© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS SERVICE TAX - NEGATIVE LIST REGIME By Jigar Shah...

57

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS SERVICE TAX - NEGATIVE LIST REGIME By Jigar Shah Advocate

-

Upload

sharleen-mcdowell -

Category

Documents

-

view

213 -

download

0

Transcript of © COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS SERVICE TAX - NEGATIVE LIST REGIME By Jigar Shah...

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS

SERVICE TAX -NEGATIVE LIST REGIME

By Jigar Shah Advocate

NEW REGIME

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 3

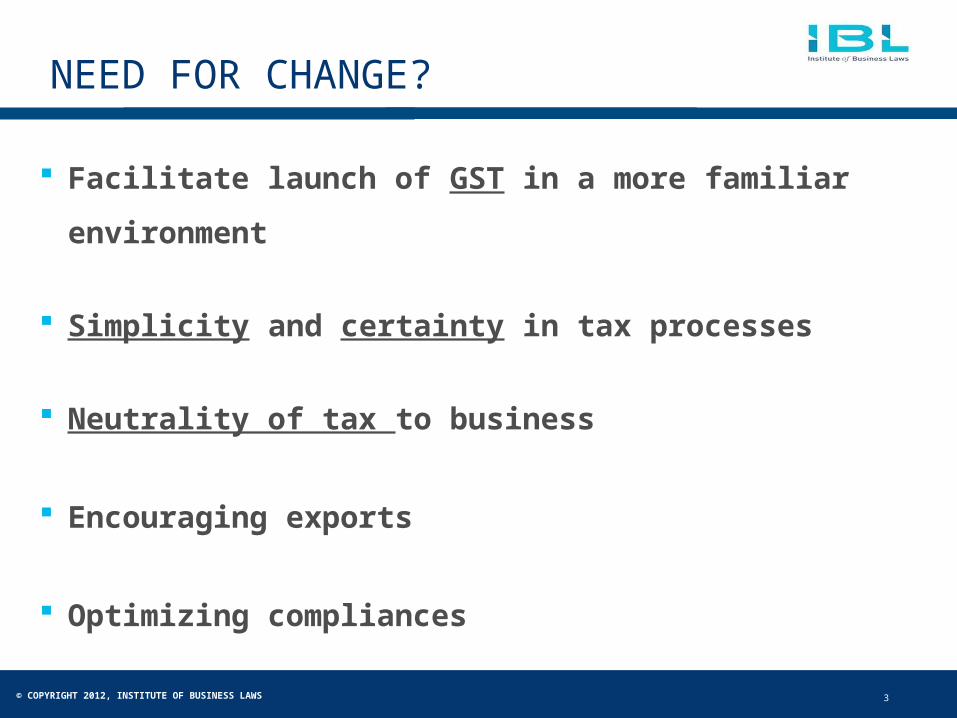

NEED FOR CHANGE?

Facilitate launch of GST in a more familiar environment

Simplicity and certainty in tax processes

Neutrality of tax to business

Encouraging exports

Optimizing compliances

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 4

PARADIGM SHIFT IN

REGIME

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 5

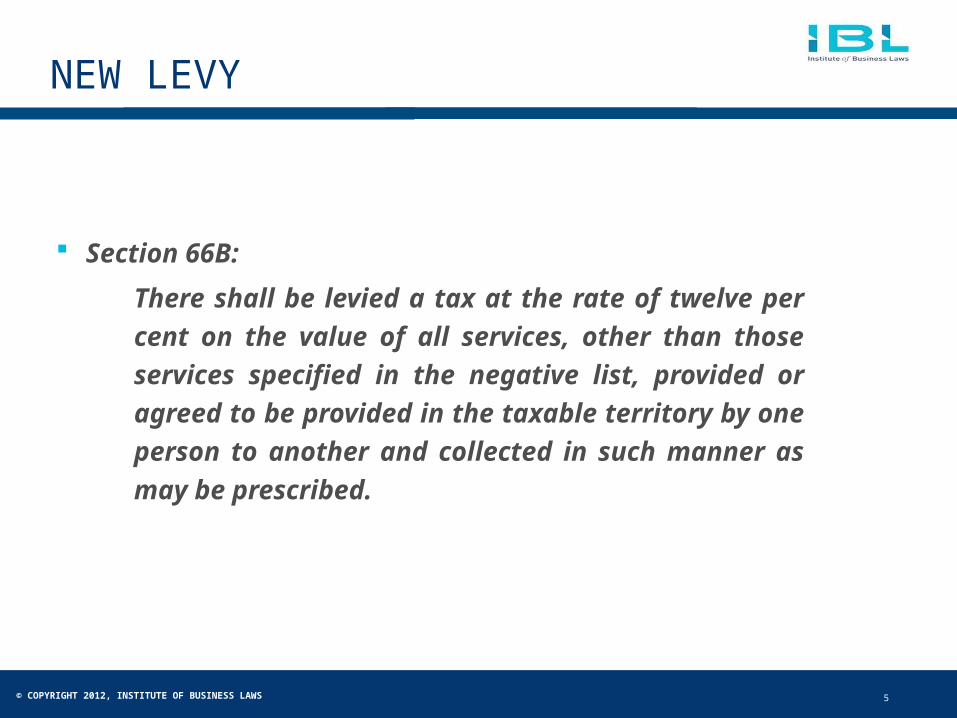

NEW LEVY

Section 66B:

There shall be levied a tax at the rate of twelve per

cent on the value of all services, other than those

services specified in the negative list, provided or

agreed to be provided in the taxable territory by one

person to another and collected in such manner as

may be prescribed.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 6

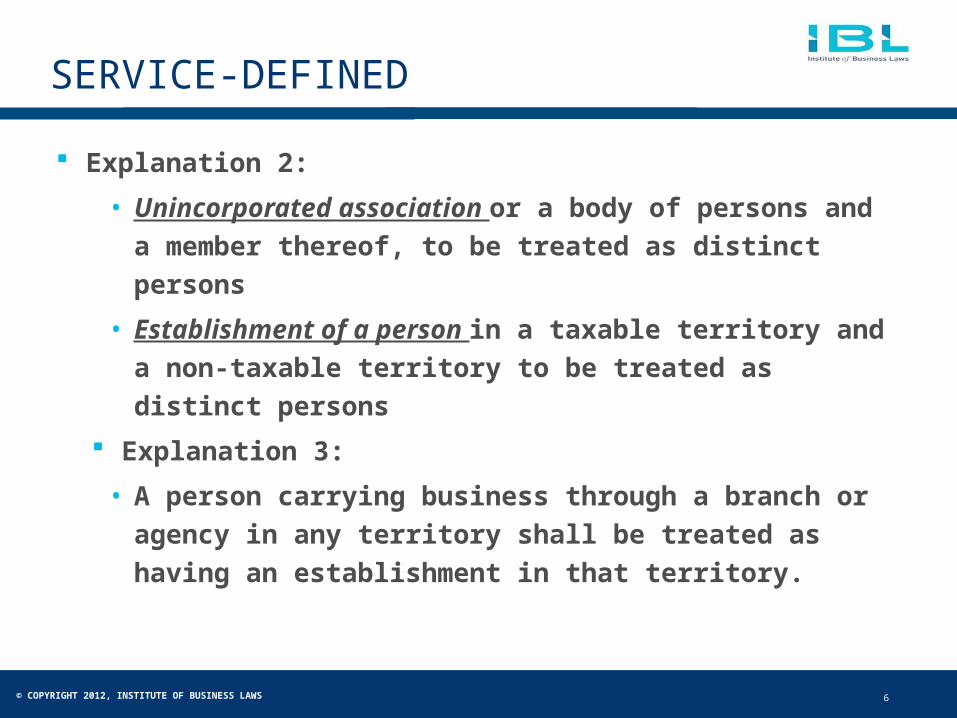

SERVICE-DEFINED

Explanation 2:

• Unincorporated association or a body of persons and a

member thereof, to be treated as distinct persons

• Establishment of a person in a taxable territory and a non-

taxable territory to be treated as distinct persons

Explanation 3:

• A person carrying business through a branch or agency in

any territory shall be treated as having an establishment in

that territory.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 7

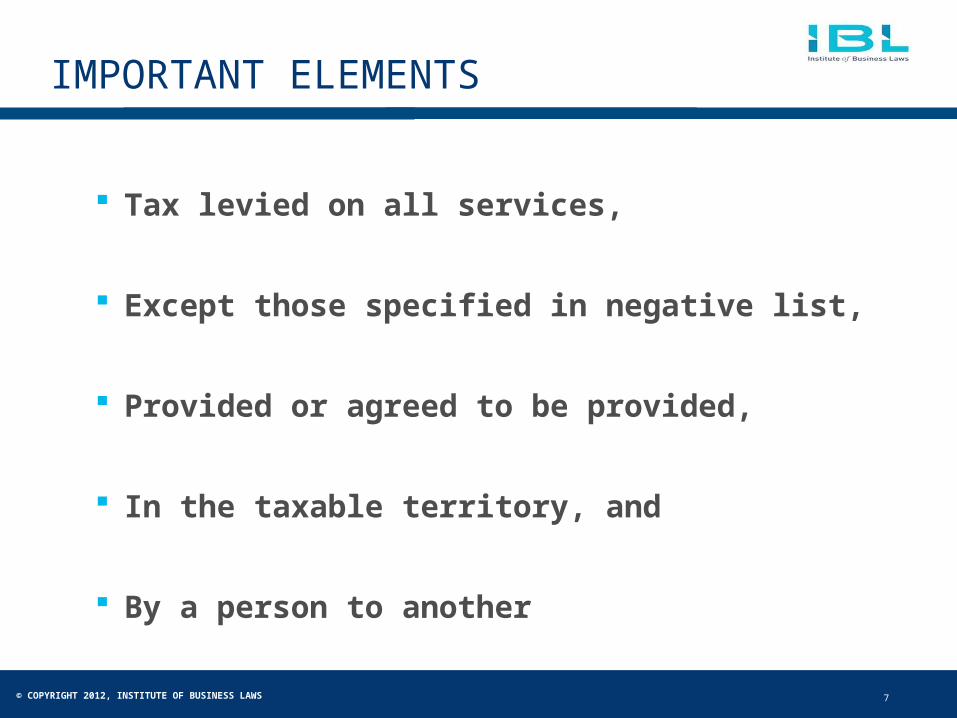

IMPORTANT ELEMENTS

Tax levied on all services,

Except those specified in negative list,

Provided or agreed to be provided,

In the taxable territory, and

By a person to another

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 8

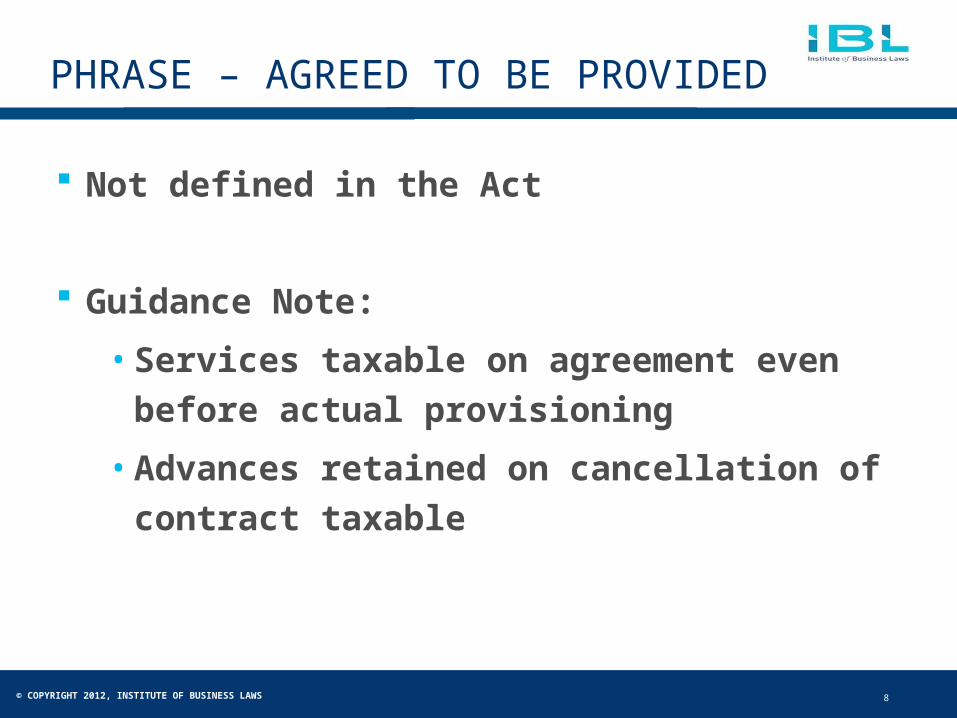

PHRASE – AGREED TO BE PROVIDED

Not defined in the Act

Guidance Note:

• Services taxable on agreement even before

actual provisioning

• Advances retained on cancellation of

contract taxable

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 9

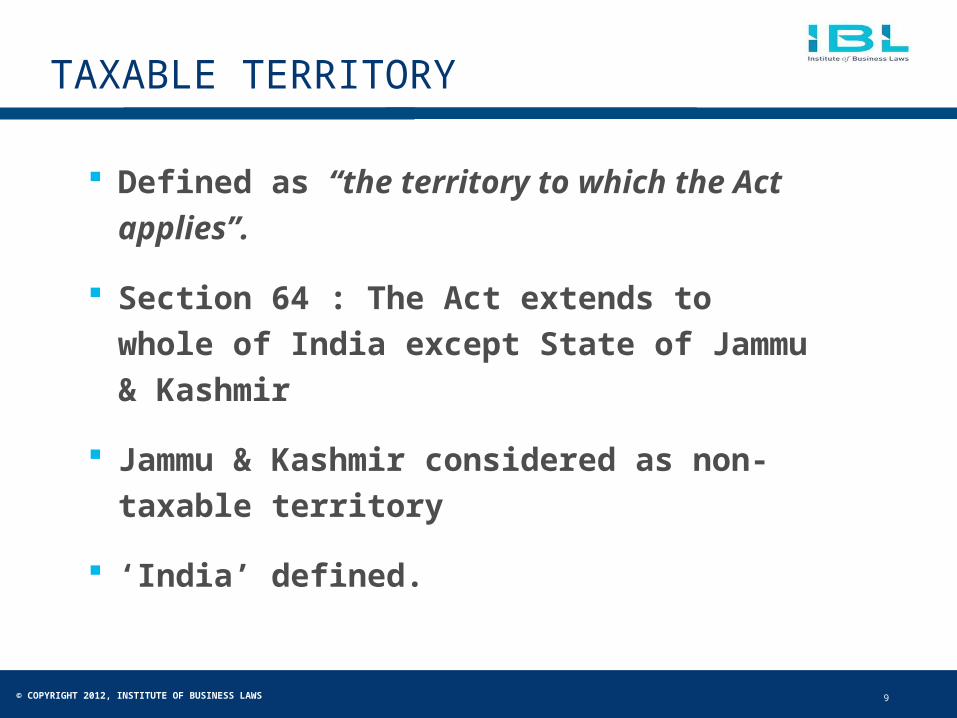

TAXABLE TERRITORY

Defined as “the territory to which the Act

applies”.

Section 64 : The Act extends to whole of India

except State of Jammu & Kashmir

Jammu & Kashmir considered as non-taxable

territory

‘India’ defined.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 10

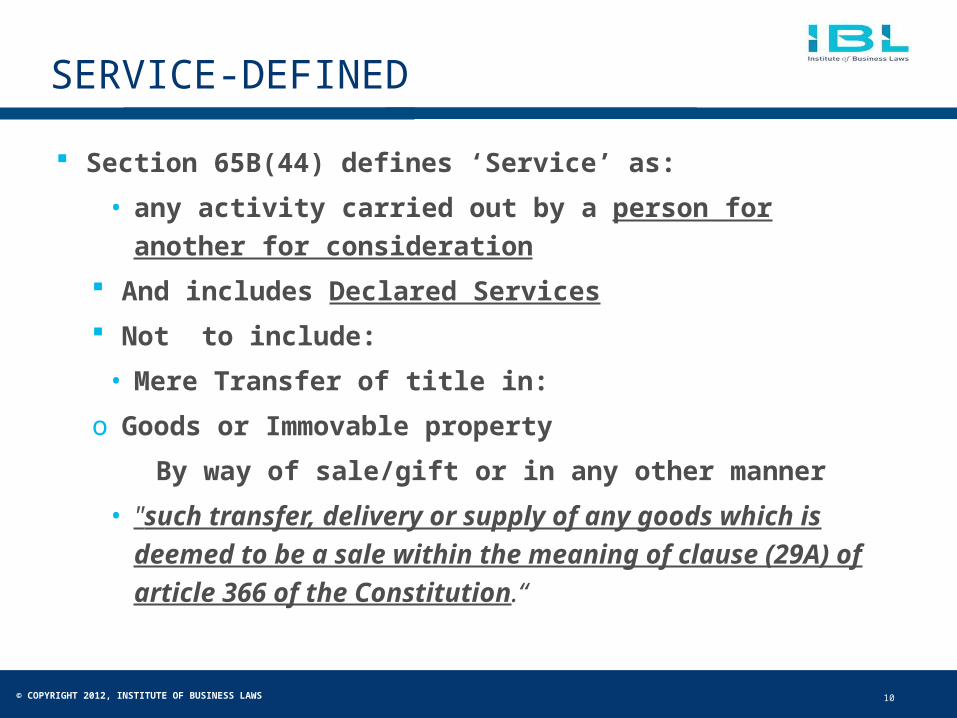

SERVICE-DEFINED

Section 65B(44) defines ‘Service’ as:

• any activity carried out by a person for another for

consideration

And includes Declared Services

Not to include:

• Mere Transfer of title in:

o Goods or Immovable property

By way of sale/gift or in any other manner

• "such transfer, delivery or supply of any goods which is

deemed to be a sale within the meaning of clause (29A) of

article 366 of the Constitution.“

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 11

SERVICE-DEFINED

Not to include Continued…

• Mere transaction in Money or Actionable claim

• Services in the course of employment provided by an

employee to employer

• Fees payable in a court/ tribunal

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 12

ACTIVITY

Not defined in the Act

Guidance Note:

• Meaning as understood in common parlance

should be given

• Activity could be active or passive so to include

act of forbearance etc

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 13

CONSIDERATION

Not defined in the Act

Guidance Note:

• Definition of consideration from Indian Contract Act,

1872 could be borrowed

• Anything which the receiver does or abstain from doing

for receiving the service

• Would include both monetary as well as non-monetary

• Section 67 to determine value of non-monetary

consideration

Whether direct nexus with activity required?

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 14

WHETHER – CONSIDERATION ?

Advance forfeited for cancellation of

agreement to provide service

Excess payment made by mistake

Security deposit forfeited for

damages/faulty action of receiver

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 15

DECLARED SERVICES

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 16

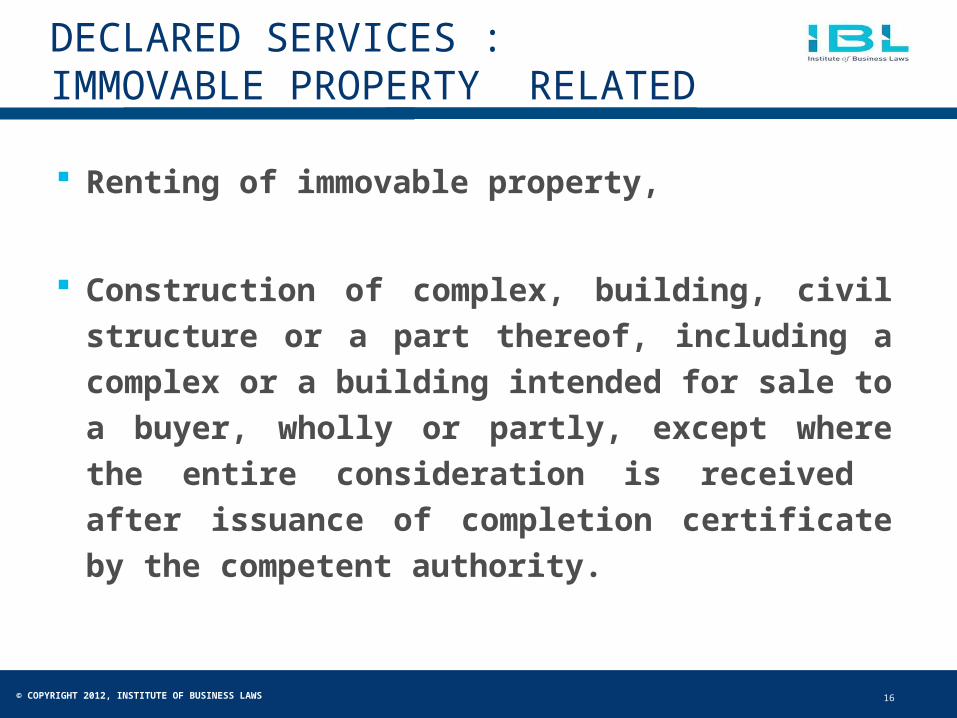

DECLARED SERVICES : IMMOVABLE PROPERTY RELATED

Renting of immovable property,

Construction of complex, building, civil structure or

a part thereof, including a complex or a building

intended for sale to a buyer, wholly or partly, except

where the entire consideration is received after

issuance of completion certificate by the competent

authority.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 17

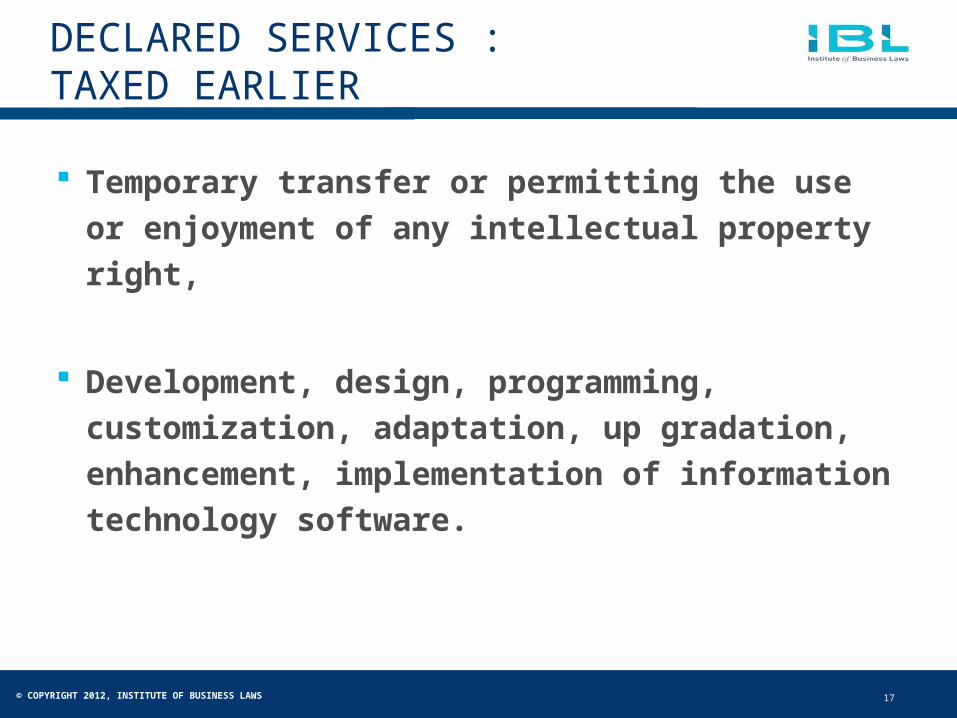

DECLARED SERVICES : TAXED EARLIER

Temporary transfer or permitting the use or

enjoyment of any intellectual property right,

Development, design, programming, customization,

adaptation, up gradation, enhancement,

implementation of information technology software.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 18

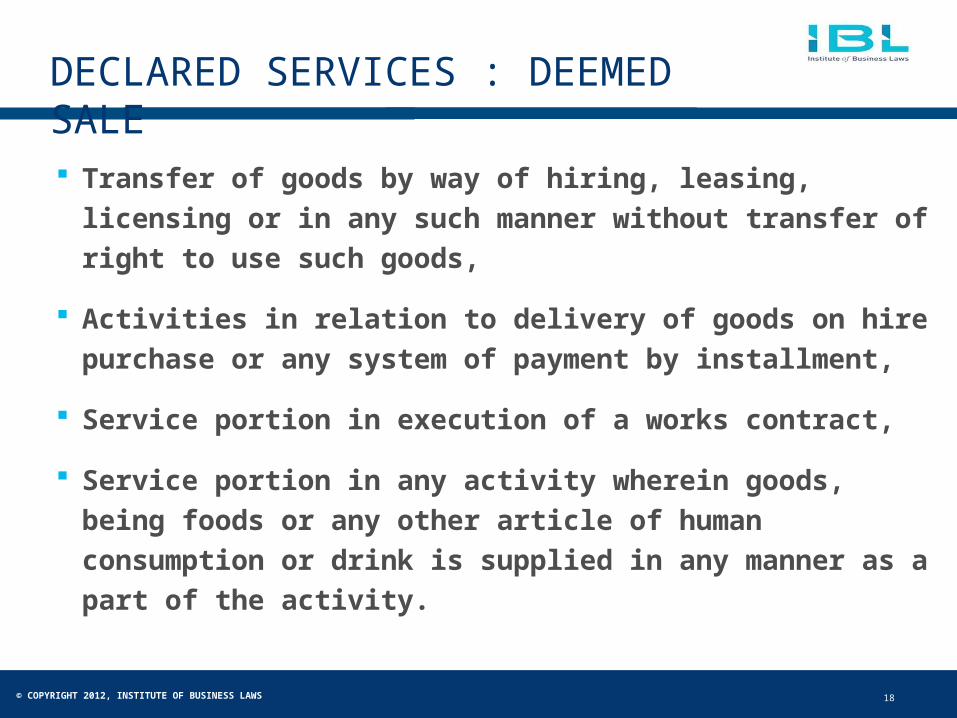

DECLARED SERVICES : DEEMED SALE Transfer of goods by way of hiring, leasing, licensing or

in any such manner without transfer of right to use

such goods,

Activities in relation to delivery of goods on hire

purchase or any system of payment by installment,

Service portion in execution of a works contract,

Service portion in any activity wherein goods, being

foods or any other article of human consumption or

drink is supplied in any manner as a part of the activity.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 19

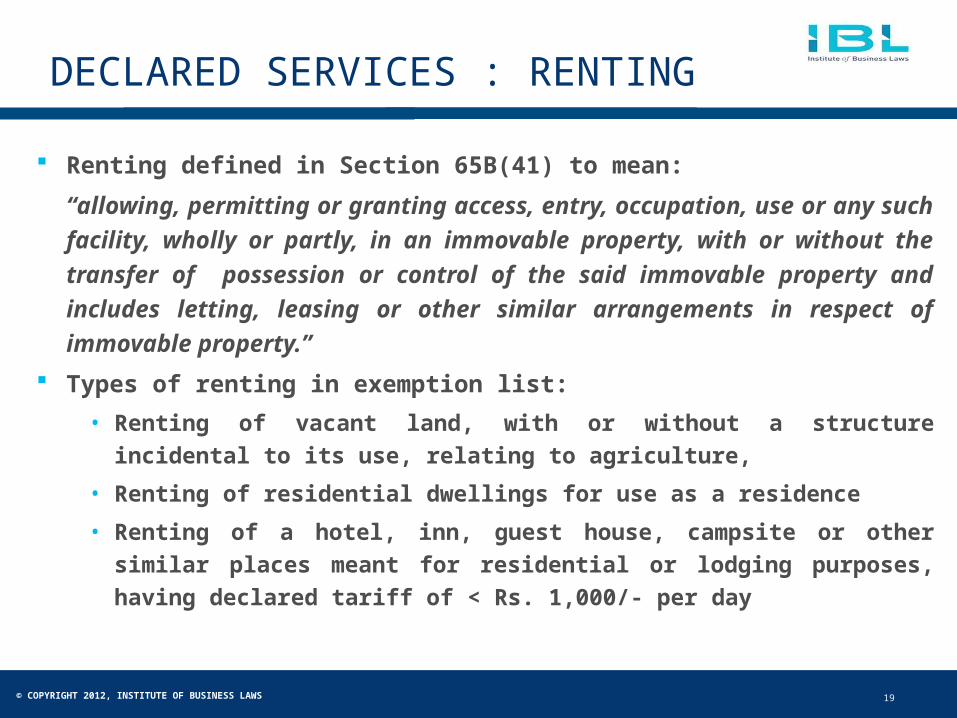

DECLARED SERVICES : RENTING

Renting defined in Section 65B(41) to mean:

“allowing, permitting or granting access, entry, occupation, use or any such

facility, wholly or partly, in an immovable property, with or without the

transfer of possession or control of the said immovable property and

includes letting, leasing or other similar arrangements in respect of

immovable property.”

Types of renting in exemption list:

• Renting of vacant land, with or without a structure incidental to its use,

relating to agriculture,

• Renting of residential dwellings for use as a residence

• Renting of a hotel, inn, guest house, campsite or other similar places meant

for residential or lodging purposes, having declared tariff of < Rs. 1,000/-

per day

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 20

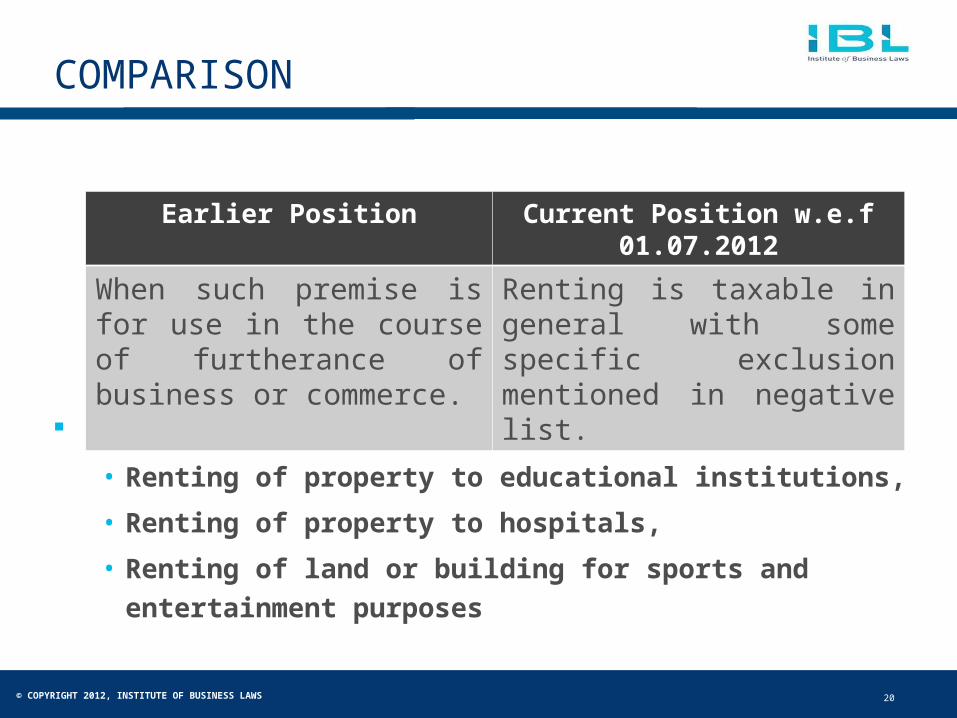

COMPARISON

Status of :

• Renting of property to educational institutions,

• Renting of property to hospitals,

• Renting of land or building for sports and

entertainment purposes

Earlier Position Current Position w.e.f 01.07.2012

When such premise is for use in the course of furtherance of business or commerce.

Renting is taxable in general with some specific exclusion mentioned in negative list.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 21

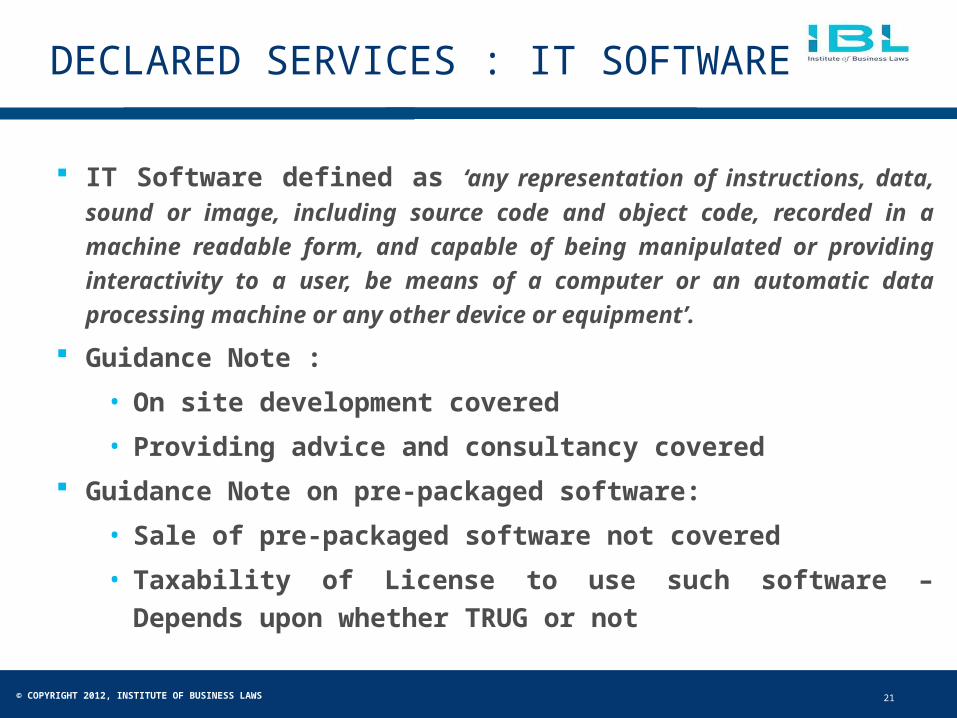

DECLARED SERVICES : IT SOFTWARE

IT Software defined as ‘any representation of instructions, data, sound

or image, including source code and object code, recorded in a machine

readable form, and capable of being manipulated or providing interactivity

to a user, be means of a computer or an automatic data processing

machine or any other device or equipment’.

Guidance Note :

• On site development covered

• Providing advice and consultancy covered

Guidance Note on pre-packaged software:

• Sale of pre-packaged software not covered

• Taxability of License to use such software – Depends upon

whether TRUG or not

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 22

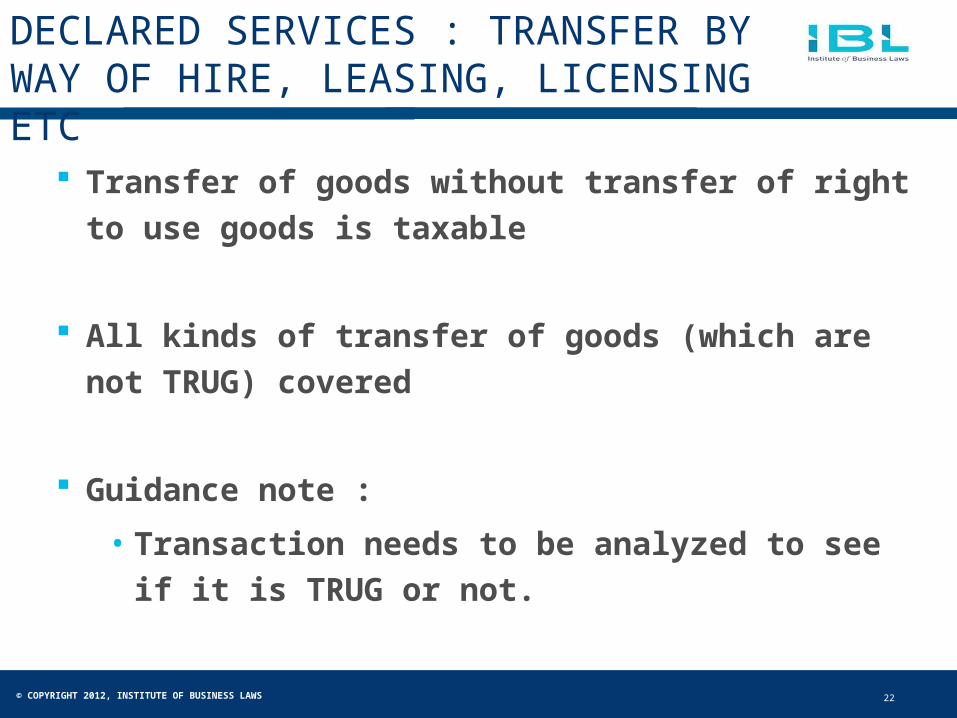

DECLARED SERVICES : TRANSFER BY WAY OF HIRE, LEASING, LICENSING ETC

Transfer of goods without transfer of right to use goods

is taxable

All kinds of transfer of goods (which are not TRUG)

covered

Guidance note :

• Transaction needs to be analyzed to see if it is

TRUG or not.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 23

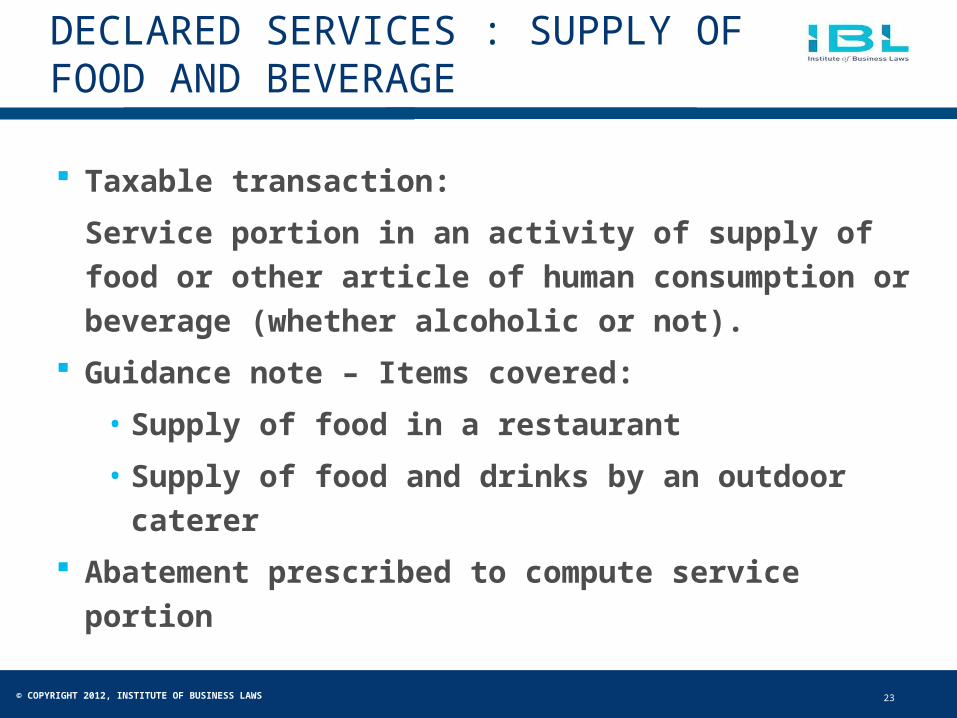

DECLARED SERVICES : SUPPLY OF FOOD AND BEVERAGE

Taxable transaction:

Service portion in an activity of supply of food or other

article of human consumption or beverage (whether

alcoholic or not).

Guidance note – Items covered:

• Supply of food in a restaurant

• Supply of food and drinks by an outdoor caterer

Abatement prescribed to compute service portion

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 24

DECLARED SERVICES : TEMPORARY TRANSFER OF IPR

Temporary transfer or permitting the use or enjoyment of any

IPR,

IPR not defined

Guidance Note:

• Phrase ‘IPR’ is to be understood as done in normal trade

parlance

• IPR to include:

• Copyrights,

• Patents,

• Trademarks,

• Design,

• Any other similar right to intangible property

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 25

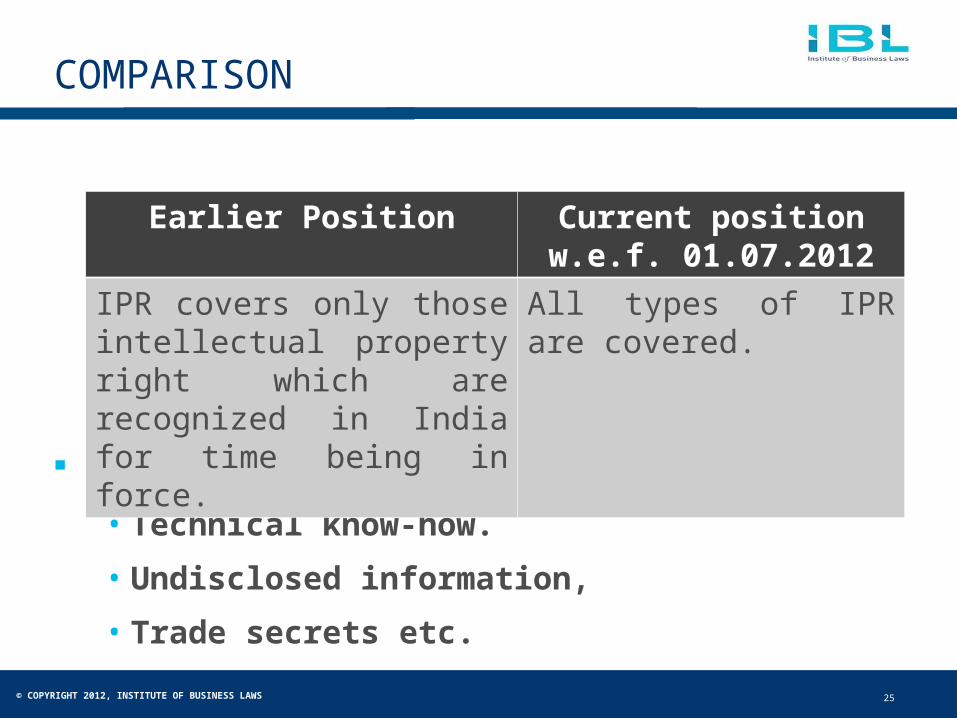

COMPARISON

Status of :

• Technical know-how.

• Undisclosed information,

• Trade secrets etc.

Earlier Position Current position w.e.f. 01.07.2012

IPR covers only those intellectual property right which are recognized in India for time being in force.

All types of IPR are covered.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 26

DECLARED SERVICES : SERVICE PORTION IN A WORKS CONTRACT

Works contract defined:

“a contract wherein transfer of property in goods involved in the

execution of such contract is leviable to tax as sale of goods and

such contract is for the purpose of carrying out construction,

erection, commissioning, installation, completion, fitting-out,

improvement, repair, renovation, alteration of any movable or

immovable property or for carrying out any other similar activity or

a part thereof in relation to such property."

Works contract definition amended to include both movable and

immovable property.

Pure labour contracts not covered here

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 27

DECLARED SERVICES : WORKS CONTRACT

Deletion of Notification

No.12/2003-ST

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 28

DECLARED SERVICES : REFRAIN FROM AN ACT ETC.

Entry covers:

• Agreeing to an obligation to refrain from an act,

• Agreeing to an obligation to tolerate an act or a situation,

• Agreeing to the obligation to do an act

Non-compete fees etc taxable

Amount charged for non-lifting desired quantity?

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 29

NEGATIVE LIST OF SERVICES

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 30

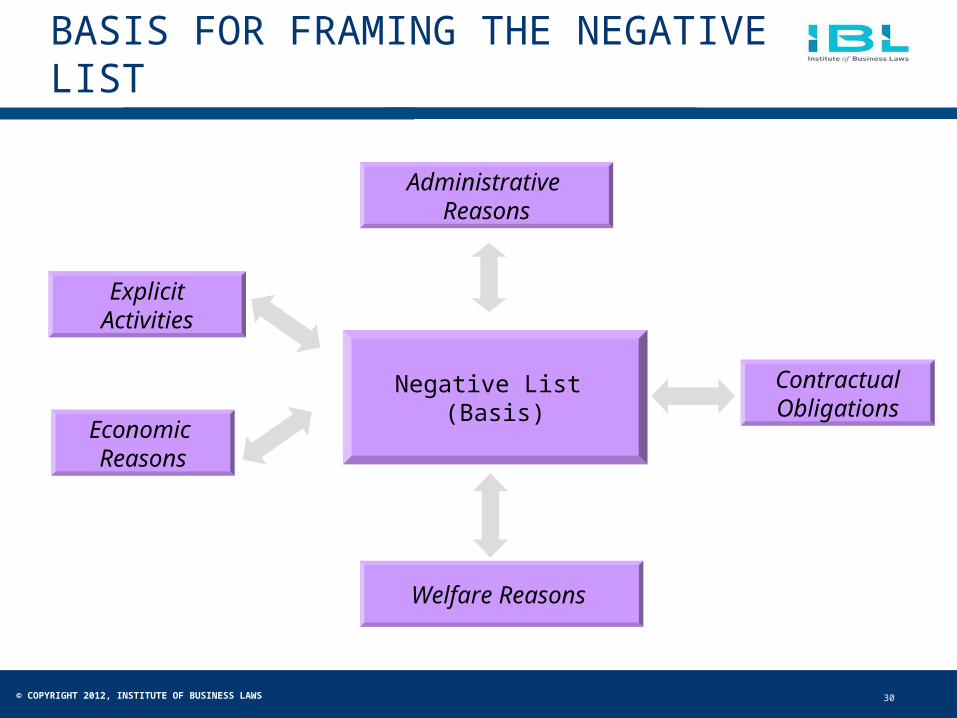

BASIS FOR FRAMING THE NEGATIVE LIST

Administrative Reasons

Welfare Reasons

Economic Reasons

ExplicitActivities

ContractualObligations

Negative List (Basis)

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 31

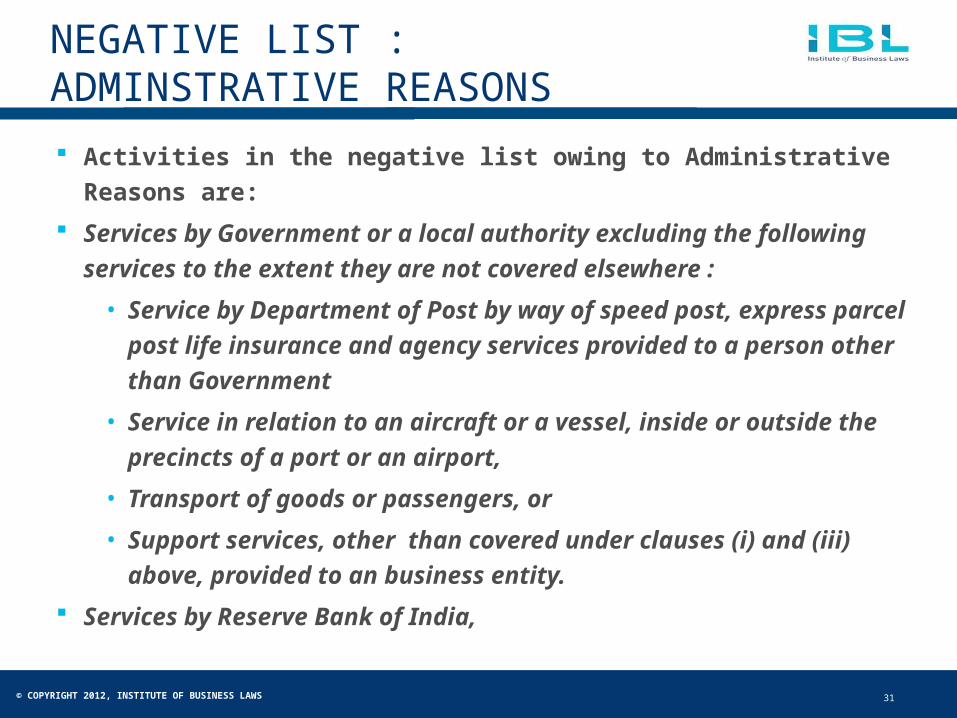

NEGATIVE LIST : ADMINSTRATIVE REASONS

Activities in the negative list owing to Administrative Reasons are:

Services by Government or a local authority excluding the

following services to the extent they are not covered elsewhere :

• Service by Department of Post by way of speed post, express

parcel post life insurance and agency services provided to a

person other than Government

• Service in relation to an aircraft or a vessel, inside or outside

the precincts of a port or an airport,

• Transport of goods or passengers, or

• Support services, other than covered under clauses (i) and (iii)

above, provided to an business entity.

Services by Reserve Bank of India,

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 32

NEGATIVE LIST : CONTRACTUAL OBLIGATIONS

Activities in the negative list owing to

Contractual obligations are :

Services by a foreign diplomatic mission located

in India

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 33

NEGATIVE LIST : WELFARE REASONS

Activities in the negative list owing to Welfare Reasons

are :

Service by way of:

• Pre-school education and education upto higher

secondary education or equivalent,

• Education as a part of a curriculum for obtaining a

qualification recognized by any law for the time being in

force,

• Education as a part of approved vocational education

course.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 34

NEGATIVE LIST : WELFARE REASONS

Services of transportation of goods :• By road except the service of -

• A goods transportation agency, or

• A courier agency.

• By an aircraft or a vessel from a place outside India up to the

custom station of clearance in India, or

• By an inland waterways

funeral, burial, crematorium or mortuary services including

transportation of deceased

Services by way of renting of residential dwellings for use

as residence

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 35

NEGATIVE LIST : ECONOMIC REASONS

Economic Reasons are :

Transmission or distribution of electricity by an electricity

transmission or distribution utility,

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 36

NEGATIVE LIST : EXPLICT ACTIVITIES

Explicit activities are :

Trading of goods

Service by way of access to a road or a bridge on

payment of toll charges,

Betting, gambling or lottery,

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 37

NEGATIVE LIST : EXPLICT ACTIVITIES

Admission to entertainment event or access to

amusement facilities

Selling or space or time slots for advertisements

other than advertisements broadcast by radio or

television Online advertisement ?

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 38

NEGATIVE LIST : EXPLICT ACTIVITIES

Any process amounting to manufacture or

production of goods Process on which duties of excise leviable under Section 3 ; or

Duties of excise leviable under any State Act;

Any process amounting to manufacture of alcoholic liquor of human

consumption, opium, Indian hemp and other narcotics drugs and narcotics

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 39

NEGATIVE LIST : OTHER ITEMS

Other activities mentioned in the negative list are :

Service by way of:

• Extending deposit, loans or advances in so far as the

consideration is represented by way of interest or

discount,’

• Inter-se sale or purchase of foreign currency amongst

banks or authorized dealer of foreign exchange or

amongst banks and such dealers

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 40

RULES OF

INTERPRETATION

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 41

CLASSIFICATION OF SERVICES

Section 66F replaces Section 65A

1 - Reference to main service not to include reference to

service used for providing main service

• Sub-contractor to main Contractor?

2 - Specific description to prevail over general

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 42

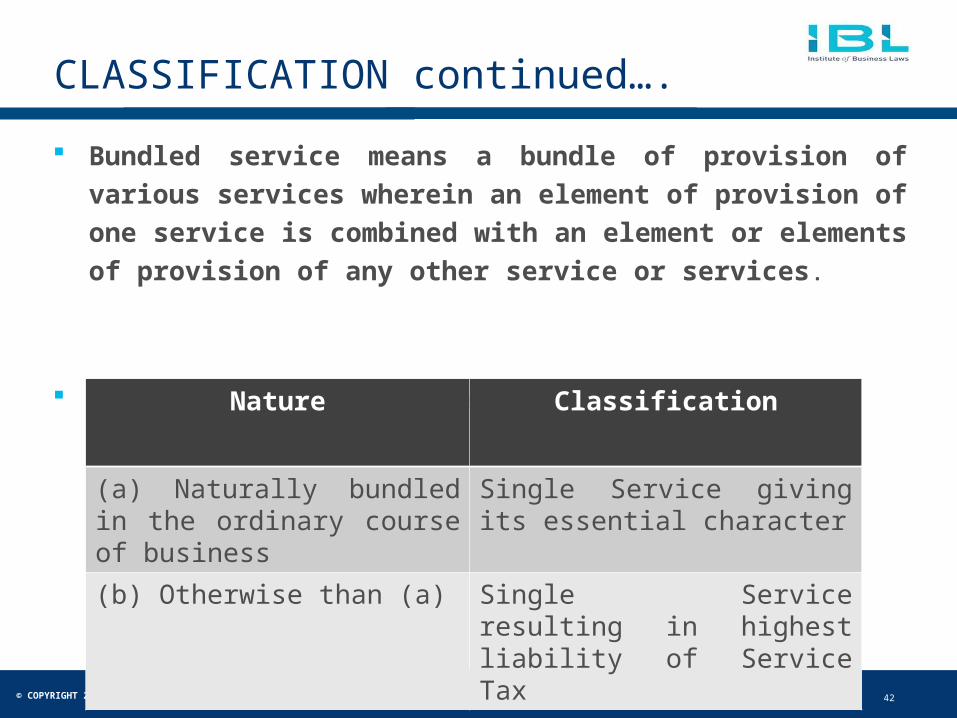

CLASSIFICATION continued….

Bundled service means a bundle of provision of various

services wherein an element of provision of one service is

combined with an element or elements of provision of any other

service or services.

Rule 3 - Bundled services

Nature Classification

(a) Naturally bundled in the ordinary course of business

Single Service giving its essential character

(b) Otherwise than (a) Single Service resulting in highest liability of Service Tax

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 43

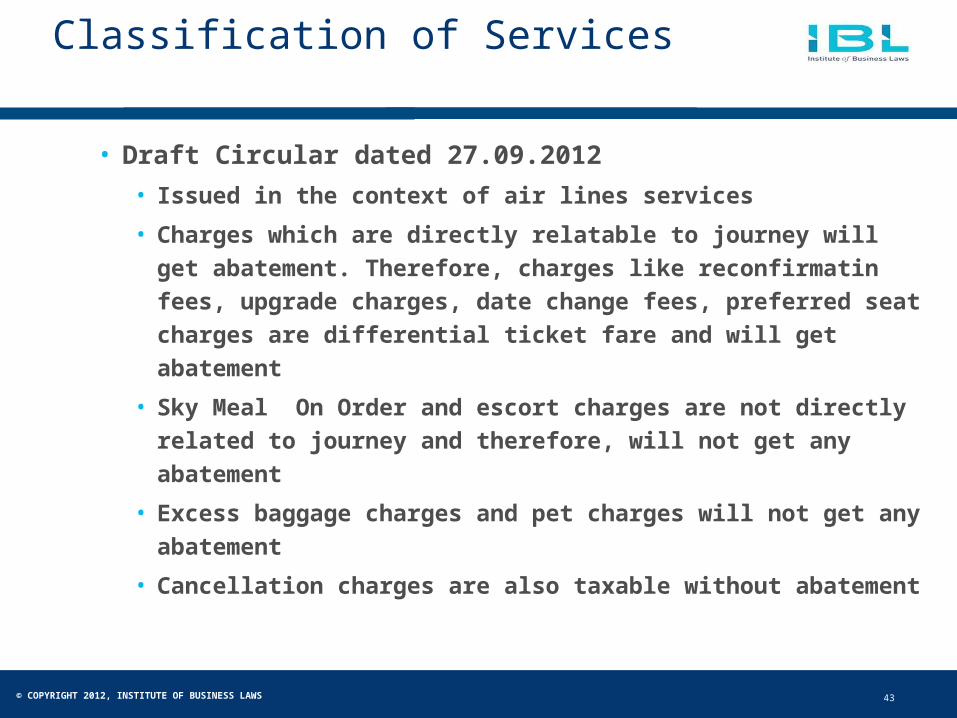

Classification of Services

• Draft Circular dated 27.09.2012

• Issued in the context of air lines services

• Charges which are directly relatable to journey will get abatement.

Therefore, charges like reconfirmatin fees, upgrade charges, date

change fees, preferred seat charges are differential ticket fare and

will get abatement

• Sky Meal On Order and escort charges are not directly related to

journey and therefore, will not get any abatement

• Excess baggage charges and pet charges will not get any

abatement

• Cancellation charges are also taxable without abatement

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 44

Classification of Services

• Some Important ECJ Rulings

• Card Protection Plan (Case No. C-349/1996)

• Societe Thermale d’Eugenie-les-Bains Vs. Ministere de

l’Economie, des Finances et del’Industrie (Case C-277/05)

• B.A.Z. Bausystem AG Vs. Finanzamt Munchen Fur

Korperschaften (1982) 3 CMLR 688

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 45

REVERSE CHARGE

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 46

REVERSE CHARGE

• Notification No.30/2012-ST replaces Notification No.36/2004-ST for

specifying person liable for payment of service tax in respect of

services provided or agreed to be provided by:

• Insurance agent to person carrying on the insurance business,

• Goods transportation agency in respect of transportation of goods by road,

where the person liable to pay freight is one of the specified persons,

• Sponsorship service to body corporate or partnership firm in taxable territory,

• Credit of inputs opened except goods specified in Chapter 1 to 22.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 47

REVERSE CHARGE

• By arbitral tribunal or an individual advocate or a firm of advocates to a

business entity

• Support service provided by Government or local authority, to any

business entity located in taxable territory, excluding:

• Renting of immovable property,

• Speed post, transport services and services in relation to aircraft or vessel

in certain cases

• Service provided by way of :

• Renting of motor vehicle designed for carrying passengers to any person

not in similar line of business,

• Supply of manpower,

• Service portion of Works contract (Notified services)

By an individual, HUF, Partnership Firm or Association of persons to a business entity

registered as body corporate in a taxable territory

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 48

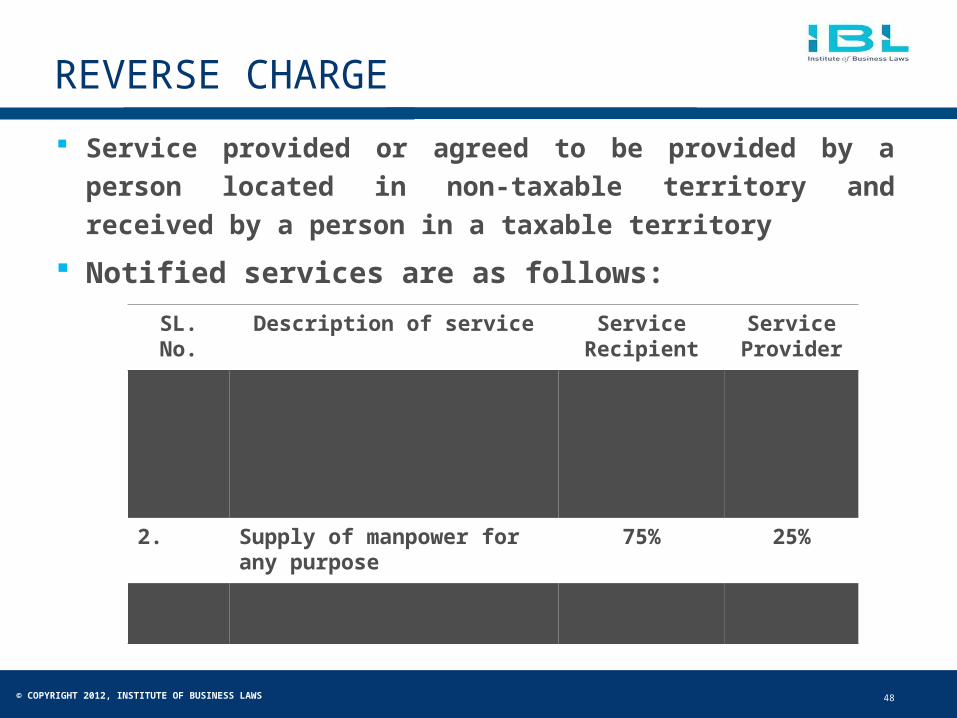

REVERSE CHARGE

Service provided or agreed to be provided by a person located

in non-taxable territory and received by a person in a taxable

territory

Notified services are as follows:

SL. No. Description of service Service Recipient

Service Provider

1. Renting of a motor vehicle designed to carry passengers:•With abatement•Without abatement

100%40%

Nil60%

2. Supply of manpower for any purpose

75% 25%

3. Service portion in Works contract service

50% 50%

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 49

REVERSE CHARGE

Whether service provider to

charge full rate of tax?

Payment of entire tax by service

provider:

- Service recipient absolved?

Different options be exercised by

provider and receiver?

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 50

VALUATION

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 51

VALUATION : RULE 2A

W.e.f. July 1, 2012

Works Contract Service

• Rule 2A substituted

o Value of service = Gross amount charged less

actual value of goods transferred in execution

• Actual value of goods for VAT purposes to be

considered for determining material value

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 52

VALUATION: RULE 2A

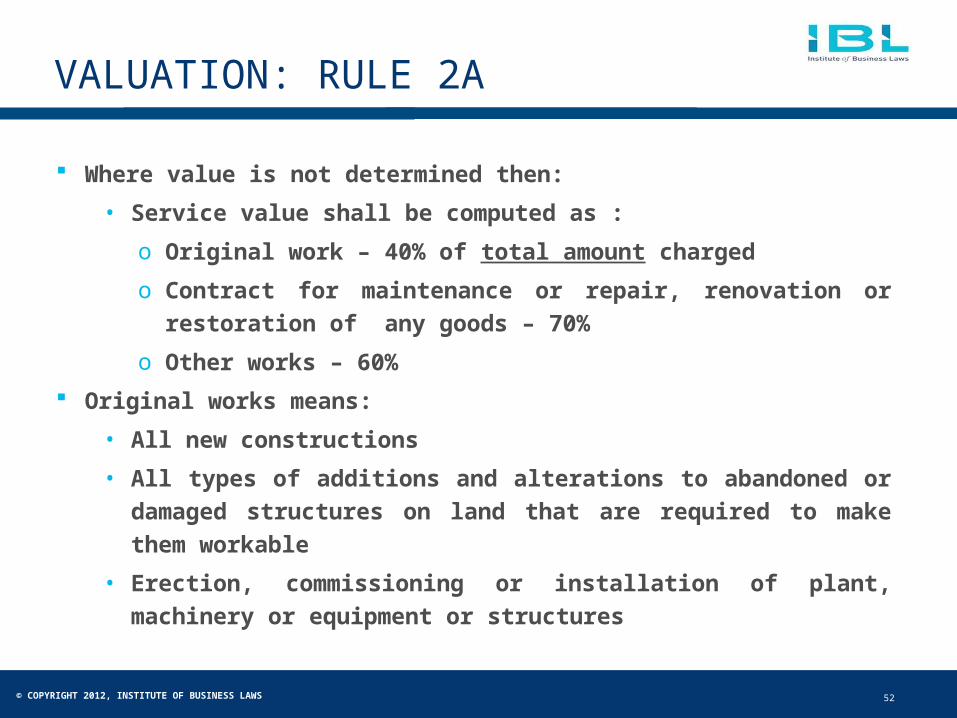

Where value is not determined then:

• Service value shall be computed as :

o Original work – 40% of total amount charged

o Contract for maintenance or repair, renovation or restoration of

any goods – 70%

o Other works – 60%

Original works means:

• All new constructions

• All types of additions and alterations to abandoned or damaged

structures on land that are required to make them workable

• Erection, commissioning or installation of plant, machinery or

equipment or structures

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 53

VALUATION: RULE 2A

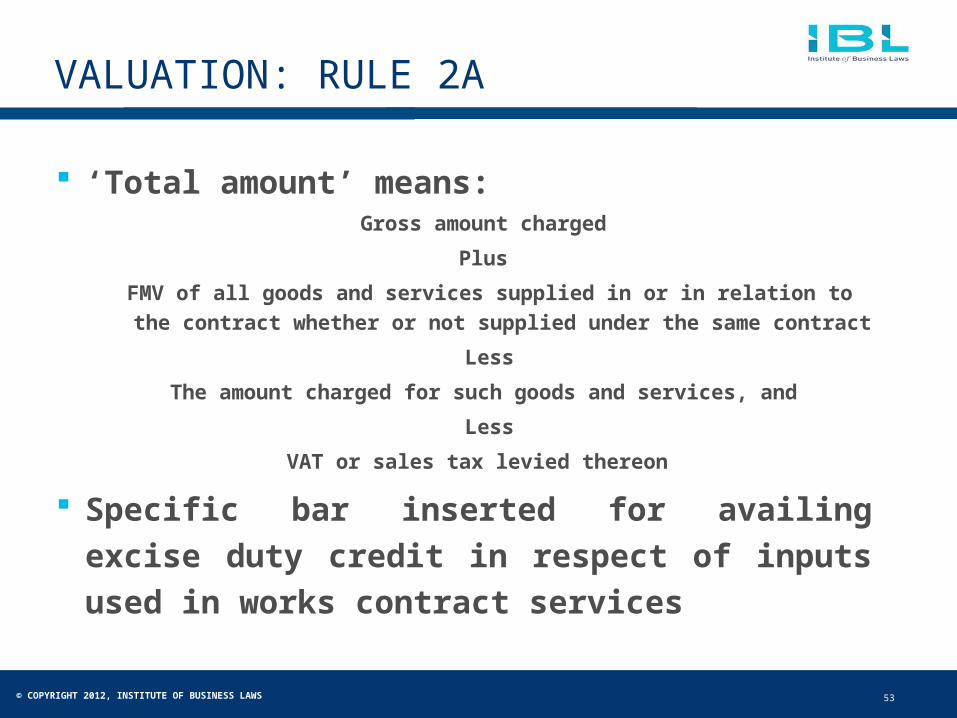

‘Total amount’ means: Gross amount charged

Plus

FMV of all goods and services supplied in or in relation to the contract

whether or not supplied under the same contract

Less

The amount charged for such goods and services, and

Less

VAT or sales tax levied thereon

Specific bar inserted for availing excise duty

credit in respect of inputs used in works contract

services

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 54

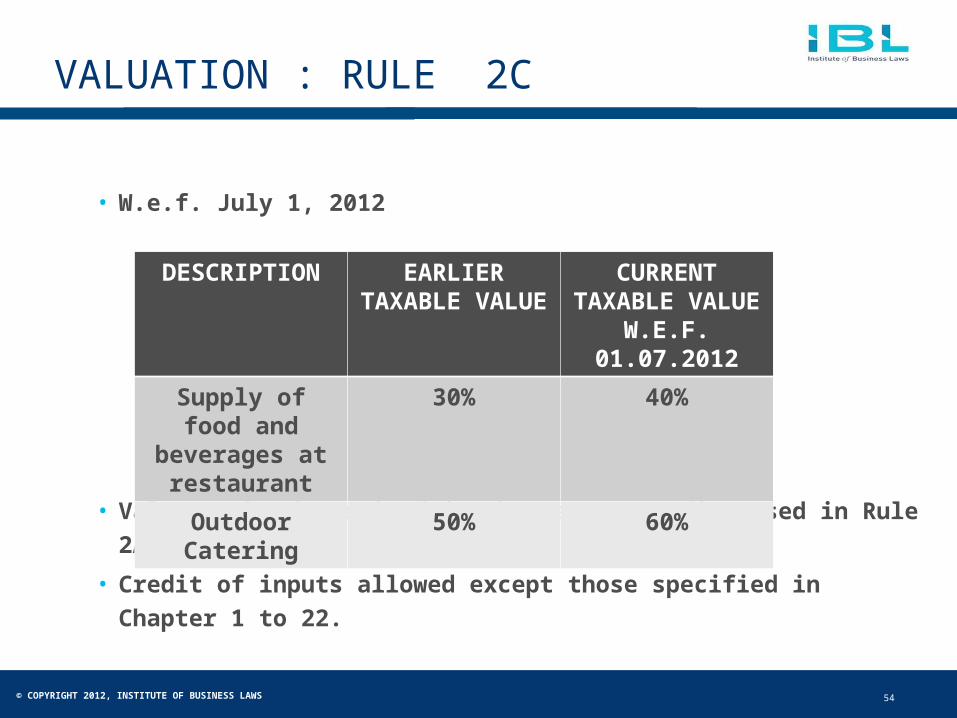

VALUATION : RULE 2C

• W.e.f. July 1, 2012

• Value to be determined in the manner as discussed in Rule 2A

• Credit of inputs allowed except those specified in Chapter 1 to

22.

DESCRIPTION EARLIER TAXABLE

VALUE

CURRENT TAXABLE

VALUE W.E.F. 01.07.2012

Supply of food and beverages at restaurant

30% 40%

Outdoor Catering

50% 60%

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 55

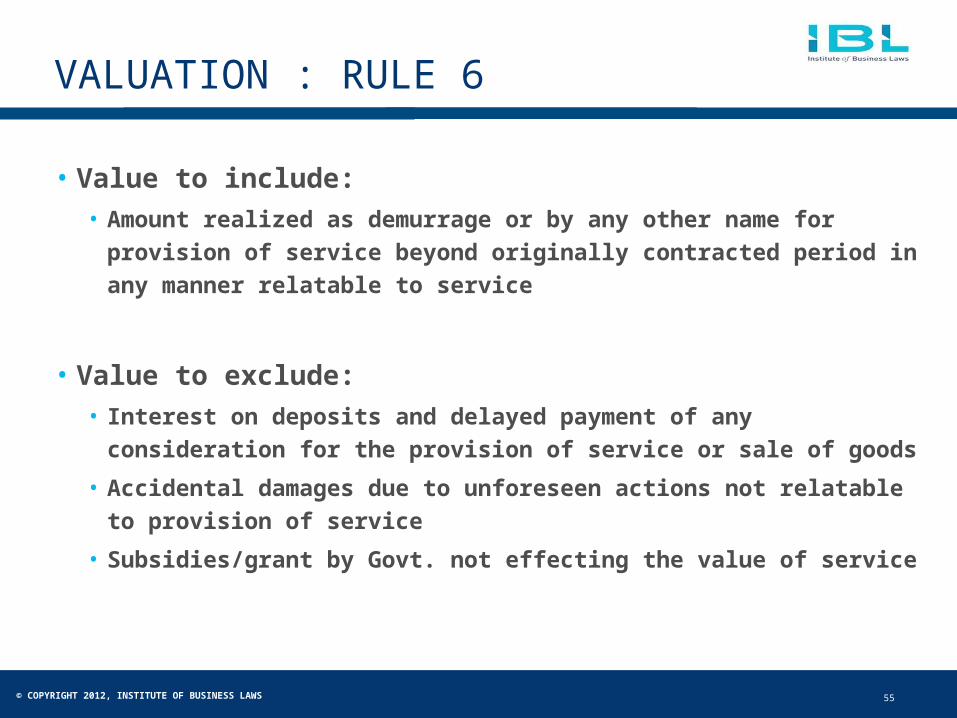

VALUATION : RULE 6

• Value to include:• Amount realized as demurrage or by any other name for

provision of service beyond originally contracted period in any

manner relatable to service

• Value to exclude:• Interest on deposits and delayed payment of any

consideration for the provision of service or sale of goods

• Accidental damages due to unforeseen actions not relatable to

provision of service

• Subsidies/grant by Govt. not effecting the value of service

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS 56

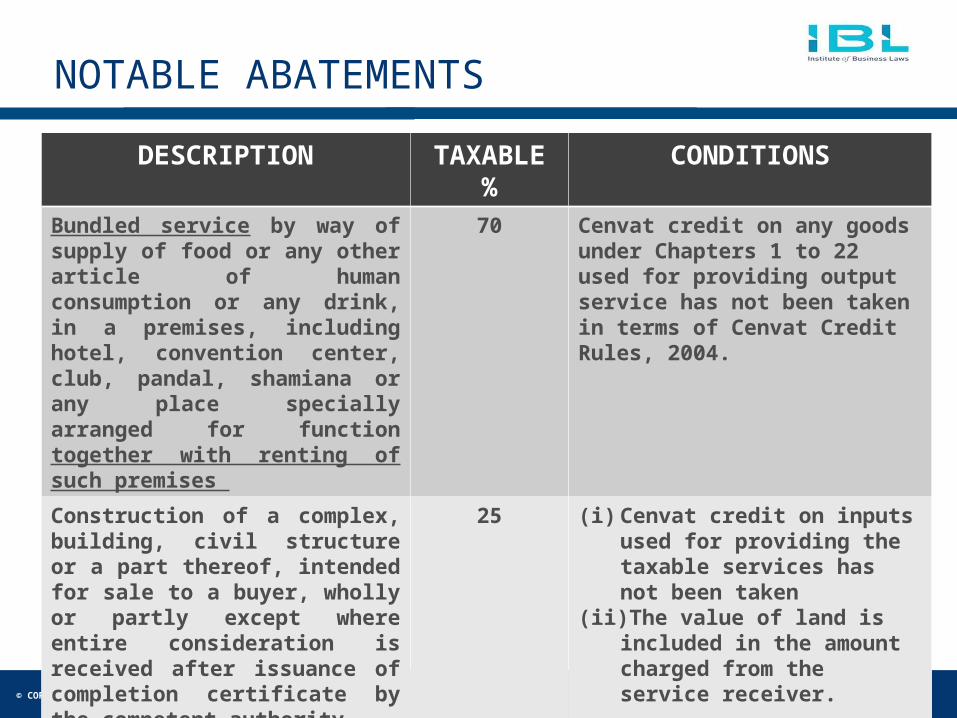

NOTABLE ABATEMENTS

DESCRIPTION TAXABLE %

CONDITIONS

Bundled service by way of supply of food or any other article of human consumption or any drink, in a premises, including hotel, convention center, club, pandal, shamiana or any place specially arranged for function together with renting of such premises

70 Cenvat credit on any goods under Chapters 1 to 22 used for providing output service has not been taken in terms of Cenvat Credit Rules, 2004.

Construction of a complex, building, civil structure or a part thereof, intended for sale to a buyer, wholly or partly except where entire consideration is received after issuance of completion certificate by the competent authority.

25 (i) Cenvat credit on inputs used for providing the taxable services has not been taken

(ii) The value of land is included in the amount charged from the service receiver.

© COPYRIGHT 2012, INSTITUTE OF BUSINESS LAWS

Contact Details Our Knowledge Partner

NEW DELHI

5, Jangpura Extension

Link Road, New Delhi - 110 018

Phone: +91 (11) 4129 9810/800

MUMBAI

401 - 404, Kakad Chambers

132, Dr. Annie Besant Road, Worli

Mumbai - 400 018

Phone: +91 (22) 2491 4382/84/86

HYDERABAD

‘Hastigiri’

5-9-163, Chapel Road, Opp. Methodist Church,

Nampally, Hyderabad - 500001

Phone: +91 (40) 2323 4924/25

BENGALURU

4th Floor World Trade Center,

Malleswaram,

Bangalore - 560 055

Phone: +91 (080) 41717777

CHENNAI

2, Wallace Garden 2nd Street

Chennai - 600 006

Phone: +91 (44) 43961600, 28334700-2

AHMEDABAD

B-334 (3rd floor), SAKAR-VII, Nehru Bridge Corner,

Ashram Road, Ahmedabad-380 009

Phone: +91 (79) 4001 4500

PUNE

EBONY Meeting Room,

Ist floor Apartment Section of Hyatt Regency

Weikfield IT Park, Nagar Road

Pune 411014, Maharashtra

Thank you