Валентина Венкова, ГфК Русь: Маркетинговая стратегия

33

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 1 Retail Business Russia | 25-26 September 2014 Framing the Generational Path to Purchase Valentina Venkova Head of Digital Market Intelligence, GfK Russia

-

Upload

b2bconferencegroup -

Category

Retail

-

view

45 -

download

1

Transcript of Валентина Венкова, ГфК Русь: Маркетинговая стратегия

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 1

Retail Business Russia | 25-26 September 2014

Framing the Generational Path to Purchase

Valentina VenkovaHead of Digital Market Intelligence, GfK Russia

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 22

Major Differences In Shopping Attitudes And Behaviors Evident Along Generational Lines

Source: GfK Consumer Trends, 2013

Age in 2014: 18-24 25-34 35-49 50-68

GEN Z GEN Y GEN X Boomers

Social natives Book smart & savvy

Street smart& skeptical

Education generation

Fun and modest

Fun first, hard work next Get it done Break the mold –

be me

Connected Confidence No drama Agelessness

Global minder “Both/And” stress Balance Do it all –

or die trying

Friends = family Close to doting parents

Prepared, rule-setting parents My self = my kids

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 3

Topics For Today

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 4

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 5

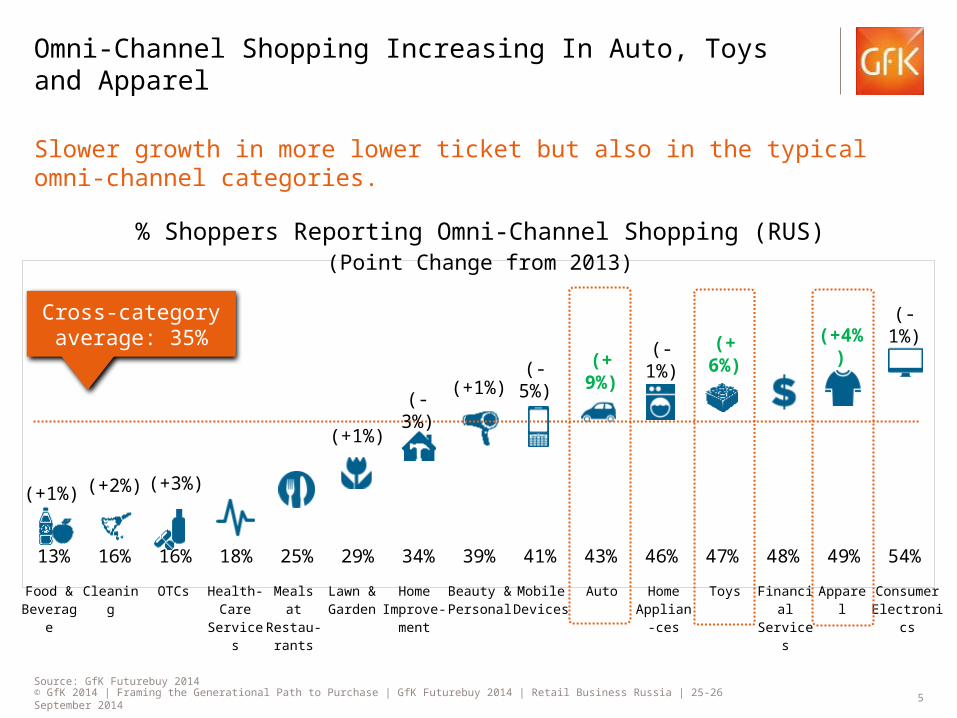

Slower growth in more lower ticket but also in the typical omni-channel categories.

Source: GfK Futurebuy 2014

Omni-Channel Shopping Increasing In Auto, Toys and Apparel

13% 16% 16% 18% 25% 29% 34% 39% 41% 43% 46% 47% 48% 49% 54%

% Shoppers Reporting Omni-Channel Shopping (RUS)(Point Change from 2013)

Cross-category average: 35%

(+1%) (+2%) (+3%)

(+1%)

(+1%)(-3%)

(+ 9%)(-5%)(-1%)

(+ 6%)

(+4%)(-1%)

Food & Beverage

Cleaning OTCs Health-Care

Services

Meals at Restau-

rants

Lawn & Garden

Home Improve-

ment

Beauty & Personal

Mobile Devices

Auto Home Applian-

ces

Toys Financial Services

Apparel Consumer Electronics

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 6

Source: GfK Futurebuy 2014

Drivers Of Channel Choice By Format Reveal Divergent Strengths

Advantage-Bricks and Mortar

Advantage-Online

“Can buy other things at the same time”

“It is recommended by people I trust”

“Getting the best advice on what to buy”

Store25%

Online23%

Store12%

Online15%

Store8%

Online11%

54%

51%

48%

40%

39%

10%

15%

11%

28%

32%

“See and feel before buying.”

“Get products sooner.”

“Hassle-free returns.”

“Faster.”

“Easier.”

Jump Ball

Bricks & Mortar Online

59%

36%

34%

33%

26%

26%

25%

28%

16%

19%

24%

13%

7%

6%

“Save money.”

“Better selection.”

“Better payment options.”

“Better information.”

“Better delivery options.”

“Already have account set up.”

“Can pay with mobile device.”

GEN X

GEN X

GEN Z

Boomers

Boomers

GEN Z

Boomers

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 7

Source: GfK Futurebuy 2014

Services And High Involvement Durables Most Frequently Shopped Exclusively Online

Incidence of Shopping Exclusively Online (RUS)

Automobile or truck

Home appliances

Consumer Electronics

Mobile Phones

Financial Services

7%12% 12%

13% 15%

Note: All other categories 5% and below for exclusive online shopping

Lead by GEN Z & YLead by GEN X

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 8

L’Oreal– Virtual Kiosk For Makeup On The Go (US)

VIRTUAL MAKE-UP KIOSK IN THE NYC SUBWAY

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 9

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 10

38%

69%

71%

73%

75%

81%

With a pronounced spike in price search, online purchases and reviews

Source: GfK Futurebuy 2014

All Web Shopping Activities Trending Up GEN Y and X most active

% Engaging in Online Shopping Activities (RUS)

Finding products & services

Check for general information about products

Purchase a product or service

Read reviews

Searching for the best price

Use social media to exchange/post info about product/service

+3pts

+6pts

+10pts

+10pts

+3pts

+12pts

GEN Z

49%

Change from 2013

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 11

Source: GfK Futurebuy 2014

Home Computer’s Dominance Of Online Shopping Eroding

% Of Total Online Shopping Activity By Device (RUS)

8%

10%

18%

61%

5%

8%

17%

67%

2013 2014

[[[[

Computer at home

Computer at work

Smartphone

Tablet

-6pts

+2pts

+3pts

GEN Z GEN Y

GEN Y

+1pts

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 12

http://www.techtimes.com/articles/11065/20140723/

Target In A Snap - Make Purchases From Print Ads

MAKE PURCHASES FROM PRINT ADS

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 13

Tablet usage more common for the most active part of the population

Source: GfK Futurebuy 2014

Uptick In Smartphone Shopping Skews Younger

Series1

10% 9%7% 4%

14% 13%

8%6%

GEN Z GEN XGEN Y Boomers

Series1

4%6% 5% 2%

7%

10%8%

5%

2013 2014

GEN Z GEN XGEN Y Boomers

Share of All Online Shopping Activity on Smartphone (RUS)

Share of All Online Shopping Activity on Tablet (RUS)

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 14

Series1

20%18%

11%9%

Driven by uniquely heavy activity of certain age groups

Source: GfK Futurebuy 2014

Mobile Shopping Predominant In Select Categories

Consumer Electronics Apparel Mobile

phonesFinancial services

Top Categories Shopped On Mobile Device (RUS)

GEN Y leads

at 26%

Boomers leads at

27%

GEN Z leads at

14%Boomers

Driven at 19%

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 15

Source: GfK Futurebuy 2014

Privacy A Highly Polarizing Issue – But Online Tracking Universally Losing Appeal

“I like when websites keep track of my visits, then recommend things to me.”

(-6pts)

(-5pts)

(-18pts)

(-7pts)

(-7pts)

Germany

Japan

France

Australia

Canada

“Open Book”

“Most Private”

65%Colombia 64%

61%60%

57%56%

Romania

China

Brazil

Mexico

Bulgaria

23%

25%

34%

35%

35%(-4pts)

41%

Russia38%

United States(-4pts)

GEN Z leads

at 46%

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 16

“Zero Tracking” Platforms Arise To Address Privacy Concerns (US)

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 17

Series1

17% 19% 11% 4%

Source: GfK Futurebuy 2014

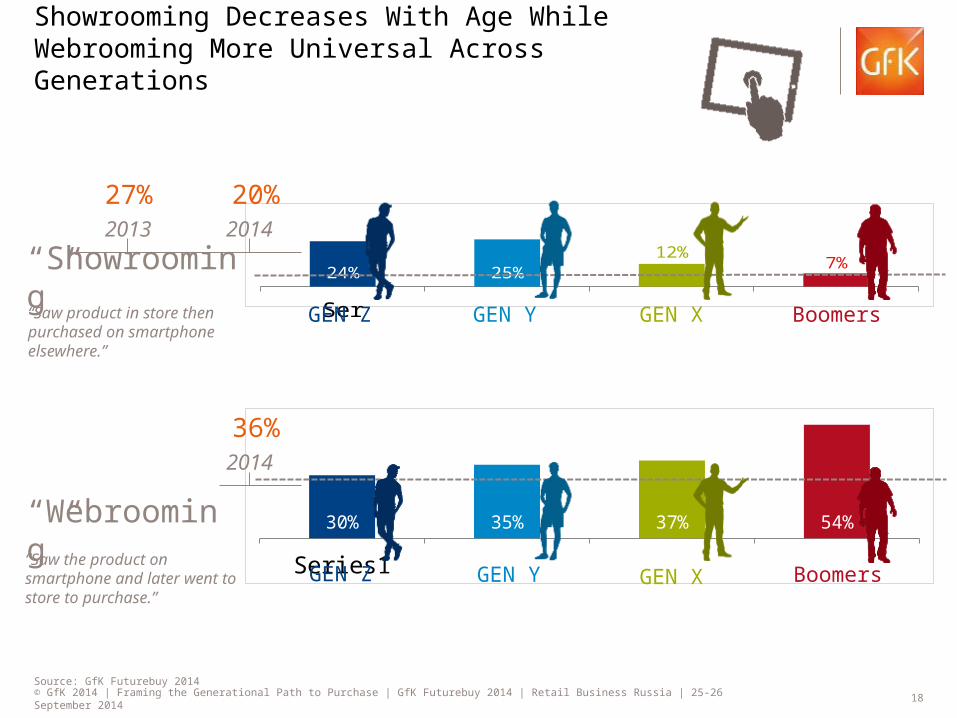

Showrooming Decreases With Age While Webrooming More Universal Across Generations

Series1

35% 31% 32% 43%

“Showrooming”

“Webrooming”

GEN Z GEN XGEN Y Boomers

GEN Z GEN XGEN Y Boomers

“Saw product in store then purchased on smartphone elsewhere.”

“Saw the product on smartphone and later went to store to purchase.”

15%2013 2014

27%

33%2014

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 18

Series1

24% 25%12%

7%

Source: GfK Futurebuy 2014

Showrooming Decreases With Age While Webrooming More Universal Across Generations

Series1

30% 35% 37% 54%

“Showrooming”

“Webrooming”

GEN Z GEN XGEN Y Boomers

GEN Z GEN XGEN Y Boomers

“Saw product in store then purchased on smartphone elsewhere.”

“Saw the product on smartphone and later went to store to purchase.”

20%2013 2014

27%

36%2014

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 19

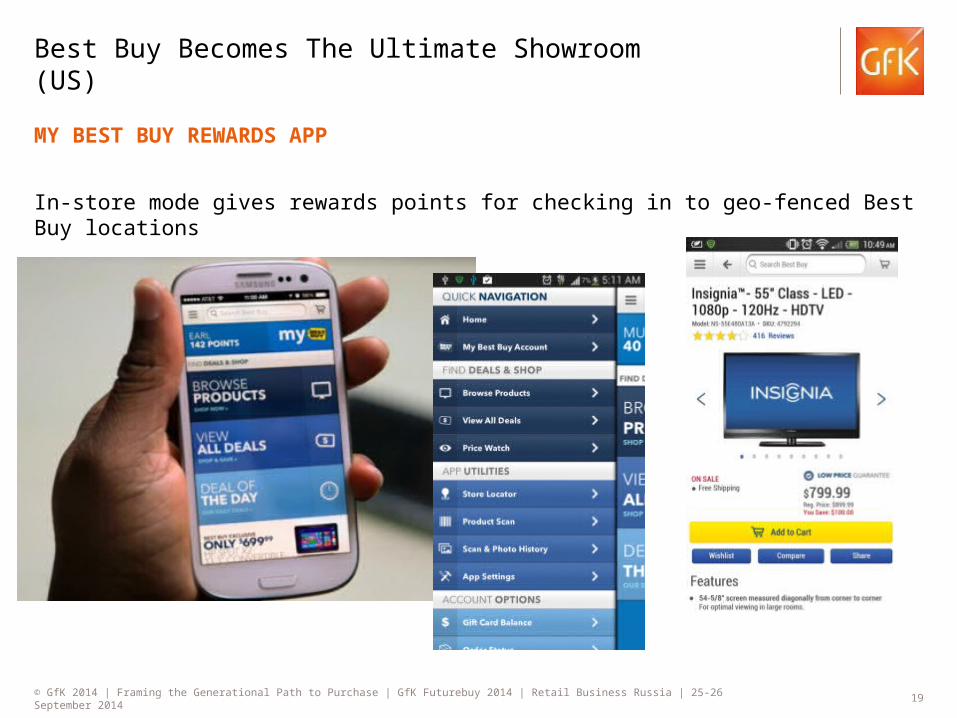

MY BEST BUY REWARDS APP

In-store mode gives rewards points for checking in to geo-fenced Best Buy locations

Best Buy Becomes The Ultimate Showroom (US)

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 20

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 21

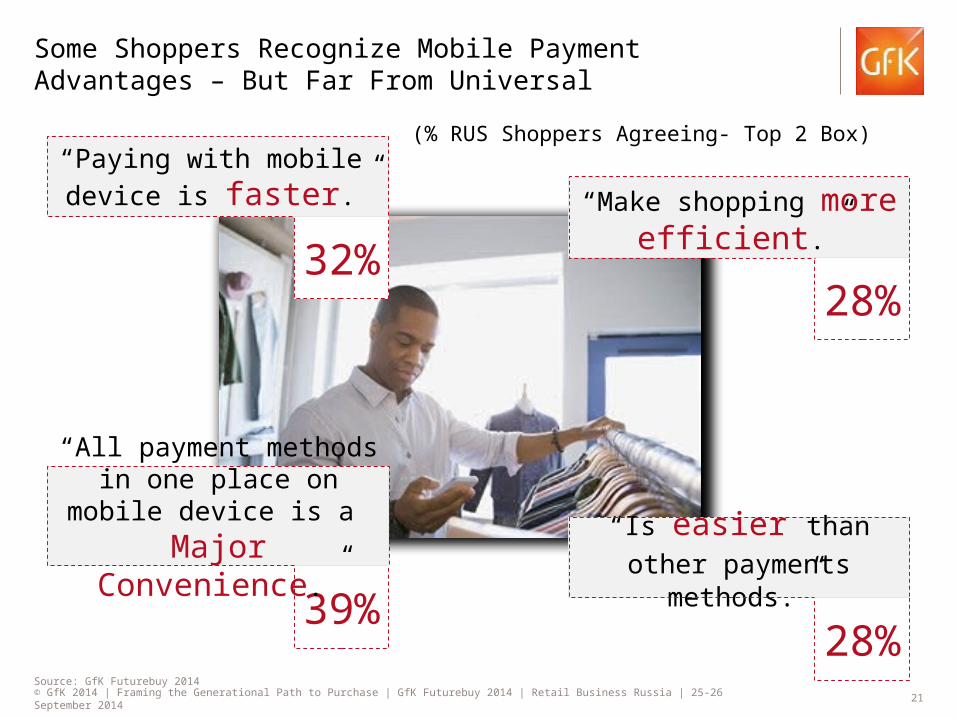

32%

Source: GfK Futurebuy 2014

Some Shoppers Recognize Mobile Payment Advantages – But Far From Universal

“Paying with mobile device is faster.”

28%

“Make shopping more efficient.”

39%

“All payment methods in one place on mobile device is a Major Convenience.”

28%

“Is easier than other payments methods.”

(% RUS Shoppers Agreeing- Top 2 Box)

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 22

Source: GfK Futurebuy 2014

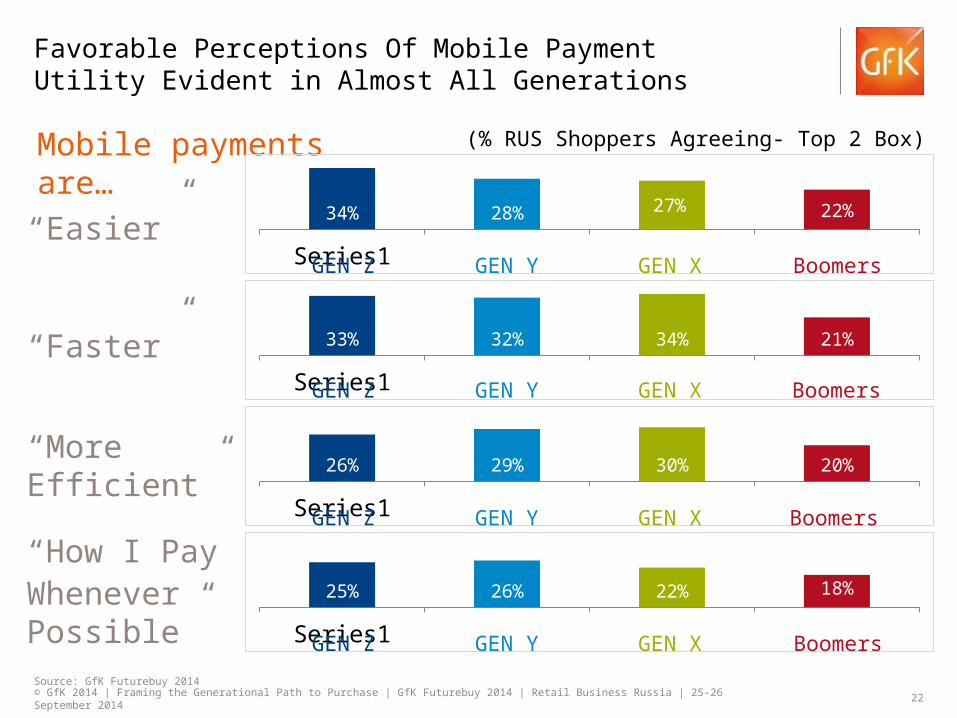

Favorable Perceptions Of Mobile Payment Utility Evident in Almost All Generations

Mobile payments are…

Series1

34% 28%27% 22%

Series1

33% 32% 34% 21%

Series1

26% 29% 30% 20%

Series1

25% 26% 22% 18%

“Easier”

“Faster”

“More Efficient”

“How I PayWhenever Possible”

GEN Z GEN XGEN Y Boomers

GEN Z GEN XGEN Y Boomers

GEN Z GEN XGEN Y Boomers

GEN Z GEN XGEN Y Boomers

(% RUS Shoppers Agreeing- Top 2 Box)

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 23

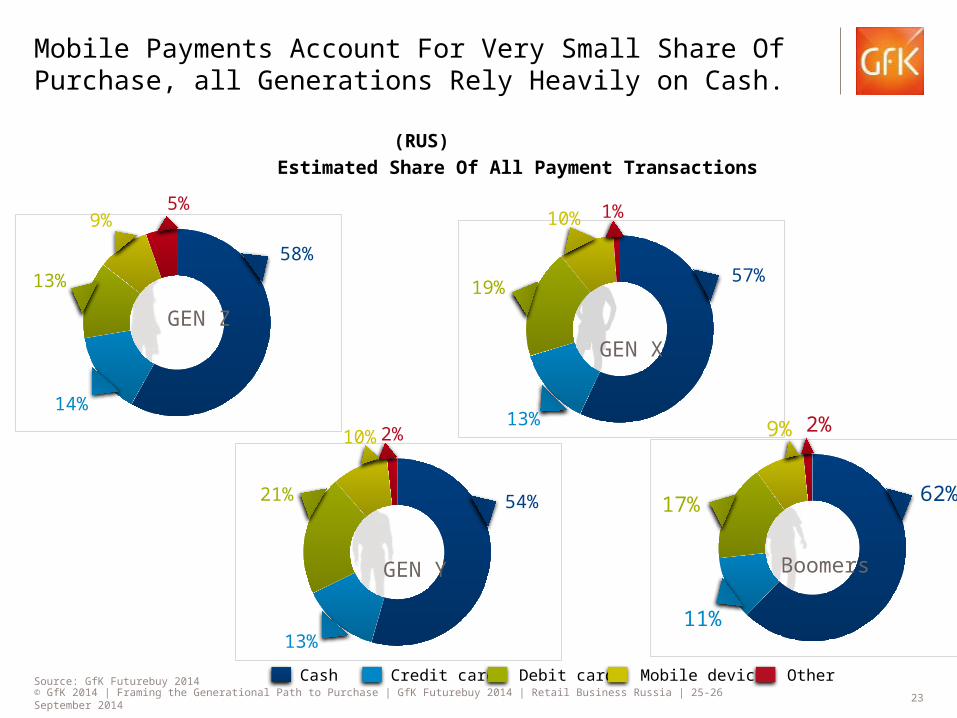

Source: GfK Futurebuy 2014

Mobile Payments Account For Very Small Share Of Purchase, all Generations Rely Heavily on Cash.

58%

14%

13%

9%

57%

13%

10% 1%

54%

13%

21%

2%

62%

11%

17%

9% 2%

Cash Credit card Debit card Mobile device Other

5%

GEN ZGEN X

BoomersGEN Y

19%

10%

Estimated Share Of All Payment Transactions

(RUS)

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 24

Source: GfK Futurebuy 2014

A Range Of Shopper Concerns Are Likely Holding Mobile Payment From Full Potential

“Mobile payment more of a GIMMICK today than a major way I pay”

48%“Mobile payment technology STILL CLUNKY”

43%“Worried about SECURITY, PERSONAL INFORMATION”

58%

“I am planning to make more mobile payments in

next 12 months”

But…34%

“Ability to make mobile payments important factor

in making more online purchases next year”

33%

(% RUS Shoppers Agreeing- Top 2 Box )

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 25

Series1

28% 19% 19% 7%

Series1

29% 22% 20% 12%

Series1

53% 61% 59% 61%

Source: GfK Futurebuy 2014

Gen Z Stands Apart In Its Trust In Security Of Mobile Payment Platforms

Mobile payment More Secure vs. other payment methods

Confident my mobile payments are 100% Secure

Worried about Personal Information when making mobile payment

GEN Z Boomers

GEN Z

GEN Z

Boomers

Boomers

GEN XGEN Y

GEN XGEN Y

GEN XGEN Y

(% RUS Shoppers Agreeing- Top 2 Box)

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 26

PayQR at Babysecret.ru

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 27

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 28

Source: GfK Futurebuy 2014

Free Delivery Remains King In Driving More Online Purchases

Most Important Factors to “Get Me to Make More Online Purchases Next Year”(RUS)

53%

55%

65%

70%

73%Free Delivery

Discounts on bulk purchases

Holiday/seasonal discounts

More user reviews

Better loyalty programs Most motivating to Gen X

Most motivating to Gen Z

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 29

Lowe’s Holoroom – An Immersive, Augmented Reality Reason To Visit Store (Toronto)

HOME IMPROVEMENT SIMULATOR

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 30

A New Twist On Mobile Wallet (Sweden)

PAY WITH YOUR HAND

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 3131

Google Express Enters The “Same-Day Fray” (US)

SAME DAY DELIVERY SERVICE FROM GOOGLE

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 32

Key Takeaways

Omni-Channel - coming soon to your category!

Mobile not yet mainstream

Showrooming slowdown?

Generation Matters- a lot!

© GfK 2014 | Framing the Generational Path to Purchase | GfK Futurebuy 2014 | Retail Business Russia | 25-26 September 2014 33

THANK YOU!

Valentina VenkovaHead of Digital Market Intelligence, GfK Russia

+7 916 150 07 59