* Corporations - Henderson - Fall 2008

35

I. What is a Corporation? ..................................................................................................................... 1 II. Promoters ........................................................................................................................................ 4 III. Limited Liability ............................................................................................................................... 7 IV. Business Judgment Rule ................................................................................................................ 10 V. Duty of Care ................................................................................................................................... 12 VI. Duty of Loyalty .............................................................................................................................. 15 A. Interested Party Transactions ..................................................................................................... 15 B. Corporate Opportunities ............................................................................................................. 17 C. Controlling Shareholders ............................................................................................................ 18 D. Executive Compensation ............................................................................................................ 19 VII. Shareholder Litigation .................................................................................................................. 22 VIII. Control Issues ............................................................................................................................. 29 A. Shareholder Voting ..................................................................................................................... 29 B. Precatory Proposals .................................................................................................................... 31 C. Shareholder Inspection Rights .................................................................................................... 32 D. Control in Closely Held Firms ...................................................................................................... 32 E. Duties to Shareholders ................................................................................................................ 34 F. Abuse of Control ......................................................................................................................... 34 G. Transfer of Control ..................................................................................................................... 34 I. What is a Corporation? One definition - The most common form of business organization Chartered by state Given many legal rights as entity separate from its owners - Characterized by Limited liability of its owners Issuance of shares of easily transferrable stock Existence as a going concern - Process of becoming corporation is called incorporation Gives company separate legal standing from its owners Protects owners from being personally liable if compan y is sued (limited liability) Provides companies w more flexible way to manage - Together, they make corporation uniquely attractive For organizing productive activity - But they also generate tensions

-

Upload

michael-fielkow -

Category

Documents

-

view

217 -

download

0

Transcript of * Corporations - Henderson - Fall 2008

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 1/35

. What is a Corporation? ...................................................................................................................

I. Promoters ......................................................................................................................................

II. Limited Liability .............................................................................................................................

V. Business Judgment Rule ................................................................................................................

V. Duty of Care ...................................................................................................................................

VI. Duty of Loyalty ..............................................................................................................................A. Interested Party Transactions ....................................................................................................

B. Corporate Opportunities .............................................................................................................

C. Controlling Shareholders ............................................................................................................

D. Executive Compensation ............................................................................................................

VII. Shareholder Litigation ..................................................................................................................

VIII. Control Issues .............................................................................................................................

A. Shareholder Voting .....................................................................................................................

B. Precatory Proposals ....................................................................................................................

C. Shareholder Inspection Rights ....................................................................................................

D. Control in Closely Held Firms .....................................................................................................

E. Duties to Shareholders ................................................................................................................

F. Abuse of Control .........................................................................................................................

G. Transfer of Control .....................................................................................................................

. What is a Corporation?

One definition

- The most common form of business organization

Chartered by state

Given many legal rights as entity separate from its owners

- Characterized by

Limited liability of its owners Issuance of shares of easily transferrable stock

Existence as a going concern

- Process of becoming corporation is called incorporation

Gives company separate legal standing from its owners

Protects owners from being personally liable if company is sued (limited liability)

Provides companies w more flexible way to manage

- Together, they make corporation uniquely attractive

For organizing productive activity

- But they also generate tensions

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 2/35

That lend a distinctively corporation character to agency problems

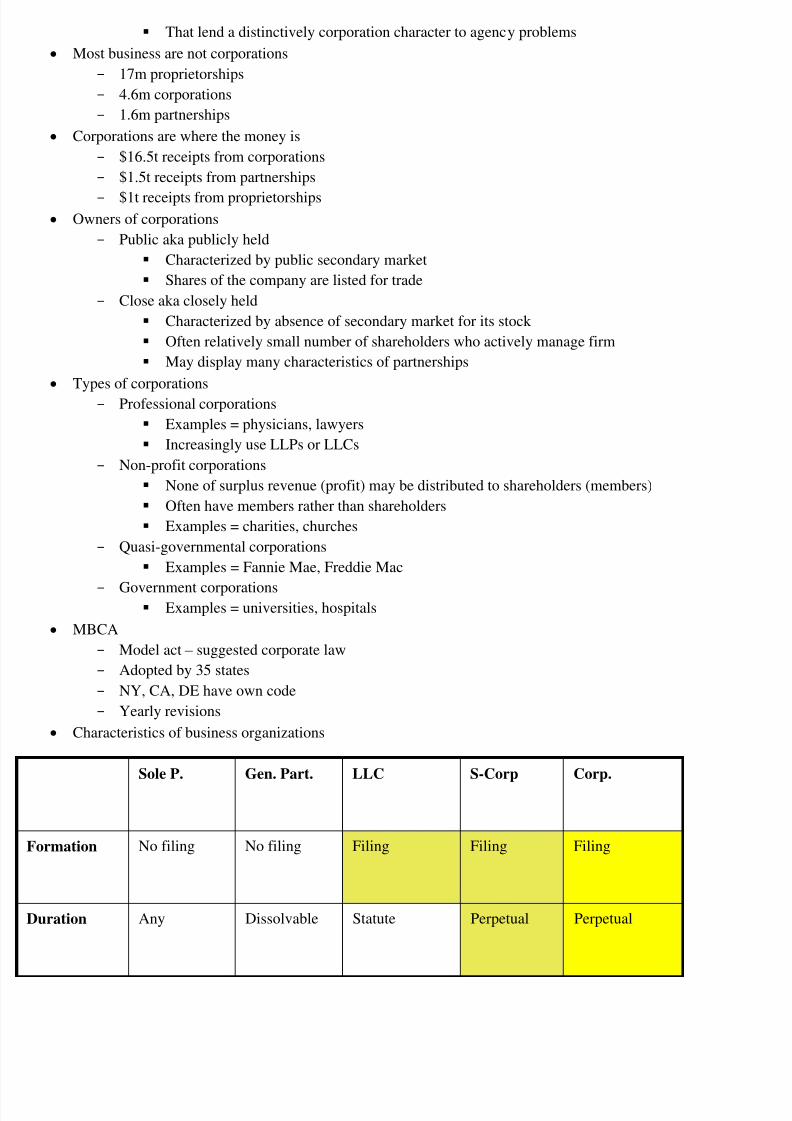

Most business are not corporations

- 17m proprietorships

- 4.6m corporations

- 1.6m partnerships

Corporations are where the money is

- $16.5t receipts from corporations

- $1.5t receipts from partnerships

- $1t receipts from proprietorships Owners of corporations

- Public aka publicly held

Characterized by public secondary market

Shares of the company are listed for trade

- Close aka closely held

Characterized by absence of secondary market for its stock

Often relatively small number of shareholders who actively manage firm

May display many characteristics of partnerships

Types of corporations

- Professional corporations

Examples = physicians, lawyers

Increasingly use LLPs or LLCs

- Non-profit corporations

None of surplus revenue (profit) may be distributed to shareholders (members)

Often have members rather than shareholders

Examples = charities, churches

- Quasi-governmental corporations

Examples = Fannie Mae, Freddie Mac

- Government corporations Examples = universities, hospitals

MBCA

- Model act – suggested corporate law

- Adopted by 35 states

- NY, CA, DE have own code

- Yearly revisions

Characteristics of business organizations

Sole P. Gen. Part. LLC S-Corp Corp.

Formation No filing No filing Filing Filing Filing

Duration Any Dissolvable Statute Perpetual Perpetual

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 3/35

Liability Unlimited Unlimited Limited Limited Limited

Simplicity Very Very Formal Formal Very formal

Management Any Partners

control

Operating

agreement

Board Board

Taxation Personal Pass through Pass through Pass through Corporate tax

Cost of form. None None Fee Fee Fee

Raising

quity

Personal From partners Can sell

interests

Stock Stock

Transferable? No No Possibly Yes, with

consent

Freely

Six core characteristics of corporations

- Formal creation (DGCL §101(a))

- Legal personality (DGCL §106)

Body corporation

Sue or be sued

Shield assets of entity form creditors of owners

- Limited liability (MBCA §6.22(b))

Shareholder not personally liable for acts of debts of corp

Unless through own acts/conduct becomes liable

- Separation of ownership & control (DGCL §141)

Managed under direction of board of directors

- Transferable shares (DGCL §122)

Issue notes, bonds, other obligations

- Infinite duration (DGCL §122(1)) Benefits of corporation form

- Eliminates messy problems from personal liability

Reduces need to monitor agents (managers)

Enlists creditors to monitor managers (creditors bear downside)

Reduces need to monitor other shareholders

Makes shares fungible – increases liquidity, lowers cost of capital

Facilitates diversification – without LL, minimize exposure by holding one corp only

- Allows investors to enter and exit the firm – just need to buy or sell shares

Permits takeovers – disciplines management

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 4/35

Allows exit without disrupting business

- Prevents minority investors from trying to hold up firm by threatening to dissolve it

- Makes it easier for 3rd

parties who contract w firm to know who they are dealing with

- Improves decision making through command and control structure

Choosing a state for incorporation

- Paul v. Virginia (US 1869)

State may not exclude foreign corporation engaged in interstate commerce

- Delaware’s dominance

More than 300k companies incorporated in DE 60% of Fortune 500

50% of NYSE companies

Enabling statutes

Standard form contract to reduce bargaining costs

Transaction costs lower for default rules

No minimum capital requirements

Only need one incorporator

Corporation can be incorporator

Favorable franchise tax in comparison to other states

Favorable taxation for companies doing business outside of DE

No corporation income tax

No sales tax, personal property tax, or intangible property tax for corps

No taxation on shares of stock held by non-residents

No inheritance tax upon non-residents holders

Corporation may keep all books/records outside of DE

May have principal place of business/address outside of DE

Highly competent judiciary in corporate law

Extensive and detailed case law on the subject

Federal law

- Disclosure & procedure

Substantive law can be “secreted in interstices of procedure”

More and more substance, though

- Securities laws

Blue Sky Laws

Merit review

Securities Act of 1933, Exchange Act of 1934

Disclosure and fraud

- Sarbanes-Oxley- Creeping federalization of corporate law

I. Promoters

Incorporators (§101)

- Any person – singly or jointly w others – may incorporate or organize a corporation

- By filing a certificate of incorporation with the Division of Corporations in Department of State

Power of incorporators (§107)

- Incorporator will manage affairs until directors are elected at first annual meeting

If ppl who will serve as directors have not been named yet

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 5/35

- May do whatever necessary and proper to perfect organization of corporation

Including adoption of original bylaws or corporation and election of directors

Promoters and corporate entities

- Third-party sales

A & B are strangers

A buys Blackacre for $125k and quickly sells to B for $200k

Does B have cause of action?

Potential cause of action for fraud

If B asked A how much he paid and he said $200k - Principal-agent sales #1

A buys Blackacre for $125k

A if B’s agent for land investments

B doesn’t know about A’s transaction and inquires about Blackacre

B hires A to represent her in purchasing Blackacre

A sells land to B for $200k

Does B have cause of action?

Agent who makes a profit in connection w transactions conducted by him or on behalf

principal is under duty to give such profit to the principal

- Principal-agent sales #2

Same facts as above, but buyer is corporation wholly owned by B

What result?

Corp has same rights as B in above

B has no rights

- Promoter sales

A & B are strangers

A buys Blackacre for $125k and contemplates selling to B for use in residential development

Option 1

A creates X Corp (so A is promoter) X sells all shares to B for $200k and B becomes president

A sells Blackacre to X for $200k

Board (made up of B’s family) approves transaction

What result?

o A is fiduciary of X so X can recover

o A has legal obligations to refrain from dealing w corporation at arm’s length

Option 2

A sells Blackacre to B for $200k

B forms X Corp. B contributes Blackacre to X corp in exchange for all shares

What result?

o Neither B nor X has cause of action unless agent of B

o Form > Substance

Option 3

A forms X Corp. and contributes $200k in cash for all shares of stock

A appointed president and director of X – A’s husband and son are other two directors

A sells Blackacre to X for $200k – transaction approved by board

A then sells all shares of X to B for $200k

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 6/35

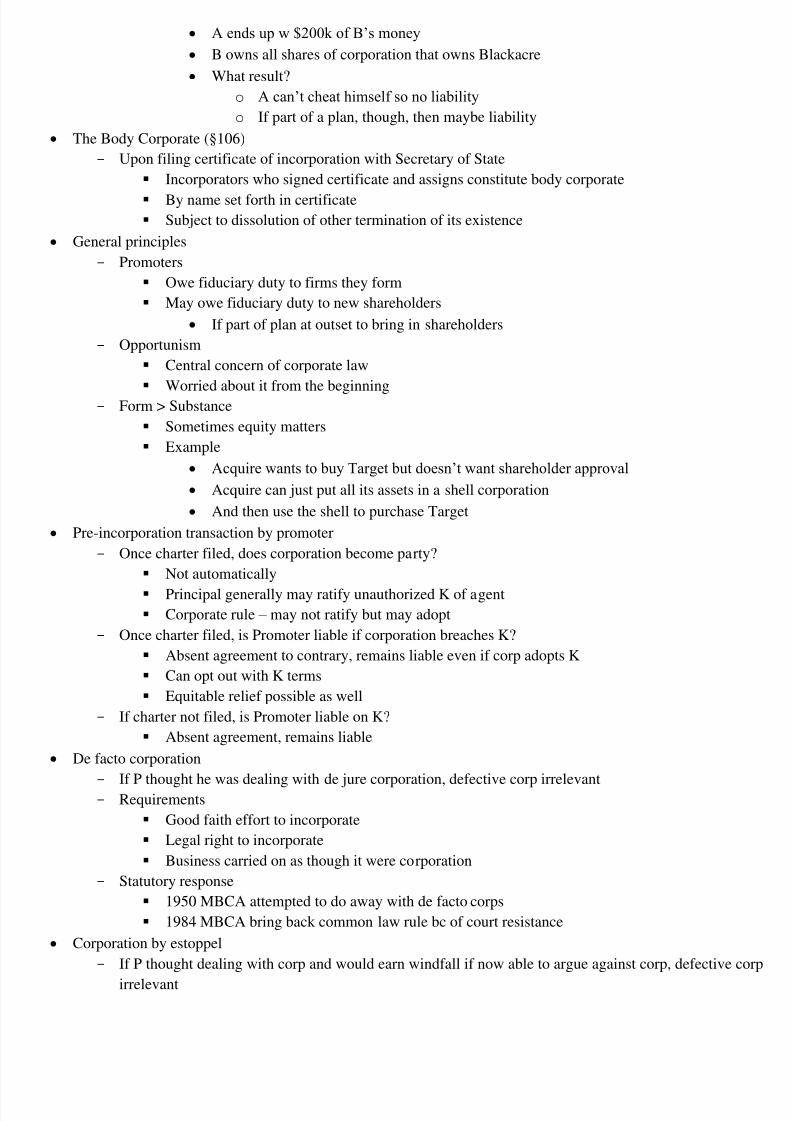

A ends up w $200k of B’s money

B owns all shares of corporation that owns Blackacre

What result?

o A can’t cheat himself so no liability

o If part of a plan, though, then maybe liability

The Body Corporate (§106)

- Upon filing certificate of incorporation with Secretary of State

Incorporators who signed certificate and assigns constitute body corporate

By name set forth in certificate Subject to dissolution of other termination of its existence

General principles

- Promoters

Owe fiduciary duty to firms they form

May owe fiduciary duty to new shareholders

If part of plan at outset to bring in shareholders

- Opportunism

Central concern of corporate law

Worried about it from the beginning

- Form > Substance

Sometimes equity matters

Example

Acquire wants to buy Target but doesn’t want shareholder approval

Acquire can just put all its assets in a shell corporation

And then use the shell to purchase Target

Pre-incorporation transaction by promoter

- Once charter filed, does corporation become party?

Not automatically

Principal generally may ratify unauthorized K of agent

Corporate rule – may not ratify but may adopt

- Once charter filed, is Promoter liable if corporation breaches K?

Absent agreement to contrary, remains liable even if corp adopts K

Can opt out with K terms

Equitable relief possible as well

- If charter not filed, is Promoter liable on K?

Absent agreement, remains liable

De facto corporation

- If P thought he was dealing with de jure corporation, defective corp irrelevant

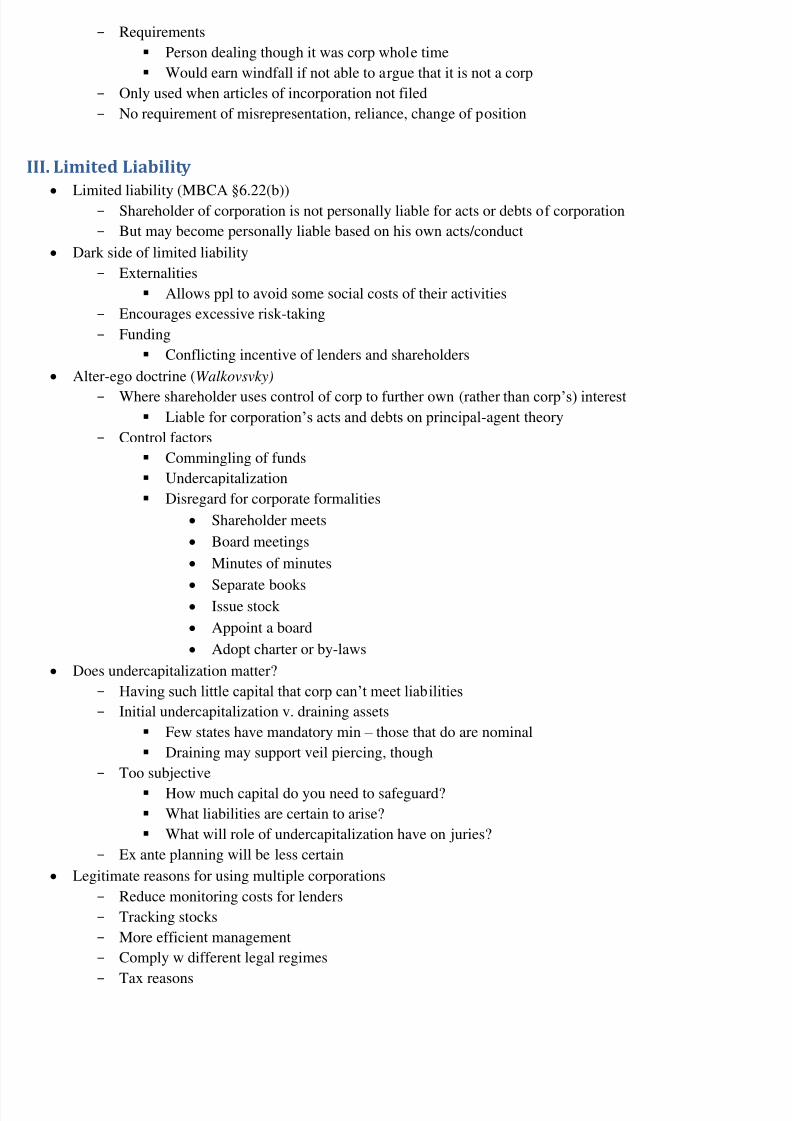

- Requirements

Good faith effort to incorporate

Legal right to incorporate

Business carried on as though it were corporation

- Statutory response

1950 MBCA attempted to do away with de facto corps

1984 MBCA bring back common law rule bc of court resistance

Corporation by estoppel

- If P thought dealing with corp and would earn windfall if now able to argue against corp, defective c

irrelevant

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 7/35

- Requirements

Person dealing though it was corp whole time

Would earn windfall if not able to argue that it is not a corp

- Only used when articles of incorporation not filed

- No requirement of misrepresentation, reliance, change of position

II. Limited Liability

Limited liability (MBCA §6.22(b))

- Shareholder of corporation is not personally liable for acts or debts of corporation

- But may become personally liable based on his own acts/conduct

Dark side of limited liability

- Externalities

Allows ppl to avoid some social costs of their activities

- Encourages excessive risk-taking

- Funding

Conflicting incentive of lenders and shareholders

Alter-ego doctrine (Walkovsvky)

- Where shareholder uses control of corp to further own (rather than corp’s) interest Liable for corporation’s acts and debts on principal-agent theory

- Control factors

Commingling of funds

Undercapitalization

Disregard for corporate formalities

Shareholder meets

Board meetings

Minutes of minutes

Separate books Issue stock

Appoint a board

Adopt charter or by-laws

Does undercapitalization matter?

- Having such little capital that corp can’t meet liabilities

- Initial undercapitalization v. draining assets

Few states have mandatory min – those that do are nominal

Draining may support veil piercing, though

- Too subjective

How much capital do you need to safeguard?

What liabilities are certain to arise?

What will role of undercapitalization have on juries?

- Ex ante planning will be less certain

Legitimate reasons for using multiple corporations

- Reduce monitoring costs for lenders

- Tracking stocks

- More efficient management

- Comply w different legal regimes

- Tax reasons

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 8/35

Generic Questions

- Is it improper to incorporate your business for purpose of avoiding personal liability?

NO

- Is it improper to split single business into multiple to limit liability of each part?

NO

Veil piercing

- Possible legal rules

Misused

Unfair result Undercapitalization

Controlling/dominating shareholders

Small firms (closely held)

- Does veil piercing induce internalization of risks?

Doesn’t have to do with policy questions at issue

Doesn’t help sort out which risks should be internalized v. externalized

Doesn’t promote populist notions of economic democracy

- Court’s decline to pierce in 90% of cases where formalities are observed

Special rule for small firms?

- Shareholder characteristics

Few in number

Actively involved in firm management

Not well-diversified

- Creditor characteristics

Few in number

Low enforcement & monitoring costs

Small equity cushion

- Line-drawing problem

Where would limited liability kick in How many shareholders

- Investor choice

Off the rack rules – one size does not fit all

- Penalty default

Force parties to bargain

Avoiding liability

- Personal liability (of you)

Just respect corporate formalities

Take out minimum insurance

- Enterprise liability (of your other corps)

Need separate books and bank accounts for each corp

Careful accounting for supplies, etc.

Policy options – what should we do?

- Raise mandatory insurance levels

- Require tort-prone companies to post large bond

- Let loss fall on victim

- Pierce corporate veil (pro-rata liability)

Ex ante bargaining re limited liability

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 9/35

Transaction cost matrix

- Contract creditor in public corporation

Shareholders

Limited liability since they are residual owners

Prefer riskier projects w bigger upside bc they don’t share downside of risk

Power very limited to direct investments – difficult to externalize costs of risky ventur

Creditors

Prefer unlimited liability

Creditors are cheaper monitors of corporate investments

Accept role as monitor w limited liability regime in return for prior claim on corp’s as- Contract creditor in close corporation

Shareholders

Much more likely to be in control – increased risk of externalizing costs

Creditors

Face low monitoring and collection costs bc small number of shareholders

Often require shareholder/manager to execute personal liability agreements

- Tort creditor in public corporation

Concession theory in bunk

Corporate law is set of standard form Ks designed to facilitate private ordering

Externalities are real problem

Pro-rata tort liability would have many problems

- Tort creditor in close corporation

Hardest case to justify limited liability default

Shareholders in control and have bargaining power

Piercing available (but also for K creditors)

Veil-piercing test

- New York (Lowendahl)

Corporate shareholder domination of corp

Corporate wrongdoing that proximately caused creditor injury- 7th Circuit (Van Dorn, Sea Land)

Unity of interest & ownership

Lack of corporate formalities

Commingling of funds and assets

Under-capitalization

Movement of funds back & forth

Failing to pierce would either sanction fraud or promote injustice

Tax fraud

Use of corporation funds for personal benefit

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 10/35

- Contract creditors (Laya, Kinney Shoe)

Unity of ownership

Such that separate personalities of corp and individual shareholder no longer exist

Inequitable result occurs if acts were treated as those of corp alone

And veil is not pierced

D still might prevail by showing assumption of risk by creditor

Who should have known of undercapitalization through investigation

Enterprise liability and parent-sub corps ( In re Silicone Implants)

- Separate corps facilitates offloading of externalities Operate high-risk activities with asset-less corp

- Best test for veil piercing here

Focus on whether corp is offloading like this

Reverse veil piercing

- Allows shareholders to disregard corp’s separate identity

- Courts split 50-50

Outsider reverse piercing

- Allows creditor of shareholder to disregard corp’s separate identity

- Unsecured creditors who relied on corporate assets disadvantaged (same w other shareholders)

V. Business Judgment Rule

Duty of Care v. Business Judgment Rule ( Dodge)- Duty of care

Common law

Officers and directors owe shareholders duty of careo Requires directors to exercise that degree of skill, diligence, careo That reasonably prudent person would exercise under ccs

MBCA §8.30(a)

Each member of board, when discharging duties of director, shallo Act in good faith; ando In manner the D reasonably believes to be in corp’s best interests

Generally

Tells directors not to be negligent- Business judgment rule

Two prerequisites

Duty of loyalty (no self-dealing)

Duty of care Generally

BJR shields directors from liability for making mistakes

Insulates directors from negligence liability – liability only for fraud or self-dealing Statutory response

- Non-shareholder constituency statutes In performing duties of director in best interests of corp, may consider the interests of

Corp’s employees

Corp’s customers

Corp’s suppliers

Corp’s creditors

Economy of region, state, nation

Impact on community

environment

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 11/35

long-term and short terms interest of corp and shareholders- Most states have these

Few are mandatory

Evaluating charity decision under BJR- What do you need to know as atty?

Applicable statute? Limits in charter or by-laws? Approval from board? Board informed? Board interested in transaction? How much is $ for corp? Was it pet charity? Was it reasonable relative to profits? What was business purpose?

Business judgment rule- Shlensky

Directors’ decision is final and not subject to judicial review

Absent fraud, illegality, or self-dealing Carte blanche to make decisions that might turn out badly No discretion to make selfish decisions

Directors immune from claims of negligence If well informed and careful about decisions

Traditional justification

Courts not business experts, so litigation is imperfect way to review business

But, court not experts on lots of things it rules on Other justifications

Designed to protect decisions not in interest of non-shareholder constituencies

Encouraging optimal risk taking

Hindsight bias

Review may disrupt board as team-based decision maker

Shareholders better off to let management make decisions w/out their voteo BJR does this w/out cutting off shareholder action for egregious caseso Tradeoff bt accountability and discretiono Judicial review threatens board’s authority

- Kamin BJR insulates Board from suit on merits

Absent fraud, dishonesty, or nonfeasance

Court will not substitute its opinion for Board’s opinion Dividend questions exclusively business judgment decision Strong abstention version of BJR

- ALI §4.01(c) D who makes business judgment in good faith fulfills the duty under this section if the D

Is not interested in the subject of business judgment

Is informed on subject of business judgment to extent that D believes appropriate

Rationally believes that the business judgment is in the best interests of corp- Chancellor Allen

BJR provides that where D is independent and disinterested, not liability for corp loss Unless no person could possibly authorize such a transaction if he was attempting to meet dut

Two ways to think about BJR- As standard of liability (this wins in the end)

No liability for negligence Instead liability based on

Gross negligence

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 12/35

Fraud

Illegal conduct

Self-dealing- As an abstention doctrine

Court will not review substance of board decisions Preconditions

No fraud

No illegality

No self-dealing

Court will examine decision-making process To extent to which Board made informed deicison

V. Duty of Care

Standards- Graham

Ds must use care which ordinarily careful and prudent men would use in similar ccs- ALI §4.01(a)

D has duty to corp to perform D’s functions

In good faith

In manner that he reasonably believes to be in best interests of corp, and

With care that ordinarily prudent person would reasonably be expected to exercise in position under similar ccs

- Van Gorkom Gross negligence

If D is grossly negligent, not protected under BJR

Board must provide some credible, contemporary evidence that it knew what it was do

If not, board member can be held personally liable Procedural due care perquisite to invoking BJR

Major transaction w final period consequences

Evidence that board has abrogated decision making authority

Ds who fail to act in informed and deliberate manner will not get BJR protection- Technicolor

First ask whether P can show evidence or breach of loyalty, good faith, or due care If P fails, BJR attaches Rule acts as both procedural guide and substantive rule of law

- Cinerama, Weinberger Entire fairness test

Process board followed

Quality of decision board reached

Disclosures made to shareholders Appraisal proceedings

Allow for fishing expedition

Always allows discovery, which can then yield procedural irregularities- Eisner

No substantive due care

Due care in decision making context is procedural due care only Expert reliance (DGCL §141(e)

Ds fully protected in relying in good faith on reports made by officers BJR can be rebutted if P shows that Ds breached fiduciary duty of care or loyalty or bad faith

Burden shifts to D to show the challenged transaction was entirely fair Bad faith standard

Conduct motivated by subjective bad faith (intent to do harm)

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 13/35

Intentional dereliction of duty (conscious disregard for responsibilities)

Not gross negligence- McMullin

NJR operates as both procedural guide and substantive rule of law P can survive MTD phase

- Francis BJR has no application where Ds have failed to exercise business judgment P still has to prove that Ds breached duty of care No violation when not on notice – free bite rule

- Caremark Test of liability = lack of good faith by sustained/systematic failure of D to exercise reasonab

oversight Makes board service by qualified persons more likely while still acting as stimulus of good fa

- Operative rule (Parnes) Presumptive validity of business judgment is rebutted only when decision is so far beyond

bounds of reasonable judgment that it seems inexplicable on any ground other than bad faith- MBCA §8.31(a)(2)(iv)

D not liable for any decision or failure to act unless P shows conduct result of

Sustained failure of D to devote attention to ongoing oversight of business; or

Failure to devote timely attn when particular facts and ccs of significant concern

materialize that would alert reasonably attentive D of need Framework for D&O liability

- Business judgment rule (RMBCA §8.31(a)(2)) Presumes that duty of care standard has been met

- Waiver of liability (DGCL §102(b)(7)) Corps can eliminate D&O liability for duty of care violations Self-insurance for gross negligence

- Indemnification (DGCL §145) May indemnify for D&O actions in good faith And for those not provided but still in good faith

- D&O Insurance (DGCL §145(g)) Corp may buy insurance whether or not they have power to indemnify such person

- Reimbursement of legal expenses (DGCL §145(c)) Even if not in good faith, success in legal action requires indemnification for legal bills

Theory of Board power- Authority-based decision making is essential for public corps

Large number of constituencies w different access to info Diverse constituencies w conflicting interests Intractable collective action problems

- Tension by authority & accountability vis-à-vis boards and managers Agency costs only eliminated by eliminating authority Market constraints important Power to hold account is power to decide

- Choosing authority raises issues of accountability Who’s watching the watcher?

- BJR prevents shifts locus of decision making from boards to judges Shareholders would bargain for BJR Hindsight bias would discourage risks Inference w internal governance Judicial decision making not subject to market discipline

Damages (Technicolor )- Cede I

Action for rescission and damages can proceed in parallel

- Cede intermezzo

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 14/35

Absent proof of D self-interest, must prove that D negligence caused injury Must introduce sufficient evidence form which responsible estimation of damage can be mad

- Cede II Gross negligence in process is sufficient to shift burden to directors Requires Ds prove that transaction was entirely fair

- Cede III Gross negligence doesn’t mean substance of deal was unfair There can be gross negligence in entirely fair transaction

Books & Records ( Eisner , DGCL §220)

- Stockholder can inspect corporation’s books and records for any proper purpose If corp refuses, shareholder can get order to compel from Chancery court

- What is proper purpose? Investigate mismanagement – no fishing expeditions though Share valuation Proxy contexts

- What is improper purpose? Proprietary business info Strike suits Serve other business interest Pursue political, social goals

Duty to be informed (Francis) - Obligation of basic knowledge and supervision

Continuing obligation to keep informed about activities of corp General monitoring – not detailed inspection of day-to-day activities

- Read and understand financial statements D should acquire at least rudimentary understanding of business of corp Not required to audit books – just maintain familiarity w financial status by reg review

- Must object to misconduct – if necessary, resign- Who are duties owed to?

Shareholder Creditors (sometimes)

Duty to monitor- Allis-Chalmers

Absent cause for suspicion, not duty on Ds to ferret out wrongdoing which they have no reasoto suspect exists

- Caremark Duty of care requires board to monitor important aspects of firm

Legally, board itself required only to authorize most significant corp actso But ordinary business decisions can vitally affect welfare of corp

Growing role of criminal law with safe harbors for compliance programso Powerful incentive for corporations to detect violation thru these programs

D’s obligation includes duty to attempt in good faith to assure that corp info and

reporting existso Must be system that board deems adequate

- Martha Stewart No duty to monitor personal behavior

Regardless of someone’s importance to corp, person is not the corp

Monitoring of personal affairs is neither legitimate or personal- Sarbanes-Oxley

Need internal control reports validated by officers Can go to jail for 30 yrs or have $5m in fines or both All firms are “biters” re accounting and financial reporting

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 15/35

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 16/35

Book value v. market value- Book value

Acquisition cost minus depreciation Value reported on firm balance sheets

- Market value Replacement cost Price of a thing is what it will fetch

- Accounting rules BV appropriate where no liquid market MV appropriate where liquid trading market Mark to market occasionally required for certain assets

Piercing-like inquiry re fairness ( Lewis) - Inquiry

Did Ds respect separateness? Did Ds do arm’s length analysis?

- Burden shifting BJR w burden on P presupposes that Ds have no conflict of interest When interested, burden shifts to Ds to show that transaction was fair

Shareholder ratification- Entire atmosphere changed when formally approved by shareholders (Gottlieb)

If ratified Director conflict

o P must show waste

Controlling shareholder conflicto P must how deal not entirely fair

If not ratified

D has to show fair deal- Competing approaches

tandard of review (burden of proof) DGCL §144 RMBCA §8.61 ALI §5.02

Neither board nor shareholders

pprove

EF (D) EF (D) EF (D)

Disinterested directors authorize BJR (P) BJR (P): §8.61(b)(1) &

Comment 2

Reasonable belief in fairness (P)

§5.02(a)(2)(B)

Disinterested directors ratify BJR (P) BJR (P): §8.62(a) &

Comment 1

EF (D): §5.02(c), §5.02(a)(2)(A),

§5.02(b).

hareholders ratify Waste (P). But see

Wheelabrator (EF, if

controller)

Waste (P) Waste (P)

- Big picture Ratification of duty of care problem kills the claim Ratification of director conflict shifts burden of proof but keeps standard at waste Ratification of dominating shareholder conflict shift burden but lowers standard to fairness

- Hierarchy considering Ability of courts to police (their perception) Ability of shareholders to recognize (court’s perception) Seriousness of problems (court’s perception)

Black letter law- Absent conflict of interest

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 17/35

P has burden of proof and will likely lose under BJR- If unratified conflict of interest

Directors have burden of showing the challenged transaction was fair/reasonable- If conflicted party transaction is ratified (by either disinterested shareholders or directors)

For director ratification

P has burden of proof and must overcome powerful BJR For shareholder ratification of director conflict

P must show waste For shareholder ratification of controlling shareholder conflict

P must show not entirely fair

B. Corporate Opportunities

Corporate opportunity doctrine- Purpose?

Deter taking new business prospects that belong to the corp- Covered persons?

Officers and directors of the corp Dominant shareholders who take active role in firm management

- Why can’t parties just bargain? Socially wasteful costs

Guth test - Line of business- Prior expectancy or interest in opporuntiry- How opportunity discovered

Broz test- Factors

Financially able? Same line of business? Expectancy or interest in opportunity? Does it create conflict of interest?

- Absence of one factor not enough

- If D believes that corp not entitled to take opportunity based on a factor D may take opportunity for himself

- Board presentation Disclosure

Not a prerequisite to show opportunity to board

But if D does so and board rejects, then safe harbor Costs

Reduces incentives to invest in info/opportunities

Risk of litigation if minority shareholders

Other relevant factors- Were there prior negotiations w firm about the opportunity?- Did the D conceal the opportunity?- Did the D use corporate fund to pursue opportunity?- Will opportunity involve competition w firm or otherwise thwart a business purpose?- Did corp have substantial need that opportunity would have satisfied?- Did corp have necessary technical, HR, other resources to exploit opportunity?- Is the D an insider?

Defenses for alleged opportunity usurpers- Capacity

Relevant to whether it was corp opportunity

Directors & officerso Corporate opportunity if learned while in corporate capacity

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 18/35

Officerso Corporate opportunity if within line of business

- Financial or technical inability Problem with this defense

Management helps raise money for firm – moral hazard problem

Management can loan it to firm if it has money

Seems like firms have to be virtually bankrupt for this to be relevant- Refusal to deal ( Energy Resources Corp)

Must be disclosed to prevent opportunism

Creates post-hoc evidence problems- Process (best defense)

Disclosure and ratification

C. Controlling Shareholders

Common law rule- Shareholders entitled to vote shares w/out regard to interests of other shareholders (Haldeman) - Shareholders qua shareholders are still allowed to act selfishly in deciding how to vote shares

Shareholders v. investors- Directors

Elected to serve interests of shareholders/firm as whole- Shareholders

Just invest to make money

Voting control- In most cases, voting control gives power to elect board- Potential to constrain thru agency law

Board is agent of shareholder; shareholder is principal Controlling shareholder can be derivatively liable for misconduct of agents

Controlling Shareholder definitions- Securities law

Presumption at 10%- ALI §1.10(b)

Presumption at 25%- Delaware

> 50% or exercises control in decision making

Controlling shareholder, then Ds must show entire fairness

Not controlling shareholder, then P must show waste- Better definition

No bright line rule for who is controlling shareholder Just whether board lacks independence

Parent subsidiary situations (Sinclair Oil)- Standards of review

BJR Intrinsic fairness

Use when parent has rec’d benefit to exclusion and at expense of minority shareholderof subsidiary

Limited to self-dealing

Capital structure situations ( Zahn) - Directors/controlling shareholders have same fiduciary relationship to corporation

Need to exercise independent judgment in changing classes of stocks Can’t just do it arbitrarily to put windfall on certain type

- Rule Firm should redeem class As

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 19/35

Bs are most junior-class of securities (biggest risk bearers) When fiduciary duties conflict, Ds should protect interests of investors bearing most risk

Arbitrary to extend but clear rule and parties can contract around it

Corporate finance- Complex capital structures allow firms to offer mixes of risk and return- Facilitates raising capital- Control follow risk

Summary – controlling shareholders- Fiduciary duties run to minority shareholders

- If self-dealing, burden shifts to Ds to show entire fairness

D. Executive Compensation

Legal basis- CEO and director pay set by directors

DGCL §122(5)

Ds appoint officers and agents and provide suitable compensation DGCL §122(15)

Ds establish and carry out pension, profit sharing, stock option, stock purchase, stock bonus, retirement, benefit, incentive, and compensation plan

- Directors typically delegate compensation decision to compensation committee

Composed of entirely independent directors (NYSE & NASDAQ rules) Committee hires compensation consultant to make recommendations

Types of pay- Salary

Fixed cash payment set at beginning of year or contract (usually 3-5 yrs)- Bonus

Addt cash payment if performance (financial or non-financial) exceeds target level Subjective element too

- Stock options Right to buy shares at fixed price Vesting and lifespan restrictions

- Performance units Stock granted if performance exceeds target over 3-5 years

- Restricted stock Stock grant with vesting tied to specific employee term

- Perks Club membership Company cars Purchased homes, Company jet

- Contractual agreements Severance agreements

Golden parachutes Post-retirement consulting contracts

- Benefits Life insurance Health insurance Regular pensions SERPS Employee stock ownership plans

Alleged problems with pay- Managerial power

CEO picks board and board sets pay

- Amounts

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 20/35

CEOs make lots of money, but so do celebrities- Disparity

CEOs make more than secretaries, but what should ratio be?- Pay not linked w performance

Some CEOs paid a lot even shareholders don’t do well

Growth of CEO pay- Total CEO compensation (salary + bonus + option value + long term incentives)

$9b in 2005- CEO compensation is

.09& of sales .07% of market capitalization 1.22% of net income

Compensation research- Top decile firms in pay outperform industries by 50%- Bottom decile underperform by 25%- Linage with firm size and market value- Technology allows returns to labor across greater asset base

Mechanisms to constrain pay- Disclosure

Shaming won’t work Involuntary disclosures won’t work

Leads to greater pay for performance

Ceilings becomes floorso Change of controlo Golden parachutes

- Ban specific practices Loans Backdating

- Improve governance- Caps

Pay in other ways Go private Jurisdictional competition

Conclusions- “Problem” is that managers paid like owners and owners doing very well

We can pay managers like something else, but what?- Contracts seem as efficient as we can expect

But there can still be learning- There are rotten apples

Prosecution of laws and internal governance improvements can help- Transparency and deterrence has own costs- Ultimately a political question

Want boards to be able to be on the next Jack Welch Qualified Immunity for Directors ( Disney)

- BJR protects director decisions Even when info and decision making process not so tidy to meet best practices

- Is this qualified immunity?

Option terminology- Types

Call option

Right to buy share at specified price (strike price Put option

Right to sell a share at specified price

- Terms

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 21/35

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 22/35

Can charge as much as market will bear Fiduciaries must disclose fees, though These fees are like corporate pay Signals the end of substantive fiduciary duties

At least at federal level

VII. Shareholder Litigation

Public markets

- Benfits Most liquid and cheapest capital Encourages greater innovation in economy

Allows entrepreneurs to cash out but keep firms independent

Public paydays attract human capital Incentive compensation Public disclosure and transparency leads to greater accountability Democratization of capitalism

- Costs Federal regulatory burden

SOX

SEC disclosure rules Transparency and loss of privacy Greater volatility Leads to short-term focus Pressure distracts from operational focus

Shareholders

Press

Plaintiffs’ lawyers Risk of shareholder suits

Purpose of shareholder litigation- Tension bt accountability and authority

Balance heavily tilted towards authority

Soviet-style elections for directors

BJR

Duty of care barely enforceable

Interested-party transaction allowed- Shareholders need to constrain

Opportunism, self-dealing behavior Illegal actions Utterly irrational behavior

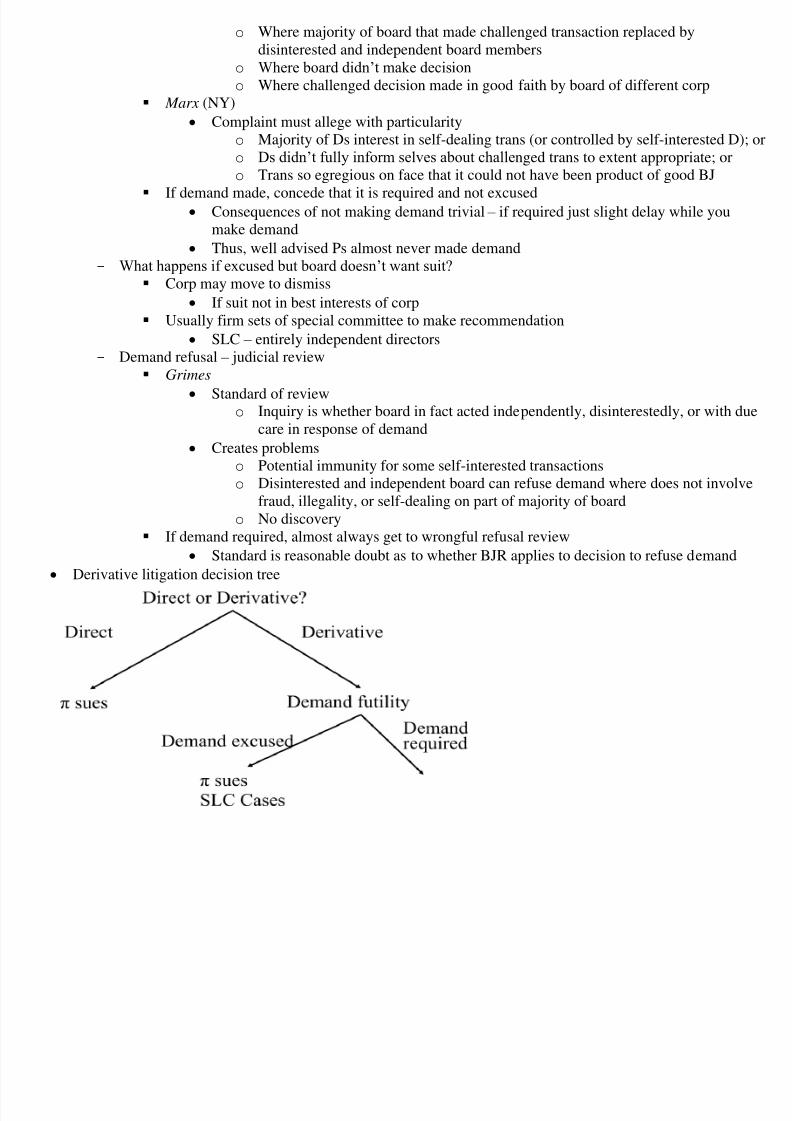

Derivative v. Direct-

Derivative suits Brought by

Shareholder on corp’s behalf (suit in equity to compel firm to sue) Cause of action

Belongs to corp as entity Arises from

Injury done to corp as entity Lawsuit in equity to compel corporation to sue third party Typical suits

Mismanagement

Executive compensation

Waste

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 23/35

Remedy

Money to corp- Direct suits

Brought by

Shareholder in his or her own name Cause of action

Belongs to shareholder in his or her individual capacity Arises from

Injury directly to shareholder and not shared by corp

Typical suits Oppression of minority shareholders

Dividends

Mergers Direct suit test

Injury to shareholder that is not derivative of prior injury to corp entity; or

Breach of contractual duty owed to shareholder independent of any right of corp Remedy

Non-monetary

Derivative suit basics- Problems

Why can’t shareholder just due whenever injured directly or indirectly?

Burdensome litigation – too many suits

But solution is class actions Who should run the derivative litigation?

Ds run firm so should have control of litigation

But when Ds are sued for breach of fiduciary duty

Thus don’t trust Ds to be unbiased

Again, board authority v. accountability- Civil procedure

Rule 23.1

Complaint shall allegeo P was shareholder at time of transaction; ando The action P desires from directors w/ particularity; ando Reasons for P’s failure to obtain the action

- Statistics Number of suits

175 in 2003

60% involve accounting (mostly revenue recognition)

33% include allegation of insider trading Average settlement

$23m – up 20% from 2002

6 suits for > $100m Probability of being sued over 5 yr period

10% chance of being named in at least one suit Institutional shareholders

Lead plaintiff in 30% of cases – up 3% from 1996 Outcomes

38% settled w/ financial recovery (most for only pennies per share)

38% settled w/o financial recovery

23% dismissed/failed

1% verdict for P

Strike suits

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 24/35

- Potential for abuse Suits are brought not to redress real wrongs, but to realize upon their nuisance value

- Settlement incentives Firms settle to avoid discovery, embarrassment, and bad PR Lawyers settle to get guaranteed fee

Expense statutes- Make unsuccessful plaintiffs reimburse firm for reasonable legal expenses

Applies to shareholders w < $50k - Few states have them

- Purpose Deter frivolous litigation Create shareholder liability for other side’s legal fees

- Do they work? Apply only to derivative suits

Careful pleading and weak-minded judges can help evade Can avoid by forum-shopping Impact can be diminished

Can bank together w other shareholders to satisfy minimum Other mechanisms exist

Sanctions for frivolous suits

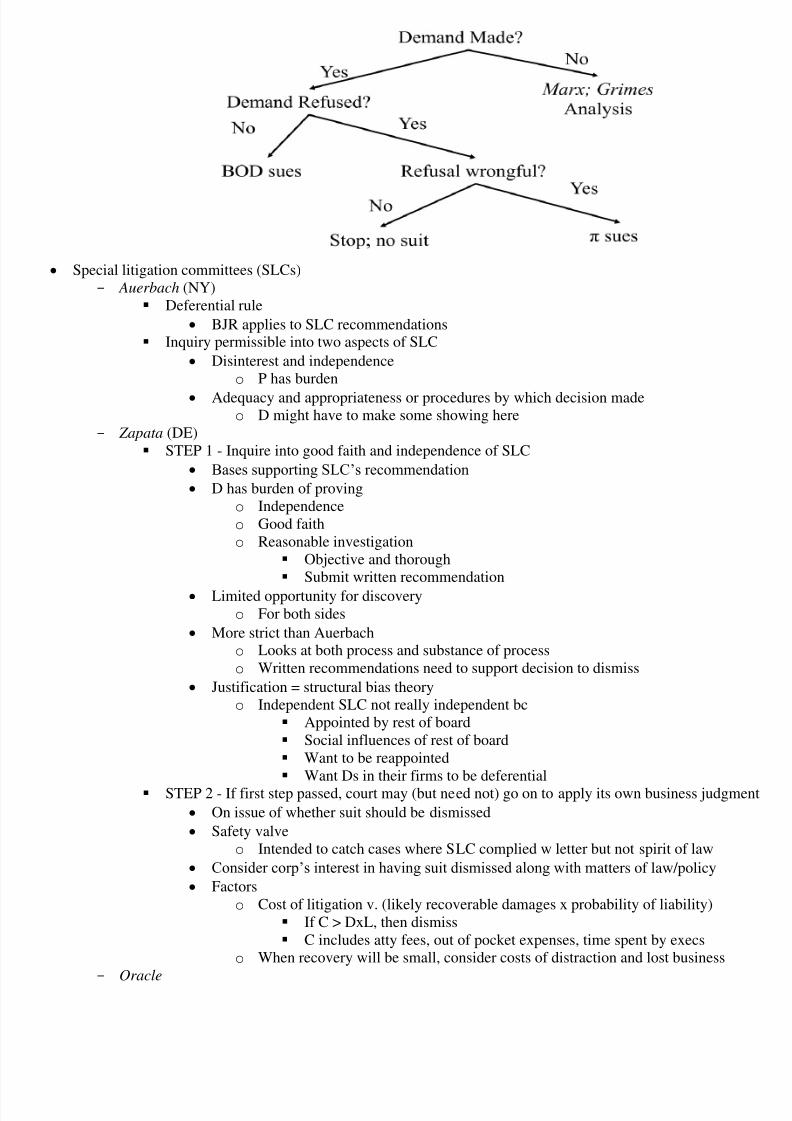

Board ability to terminate non-meritorious litigation Demand requirement

- Basics Most states requires P demand firm sue alleged wrongdoers

Demand musto Identify wrongdoerso Describe basis of wrongful acts and harm caused to corpo Request remedial relief

Does not have to be formal complaint

Shows that Ds manage business and affairs of corp If demand required, failure to make demand is procedural bar to suit Purpose of demand

Exhaustion of intra-corporate remedies serves ADR procedure to avoid litigation

If beneficial to corp, corp can control

If demand wrongfully refused, shareholder can control

Collapses relevant judicial inquiry to demand stage to conserve resources- When is demand excused?

Business judgment rule

Reviewing demand decision, board gets protection of BJR

P usually loses

Generally no discovery on these cases Grimes (DE)

Excuse based on facts supporting reasonable doubt that board is capable of makingindependent decision (if the following met, no BJR)

o Majority of board has financial or familial interest excluding the suit; oro Majority of board incapable of acting independently bc of domination/control;

But, rejection of structural bias theory – don’t presume insiders biased o Underlying transaction is not valid exercise of business judgment

Gross negligence standard applied to decision making process ( Brehm)

Rales test

Excused if facts create reasonable doubt that board COULD HAVE properly exercisedindependent and disinterested business judgment in responding to demand

Applies in three cases

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 25/35

o Where majority of board that made challenged transaction replaced bydisinterested and independent board members

o Where board didn’t make decisiono Where challenged decision made in good faith by board of different corp

Marx (NY)

Complaint must allege with particularityo Majority of Ds interest in self-dealing trans (or controlled by self-interested D)o Ds didn’t fully inform selves about challenged trans to extent appropriate; oro Trans so egregious on face that it could not have been product of good BJ

If demand made, concede that it is required and not excused Consequences of not making demand trivial – if required just slight delay while you

make demand

Thus, well advised Ps almost never made demand- What happens if excused but board doesn’t want suit?

Corp may move to dismiss

If suit not in best interests of corp Usually firm sets of special committee to make recommendation

SLC – entirely independent directors- Demand refusal – judicial review

Grimes

Standard of reviewo Inquiry is whether board in fact acted independently, disinterestedly, or with d

care in response of demand

Creates problemso Potential immunity for some self-interested transactionso Disinterested and independent board can refuse demand where does not involv

fraud, illegality, or self-dealing on part of majority of boardo No discovery

If demand required, almost always get to wrongful refusal review

Standard is reasonable doubt as to whether BJR applies to decision to refuse demand

Derivative litigation decision tree

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 26/35

Special litigation committees (SLCs)

- Auerbach (NY) Deferential rule

BJR applies to SLC recommendations Inquiry permissible into two aspects of SLC

Disinterest and independenceo P has burden

Adequacy and appropriateness or procedures by which decision madeo D might have to make some showing here

- Zapata (DE) STEP 1 - Inquire into good faith and independence of SLC

Bases supporting SLC’s recommendation

D has burden of provingo Independenceo Good faitho Reasonable investigation

Objective and thorough Submit written recommendation

Limited opportunity for discoveryo For both sides

More strict than Auerbacho Looks at both process and substance of processo Written recommendations need to support decision to dismiss

Justification = structural bias theoryo Independent SLC not really independent bc

Appointed by rest of board Social influences of rest of board Want to be reappointed Want Ds in their firms to be deferential

STEP 2 - If first step passed, court may (but need not) go on to apply its own business judgme

On issue of whether suit should be dismissed

Safety valveo Intended to catch cases where SLC complied w letter but not spirit of law

Consider corp’s interest in having suit dismissed along with matters of law/policy

Factorso Cost of litigation v. (likely recoverable damages x probability of liability)

If C > DxL, then dismiss C includes atty fees, out of pocket expenses, time spent by execs

o When recovery will be small, consider costs of distraction and lost business-

Oracle

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 27/35

Independence test

Turns on whether D is – for any substantial reason – incapable of making decision witonly the best interests of the corp in mind

o Focus on impartiality and objectivity SLC has burden of proving its own independence

Unlike demand-excusal context where board is presumed independent

DE derivative suit decision tree (w/ SLC)

MBCA alternative- Demand required (§7.42)

Demand required in all cases Shareholder cannot bring suit for 90 days unless

Irreparable injury or

Board refusal

- Demand review (§7.44) If disinterested/independent Ds are quorum, board can review In all cases, independent Ds may vote by majority to appoint committee of indy Ds to review Board review must be in good faith after reasonable investigation

Demand can be refused if board concludes that proceeding not in best interests of corp If board that votes is majority independent

Burden of inquiry into independence/adequacy of investigation is on P If board not majority independent

Burden of inquiry on D Does not authorize review by court of reasonableness of determination made by board/commi

Rejects Zapata

Insurance, Indemnification, & Expenses- §145(a)

Firm can indemnify if person acted in good faith Makes charter provision unenforceable if no good faith

- §145(b) Corp may not reimburse D for liability in derivative suit that he loses unless court approval

- §145(c) Corp must reimburse D for expense in successful suit Indemnification not limited to good faith

Reimbursement of proxy fights- Rosenfeld

General

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 28/35

When directors act in good faith in a contest over policyo They have right to incur reasonable/proper expenses for

Solicitation of proxies and Defense of corporate policies

Specifics

Corporation may not reimburse either party unless dispute is of Qs of corporate policy

Corp may only reimburse reasonable expenses

Corp may reimburse incumbents if o They win; or

o They lose Corp may reimburse insurgents only if

o They win ando Shareholders ratify payment

Problems

Distinction bt policy and personnel largely charade

Reasonableness – burden should be on Ds

Obvious and intractable asymmetry in paymento Bias in favor of management – disincentive to mounting as insurgency

Decision tree analysis

Assumptions:

Dissident owns 15% of shares

G = gain to the corporation from the contest

50% likelihood of winning if insurgent spends $5M

No chance of winning if insurgent spends less; and corporation will spend $5M opposing

Anti Takeover Defenses

- Dual class recapitalizations Firm asks shareholders to approve votes w/ super voting powers

Class A stock – existing common stock

Class B stock – distributed pro rata to shareholderso Nontransferableo Convertible to class A shareso Super voting rights (10 votes per share)

Most public shareholders convert to class A

Bc they want shares to be transferrable

Leaves most voting power to management Problems

Management conflict of interest

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 29/35

- DGCL §160(c) Prohibits corps form voting stock ownership if issuing company is majority shareholder in co Most applicable to parent-sub relationships

VIII. Control Issues

A. Shareholder Voting

Why we give shareholders right to vote

- Makes most sense in closely held firm Information asymmetries are lower Managers are owners

- What about large public corps? Facilitates takeovers

Disciplines management Prevents dilution of rights

Protects minority shareholders- Voting is rare

Expensive Collective choice problems

Informational asymmetries Basic feature of voting system

- Shareholders vote on 3 kinds of matters Election of Ds Organic or fundamental changes

Mergers

Sales of assets

Corporate dissolutions

Charter amendments Shareholder resolutions

- Registered shares Each share has holder of record, which facilitates getting in touch w beneficial holder

- Proxy system If you can’t attend shareholder meeting, you can still vote by finding rep (proxy) Who goes to meeting on your behalf

- State law mandatory rules All state statutes require annual meeting for election of Ds Quorum requirements

- State law default rules All state statutes permit special meetings and action by written consent

- State v. federal law State law governs substance

Federal law governs procedures Voting patterns

- State laws are enabling statutes Alterable by contract

- Patterns of choice are clear One share, one vote Only shares possess vote Cumulative voting is rate Nonvoting stock is rare Shareholder rarely chose managers

Usually chose board who selects managers No special elections

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 30/35

Ds not typically recalled from office Shareholders vote by proxy Incumbent slate is elected Issues decided by majority of votes cast

- Limits No vote selling Proxies are revocable up until time of voting Voting required for certain fundamental transactions

Voting apathy

- Individual investors Only informed when benefits > costs

Benefitso Nearly all holder have very small stake in firmo No evidence that corporate governance reforms have impact on performance

Costso Proxy statements long and complex

- Institutional investors Growing role in proxy fights and governance – taking voting more seriously

Costs reduced by outsources to intermediaries

Still very little monitoring

More monitoring good? Pros

o Repeat players w large holdingso If not them monitoring, then who?

Conso May limit development of new bizo May lead to other corp governance problemso Undermines board-centric view of firmo Who is watching the institutional monitors?

Board action re votes (Peerless Systems) - Two possibility for standard of review

If board acted w primary purpose of interfering w shareholder franchise Then board must demonstrate compelling justification for actions

If can’t meet primary purpose test

Then BJR for Ds’ actions - Side lessons

Non-confidential nature of proxy voting

Allows selective solicitation of voters Management control over process

Not only does management draft proxy

But can play fast and loose w voting process

Proxy system- Separation of ownership and control

Fear of managers capitalizing on agency costs

Diffuse, uninformed, disinterested shareholders To keep themselves in office

By seizing control of the proxy machinery- 1934 Act §14(a)

Unlawful to use any mean of interstate commerce to solicit any proxy in respect of any securi

In contravention of SEC rules/regs necessary in public interest/shareholder protection Key components

General disclosure provisions

Disclosure requirement for rival groups

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 31/35

General antifraud provision

Shareholder communications provision – placing proposal in proxy- Levin

Decision to continue present management rests entirely w stockholders

Director performance irrelevant Disclosure is key foundation for proxy process

Amount spent should not be excessive- Shareholder meetings

Uncontested meetings

Managers can charge firm for proxies to get quorum Can charge firm for cost of informing shareholders on issues

Contested meetings

Managers may also charge firm for proxies to get quorum

SEC rules- §13(d)

> 5% holders must register w SEC- §13(f)

Institutional investors must register all holdings w SEC- §14(a)(8)

Following are exempt from having to be included in proxy Public statements about how one going to vote Public advertisement asking to vote one way or other Communication w less than 10 persons Communications w someone w whom shareholder has biz relationship

Proxy advisors

Proxy card- Required disclosures

Firm must send shareholders annual report Must file preliminary proxy card w SEC 10 days before solicitation Director and executive compensation Biographical material about D, including personal misconduct

B. Precatory Proposals

Proposal requirements- Any shareholder can being as long as

Has >$2,000 invested and Has held stock for at least one year

Can aggregate for amount of time- Resolutions must be couched as non-binding- Shareholder can submit only one proposal per year- Limited to 500 word

Outcomes- Proposals never “win” – never get majority of votes- Stunning victory is 10% of vote

Grounds for excluding (14a-8(i))- (1) it is not proper subject for shareholders

Choosing the CEO- (2) it is illegal

Firm should bribe senators- (3) it violates proxy rules

Misleading proposals- (4) it concerns personal grievance or benefit

Austin – labor union and employment practices (not resolved)

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 32/35

- (5) it relate to operations which account for < 5% of its net earnings and gross sales AND if nototherwise significantly related to issuer’s business

o Lovenheim Not limited to economically significant issues Matters of ethical and social significance can be included

- (6) it is beyond power of firm to effectuate- (7) it relates to firm’s ordinary business operations

Dole – pension fund wants health study (fine since just study)- (8) it relates to an election for membership on company’s board of directors

AIG – process needs to deal w election of removal of directors to be excluded- (12) It was submitted in past and didn’t get support

Must get 3-10% of votes to include in next year

Method of excluding- Firm sends “no action” letter to SEC - If firm loses, always acquiesces- If shareholder loses, can go to DC Cir.

Employment practices proposals- SEC 1992

Bright line rule banning all employment related proposals Under ordinary business exception

- Cracker Barrel No action letter excludes all proposals regarding affirmative action

- SEC 1998 Employment related proposals that raise significant social policy issues can be okay Case by case approach

Day to day stuff like hiring, firing = ordinary business

Affirmative action = social policy

C. Shareholder Inspection Rights

Shareholder lists- NY statute

Can get lists if You are shareholder of record for at least 6 mos if not >5% holder

It’s for purpose which is in interest of business of foreign corp- Anaconda

Whenever corp faces situation having potential substantial effect on its wellbeing/value

Shareholders are necessarily affected and biz of corp is involved under NY statute- DGCL §220(b)

Requesting shareholder must submit demand asserting proper purpose

Something reasonably related to such person’s interest as stockholder If request for shareholder list, burden on corp to show improper If request for other records, burden on shareholder to show proper

- Pillsbury Not proper purpose when

Impressing opinion favoring reordering of priorities

If it was about money and not just moral, it would proper- Sadler

Law should be liberally construed in favor of stockholder DE doesn’t require firm to compile NOBO list Firm has to produce on what is (or should be) in its possession

D. Control in Closely Held Firms

Shareholder agreements

- Ringling (DE 1947)

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 33/35

Generally enforceable

Shareholders can contractually bind selves as shareholders

- McQuade

ALL agmts among shareholders binding actions of Ds are void

Stockholders may NOT (by agmt amongst selves) control D in exercise of judgmentvested in D

D may not (by agmt as stockholder) abrogate their independent judgment - Clark

Voting agreements to constrain Ds okay if no minority shareholders Shareholder agmts binding if unanimous

- Galler If not unanimous vote, three factors re enforceability

Close corporationo No market for shares – more than just investor – human capitalo Shareholders often directors

No objection from minority shareholders

Agreement reasonableness- Ramos

Voting agmts can limit shareholder power

Even if end result is (indirect) constraint on D discretion

Vote pooling agmts valid even if firm isn’t statutorily close corporation You can agree about how you’ll vote as shareholders

You can NOT agree about how you’ll vote as directors o Can evade this by penalizing D votes

Why voting agreement Ks necessary?- Generally

Investors/entrepreneurs will NOT agree to form new firm and leave out details of who runs Rather, they insists on deciding crucial details in advance of investment Voting agreement one way to solve this problem

- Buy/sell agreement as rider to shareholder agmt – sometimes required for close corp Cross-Purchase Agmt

Withdrawing owner agrees to sell interest to remaining officers Suited for small biz w few owners

Entity-Purchase Agmt

Withdrawing owner agrees to sell interest to entity

Which then retires ownership interest Hybrid Agmt

Withdrawing owner must first offer ownership interest to entity

If entity declines/unable to purchase, then shares must be offered to other owners- Setting the price

Right of first refusal Bargain in good faith Valuation formula Book value of assets

o Appraiser

Coase theorem- Private ordering will result in efficient renegotiation or contractual obligation

Modern state law- IBCA §7.70

Generally authorizes voting agmts among shareholders Doesn’t apply to statutorily close corps SCCs can replace board governance w shareholder governance

- IBCA §7.71(b)

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 34/35

Shareholder agmt is effective against shareholder not party to K as long as

Shareholder had actual knowledge of agmt when became holder

Agmt is conspicuously noticed on certificate of incorporation- MBCA §7.32(b)

Must be unanimous vote Limited to 10 yrs in duration Must be conspicuously noticed on stock Any purchaser without notice entitled to rescission

E. Duties to Shareholders Wilkes

- Fiduciary duties of partnerships apply to corps as well- Modified Donahue test

Shareholders in close corp owe each other a duty of strict good faith If challenged by minority shareholder, controlling group must show

Legit business objective for its action Minority shareholders can nevertheless prevail if can show that

Same purpose could have been achieved in less harmful manner- Court offers intermediate level of fiduciary duty – between partners and BJR

Muddy like this limits clarity and incentives to contract on terms

Nixon - Wilkes is wrong- Holder who buys stock in closely held corp can make BJ whether to buy minority position- Parties can contract for protection and should do so – the court shouldn’t do this if no K

Ingle - Minority shareholder in close corp who contractually agrees to repurchase of his shares upon term- Acquires no right from corp or majority shareholders against at-will discharge

F. Abuse of Control

Smith

- Key Q is whether one has control – not size of holdings

25% holder has duty to other holders in close corp under 80% majority rule Can’t act out of personal greed and spite

Jordan

- Minority shareholder in close corp must be told about merger at earlier stage than in public corp- Shareholder incidental to employment so seems like at-will should trump

G. Transfer of Control

Zetlin

- No duty to share control premium w minority shareholders

- Absent looting of corp assets, conversion of corp opportunity, fraud, bad faith

Controlling shareholder free to sell controlling interest at premium price

- Majority can sell control block at a premium Minority shareholders have no automatic tag-along rights

- Any other rule would require tender offer in all cases Too radical of a rule for judges to make

Perlman

- When sale necessarily results in sacrifice of obvious business opportunities and consequently unusuaprofit to fiduciary who caused sacrifice

He should account for his gains

Corporate opportunity transfer- DE

Show that benefit appropriate to the exclusion of detriment of minority- MBCA

7/30/2019 * Corporations - Henderson - Fall 2008

http://slidepdf.com/reader/full/-corporations-henderson-fall-2008 35/35

Financial interest of D likely to influence judgment