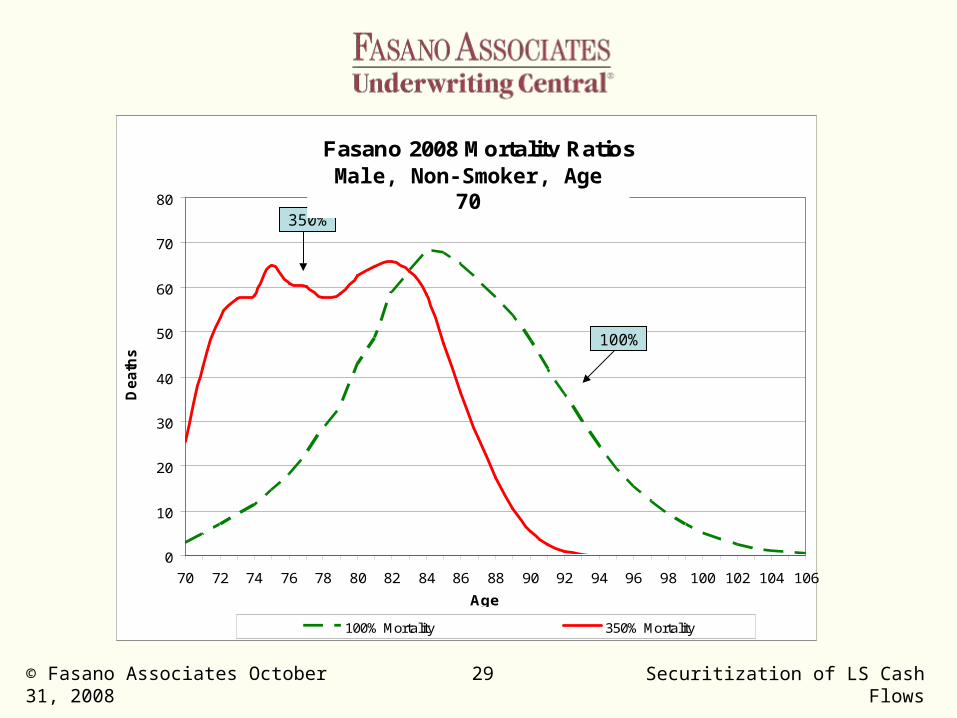

© Fasano Associates October 31, 2008 29 Securitization of LS Cash Flows

Fasano 2008 Mortality Ratios

0

10

20

30

40

50

60

70

80

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 100 102 104 106

De

ath

s

100% Mortality 350% Mortality

Age

350%

100%

Male, Non-Smoker, Age 70

© Fasano Associates October 31, 2008 30 Securitization of LS Cash Flows

Why Would The Mortality Curve Flatten With Increased Mortality?

• Nature of impairments are different:

- Coronary Artery Disease versus Congestive Heart Failure

- Low Risk versus High Risk Cancer

• Most impairments are slowly progressive

• Severe impairments are not

© Fasano Associates October 31, 2008 31 Securitization of LS Cash Flows

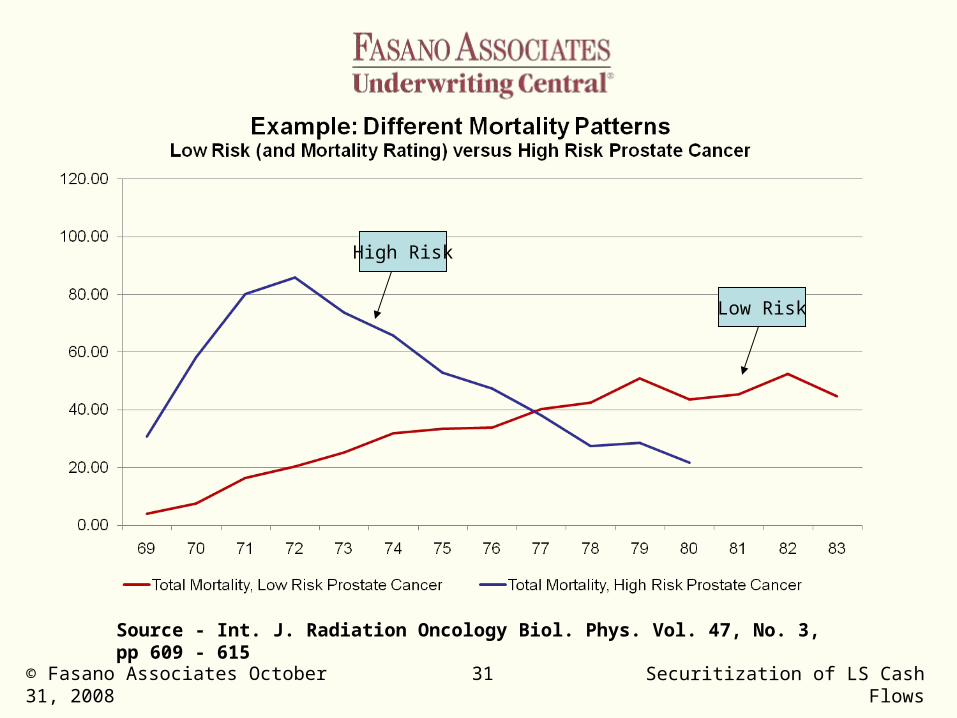

Source - Int. J. Radiation Oncology Biol. Phys. Vol. 47, No. 3, pp 609 - 615

High Risk

Low Risk

© Fasano Associates October 31, 2008 32 Securitization of LS Cash Flows

Prospects for Life Settlement Securitizations

• More accurate and consistent underwriting

PLUS

• Extension risk products

PLUS

• Huge underlying U.S. Life Insurance Market

Substantial Market for Life Settlement

Securitizations

© Fasano Associates October 31, 2008 33 Securitization of LS Cash Flows

5 November 2008

Washington, DC

Michael FasanoFasano Associates1201 15th Street, NW – Suite 250Washington, DC 20005202-457-8188202-457-8198 (fax)[email protected]

33

Fasano Associates 5th Annual Life Settlement Conference