بسم الله الرحم الرحیم

14

م ر ل ه ا ل ل م ا م ی ح ر ل ا

-

Upload

dennis-walters -

Category

Documents

-

view

15 -

download

1

description

بسم الله الرحم الرحیم. The 10 th Russian Petroleum & Gas congress / RPGC 2012. New Roles for Iranian companies in oil & Gas activities ,Necessity of the International interactions & Sadid Industrial Group’s new direction. Dr. Gholam reza Manouchehri - PowerPoint PPT Presentation

Transcript of بسم الله الرحم الرحیم

بسم الله الرحم الرحیم

New Roles for Iranian companies in oil & Gas activities ,Necessity of the International interactions

& Sadid Industrial Group’s new direction.

Dr. Gholam reza ManouchehriAdviser to NIOC managing Director CEO of Sadid industrial group

2012-06-27

The 10th Russian Petroleum & Gas congress / RPGC 2012

Contents

1.Huge oil & Gas potentials in Iran.

2 .Private sector’s recent approach in the Iranian oil & Gas activities.

3.Necessity of diversity and pluralization in Iran's oil & gas related companies.

4.Institutional deficiencies of private oil and gas companies in Iran.

5 .Cooperation and Partnership with Russian companies.

6.Sadid Industrial Group capabilities and partnership opportunities.

7 .Enhancement of Sadid I.G. presence in the Iranian oil and gas sector.

introductionThe 10th Russian Petroleum & Gas congress

Russia as an economic and political superpower and an energy rich country is the appropriate place where oil and gas related companies can showcase their strengths, potentials and capabilities.

RPGC has provided a great opportunity for sadid in order to demonstrate its strengths and capabilities in the oil and gas sector and also amongst the most important players in the field of energy and petroleum. RPGC provides excellent networking that can bring new chances and prospects for Iranian companies and also the industry as a whole .

The past 10 years has been a missed opportunity for sadid, nevertheless Sadid will be present at RPGC for the years to come and it will offer its expertise and know-how to the rest of the industry and as well as expanding its knowledge through

employing the skills and innovations of its counterparts.

I .oil and gas potentials and challenges in Iran

1 .17% of the world Gas reserves amounting to 34 trillion cubic meter (TCM) belongs to Iran.

2 .10.5% of the world oil reserves amounting to 155 billion barrel belongs to Iran.

3.Iran has the largest reserves of hydrocarbon in the world ( oil & gas accumulated-equivalent reserves ) exceeding to 355 billion barrels.

4.only 21% of total the total Iranian hydrocarborn (exploitable) has been exploited during the last hundred years and almost 79% of that has been remained and could be available in the future.

I .oil and gas potentials in Iran and challenges for development

5.The reserve to production ratio in Iranian oil fields is 89% that shows a high capacity for production enhancement in the future.

7 .The growth of oil & gas consumption in Iran is very high, which makes Iran the fourth largest consumer of natural gas in the world.

6.The average rate of Iranian oil recovery has reached to 29% which shows a non serious entrance into the second recovery and the third recovery and which again shows a huge volume of works that should be fulfilled .

II. A new approach to the Iranian oil and gas activities by private sector.

1 .Implementation of the principal 44 of the Iranian Constitution concerned to authorization of investment in the oil fields to non-state owned companies and private companies.

2 .Privatization of National Iranian gas company's activities in the fields of investing and operation.

3 .Privatization of investment, exploitation, export & import of petrochemical.

II. A new approach to the Iranian oil and gas activities by private sector.

4 .Considering of non-state owned as reliable companies to become active in the development projects for upstream oil fields and their presence in the processes of exploration, development and operation according to the Fifth year development plan of the Islamic Republic of Iran.

5 .Entrance of Iranian and foreign private sector into oil & gas upstream activities in the form of new contract models which will guarantee the presence of the investment companies activities for a long term and also their interest in accordance with the volume of production ( Per barrel Ratio) according to a law which recently approved by the parliament.

III .Necessity of diversity and puloralization of oil & gas companies in Iran

1.Equipment manufacturing companies related to Drilling and offshore facilities.

2.Equipment manufacturing companies related to refineries and pipelines

3.Technical and service companies for drilling.

4.Engineering companies related to drilling and refinery consulting engineers.

7.Companies active in procurement ,commerce, sales and export & import.

5.E.P.C companies related to offshore facilities, refinery and surface facilities.

6.General contracting companies and developer’s companies.

8.Companies active in the fields of storage , transportation for crude and refined products.

9.Companies which provide financial , banking and credit facilities.

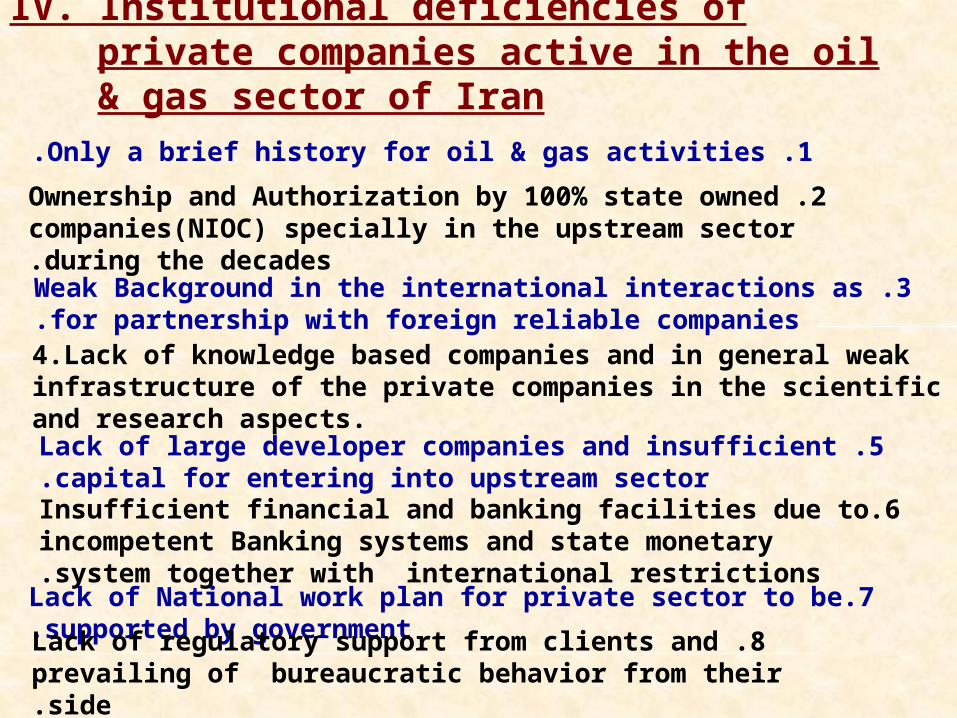

IV. Institutional deficiencies of private companies active in the oil & gas sector of Iran

1 .Only a brief history for oil & gas activities.

2 .Ownership and Authorization by 100% state owned companies(NIOC) specially in the upstream sector during the decades.

3 .Weak Background in the international interactions as for partnership with foreign reliable companies.

4.Lack of knowledge based companies and in general weak infrastructure of the private companies in the scientific and research aspects.

6.Insufficient financial and banking facilities due to incompetent Banking systems and state monetary system together with international restrictions.

5 .Lack of large developer companies and insufficient capital for entering into upstream sector.

7.Lack of National work plan for private sector to be supported by government.

8 .Lack of regulatory support from clients and prevailing of bureaucratic behavior from their side.

V. Partnership and participation with the Russian investment & technology companies

1 .Entrance of Russian companies into Iranian upstream projects of oil & gas by means of partnership with Iranian companies.

2 .Know-how transfer and granting License from reliable Russian institutions to the Iranian counterparts.

3.Russian companies participation in the manufacturing of equipment for upstream and downstream.

5.Purchase of Iranian companies shares by the Russian companies in order to promote their technology.

4 .Export of Russian oil & gas equipment to the Iranian market.

6.Purchase of reliable Russian companies shares by the Iranian groups

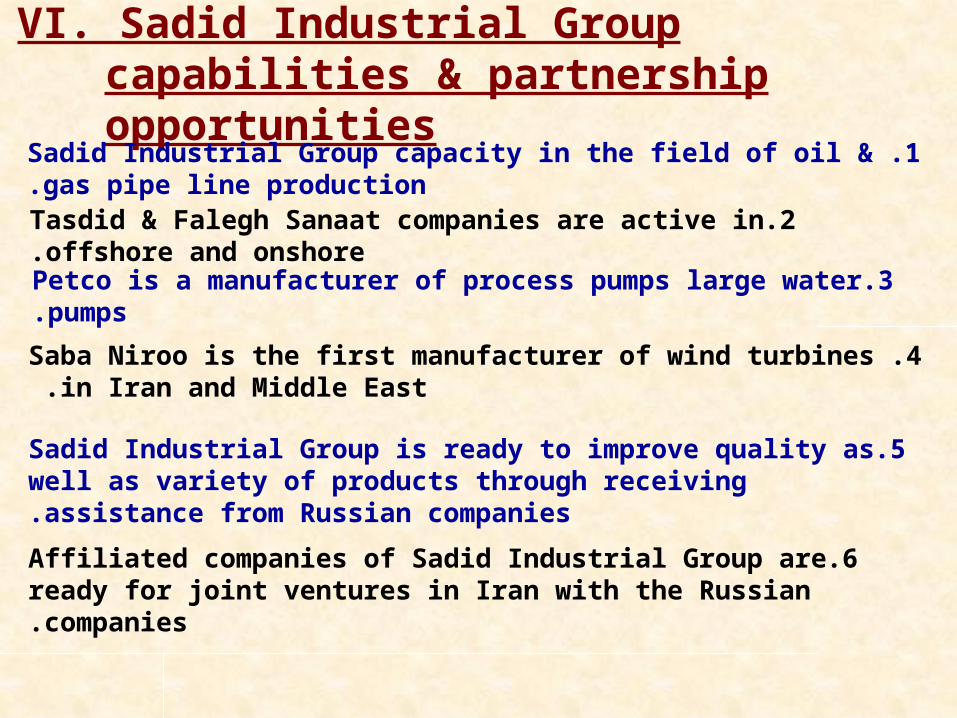

VI. Sadid Industrial Group capabilities & partnership opportunities

1 .Sadid Industrial Group capacity in the field of oil & gas pipe line production.

2.Tasdid & Falegh Sanaat companies are active in offshore and onshore.

3.Petco is a manufacturer of process pumps large water pumps.

4 .Saba Niroo is the first manufacturer of wind turbines in Iran and Middle East .

5.Sadid Industrial Group is ready to improve quality as well as variety of products through receiving assistance from Russian companies.

6.Affiliated companies of Sadid Industrial Group are ready for joint ventures in Iran with the Russian companies.

VII. SADID INDUSTRIAL GROUP New direction in oil & gas

1.Establishment of Sadid oil & gas group with the participation of affiliated companies as well as reliable foreign companies.

2 .Progress in negotiation with National Iranian oil company for entering into upstream projects as EPCF or Buy Back contract models.

3.Organize a Consortium consisted of Sadid affiliates for the purpose of participation in the EPC activities in the downstream.

4 .Sadid interested in establishing consortium with Russian companies for upstream projects of oil & gas in Iran.

5 .Sadid is interested in cooperating with Russian companies in the fields of transferring technology and management as well as partnership in oil & gas projects also cooperating in software and knowledge management.

THANK YOU