© 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved....

26

© 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. Insurance 2020 & Beyond IIS Global Insurance Forum www.pwc.com/insurance June , 2015

Transcript of © 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved....

© 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Insurance 2020 & BeyondIIS Global Insurance Forum

www.pwc.com/insurance

June , 2015

© 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Introduction & Welcome

Stephen O’HearnPwC Global Insurance LeaderPwC

1

PwC

88%

66%

71%

61%

64%

61%

69%

50%

61%

47%

Changes in industry regulation

Changes in customer behaviors

Increase in number of significant competitors

traditional and new

Changes in distribution channels

Changes in core technologies of

production or service provision

Q: How disruptive do you think the following trends will be for your industry over the next five years? Respondents stating very or somewhat disruptive

Insurance All Industries

The insurance industry is undergoing more upheaval than any other industry

Source: PwC18th Annual Global CEO Survey

PwC

of insurance CEOs believe there are more growth opportunities than there were three years ago

59%

of insurance CEOs see more threats than they did in 2012

61%

Sources: PwC 18th Annual Global CEO Survey

Insurance executives are preparing to navigate a market filled with nearly an equal amount of opportunities and threats

4Source: PwC 18th Annual Global CEO Survey

Industry Trends & Disruptors

PwC

Jamie YoderPwC Global Insurance Advisory Leader

2

PwC

In 2011 when we put forward our perspective on the future of insurance, we considered scenarios for 32 distinct drivers of change

6

SocialCustomer Behaviors

– Social Networking– Customer Expectations– Risk Awareness– Health

Talent Drain

Stakeholder Trust

Corporate Social Responsibility

Demographic Shifts– Dynamics of the Middle

Class– New Family Structure– Dependency Ratio– Aging

EconomicUrbanization

New Growth Opportunities

Fiscal Pressure

Inflation/Deflation

Risk Sharing & Transfer

Social Security & Benefits

Distributor Shift

Partnerships

TechnologyInformation & Analytics

Devices & Sensors

Software & Applications

Medical Advances

Environmental

Climate Change & Catastrophes

Sustainability

Pollution

PoliticalRegulatory Reform

Geo-political Risk

Rise of State-Directed Capitalism

Terrorism

Tax Treatment

Sharia Compliance (Takaful)

PwC

The implications of these trends are altering the way insurers compete

7

Social The balance of power is shifting towards customers

TechnologicalAdvances in software & hardware are transforming ‘big data’ into actionable insightsEnvironmentalIncreasing severity and frequency of catastrophic events are giving rise to more sophisticated risk models & risk transfer

EconomicThe rise of economic and political power in emerging markets

PoliticalThere is harmonization, standardization and globalization of the insurance market

PwC 8

4% 10% 39%

Distribution disruption where integrated multi-channel interaction is the norm

Regressive Progressive

Source: PwC Analysis; IIS Conference, Toronto, 2011

21% 24%

In 2011, when we asked how far the balance of power would shift to the customers…

PwC 9

Today…

of insurance CEOs recognize the power of digital and are using it to enhance customer experience

81%

Source: PwC 18th Annual Global CEO Survey

of consumers shopped for auto insurance online in 2014

46%

of consumers shopping in 2014 obtained a quote online

71%

Sources: PwC 18th Annual Global CEO Survey; comScore 2o14 U.S. Online Auto Insurance Shopping Report

PwC 10

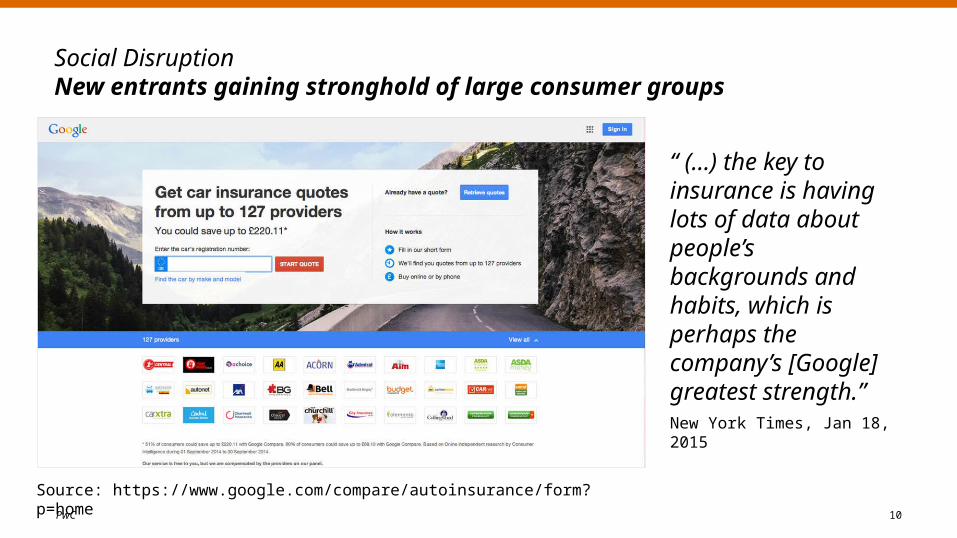

Social DisruptionNew entrants gaining stronghold of large consumer groups

“ (…) the key to insurance is having lots of data about people’s backgrounds and habits, which is perhaps the company’s [Google] greatest strength.”New York Times, Jan 18, 2015

Source: https://www.google.com/compare/autoinsurance/form?p=home

PwC 11

Social DisruptionThe eCommerce player Alibaba is transforming the Chinese market and innovating in financial services and insurance

Three companies joined together to launch…

Ping AnTencentAlibaba

...Zhong An - the first online insurance company in China

Source: https://www.zhongan.com/index.html

PwC 12

Social DisruptionNew entrants in the robo-advisor space are developing new models of assisted and automated omni-channel education and advice

Sources: http://www.bloomberg.com/news/videos/2015-03-26/northwestern-mutual-acquires-learnvest; https://intelligent.schwab.com/

PwC 13

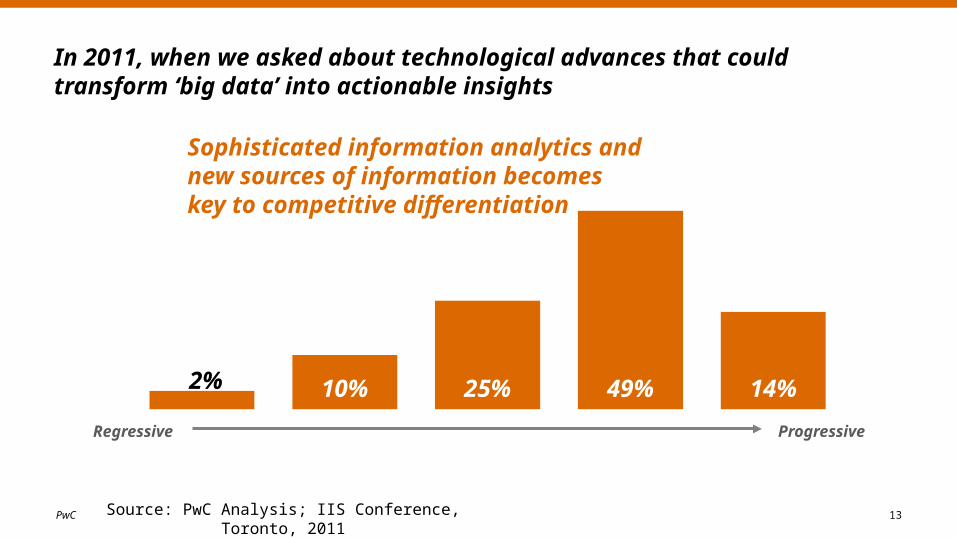

In 2011, when we asked about technological advances that could transform ‘big data’ into actionable insights

10% 25%

Sophisticated information analytics and new sources of information becomes key to competitive differentiation

Regressive Progressive

49% 14%2%

Source: PwC Analysis; IIS Conference, Toronto, 2011

PwC 14

Today…

Source: PwC 18th Annual Global CEO Survey; Industry Forecasts Compilation, 2020 forecast from IDC; PwC Analysis

70%more than all but one other industry, see the speed of technological change as a threat to their growth prospect 2014 2020

$3.5T

$8.9T

The Internet of Things is Exploding

IoT Global Revenue

PwC 15

Pricing Risk• New data sources

(IoT, mobile, etc)• Better data

Ongoing Relationship• Empowering to

make smart lifestyle decisions

• Services to support easier lifestyle

Crowdsourcing• Cheaper option to

pool capital• Help diversify

assets

Andreesen Horowitz shares the 16 tech trends it’s most excited about

Source: http://a16z.com/2015/01/22/16-things/

Virtual Reality

Sensorifi- cation of the

Enterprise

Machine Learning + Big Data

The Full-Stack Start-up

Digital HealthOnline

MarketplacesSecurity

Cloud-Client Computing

Crowd Funding Internet of Things

‘Failure’ DevOps Insurance

Containers

Bitcoin (and Blockchain)

Online Video

PwC 16

Technological DisruptionThe Climate Corporation revolutionized yield management and crop insurance using machine learning techniques

Source: http://www.climate.com/; FastCompany, October 7, 2013

PwC 17

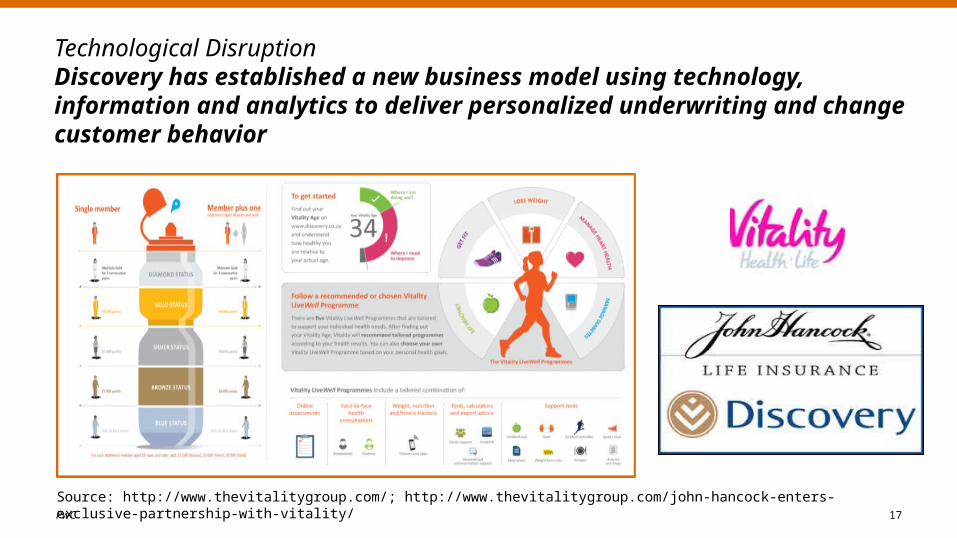

Technological DisruptionDiscovery has established a new business model using technology, information and analytics to deliver personalized underwriting and change customer behavior

Source: http://www.thevitalitygroup.com/; http://www.thevitalitygroup.com/john-hancock-enters-exclusive-partnership-with-vitality/

PwC 18Source: PwC Analysis; IIS Conference, Toronto, 2011

7% 12% 11%

Emerging markets do not harmonize their regulations with the developed markets, but they

change the regulations to make it easier for new entrants

Regressive Progressive

39% 30%

In 2011, when we asked about the opposing forces of harmonization and regionalization/nationalization of regulations, products, and practices globally…

PwC 19

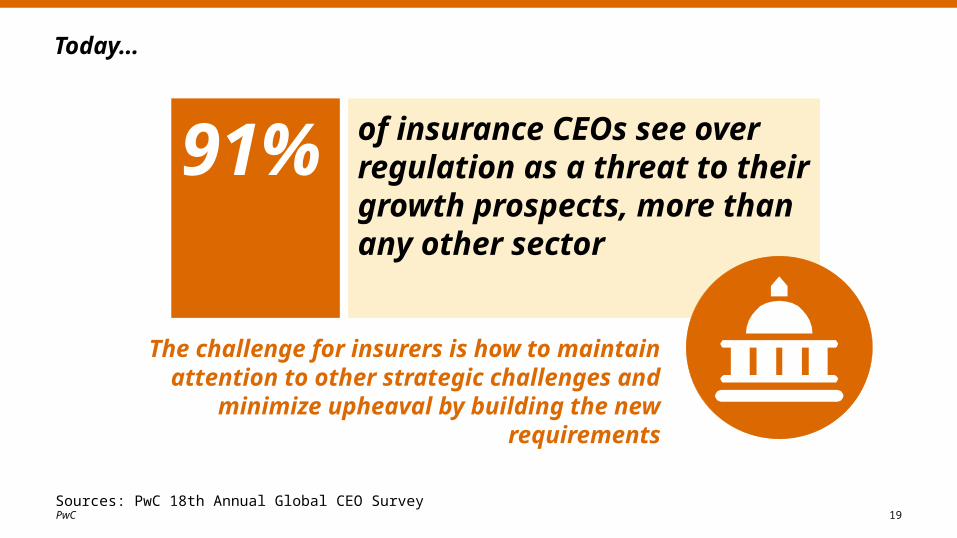

of insurance CEOs see over regulation as a threat to their growth prospects, more than any other sector

91%

Today…

The challenge for insurers is how to maintain attention to other strategic challenges and minimize upheaval by

building the new requirements

Sources: PwC 18th Annual Global CEO Survey

PwC20

Manifestation of Mega Trends

Disruption in Insurance

Digitization Intelligence & Automation

Innovative Business Model

Customer Revolution

Two-Speed Growth

Regulation

What risks and opportunities do these trends and potential disruptors mean to you?

Introducing the Panel

PwC

3

© 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Stephen O’HearnPwC Global

Insurance Leader

Jamie YoderPwC Global

Insurance Advisory Leader

Thomas SullivanAssociate DirectorFederal Reserve

Board

Sean GildayVP of Strategic Partnerships

RGA

Panelist

Panelist

Panelist

Moderator

22

Panelists

© 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Q&A

PwC

4

© 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

In summary, there are 5 things to remember…

24

1)No one knows what the winning bets are so learn fast

2) Fail quickly, fail cheaply

3) ‘Test and refine’ is more important than ‘plan and design’

4) Do something different – you’ve not got long!

5) Focus on the customer…

© 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Thank you

PwC

5

© 2015 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

PwC firms provide industry-focused assurance, tax and advisory services to enhance value for their clients. More than 161,000 people in 154 countries in firms across the PwC network share their thinking, experience and solutions to develop fresh perspectives and practical advice. See www.pwc.com for more information.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2015 PwC. All rights reserved. Not for further distribution without the permission of PwC. “PwC” refers to the network of member firms of PricewaterhouseCoopers International Limited (PwCIL), or, as the context requires, individual member firms of the PwC network. Each member firm is a separate legal entity and does not act as agent of PwCIL or any other member firm. PwCIL does not provide any services to clients. PwCIL is not responsible or liable for the acts or omissions of any of its member firms nor can it control the exercise of their professional judgment or bind them in any way. No member firm is responsible or liable for the acts or omissions of any other member firm nor can it control the exercise of another member firm’s professional judgment or bind another member firm or PwCIL in any way.HB8763