© 2004 South-Western Publishing 1 Chapter 4 Option Combinations and Spreads.

59

© 2004 South-Western Publishing 1 Chapter 4 Option Combination s and Spreads

-

Upload

pamela-conley -

Category

Documents

-

view

215 -

download

1

Transcript of © 2004 South-Western Publishing 1 Chapter 4 Option Combinations and Spreads.

© 2004 South-Western Publishing 1

Chapter 4Option

Combinations and

Spreads

2

Options Combinations

Introduction Straddles Strangles

Condors

3

Introduction

A combination is a strategy in which you are simultaneously long or short

options of different types

It seeks a trading profit rather than being motivated by a hedging or

income generation objective

4

Straddles

A straddle is the best-known option combination

You are long (short) a straddle if you own (are short) both a put and a call

with the same– Striking price

– Expiration date– Underlying security

5

Buying a Straddle

A long call is bullish A long put is bearish

Why buy a long straddle?– Whenever a situation exists when it is likely that a

stock will move sharply one way or the other but you do not know with certainty in which direction.

Examples: – On going negotiation for merger or acquisition.– Suit case in the court where no body can expect

the decision with certainty. We are sure about the price change, but we

do not know in which direction.

6

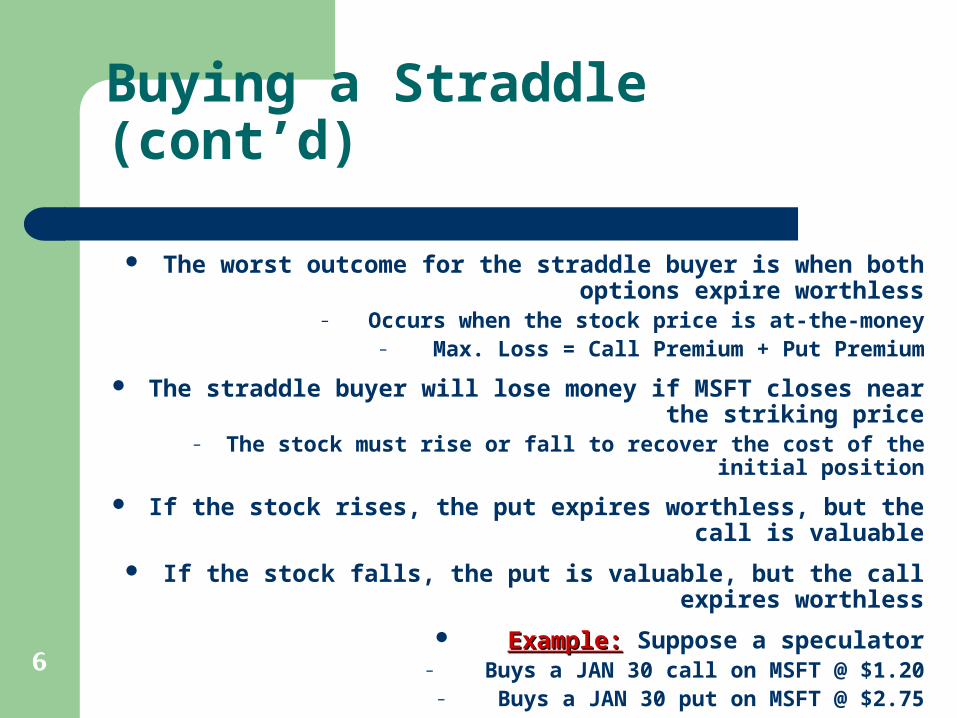

Buying a Straddle (cont’d)

The worst outcome for the straddle buyer is when both options expire worthless

– Occurs when the stock price is at-the-money– Max. Loss = Call Premium + Put Premium

The straddle buyer will lose money if MSFT closes near the striking price

– The stock must rise or fall to recover the cost of the initial position

If the stock rises, the put expires worthless, but the call is valuable

If the stock falls, the put is valuable, but the call expires worthless

Example:Example: Suppose a speculator– Buys a JAN 30 call on MSFT @ $1.20– Buys a JAN 30 put on MSFT @ $2.75

7

Buying a Straddle (cont’d)

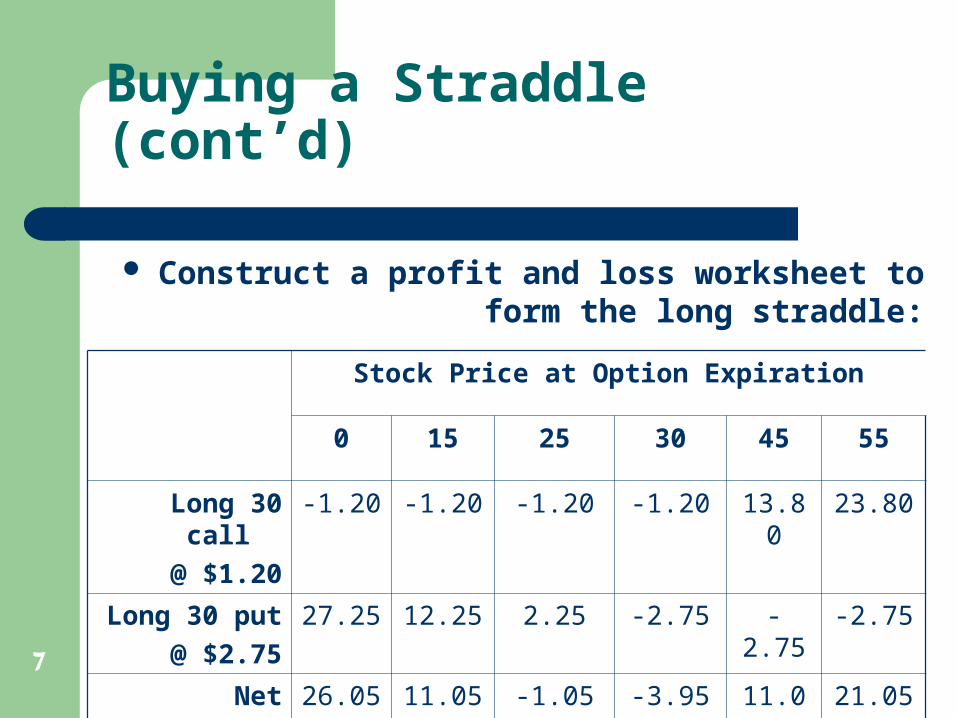

Construct a profit and loss worksheet to form the long straddle:

Stock Price at Option Expiration

0 15 25 30 45 55

Long 30 call

@ $1.20

-1.20 -1.20 -1.20 -1.20 13.80 23.80

Long 30 put @ $2.75

27.25 12.25 2.25 -2.75 -2.75 -2.75

Net 26.05 11.05 -1.05 -3.95 11.05 21.05

8

Buying a Straddle (cont’d)

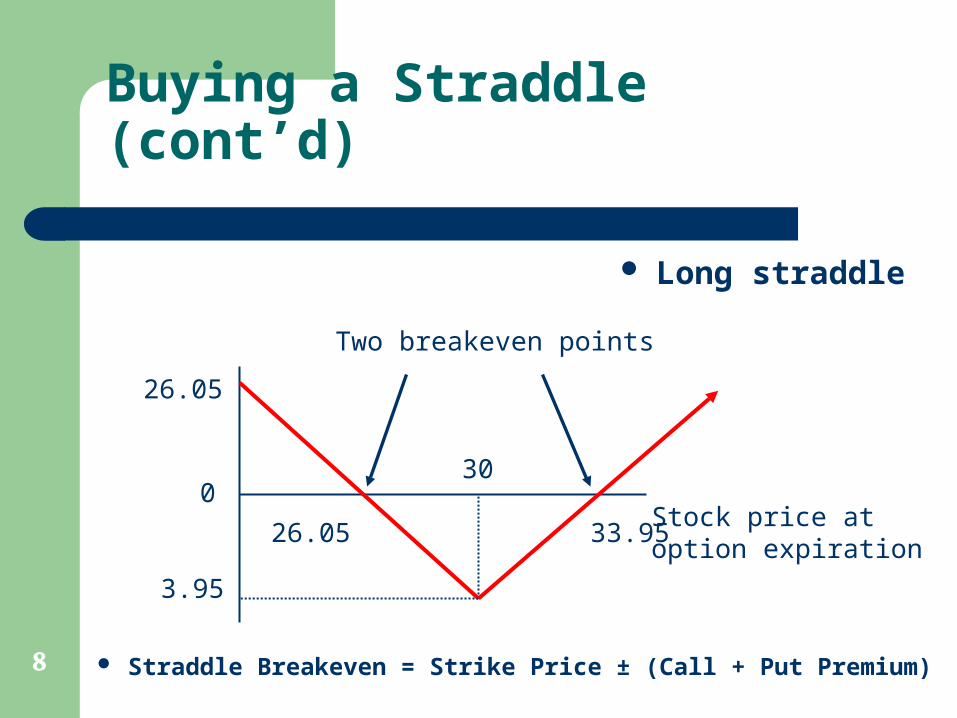

Long straddle

Stock price at option expiration

0

3.95

30

26.05

26.05 33.95

Two breakeven points

Straddle Breakeven = Strike Price ± (Call + Put Premium)

9

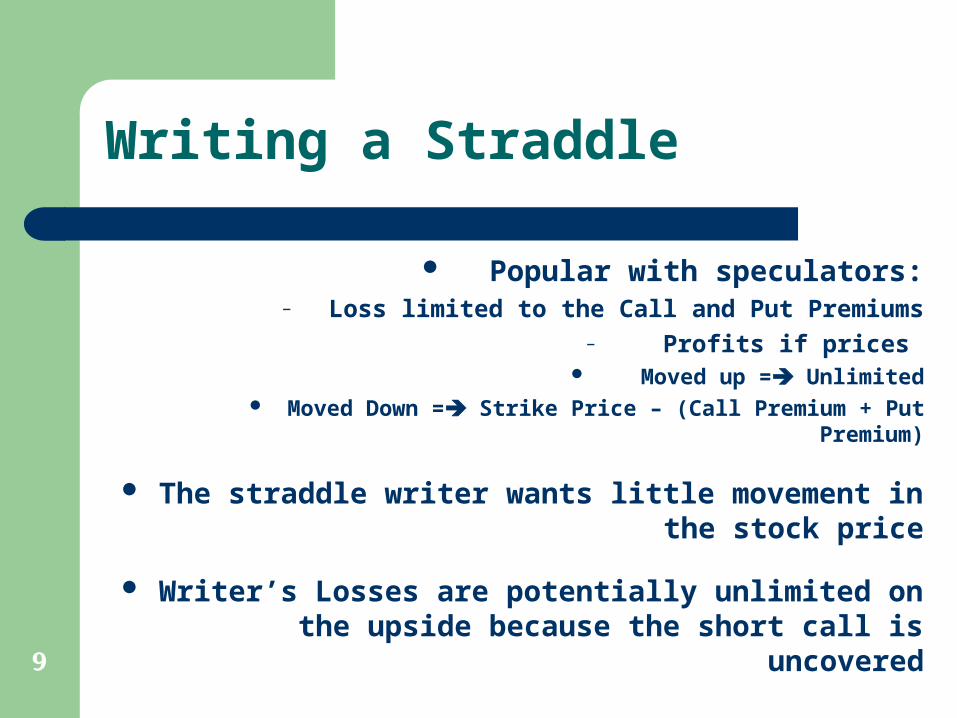

Writing a Straddle

Popular with speculators:– Loss limited to the Call and Put Premiums

– Profits if prices Moved up = Unlimited

Moved Down = Strike Price – (Call Premium + Put Premium)

The straddle writer wants little movement in the stock price

Writer’s Losses are potentially unlimited on the upside because the short call is uncovered

10

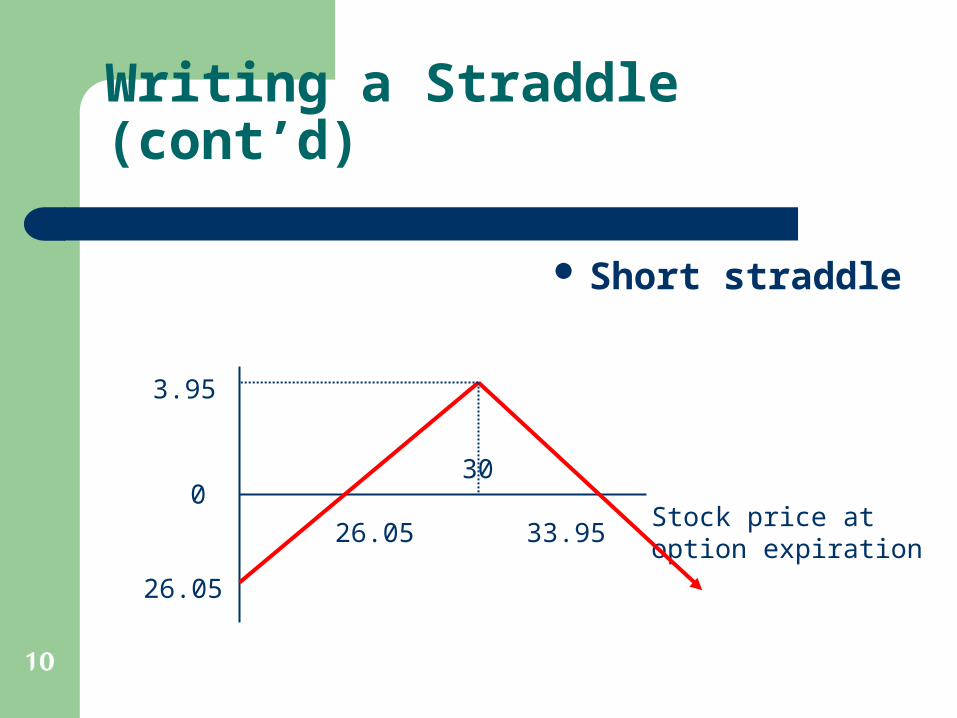

Writing a Straddle (cont’d)

Short straddle

Stock price at option expiration

0

26.05

30

3.95

26.05 33.95

11

Strangles

A strangle is similar to a straddle, except the puts and calls have different striking prices

Strangles are very popular with professional option traders

You are long (short) a strangle if you own (are short) both a put and a call with

– The Same Expiration Date

Underlying Security

– Different Striking Price

12

Buying a Strangle

The speculator long a strangle expects a sharp price movement either up or

down in the underlying security

With a long strangle, the most popular version involves buying a put with a

lower striking price than the call

Example:Example: Suppose a speculator:– Buys a MSFT JAN 25 put @ $0.70– Buys a MSFT JAN 30 call @ $1.20

13

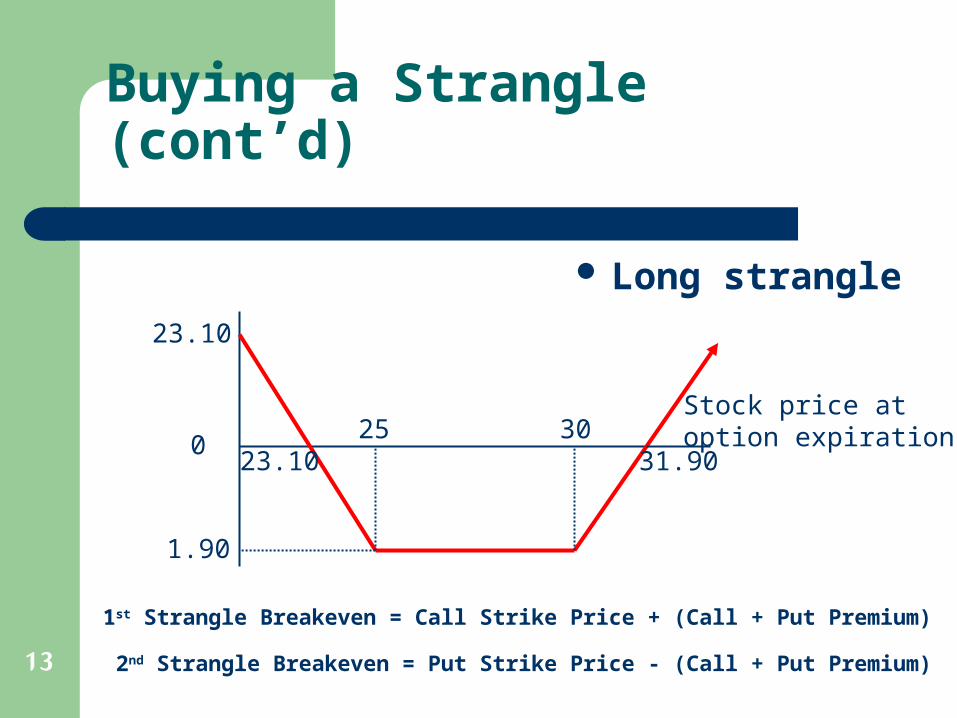

Buying a Strangle (cont’d)

Long strangle

Stock price at option expiration0

1.90

25

23.10

23.10 31.9030

1st Strangle Breakeven = Call Strike Price + (Call + Put Premium)

2nd Strangle Breakeven = Put Strike Price - (Call + Put Premium)

14

Writing a Strangle

The maximum gains for the strangle writer occurs if both option expire worthless

– Occurs in the price range between the two exercise prices

– Therefore, strangle gives the writer more chances to make money on the cost of the buyer who will face

more chance to loss his premiums (within the price range between the 2 exercise prices).

The loss for the strangle writer– If Stock Price Moved Up = loss will be Unlimited.

– If Stock Price Moved Down = loss will be limited to

= Strike Price – (Put Premium + Call Premium)

15

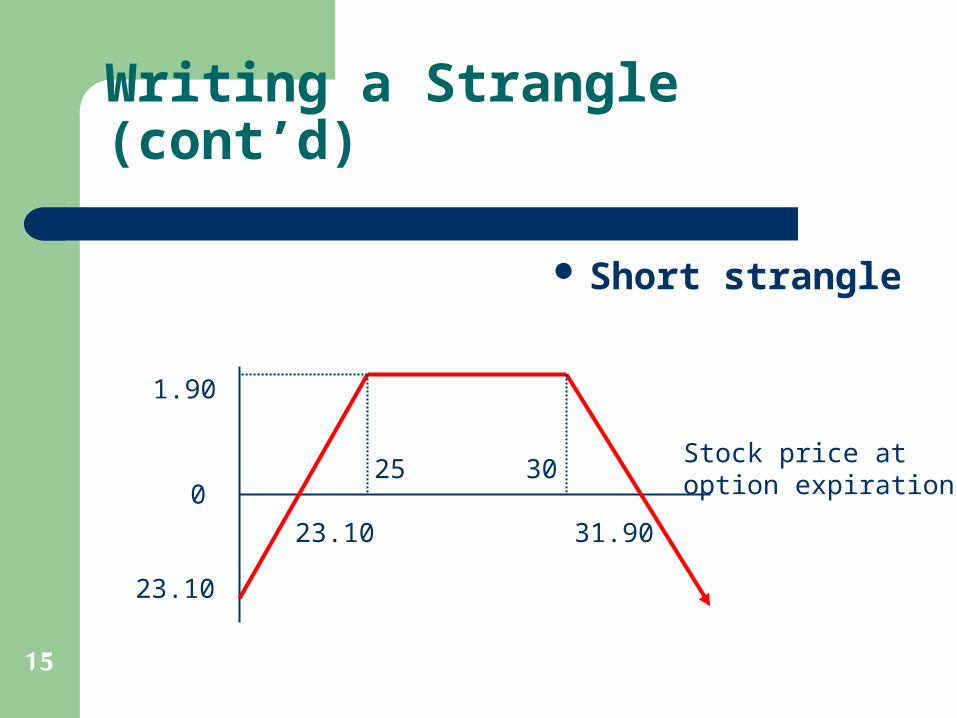

Writing a Strangle (cont’d)

Short strangle

Stock price at option expiration0

23.10

25

1.90

23.10 31.90

30

16

Condors

A condor is a less risky version of the strangle, write & buy call & put options on the same stock

with the same expiration date, but with 4 different striking prices.

Write & Buy Call Options with 2 different exercise prices as follow:

– Exercise Price of Written Call > Exercise Price of Bought Call

– Premium of Written Call < Premium of Bought Call.

Write & Buy Put Options with 2 different exercise prices as follow:

– Exercise Price of Written Put < Exercise Price of Bought Put

– Premium of Written Put < Premium of Bought Put.

17

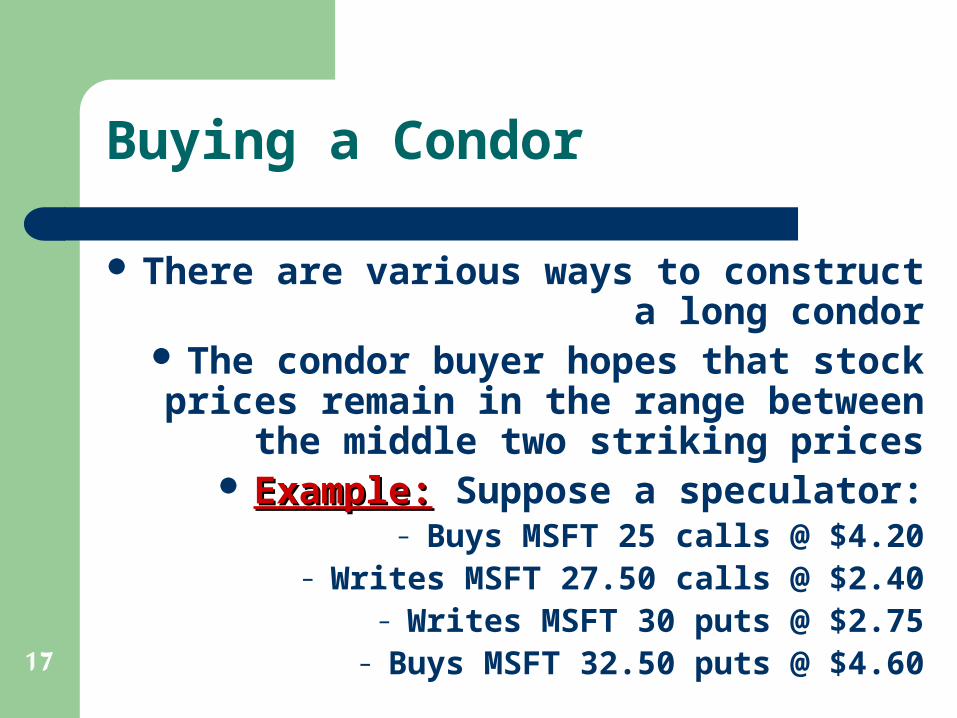

Buying a Condor

There are various ways to construct a long condor

The condor buyer hopes that stock prices remain in the range between

the middle two striking prices Example:Example: Suppose a speculator:

– Buys MSFT 25 calls @ $4.20– Writes MSFT 27.50 calls @ $2.40

– Writes MSFT 30 puts @ $2.75– Buys MSFT 32.50 puts @ $4.60

18

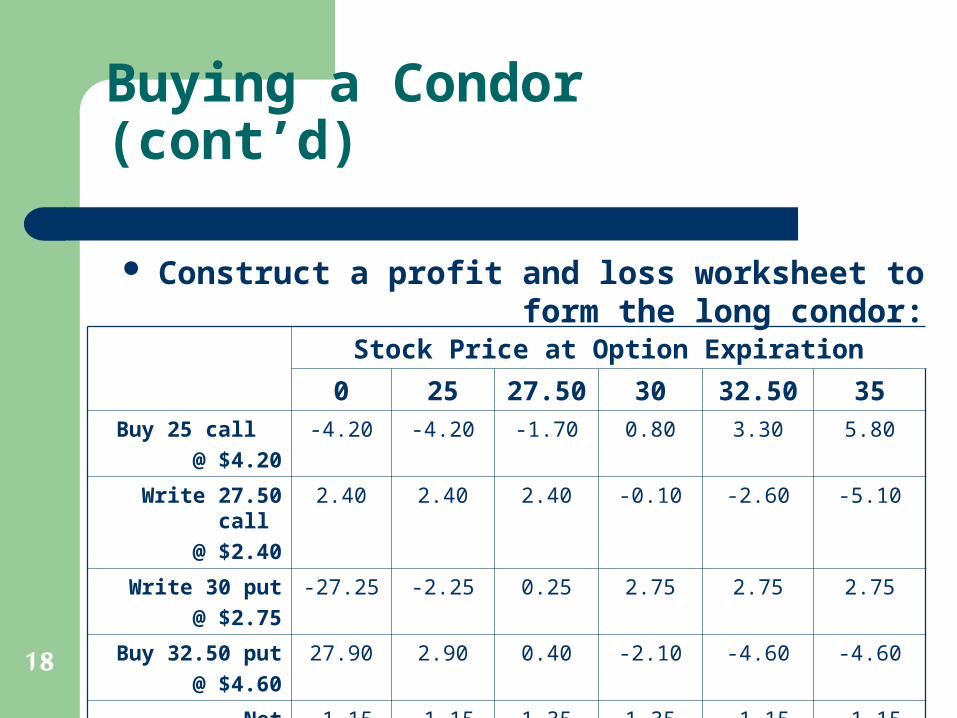

Buying a Condor (cont’d)

Construct a profit and loss worksheet to form the long condor:

Stock Price at Option Expiration

0 25 27.50 30 32.50 35Buy 25 call

@ $4.20-4.20 -4.20 -1.70 0.80 3.30 5.80

Write 27.50 call

@ $2.40

2.40 2.40 2.40 -0.10 -2.60 -5.10

Write 30 put@ $2.75

-27.25 -2.25 0.25 2.75 2.75 2.75

Buy 32.50 put@ $4.60

27.90 2.90 0.40 -2.10 -4.60 -4.60

Net -1.15 -1.15 1.35 1.35 -1.15 -1.15

19

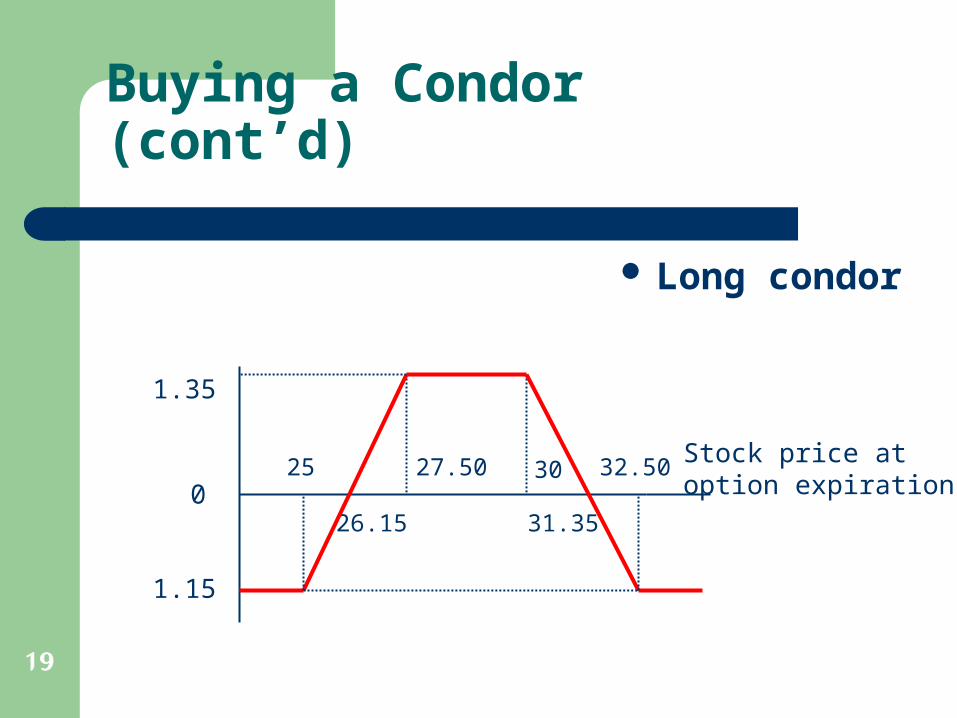

Buying a Condor (cont’d)

Long condor

Stock price at option expiration0

1.15

25

1.35

26.15

30

31.35

27.50 32.50

20

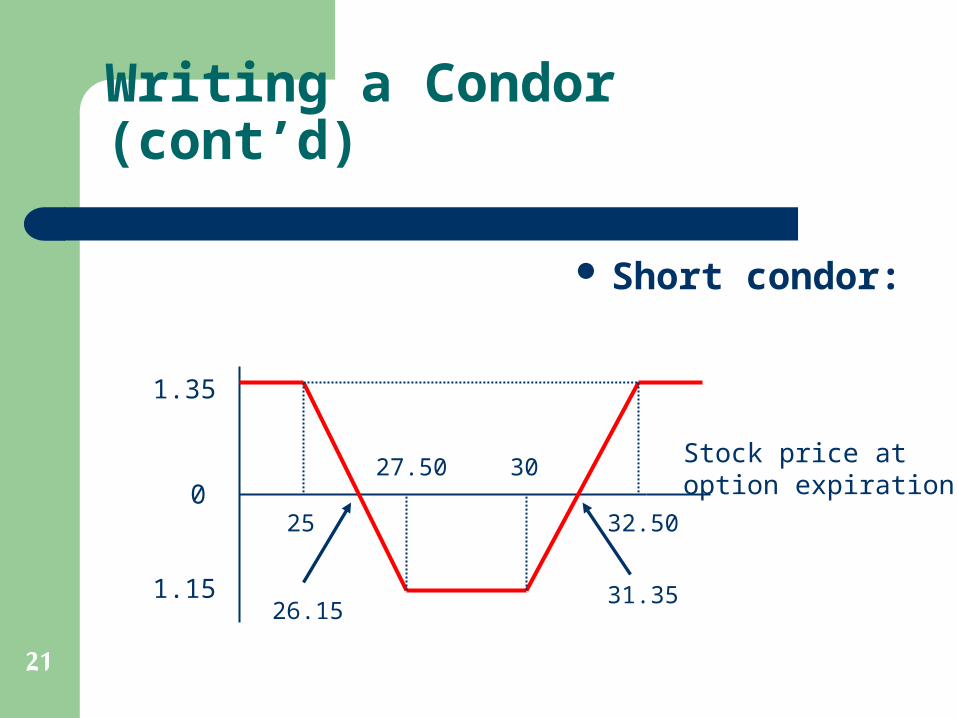

Writing a Condor

The condor writer makes money when prices move sharply in either

direction

The maximum gain is limited to the premium

21

Writing a Condor (cont’d)

Short condor:

Stock price at option expiration0

1.15

25

1.35

26.15

30

31.35

27.50

32.50

22

Spreads

Vertical spreads

Vertical spreads with calls

Vertical spreads with puts

Calendar spreads

Diagonal spreads

Butterfly spreads

23

Introduction

Option spreads are strategies in which the player is simultaneously long and

short options of the same type, but with different

– Striking prices Vertical Spread with

– Calls or – Puts

– Expiration dates Calendar Spread

24

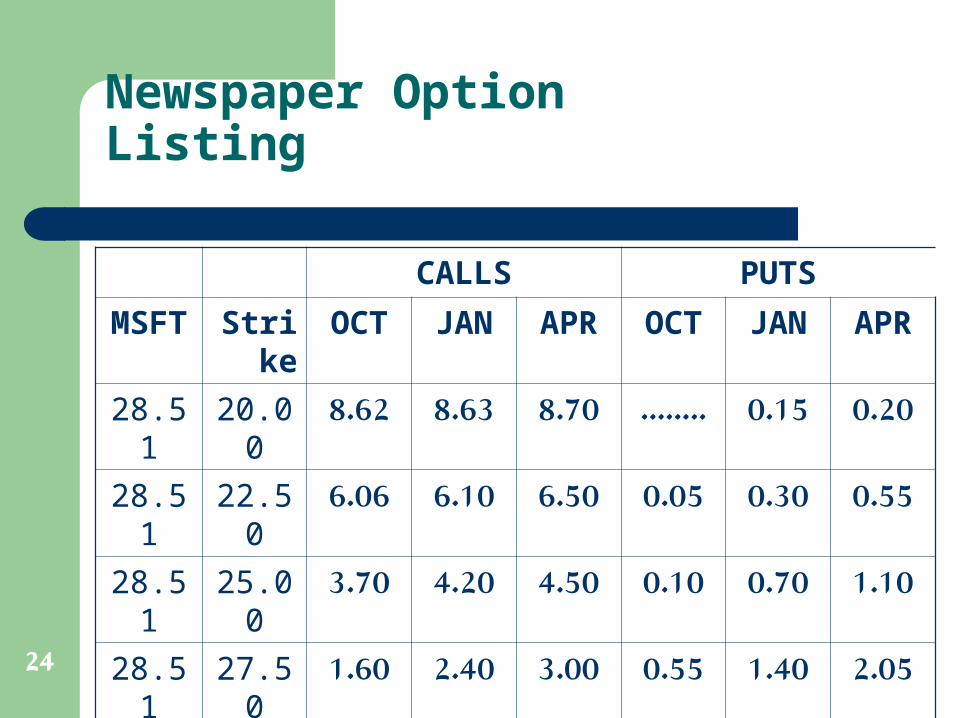

Newspaper Option Listing

CALLS PUTS

MSFT

Strike

OCT JAN APR OCT JAN APR

28.51

20.00

8.62 8.63 8.70 ........ 0.15 0.20

28.51

22.50

6.06 6.10 6.50 0.05 0.30 0.55

28.51

25.00

3.70 4.20 4.50 0.10 0.70 1.10

28.51

27.50

1.60 2.40 3.00 0.55 1.40 2.05

28.51

30.00

0.45 1.20 1.85 2.00 2.75 3.30

28.51

32.50

0.10 0.50 1.00 4.20 4.60 5.00

25

Vertical Spreads

In a vertical spread, options are selected vertically from the financial pages

– The options have the same expiration date, but different striking prices.

– The spreader will long one option and short the other

Vertical spreads with calls– Bullspread– Bearspread

26

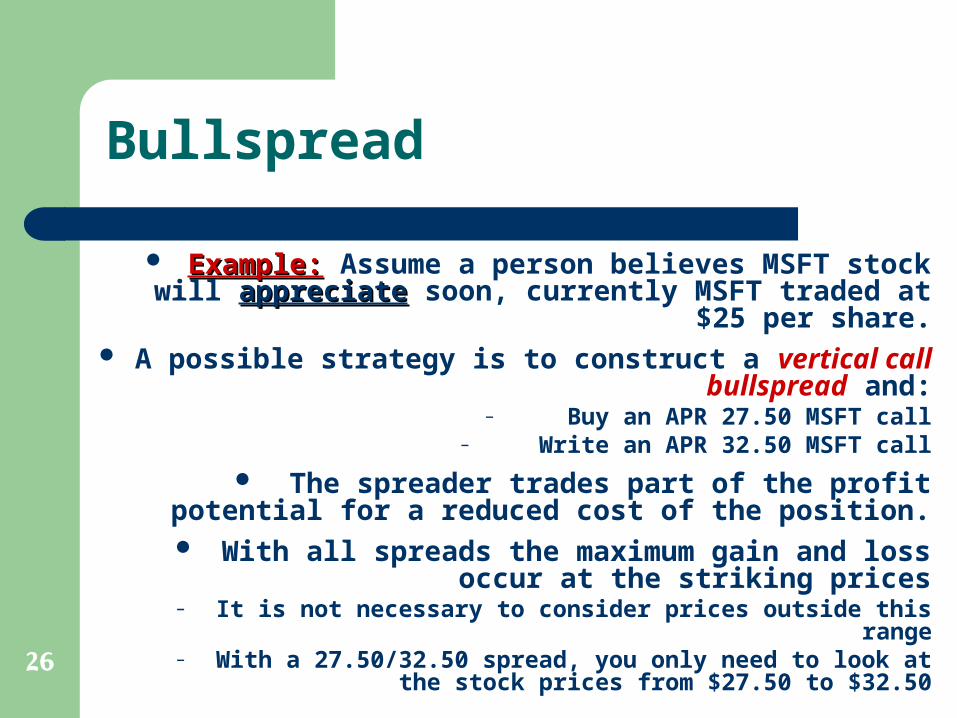

Bullspread

Example:Example: Assume a person believes MSFT stock will appreciateappreciate soon, currently MSFT traded at

$25 per share. A possible strategy is to construct a vertical call

bullspread and:– Buy an APR 27.50 MSFT call

– Write an APR 32.50 MSFT call The spreader trades part of the profit potential

for a reduced cost of the position. With all spreads the maximum gain and loss

occur at the striking prices– It is not necessary to consider prices outside this range– With a 27.50/32.50 spread, you only need to look at the

stock prices from $27.50 to $32.50

27

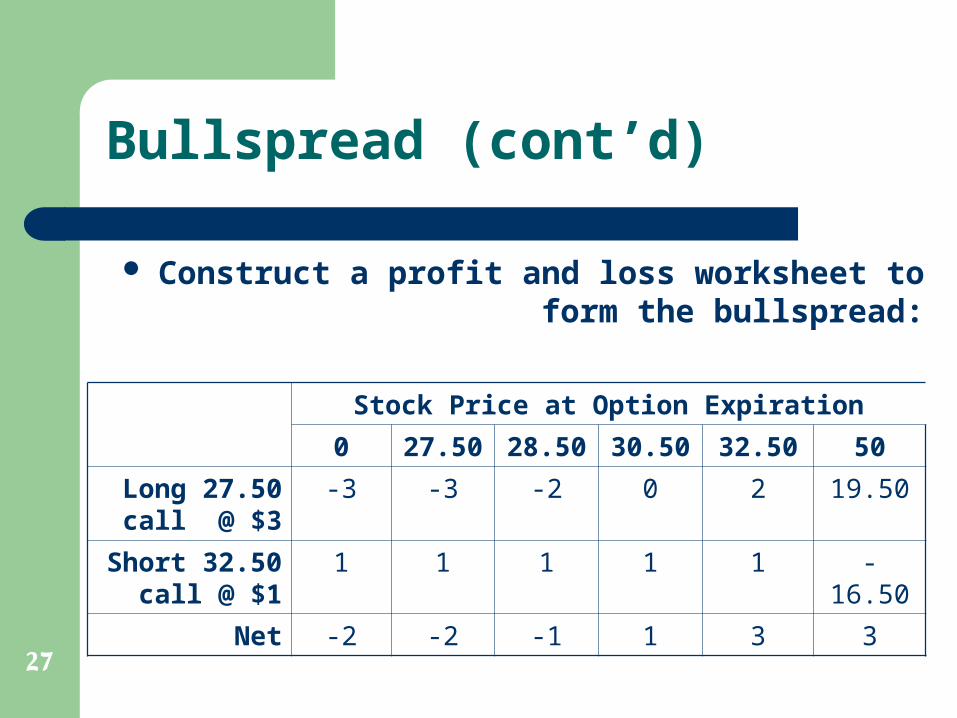

Bullspread (cont’d)

Construct a profit and loss worksheet to form the bullspread:

Stock Price at Option Expiration

0 27.50 28.50 30.50 32.50 50

Long 27.50 call @ $3

-3 -3 -2 0 2 19.50

Short 32.50 call @ $1

1 1 1 1 1 -16.50

Net -2 -2 -1 1 3 3

28

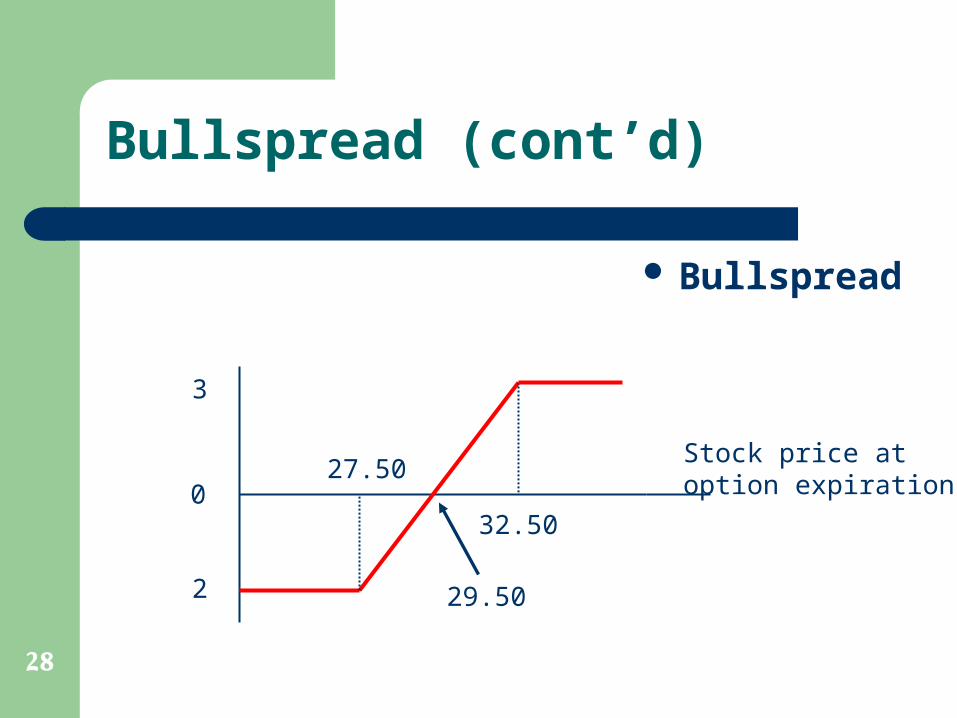

Bullspread (cont’d)

Bullspread

Stock price at option expiration0

2

3

32.50

29.50

27.50

29

Bearspread

A bearspread is the reverse of a bullspread

– The maximum profit occurs with falling prices

– The investor buys the option with the lower striking price and writes the

option with the higher striking price

30

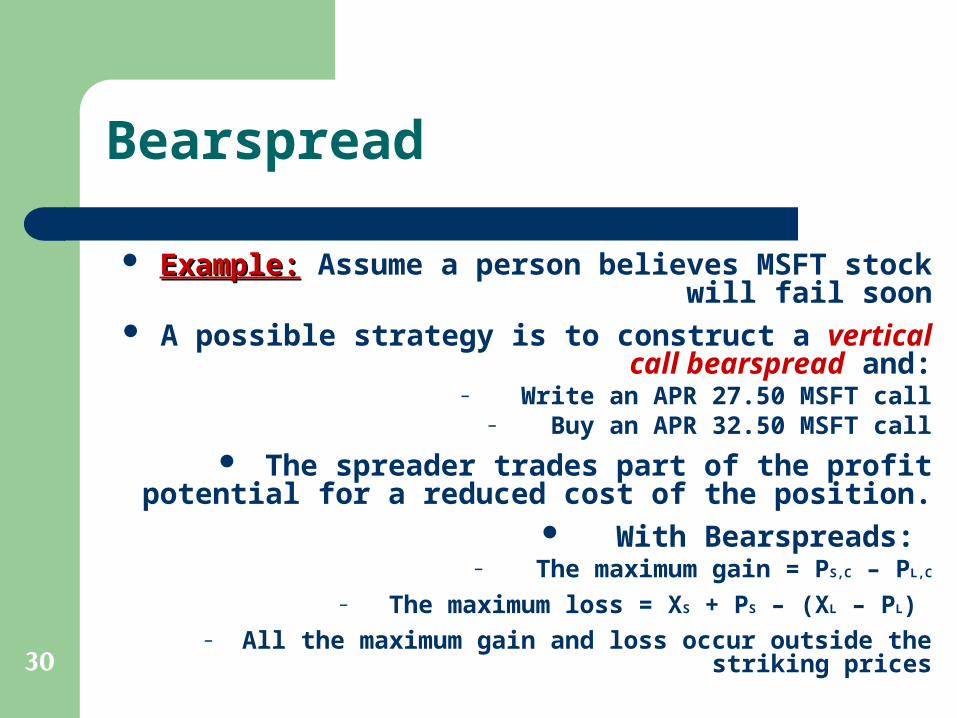

Bearspread

Example:Example: Assume a person believes MSFT stock will fail soon

A possible strategy is to construct a vertical call bearspread and:

– Write an APR 27.50 MSFT call– Buy an APR 32.50 MSFT call

The spreader trades part of the profit potential for a reduced cost of the position.

With Bearspreads: – The maximum gain = PS,C – PL,C

– The maximum loss = XS + PS – (XL – PL) – All the maximum gain and loss occur outside the

striking prices

31

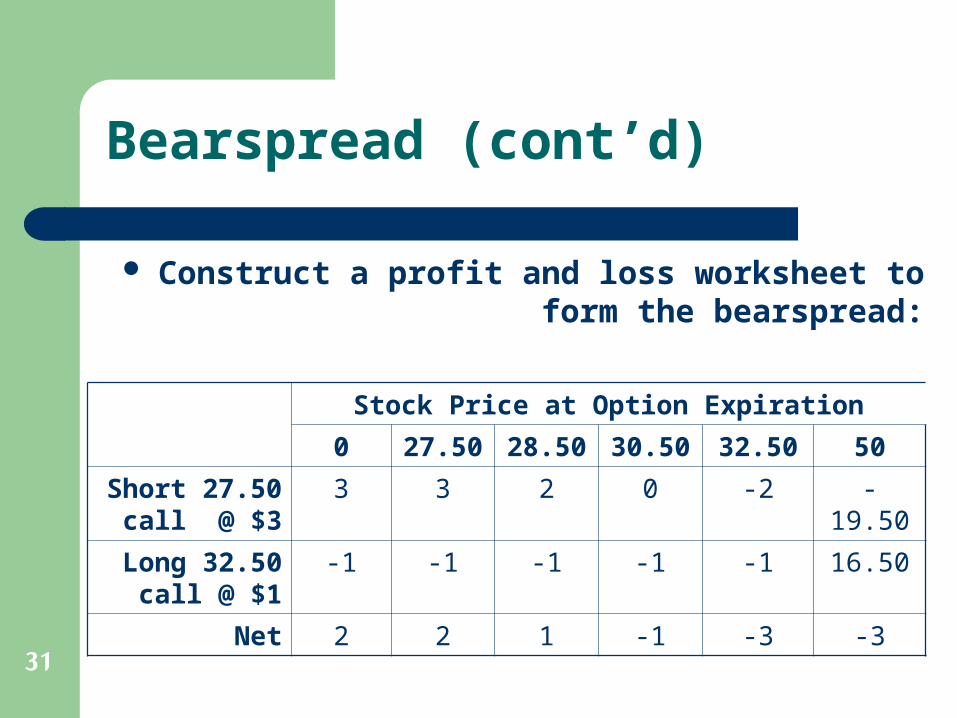

Bearspread (cont’d)

Construct a profit and loss worksheet to form the bearspread:

Stock Price at Option Expiration

0 27.50 28.50 30.50 32.50 50

Short 27.50 call @ $3

3 3 2 0 -2 -19.50

Long 32.50 call @ $1

-1 -1 -1 -1 -1 16.50

Net 2 2 1 -1 -3 -3

32

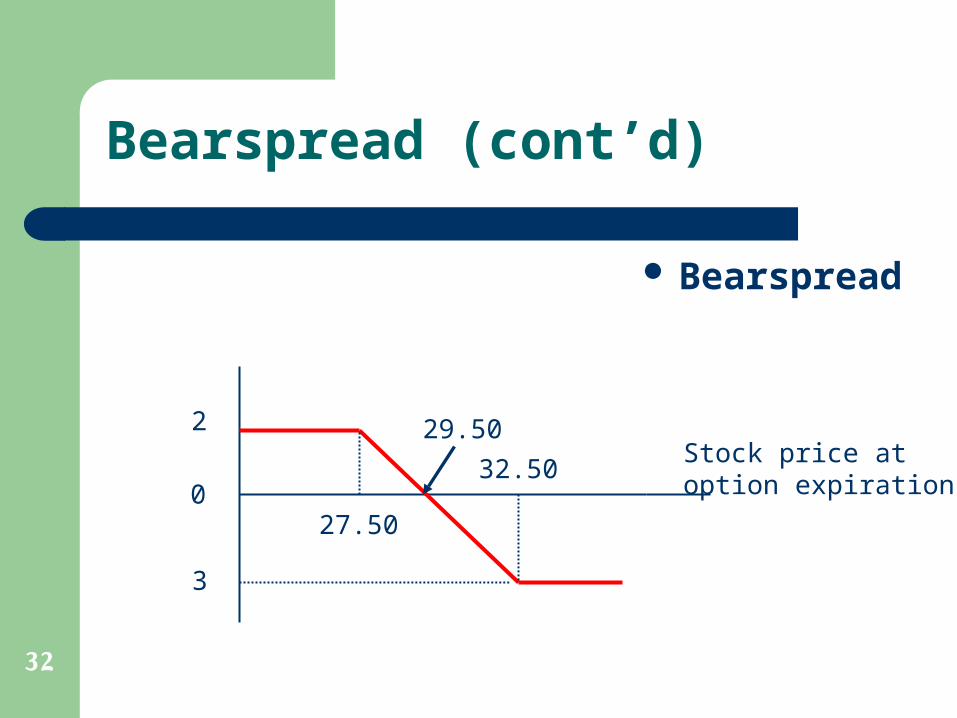

Bearspread (cont’d)

Bearspread

Stock price at option expiration0

2

3

32.50

29.50

27.50

33

Vertical Spreads With Puts: Bullspread

Involves using puts instead of calls

Buy the option with the lower striking price and write the option with the

higher one

The put spread results in a credit to the spreader’s account (credit spread)

The call spread results in a debit to the spreader’s account (debit spread)

34

Bullspread (cont’d)

A general characteristic of the call and put bullspreads is that the profit and loss payoffs for the two spreads

are approximately the same– The maximum profit occurs at all stock

prices above the higher striking price– The maximum loss occurs at stock prices

below the lower striking price

35

Calendar Spreads

In a calendar spread, options are chosen horizontally from a given row

in the financial pages– They have the same striking price

– The spreader will long one option and short the other

36

Calendar Spreads (cont’d)

Calendar spreads are either bullspreads or bearspreads

– In a bullspread, the spreader will buy a call with a distant expiration and write a

call that is near expiration– In a bearspread, the spreader will buy a

call that is near expiration and write a call with a distant expiration

37

Calendar Spreads (cont’d)

Calendar spreaders are concerned with time decay

– Options are worth more the longer they have until expiration

38

Diagonal Spreads

A diagonal spread involves options from different expiration months and

with different striking prices– They are chosen diagonally from the

option listing in the financial pages

Diagonal spreads can be bullish or bearish

39

Butterfly Spreads

A butterfly spread can be constructed for very little cost

beyond commissions

A butterfly spread can be constructed using puts and calls

40

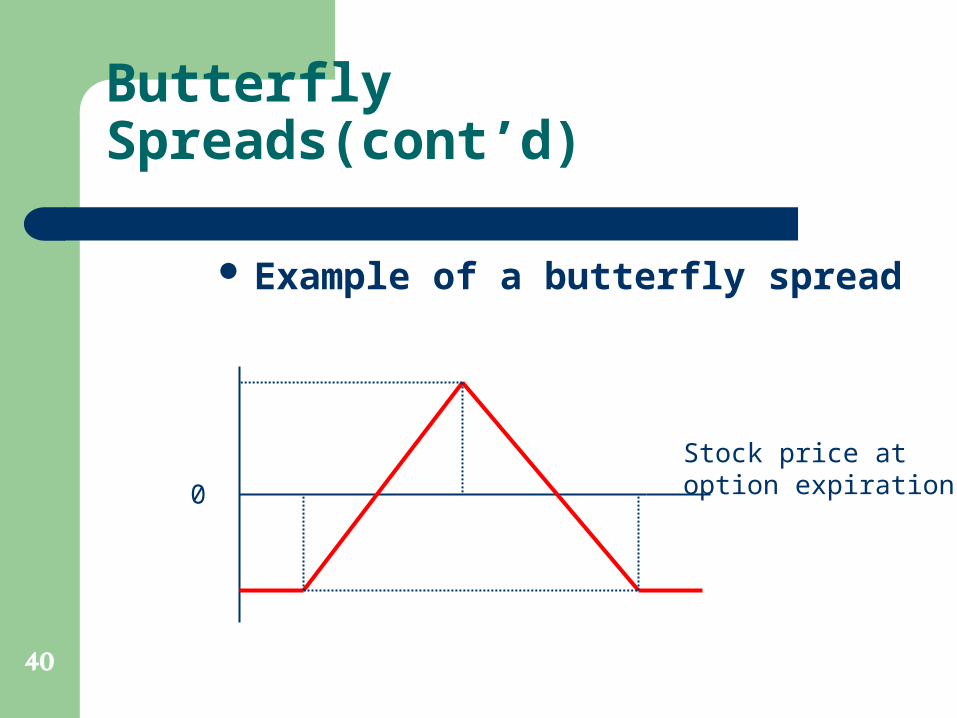

Butterfly Spreads(cont’d)

Example of a butterfly spread

Stock price at option expiration0

41

Nonstandard Spreads: Ratio Spreads

A ratio spread is a variation on bullspreads and bearspreads

– Instead of “long one, short one,” ratio spreads involve an unequal number of

long and short options– E.g., a call bullspread is a call ratio

spread if it involves writing more than one call at a higher striking price

42

Nonstandard Spreads:Ratio Backspreads

A ratio backspread is constructed the opposite of ratio spreads

– Call bearspreads are transformed into call ratio backspreads by adding to the

long call position– Put bullspreads are transformed into put

ratio backspreads by adding more long puts

43

Nonstandard Spreads: Hedge Wrapper

A hedge wrapper involves writing a covered call and buying a put

– Useful if a stock you own has appreciated and is expected to appreciate further with a temporary

decline– An alternative to selling the stock or creating a

protective put The maximum profit occurs once the stock

price rises to the striking price of the call The lowest return occurs if the stock falls to

the striking price of the put or below

44

Hedge Wrapper (cont’d)

The profitable stock position is transformed into a certain winner

The potential for further gain is reduced

45

Combined Call Writing

In combined call writing, the investor writes calls using more than

one striking price An alternative to other covered call

strategies The combined write is a compromise

between income and potential for further price appreciation

46

Margin Considerations

Introduction Margin requirements on long puts or

calls Margin requirements on short puts

or calls Margin requirements on spreads Margin requirements on covered

calls

47

Margin Considerations: Introduction

Necessity to post margin is an important consideration in spreading

– The speculator in short options must have sufficient equity in his or her

brokerage account before the option positions can be assumed

48

Margin Requirements on Long Puts or Calls

There is no requirement to advance any sum of money - other than the

option premium and the commission required - to long calls or puts

Can borrow up to 25% of the cost of the option position from a brokerage

firm if the option has at least nine months until expiration

49

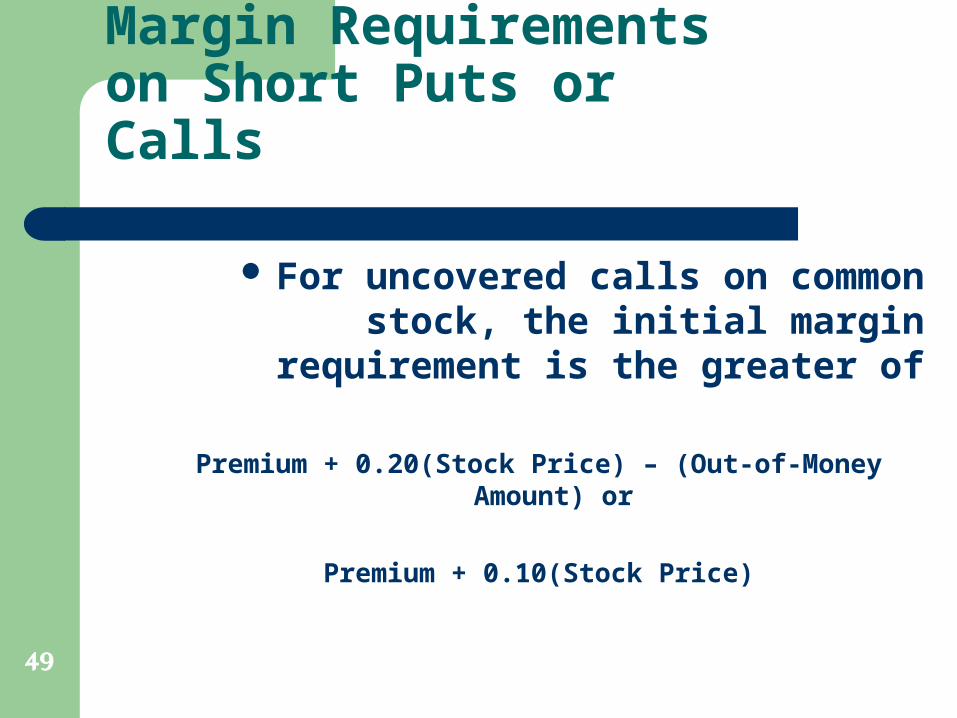

Margin Requirements on Short Puts or Calls

For uncovered calls on common stock, the initial margin requirement

is the greater of

Premium + 0.20(Stock Price) – (Out-of-Money Amount) or

Premium + 0.10(Stock Price)

50

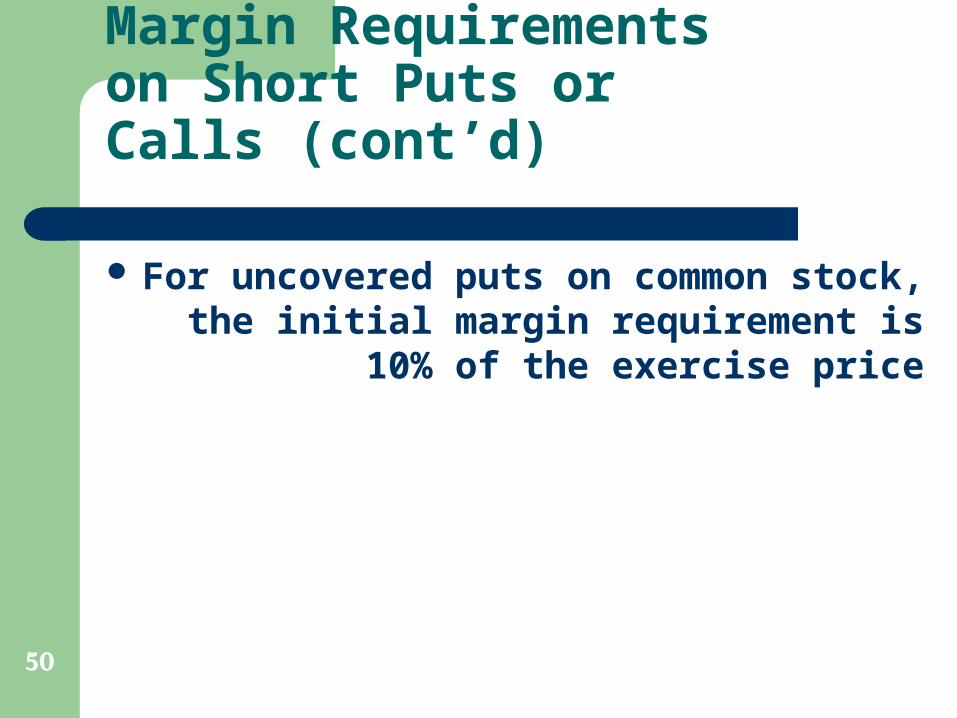

Margin Requirements on Short Puts or Calls (cont’d)

For uncovered puts on common stock, the initial margin requirement

is 10% of the exercise price

51

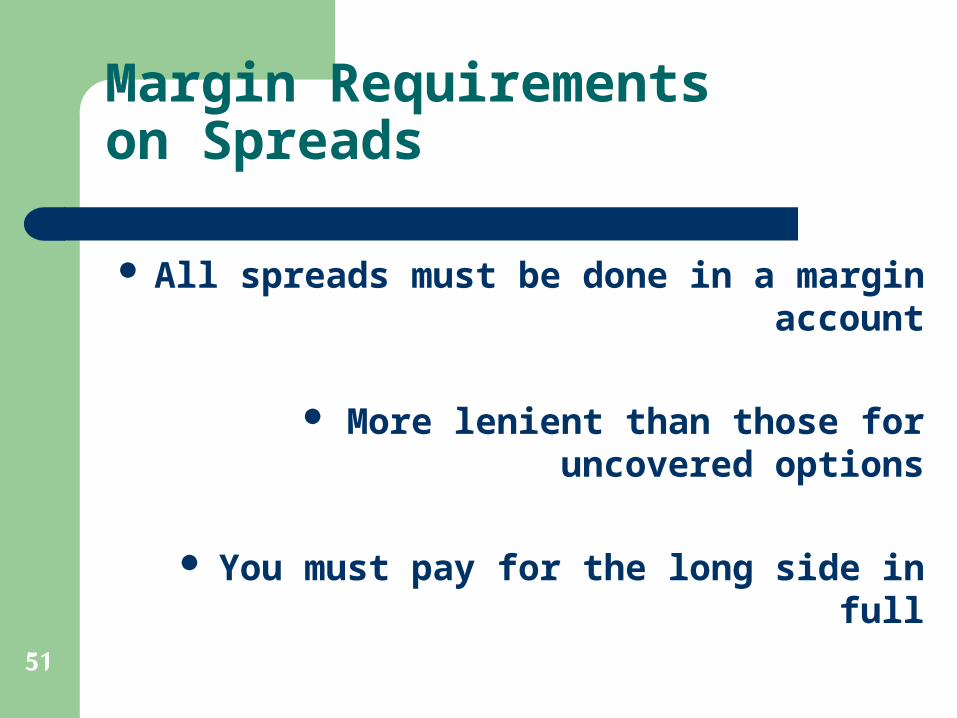

Margin Requirements on Spreads

All spreads must be done in a margin account

More lenient than those for uncovered options

You must pay for the long side in full

52

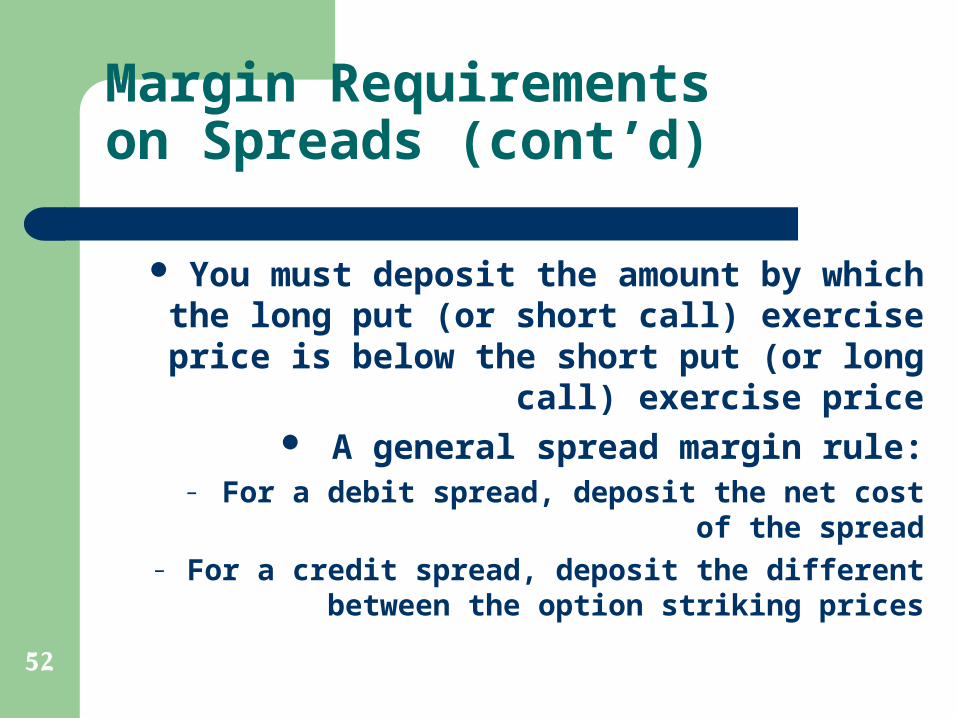

Margin Requirements on Spreads (cont’d)

You must deposit the amount by which the long put (or short call)

exercise price is below the short put (or long call) exercise price

A general spread margin rule:– For a debit spread, deposit the net cost of

the spread– For a credit spread, deposit the different

between the option striking prices

53

Margin Requirements on Covered Calls

There is no margin requirement when writing covered calls

Brokerage firms may restrict clients’ ability to sell shares of the

underlying stock

54

Evaluating Spreads: Introduction

Spreads and combinations are– Bullish,

– Bearish, or– Neutral

You must decide on your outlook for the market before deciding on a

strategy

55

Evaluating Spreads: The Debit/Credit Issue

An outlay requires a debit An inflow generates a credit

There are several strategies that may serve a particular end, and some will

involve a debt and others a credit

56

Evaluating Spreads: The Reward/Risk Ratio

Examine the maximum gain relative to the maximum loss

E.g., if a call bullspread has a maximum gain of $300.00 and a

maximum loss of $200.00, the reward/risk ratio is 1.50

57

Evaluating Spreads: The “Movement to Loss” Issue

The magnitude of stock price movement necessary for a position to

become unprofitable can be used to evaluate spreads

58

Evaluating Spreads: Specify A Limit Price

In spreads:– You want to obtain a high price for the

options you sell– You want to pay a low price for the

options you buy

Specify a dollar amount for the debit or credit at which you are willing to

trade

59

Determining the Appropriate Strategy: Some Final Thoughts

The basic steps involved in any decision making process:

– Learn the fundamentals– Gather information

– Evaluate alternatives– Make a decision