Common application issues of HKFRS 3 ...

40

Common application issues of HKFRS 3 Business Combinations www.pwchk.com 11 June 2021

Transcript of Common application issues of HKFRS 3 ...

Common application issues of HKFRS 3 Business Combinations

www.pwchk.com

11 June 2021

PwC

Overall recap of HKFRS 3 and its amendment

2

Definition of a Business

Identifying the Acquirer

Determining the Acquisition Date

Identifying Separate Transaction,

Recognising and measuring

Consideration Transferred

Recognising and measuring Assets and

Liabilities

Recognising and measuring Non-

controlling Interest

Subsequent measurement and

accountingDisclosure Latest Development

PwC

Agenda

3

I. Business or asset?Identifying the

AcquirerDetermining the Acquisition Date

II. Part of BC or separate transaction?

III. Fair value or not?Recognising and measuring Non-

controlling Interest

Subsequent measurement and

accountingDisclosure IV. What is Next?

PwC

I. Business or asset?

4

PwC

What is Business Combination?

5

AcquirerAcquiree(Business)

Control

Introduction of new assessments on business VS asset deal- Concentration test (single asset or group of similar assets)

- Substantive assessment (process)

PwC

Concentration test

6

Fair value of consideration

Fair value of liabilities assumed

Non-controlling

interest

Previously held interest

- Goodwill resulting from the effects of deferred tax liabilities

- Deferred tax assets- Cash and cash

equivalents

Fair value of gross assets acquired in

Business Combinations Fair value of

Gross Assetsconsidered in

concentration test

PwC

Concentration test (Continued)

7

Is it a single identifiable asset? a

group of similar identifiable assets?

Nature and risk associated

PwC

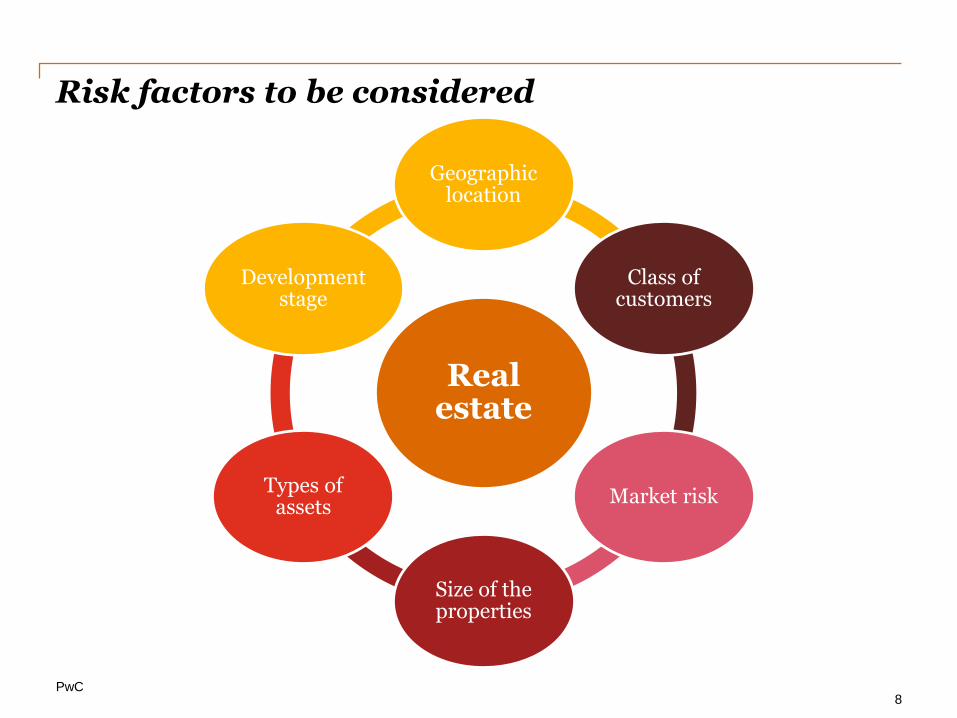

Risk factors to be considered

8

Real estate

Geographic location

Class of customers

Market risk

Size of the properties

Types of assets

Development stage

PwC

Common differences in accounting between a business combination and an asset acquisition

9

Measurement of assets and liabilities

Goodwill/Bargain purchase

Contingent liabilities

Transaction costs

Deferred tax

Contingent consideration

Non-controlling

interest

Previously held non-controlling

interest

PwC

Hot topics on asset acquisitionObtaining control over a previously held joint operation which is not a business

10

Should we remeasure the previously held

interest?

Group of assets(Joint operation)

Joint investor

Joint investor

Control passed…A. Yes

B. No

C. Policy choice

PwC

Hot topics on asset acquisition (Continued)Step acquisition of a corporate wrapper

11

Should we remeasure the previously held

interest?

Group of assets

Joint investor

Joint investor

Control passed…

Corporate Wrapper

(Joint Venture)

A. Yes

B. No

C. Policy choice

PwC

Hot topics on asset acquisition (Continued)Accounting for NCI on an asset acquisition

12

Corporate Wrapper

Holding company

NCI

Should we account for NCI?

Post-implementation Review of IFRS 10, IFRS 11 and IFRS 12

A. Yes

B. No

C. Seek for guidance from the IASB to fill the gap

PwC

Hot topics on asset acquisition (Continued)Selling a corporate wrapper in the real estate industry

13

HKFRS 15

HKFRS 10

PwC

II. Part of business combination or separate transaction?

14

PwC

What is part of business combination?

15

Buyer Seller

Exchange for business

Business(assets, liabilities, non-

controlling interest)

Consideration

Part of Business Combination

PwC

What are indicators for separate transactions?

16

The reasons for the transaction

Who initiated the transaction

The timing of the transaction

)“…, where it has been entered into by or on behalf of the buyer or for the benefit of the buyer or the combined entity.”

A transaction is more likely to be a separate transaction

PwC

Pre-existing relationships

17

Settlement of relationship

At FV Lower of:

Favourable/ unfavourable element

Settlement provision in contract

Contractual relationship

No Yes

1 2

PwC

Pre-existing relationships (Continued)Example… Law suit provision

18

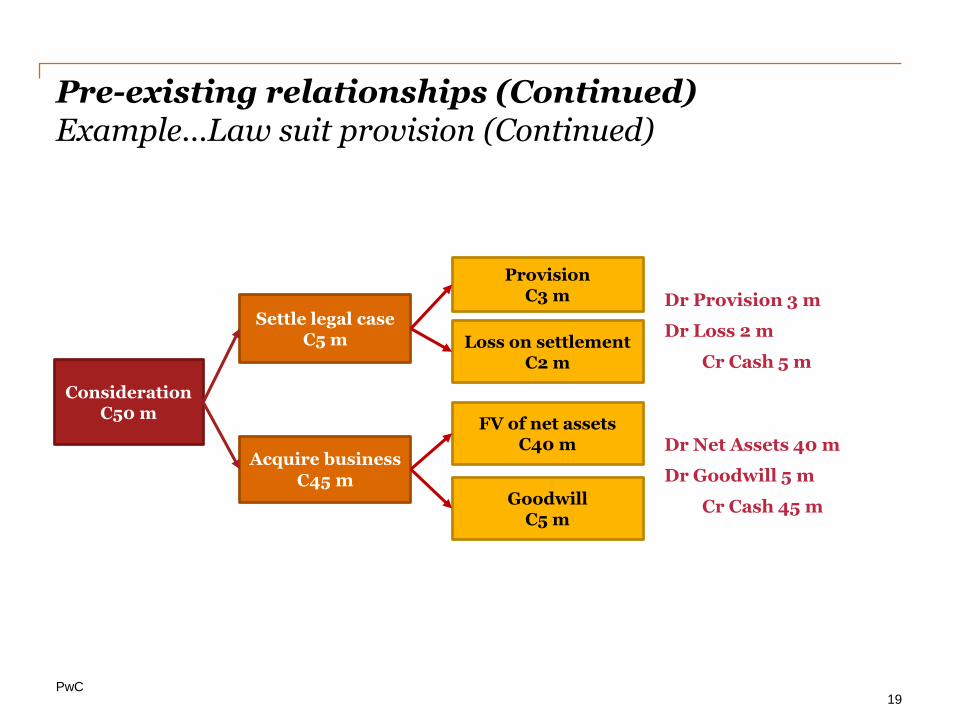

Background

• Entity A is a defendant in the lawsuit against Entity B. Litigation provision in Entity A’s books is C3 million.

• Entity A pays C50 million to acquire Entity B (business)

• Fair value of the law suit is C5 million.

• Fair value of B’s net assets is C40 million.

What would the accounting look

like?

PwC

Pre-existing relationships (Continued)Example…Law suit provision (Continued)

19

Consideration C50 m

Settle legal case C5 m

Acquire business

C45 m

Provision C3 m

Loss on settlement C2 m

FV of net assets C40 m

Goodwill C5 m

Dr Provision 3 m

Dr Loss 2 m

Cr Cash 5 m

Dr Net Assets 40 m

Dr Goodwill 5 m

Cr Cash 45 m

PwC

Pre-existing relationships (Continued)Example…Re-acquired franchise

20

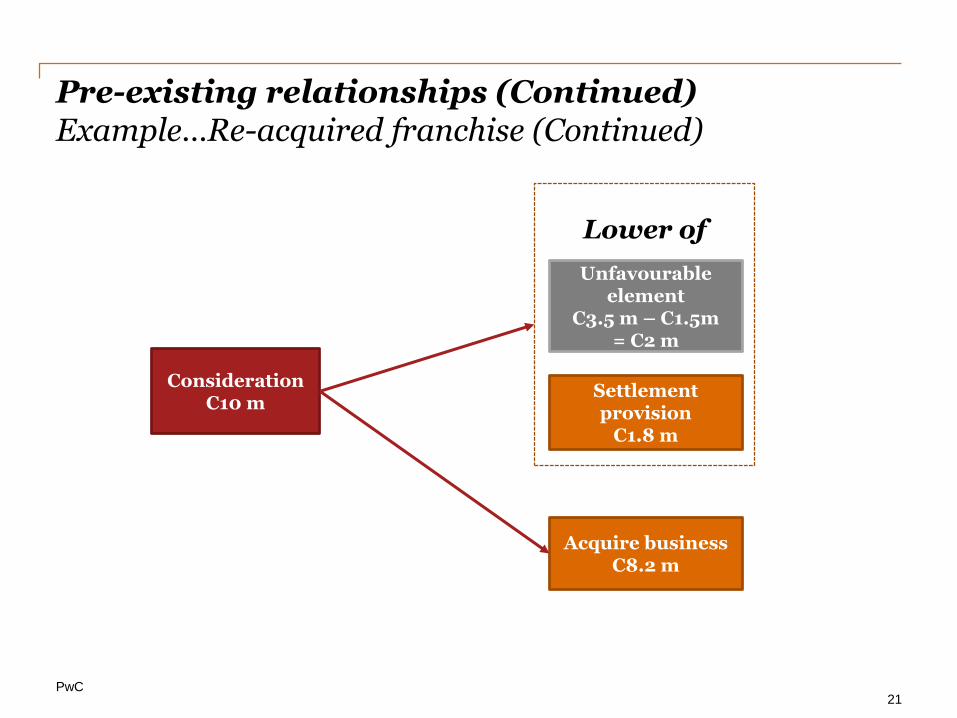

Background

• Entity C acquires Entity D at cash of C10 million.

• Entity C had earlier granted a 10-year franchise to Entity D at full payment of C2.5 million. The contract price of the franchise allocated to the remaining 6-year franchise was C1.5 million.

• The contract allows either party to terminate the franchise at settlement provision of C1.8 million.

• Under current economic conditions and at current prices, Entity C could grant a 6-year franchise for a price of C3.5 million.

How Entity C accounts for

the settlement of franchise

arrangement?

PwC

Lower of

Pre-existing relationships (Continued)Example…Re-acquired franchise (Continued)

21

Consideration C10 m

Unfavourable element

C3.5 m – C1.5m = C2 m

Acquire business C8.2 m

Settlement provision

C1.8 m

PwC

Contingent consideration or employee compensation?

22

Continuing employment

Remuneration level

Higher payment to employees

% of shares held by

employees

Consideration vs. value of the

business

Other agreements

Formula to calculate payment

Duration of continuing

employment

Employee compensation

vs. Cost of

consideration

PwC

Stay bonus arrangement

23

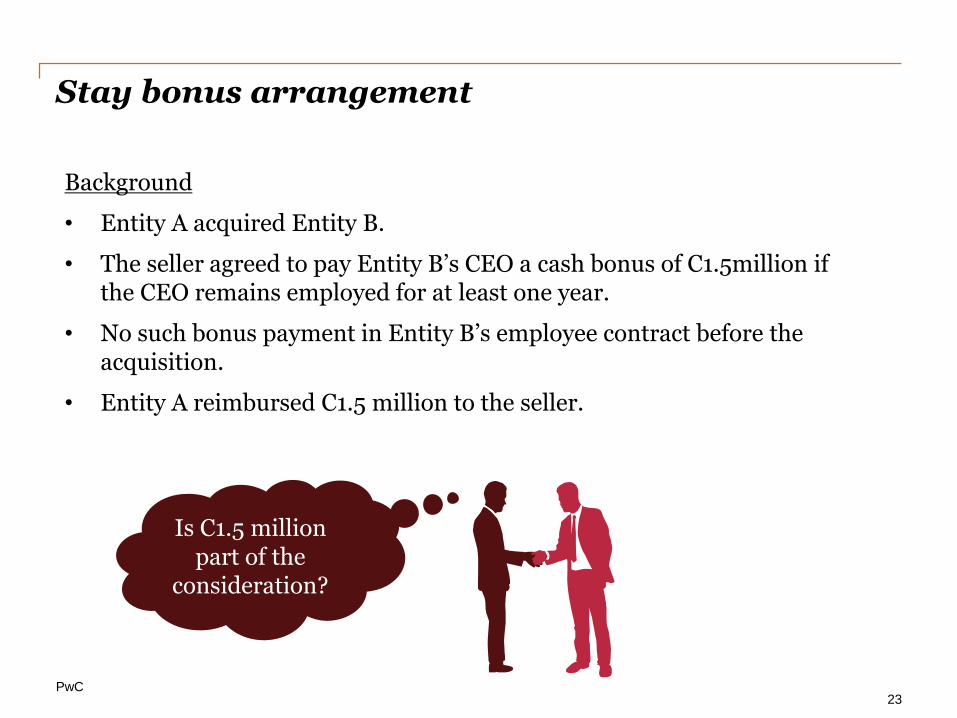

Background

• Entity A acquired Entity B.

• The seller agreed to pay Entity B’s CEO a cash bonus of C1.5million if the CEO remains employed for at least one year.

• No such bonus payment in Entity B’s employee contract before the acquisition.

• Entity A reimbursed C1.5 million to the seller.

Is C1.5 million part of the

consideration?

PwC

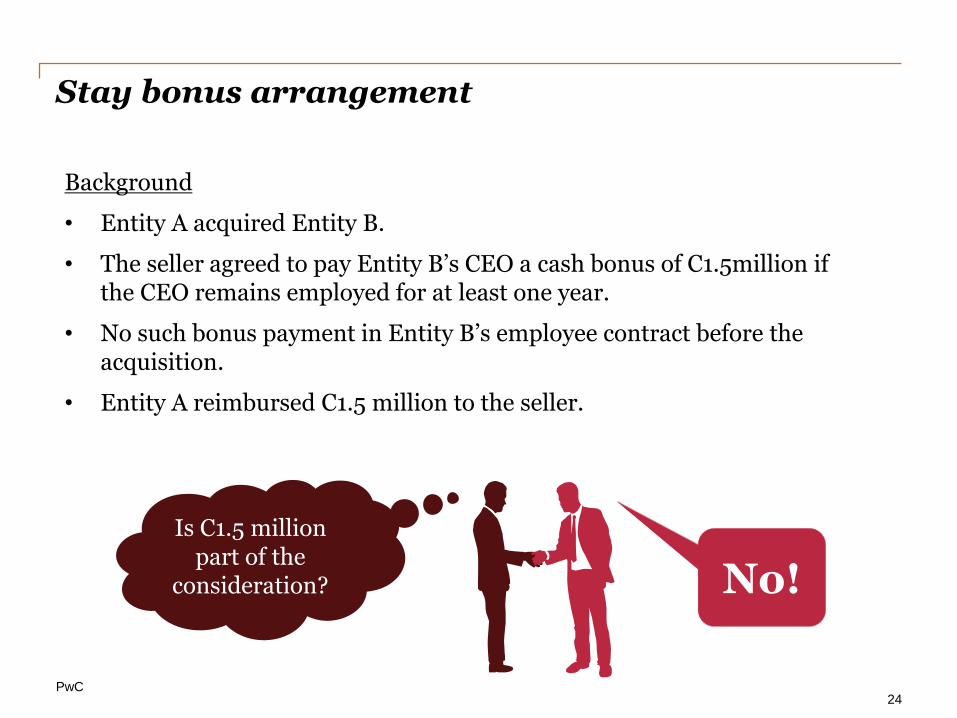

Stay bonus arrangement

24

Background

• Entity A acquired Entity B.

• The seller agreed to pay Entity B’s CEO a cash bonus of C1.5million if the CEO remains employed for at least one year.

• No such bonus payment in Entity B’s employee contract before the acquisition.

• Entity A reimbursed C1.5 million to the seller.

Is C1.5 million part of the

consideration? No!

PwC

Decision tree for allocating consideration

Identify separate transactions

• Pre-existing relationship; • Employee compensation; or

• Share-based payment?

Follow application guidance in HKFRS 3

para B52-B62

Other transactions

NoYes

Identify amount not part of BC and account for in accordance

with the relevant HKFRSs[HKFRS 3 para 51]

PwC

Illustration – Acquire a retail business withlicensing trademarks at nil consideration

26

Remaining consideration >

FV of net identifiable assets

FV of net identifiable assets

(C9M) > Remaining

consideration (C8M)

Residual as goodwill

Allocate discount proportionally to

FV of the business (C9M) and separate transaction (C2M)

[HKFRS 3para 2(b)]

Other transaction(Licensing trademark from

the seller for 3 years )

Account for in accordance with the

relevant HKFRSs[HKFRS 3 para 51]

Allocate a portion of consideration paid for licensing at fair

value (C2M)

Entity A acquires retail business from Entity B

and a separate licence at a consideration of C10M…

C2M

C9M

PwC

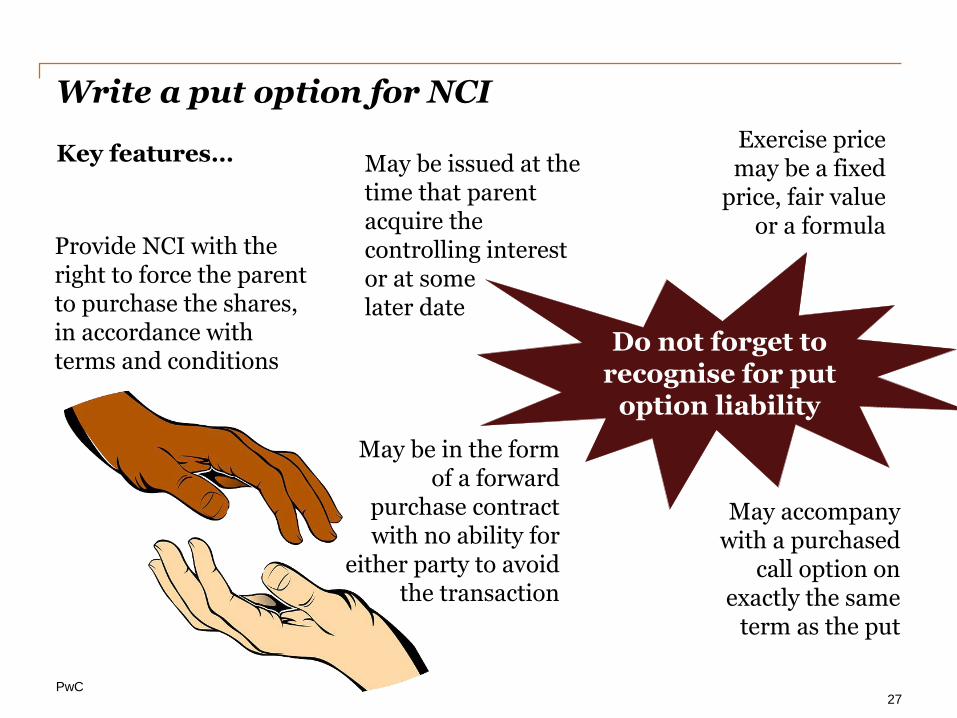

Write a put option for NCI

27

Provide NCI with the right to force the parent to purchase the shares, in accordance with terms and conditions

Do not forget to recognise for put

option liability

May be issued at the time that parent acquire the controlling interest or at some later date

Exercise price may be a fixed

price, fair value or a formula

May accompany with a purchased

call option on exactly the same

term as the put

May be in the form of a forward

purchase contract with no ability for

either party to avoid the transaction

Key features…

PwC

III. Fair value or not?

28

PwC

Which assets and liabilities are not measured at FV?

29

Employee benefits

Indemnification asset

Share-based payment

Contingent liabilities

Trade and other payables

Trade and other receivables Deferred tax

Assets held for sale

Inventories

Intangible assets

Property, plant and equipment

Bank borrowings

Leases (acquiree as lessee)

PwC

Which assets and liabilities are not measured at FV? (Continued)

30

Employee benefits

Indemnification asset

Share-based payment

Contingent liabilities

Trade and other payables

Trade and other receivables Deferred tax

Assets held for sale

Intangible assets

Property, plant and equipment

Bank borrowings

Inventories

Leases (acquiree as lessee)

PwC

Additional assets and liabilities may be recognised in the consolidated financial statements

31

Typical examples

Typical examples include:

• Certain identifiable intangible assets

• Deferred tax

• Contingent liabilities

PwC

Accounting for leases in which the acquiree is the lessee

Background

• An acquired entity leases its head office

• Rent for the next 5 years is fixed at C120K which is in excess of the rents payable on leases of comparable buildings at C100K at the time of the acquisition

• Assume 0% discount rate for simplicity

How should the acquirer recognise the right-of-use asset and lease liability?

32

Acquirer recognises the acquired lease liability AS IF the lease contract was A NEW LEASE at the acquisition date.

PwC

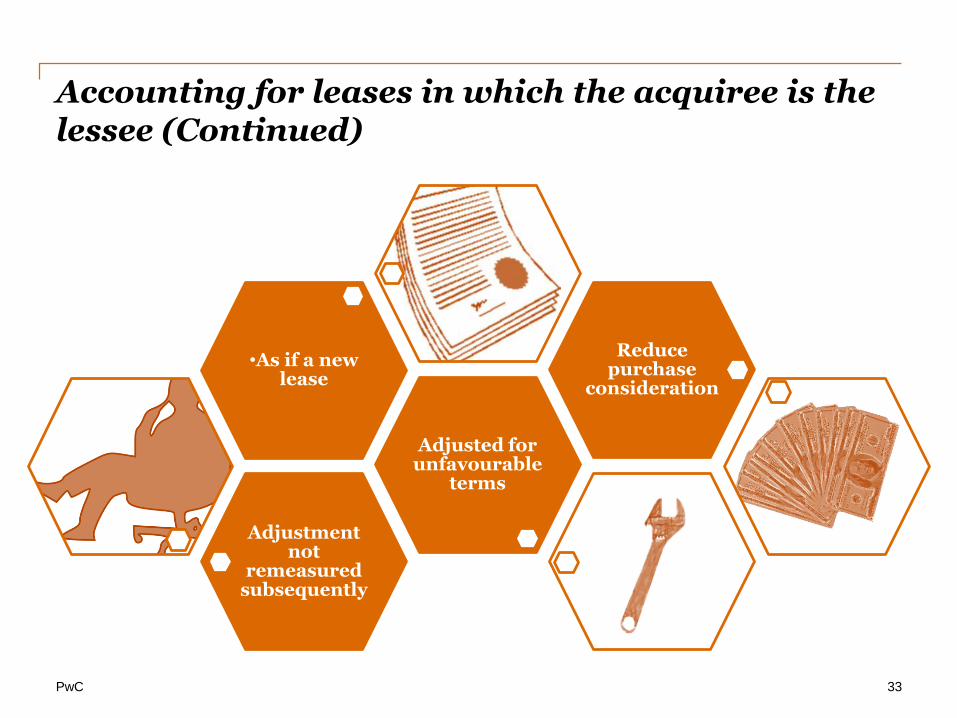

Accounting for leases in which the acquiree is the lessee (Continued)

33

Adjustment not

remeasured subsequently

Adjusted for unfavourable

terms

•As if a new lease

Reduce purchase

consideration

PwC

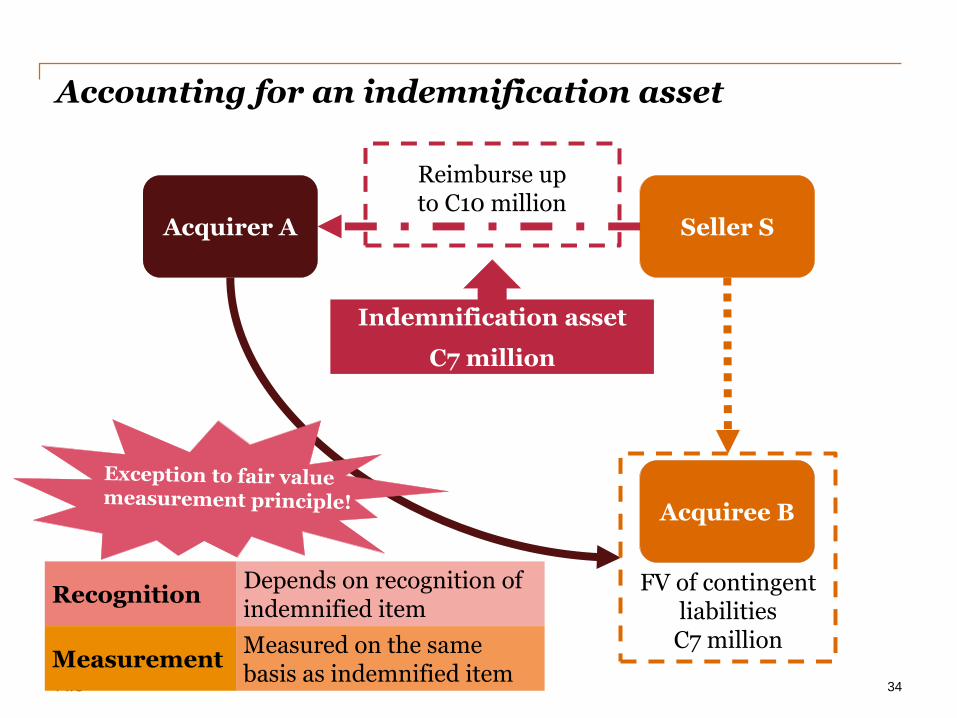

Accounting for an indemnification asset

34

Acquirer A Seller S

Acquiree B

FV of contingent liabilitiesC7 million

Reimburse up to C10 million

Indemnification asset

C7 million

RecognitionDepends on recognition of indemnified item

MeasurementMeasured on the same basis as indemnified item

PwC

IV. What is next?

35

PwC

BCUCC project

In November 2020, the International Accounting Standards Board (Board) published the Discussion Paper Business Combinations under Common Control…

36

PwC

BCUCC project (Continued)

37

Summary of the Board’s preliminary views…

To determine the accounting method- Are the receiving company’s shares traded in a public market? - Does the receiving company have non-related party NCI who

disagree to use book value method?

Book value method

Acquisition method

Consideration > FV of identified net assets

Goodwill

Consideration < FV of identified net assets

Contribution

No for both

Yes for either

PwC

BCUCC project (Continued)

38

Comment letter period is open until 1 September 2021!

PwC

Q&A

39

Thank you

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

© 2021 PwC. All rights reserved. Not for further distribution without the permission of PwC. “PwC” refers to the network of member firmsof PricewaterhouseCoopers International Limited (PwCIL), or, as the context requires, individual member firms of the PwC network. Eachmember firm is a separate legal entity and does not act as agent of PwCIL or any other member firm. PwCIL does not provide any services toclients. PwCIL is not responsible or liable for the acts or omissions of any of its member firms nor can it control the exercise of theirprofessional judgment or bind them in any way. No member firm is responsible or liable for the acts or omissions of any other member firmnor can it control the exercise of another member firm’s professional judgment or bind another member firm or PwCIL in any way.